Finance and Funding: Analysis of the Travel and Tourism Sector

VerifiedAdded on 2020/11/23

|19

|4388

|299

Report

AI Summary

This report provides a comprehensive analysis of finance and funding within the travel and tourism sector. It begins by examining the importance of cost, volume, and profits for financial management, using Carnival Corporation & plc as a case study. The report then explores various pricing techniques used in the industry and identifies factors that influence profit. Furthermore, it delves into management accounting information, including budget reports, financial statements, variance analysis, and job costing reports, using The Fulham Shore plc as a context. The report also covers the use of investment appraisal techniques and concludes with an interpretation of the financial accounts of The Fulham Shore plc. A leaflet is also included as part of the assignment.

Finance and Funding in

Travel and Tourism

Sector

Travel and Tourism

Sector

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Importance of cost, volume and profits for financial management of Carnival Corporation

& plc.......................................................................................................................................3

1.2 Pricing techniques which are used in travel and tourism sector.......................................6

1.3 Factors that influence profit in travel and tourism businesses.........................................7

TASK 2............................................................................................................................................8

2.1 Different types of management accounting information..................................................8

2.2 Use of investment appraisal techniques as decision making tools.................................12

TASK 3..........................................................................................................................................14

3.1 Interpretation of financial accounts of The Fulham Shore plc.......................................14

TASK 4..........................................................................................................................................18

Leaflet...................................................................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Importance of cost, volume and profits for financial management of Carnival Corporation

& plc.......................................................................................................................................3

1.2 Pricing techniques which are used in travel and tourism sector.......................................6

1.3 Factors that influence profit in travel and tourism businesses.........................................7

TASK 2............................................................................................................................................8

2.1 Different types of management accounting information..................................................8

2.2 Use of investment appraisal techniques as decision making tools.................................12

TASK 3..........................................................................................................................................14

3.1 Interpretation of financial accounts of The Fulham Shore plc.......................................14

TASK 4..........................................................................................................................................18

Leaflet...................................................................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION

Finance is a term which describe study of money, investments and financial instruments

that categorises in public, corporate and personal finance. Funding is an act of money which is

contributed by business owner for buying shares for company (Ambrose, 2012). In travel and

tourism, their financial assistance is made on heritage hotels, restaurants, food courts, pubs,

travel agents, etc. This report is based on Carnival Corporation which is British- American

company and world largest travel leisure company. Relevant importance of cost and volume with

different cruise brands of Carnival Corporation are addressed in this context. This report is going

to determine management accounting information in context to travel and tourism company

Fulham Shore plc. An organisation interprets financial accounts of Fulham Shore plc and analyse

sources and distribution of funding of capital projects.

TASK 1

1.1 Importance of cost, volume and profits for financial management of Carnival Corporation &

plc

Carnival Corporation & plc is a world largest travel leisure company with having 100

vessel fleet across 10 cruise line brands. It is a merger of Carnival Corporation and Carnival plc

which functioning as one entity. It is the only company which is listed in world on both S& P

500 and FTSE 100 indices. Company provides quintessential holiday experience which based on

guest capacity. Organisation is focusing on innovative design and wide array with choices in

dining, entertainment and amenities. Travel and tourism industry provides an attractive profit in

business scenario. Their major growth in industry seen in weekends and holidays. Travel and

tourism industry are working through various aspects related with finance are define below:

Cost

Cost is a major part of travel and tourism that occur in tour packages of customers. Cost

estimation helps in achieving growth in Carnival Corporation & plc. In travel and tourism

business, cost is helpful in organising trip and providing relevant packages to customers.

Direct cost – A direct cost is mainly defined as overall attributes included in production

process of particular good and services. But sometimes, direct cost is considered as variable also

Finance is a term which describe study of money, investments and financial instruments

that categorises in public, corporate and personal finance. Funding is an act of money which is

contributed by business owner for buying shares for company (Ambrose, 2012). In travel and

tourism, their financial assistance is made on heritage hotels, restaurants, food courts, pubs,

travel agents, etc. This report is based on Carnival Corporation which is British- American

company and world largest travel leisure company. Relevant importance of cost and volume with

different cruise brands of Carnival Corporation are addressed in this context. This report is going

to determine management accounting information in context to travel and tourism company

Fulham Shore plc. An organisation interprets financial accounts of Fulham Shore plc and analyse

sources and distribution of funding of capital projects.

TASK 1

1.1 Importance of cost, volume and profits for financial management of Carnival Corporation &

plc

Carnival Corporation & plc is a world largest travel leisure company with having 100

vessel fleet across 10 cruise line brands. It is a merger of Carnival Corporation and Carnival plc

which functioning as one entity. It is the only company which is listed in world on both S& P

500 and FTSE 100 indices. Company provides quintessential holiday experience which based on

guest capacity. Organisation is focusing on innovative design and wide array with choices in

dining, entertainment and amenities. Travel and tourism industry provides an attractive profit in

business scenario. Their major growth in industry seen in weekends and holidays. Travel and

tourism industry are working through various aspects related with finance are define below:

Cost

Cost is a major part of travel and tourism that occur in tour packages of customers. Cost

estimation helps in achieving growth in Carnival Corporation & plc. In travel and tourism

business, cost is helpful in organising trip and providing relevant packages to customers.

Direct cost – A direct cost is mainly defined as overall attributes included in production

process of particular good and services. But sometimes, direct cost is considered as variable also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in the case of inconsistent as well fluctuate in amount. For instance, salary paid by Carnival

Corporation & plc to their employees are consider as direct cost.

Indirect cost – It is the cost which not directly occur while doing any activity of Carnival

Corporation & plc. Indirect cost may be fixed as well as variable both. Indirect cost are

advertising expenses, security, computing, maintenance and so on.

Fixed cost – It is that cost or expense which does not change with the increasing or

decreasing in the number of goods and services sold and produced. For Carnival Corporation &

plc it can be a beneficial term that assist them in offering appropriate cost to direct customers.

Variable cost – It is the corporate expense which are change or alter in proportion along

with producing specific output. This cost increment and decrement are depending on Carnival

Corporation & plc's production volume.

Importance of costs

In travel and tourism sector cost help its owner in making decisions for enhancing

sustainable growth and profitability. This is a systematic process which is adopted by business

organisation. As a Trainee Business advisor, an organisation always focusses on cost by

maintaining quality of product and service. Cost reduction: It is an effective system in an organisation which increases profits.

Travel and tourism sector are removing unwarranted expenses on product and services of

Carnival Corporation & plc. As a Trainee Business Advisor, this approach increases

overall profits with reducing overheads. Decision-making: Decision making denotes as a process which is made by choices that

identify, gather information and assess resolution. In context to travel and tourism

industry, manager make thoughtful decisions with relevant information and define

alternatives. Decisions are made in regarding with prospects to competitors for achieving

sustainable growth (Donaldson, 2013).

Volume

Volume is defined as a quantity which enclosed by the capacity of travellers as approx.

2500 to 3000 members. It defines level of production in quantity terms. Carnival corporation &

plc is measuring terms of volume by trips taken, nights away etc. and value is defined by

expenditure.

Importance of volume

Corporation & plc to their employees are consider as direct cost.

Indirect cost – It is the cost which not directly occur while doing any activity of Carnival

Corporation & plc. Indirect cost may be fixed as well as variable both. Indirect cost are

advertising expenses, security, computing, maintenance and so on.

Fixed cost – It is that cost or expense which does not change with the increasing or

decreasing in the number of goods and services sold and produced. For Carnival Corporation &

plc it can be a beneficial term that assist them in offering appropriate cost to direct customers.

Variable cost – It is the corporate expense which are change or alter in proportion along

with producing specific output. This cost increment and decrement are depending on Carnival

Corporation & plc's production volume.

Importance of costs

In travel and tourism sector cost help its owner in making decisions for enhancing

sustainable growth and profitability. This is a systematic process which is adopted by business

organisation. As a Trainee Business advisor, an organisation always focusses on cost by

maintaining quality of product and service. Cost reduction: It is an effective system in an organisation which increases profits.

Travel and tourism sector are removing unwarranted expenses on product and services of

Carnival Corporation & plc. As a Trainee Business Advisor, this approach increases

overall profits with reducing overheads. Decision-making: Decision making denotes as a process which is made by choices that

identify, gather information and assess resolution. In context to travel and tourism

industry, manager make thoughtful decisions with relevant information and define

alternatives. Decisions are made in regarding with prospects to competitors for achieving

sustainable growth (Donaldson, 2013).

Volume

Volume is defined as a quantity which enclosed by the capacity of travellers as approx.

2500 to 3000 members. It defines level of production in quantity terms. Carnival corporation &

plc is measuring terms of volume by trips taken, nights away etc. and value is defined by

expenditure.

Importance of volume

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Volume is the number of shares which lead with overall activity of security market. It is

an amount or quantity which is an indicator of business and uses to confirm a scenario. This

provide investor an idea about price action by buying and selling security. Major aspects of

volume are:

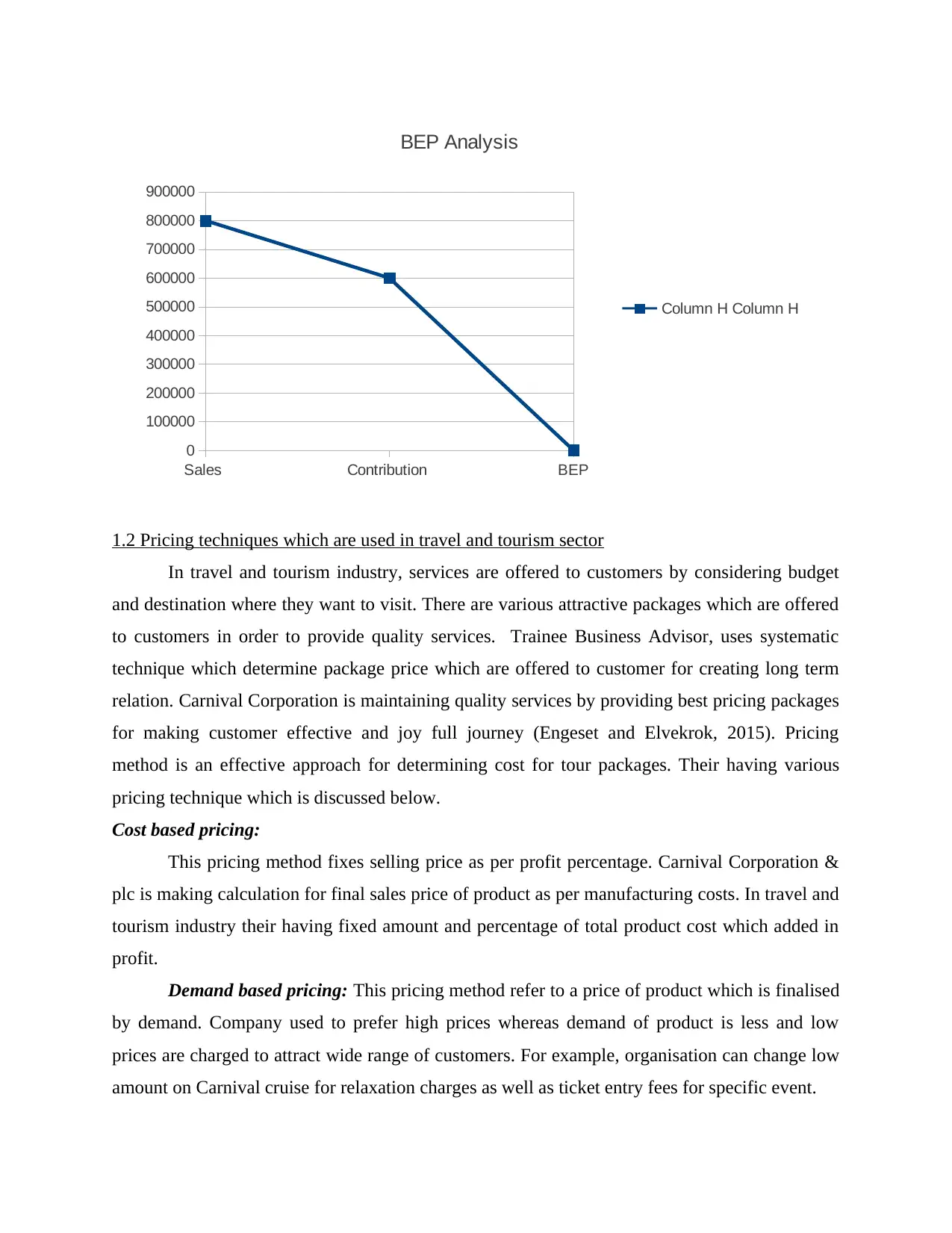

BEP analysis: Break-even analysis is a technique which is widely used by production

and management accountants. This analysis tool is determined by level of company product and

service which is more profitable in travel and tourism industry. As a Trainee Business Advisor,

Carnival Corporation & plc is comparing variable and fixed costs with sales revenue in order to

determine sales volume which makes neither profit nor loss.

Economies of scale: It denote as a competitive advantage which having large entities

over smaller ones. In context to travel and tourism, company optimises variable cost per units

with respect to operational efficiency and sustainable growth (El-Gohary, 2016).

Diseconomies of scale: This is an opposite of economies of scale which faces condition

in relation to performance and generate profits. This arises conditions like high competition,

compromises, low performance with respect to quality services of Carnival Corporation & plc

and therefore is important for financial management of firm.

BEV

Sales 800000

Fixed cost 120000

Contribution 600000

BEP 0.2

an amount or quantity which is an indicator of business and uses to confirm a scenario. This

provide investor an idea about price action by buying and selling security. Major aspects of

volume are:

BEP analysis: Break-even analysis is a technique which is widely used by production

and management accountants. This analysis tool is determined by level of company product and

service which is more profitable in travel and tourism industry. As a Trainee Business Advisor,

Carnival Corporation & plc is comparing variable and fixed costs with sales revenue in order to

determine sales volume which makes neither profit nor loss.

Economies of scale: It denote as a competitive advantage which having large entities

over smaller ones. In context to travel and tourism, company optimises variable cost per units

with respect to operational efficiency and sustainable growth (El-Gohary, 2016).

Diseconomies of scale: This is an opposite of economies of scale which faces condition

in relation to performance and generate profits. This arises conditions like high competition,

compromises, low performance with respect to quality services of Carnival Corporation & plc

and therefore is important for financial management of firm.

BEV

Sales 800000

Fixed cost 120000

Contribution 600000

BEP 0.2

Sales Contribution BEP

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

BEP Analysis

Column H Column H

1.2 Pricing techniques which are used in travel and tourism sector

In travel and tourism industry, services are offered to customers by considering budget

and destination where they want to visit. There are various attractive packages which are offered

to customers in order to provide quality services. Trainee Business Advisor, uses systematic

technique which determine package price which are offered to customer for creating long term

relation. Carnival Corporation is maintaining quality services by providing best pricing packages

for making customer effective and joy full journey (Engeset and Elvekrok, 2015). Pricing

method is an effective approach for determining cost for tour packages. Their having various

pricing technique which is discussed below.

Cost based pricing:

This pricing method fixes selling price as per profit percentage. Carnival Corporation &

plc is making calculation for final sales price of product as per manufacturing costs. In travel and

tourism industry their having fixed amount and percentage of total product cost which added in

profit.

Demand based pricing: This pricing method refer to a price of product which is finalised

by demand. Company used to prefer high prices whereas demand of product is less and low

prices are charged to attract wide range of customers. For example, organisation can change low

amount on Carnival cruise for relaxation charges as well as ticket entry fees for specific event.

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

BEP Analysis

Column H Column H

1.2 Pricing techniques which are used in travel and tourism sector

In travel and tourism industry, services are offered to customers by considering budget

and destination where they want to visit. There are various attractive packages which are offered

to customers in order to provide quality services. Trainee Business Advisor, uses systematic

technique which determine package price which are offered to customer for creating long term

relation. Carnival Corporation is maintaining quality services by providing best pricing packages

for making customer effective and joy full journey (Engeset and Elvekrok, 2015). Pricing

method is an effective approach for determining cost for tour packages. Their having various

pricing technique which is discussed below.

Cost based pricing:

This pricing method fixes selling price as per profit percentage. Carnival Corporation &

plc is making calculation for final sales price of product as per manufacturing costs. In travel and

tourism industry their having fixed amount and percentage of total product cost which added in

profit.

Demand based pricing: This pricing method refer to a price of product which is finalised

by demand. Company used to prefer high prices whereas demand of product is less and low

prices are charged to attract wide range of customers. For example, organisation can change low

amount on Carnival cruise for relaxation charges as well as ticket entry fees for specific event.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Competition- based pricing: This refers to a method in which prices are consider as per

competitors in market. For example, Carnival Corporation & plc tourism company is charging

higher, lower or equal prices on accommodation services as per competitors.

Cost plus pricing method: This method is useful in determining prices within a simplest

form. It is a most common method which is used in manufacturing organisation. For example,

ABC company bears total cost 100 per unit for producing product and add 70 per unit price of

product as a profit. In this case determine final price of product is 170.

1.3 Factors that influence profit in travel and tourism businesses

Travel and Tourism is dealing primarily with a factor and encouraging people to go and

visit desire location. As a Trainee Business Advisor, company is driving several factors which

increases profit margins. There are various aspects which enhances profit in an organisation are

define below (Fayos-Sola, 2012).

Seasonal variations – These kinds of aspects are based on climate suitability that

influence tourist's decision making. Some visitors prefer to visit countries during the winter

season at this situation it is hard for travel and tourism organisation to sustain in the market with

active profit in other seasons. These kinds of factors can influence business profitability as well

as its sale.

Political environment - Political environmental factors directly affect business

operations and its functions in effective manner. Travel and tourism industry is highly dependent

on political stability of a nation. Incidents relating to corruption, terrorism make a huge negative

impact on popularity of a tourist destination. For example, countries like Syria are getting

vanished from travel plans of many people because of the presence of ISIS terrorist organisation.

Current trends - This factor affect the decision making and profitability of tour and

travel company such as if there is trend of Italian cuisine but respective hotel or restaurant is

offering other type of dishes. In this case they will not able to satisfy their customers wants and

needs and reduce the footfall which directly impact on profit and growth of the hotel.

Lack of trained Staff – In an organisation employees are considered as a strength who

helps in managing customer's experience properly. Thus, untrained staff member can impact

negatively upon the decision making of tourists. Therefore, it is required for carnival corporation

& plc to provide appropriate training to their staff members.

Competitors:

competitors in market. For example, Carnival Corporation & plc tourism company is charging

higher, lower or equal prices on accommodation services as per competitors.

Cost plus pricing method: This method is useful in determining prices within a simplest

form. It is a most common method which is used in manufacturing organisation. For example,

ABC company bears total cost 100 per unit for producing product and add 70 per unit price of

product as a profit. In this case determine final price of product is 170.

1.3 Factors that influence profit in travel and tourism businesses

Travel and Tourism is dealing primarily with a factor and encouraging people to go and

visit desire location. As a Trainee Business Advisor, company is driving several factors which

increases profit margins. There are various aspects which enhances profit in an organisation are

define below (Fayos-Sola, 2012).

Seasonal variations – These kinds of aspects are based on climate suitability that

influence tourist's decision making. Some visitors prefer to visit countries during the winter

season at this situation it is hard for travel and tourism organisation to sustain in the market with

active profit in other seasons. These kinds of factors can influence business profitability as well

as its sale.

Political environment - Political environmental factors directly affect business

operations and its functions in effective manner. Travel and tourism industry is highly dependent

on political stability of a nation. Incidents relating to corruption, terrorism make a huge negative

impact on popularity of a tourist destination. For example, countries like Syria are getting

vanished from travel plans of many people because of the presence of ISIS terrorist organisation.

Current trends - This factor affect the decision making and profitability of tour and

travel company such as if there is trend of Italian cuisine but respective hotel or restaurant is

offering other type of dishes. In this case they will not able to satisfy their customers wants and

needs and reduce the footfall which directly impact on profit and growth of the hotel.

Lack of trained Staff – In an organisation employees are considered as a strength who

helps in managing customer's experience properly. Thus, untrained staff member can impact

negatively upon the decision making of tourists. Therefore, it is required for carnival corporation

& plc to provide appropriate training to their staff members.

Competitors:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Competitors are those who sell similar products or facilitates same services into the

market. For high competition Carnival Corporation & plc provides cruise such as celebrity

cruises, Royal Caribbean cruises and so on. Whereas for low competition it facilitates

aeroplanes, ship etc. like the small cruise ship collection and also arrange funds for them.

TASK 2

2.1 Different types of management accounting information

Management accounting is focused on internal managers and decision makers that can

used to provide financial data relevant to managers operations in a business decision. This is the

efficient tool used to find out the effective decisions of an industry. Travel and tourism are the

fastest growing industry in service sector throughout the world which have global market

scenarios which can analyse budget report, financial statement, variance analysis and job cost

report.

Budget report: -

A budget report is an internal report which can be used by management of The Fulham

Shore plc to compare estimate budgeted projections with actual performance during a given

period of time that mobilise all resources. The company have to designed the budgeted

performance to actual performance in an accounting period to achieve long term goals.

Financial statement: -

It is a formal records of financial activities and position of a business, person or other

entity of a firm. It can help managers of Fulham Shore plc in making decisions that can make a

financial position of The Fulham shore that can make an organisation fully financial decisions. It

is effective management accounting tool consist of all necessary information like, owners’

equity, liabilities and assets.

Variance analysis: -

The Fulham shore can used to compare actual performance and planned behaviour in

which analysis can used to maintain control over a business. It is a tool of budgetary control by

evaluation of performance variances that can used to manipulate data with actual amount

incurred sold (Halkier, 2014).

Job costing report: -

market. For high competition Carnival Corporation & plc provides cruise such as celebrity

cruises, Royal Caribbean cruises and so on. Whereas for low competition it facilitates

aeroplanes, ship etc. like the small cruise ship collection and also arrange funds for them.

TASK 2

2.1 Different types of management accounting information

Management accounting is focused on internal managers and decision makers that can

used to provide financial data relevant to managers operations in a business decision. This is the

efficient tool used to find out the effective decisions of an industry. Travel and tourism are the

fastest growing industry in service sector throughout the world which have global market

scenarios which can analyse budget report, financial statement, variance analysis and job cost

report.

Budget report: -

A budget report is an internal report which can be used by management of The Fulham

Shore plc to compare estimate budgeted projections with actual performance during a given

period of time that mobilise all resources. The company have to designed the budgeted

performance to actual performance in an accounting period to achieve long term goals.

Financial statement: -

It is a formal records of financial activities and position of a business, person or other

entity of a firm. It can help managers of Fulham Shore plc in making decisions that can make a

financial position of The Fulham shore that can make an organisation fully financial decisions. It

is effective management accounting tool consist of all necessary information like, owners’

equity, liabilities and assets.

Variance analysis: -

The Fulham shore can used to compare actual performance and planned behaviour in

which analysis can used to maintain control over a business. It is a tool of budgetary control by

evaluation of performance variances that can used to manipulate data with actual amount

incurred sold (Halkier, 2014).

Job costing report: -

Job costing report is prepared to identify he cost and revenue that can manipulate

jobseekers into job provider. Managers of The Fulham shore use this to find out profitability and

management decision to find job cost in order to determine needs and objectives of company.

Training package:

Basis of package Requirement

Purpose To reduce the ineffectiveness in the

nature of employees

To enhance the competence subject to

handling risk and query

Format The format will be bifurcated as per the

strength of employees such as medium

low and high

Time of training Morning (9.30 am to 12.00)

Evening (4.00 pm to 6.00 pm)

Income statement:

It is known as core financial statements of company which shows its profit and loss.

Incomes statements generally summarise the incomes and expenditures that are produced within

reporting period. The Fulham shore use this to know about their revenues and expenses over a

period of time.

Cash flow:

It is considered as a amount of cash or cash equivalents which are being transferred into

as well as out of a company. The Fulham shore can utilise this to analyse the inflows and

outflows of cash in given time period.

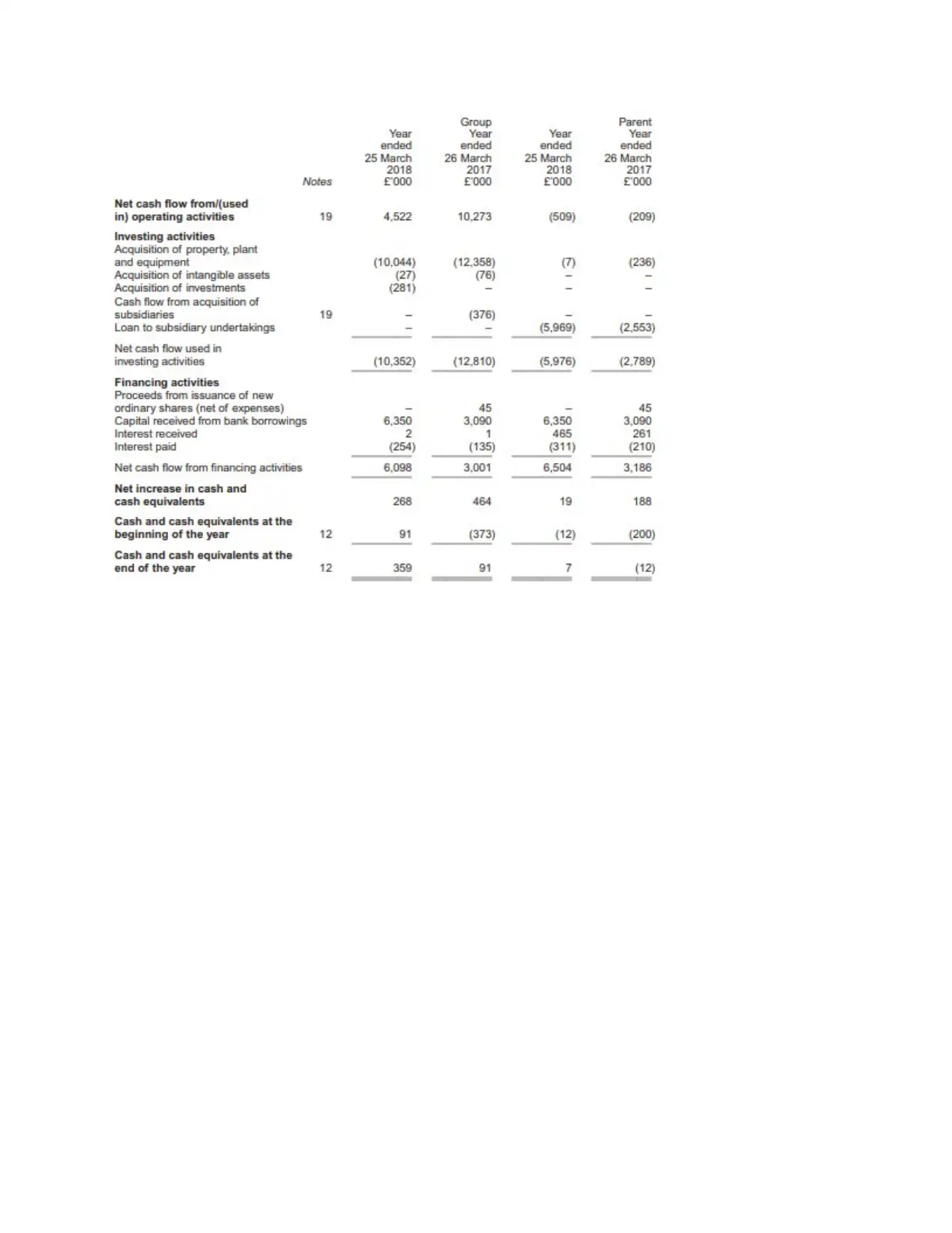

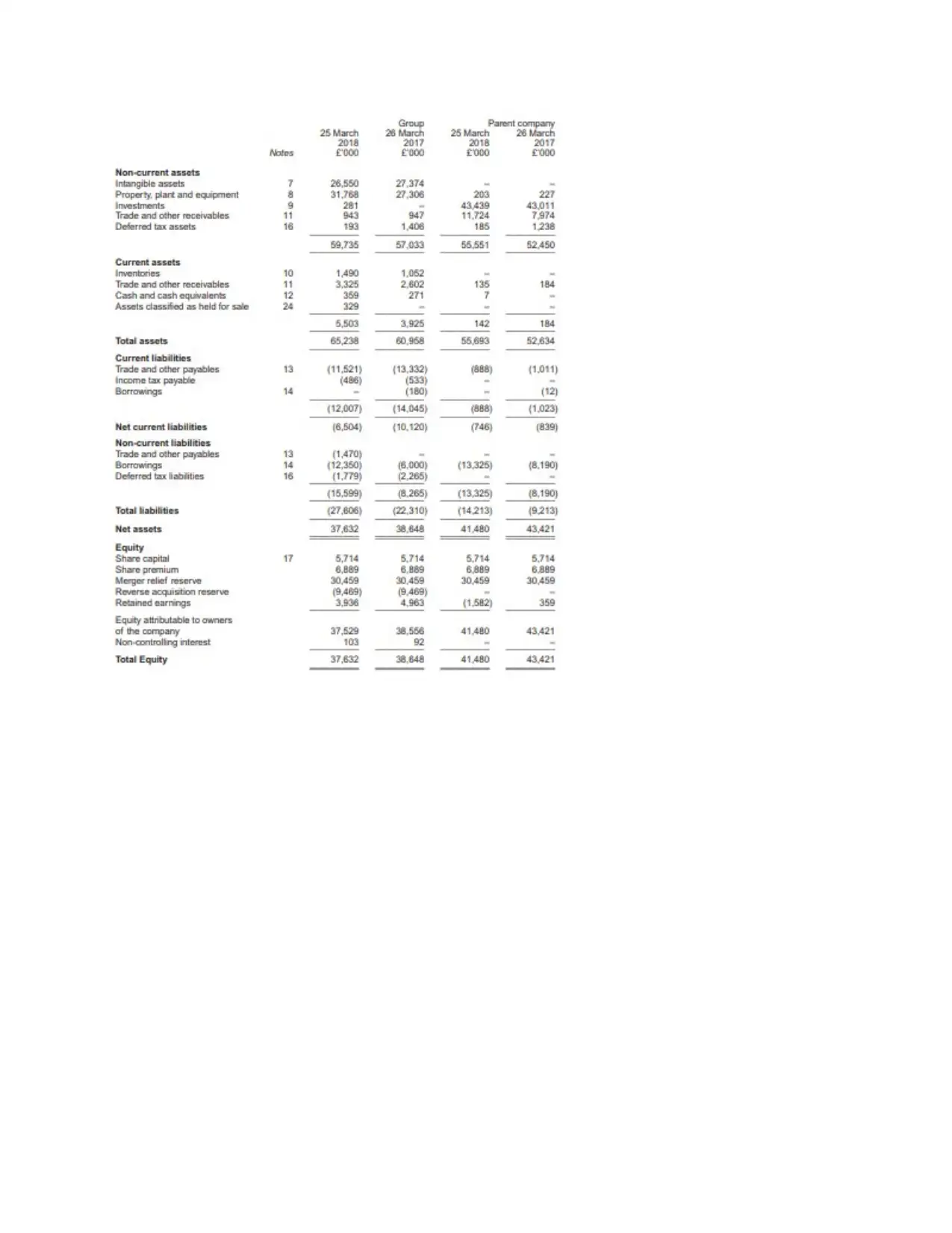

Financial statements of THE FULHAM SHORE PLC

jobseekers into job provider. Managers of The Fulham shore use this to find out profitability and

management decision to find job cost in order to determine needs and objectives of company.

Training package:

Basis of package Requirement

Purpose To reduce the ineffectiveness in the

nature of employees

To enhance the competence subject to

handling risk and query

Format The format will be bifurcated as per the

strength of employees such as medium

low and high

Time of training Morning (9.30 am to 12.00)

Evening (4.00 pm to 6.00 pm)

Income statement:

It is known as core financial statements of company which shows its profit and loss.

Incomes statements generally summarise the incomes and expenditures that are produced within

reporting period. The Fulham shore use this to know about their revenues and expenses over a

period of time.

Cash flow:

It is considered as a amount of cash or cash equivalents which are being transferred into

as well as out of a company. The Fulham shore can utilise this to analyse the inflows and

outflows of cash in given time period.

Financial statements of THE FULHAM SHORE PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

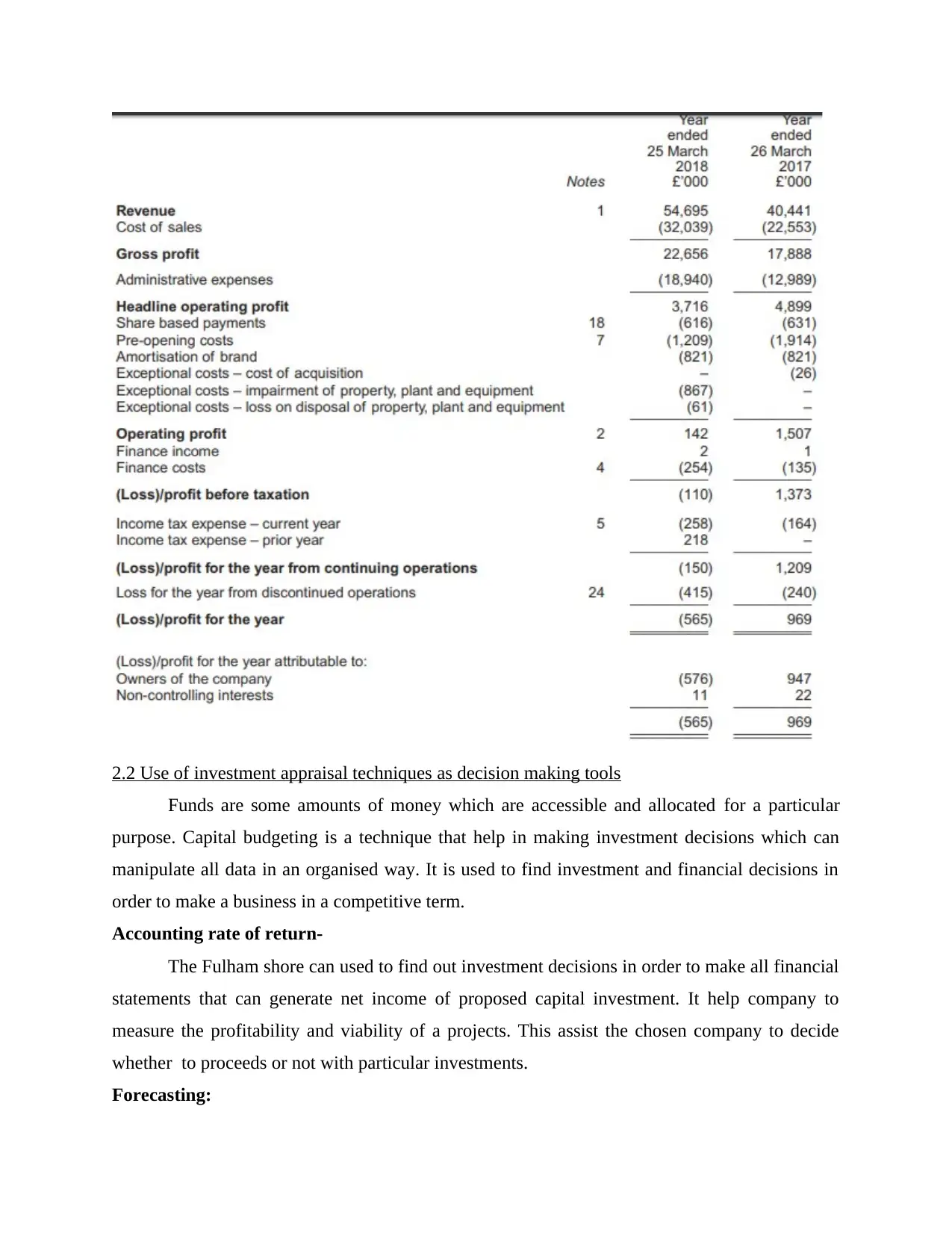

2.2 Use of investment appraisal techniques as decision making tools

Funds are some amounts of money which are accessible and allocated for a particular

purpose. Capital budgeting is a technique that help in making investment decisions which can

manipulate all data in an organised way. It is used to find investment and financial decisions in

order to make a business in a competitive term.

Accounting rate of return-

The Fulham shore can used to find out investment decisions in order to make all financial

statements that can generate net income of proposed capital investment. It help company to

measure the profitability and viability of a projects. This assist the chosen company to decide

whether to proceeds or not with particular investments.

Forecasting:

Funds are some amounts of money which are accessible and allocated for a particular

purpose. Capital budgeting is a technique that help in making investment decisions which can

manipulate all data in an organised way. It is used to find investment and financial decisions in

order to make a business in a competitive term.

Accounting rate of return-

The Fulham shore can used to find out investment decisions in order to make all financial

statements that can generate net income of proposed capital investment. It help company to

measure the profitability and viability of a projects. This assist the chosen company to decide

whether to proceeds or not with particular investments.

Forecasting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.