Financial Analysis of Hospitality Businesses: A Detailed Report

VerifiedAdded on 2020/10/22

|14

|3414

|470

Report

AI Summary

This report offers a comprehensive financial analysis tailored to the hospitality industry. It begins by exploring various sources of finance, including short-term options like bank overdrafts and accounts receivable financing, and long-term options such as equity financing and retained earnings. The report then delves into income generation methods, including fee-for-service, product and service sales, and investment dividends. It discusses key cost elements like direct and indirect materials, labor, and overheads, as well as gross profit percentage calculations. The report also evaluates cash and stock control systems, emphasizing the importance of setting cash flow limits and employing stock control techniques like inventory turnover ratios and ABC costing. A trial balance is presented and assessed. The report concludes with an analysis of financial ratios, a recommendation of future management strategies, and a discussion of cost categorization and contribution per unit, all aimed at improving financial management within the hospitality sector.

FINANCE IN HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Reviewing the sources of finance available to business..................................................1

1.2: Various forms of income generation methods................................................................3

TASK 2............................................................................................................................................3

2.1: Discuss Elements of cost, gross profit percentage and selling price...............................3

2.2: Evaluate methods cash and stock control system............................................................4

TASK 3............................................................................................................................................5

3.1: Assess the source and structure of trial balance..............................................................5

3.2: Evaluate the business accounts and adjustments.............................................................6

3.3: Process and purpose behind preparation of budgetary control.......................................7

3.4: Analysing variances from budget and actual figures......................................................8

TASK 4............................................................................................................................................9

4.1: Calculating various ratios of the given companies..........................................................9

4.2: Recommend future management strategies ..................................................................10

TASK 5..........................................................................................................................................10

5.1: Formulate categories as Fixed, variable and semi-variable .........................................10

5.2: Calculation of contribution per unit..............................................................................11

5.3: Justify Short-term management decision......................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1: Reviewing the sources of finance available to business..................................................1

1.2: Various forms of income generation methods................................................................3

TASK 2............................................................................................................................................3

2.1: Discuss Elements of cost, gross profit percentage and selling price...............................3

2.2: Evaluate methods cash and stock control system............................................................4

TASK 3............................................................................................................................................5

3.1: Assess the source and structure of trial balance..............................................................5

3.2: Evaluate the business accounts and adjustments.............................................................6

3.3: Process and purpose behind preparation of budgetary control.......................................7

3.4: Analysing variances from budget and actual figures......................................................8

TASK 4............................................................................................................................................9

4.1: Calculating various ratios of the given companies..........................................................9

4.2: Recommend future management strategies ..................................................................10

TASK 5..........................................................................................................................................10

5.1: Formulate categories as Fixed, variable and semi-variable .........................................10

5.2: Calculation of contribution per unit..............................................................................11

5.3: Justify Short-term management decision......................................................................11

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION

Finance is the lifeblood of every business whether it is hospitality or any other industry,

without finance it is Impossible for the businesses to operate in the market successfully.

Procuring finance for the business is one of the most essential and critical task of the managers.

Because of the existence of the complexities in the business , financial models are evolved for

achieving the common objectives of the organisation. Therefore it is a great opportunity for the

managers for introduction of individual jobs and the reasons that has motivated them to select the

right path for attainment of objectives in business. This will assists the accounting managers in

understanding the techniques of accounting in hospitality sector such that more enhanced results

can be generated in given time period( Yuan, Li, and Zeng, 2018).

The motive behind the analysis is to formulate financing decisions in the hospitality

industry so as to improve the effectiveness of financial management. This project will perform

an evaluation about the various sources that are available for the purpose of funding and the

techniques that are available for income generation. Understanding the elements of cost and

systems are discussed under the report.

TASK 1

1.1: Reviewing the sources of finance available to business

There are various sources of funding that are available for the “Trident group” from

where they can manage the funds for the operations of business. The sources of funds are

broadly divided in two categories namely Long term sources and short term sources, these are

discussed in brief as under:

Short term Finance:

This is a source of finance which the company undertakes so as to get the additional

funds for the regular operation of the business. The short term finance is available for one

accounting year and the company has to repay the amount in that particular time. Some of the

basic components of short term finance include:

Bank overdraft: This facility is provided by the banks to the current account holders ,

under this the bank will allow the business to withdraw the amount up to certain limit.

Under the bank overdraft the account holder is allowed to withdraw the extra amount

from the bank then the existing balance in his account. Under this method, the bank may

1

Finance is the lifeblood of every business whether it is hospitality or any other industry,

without finance it is Impossible for the businesses to operate in the market successfully.

Procuring finance for the business is one of the most essential and critical task of the managers.

Because of the existence of the complexities in the business , financial models are evolved for

achieving the common objectives of the organisation. Therefore it is a great opportunity for the

managers for introduction of individual jobs and the reasons that has motivated them to select the

right path for attainment of objectives in business. This will assists the accounting managers in

understanding the techniques of accounting in hospitality sector such that more enhanced results

can be generated in given time period( Yuan, Li, and Zeng, 2018).

The motive behind the analysis is to formulate financing decisions in the hospitality

industry so as to improve the effectiveness of financial management. This project will perform

an evaluation about the various sources that are available for the purpose of funding and the

techniques that are available for income generation. Understanding the elements of cost and

systems are discussed under the report.

TASK 1

1.1: Reviewing the sources of finance available to business

There are various sources of funding that are available for the “Trident group” from

where they can manage the funds for the operations of business. The sources of funds are

broadly divided in two categories namely Long term sources and short term sources, these are

discussed in brief as under:

Short term Finance:

This is a source of finance which the company undertakes so as to get the additional

funds for the regular operation of the business. The short term finance is available for one

accounting year and the company has to repay the amount in that particular time. Some of the

basic components of short term finance include:

Bank overdraft: This facility is provided by the banks to the current account holders ,

under this the bank will allow the business to withdraw the amount up to certain limit.

Under the bank overdraft the account holder is allowed to withdraw the extra amount

from the bank then the existing balance in his account. Under this method, the bank may

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

also require the business to put some collateral and they charge a certain fixed interest on

the extra amount withdrawn for each day until the amount is repaid.

Accounts receivable financing: Many of the commercial banks and other small financial

institution provide the facility of discounting the invoice. Under this method the

business , transfers their commercial bills to the banks, against which the bank makes the

payment by deducting a small fee. And when the due date occurs the bank collects the

payment from the customer. This is considered as one of the most famous short term

financing generally among the small traders.

Customer advances: There are various companies that have a good brand image, which

insists the customers to make the advance payments before selling or providing goods

and services to them. This technique is applicable on the large orders which require a

long time to accomplish. This provides the business the funds for the operations that will

be required to execute those orders.

Long term Finance:

Long term loans from banks: The businesses which have surety regarding their

earnings in the future or the companies who are confident about the consistency of the

profits in the business, are generally the ones who opt for loans from bank as they are

cheaper then equity but the interest payments are required to be consistent whether there

is profit or loss( Tsai, Pan, and Lee, 2011).

Equity Financing: When the companies operate on large scale, they generally require a

source of funding which provides them a large amount of money. Under this the

companies issue shares to the general public and those who buys the shares become the

shareholders and the company is required to pay dividends to them.

Retained earnings: Retained earnings are those part of the profits which the company

retains after distributing the profits of the company to shareholders. Sometimes the

company uses these retained profits to fund the activities of the business.

Venture Funding: This is also a good source of funding which the businesses can opt in

the early stages of their operations. The venture funding is provided by financial

institutions to the company in the early stage and then they withdraw after the company

has developed to a certain position.

2

the extra amount withdrawn for each day until the amount is repaid.

Accounts receivable financing: Many of the commercial banks and other small financial

institution provide the facility of discounting the invoice. Under this method the

business , transfers their commercial bills to the banks, against which the bank makes the

payment by deducting a small fee. And when the due date occurs the bank collects the

payment from the customer. This is considered as one of the most famous short term

financing generally among the small traders.

Customer advances: There are various companies that have a good brand image, which

insists the customers to make the advance payments before selling or providing goods

and services to them. This technique is applicable on the large orders which require a

long time to accomplish. This provides the business the funds for the operations that will

be required to execute those orders.

Long term Finance:

Long term loans from banks: The businesses which have surety regarding their

earnings in the future or the companies who are confident about the consistency of the

profits in the business, are generally the ones who opt for loans from bank as they are

cheaper then equity but the interest payments are required to be consistent whether there

is profit or loss( Tsai, Pan, and Lee, 2011).

Equity Financing: When the companies operate on large scale, they generally require a

source of funding which provides them a large amount of money. Under this the

companies issue shares to the general public and those who buys the shares become the

shareholders and the company is required to pay dividends to them.

Retained earnings: Retained earnings are those part of the profits which the company

retains after distributing the profits of the company to shareholders. Sometimes the

company uses these retained profits to fund the activities of the business.

Venture Funding: This is also a good source of funding which the businesses can opt in

the early stages of their operations. The venture funding is provided by financial

institutions to the company in the early stage and then they withdraw after the company

has developed to a certain position.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.2: Various forms of income generation methods

The companies have different methods from where they can generate the income for

sustaining the operations of the business. At a certain point of time the company can undertake

any combination of these techniques and utilise them which is crucial kind of planning related to

business. These are discussed as under:

Fee-for-service: This is a form of charging component for the business where they

charge customers for the social services so as to recover the cost of service provisions(

Sisson, and Adams, 2012).

Products and Services: Under this income generation method, the income is earned by

manufacturing and sales of product or by re-sailing the products or through mark-up.

The income generation through providing services include merchandising the skill set of

a person or providing expertise to the market who is willing and able to pay.

Investment Dividend: The Income that is generated by the business with help of the

Investment done by the company are best for the purpose of funding the operations of

business. Under this interest or dividend received from the investment done by the

company are included.

TASK 2

2.1: Discuss Elements of cost, gross profit percentage and selling price

The Cost is the approximation regarding the amount which the company has to pay for

the total capital that is acquired by the business and in the production of the products and

services. Some of these elements are quite significant for improving the operations and

productivity of the business:

Direct material: These are those costs that are related to the to the manufacturing and

production department of the company. The cost related to the production department vary with

the output level that the company is producing. Primarily enclosing material and half developed

products are the examples related to direct material(Paster, 2013).

Indirect material: These are considered as those material which is used in the

production process as the secondary tool for easing the handling of the physical units. The

examples of these includes oil and waste and stationary products.

3

The companies have different methods from where they can generate the income for

sustaining the operations of the business. At a certain point of time the company can undertake

any combination of these techniques and utilise them which is crucial kind of planning related to

business. These are discussed as under:

Fee-for-service: This is a form of charging component for the business where they

charge customers for the social services so as to recover the cost of service provisions(

Sisson, and Adams, 2012).

Products and Services: Under this income generation method, the income is earned by

manufacturing and sales of product or by re-sailing the products or through mark-up.

The income generation through providing services include merchandising the skill set of

a person or providing expertise to the market who is willing and able to pay.

Investment Dividend: The Income that is generated by the business with help of the

Investment done by the company are best for the purpose of funding the operations of

business. Under this interest or dividend received from the investment done by the

company are included.

TASK 2

2.1: Discuss Elements of cost, gross profit percentage and selling price

The Cost is the approximation regarding the amount which the company has to pay for

the total capital that is acquired by the business and in the production of the products and

services. Some of these elements are quite significant for improving the operations and

productivity of the business:

Direct material: These are those costs that are related to the to the manufacturing and

production department of the company. The cost related to the production department vary with

the output level that the company is producing. Primarily enclosing material and half developed

products are the examples related to direct material(Paster, 2013).

Indirect material: These are considered as those material which is used in the

production process as the secondary tool for easing the handling of the physical units. The

examples of these includes oil and waste and stationary products.

3

Direct labour: The direct labour constitutes that employees who are involved in the

production and manufacturing process relates to goods and services of company. This is called as

direct as this impacts the cost of goods and services directly( Lupton, 2013).

Indirect labour: The indirect labour are those employees and workers which do not

impact the cost of goods and services directly or that labour which is not engaged in the

production process. The indirect labour are that employees which are involved in activities such

as selling and administration which impacts the cost indirectly.

Expenses: This refers to the cost which is incurred during the operations and production

activities of the business. The expenses of the company are are further classified into two broad

categories namely Direct expenses and Indirect expenses.

Overheads: The overheads of the company are also the combination of variable and

fixed costs. The overheads of the company are related to factory, office, selling and distributions.

Gross profit percentage: The gross profit percentage of the company is calculated as

gross profit that is made by the company divided by the total revenues made by company during

a year. The basis for calculating the gross profit is the net revenue of the company it is done as

under:

GPP(Gross profit percentage) : Gross profit / Total sales* 100

Selling price + COGS+ Gross profit= This has been observed that net profits of the

company are calculated by deducting the other overheads from gross profit margin. Firstly , the

company prepares the trading account for the determination of gross profit and then calculates

the net profit by preparing income statement.

2.2: Evaluate methods cash and stock control system

This is significant for the companies in hospitality sector such as Oberoi group to

determine the operation of the company in much efficient manner. According to which it is

necessary to maintain the cash and stock as these are major elements of workigncapital of the

company( Liu, 2012).

Cash Control methods:

Set cash flow limits: The companies should set a standard limit on spending of cash and

managers should regularly forecast the cash balances.

Making payment getaway more simplified: the managers recommend and focuses on

removing the payment options through cheque as it requires time to encash.

4

production and manufacturing process relates to goods and services of company. This is called as

direct as this impacts the cost of goods and services directly( Lupton, 2013).

Indirect labour: The indirect labour are those employees and workers which do not

impact the cost of goods and services directly or that labour which is not engaged in the

production process. The indirect labour are that employees which are involved in activities such

as selling and administration which impacts the cost indirectly.

Expenses: This refers to the cost which is incurred during the operations and production

activities of the business. The expenses of the company are are further classified into two broad

categories namely Direct expenses and Indirect expenses.

Overheads: The overheads of the company are also the combination of variable and

fixed costs. The overheads of the company are related to factory, office, selling and distributions.

Gross profit percentage: The gross profit percentage of the company is calculated as

gross profit that is made by the company divided by the total revenues made by company during

a year. The basis for calculating the gross profit is the net revenue of the company it is done as

under:

GPP(Gross profit percentage) : Gross profit / Total sales* 100

Selling price + COGS+ Gross profit= This has been observed that net profits of the

company are calculated by deducting the other overheads from gross profit margin. Firstly , the

company prepares the trading account for the determination of gross profit and then calculates

the net profit by preparing income statement.

2.2: Evaluate methods cash and stock control system

This is significant for the companies in hospitality sector such as Oberoi group to

determine the operation of the company in much efficient manner. According to which it is

necessary to maintain the cash and stock as these are major elements of workigncapital of the

company( Liu, 2012).

Cash Control methods:

Set cash flow limits: The companies should set a standard limit on spending of cash and

managers should regularly forecast the cash balances.

Making payment getaway more simplified: the managers recommend and focuses on

removing the payment options through cheque as it requires time to encash.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Provide healthy package to guest: By using a fixed package rates the companies in

hospitality sectors would assists in controlling cash transactions from extra flows.

Stock control techniques:

Identification of annual policies related to inventories: This will assist the company

for the analysis of maximum and minimum levels of inventory which has to be kept in

storehouses. There are different techniques such as LIFO, FIFO which assists the

managers in the examination of inventory level of the company.

Inventory turnover ratio: this refers to the sum total of time which the company

requires to sell the goods in the inventory. It is calculated as cost of goods sold divided

by the Average inventory of the company.

ABC costing: This technique of inventory management assists the managers in

dividing the total stock of the company according to the durability of the goods.

TASK 3

3.1: Assess the source and structure of trial balance

Trial balance of the company is prepared using the journal book and ledger of the

company. The preparation of trial balance is the first step in the preparation of financial accounts

of the business. The managers of the Oberoi group makes use of the trial balance to initiate the

preparation of income statement as per the dates specified in the company. In the preparation of

trial balance the accountant must ensure that credit balances and debit balances are matched in

the accounts. Each transaction is posted firstly in trial balance and then it goes to financial

statements which guides the accountants in rectifying the errors in financial statements that are

daunting the activities of the company( Kapiki, 2011).

Particulars L/F Debit Amount

(in £)

Credit Amount

(in £)

Opening Stock

Purchases

Salaries

Wages

Carriage Inwards

Trading Charges

–

–

–

–

–

–

86,000

1,136,000

110,000

61,000

26,900

64,000

5

hospitality sectors would assists in controlling cash transactions from extra flows.

Stock control techniques:

Identification of annual policies related to inventories: This will assist the company

for the analysis of maximum and minimum levels of inventory which has to be kept in

storehouses. There are different techniques such as LIFO, FIFO which assists the

managers in the examination of inventory level of the company.

Inventory turnover ratio: this refers to the sum total of time which the company

requires to sell the goods in the inventory. It is calculated as cost of goods sold divided

by the Average inventory of the company.

ABC costing: This technique of inventory management assists the managers in

dividing the total stock of the company according to the durability of the goods.

TASK 3

3.1: Assess the source and structure of trial balance

Trial balance of the company is prepared using the journal book and ledger of the

company. The preparation of trial balance is the first step in the preparation of financial accounts

of the business. The managers of the Oberoi group makes use of the trial balance to initiate the

preparation of income statement as per the dates specified in the company. In the preparation of

trial balance the accountant must ensure that credit balances and debit balances are matched in

the accounts. Each transaction is posted firstly in trial balance and then it goes to financial

statements which guides the accountants in rectifying the errors in financial statements that are

daunting the activities of the company( Kapiki, 2011).

Particulars L/F Debit Amount

(in £)

Credit Amount

(in £)

Opening Stock

Purchases

Salaries

Wages

Carriage Inwards

Trading Charges

–

–

–

–

–

–

86,000

1,136,000

110,000

61,000

26,900

64,000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

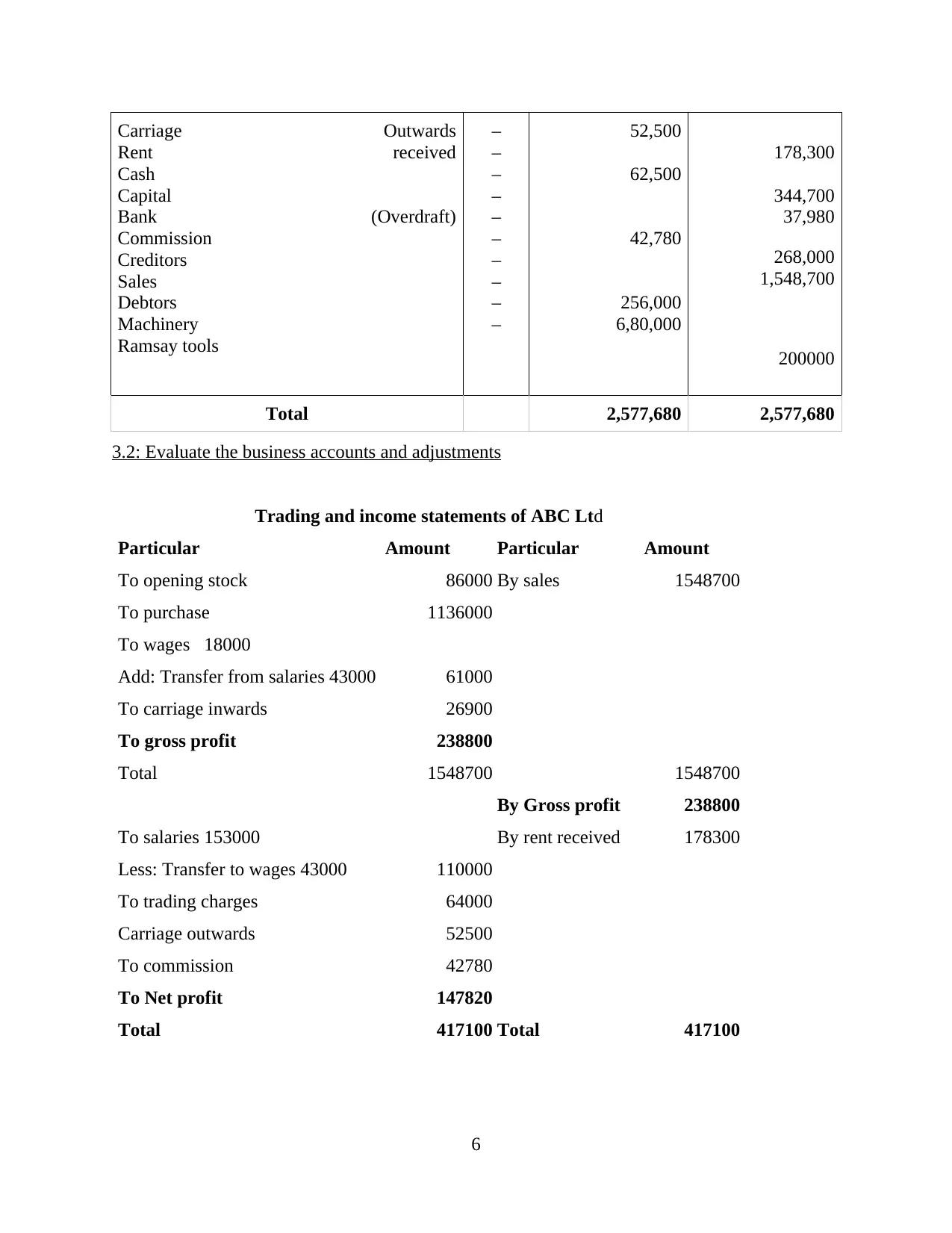

Carriage Outwards

Rent received

Cash

Capital

Bank (Overdraft)

Commission

Creditors

Sales

Debtors

Machinery

Ramsay tools

–

–

–

–

–

–

–

–

–

–

52,500

62,500

42,780

256,000

6,80,000

178,300

344,700

37,980

268,000

1,548,700

200000

Total 2,577,680 2,577,680

3.2: Evaluate the business accounts and adjustments

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To wages 18000

Add: Transfer from salaries 43000 61000

To carriage inwards 26900

To gross profit 238800

Total 1548700 1548700

By Gross profit 238800

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

Carriage outwards 52500

To commission 42780

To Net profit 147820

Total 417100 Total 417100

6

Rent received

Cash

Capital

Bank (Overdraft)

Commission

Creditors

Sales

Debtors

Machinery

Ramsay tools

–

–

–

–

–

–

–

–

–

–

52,500

62,500

42,780

256,000

6,80,000

178,300

344,700

37,980

268,000

1,548,700

200000

Total 2,577,680 2,577,680

3.2: Evaluate the business accounts and adjustments

Trading and income statements of ABC Ltd

Particular Amount Particular Amount

To opening stock 86000 By sales 1548700

To purchase 1136000

To wages 18000

Add: Transfer from salaries 43000 61000

To carriage inwards 26900

To gross profit 238800

Total 1548700 1548700

By Gross profit 238800

To salaries 153000 By rent received 178300

Less: Transfer to wages 43000 110000

To trading charges 64000

Carriage outwards 52500

To commission 42780

To Net profit 147820

Total 417100 Total 417100

6

3.3: Process and purpose behind preparation of budgetary control

Purpose of Budgetary control:

The budgetary control assists the managers in the comparing actual results with the

budgeted ones so that company can ensure that resources and finance of business are

utilised in an efficient manner.

The main motive behind the preparation of budgets is to reduce and eliminate the

amount of wastages by utilising resources as defined in budgets, which increases the

profitability of company( Gursoy, Rahman, and Swanger, 2012).

Process:

Gathering of information from relevant sources.

Keeping in record all sources of income.

Keep track record of monthly expense.

Dividing expenses under various heads.

Estimation of monthly income and expense.

Making adjustments to reduce expense.

Cutting expenditure.

Review budget Monthly.

Planning for infrequent expenses.

7

Purpose of Budgetary control:

The budgetary control assists the managers in the comparing actual results with the

budgeted ones so that company can ensure that resources and finance of business are

utilised in an efficient manner.

The main motive behind the preparation of budgets is to reduce and eliminate the

amount of wastages by utilising resources as defined in budgets, which increases the

profitability of company( Gursoy, Rahman, and Swanger, 2012).

Process:

Gathering of information from relevant sources.

Keeping in record all sources of income.

Keep track record of monthly expense.

Dividing expenses under various heads.

Estimation of monthly income and expense.

Making adjustments to reduce expense.

Cutting expenditure.

Review budget Monthly.

Planning for infrequent expenses.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

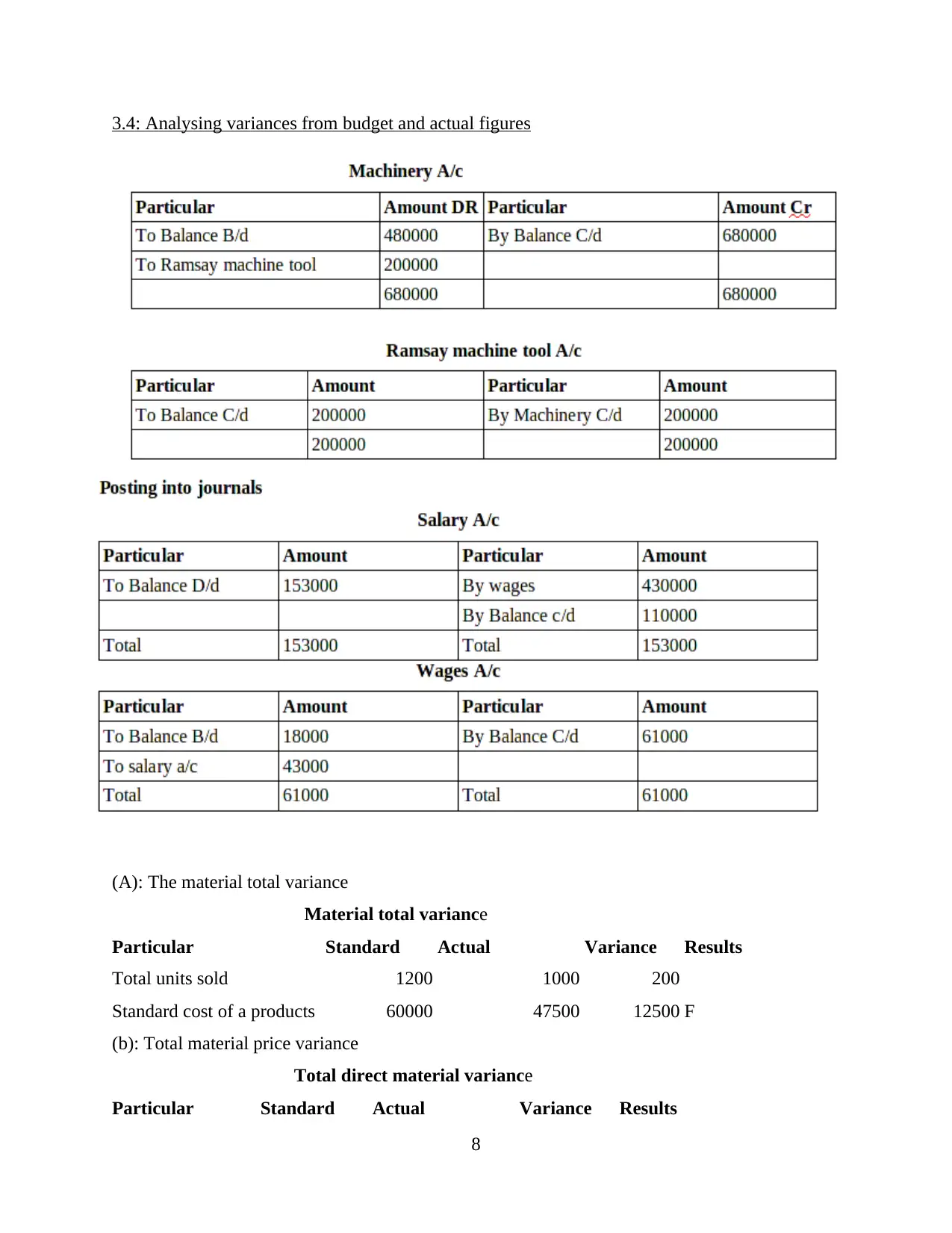

3.4: Analysing variances from budget and actual figures

(A): The material total variance

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

(b): Total material price variance

Total direct material variance

Particular Standard Actual Variance Results

8

(A): The material total variance

Material total variance

Particular Standard Actual Variance Results

Total units sold 1200 1000 200

Standard cost of a products 60000 47500 12500 F

(b): Total material price variance

Total direct material variance

Particular Standard Actual Variance Results

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total units sold 50000 47500 2500 F

(c): Total material usage variance

MUV: Selling price ( Actual quantity * Standard quantity)

: 50(1000-1200)

: -10000 Adverse

TASK 4

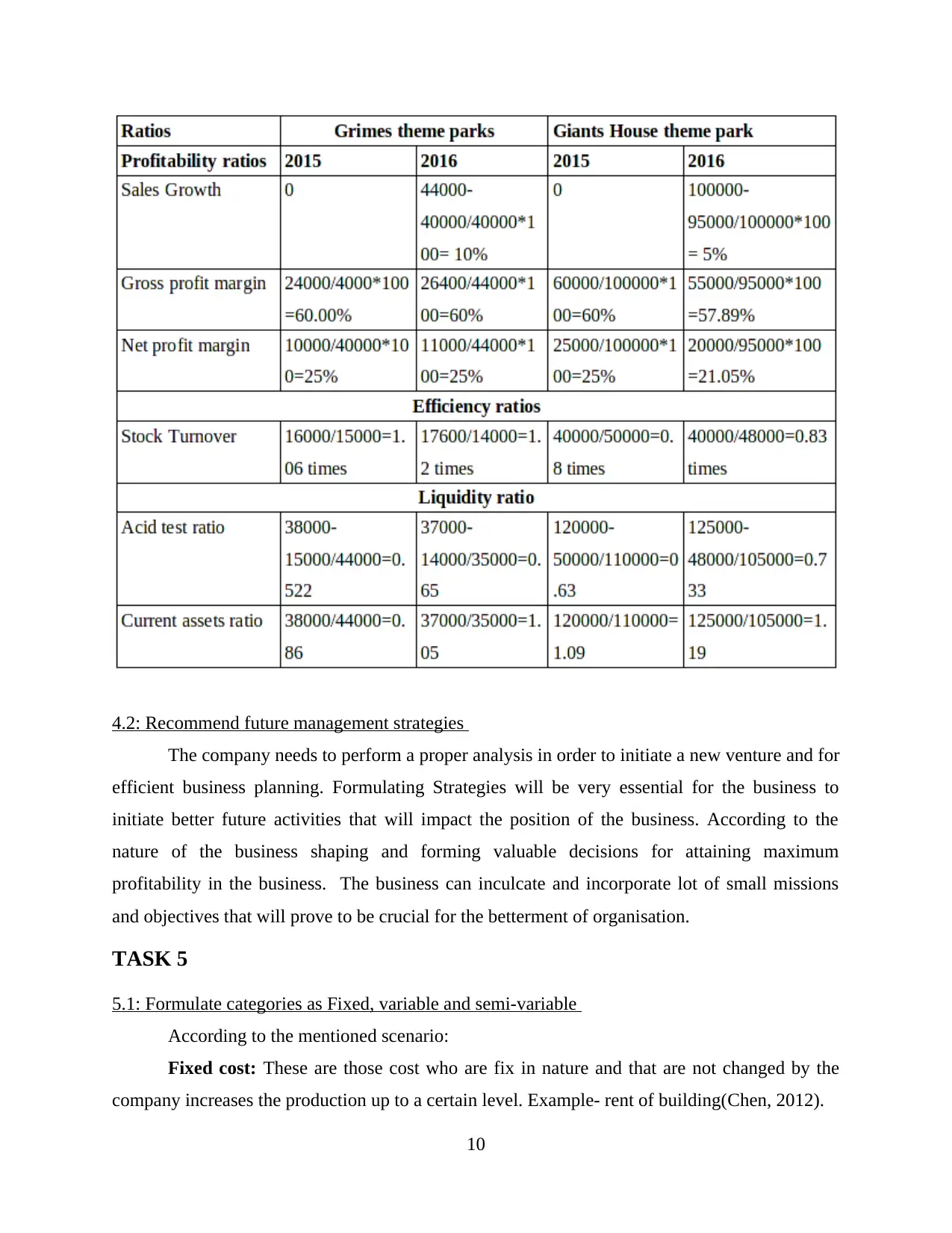

4.1: Calculating various ratios of the given companies

Profitability ratios: The profitability ratios are ascertained by the companies in order to know

about the profit making ability of the company and how efficient and consistent company is

generating profits. The profitability ratios are calculated in proportion to the total revenue of the

company. The ratios which are calculated under this head include net profit margin, gross profit

margin etc.

Liquidity ratios: These are the ratios which are estimated by the company for measuring the

ability of the company to meet the short term obligations and the liquid assets of the company.

The ratios which are calculated under this include current ratio, acid test ratio, defence interval

ratio etc( Engel, Fischer, and Galetovic, 2013).

Efficiency ratio: This ratio is calculated to measure how efficient the business is in utilising the

assets and other resources of the business. It is the duty of the managers to ensure that the assets

of the company are optimum utilised for the better productivity. The turnover of the company is

considered under its calculation:

9

(c): Total material usage variance

MUV: Selling price ( Actual quantity * Standard quantity)

: 50(1000-1200)

: -10000 Adverse

TASK 4

4.1: Calculating various ratios of the given companies

Profitability ratios: The profitability ratios are ascertained by the companies in order to know

about the profit making ability of the company and how efficient and consistent company is

generating profits. The profitability ratios are calculated in proportion to the total revenue of the

company. The ratios which are calculated under this head include net profit margin, gross profit

margin etc.

Liquidity ratios: These are the ratios which are estimated by the company for measuring the

ability of the company to meet the short term obligations and the liquid assets of the company.

The ratios which are calculated under this include current ratio, acid test ratio, defence interval

ratio etc( Engel, Fischer, and Galetovic, 2013).

Efficiency ratio: This ratio is calculated to measure how efficient the business is in utilising the

assets and other resources of the business. It is the duty of the managers to ensure that the assets

of the company are optimum utilised for the better productivity. The turnover of the company is

considered under its calculation:

9

4.2: Recommend future management strategies

The company needs to perform a proper analysis in order to initiate a new venture and for

efficient business planning. Formulating Strategies will be very essential for the business to

initiate better future activities that will impact the position of the business. According to the

nature of the business shaping and forming valuable decisions for attaining maximum

profitability in the business. The business can inculcate and incorporate lot of small missions

and objectives that will prove to be crucial for the betterment of organisation.

TASK 5

5.1: Formulate categories as Fixed, variable and semi-variable

According to the mentioned scenario:

Fixed cost: These are those cost who are fix in nature and that are not changed by the

company increases the production up to a certain level. Example- rent of building(Chen, 2012).

10

The company needs to perform a proper analysis in order to initiate a new venture and for

efficient business planning. Formulating Strategies will be very essential for the business to

initiate better future activities that will impact the position of the business. According to the

nature of the business shaping and forming valuable decisions for attaining maximum

profitability in the business. The business can inculcate and incorporate lot of small missions

and objectives that will prove to be crucial for the betterment of organisation.

TASK 5

5.1: Formulate categories as Fixed, variable and semi-variable

According to the mentioned scenario:

Fixed cost: These are those cost who are fix in nature and that are not changed by the

company increases the production up to a certain level. Example- rent of building(Chen, 2012).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.