Financial Analysis of Comvita Limited: A PESTLE Perspective

VerifiedAdded on 2023/03/20

|9

|1524

|80

Report

AI Summary

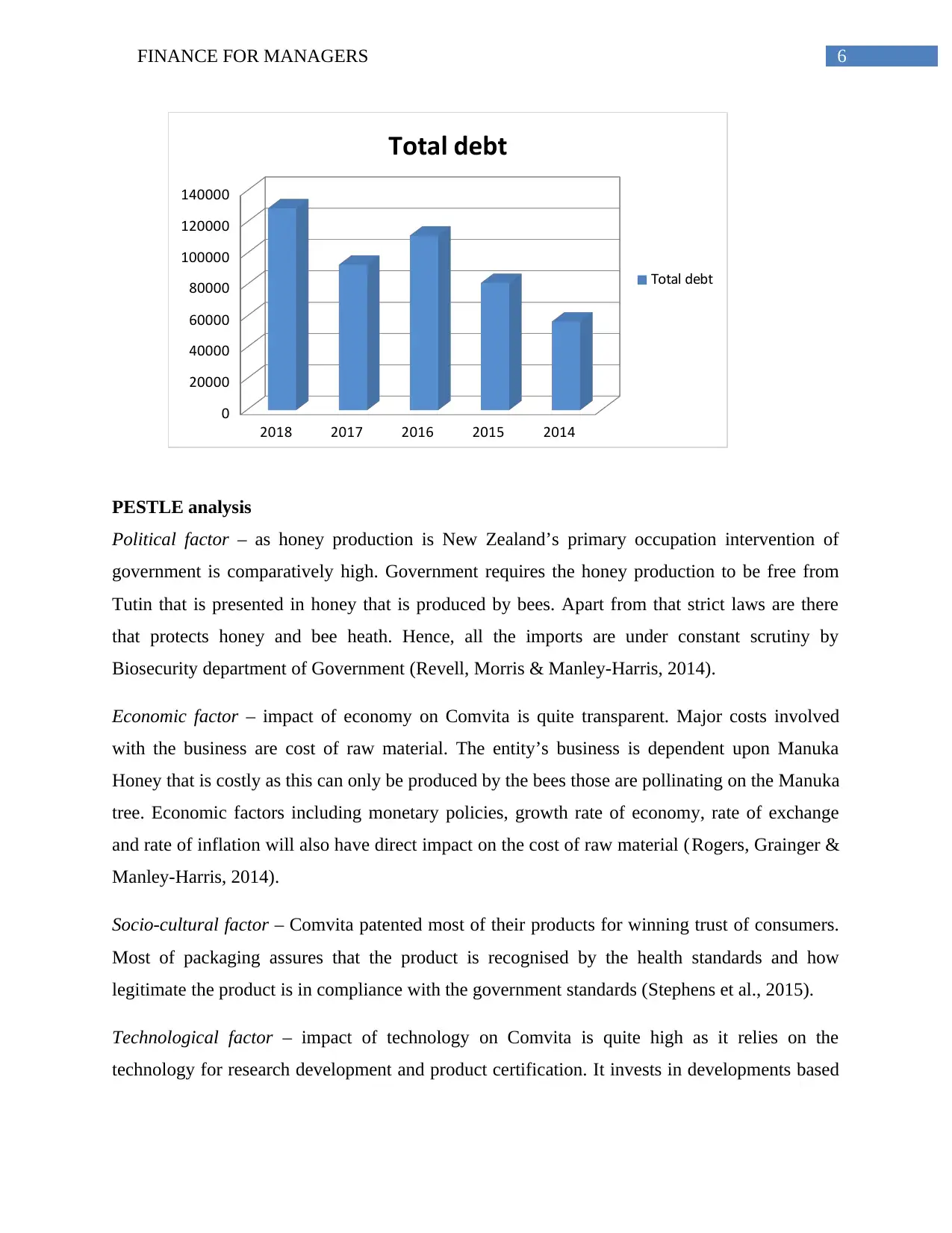

This report presents a comprehensive financial analysis of Comvita Limited, focusing on its performance metrics and the impact of external factors. The analysis begins with an executive summary that outlines the report's objectives, which include assessing the trends in Comvita's revenue, profit after tax, shareholder's equity, debtors, assets, and total debt over a five-year period. The report then delves into a detailed discussion of these financial trends, providing data-driven insights into the company's performance. Furthermore, a PESTLE analysis is conducted to examine the political, economic, socio-cultural, technological, environmental, and legal factors influencing Comvita's operations. This includes examining the impact of government regulations, economic conditions, consumer preferences, technological advancements, environmental sustainability, and legal frameworks. The report concludes by summarizing the key findings and highlighting the overall financial health and challenges faced by Comvita Limited. The analysis uses data from the company's annual reports and relevant academic sources to support its conclusions, providing a well-rounded assessment of Comvita's financial position and external influences.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.