Tesco Financial Analysis: Finance for Managers Assignment

VerifiedAdded on 2023/01/09

Paraphrase This Document

INTRODUCTION......................................................................................................................3

Task 1.........................................................................................................................................3

1.1 ..........................................................................................................................................3

1.2...........................................................................................................................................6

1.3...........................................................................................................................................8

1.4.........................................................................................................................................11

Task 2.......................................................................................................................................11

2.1.........................................................................................................................................11

2.2.........................................................................................................................................13

2.3.........................................................................................................................................13

Task 3.......................................................................................................................................14

3.1.........................................................................................................................................14

3.2.........................................................................................................................................14

3.3.........................................................................................................................................16

3.4 Analyse the viability of a proposal for expenditure.......................................................17

CONCLUSION........................................................................................................................17

REFERENCES.........................................................................................................................18

The finance is the field of study which talks about the role and importance of finance

in a business organization along with its relevance to the users of its. It provides assistance to

the management in determining the financial performance and position of the company which

is used as the base for taking various business decisions. This report provides an insight about

the financial aspects of the Tesco plc company. It covers the ratio and comparative analysis

budgeting and capital investment decisions.

Task 1

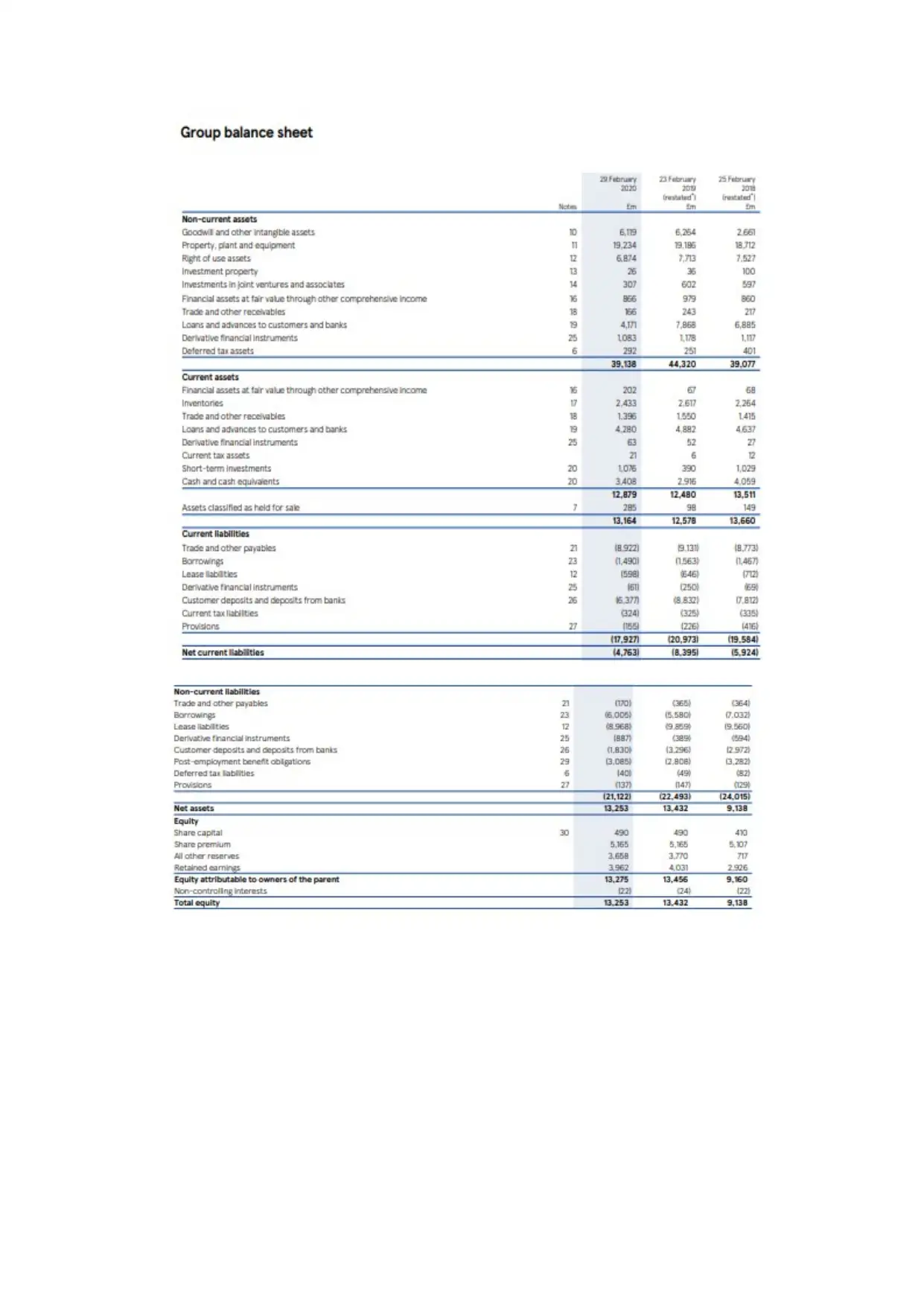

1.1

For evaluating the performance of the organization, it is very important to determine

the mission and vision of the organization which can be assessed looking at the auditors and

the director’s reports of the company (Lie and Sormin, 2016). The three important financial

statements of the company states about the flow of incomes and expenses of the company

whether it is flowing in the right direction or not. It is also used in gaining insight about the

assets and liabilities of the company. The information taken from the official website of the

company proves its validity and reliability. The three important statement are income

statement, balance sheet and the cashflow statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

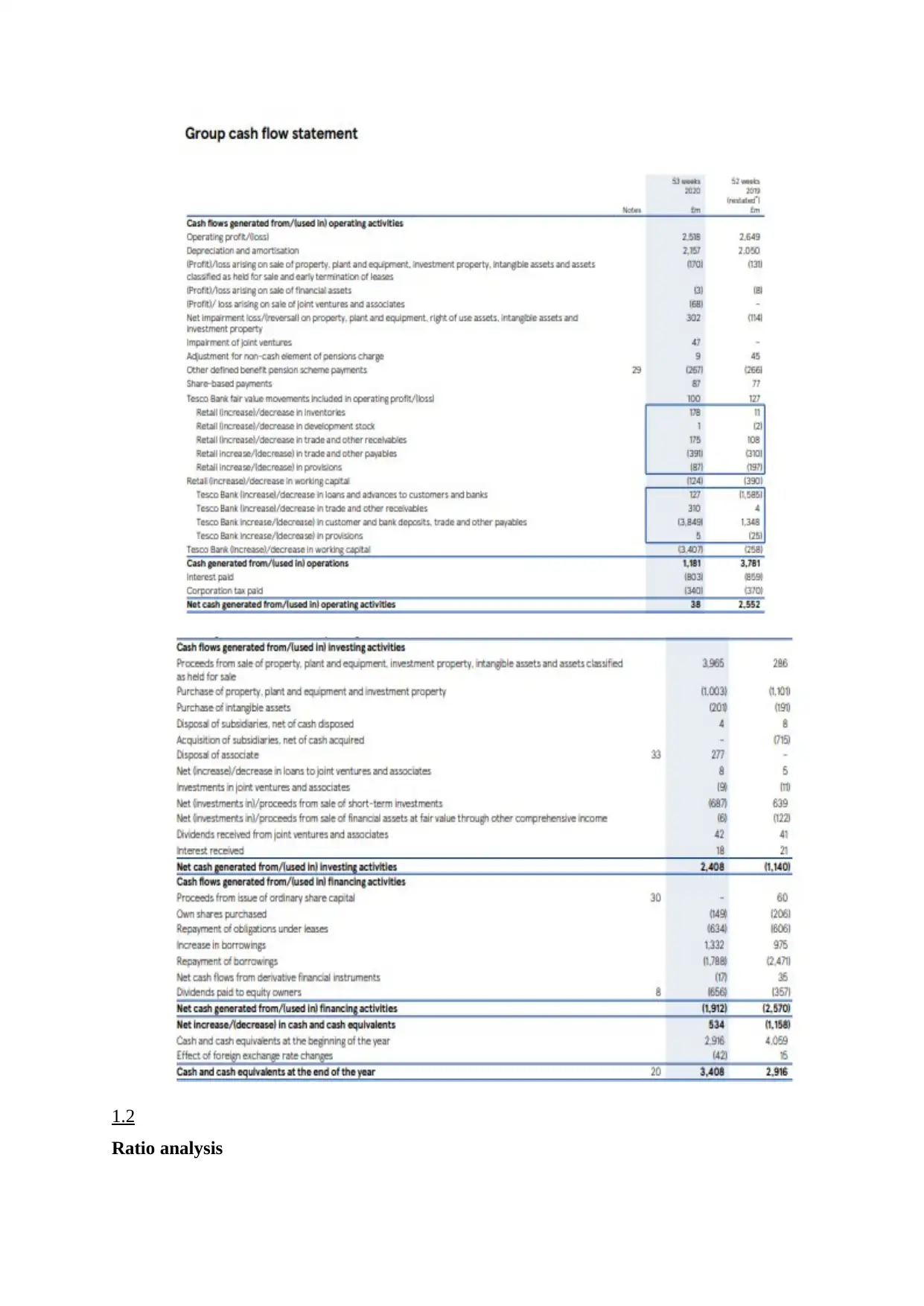

Ratio analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with the help of the income statement and balance sheet of the company. This these ratios

will help in determining the current level position of the company as compared to its past

performance which will help in taking valuable future business decisions.

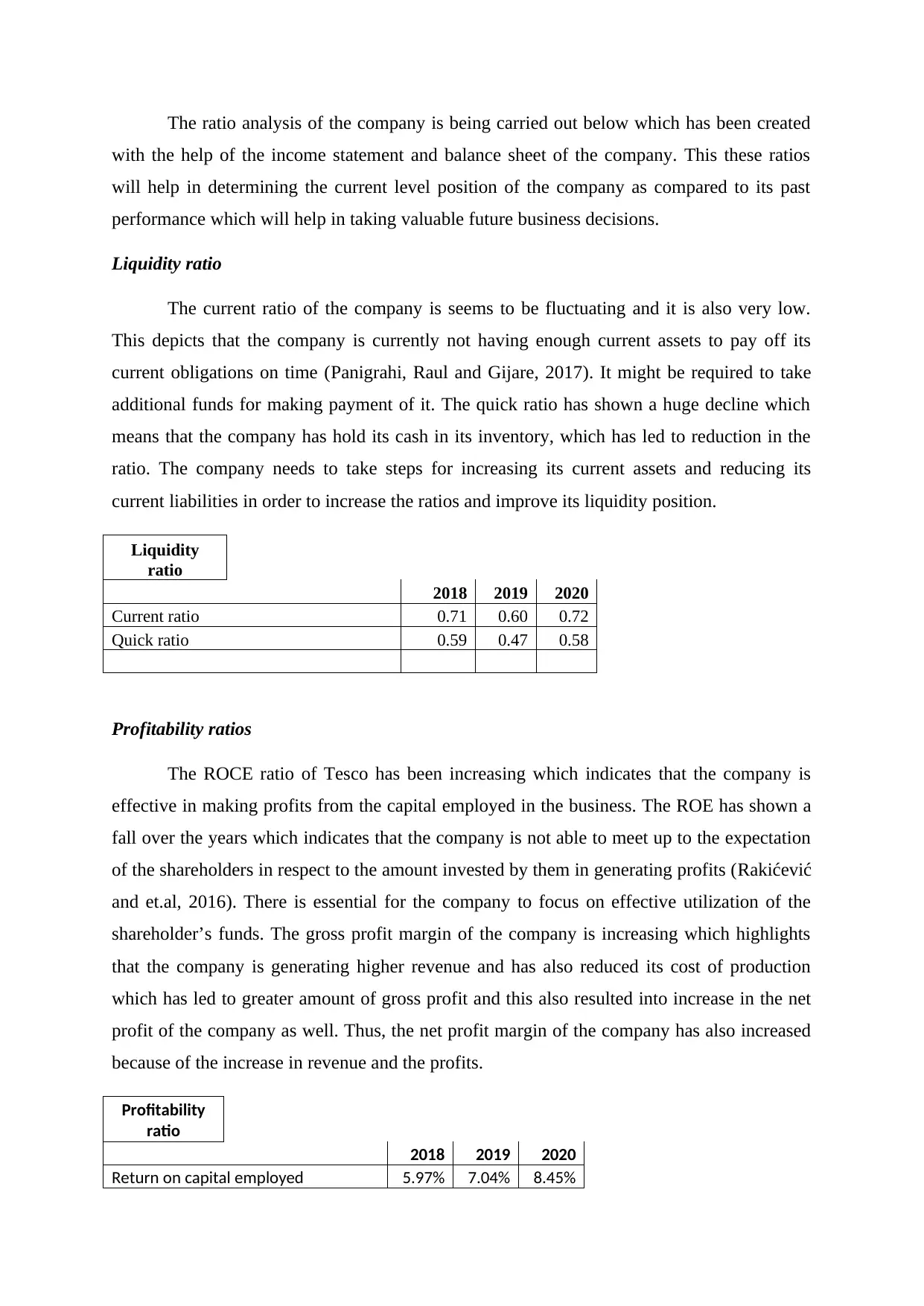

Liquidity ratio

The current ratio of the company is seems to be fluctuating and it is also very low.

This depicts that the company is currently not having enough current assets to pay off its

current obligations on time (Panigrahi, Raul and Gijare, 2017). It might be required to take

additional funds for making payment of it. The quick ratio has shown a huge decline which

means that the company has hold its cash in its inventory, which has led to reduction in the

ratio. The company needs to take steps for increasing its current assets and reducing its

current liabilities in order to increase the ratios and improve its liquidity position.

Liquidity

ratio

2018 2019 2020

Current ratio 0.71 0.60 0.72

Quick ratio 0.59 0.47 0.58

Profitability ratios

The ROCE ratio of Tesco has been increasing which indicates that the company is

effective in making profits from the capital employed in the business. The ROE has shown a

fall over the years which indicates that the company is not able to meet up to the expectation

of the shareholders in respect to the amount invested by them in generating profits (Rakićević

and et.al, 2016). There is essential for the company to focus on effective utilization of the

shareholder’s funds. The gross profit margin of the company is increasing which highlights

that the company is generating higher revenue and has also reduced its cost of production

which has led to greater amount of gross profit and this also resulted into increase in the net

profit of the company as well. Thus, the net profit margin of the company has also increased

because of the increase in revenue and the profits.

Profitability

ratio

2018 2019 2020

Return on capital employed 5.97% 7.04% 8.45%

Paraphrase This Document

Gross profit margin 5.92% 7.05% 7.43%

Net profit ratio 2.66% 3.96% 4.5%

Efficiency ratio:

The asset turnover ratio of Tesco has been fluctuating and in 2020 it has increased

from 2019 which means that the company is able to effectively utilize its assets in generating

higher revenue. Also, the inventory turnover ratio has increased over the period which depicts

that the company is able to sell out its stock in very quickly (Sunjoko, and ARILYN, 2016).

The a/c receivable turnover ratio has been rising but the too it is very low which means that

the organization is working on improving its credit policy and is having better collection

teams for collecting the due amount on time. On an overall basis the efficiency level of the

company is good.

Efficiency

ratio

2018 2019 2020

Asset turnover ratio 1.28 1.12 1.24

Inventory turnover ratio 23.89

22.7

0

24.6

4

Account receivable turnover ratio 9.34 9.93

11.3

7

Stability ratio:

The Debt to equity ratio of the company has declined over the past 3 years which

means that the Tesco has started paying off its debt or has increased its equity base. This

indicates that the composition of debt in the capital structure of the company is reducing

which leads to reduction in financial burden.

Stability ratio

2018 2019 2020

Debt equity ratio 3.28 3.23 2.94

1.3

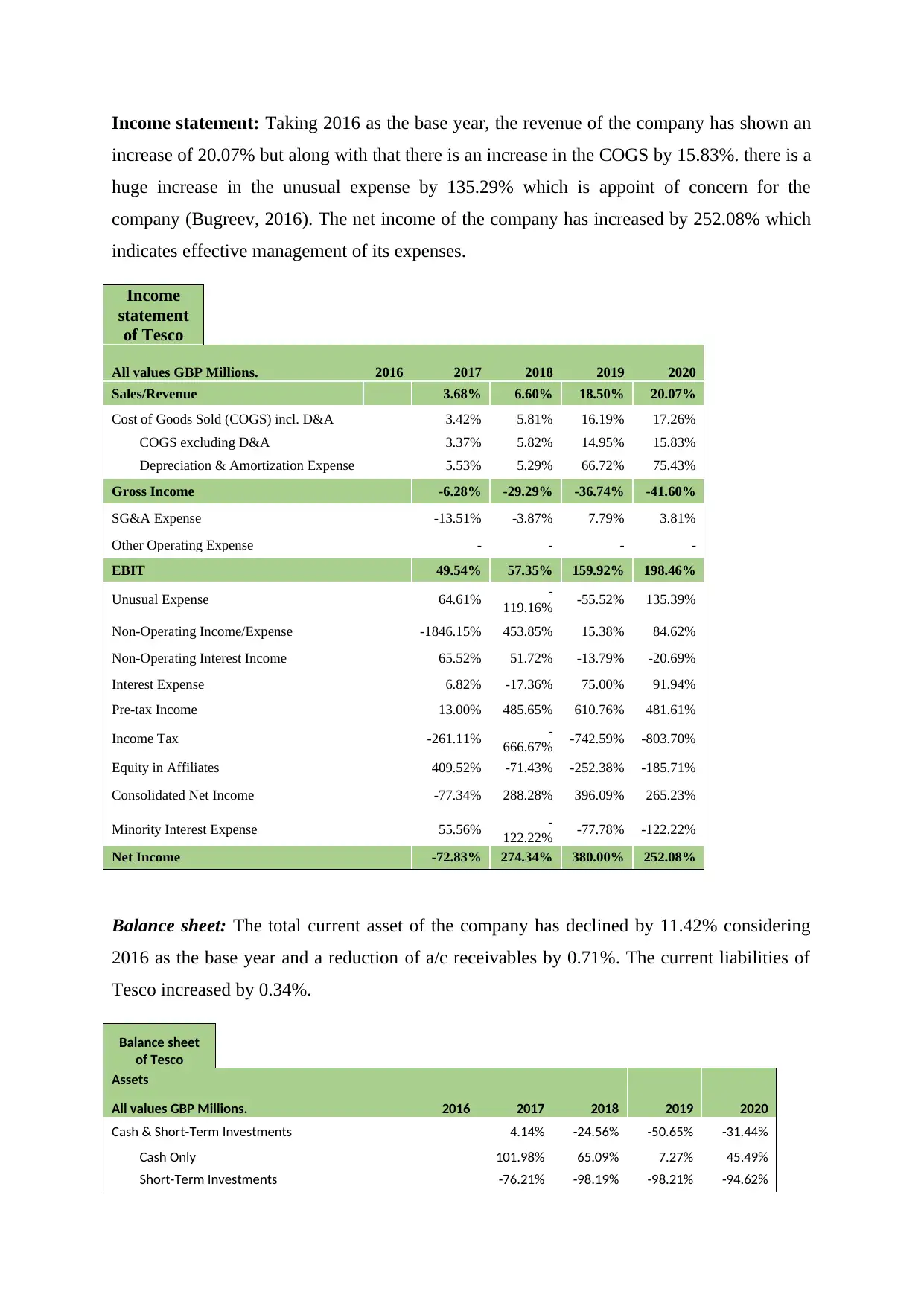

Comparative analysis

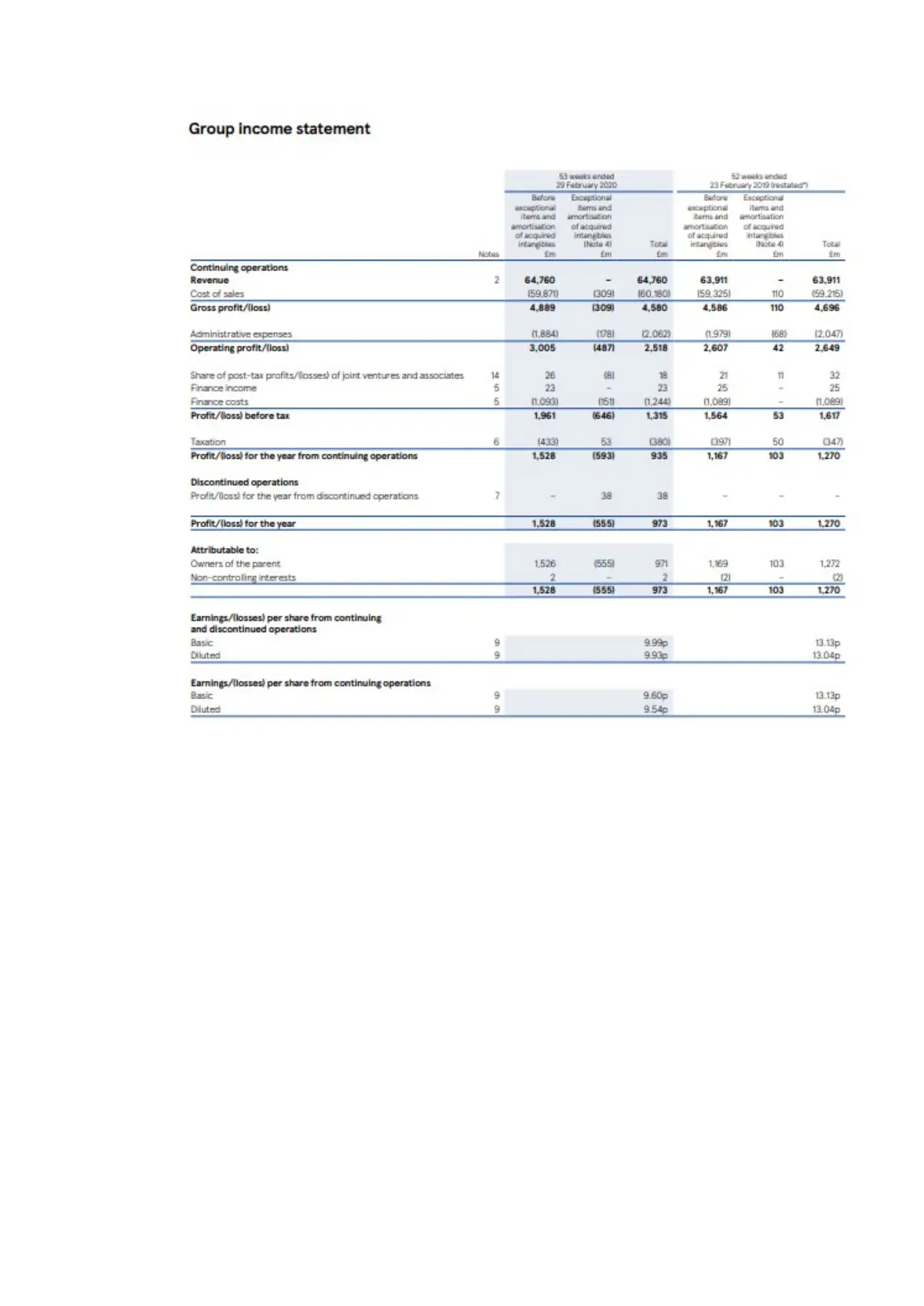

increase of 20.07% but along with that there is an increase in the COGS by 15.83%. there is a

huge increase in the unusual expense by 135.29% which is appoint of concern for the

company (Bugreev, 2016). The net income of the company has increased by 252.08% which

indicates effective management of its expenses.

Income

statement

of Tesco

All values GBP Millions. 2016 2017 2018 2019 2020

Sales/Revenue 3.68% 6.60% 18.50% 20.07%

Cost of Goods Sold (COGS) incl. D&A 3.42% 5.81% 16.19% 17.26%

COGS excluding D&A 3.37% 5.82% 14.95% 15.83%

Depreciation & Amortization Expense 5.53% 5.29% 66.72% 75.43%

Gross Income -6.28% -29.29% -36.74% -41.60%

SG&A Expense -13.51% -3.87% 7.79% 3.81%

Other Operating Expense - - - -

EBIT 49.54% 57.35% 159.92% 198.46%

Unusual Expense 64.61% -

119.16% -55.52% 135.39%

Non-Operating Income/Expense -1846.15% 453.85% 15.38% 84.62%

Non-Operating Interest Income 65.52% 51.72% -13.79% -20.69%

Interest Expense 6.82% -17.36% 75.00% 91.94%

Pre-tax Income 13.00% 485.65% 610.76% 481.61%

Income Tax -261.11% -

666.67% -742.59% -803.70%

Equity in Affiliates 409.52% -71.43% -252.38% -185.71%

Consolidated Net Income -77.34% 288.28% 396.09% 265.23%

Minority Interest Expense 55.56% -

122.22% -77.78% -122.22%

Net Income -72.83% 274.34% 380.00% 252.08%

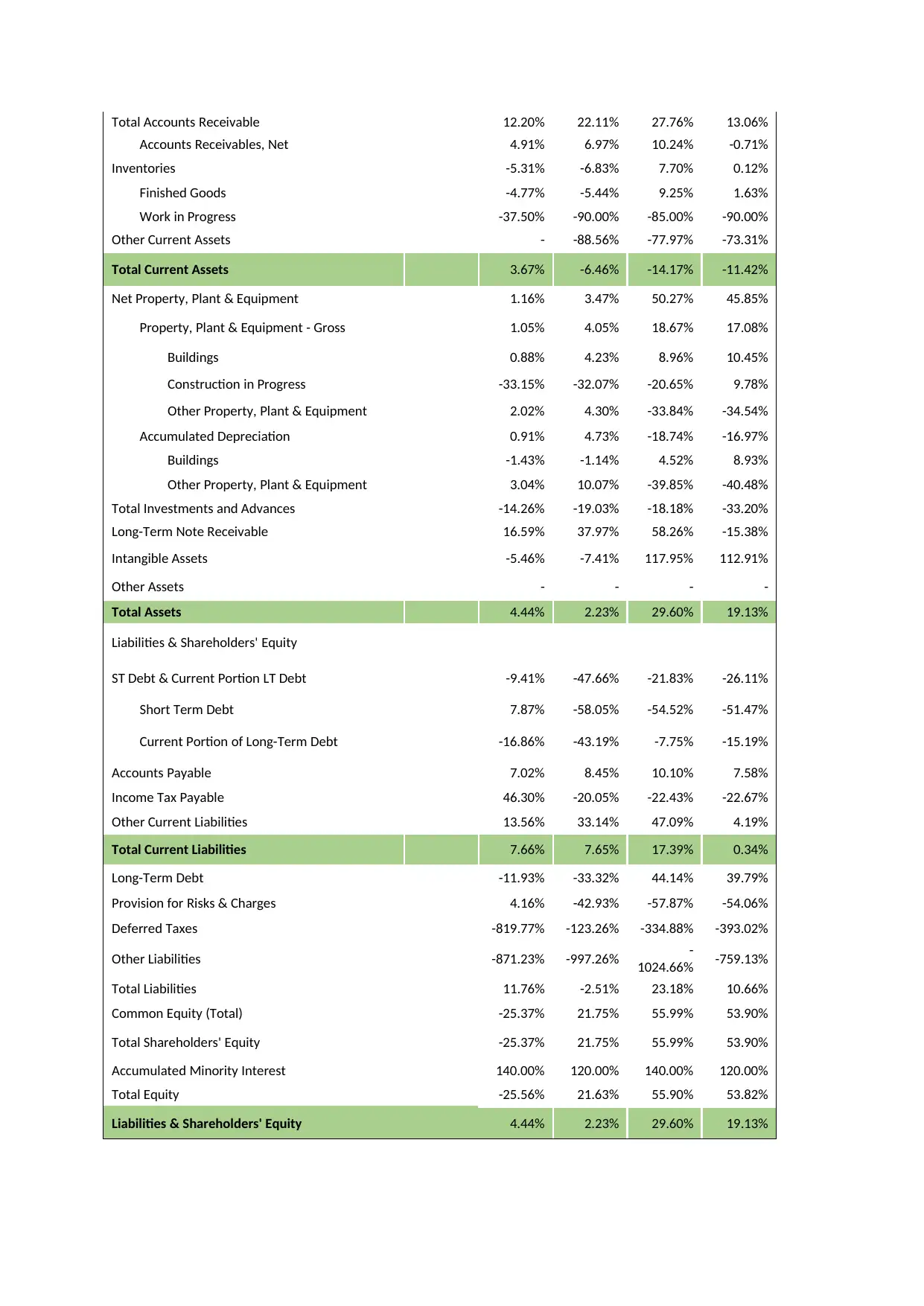

Balance sheet: The total current asset of the company has declined by 11.42% considering

2016 as the base year and a reduction of a/c receivables by 0.71%. The current liabilities of

Tesco increased by 0.34%.

Balance sheet

of Tesco

Assets

All values GBP Millions. 2016 2017 2018 2019 2020

Cash & Short-Term Investments 4.14% -24.56% -50.65% -31.44%

Cash Only 101.98% 65.09% 7.27% 45.49%

Short-Term Investments -76.21% -98.19% -98.21% -94.62%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts Receivables, Net 4.91% 6.97% 10.24% -0.71%

Inventories -5.31% -6.83% 7.70% 0.12%

Finished Goods -4.77% -5.44% 9.25% 1.63%

Work in Progress -37.50% -90.00% -85.00% -90.00%

Other Current Assets - -88.56% -77.97% -73.31%

Total Current Assets 3.67% -6.46% -14.17% -11.42%

Net Property, Plant & Equipment 1.16% 3.47% 50.27% 45.85%

Property, Plant & Equipment - Gross 1.05% 4.05% 18.67% 17.08%

Buildings 0.88% 4.23% 8.96% 10.45%

Construction in Progress -33.15% -32.07% -20.65% 9.78%

Other Property, Plant & Equipment 2.02% 4.30% -33.84% -34.54%

Accumulated Depreciation 0.91% 4.73% -18.74% -16.97%

Buildings -1.43% -1.14% 4.52% 8.93%

Other Property, Plant & Equipment 3.04% 10.07% -39.85% -40.48%

Total Investments and Advances -14.26% -19.03% -18.18% -33.20%

Long-Term Note Receivable 16.59% 37.97% 58.26% -15.38%

Intangible Assets -5.46% -7.41% 117.95% 112.91%

Other Assets - - - -

Total Assets 4.44% 2.23% 29.60% 19.13%

Liabilities & Shareholders' Equity

ST Debt & Current Portion LT Debt -9.41% -47.66% -21.83% -26.11%

Short Term Debt 7.87% -58.05% -54.52% -51.47%

Current Portion of Long-Term Debt -16.86% -43.19% -7.75% -15.19%

Accounts Payable 7.02% 8.45% 10.10% 7.58%

Income Tax Payable 46.30% -20.05% -22.43% -22.67%

Other Current Liabilities 13.56% 33.14% 47.09% 4.19%

Total Current Liabilities 7.66% 7.65% 17.39% 0.34%

Long-Term Debt -11.93% -33.32% 44.14% 39.79%

Provision for Risks & Charges 4.16% -42.93% -57.87% -54.06%

Deferred Taxes -819.77% -123.26% -334.88% -393.02%

Other Liabilities -871.23% -997.26% -

1024.66% -759.13%

Total Liabilities 11.76% -2.51% 23.18% 10.66%

Common Equity (Total) -25.37% 21.75% 55.99% 53.90%

Total Shareholders' Equity -25.37% 21.75% 55.99% 53.90%

Accumulated Minority Interest 140.00% 120.00% 140.00% 120.00%

Total Equity -25.56% 21.63% 55.90% 53.82%

Liabilities & Shareholders' Equity 4.44% 2.23% 29.60% 19.13%

Paraphrase This Document

Financial records of an organization should be checked and seen as being valid and

reasonable. To guarantee exactness and verity of money related records need to check

through different assessments and it is obliged by law to lead independent audit on the

financial operations so as to secure investor's faith. For the most part, internal and external

reviewers (auditors) are answerable for guaranteeing precision and verity of money related

records. There are chances that the information presented in the financial records are

manipulated which result into depicting the wrong financial position and performance of the

business. Therefore, external auditing should be carried out. Based on the data provided, it

can be seen that the revenue of the company increased at 20.07% in 2020 taking 2016 as the

base year while on the other hand the cost of sales increased by 17.26% which is also very

high therefore, the company is required to analyse the cost that resulted into the increase

mainly the variable cost. The current assets of the company showed a negative change which

creates a point of concern over which proper review and questioning should be done in order

to identify the reason for such change.

Task 2

2.1

Budgeting plan gives extensive money related outline of planned organization

activity. An organization's targets budgeting plan is the general money related arrangement

demonstrating use of the accessible assets. Tesco’s financial plan is driven by the aims and

targets of the company along with what it can really achieve (Wang and Yao, 2017).

Numerous factors in a business can be planned which incorporates sales, yield, cost -

(variable and fixed), benefits, income, capital venture. Financial plan ought to be SMART,

that is, specific, feasible (measurable), achievable and reasonable, and with time bound or

else the budgeting will be inadequate.

Vital goal of Tesco is the principal factor that is required to be viewed as when

figuring budgeting plans in light of the fact that unaligned financial plan with vital aims and

objectives lead to disappointment. The subsequent stage of planning is recognizing the

limiting variable that the association is confronted with which is known as constraints which

might be a cut-off on the quantity of products a business could sell (demand is constraining

element) or on the quantity of hours a specific kind of workforce could work and so forth.

When association recognizes the limiting element, they set the budgetary guideline (Vidal-

coordination of inner elements for example abilities of representatives and assets and draft

departmental financial plan. After this progression, the association ought to evaluate the

outside affecting component, for example, estimated economic, political and global condition

which assists with limiting the risk associated with the financial plan. At last, organization

need to arrange the whole departmental budgeting plan for example sales plan, production

financial plan, material and labour spending plan, overhead budget which is called as the

master budget.

The master budget plan is a synopsis of an organization's arrangements that sets

explicit goals for the sales, manufacturing, appropriation and financing exercises which for

the most part comes full circle in a cash budgeting plan, a planned income statement and a

planned balance sheet report.

The master budget begins with sales anticipating which should be possible by top to

bottom investigation of past sales pattern, estimation made by the relevant business or

workforces, general monetary condition, contender's activities, change in the association's

costs, change in item mic, statistical surveying, publicizing and sales advancement plans.

Sales evaluating prompts the sales spending plan that is a definite timetable indicating the

expected sales for the spending time frame. It very well may be communicated in units and

money both. The sales financial plan is the fundamental pillar of the master budget (Marzlin

Marzuki and Ismail, 2019). The following financial plan is production budget which decides

amount of manufacturing relies on the quantity of units to be sold and upon the quantity of

units in the closure and opening inventories. Another segment of spending plan is material

budget plan which shows the amount and cost of buying material for planned production and

inventories. The labour budget shows the financial plan for all sort of work for example

skilled and unskilled which rely on the level of production. Another spending plan is the

overhead spending that shows amounts of an enormous number of items of expenses for

example compensation, power, lease, administrative costs. After this association get ready

projected income statement, balance sheet and the cash budget.

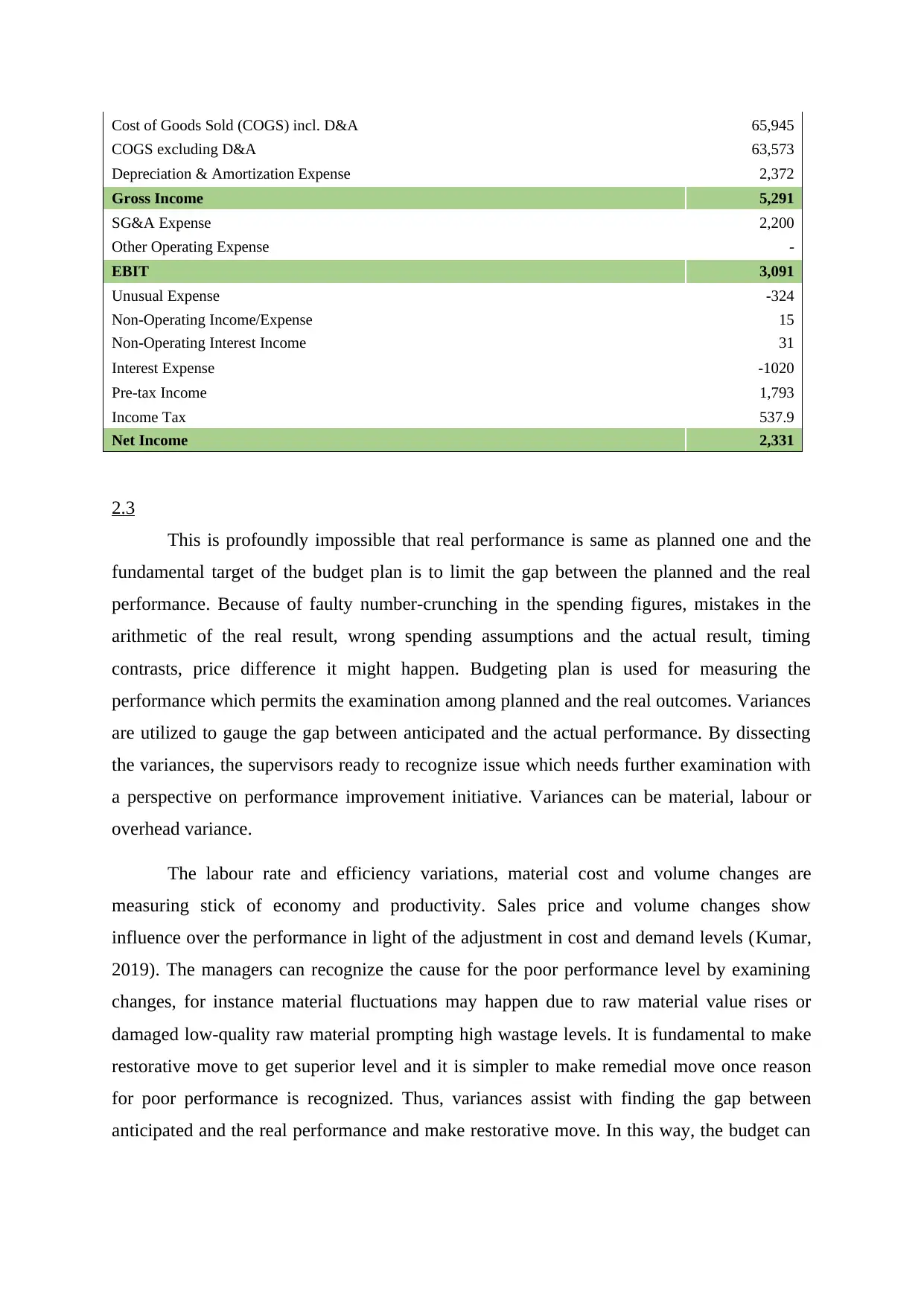

2.2

Budgeted Income statement of Tesco

All values GBP Millions. 2021

Sales/Revenue 71,236

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COGS excluding D&A 63,573

Depreciation & Amortization Expense 2,372

Gross Income 5,291

SG&A Expense 2,200

Other Operating Expense -

EBIT 3,091

Unusual Expense -324

Non-Operating Income/Expense 15

Non-Operating Interest Income 31

Interest Expense -1020

Pre-tax Income 1,793

Income Tax 537.9

Net Income 2,331

2.3

This is profoundly impossible that real performance is same as planned one and the

fundamental target of the budget plan is to limit the gap between the planned and the real

performance. Because of faulty number-crunching in the spending figures, mistakes in the

arithmetic of the real result, wrong spending assumptions and the actual result, timing

contrasts, price difference it might happen. Budgeting plan is used for measuring the

performance which permits the examination among planned and the real outcomes. Variances

are utilized to gauge the gap between anticipated and the actual performance. By dissecting

the variances, the supervisors ready to recognize issue which needs further examination with

a perspective on performance improvement initiative. Variances can be material, labour or

overhead variance.

The labour rate and efficiency variations, material cost and volume changes are

measuring stick of economy and productivity. Sales price and volume changes show

influence over the performance in light of the adjustment in cost and demand levels (Kumar,

2019). The managers can recognize the cause for the poor performance level by examining

changes, for instance material fluctuations may happen due to raw material value rises or

damaged low-quality raw material prompting high wastage levels. It is fundamental to make

restorative move to get superior level and it is simpler to make remedial move once reason

for poor performance is recognized. Thus, variances assist with finding the gap between

anticipated and the real performance and make restorative move. In this way, the budget can

Paraphrase This Document

financial constraints and accounting conventions.

Task 3

3.1

Business needs to evaluate its proposition to choose the best venture project that

produce yield effectiveness. A best proposition can be select as per the adequate degree of

risk (least risk), biggest degree of advantage (productivity), most minimal expense and best

money saving advantage proportion (Evaluation of Investment Proposals: 7 Methods. 2020).

In spite of the fact that, association can set the standards to choose the recommendation that

may incorporate money related viability of the proposal, influence on vital goal, hierarchical

risk, influence on the future budgetary proportions and KFI, strengths and shortcomings of

the undertaking.

The Tucker's five model is the compelling method to pass judgment on the

undertakings that permits administrator knowledge into the decision-making procedure. The

five inquiries are:

Is the proposition beneficial?

Does the proposition fulfil lawful prerequisite?

Is the proposition reasonable for all stakeholders?

Is the proposition ethical?

Is the proposition maintainable?

By utilizing these measures directors can choose the best proposition which prompts okay

and viable execution.

3.2

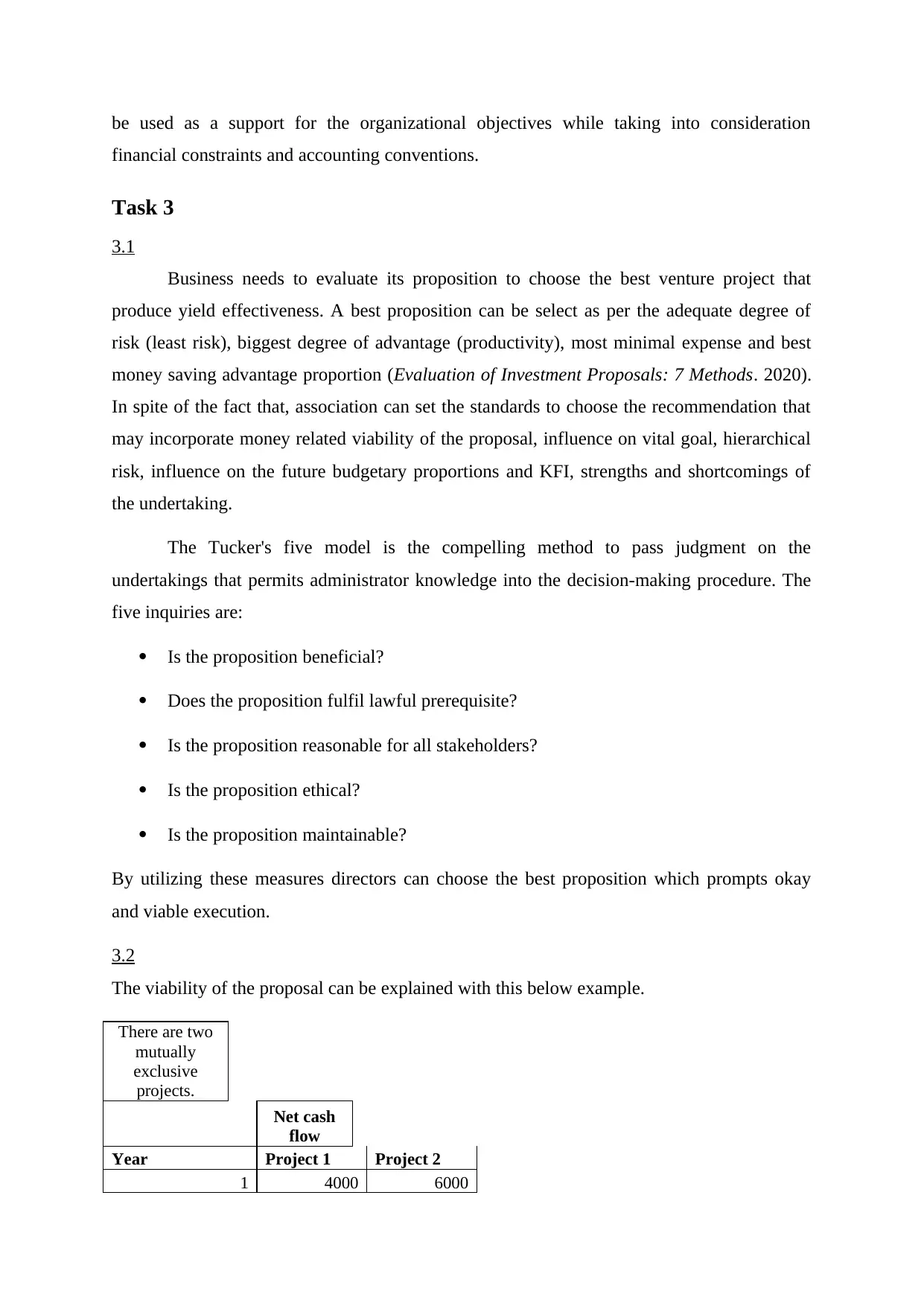

The viability of the proposal can be explained with this below example.

There are two

mutually

exclusive

projects.

Net cash

flow

Year Project 1 Project 2

1 4000 6000

3 4000 2000

4 4000 5000

5 4000 5000

Initial investment $10000 each

Life of the project 5 years

Tax rate 50%

Cost of capital 10%

Depreciation on

straight line method

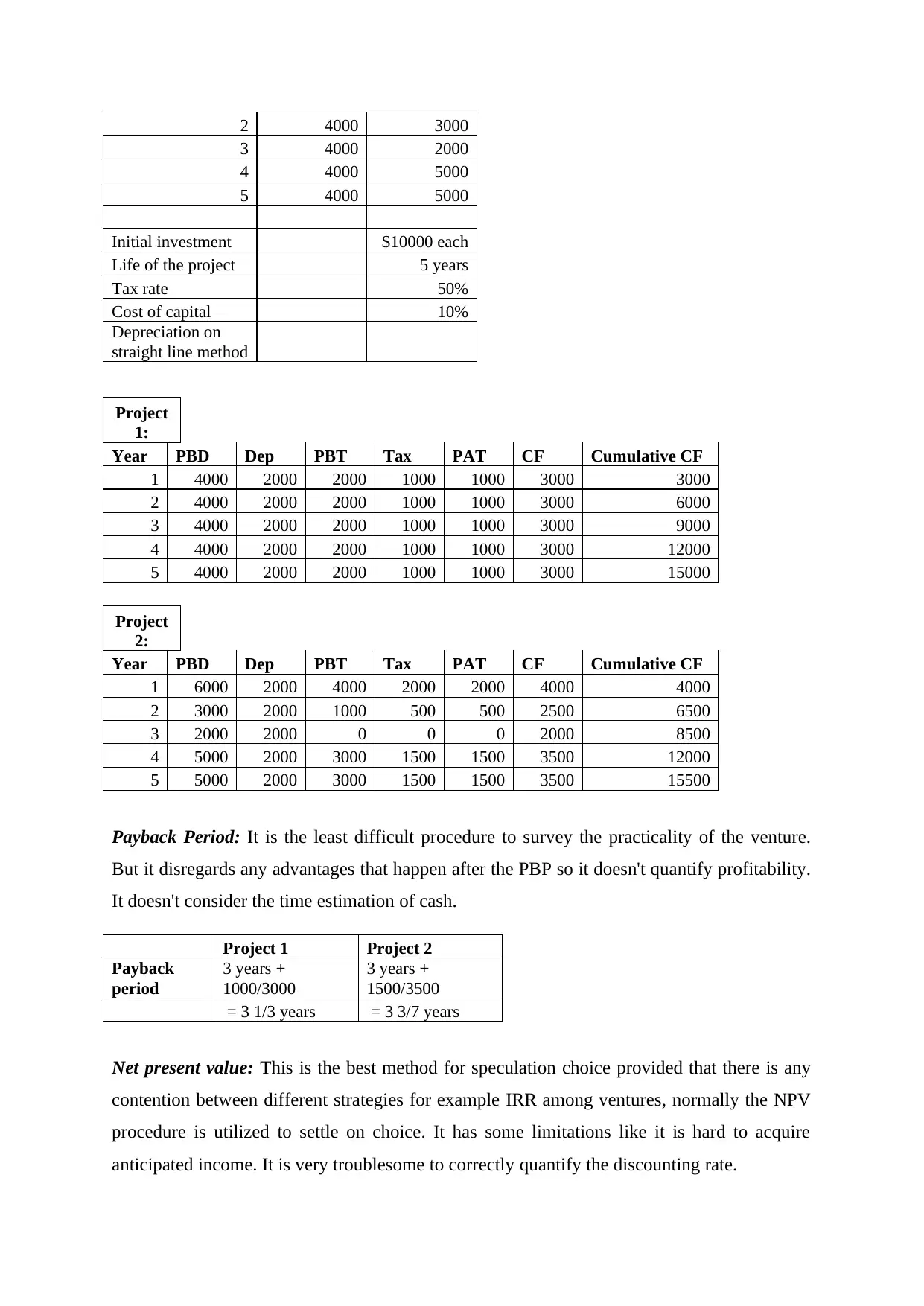

Project

1:

Year PBD Dep PBT Tax PAT CF Cumulative CF

1 4000 2000 2000 1000 1000 3000 3000

2 4000 2000 2000 1000 1000 3000 6000

3 4000 2000 2000 1000 1000 3000 9000

4 4000 2000 2000 1000 1000 3000 12000

5 4000 2000 2000 1000 1000 3000 15000

Project

2:

Year PBD Dep PBT Tax PAT CF Cumulative CF

1 6000 2000 4000 2000 2000 4000 4000

2 3000 2000 1000 500 500 2500 6500

3 2000 2000 0 0 0 2000 8500

4 5000 2000 3000 1500 1500 3500 12000

5 5000 2000 3000 1500 1500 3500 15500

Payback Period: It is the least difficult procedure to survey the practicality of the venture.

But it disregards any advantages that happen after the PBP so it doesn't quantify profitability.

It doesn't consider the time estimation of cash.

Project 1 Project 2

Payback

period

3 years +

1000/3000

3 years +

1500/3500

= 3 1/3 years = 3 3/7 years

Net present value: This is the best method for speculation choice provided that there is any

contention between different strategies for example IRR among ventures, normally the NPV

procedure is utilized to settle on choice. It has some limitations like it is hard to acquire

anticipated income. It is very troublesome to correctly quantify the discounting rate.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Annuity of cash inflows for 5

years

300

0

PVAF @10% for 5 years

3.7

91

PV of Annuity (3,000 x 3.791)

113

73

Less: Initial investment

100

00

NPV

137

3

Project

2

Yea

r

Cash

flow

PVF

@10%

PV of

cash flow

0 -10000 1.000 -10000

1 4000 0.909 3636

2 2500 0.826 2066

3 2000 0.751 1503

4 3500 0.683 2391

5 3500 0.621 2173

NPV 1769

3.3

Every capital budgeting technique has its strengths and weaknesses in evaluating the

proposal. PBP is the least complex strategy to assess the project. It gives a few signs of risk

by isolating long term ventures from short term undertaking since it considers that longer the

period riskier it is. It can be considered as a target approach as it concentrates on incomes and

time than profitability only (Michelon, Lunkes and Bornia, 2020). Proposals which are

evaluated with PBP method are fast growth generator on account of fast liquidity and venture

recovery. Nonetheless PBP doesn't consider the profitability and overlooks the time factor. It

additionally overlooks the budgetary exhibition after the break-even point. So, venture with

shorter PBP may have shorter activity life and henceforth might be less valuable later. It

might possible in the event of two projects having same PBP however their inflows might be

unique, one, for example, being more liquid at first than the other.

Paraphrase This Document

needs enormous volume of count and it is hard to distinguish the right discounting rate

(Graham, 2020). Consequently, to settle on successful choice supervisor needs to utilize more

than one strategy for speculation proposition in light of the fact that every single procedure

has shortcoming nonetheless, shortcomings of one method is wiped out by qualities of other

procedure.

3.4 Analyse the viability of a proposal for expenditure

On the basis of the above, it is better for the company to go for Project 1 as it is

having over PBP while in contrast to this, under NPV it should go for project 2 as it is having

higher Net present value. Since both the investment appraisal techniques are providing

different answers it is better to consider NPV as it is more reliable as it considers time value

of money. Therefore, the company should go with project 2 since it is having higher NPV of

1769 as it makes use of cash flows and not net income and can be used in comparison of

multiple projects. In addition, it is helpful in evaluating projects of different sizes and

idnetifying whether the project is making expected profit or not. Thus, it is ideal to measure

the viability of the investment expenditure through NPV.

CONCLUSION

It can be summed up from the above that the finance plays a crucial role in effectively

managing the business as it is the centre part of every decision making. Without this, the

things may not go in the right direction leading to failure. It is involved in every aspect such

as investment decisions, budgeting, company’s performance analysis and so forth. Thus, it is

essential to have some knowledge about it.

Books and Journals

Bugreev, D. O., 2016. Financial analysis of small business enterprises. Contemporary

Problems of Social Work. 2(1). pp.28-35.

Kumar, A., 2019. Standard Costing and Labour Cost Variance. The Management Accountant

Journal. 54(10). pp.65-73.

Lie, C. A. and Sormin, P., 2016. Determining The Influence Of Current Ratio, Return On

Assets, Total Assets Turnover Ratio And Debt To Equity Ratio On Stock Return (A

Study Of The Manufacturing Company Listed In Indonesia Stock Exchange Period

2010-2014). JURNAL TRANSFORMATIF UNKRISWINA SUMBA. 6(1). pp.77-90.

Marzlin Marzuki, N. A. R. and Ismail, J., 2019. Benefits and limitations of variance analysis

in management accounting. ACCOUNTING BULLETIN. p.15.

Panigrahi, C. M. A., Raul, N. and Gijare, C., 2017. Liquidity Analysis of Selected

Pharmaceutical Companies: A Comparative Study. Journal of Management &

Entrepreneurship. 12(3).

Rakićević, A. and et.al, 2016. DuPont financial ratio analysis using logical aggregation.

In Soft computing applications (pp. 727-739). Springer, Cham.

Sunjoko, M. I. and ARILYN, E. J., 2016. Effects of inventory turnover, total asset turnover,

fixed asset turnover, current ratio and average collection period on

profitability. Jurnal Bisnis dan Akuntansi. 18(1). pp.79-83.

Vidal-Carreras, P. I., Garcia-Sabater, J. P. and Garcia-Sabater, J. J., 2017. A practical model

for managing inventories with unknown costs and a budget constraint. International

Journal of Production Research. 55(1). pp.118-129.

Wang, L. and Yao, D., 2017. Production planning with shortfall hedging under partial

information and budget constraint. Available at SSRN 2877378.

Michelon, P. D. S., Lunkes, R. J. and Bornia, A. C., 2020. Capital budgeting: a systematic

review of the literature. Production. 30.

Online

Evaluation of Investment Proposals: 7 Methods. 2020. [Online]. Available Through:<

https://www.businessmanagementideas.com/investment/proposals-investment/

evaluation-of-investment-proposals-7-methods-financial-management/16523 >.

Graham, R., 2020. How to Evaluate Business Investment Proposals. [Online]. Available

Through:< https://www.dummies.com/education/economics/how-to-evaluate-

business-investment-proposals/ >.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.