Effective Management of Resources in Hospitality Industry

VerifiedAdded on 2020/07/23

|16

|4715

|41

AI Summary

The assignment report concludes that effective management of resources is crucial for achieving better management of an organisation. It highlights various sources of finance available for the hospitality industry, such as BEP, to increase overall growth and performance. The report also discusses the importance of corporate social responsibility in tourism and provides references to relevant studies and journals.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance in Hospitality

Industry

Industry

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1.1: Sources of funding available to business and service sector.........................................1

P1.2: Evaluating contribution made by range of method in generating income....................2

TASK 2............................................................................................................................................2

P2.1: Discussion of elements of costs and profit and role of setting selling prices...............2

P2.2: Methods of controlling stock and cash..........................................................................3

TASK 3............................................................................................................................................4

P3.1: Process of trail balance and sources or structure..........................................................4

P3.2: Evaluating of business accounts, adjustments..............................................................5

P3.3: Process and objectives of budgetary control.................................................................7

P3.4: Analysis of budget variance..........................................................................................8

TASK 4............................................................................................................................................9

P4.1: Computation of various ratios of Belgravia Hotels.......................................................9

P4.2: Recommendation for future management strategies to improve performance...........11

TASK 5..........................................................................................................................................11

P5.1: Categories cost of components....................................................................................11

P5.2: Calculation of Contribution per units..........................................................................12

P5.3: Importance of BEP......................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1.1: Sources of funding available to business and service sector.........................................1

P1.2: Evaluating contribution made by range of method in generating income....................2

TASK 2............................................................................................................................................2

P2.1: Discussion of elements of costs and profit and role of setting selling prices...............2

P2.2: Methods of controlling stock and cash..........................................................................3

TASK 3............................................................................................................................................4

P3.1: Process of trail balance and sources or structure..........................................................4

P3.2: Evaluating of business accounts, adjustments..............................................................5

P3.3: Process and objectives of budgetary control.................................................................7

P3.4: Analysis of budget variance..........................................................................................8

TASK 4............................................................................................................................................9

P4.1: Computation of various ratios of Belgravia Hotels.......................................................9

P4.2: Recommendation for future management strategies to improve performance...........11

TASK 5..........................................................................................................................................11

P5.1: Categories cost of components....................................................................................11

P5.2: Calculation of Contribution per units..........................................................................12

P5.3: Importance of BEP......................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Nowadays, it has been seen that plenty of organisations are looking for an effective system

that can help account officers to manage and control their everyday business operations. Finance

is more valuable aspect for any profit generating sector. Without having sufficient amount of

capital they cannot be able to manage its day to day business activities. In case of hospitality

sector they need to have valuable amount of finance to control accommodation facilities that are

needed by various people (Jones, Hillier and Comfort, 2016).

The project report is providing more effective information about availability of resources

that can assist in formulating better understanding of crucial matters that are helpful in

determining overall growth and profitability of an organisation. Identification of various sources

of funds available to hospitality sectors are discuss under this report. Certain components of

costs and gains in setting selling prices in services sectors are explain under this project.

TASK 1

P1.1: Sources of funding available to business and service sector

In every business organisation, it is necessary to have establishment of hotelier with

expansion strategies for an ongoing prosperous of business. The requirement of capital in their

management operations is utmost crucial aspects that are needed to be taken into consideration.

There are various sources of finance available to an any hospitality sectors. Some of them are

discuss underneath:

Retained earnings: It is known as one of the primary sources of profit that a company

has earned to date, less any dividends or other distribution which are paid to the investors. These

profits are further utilised in planning of expansion of the new business.

Venture funding: It is a kind of private equity which is form of financing that is

provided by the firm or capital to small in their earlier phase. Investors of the Belgravia Hotels

can for this types of sources which will assist them to plan their business more effectively

(Martínez, Pérez and Rodríguez del Bosque, 2013).

Personal finance: It is said to be riskier and small and medium source of funding is more

economical through use of personal loans. Belgravia Hotels are having appropriate opportunities

to increase profitability of an organisation.

1

Nowadays, it has been seen that plenty of organisations are looking for an effective system

that can help account officers to manage and control their everyday business operations. Finance

is more valuable aspect for any profit generating sector. Without having sufficient amount of

capital they cannot be able to manage its day to day business activities. In case of hospitality

sector they need to have valuable amount of finance to control accommodation facilities that are

needed by various people (Jones, Hillier and Comfort, 2016).

The project report is providing more effective information about availability of resources

that can assist in formulating better understanding of crucial matters that are helpful in

determining overall growth and profitability of an organisation. Identification of various sources

of funds available to hospitality sectors are discuss under this report. Certain components of

costs and gains in setting selling prices in services sectors are explain under this project.

TASK 1

P1.1: Sources of funding available to business and service sector

In every business organisation, it is necessary to have establishment of hotelier with

expansion strategies for an ongoing prosperous of business. The requirement of capital in their

management operations is utmost crucial aspects that are needed to be taken into consideration.

There are various sources of finance available to an any hospitality sectors. Some of them are

discuss underneath:

Retained earnings: It is known as one of the primary sources of profit that a company

has earned to date, less any dividends or other distribution which are paid to the investors. These

profits are further utilised in planning of expansion of the new business.

Venture funding: It is a kind of private equity which is form of financing that is

provided by the firm or capital to small in their earlier phase. Investors of the Belgravia Hotels

can for this types of sources which will assist them to plan their business more effectively

(Martínez, Pérez and Rodríguez del Bosque, 2013).

Personal finance: It is said to be riskier and small and medium source of funding is more

economical through use of personal loans. Belgravia Hotels are having appropriate opportunities

to increase profitability of an organisation.

1

Government grants: Most of the time, industries are not being able to manager

sufficient amount of capital for their business. Thus, certain government agencies used to

provide financing such as grants and subsidies that can be available to their business.

Bank loan: It is necessary to make use of short term loan for their businesses so that

available requirements can be meet out in more quick time. In order to provide loan bank uses to

charge certain amount as interest (Leung and Law, 2013).

P1.2: Evaluating contribution made by range of method in generating income

There are various aspects or modes which are helpful in generating income and sufficient

contribution to hospitality industry can be examined by using various methods:

Sales: It has been seen in hospitality sector which associated with provide various hotel

facilities such as allocating rooms, food and beverages and other effective services that

are useful in generating sufficient amount of capital to the company.

Commission: These are mainly related with those parties those are responsible for

providing vital information about best hotel and their services from which income would

retain from the third party.

Sponsorship: It is one of the important modes from which valuable amount of capital can

be raised. This will be achieving from other companies for the promotion of their hotel

names (McManus, 2013).

Grants: These kinds of incomes and supportive contribution can be collected from

government side or any other legal authorities those are helpful in regulating their hotel

requirements.

Sub-letting: As some of hotel units are transfer to third parties in order to increase their

maximum gains so they need to sub letting their business operations to cover up their

losses or to increase profitability for the company up to an extent.

TASK 2

P2.1: Discussion of elements of costs and profit and role of setting selling prices

There are various cost which are determined as crucial elements of costs those are

associated with hospitality sectors. Some of them are discuss underneath:

Material: These are related with those costs in the final product or services those are being

incurred to deliver a specific products and services. Some of them are Linen, Cutlery and

glassware.

2

sufficient amount of capital for their business. Thus, certain government agencies used to

provide financing such as grants and subsidies that can be available to their business.

Bank loan: It is necessary to make use of short term loan for their businesses so that

available requirements can be meet out in more quick time. In order to provide loan bank uses to

charge certain amount as interest (Leung and Law, 2013).

P1.2: Evaluating contribution made by range of method in generating income

There are various aspects or modes which are helpful in generating income and sufficient

contribution to hospitality industry can be examined by using various methods:

Sales: It has been seen in hospitality sector which associated with provide various hotel

facilities such as allocating rooms, food and beverages and other effective services that

are useful in generating sufficient amount of capital to the company.

Commission: These are mainly related with those parties those are responsible for

providing vital information about best hotel and their services from which income would

retain from the third party.

Sponsorship: It is one of the important modes from which valuable amount of capital can

be raised. This will be achieving from other companies for the promotion of their hotel

names (McManus, 2013).

Grants: These kinds of incomes and supportive contribution can be collected from

government side or any other legal authorities those are helpful in regulating their hotel

requirements.

Sub-letting: As some of hotel units are transfer to third parties in order to increase their

maximum gains so they need to sub letting their business operations to cover up their

losses or to increase profitability for the company up to an extent.

TASK 2

P2.1: Discussion of elements of costs and profit and role of setting selling prices

There are various cost which are determined as crucial elements of costs those are

associated with hospitality sectors. Some of them are discuss underneath:

Material: These are related with those costs in the final product or services those are being

incurred to deliver a specific products and services. Some of them are Linen, Cutlery and

glassware.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Consumable: There are many components in final goods in hospitality sector. This will require

upcoming processing to deliver the overall products to their guests. Like Foods and beverages.

Labour: All these costs are related with maintaining overall growth of the company.

These would be responsible for providing relevant operating functions in delivery more better

services to an organization. Examples, salary paid to staff, waiters and front office members

(Bowie and et. al., 2016).

Selling price and gross profit margin:

These approaches are being helpful for hospital sectors which can be determine as follows:

Pricing in tourism sectors (Peak /peak off- trading cost):

In case of any peal seasons which is being prepared by including additional cost as mark-

up to the operational costs as selling cost price. Whereas in peak off season, it is adjustment

through reducing mark up and offering discounts for selling cost through considering

competition as primary aspects.

Absorption price approach: Under this, variable cost per units has been calculated initially and

make after all overhead cost are said to be absorbed to unit cost.

Conventional pricing approach: It is primary focus on all those aspects that setting

contribution margins as difference planning income by making segmentation such as beverages,

rooms and other operational parts (Campo, Díaz and J. Yagüe, 2014).

P2.2: Methods of controlling stock and cash

It is essential for every business to make proper control and management of their cash

and stock in more effective manner so that maximum opportunities can be generated in more

quick time. This will provide specific ways to operate proper functioning of everyday operations

and their working management in an organisation. There are various inventory control measures

which are mentioned underneath:

EOQ (Economic order quantity): It is necessary for the hotel company to make

identification of their available stocks position or re-order level so that during nay urgency it can

be measure in more effective manner (Nwokorie and Ezeibe, 2016).

It is necessary to avoid unnecessary stock buying that has been done by hotel managers in their

regular course of actions.

It is essential to just in time management system so that proper control and management can be

determined by the hotel industry.

3

upcoming processing to deliver the overall products to their guests. Like Foods and beverages.

Labour: All these costs are related with maintaining overall growth of the company.

These would be responsible for providing relevant operating functions in delivery more better

services to an organization. Examples, salary paid to staff, waiters and front office members

(Bowie and et. al., 2016).

Selling price and gross profit margin:

These approaches are being helpful for hospital sectors which can be determine as follows:

Pricing in tourism sectors (Peak /peak off- trading cost):

In case of any peal seasons which is being prepared by including additional cost as mark-

up to the operational costs as selling cost price. Whereas in peak off season, it is adjustment

through reducing mark up and offering discounts for selling cost through considering

competition as primary aspects.

Absorption price approach: Under this, variable cost per units has been calculated initially and

make after all overhead cost are said to be absorbed to unit cost.

Conventional pricing approach: It is primary focus on all those aspects that setting

contribution margins as difference planning income by making segmentation such as beverages,

rooms and other operational parts (Campo, Díaz and J. Yagüe, 2014).

P2.2: Methods of controlling stock and cash

It is essential for every business to make proper control and management of their cash

and stock in more effective manner so that maximum opportunities can be generated in more

quick time. This will provide specific ways to operate proper functioning of everyday operations

and their working management in an organisation. There are various inventory control measures

which are mentioned underneath:

EOQ (Economic order quantity): It is necessary for the hotel company to make

identification of their available stocks position or re-order level so that during nay urgency it can

be measure in more effective manner (Nwokorie and Ezeibe, 2016).

It is necessary to avoid unnecessary stock buying that has been done by hotel managers in their

regular course of actions.

It is essential to just in time management system so that proper control and management can be

determined by the hotel industry.

3

This has been observed that hospitality industry is mostly deal with perishable products such as

food and beverages. Henceforth, it is associated to maintain proper JIT inventory system to

reduce extra wastage of hotel.

Cash control measures are:

It is necessary to keep hold of considerable cash amount which is encouraged to conduct

smooth operation of hotel business. It can be manage by using:

Effective dual control over the cash flows incur during the time.

IT is primary responsibility of front office department to provide authorities for two

persons to verify and keep record of cash balances.

Entry in the cash books on regular basis is needed to be done so that banks statements

should indicate proper balances (Singh, 2016).

TASK 3

P3.1: Process of trail balance and sources or structure

In every business, there financial records are overall base which can be use for making

valuable decision in near future. The primary sources of trail balance are taken from journal

entries which are further posted into ledger accounting and from there it would be transfer into

trail balance. It has been divided into three parts, general ledger, purchase ledger and name

ledger. Purchase books include the personal accounting which is associated with supplier. Sales

books are mainly related to personal account of customers as debtors. It is one of the primary

accounting by which the other sources of financial statements of the company can be formulated

in easier manner (Ndoda, 2013).

Structure of trail balance:

Particular Debit amount Credit amount

Cash Xxx

Accountant receivable Xxx

Office supplies Xxx

Office equipment Xxx

Rent expenses Xxx

Salary expense Xxx

Utilities expenses Xxx

4

food and beverages. Henceforth, it is associated to maintain proper JIT inventory system to

reduce extra wastage of hotel.

Cash control measures are:

It is necessary to keep hold of considerable cash amount which is encouraged to conduct

smooth operation of hotel business. It can be manage by using:

Effective dual control over the cash flows incur during the time.

IT is primary responsibility of front office department to provide authorities for two

persons to verify and keep record of cash balances.

Entry in the cash books on regular basis is needed to be done so that banks statements

should indicate proper balances (Singh, 2016).

TASK 3

P3.1: Process of trail balance and sources or structure

In every business, there financial records are overall base which can be use for making

valuable decision in near future. The primary sources of trail balance are taken from journal

entries which are further posted into ledger accounting and from there it would be transfer into

trail balance. It has been divided into three parts, general ledger, purchase ledger and name

ledger. Purchase books include the personal accounting which is associated with supplier. Sales

books are mainly related to personal account of customers as debtors. It is one of the primary

accounting by which the other sources of financial statements of the company can be formulated

in easier manner (Ndoda, 2013).

Structure of trail balance:

Particular Debit amount Credit amount

Cash Xxx

Accountant receivable Xxx

Office supplies Xxx

Office equipment Xxx

Rent expenses Xxx

Salary expense Xxx

Utilities expenses Xxx

4

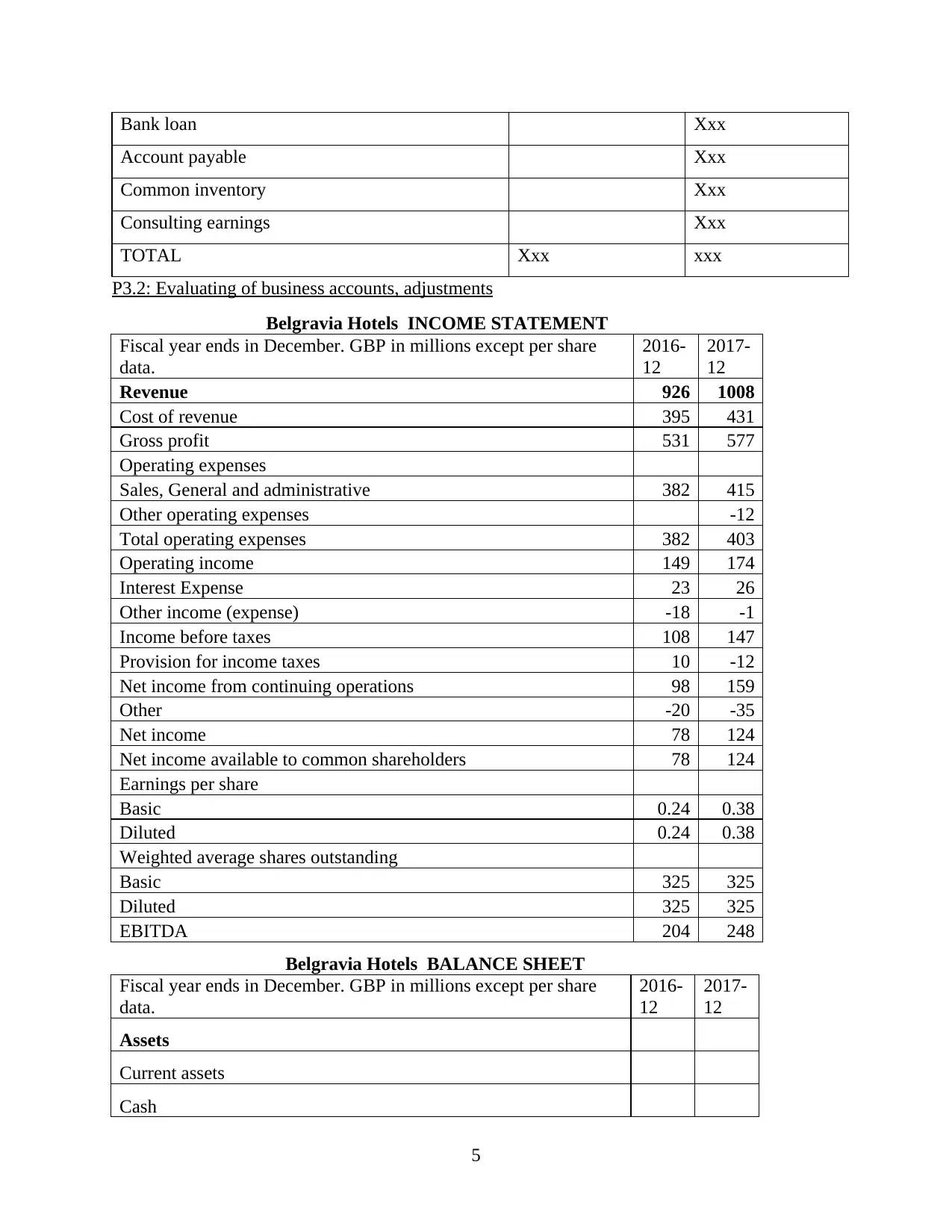

Bank loan Xxx

Account payable Xxx

Common inventory Xxx

Consulting earnings Xxx

TOTAL Xxx xxx

P3.2: Evaluating of business accounts, adjustments

Belgravia Hotels INCOME STATEMENT

Fiscal year ends in December. GBP in millions except per share

data.

2016-

12

2017-

12

Revenue 926 1008

Cost of revenue 395 431

Gross profit 531 577

Operating expenses

Sales, General and administrative 382 415

Other operating expenses -12

Total operating expenses 382 403

Operating income 149 174

Interest Expense 23 26

Other income (expense) -18 -1

Income before taxes 108 147

Provision for income taxes 10 -12

Net income from continuing operations 98 159

Other -20 -35

Net income 78 124

Net income available to common shareholders 78 124

Earnings per share

Basic 0.24 0.38

Diluted 0.24 0.38

Weighted average shares outstanding

Basic 325 325

Diluted 325 325

EBITDA 204 248

Belgravia Hotels BALANCE SHEET

Fiscal year ends in December. GBP in millions except per share

data.

2016-

12

2017-

12

Assets

Current assets

Cash

5

Account payable Xxx

Common inventory Xxx

Consulting earnings Xxx

TOTAL Xxx xxx

P3.2: Evaluating of business accounts, adjustments

Belgravia Hotels INCOME STATEMENT

Fiscal year ends in December. GBP in millions except per share

data.

2016-

12

2017-

12

Revenue 926 1008

Cost of revenue 395 431

Gross profit 531 577

Operating expenses

Sales, General and administrative 382 415

Other operating expenses -12

Total operating expenses 382 403

Operating income 149 174

Interest Expense 23 26

Other income (expense) -18 -1

Income before taxes 108 147

Provision for income taxes 10 -12

Net income from continuing operations 98 159

Other -20 -35

Net income 78 124

Net income available to common shareholders 78 124

Earnings per share

Basic 0.24 0.38

Diluted 0.24 0.38

Weighted average shares outstanding

Basic 325 325

Diluted 325 325

EBITDA 204 248

Belgravia Hotels BALANCE SHEET

Fiscal year ends in December. GBP in millions except per share

data.

2016-

12

2017-

12

Assets

Current assets

Cash

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

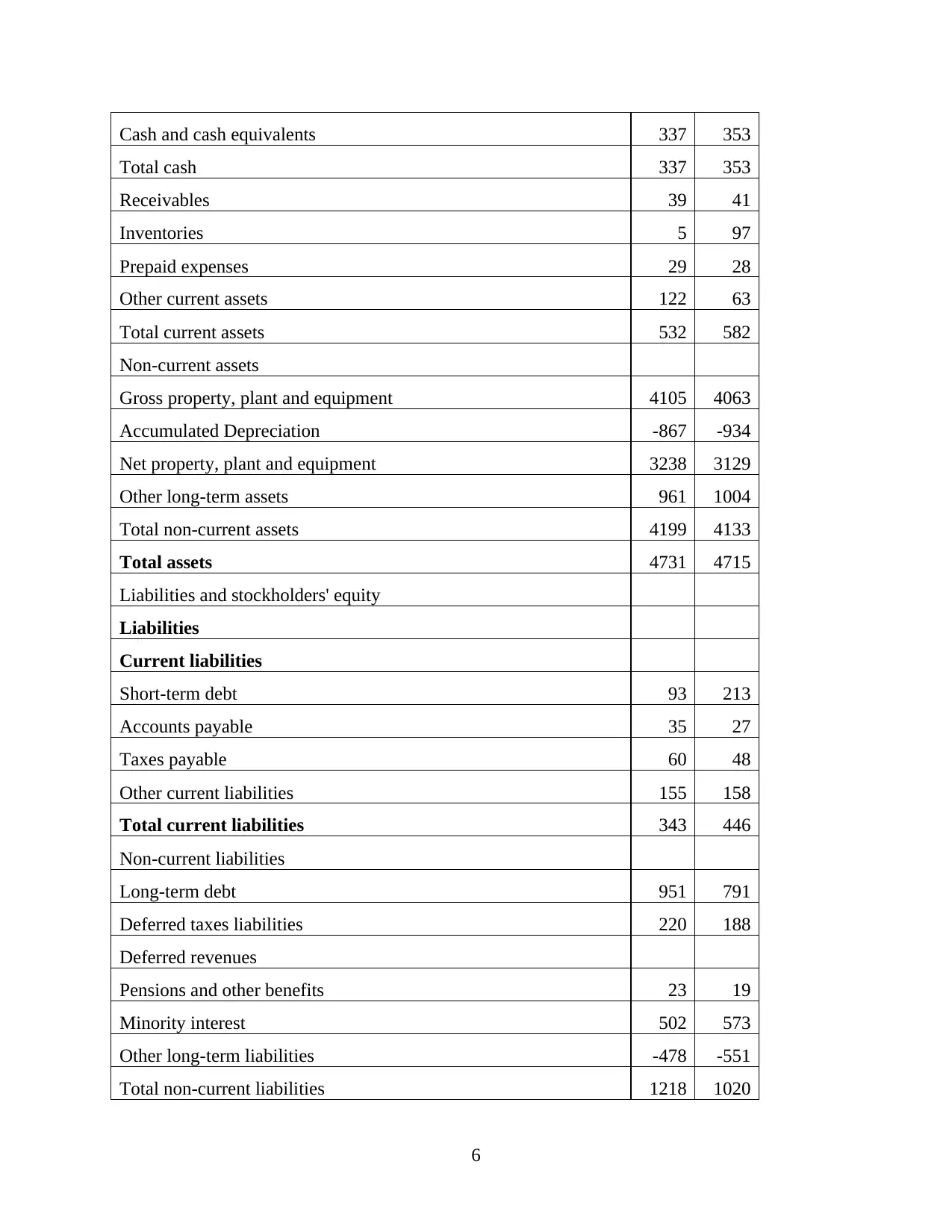

Cash and cash equivalents 337 353

Total cash 337 353

Receivables 39 41

Inventories 5 97

Prepaid expenses 29 28

Other current assets 122 63

Total current assets 532 582

Non-current assets

Gross property, plant and equipment 4105 4063

Accumulated Depreciation -867 -934

Net property, plant and equipment 3238 3129

Other long-term assets 961 1004

Total non-current assets 4199 4133

Total assets 4731 4715

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 93 213

Accounts payable 35 27

Taxes payable 60 48

Other current liabilities 155 158

Total current liabilities 343 446

Non-current liabilities

Long-term debt 951 791

Deferred taxes liabilities 220 188

Deferred revenues

Pensions and other benefits 23 19

Minority interest 502 573

Other long-term liabilities -478 -551

Total non-current liabilities 1218 1020

6

Total cash 337 353

Receivables 39 41

Inventories 5 97

Prepaid expenses 29 28

Other current assets 122 63

Total current assets 532 582

Non-current assets

Gross property, plant and equipment 4105 4063

Accumulated Depreciation -867 -934

Net property, plant and equipment 3238 3129

Other long-term assets 961 1004

Total non-current assets 4199 4133

Total assets 4731 4715

Liabilities and stockholders' equity

Liabilities

Current liabilities

Short-term debt 93 213

Accounts payable 35 27

Taxes payable 60 48

Other current liabilities 155 158

Total current liabilities 343 446

Non-current liabilities

Long-term debt 951 791

Deferred taxes liabilities 220 188

Deferred revenues

Pensions and other benefits 23 19

Minority interest 502 573

Other long-term liabilities -478 -551

Total non-current liabilities 1218 1020

6

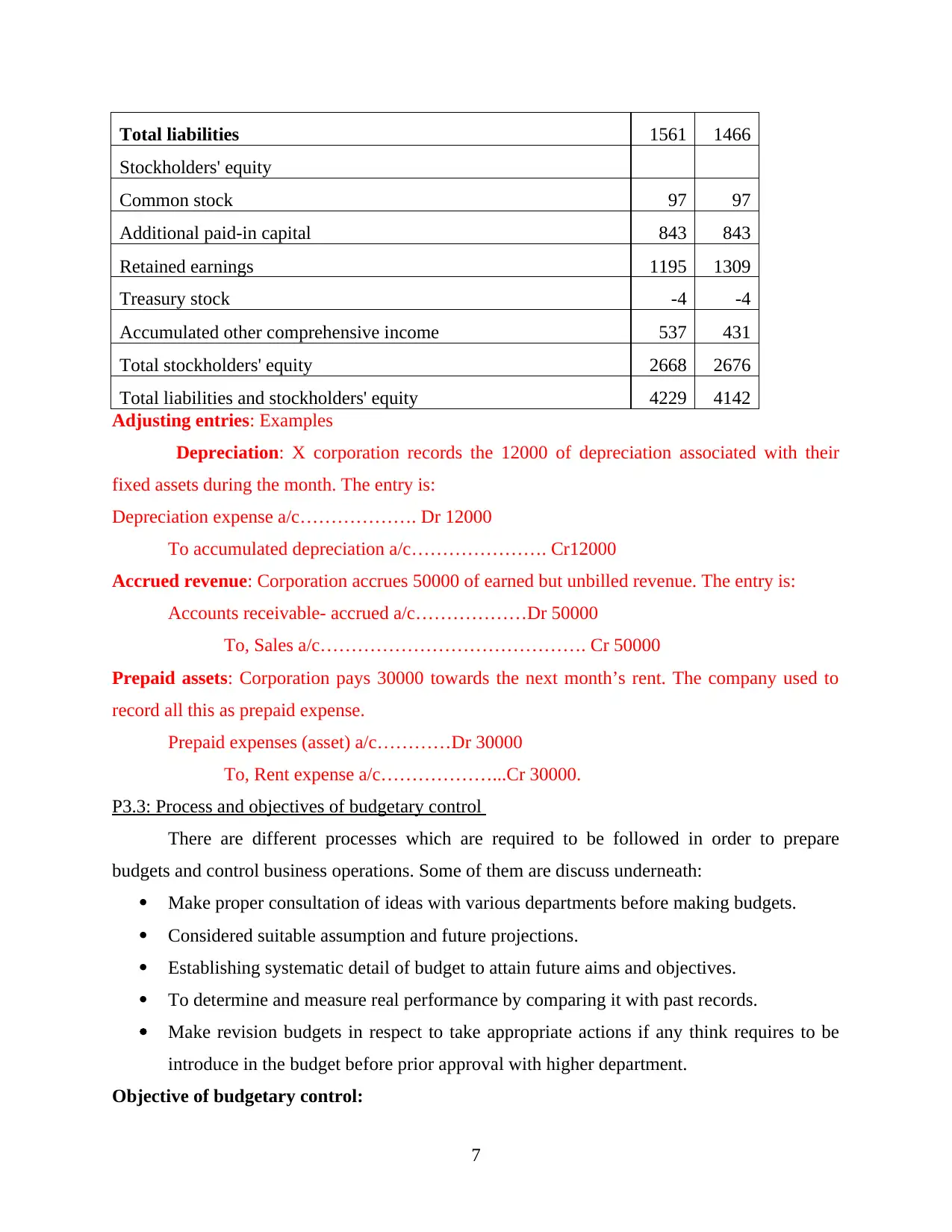

Total liabilities 1561 1466

Stockholders' equity

Common stock 97 97

Additional paid-in capital 843 843

Retained earnings 1195 1309

Treasury stock -4 -4

Accumulated other comprehensive income 537 431

Total stockholders' equity 2668 2676

Total liabilities and stockholders' equity 4229 4142

Adjusting entries: Examples

Depreciation: X corporation records the 12000 of depreciation associated with their

fixed assets during the month. The entry is:

Depreciation expense a/c………………. Dr 12000

To accumulated depreciation a/c…………………. Cr12000

Accrued revenue: Corporation accrues 50000 of earned but unbilled revenue. The entry is:

Accounts receivable- accrued a/c………………Dr 50000

To, Sales a/c……………………………………. Cr 50000

Prepaid assets: Corporation pays 30000 towards the next month’s rent. The company used to

record all this as prepaid expense.

Prepaid expenses (asset) a/c…………Dr 30000

To, Rent expense a/c………………...Cr 30000.

P3.3: Process and objectives of budgetary control

There are different processes which are required to be followed in order to prepare

budgets and control business operations. Some of them are discuss underneath:

Make proper consultation of ideas with various departments before making budgets.

Considered suitable assumption and future projections.

Establishing systematic detail of budget to attain future aims and objectives.

To determine and measure real performance by comparing it with past records.

Make revision budgets in respect to take appropriate actions if any think requires to be

introduce in the budget before prior approval with higher department.

Objective of budgetary control:

7

Stockholders' equity

Common stock 97 97

Additional paid-in capital 843 843

Retained earnings 1195 1309

Treasury stock -4 -4

Accumulated other comprehensive income 537 431

Total stockholders' equity 2668 2676

Total liabilities and stockholders' equity 4229 4142

Adjusting entries: Examples

Depreciation: X corporation records the 12000 of depreciation associated with their

fixed assets during the month. The entry is:

Depreciation expense a/c………………. Dr 12000

To accumulated depreciation a/c…………………. Cr12000

Accrued revenue: Corporation accrues 50000 of earned but unbilled revenue. The entry is:

Accounts receivable- accrued a/c………………Dr 50000

To, Sales a/c……………………………………. Cr 50000

Prepaid assets: Corporation pays 30000 towards the next month’s rent. The company used to

record all this as prepaid expense.

Prepaid expenses (asset) a/c…………Dr 30000

To, Rent expense a/c………………...Cr 30000.

P3.3: Process and objectives of budgetary control

There are different processes which are required to be followed in order to prepare

budgets and control business operations. Some of them are discuss underneath:

Make proper consultation of ideas with various departments before making budgets.

Considered suitable assumption and future projections.

Establishing systematic detail of budget to attain future aims and objectives.

To determine and measure real performance by comparing it with past records.

Make revision budgets in respect to take appropriate actions if any think requires to be

introduce in the budget before prior approval with higher department.

Objective of budgetary control:

7

There is certain essential motive to make use of budgetary control. Some of them are

discuss underneath:

Communication: It is vital to make enable budgets by communicating with other

department through effective planning or controlling systems (Varghese, 2013).

Accountant need to have clear understanding of all their part within Belgravia Hotels

aims. This is prepared with best possible by ensuring their overall participation in the

formulation of budgetary process.

Performance analysis: This is primary purpose of account officers to make use of

budgets in order to make analysis of their overall growth and performance of an

organisation. Overall variance is shown and corrective action can be taken into account.

budgets are also from the basis of performance evaluation in an organisation as they

reflect realistic aspects of acceptable and future performance within an hotel.

Co-ordination: It is an effective managerial functions within the hotel can analyse all the

factors of production and departmental activities and balanced to achieve the goals of an

organisation.

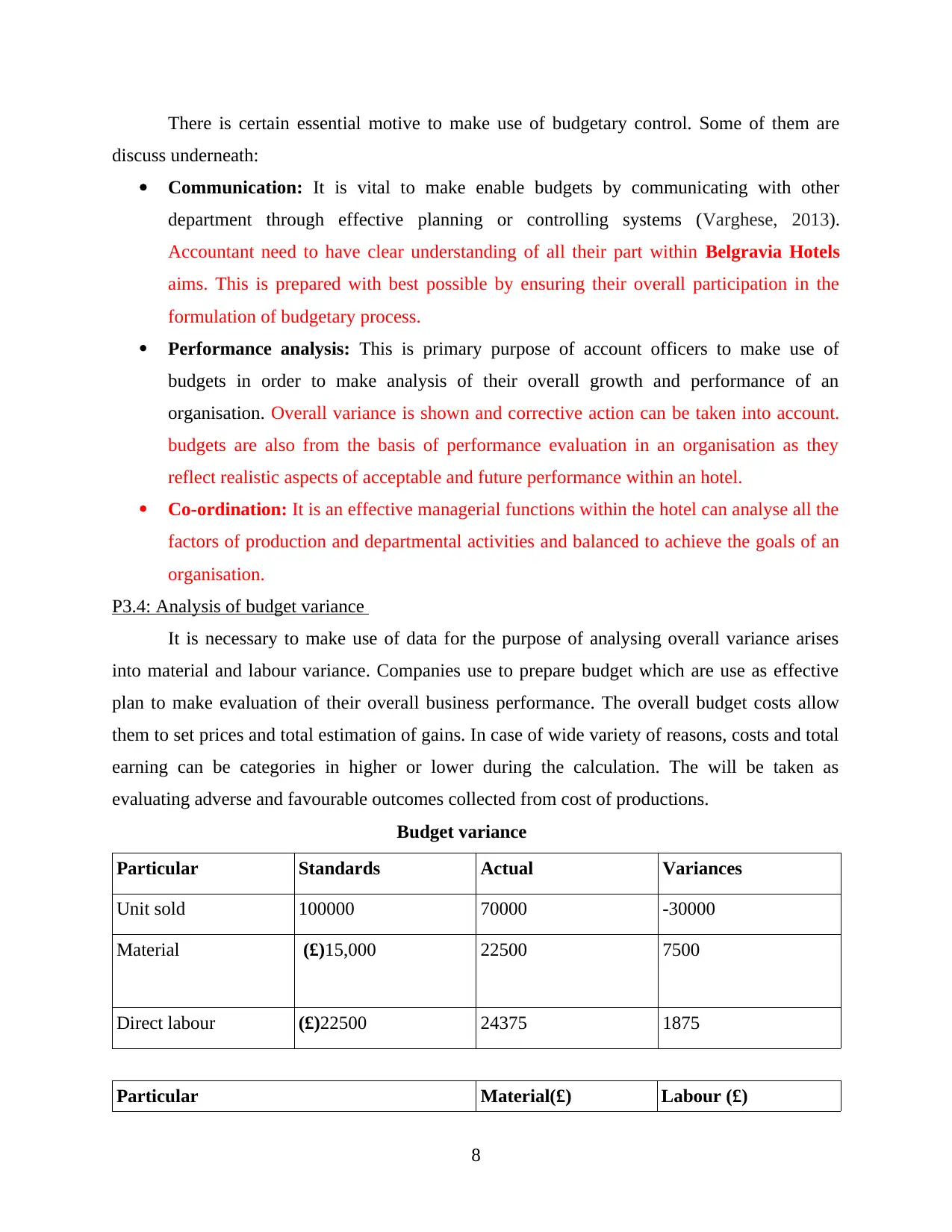

P3.4: Analysis of budget variance

It is necessary to make use of data for the purpose of analysing overall variance arises

into material and labour variance. Companies use to prepare budget which are use as effective

plan to make evaluation of their overall business performance. The overall budget costs allow

them to set prices and total estimation of gains. In case of wide variety of reasons, costs and total

earning can be categories in higher or lower during the calculation. The will be taken as

evaluating adverse and favourable outcomes collected from cost of productions.

Budget variance

Particular Standards Actual Variances

Unit sold 100000 70000 -30000

Material (£)15,000 22500 7500

Direct labour (£)22500 24375 1875

Particular Material(£) Labour (£)

8

discuss underneath:

Communication: It is vital to make enable budgets by communicating with other

department through effective planning or controlling systems (Varghese, 2013).

Accountant need to have clear understanding of all their part within Belgravia Hotels

aims. This is prepared with best possible by ensuring their overall participation in the

formulation of budgetary process.

Performance analysis: This is primary purpose of account officers to make use of

budgets in order to make analysis of their overall growth and performance of an

organisation. Overall variance is shown and corrective action can be taken into account.

budgets are also from the basis of performance evaluation in an organisation as they

reflect realistic aspects of acceptable and future performance within an hotel.

Co-ordination: It is an effective managerial functions within the hotel can analyse all the

factors of production and departmental activities and balanced to achieve the goals of an

organisation.

P3.4: Analysis of budget variance

It is necessary to make use of data for the purpose of analysing overall variance arises

into material and labour variance. Companies use to prepare budget which are use as effective

plan to make evaluation of their overall business performance. The overall budget costs allow

them to set prices and total estimation of gains. In case of wide variety of reasons, costs and total

earning can be categories in higher or lower during the calculation. The will be taken as

evaluating adverse and favourable outcomes collected from cost of productions.

Budget variance

Particular Standards Actual Variances

Unit sold 100000 70000 -30000

Material (£)15,000 22500 7500

Direct labour (£)22500 24375 1875

Particular Material(£) Labour (£)

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

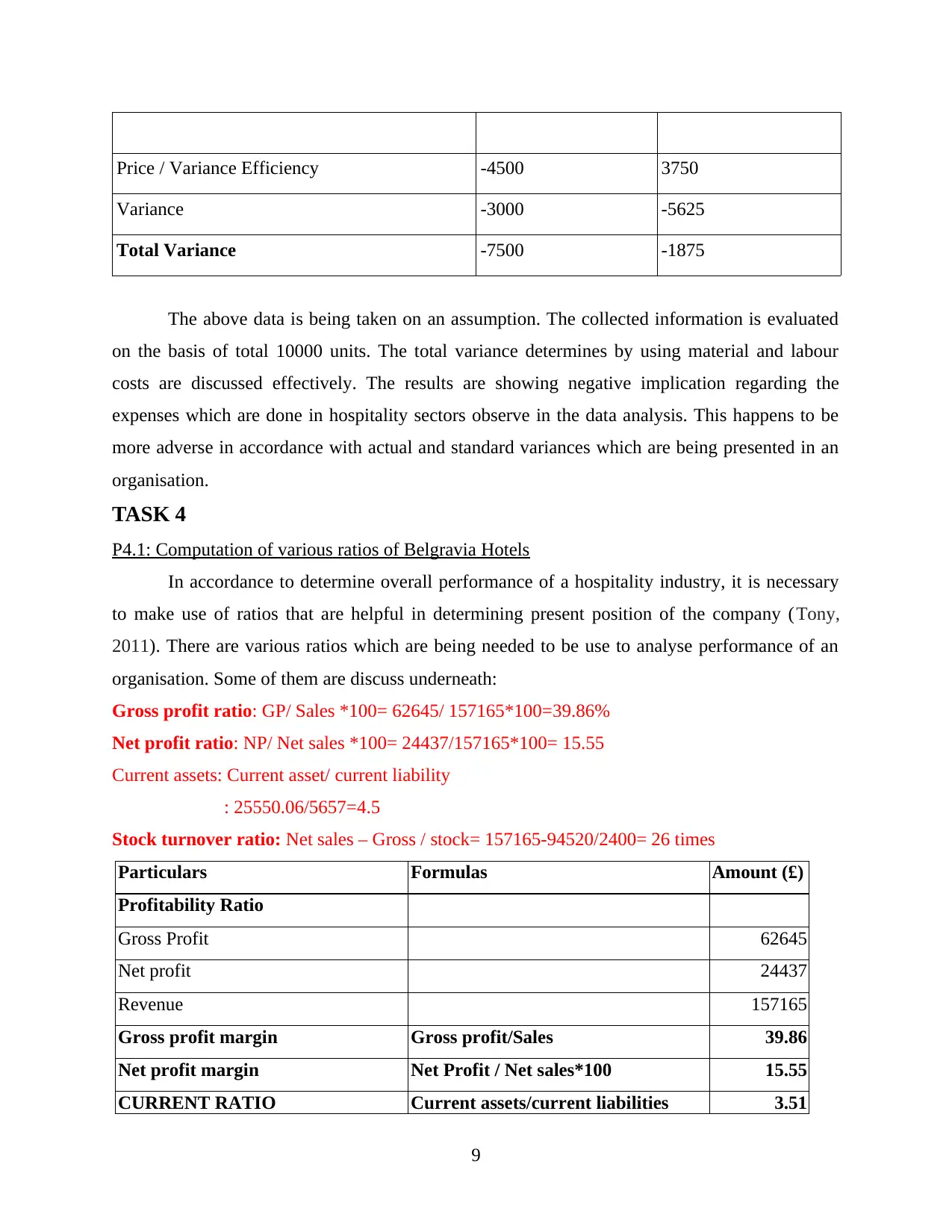

Price / Variance Efficiency -4500 3750

Variance -3000 -5625

Total Variance -7500 -1875

The above data is being taken on an assumption. The collected information is evaluated

on the basis of total 10000 units. The total variance determines by using material and labour

costs are discussed effectively. The results are showing negative implication regarding the

expenses which are done in hospitality sectors observe in the data analysis. This happens to be

more adverse in accordance with actual and standard variances which are being presented in an

organisation.

TASK 4

P4.1: Computation of various ratios of Belgravia Hotels

In accordance to determine overall performance of a hospitality industry, it is necessary

to make use of ratios that are helpful in determining present position of the company (Tony,

2011). There are various ratios which are being needed to be use to analyse performance of an

organisation. Some of them are discuss underneath:

Gross profit ratio: GP/ Sales *100= 62645/ 157165*100=39.86%

Net profit ratio: NP/ Net sales *100= 24437/157165*100= 15.55

Current assets: Current asset/ current liability

: 25550.06/5657=4.5

Stock turnover ratio: Net sales – Gross / stock= 157165-94520/2400= 26 times

Particulars Formulas Amount (£)

Profitability Ratio

Gross Profit 62645

Net profit 24437

Revenue 157165

Gross profit margin Gross profit/Sales 39.86

Net profit margin Net Profit / Net sales*100 15.55

CURRENT RATIO Current assets/current liabilities 3.51

9

Variance -3000 -5625

Total Variance -7500 -1875

The above data is being taken on an assumption. The collected information is evaluated

on the basis of total 10000 units. The total variance determines by using material and labour

costs are discussed effectively. The results are showing negative implication regarding the

expenses which are done in hospitality sectors observe in the data analysis. This happens to be

more adverse in accordance with actual and standard variances which are being presented in an

organisation.

TASK 4

P4.1: Computation of various ratios of Belgravia Hotels

In accordance to determine overall performance of a hospitality industry, it is necessary

to make use of ratios that are helpful in determining present position of the company (Tony,

2011). There are various ratios which are being needed to be use to analyse performance of an

organisation. Some of them are discuss underneath:

Gross profit ratio: GP/ Sales *100= 62645/ 157165*100=39.86%

Net profit ratio: NP/ Net sales *100= 24437/157165*100= 15.55

Current assets: Current asset/ current liability

: 25550.06/5657=4.5

Stock turnover ratio: Net sales – Gross / stock= 157165-94520/2400= 26 times

Particulars Formulas Amount (£)

Profitability Ratio

Gross Profit 62645

Net profit 24437

Revenue 157165

Gross profit margin Gross profit/Sales 39.86

Net profit margin Net Profit / Net sales*100 15.55

CURRENT RATIO Current assets/current liabilities 3.51

9

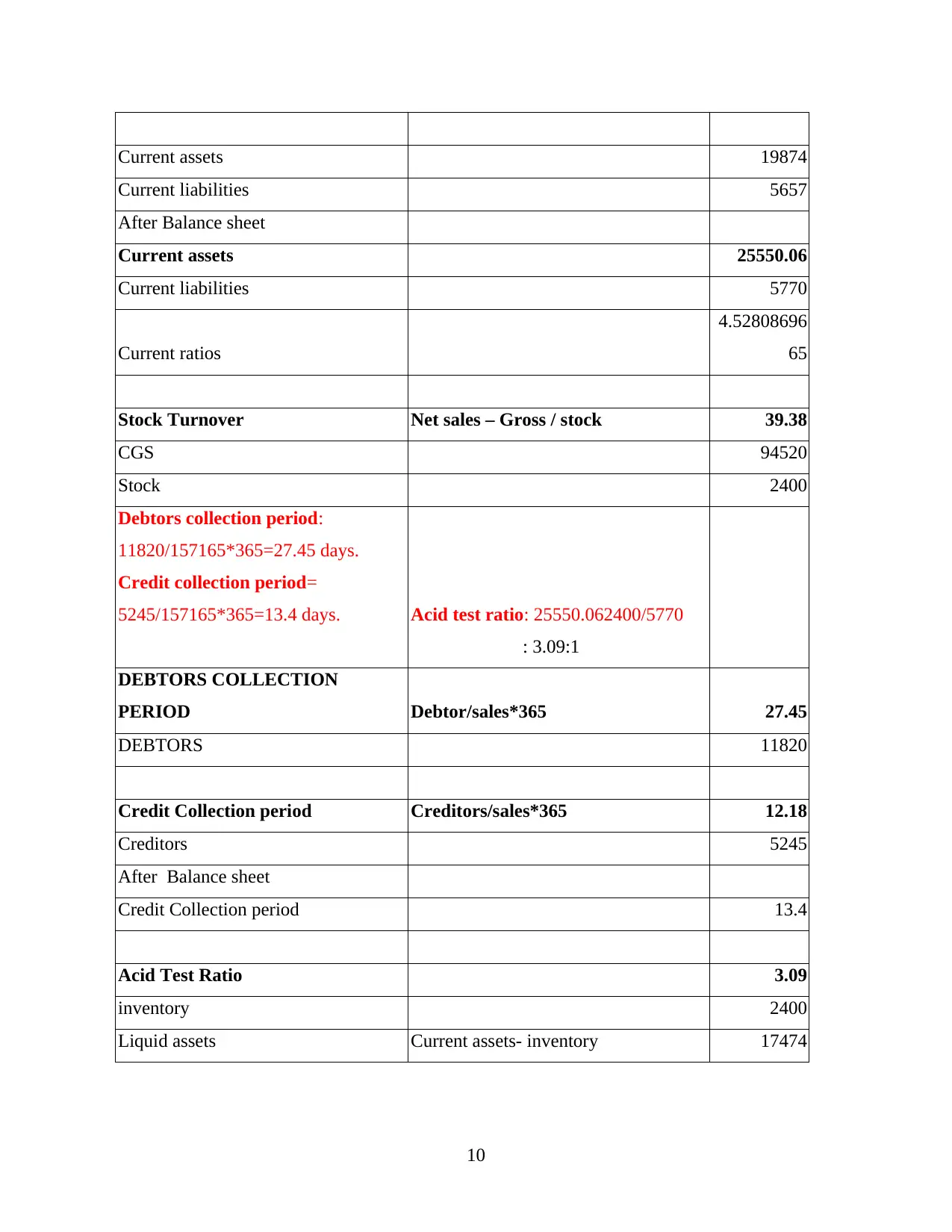

Current assets 19874

Current liabilities 5657

After Balance sheet

Current assets 25550.06

Current liabilities 5770

Current ratios

4.52808696

65

Stock Turnover Net sales – Gross / stock 39.38

CGS 94520

Stock 2400

Debtors collection period:

11820/157165*365=27.45 days.

Credit collection period=

5245/157165*365=13.4 days. Acid test ratio: 25550.062400/5770

: 3.09:1

DEBTORS COLLECTION

PERIOD Debtor/sales*365 27.45

DEBTORS 11820

Credit Collection period Creditors/sales*365 12.18

Creditors 5245

After Balance sheet

Credit Collection period 13.4

Acid Test Ratio 3.09

inventory 2400

Liquid assets Current assets- inventory 17474

10

Current liabilities 5657

After Balance sheet

Current assets 25550.06

Current liabilities 5770

Current ratios

4.52808696

65

Stock Turnover Net sales – Gross / stock 39.38

CGS 94520

Stock 2400

Debtors collection period:

11820/157165*365=27.45 days.

Credit collection period=

5245/157165*365=13.4 days. Acid test ratio: 25550.062400/5770

: 3.09:1

DEBTORS COLLECTION

PERIOD Debtor/sales*365 27.45

DEBTORS 11820

Credit Collection period Creditors/sales*365 12.18

Creditors 5245

After Balance sheet

Credit Collection period 13.4

Acid Test Ratio 3.09

inventory 2400

Liquid assets Current assets- inventory 17474

10

From the above calculation of ratios, it has been found that all the data would be taken on

an assumptions basis. The profitability position of the company is indicating more valuable net

profit margin of 15 %. Whereas the overall liquidity position is also more sufficient amount to

meet out their short-term and long term cash requirement. The hospitality sectors are growing

with faster rate and in order to go with the current trend they need to make of data in more

effective manner. On the basis of the liquidity position of Belgravia Hotels is much more

effective as they are having sufficient amount of capital to make further investment in various

projects of the company. Current ratio is 4.5 which is very much high from the ideal ratio of 2:1.

Similarly, acid test ratio is 3.09. The profitability position of the hotel is also very much

attractive which will assist them to make further planning in near future time.

P4.2: Recommendation for future management strategies to improve performance

By the use of effective ratios, an organisation can make use of their current position in

accordance with other company. The strategies planning is more helpful in evaluating overall

growth and positions. In fact, Hospitality Company can gain competitive benefits by

implementing resources in more reliable manner. From the above computed ratios, this has been

done to determine overall growth and potential of Belgravia Hotels in accordance with other

company (Guerrier, 2013). The growth rate of this hotel is increasing at faster rate. According to

the results, total investment in their projects would be increase shareholder values in coming

time.

The company is having sufficient amount of cash and net earnings which can helpful in

generating maximum return in near future. The gross profit margin is 39.86% which is collected

from total sales done from providing rooms and other facilities to their guest. In accordance to

evaluating net profit for the company is generating a total profit of 15% during the time. In case

of liquidity position, they are having current ratio of 3.5 which is much higher as compare to

ideal ratio. Whereas acid test ratio is delivering positive outcomes to the managers. This will

assist in better planning which would be further helpful in improving performance of an

organisation.

TASK 5

P5.1: Categories cost of components

There are various types of cost those are directly or indirectly related with production of

products and services. Cost is the value of money which is incur to get something. In other

11

an assumptions basis. The profitability position of the company is indicating more valuable net

profit margin of 15 %. Whereas the overall liquidity position is also more sufficient amount to

meet out their short-term and long term cash requirement. The hospitality sectors are growing

with faster rate and in order to go with the current trend they need to make of data in more

effective manner. On the basis of the liquidity position of Belgravia Hotels is much more

effective as they are having sufficient amount of capital to make further investment in various

projects of the company. Current ratio is 4.5 which is very much high from the ideal ratio of 2:1.

Similarly, acid test ratio is 3.09. The profitability position of the hotel is also very much

attractive which will assist them to make further planning in near future time.

P4.2: Recommendation for future management strategies to improve performance

By the use of effective ratios, an organisation can make use of their current position in

accordance with other company. The strategies planning is more helpful in evaluating overall

growth and positions. In fact, Hospitality Company can gain competitive benefits by

implementing resources in more reliable manner. From the above computed ratios, this has been

done to determine overall growth and potential of Belgravia Hotels in accordance with other

company (Guerrier, 2013). The growth rate of this hotel is increasing at faster rate. According to

the results, total investment in their projects would be increase shareholder values in coming

time.

The company is having sufficient amount of cash and net earnings which can helpful in

generating maximum return in near future. The gross profit margin is 39.86% which is collected

from total sales done from providing rooms and other facilities to their guest. In accordance to

evaluating net profit for the company is generating a total profit of 15% during the time. In case

of liquidity position, they are having current ratio of 3.5 which is much higher as compare to

ideal ratio. Whereas acid test ratio is delivering positive outcomes to the managers. This will

assist in better planning which would be further helpful in improving performance of an

organisation.

TASK 5

P5.1: Categories cost of components

There are various types of cost those are directly or indirectly related with production of

products and services. Cost is the value of money which is incur to get something. In other

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

situation, it has been categories into various parts. This will increase extra cost for the company

is more separated by using various aspects such as raw material, overhead and other external

activities. Some of them are discuss underneath:

Variable cost: It refers to the costs which can changes with the production of one

additional unit. It varies with the increase of decrease in total quantity of production

level. Some of them are direct material and labour costs (Variable Costs, 2018).

Fixed cost: This would remain unchanged with the production of any extra costs. This

cannot get dis-balanced with increase or decrease in production costs. The project

managers need to make payment of these types of costs. Some crucial examples are,

office rent, taxes and insurances etc (Schneider and dos Santos, 2013).

Semi-variable: These are said to be combination of both fixed and variable costs that are

being charged during providing accommodation facilities to their guest. This will assist in

determining overall image of the company. Examples, Power and fuel expenses.

P5.2: Calculation of Contribution per units

Total number of people: 80

Normal charges= £25

Sales: 85*25=2125

Variable cost= 85*£15.50= 1317.5

Total contribution: Sales – Variable cost

: 2125-1317.5=807.5

Margin of safety = 807.5-380/2125*100

= 427.5/2125=20.11%

In case of 100 people there would be increasing charges for ticket prices.

Sales= 100*22= 2200

Variable cost: 1550

Total contribution: Sales- Variable cost

: 2200-1550= 650

Margin of safety: 650-380/2200=12.27%

Relationship among cost volume and profit:

It is one of the effective analysis which is been used by management of Belgravia Hotels to

assist better understanding of relationship among relationships between cost, sale volume and

12

is more separated by using various aspects such as raw material, overhead and other external

activities. Some of them are discuss underneath:

Variable cost: It refers to the costs which can changes with the production of one

additional unit. It varies with the increase of decrease in total quantity of production

level. Some of them are direct material and labour costs (Variable Costs, 2018).

Fixed cost: This would remain unchanged with the production of any extra costs. This

cannot get dis-balanced with increase or decrease in production costs. The project

managers need to make payment of these types of costs. Some crucial examples are,

office rent, taxes and insurances etc (Schneider and dos Santos, 2013).

Semi-variable: These are said to be combination of both fixed and variable costs that are

being charged during providing accommodation facilities to their guest. This will assist in

determining overall image of the company. Examples, Power and fuel expenses.

P5.2: Calculation of Contribution per units

Total number of people: 80

Normal charges= £25

Sales: 85*25=2125

Variable cost= 85*£15.50= 1317.5

Total contribution: Sales – Variable cost

: 2125-1317.5=807.5

Margin of safety = 807.5-380/2125*100

= 427.5/2125=20.11%

In case of 100 people there would be increasing charges for ticket prices.

Sales= 100*22= 2200

Variable cost: 1550

Total contribution: Sales- Variable cost

: 2200-1550= 650

Margin of safety: 650-380/2200=12.27%

Relationship among cost volume and profit:

It is one of the effective analysis which is been used by management of Belgravia Hotels to

assist better understanding of relationship among relationships between cost, sale volume and

12

profit. This particular technique used to target on overall selling prices, volume and variable cost

and the mix of product and services that are delivered to the customers can directly affect the

profitability. The contribution margin ratio divided by sales, tells management about total much

of every dollar is going to contribute to cover fixed expense up until the breakeven. Total sales

contribution with the total number of 80 people they can earn contribution of 807.5. while, with

the increase in number of people as 100, total contribution is about 650.

P5.3: Importance of BEP

Break even point is considered as sales value at which business reaches the situation of

no profit and loss. Through calculation of this point large number of importance are gathered by

organisation which is mentioned below:

It helps in understanding the relationship between cost-volume-profit. It helps to attain

better results.

Understanding such relationship helps the organisation to take better business decisions

regarding buying and selling of different things.

This will provide the opportunity to the management of organisation is to formulate

business plans which help in achievement of particular results.

It is difficult to achieve the business tasks but achievement of the BEP helps in

accomplishment of business objectives.

Monitoring of BEP and Margin of safety helps to ascertain about the viability of

business.

Use of BEP analysis: It is more effective aspects for a good business plan, since it will assist

business to determine the cost structure and overall number of units those are required to be sold

in order to make short term decision. The key is to work out the overall contribution from the

sale of each unit. The value of money with each unit sold must contribute to the fixed and

indirect cost of the business.

CONCLUSION

From the above project report, it has been concluded that finance is utmost important

aspects which are needed to be manage in more systematic manner. In order to attain better

management of an organisation, it is essential to make proper use of resources in more effective

manner. For this purpose, various sources of finance would be available for hospitality industry

13

and the mix of product and services that are delivered to the customers can directly affect the

profitability. The contribution margin ratio divided by sales, tells management about total much

of every dollar is going to contribute to cover fixed expense up until the breakeven. Total sales

contribution with the total number of 80 people they can earn contribution of 807.5. while, with

the increase in number of people as 100, total contribution is about 650.

P5.3: Importance of BEP

Break even point is considered as sales value at which business reaches the situation of

no profit and loss. Through calculation of this point large number of importance are gathered by

organisation which is mentioned below:

It helps in understanding the relationship between cost-volume-profit. It helps to attain

better results.

Understanding such relationship helps the organisation to take better business decisions

regarding buying and selling of different things.

This will provide the opportunity to the management of organisation is to formulate

business plans which help in achievement of particular results.

It is difficult to achieve the business tasks but achievement of the BEP helps in

accomplishment of business objectives.

Monitoring of BEP and Margin of safety helps to ascertain about the viability of

business.

Use of BEP analysis: It is more effective aspects for a good business plan, since it will assist

business to determine the cost structure and overall number of units those are required to be sold

in order to make short term decision. The key is to work out the overall contribution from the

sale of each unit. The value of money with each unit sold must contribute to the fixed and

indirect cost of the business.

CONCLUSION

From the above project report, it has been concluded that finance is utmost important

aspects which are needed to be manage in more systematic manner. In order to attain better

management of an organisation, it is essential to make proper use of resources in more effective

manner. For this purpose, various sources of finance would be available for hospitality industry

13

that can help in increasing goodwill of the company. The use of BEP would increase overall

growth and performance in order to attain short-term objectives for an organisation.

14

growth and performance in order to attain short-term objectives for an organisation.

14

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.