Comprehensive Financial Analysis Report for Liverton Co. (Finance)

VerifiedAdded on 2023/06/04

|17

|4029

|484

Report

AI Summary

This finance report critically analyzes the financial statements of Liverton Co., incorporating various financial analysis techniques. It begins with an introduction to finance, defining key concepts and types of finance. The report then calculates and interprets financial ratios for 2018 and 2019, i...

Introduction to

Finance

Contents

Finance

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Question 1........................................................................................................................................3

Significance of financial statements analysis...........................................................................5

Question 2........................................................................................................................................6

A) opening statement of financial position..............................................................................6

B ) Monthly cash budget for 6 months.....................................................................................6

Question 3........................................................................................................................................8

A) Calculation of Breakeven point (BEP)...............................................................................8

B) Margin of Safety ( MOS ) for the year ended 2019 and 2020...........................................9

C) Discussion of the new strategy that has been formed by Jessica....................................10

Question 4......................................................................................................................................10

A) Calculation of Pay Back Period, Net Present Value and Average Rate of Return......10

B) Discuss the best method of appraisal technique...............................................................13

Net Present Value-.........................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

TASK...............................................................................................................................................3

Question 1........................................................................................................................................3

Significance of financial statements analysis...........................................................................5

Question 2........................................................................................................................................6

A) opening statement of financial position..............................................................................6

B ) Monthly cash budget for 6 months.....................................................................................6

Question 3........................................................................................................................................8

A) Calculation of Breakeven point (BEP)...............................................................................8

B) Margin of Safety ( MOS ) for the year ended 2019 and 2020...........................................9

C) Discussion of the new strategy that has been formed by Jessica....................................10

Question 4......................................................................................................................................10

A) Calculation of Pay Back Period, Net Present Value and Average Rate of Return......10

B) Discuss the best method of appraisal technique...............................................................13

Net Present Value-.........................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Finance is defined as matters of management of money and includes various activities

such as creation, study of money and investment, borrowing, saving, and forecasting of money.

It involves the use of banking, leverage or debt, security, creation and oversight of various

financial statements (Broadstock and Cheng, 2019). These are the written documents used in day

to day operating life of an enterprise. It can be termed as the broader term in describing the study

system of financials. It is not limited to the money but it is beyond that. Although money act as a

legal tender used in various legal settlements and many more. Usually there are three types of

finance Personal Finance, Corporate Finance and the last one Public Finance. The main aim of

this report is to critically analyse the financial statement of Liverton Co. (Dewick and Schröder,

2020). This report includes different types of ratio analysis, importance of audience, opening

statement of financial position, cash flow forecast, evaluating the expenses, payback period, rate

of return, NPV, investments approaches, profitability of each project, cash budget and many

more.

TASK

Question 1

Calculation of ratios for the year 2019 and the year 2018

1. Gross Profit Margin = (sales - COGS) * 100 / sales

= (3495 – 2182) * 100 / 3495

= (1313 / 3495) * 100

= 37.57 %

Interpretation: Gross profit margin is the measure of profitability that evaluates the percentage

of profit that exceeds the cost of goods sold. It is just a measure of comparison between gross

profit and sales revenue. In the given question gross profit for the specified year comes out to

37.57% which is almost equal to 38% that shows that the company is growing as the cost of

these is already reducing.

Finance is defined as matters of management of money and includes various activities

such as creation, study of money and investment, borrowing, saving, and forecasting of money.

It involves the use of banking, leverage or debt, security, creation and oversight of various

financial statements (Broadstock and Cheng, 2019). These are the written documents used in day

to day operating life of an enterprise. It can be termed as the broader term in describing the study

system of financials. It is not limited to the money but it is beyond that. Although money act as a

legal tender used in various legal settlements and many more. Usually there are three types of

finance Personal Finance, Corporate Finance and the last one Public Finance. The main aim of

this report is to critically analyse the financial statement of Liverton Co. (Dewick and Schröder,

2020). This report includes different types of ratio analysis, importance of audience, opening

statement of financial position, cash flow forecast, evaluating the expenses, payback period, rate

of return, NPV, investments approaches, profitability of each project, cash budget and many

more.

TASK

Question 1

Calculation of ratios for the year 2019 and the year 2018

1. Gross Profit Margin = (sales - COGS) * 100 / sales

= (3495 – 2182) * 100 / 3495

= (1313 / 3495) * 100

= 37.57 %

Interpretation: Gross profit margin is the measure of profitability that evaluates the percentage

of profit that exceeds the cost of goods sold. It is just a measure of comparison between gross

profit and sales revenue. In the given question gross profit for the specified year comes out to

37.57% which is almost equal to 38% that shows that the company is growing as the cost of

these is already reducing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Assets usage ratio= Total sales / average total assets

= 3495 / [(3812 + 2503) / 2]

= 3495 / 3157.5

= 1.10 times

Interpretation: This ratio measures the efficiency of an organisation that is how efficient an

organisation is in using the assets at its disposable to make something from it in terms of money

and turn it in the form of profit. In this ratio the value is 1.10. When it come to the ideal ratio for

this ratio it is 2.5 times or more. In the given question, the assets usage ratio of this organisation

is 1.10 which is very low when compared with the ideal ratio measurement. So the company nee

to improve their revenue generation ability and need to look and optimise their assets in a proper

and efficient manner.

3. Current Ratio = Current Assets / Current Liabilities

= 1687 / 744

= 2.27 times

Interpretation: Current ratio is a liquidity ratio that is used to calculate the company's ability to

meet its obligations which are due for less than a year or a year. It is used with the assets

available on the balance sheet. It is also termed as the Working capital ratio. It’s ideal ratio is 2:1

in in the company given in the question company has 2.27 which is more than the ideal ratio. So

this is the good situation for the company as they have more current assets than their current

liabilities.

4. Acid Test Ratio = (Current asset – stock) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation: Acid test ratio also known as Quick Ratio measures capacity of a firm to meet

their short term liabilities by liquidating the assets. The ideal ratio of this is 1:1. in this question

the ratio comes out as 2.06 time which is quite impressive, significant and adequate capacity to

meet short term Obligations.

= 3495 / [(3812 + 2503) / 2]

= 3495 / 3157.5

= 1.10 times

Interpretation: This ratio measures the efficiency of an organisation that is how efficient an

organisation is in using the assets at its disposable to make something from it in terms of money

and turn it in the form of profit. In this ratio the value is 1.10. When it come to the ideal ratio for

this ratio it is 2.5 times or more. In the given question, the assets usage ratio of this organisation

is 1.10 which is very low when compared with the ideal ratio measurement. So the company nee

to improve their revenue generation ability and need to look and optimise their assets in a proper

and efficient manner.

3. Current Ratio = Current Assets / Current Liabilities

= 1687 / 744

= 2.27 times

Interpretation: Current ratio is a liquidity ratio that is used to calculate the company's ability to

meet its obligations which are due for less than a year or a year. It is used with the assets

available on the balance sheet. It is also termed as the Working capital ratio. It’s ideal ratio is 2:1

in in the company given in the question company has 2.27 which is more than the ideal ratio. So

this is the good situation for the company as they have more current assets than their current

liabilities.

4. Acid Test Ratio = (Current asset – stock) / current liability

= ( 1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation: Acid test ratio also known as Quick Ratio measures capacity of a firm to meet

their short term liabilities by liquidating the assets. The ideal ratio of this is 1:1. in this question

the ratio comes out as 2.06 time which is quite impressive, significant and adequate capacity to

meet short term Obligations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

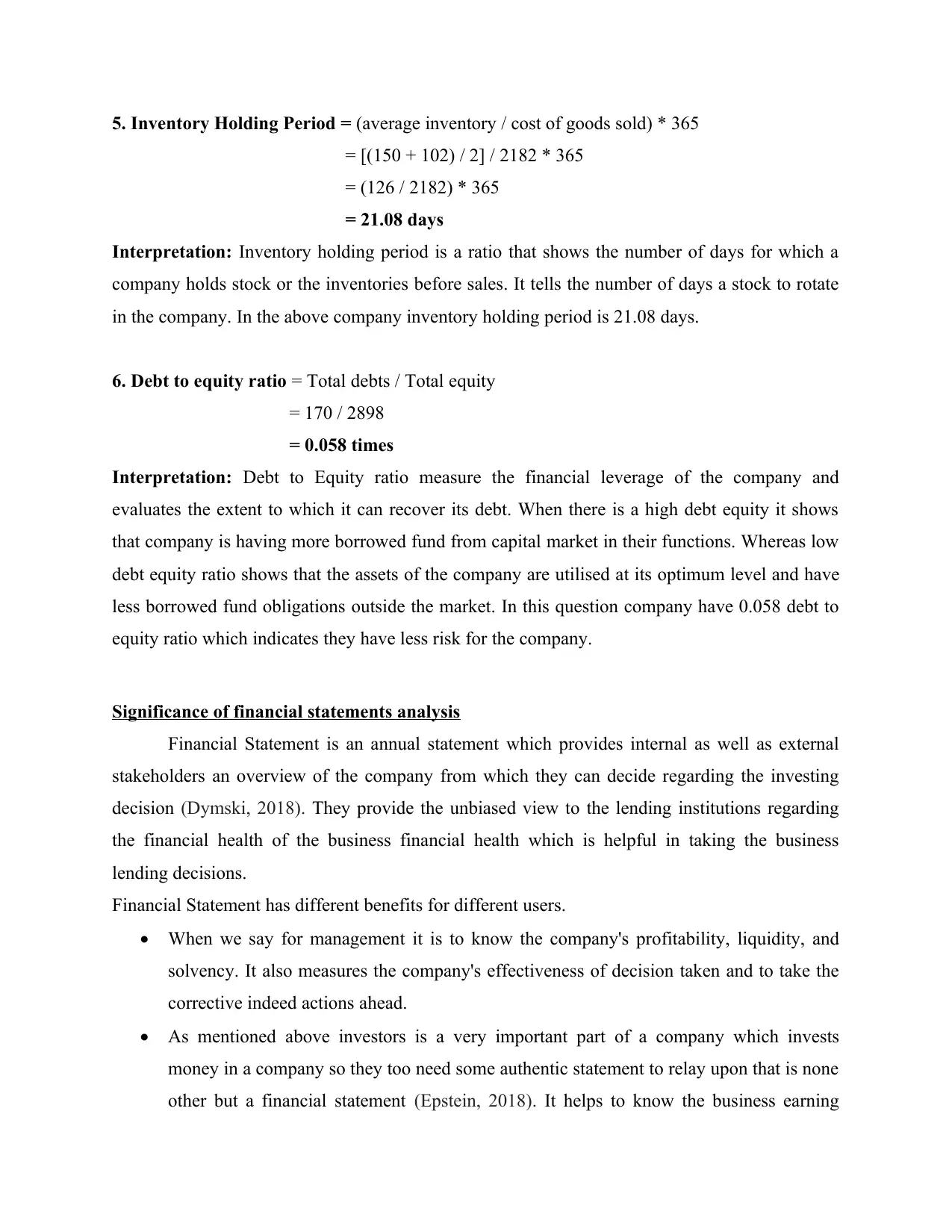

5. Inventory Holding Period = (average inventory / cost of goods sold) * 365

= [(150 + 102) / 2] / 2182 * 365

= (126 / 2182) * 365

= 21.08 days

Interpretation: Inventory holding period is a ratio that shows the number of days for which a

company holds stock or the inventories before sales. It tells the number of days a stock to rotate

in the company. In the above company inventory holding period is 21.08 days.

6. Debt to equity ratio = Total debts / Total equity

= 170 / 2898

= 0.058 times

Interpretation: Debt to Equity ratio measure the financial leverage of the company and

evaluates the extent to which it can recover its debt. When there is a high debt equity it shows

that company is having more borrowed fund from capital market in their functions. Whereas low

debt equity ratio shows that the assets of the company are utilised at its optimum level and have

less borrowed fund obligations outside the market. In this question company have 0.058 debt to

equity ratio which indicates they have less risk for the company.

Significance of financial statements analysis

Financial Statement is an annual statement which provides internal as well as external

stakeholders an overview of the company from which they can decide regarding the investing

decision (Dymski, 2018). They provide the unbiased view to the lending institutions regarding

the financial health of the business financial health which is helpful in taking the business

lending decisions.

Financial Statement has different benefits for different users.

When we say for management it is to know the company's profitability, liquidity, and

solvency. It also measures the company's effectiveness of decision taken and to take the

corrective indeed actions ahead.

As mentioned above investors is a very important part of a company which invests

money in a company so they too need some authentic statement to relay upon that is none

other but a financial statement (Epstein, 2018). It helps to know the business earning

= [(150 + 102) / 2] / 2182 * 365

= (126 / 2182) * 365

= 21.08 days

Interpretation: Inventory holding period is a ratio that shows the number of days for which a

company holds stock or the inventories before sales. It tells the number of days a stock to rotate

in the company. In the above company inventory holding period is 21.08 days.

6. Debt to equity ratio = Total debts / Total equity

= 170 / 2898

= 0.058 times

Interpretation: Debt to Equity ratio measure the financial leverage of the company and

evaluates the extent to which it can recover its debt. When there is a high debt equity it shows

that company is having more borrowed fund from capital market in their functions. Whereas low

debt equity ratio shows that the assets of the company are utilised at its optimum level and have

less borrowed fund obligations outside the market. In this question company have 0.058 debt to

equity ratio which indicates they have less risk for the company.

Significance of financial statements analysis

Financial Statement is an annual statement which provides internal as well as external

stakeholders an overview of the company from which they can decide regarding the investing

decision (Dymski, 2018). They provide the unbiased view to the lending institutions regarding

the financial health of the business financial health which is helpful in taking the business

lending decisions.

Financial Statement has different benefits for different users.

When we say for management it is to know the company's profitability, liquidity, and

solvency. It also measures the company's effectiveness of decision taken and to take the

corrective indeed actions ahead.

As mentioned above investors is a very important part of a company which invests

money in a company so they too need some authentic statement to relay upon that is none

other but a financial statement (Epstein, 2018). It helps to know the business earning

capacity and its future growth indications and evaluates the safety of the money they have

invested in the company.

Liquidation and solvency position of a business is very important for the creditors.

Creditors should be well versed with the current situation of the company.

Government plays the important role in every business. Government need the financial

statements of a company for the taxation purpose and to take the decisions about the price

regulations.

Customers get the longevity of the company by seeing the financial statement of the

company.

Employees represents the company but they can't be confidant without knowing the

financials statement of the company. When they will know the progress of the company

they can be familiar by the policies and changes in the wages, bonus, job stability, etc.

Question 2

A) opening statement of financial position

Assets

Non-current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

Total £ 200,000

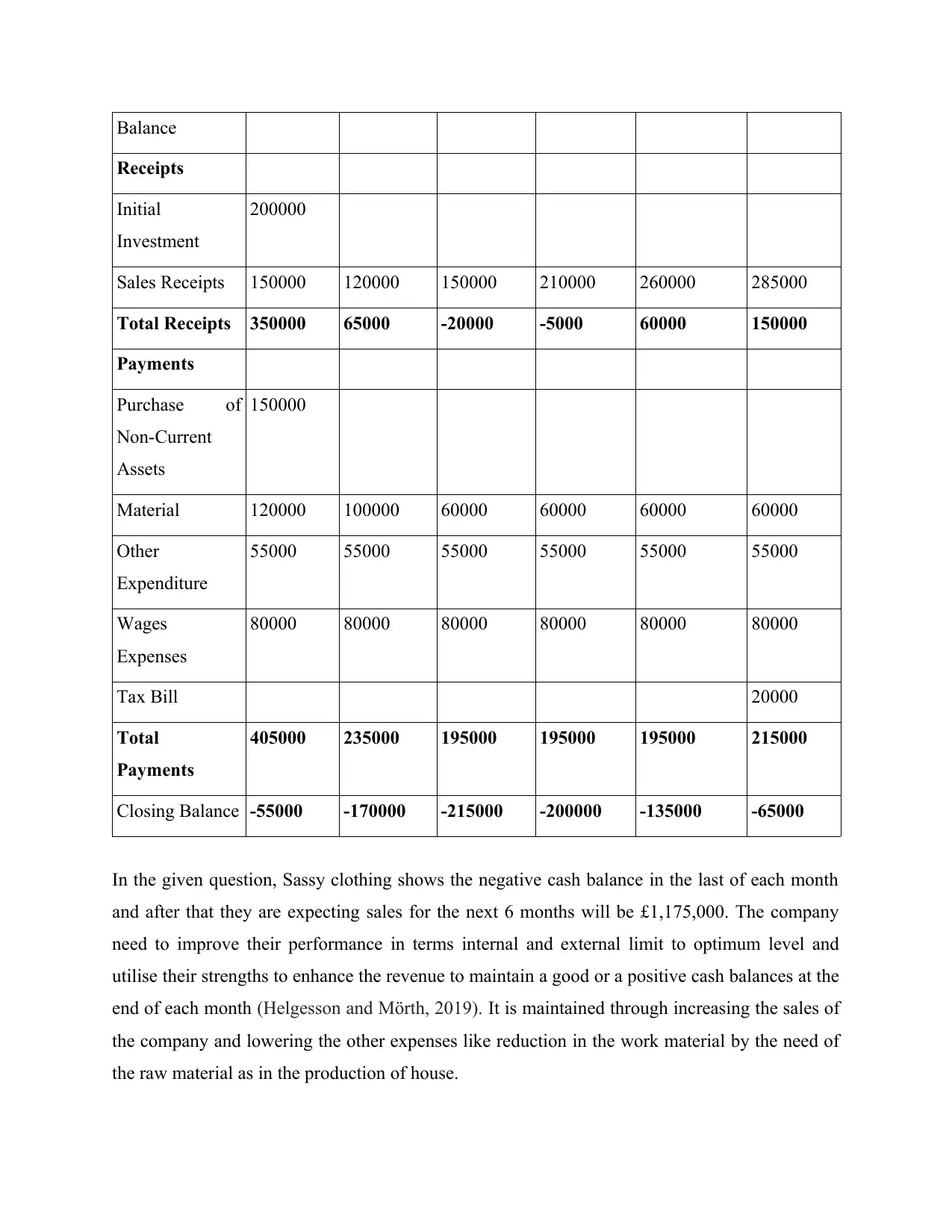

B ) Monthly cash budget for 6 months

Particulars July August September October November December

Opening -55000 -170000 -215000 -200000 -135000

invested in the company.

Liquidation and solvency position of a business is very important for the creditors.

Creditors should be well versed with the current situation of the company.

Government plays the important role in every business. Government need the financial

statements of a company for the taxation purpose and to take the decisions about the price

regulations.

Customers get the longevity of the company by seeing the financial statement of the

company.

Employees represents the company but they can't be confidant without knowing the

financials statement of the company. When they will know the progress of the company

they can be familiar by the policies and changes in the wages, bonus, job stability, etc.

Question 2

A) opening statement of financial position

Assets

Non-current assets

Tangible assets £ 150,000

Current assets

cash at bank £ 50,000

Total assets £ 200,000

liabilities

Capital £ 200,000

Total £ 200,000

B ) Monthly cash budget for 6 months

Particulars July August September October November December

Opening -55000 -170000 -215000 -200000 -135000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance

Receipts

Initial

Investment

200000

Sales Receipts 150000 120000 150000 210000 260000 285000

Total Receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of

Non-Current

Assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

Expenditure

55000 55000 55000 55000 55000 55000

Wages

Expenses

80000 80000 80000 80000 80000 80000

Tax Bill 20000

Total

Payments

405000 235000 195000 195000 195000 215000

Closing Balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, Sassy clothing shows the negative cash balance in the last of each month

and after that they are expecting sales for the next 6 months will be £1,175,000. The company

need to improve their performance in terms internal and external limit to optimum level and

utilise their strengths to enhance the revenue to maintain a good or a positive cash balances at the

end of each month (Helgesson and Mörth, 2019). It is maintained through increasing the sales of

the company and lowering the other expenses like reduction in the work material by the need of

the raw material as in the production of house.

Receipts

Initial

Investment

200000

Sales Receipts 150000 120000 150000 210000 260000 285000

Total Receipts 350000 65000 -20000 -5000 60000 150000

Payments

Purchase of

Non-Current

Assets

150000

Material 120000 100000 60000 60000 60000 60000

Other

Expenditure

55000 55000 55000 55000 55000 55000

Wages

Expenses

80000 80000 80000 80000 80000 80000

Tax Bill 20000

Total

Payments

405000 235000 195000 195000 195000 215000

Closing Balance -55000 -170000 -215000 -200000 -135000 -65000

In the given question, Sassy clothing shows the negative cash balance in the last of each month

and after that they are expecting sales for the next 6 months will be £1,175,000. The company

need to improve their performance in terms internal and external limit to optimum level and

utilise their strengths to enhance the revenue to maintain a good or a positive cash balances at the

end of each month (Helgesson and Mörth, 2019). It is maintained through increasing the sales of

the company and lowering the other expenses like reduction in the work material by the need of

the raw material as in the production of house.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C ) Explanation of additional expenditures

This company need to surround the cost within the month side of July and December

which includes various expenses like software bills, running fees, charge to the suppliers and

rent. Overdraft Mortgage shows more price range after they no longer have any remain in the

company (Zhang and Taghizadeh-Hesary, 2022). It allows the company in dealing with the

timing mismatch in price range and helps in keeping the positive track record. The enterprise is

capable in doing the bills in their cost on the time with the help of financial Institution overdraft

(Jones, 2020).

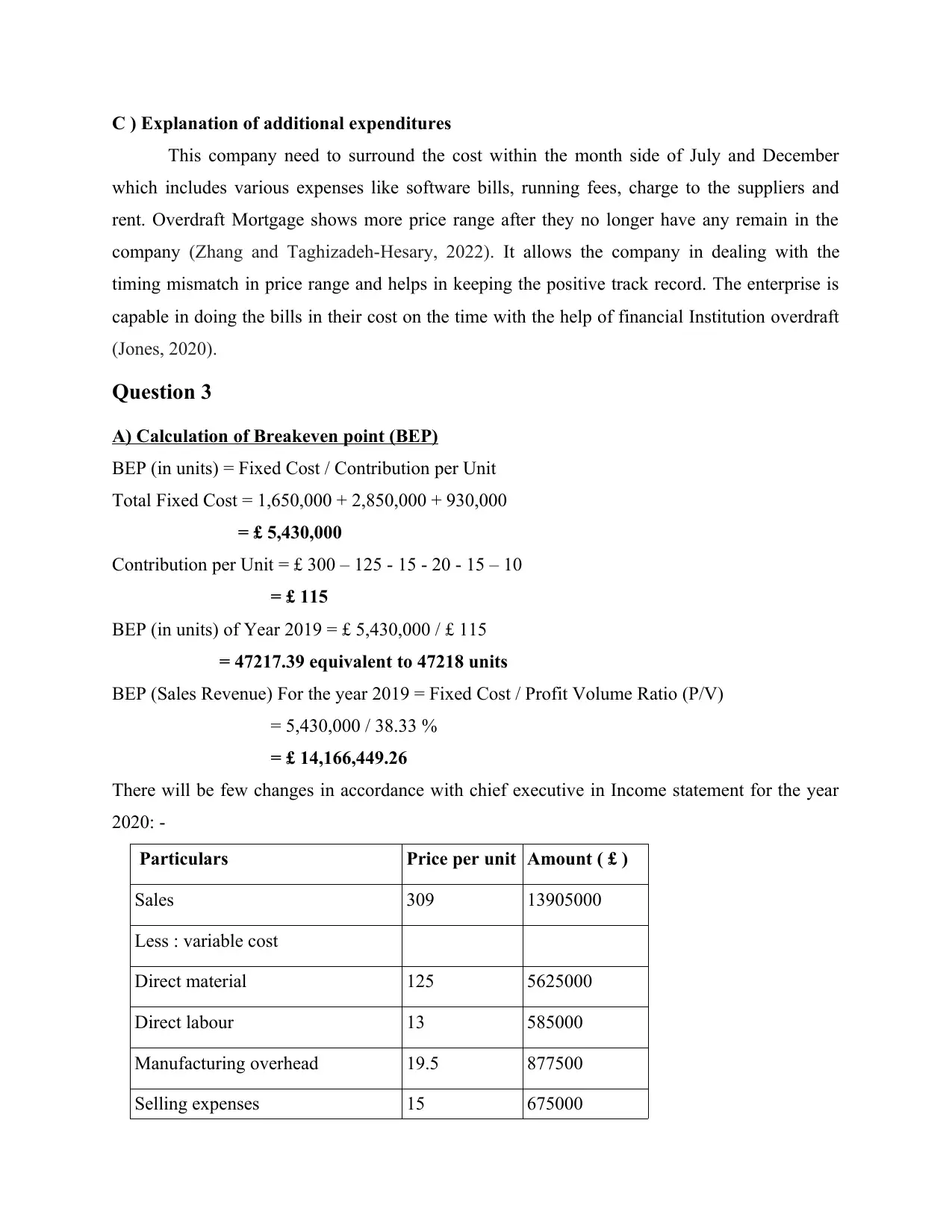

Question 3

A) Calculation of Breakeven point (BEP)

BEP (in units) = Fixed Cost / Contribution per Unit

Total Fixed Cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

Contribution per Unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of Year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (Sales Revenue) For the year 2019 = Fixed Cost / Profit Volume Ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

There will be few changes in accordance with chief executive in Income statement for the year

2020: -

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

This company need to surround the cost within the month side of July and December

which includes various expenses like software bills, running fees, charge to the suppliers and

rent. Overdraft Mortgage shows more price range after they no longer have any remain in the

company (Zhang and Taghizadeh-Hesary, 2022). It allows the company in dealing with the

timing mismatch in price range and helps in keeping the positive track record. The enterprise is

capable in doing the bills in their cost on the time with the help of financial Institution overdraft

(Jones, 2020).

Question 3

A) Calculation of Breakeven point (BEP)

BEP (in units) = Fixed Cost / Contribution per Unit

Total Fixed Cost = 1,650,000 + 2,850,000 + 930,000

= £ 5,430,000

Contribution per Unit = £ 300 – 125 - 15 - 20 - 15 – 10

= £ 115

BEP (in units) of Year 2019 = £ 5,430,000 / £ 115

= 47217.39 equivalent to 47218 units

BEP (Sales Revenue) For the year 2019 = Fixed Cost / Profit Volume Ratio (P/V)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

There will be few changes in accordance with chief executive in Income statement for the year

2020: -

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

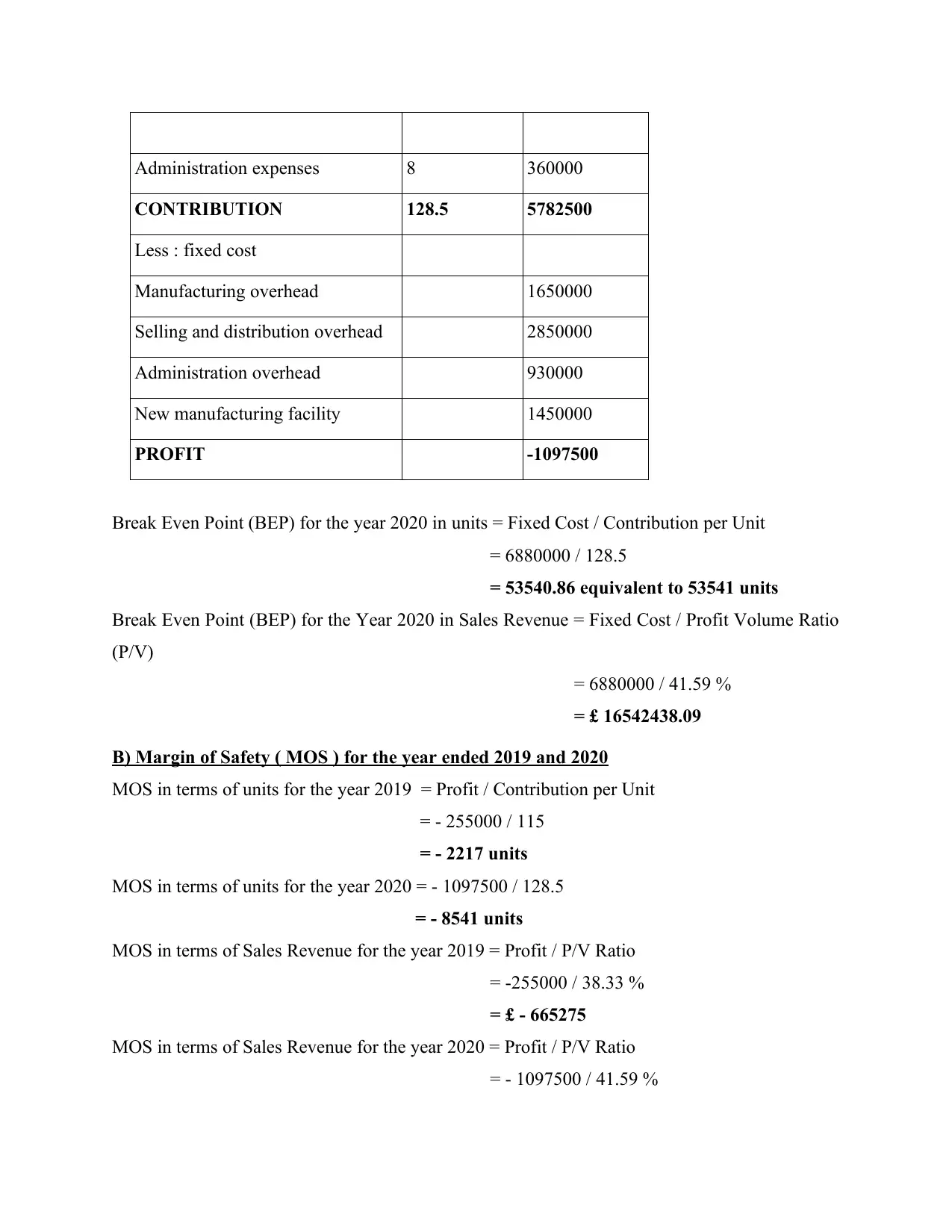

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break Even Point (BEP) for the year 2020 in units = Fixed Cost / Contribution per Unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break Even Point (BEP) for the Year 2020 in Sales Revenue = Fixed Cost / Profit Volume Ratio

(P/V)

= 6880000 / 41.59 %

= £ 16542438.09

B) Margin of Safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = Profit / Contribution per Unit

= - 255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = - 1097500 / 128.5

= - 8541 units

MOS in terms of Sales Revenue for the year 2019 = Profit / P/V Ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of Sales Revenue for the year 2020 = Profit / P/V Ratio

= - 1097500 / 41.59 %

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

Break Even Point (BEP) for the year 2020 in units = Fixed Cost / Contribution per Unit

= 6880000 / 128.5

= 53540.86 equivalent to 53541 units

Break Even Point (BEP) for the Year 2020 in Sales Revenue = Fixed Cost / Profit Volume Ratio

(P/V)

= 6880000 / 41.59 %

= £ 16542438.09

B) Margin of Safety ( MOS ) for the year ended 2019 and 2020

MOS in terms of units for the year 2019 = Profit / Contribution per Unit

= - 255000 / 115

= - 2217 units

MOS in terms of units for the year 2020 = - 1097500 / 128.5

= - 8541 units

MOS in terms of Sales Revenue for the year 2019 = Profit / P/V Ratio

= -255000 / 38.33 %

= £ - 665275

MOS in terms of Sales Revenue for the year 2020 = Profit / P/V Ratio

= - 1097500 / 41.59 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

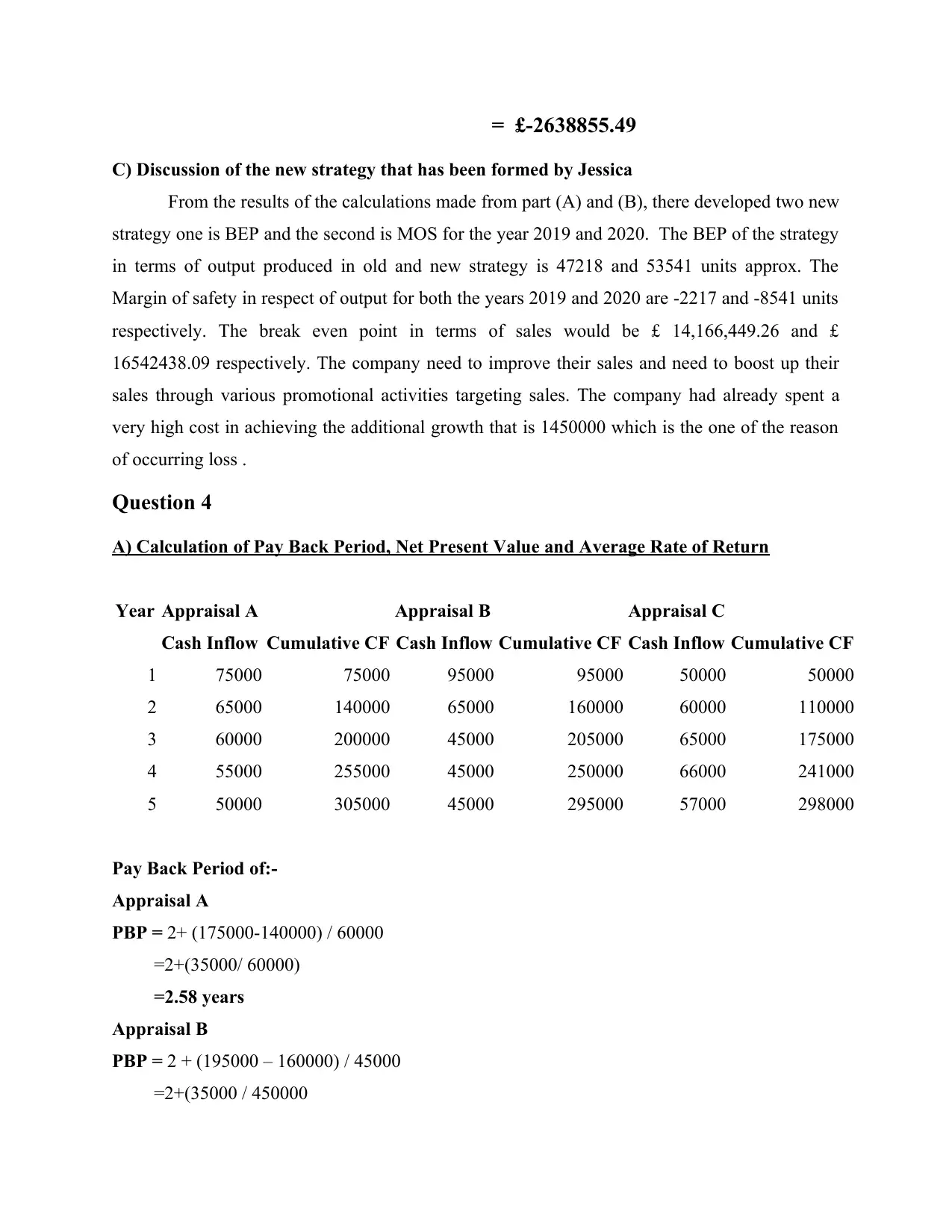

= £-2638855.49

C) Discussion of the new strategy that has been formed by Jessica

From the results of the calculations made from part (A) and (B), there developed two new

strategy one is BEP and the second is MOS for the year 2019 and 2020. The BEP of the strategy

in terms of output produced in old and new strategy is 47218 and 53541 units approx. The

Margin of safety in respect of output for both the years 2019 and 2020 are -2217 and -8541 units

respectively. The break even point in terms of sales would be £ 14,166,449.26 and £

16542438.09 respectively. The company need to improve their sales and need to boost up their

sales through various promotional activities targeting sales. The company had already spent a

very high cost in achieving the additional growth that is 1450000 which is the one of the reason

of occurring loss .

Question 4

A) Calculation of Pay Back Period, Net Present Value and Average Rate of Return

Year Appraisal A Appraisal B Appraisal C

Cash Inflow Cumulative CF Cash Inflow Cumulative CF Cash Inflow Cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay Back Period of:-

Appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

C) Discussion of the new strategy that has been formed by Jessica

From the results of the calculations made from part (A) and (B), there developed two new

strategy one is BEP and the second is MOS for the year 2019 and 2020. The BEP of the strategy

in terms of output produced in old and new strategy is 47218 and 53541 units approx. The

Margin of safety in respect of output for both the years 2019 and 2020 are -2217 and -8541 units

respectively. The break even point in terms of sales would be £ 14,166,449.26 and £

16542438.09 respectively. The company need to improve their sales and need to boost up their

sales through various promotional activities targeting sales. The company had already spent a

very high cost in achieving the additional growth that is 1450000 which is the one of the reason

of occurring loss .

Question 4

A) Calculation of Pay Back Period, Net Present Value and Average Rate of Return

Year Appraisal A Appraisal B Appraisal C

Cash Inflow Cumulative CF Cash Inflow Cumulative CF Cash Inflow Cumulative CF

1 75000 75000 95000 95000 50000 50000

2 65000 140000 65000 160000 60000 110000

3 60000 200000 45000 205000 65000 175000

4 55000 255000 45000 250000 66000 241000

5 50000 305000 45000 295000 57000 298000

Pay Back Period of:-

Appraisal A

PBP = 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2.58 years

Appraisal B

PBP = 2 + (195000 – 160000) / 45000

=2+(35000 / 450000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

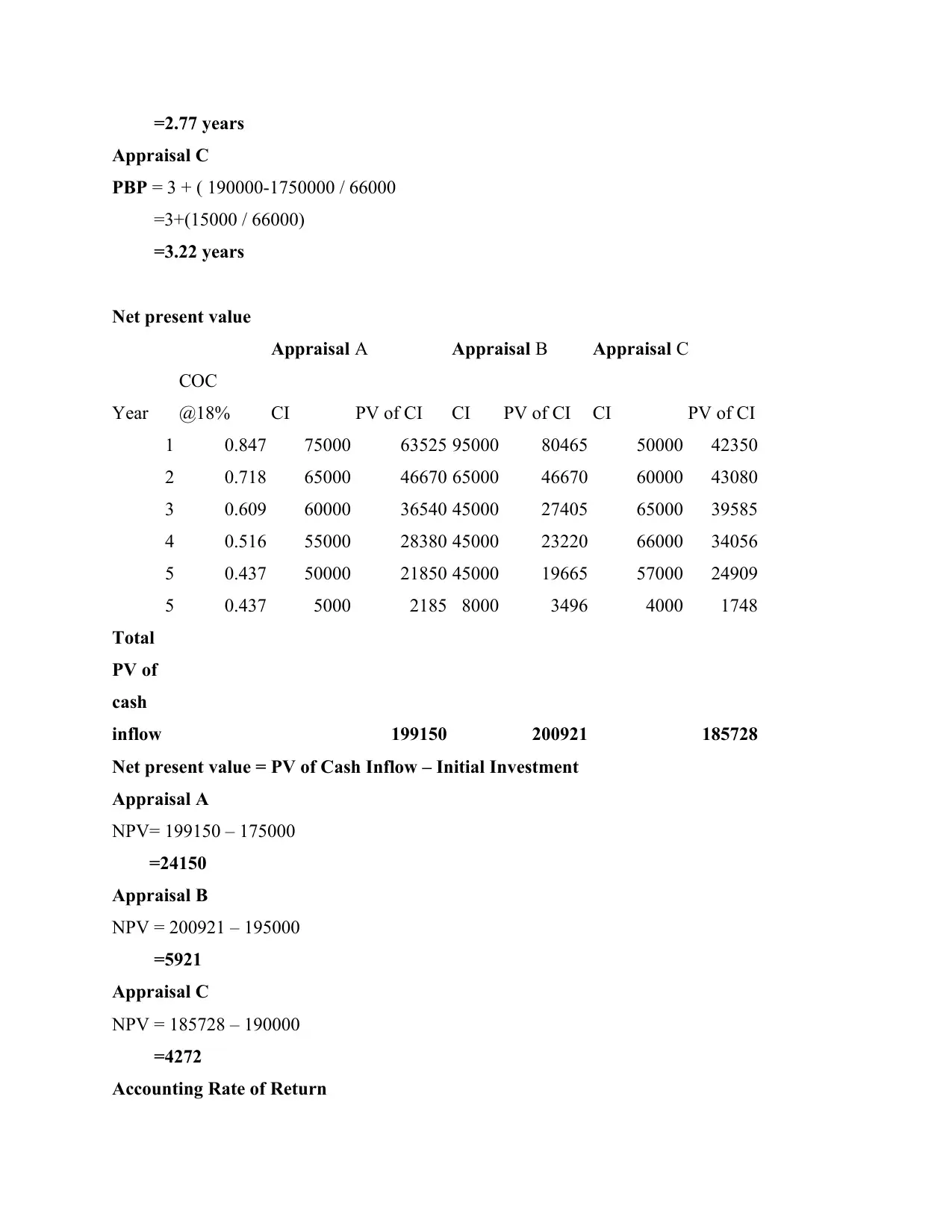

=2.77 years

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of Cash Inflow – Initial Investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting Rate of Return

Appraisal C

PBP = 3 + ( 190000-1750000 / 66000

=3+(15000 / 66000)

=3.22 years

Net present value

Appraisal A Appraisal B Appraisal C

Year

COC

@18% CI PV of CI CI PV of CI CI PV of CI

1 0.847 75000 63525 95000 80465 50000 42350

2 0.718 65000 46670 65000 46670 60000 43080

3 0.609 60000 36540 45000 27405 65000 39585

4 0.516 55000 28380 45000 23220 66000 34056

5 0.437 50000 21850 45000 19665 57000 24909

5 0.437 5000 2185 8000 3496 4000 1748

Total

PV of

cash

inflow 199150 200921 185728

Net present value = PV of Cash Inflow – Initial Investment

Appraisal A

NPV= 199150 – 175000

=24150

Appraisal B

NPV = 200921 – 195000

=5921

Appraisal C

NPV = 185728 – 190000

=4272

Accounting Rate of Return

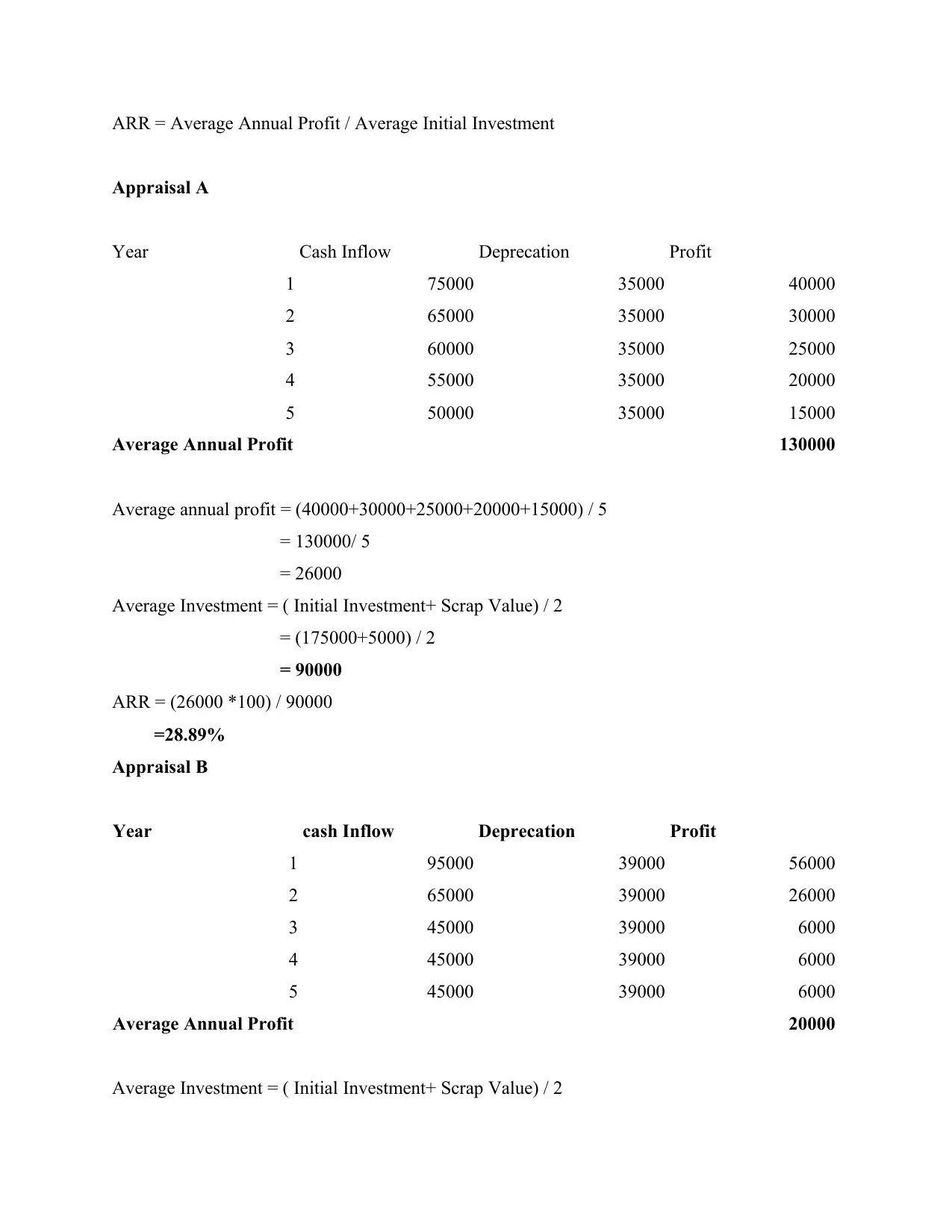

ARR = Average Annual Profit / Average Initial Investment

Appraisal A

Year Cash Inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average Annual Profit 130000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

= 26000

Average Investment = ( Initial Investment+ Scrap Value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year cash Inflow Deprecation Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average Annual Profit 20000

Average Investment = ( Initial Investment+ Scrap Value) / 2

Appraisal A

Year Cash Inflow Deprecation Profit

1 75000 35000 40000

2 65000 35000 30000

3 60000 35000 25000

4 55000 35000 20000

5 50000 35000 15000

Average Annual Profit 130000

Average annual profit = (40000+30000+25000+20000+15000) / 5

= 130000/ 5

= 26000

Average Investment = ( Initial Investment+ Scrap Value) / 2

= (175000+5000) / 2

= 90000

ARR = (26000 *100) / 90000

=28.89%

Appraisal B

Year cash Inflow Deprecation Profit

1 95000 39000 56000

2 65000 39000 26000

3 45000 39000 6000

4 45000 39000 6000

5 45000 39000 6000

Average Annual Profit 20000

Average Investment = ( Initial Investment+ Scrap Value) / 2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= (195000+8000) / 2

= 101500

ARR = (20000*100) / 101500

=19.70%

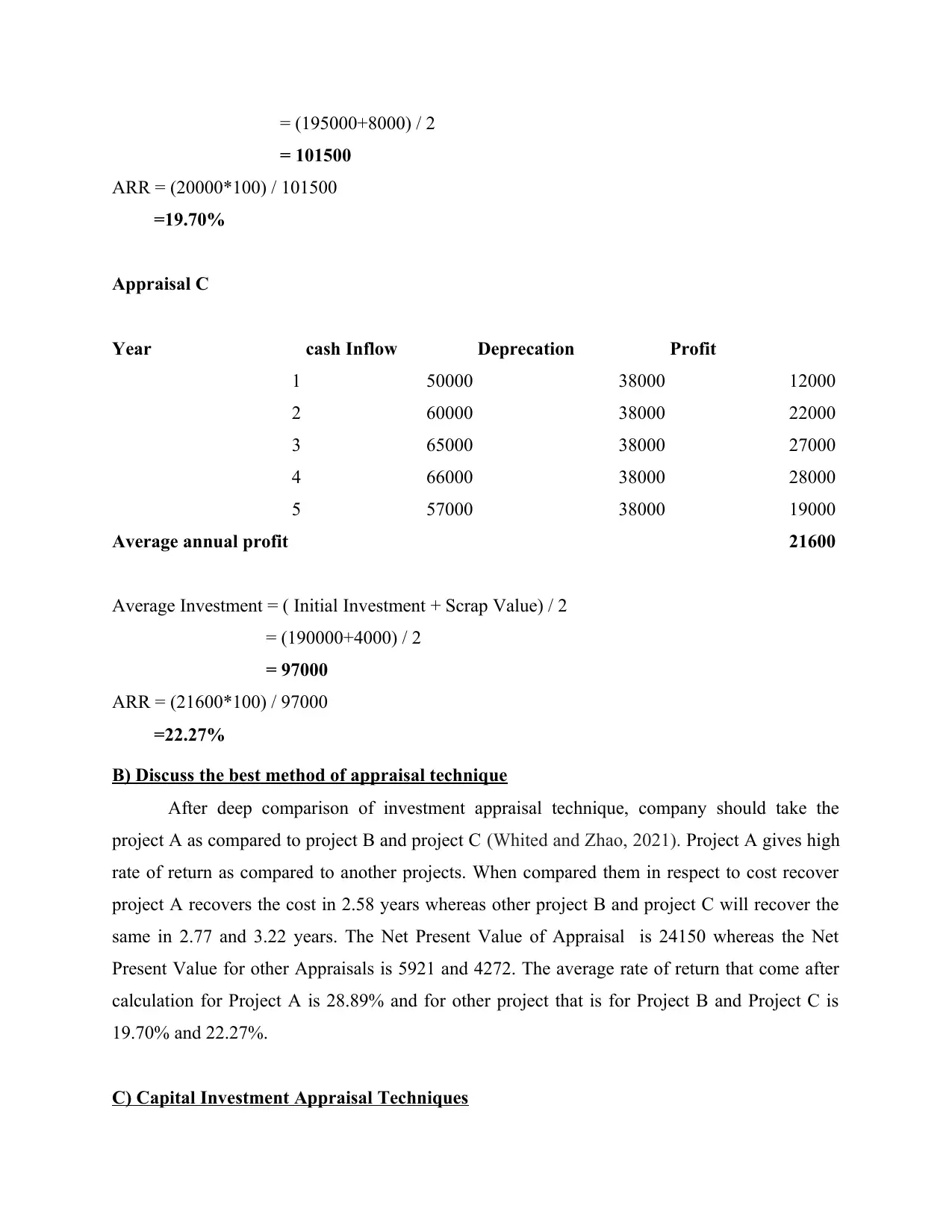

Appraisal C

Year cash Inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average annual profit 21600

Average Investment = ( Initial Investment + Scrap Value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

B) Discuss the best method of appraisal technique

After deep comparison of investment appraisal technique, company should take the

project A as compared to project B and project C (Whited and Zhao, 2021). Project A gives high

rate of return as compared to another projects. When compared them in respect to cost recover

project A recovers the cost in 2.58 years whereas other project B and project C will recover the

same in 2.77 and 3.22 years. The Net Present Value of Appraisal is 24150 whereas the Net

Present Value for other Appraisals is 5921 and 4272. The average rate of return that come after

calculation for Project A is 28.89% and for other project that is for Project B and Project C is

19.70% and 22.27%.

C) Capital Investment Appraisal Techniques

= 101500

ARR = (20000*100) / 101500

=19.70%

Appraisal C

Year cash Inflow Deprecation Profit

1 50000 38000 12000

2 60000 38000 22000

3 65000 38000 27000

4 66000 38000 28000

5 57000 38000 19000

Average annual profit 21600

Average Investment = ( Initial Investment + Scrap Value) / 2

= (190000+4000) / 2

= 97000

ARR = (21600*100) / 97000

=22.27%

B) Discuss the best method of appraisal technique

After deep comparison of investment appraisal technique, company should take the

project A as compared to project B and project C (Whited and Zhao, 2021). Project A gives high

rate of return as compared to another projects. When compared them in respect to cost recover

project A recovers the cost in 2.58 years whereas other project B and project C will recover the

same in 2.77 and 3.22 years. The Net Present Value of Appraisal is 24150 whereas the Net

Present Value for other Appraisals is 5921 and 4272. The average rate of return that come after

calculation for Project A is 28.89% and for other project that is for Project B and Project C is

19.70% and 22.27%.

C) Capital Investment Appraisal Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

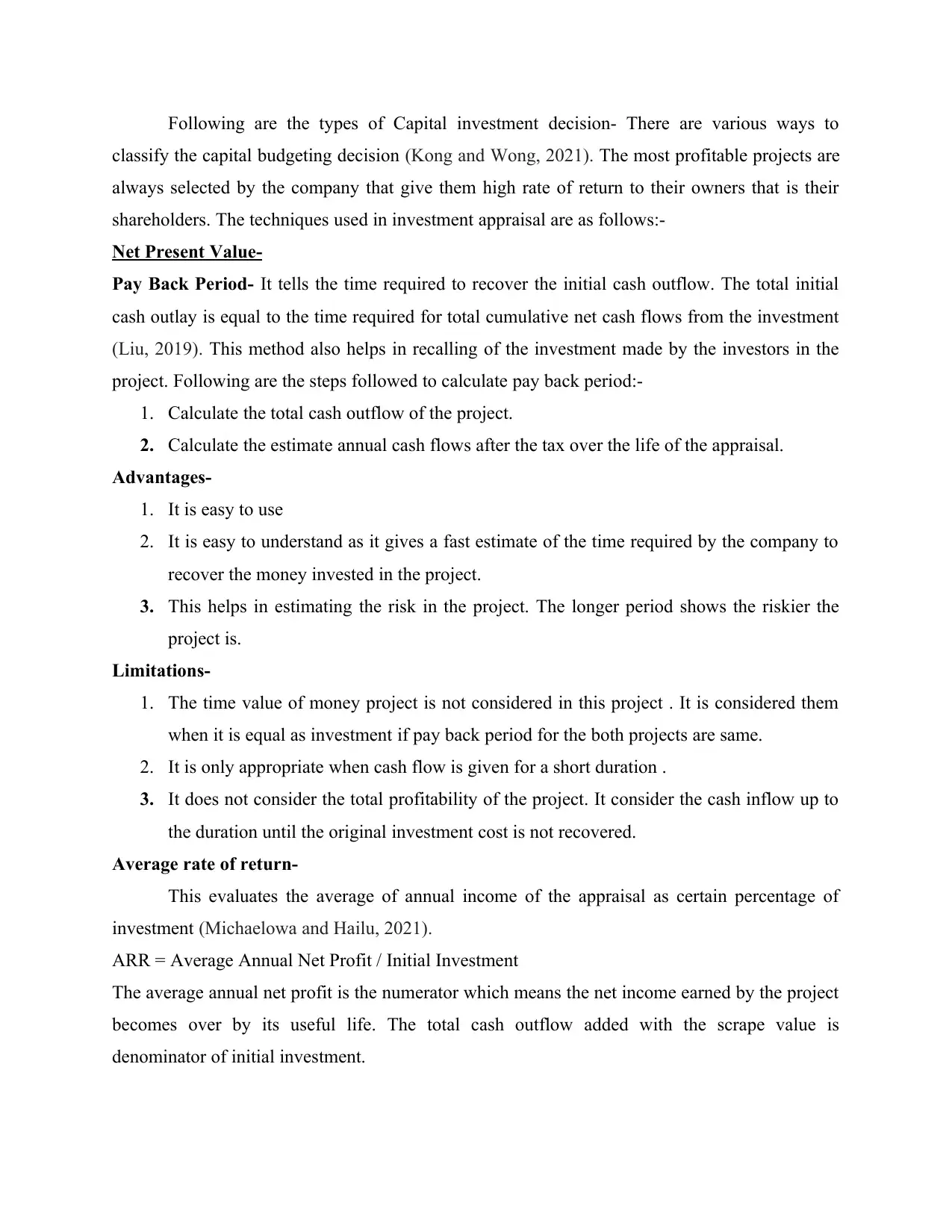

Following are the types of Capital investment decision- There are various ways to

classify the capital budgeting decision (Kong and Wong, 2021). The most profitable projects are

always selected by the company that give them high rate of return to their owners that is their

shareholders. The techniques used in investment appraisal are as follows:-

Net Present Value-

Pay Back Period- It tells the time required to recover the initial cash outflow. The total initial

cash outlay is equal to the time required for total cumulative net cash flows from the investment

(Liu, 2019). This method also helps in recalling of the investment made by the investors in the

project. Following are the steps followed to calculate pay back period:-

1. Calculate the total cash outflow of the project.

2. Calculate the estimate annual cash flows after the tax over the life of the appraisal.

Advantages-

1. It is easy to use

2. It is easy to understand as it gives a fast estimate of the time required by the company to

recover the money invested in the project.

3. This helps in estimating the risk in the project. The longer period shows the riskier the

project is.

Limitations-

1. The time value of money project is not considered in this project . It is considered them

when it is equal as investment if pay back period for the both projects are same.

2. It is only appropriate when cash flow is given for a short duration .

3. It does not consider the total profitability of the project. It consider the cash inflow up to

the duration until the original investment cost is not recovered.

Average rate of return-

This evaluates the average of annual income of the appraisal as certain percentage of

investment (Michaelowa and Hailu, 2021).

ARR = Average Annual Net Profit / Initial Investment

The average annual net profit is the numerator which means the net income earned by the project

becomes over by its useful life. The total cash outflow added with the scrape value is

denominator of initial investment.

classify the capital budgeting decision (Kong and Wong, 2021). The most profitable projects are

always selected by the company that give them high rate of return to their owners that is their

shareholders. The techniques used in investment appraisal are as follows:-

Net Present Value-

Pay Back Period- It tells the time required to recover the initial cash outflow. The total initial

cash outlay is equal to the time required for total cumulative net cash flows from the investment

(Liu, 2019). This method also helps in recalling of the investment made by the investors in the

project. Following are the steps followed to calculate pay back period:-

1. Calculate the total cash outflow of the project.

2. Calculate the estimate annual cash flows after the tax over the life of the appraisal.

Advantages-

1. It is easy to use

2. It is easy to understand as it gives a fast estimate of the time required by the company to

recover the money invested in the project.

3. This helps in estimating the risk in the project. The longer period shows the riskier the

project is.

Limitations-

1. The time value of money project is not considered in this project . It is considered them

when it is equal as investment if pay back period for the both projects are same.

2. It is only appropriate when cash flow is given for a short duration .

3. It does not consider the total profitability of the project. It consider the cash inflow up to

the duration until the original investment cost is not recovered.

Average rate of return-

This evaluates the average of annual income of the appraisal as certain percentage of

investment (Michaelowa and Hailu, 2021).

ARR = Average Annual Net Profit / Initial Investment

The average annual net profit is the numerator which means the net income earned by the project

becomes over by its useful life. The total cash outflow added with the scrape value is

denominator of initial investment.

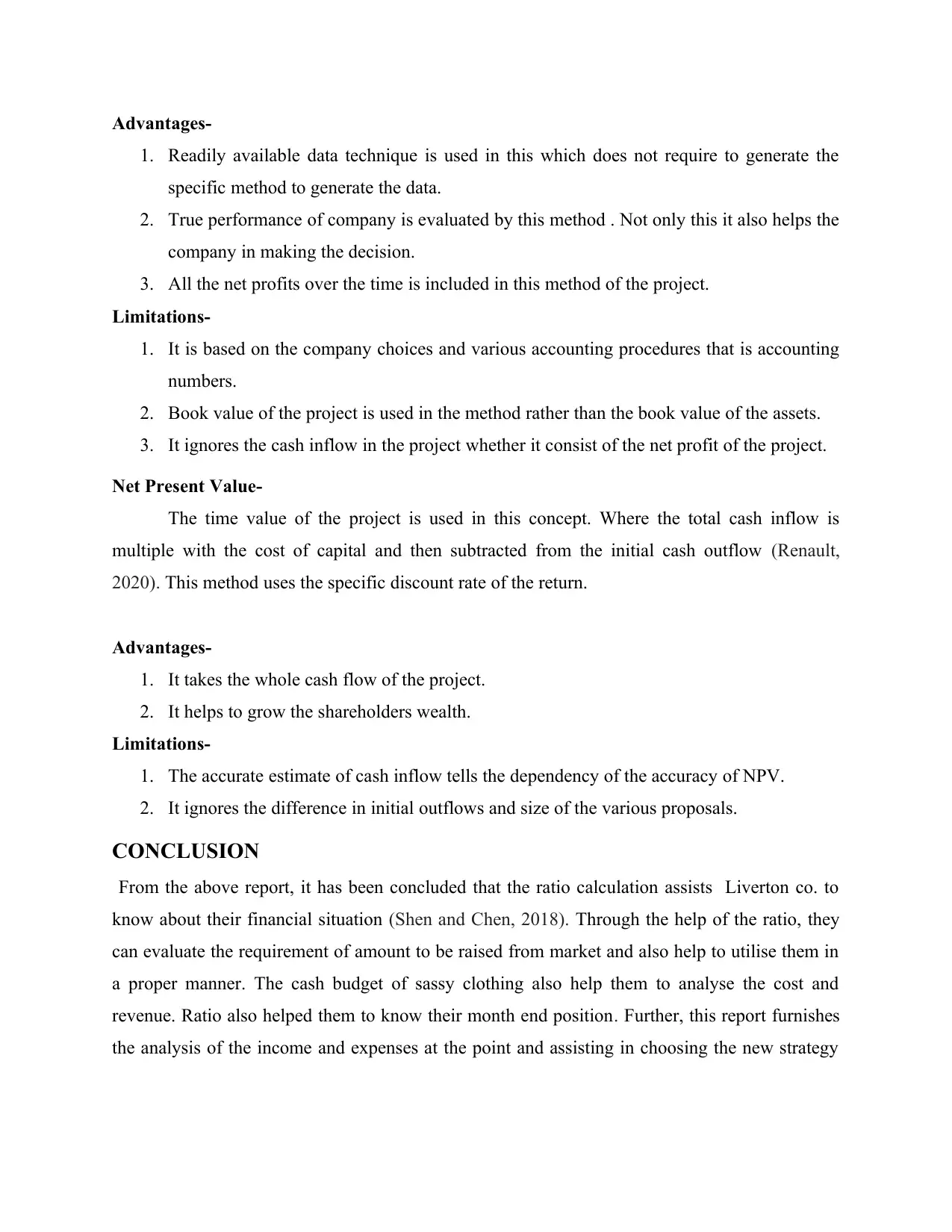

Advantages-

1. Readily available data technique is used in this which does not require to generate the

specific method to generate the data.

2. True performance of company is evaluated by this method . Not only this it also helps the

company in making the decision.

3. All the net profits over the time is included in this method of the project.

Limitations-

1. It is based on the company choices and various accounting procedures that is accounting

numbers.

2. Book value of the project is used in the method rather than the book value of the assets.

3. It ignores the cash inflow in the project whether it consist of the net profit of the project.

Net Present Value-

The time value of the project is used in this concept. Where the total cash inflow is

multiple with the cost of capital and then subtracted from the initial cash outflow (Renault,

2020). This method uses the specific discount rate of the return.

Advantages-

1. It takes the whole cash flow of the project.

2. It helps to grow the shareholders wealth.

Limitations-

1. The accurate estimate of cash inflow tells the dependency of the accuracy of NPV.

2. It ignores the difference in initial outflows and size of the various proposals.

CONCLUSION

From the above report, it has been concluded that the ratio calculation assists Liverton co. to

know about their financial situation (Shen and Chen, 2018). Through the help of the ratio, they

can evaluate the requirement of amount to be raised from market and also help to utilise them in

a proper manner. The cash budget of sassy clothing also help them to analyse the cost and

revenue. Ratio also helped them to know their month end position. Further, this report furnishes

the analysis of the income and expenses at the point and assisting in choosing the new strategy

1. Readily available data technique is used in this which does not require to generate the

specific method to generate the data.

2. True performance of company is evaluated by this method . Not only this it also helps the

company in making the decision.

3. All the net profits over the time is included in this method of the project.

Limitations-

1. It is based on the company choices and various accounting procedures that is accounting

numbers.

2. Book value of the project is used in the method rather than the book value of the assets.

3. It ignores the cash inflow in the project whether it consist of the net profit of the project.

Net Present Value-

The time value of the project is used in this concept. Where the total cash inflow is

multiple with the cost of capital and then subtracted from the initial cash outflow (Renault,

2020). This method uses the specific discount rate of the return.

Advantages-

1. It takes the whole cash flow of the project.

2. It helps to grow the shareholders wealth.

Limitations-

1. The accurate estimate of cash inflow tells the dependency of the accuracy of NPV.

2. It ignores the difference in initial outflows and size of the various proposals.

CONCLUSION

From the above report, it has been concluded that the ratio calculation assists Liverton co. to

know about their financial situation (Shen and Chen, 2018). Through the help of the ratio, they

can evaluate the requirement of amount to be raised from market and also help to utilise them in

a proper manner. The cash budget of sassy clothing also help them to analyse the cost and

revenue. Ratio also helped them to know their month end position. Further, this report furnishes

the analysis of the income and expenses at the point and assisting in choosing the new strategy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which they require and minimise the financial threats. In the end this tells that the investment

decisions are too crucial for opting the best forecast for the particular investment.

decisions are too crucial for opting the best forecast for the particular investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Broadstock, D. C. and Cheng, L. T., 2019. Time-varying relation between black and green bond

price benchmarks: Macroeconomic determinants for the first decade. Finance research

letters. 29. pp.17-22.

Dewick, P. and Schröder, P., 2020. Circular economy finance: Clear winner or risky

proposition?. Journal of industrial Ecology. 24(6), pp.1192-1200

Dymski, G. A., 2018. US housing as capital accumulation: the transformation of American

housing finance, households, and communities. In Seeking Shelter on the Pacific Rim

(pp. 63-96).

Epstein, G., 2018. On the social efficiency of finance. Development and Change. 49(2). pp.330-

352.

Helgesson, K. S. and Mörth, U., 2019. Instruments of securitization and resisting subjects: For-

profit professionals in the finance–security nexus. Security Dialogue. 50(3). pp.257-274.

Jones, W. A., 2020. A Benford Analysis of National Collegiate Athletic Association Division I

Finance Data. Journal of Sports Economics. 21(3). pp.234-255.

Kong, Q., and Wong, Z., 2021. High-speed railway opening and urban green productivity in the

post-COVID-19: Evidence from green finance. Global Finance Journal. 49. p.100645.

Liu, C., 2019. Finance strategies for medium-sized enterprises: Fintech as the game changer.

In Strategic Optimization of Medium-Sized Enterprises in the Global Market (pp. 162-

184).

Michaelowa, A., and Hailu, T., 2021. Mobilising private climate finance for sustainable energy

access and climate change mitigation in Sub-Saharan Africa. Climate Policy. 21(1).

pp.47-62.

Renault, T., 2020. Sentiment analysis and machine learning in finance: a comparison of methods

and models on one million messages. Digital Finance. 2(1). pp.1-13.

Shen, D. and Chen, S. H., 2018. Big data finance and financial markets. In Big Data in

Computational Social Science and Humanities (pp. 235-248).

Swamy, V. and Dharani, M., 2021. Thresholds in finance–growth nexus: Evidence from G 7‐

economies. Australian Economic Papers. 60(1). pp.1-40.

Whited, T. M. and Zhao, J., 2021. The misallocation of finance. The Journal of Finance. 76(5).

pp.2359-2407.

Zhang, D., Mohsin, M. and Taghizadeh-Hesary, F., 2022. Does green finance counteract the

climate change mitigation: asymmetric effect of renewable energy investment and

R&D. Energy Economics. 113. p.106183.

Books and Journals

Broadstock, D. C. and Cheng, L. T., 2019. Time-varying relation between black and green bond

price benchmarks: Macroeconomic determinants for the first decade. Finance research

letters. 29. pp.17-22.

Dewick, P. and Schröder, P., 2020. Circular economy finance: Clear winner or risky

proposition?. Journal of industrial Ecology. 24(6), pp.1192-1200

Dymski, G. A., 2018. US housing as capital accumulation: the transformation of American

housing finance, households, and communities. In Seeking Shelter on the Pacific Rim

(pp. 63-96).

Epstein, G., 2018. On the social efficiency of finance. Development and Change. 49(2). pp.330-

352.

Helgesson, K. S. and Mörth, U., 2019. Instruments of securitization and resisting subjects: For-

profit professionals in the finance–security nexus. Security Dialogue. 50(3). pp.257-274.

Jones, W. A., 2020. A Benford Analysis of National Collegiate Athletic Association Division I

Finance Data. Journal of Sports Economics. 21(3). pp.234-255.

Kong, Q., and Wong, Z., 2021. High-speed railway opening and urban green productivity in the

post-COVID-19: Evidence from green finance. Global Finance Journal. 49. p.100645.

Liu, C., 2019. Finance strategies for medium-sized enterprises: Fintech as the game changer.

In Strategic Optimization of Medium-Sized Enterprises in the Global Market (pp. 162-

184).

Michaelowa, A., and Hailu, T., 2021. Mobilising private climate finance for sustainable energy

access and climate change mitigation in Sub-Saharan Africa. Climate Policy. 21(1).

pp.47-62.

Renault, T., 2020. Sentiment analysis and machine learning in finance: a comparison of methods

and models on one million messages. Digital Finance. 2(1). pp.1-13.

Shen, D. and Chen, S. H., 2018. Big data finance and financial markets. In Big Data in

Computational Social Science and Humanities (pp. 235-248).

Swamy, V. and Dharani, M., 2021. Thresholds in finance–growth nexus: Evidence from G 7‐

economies. Australian Economic Papers. 60(1). pp.1-40.

Whited, T. M. and Zhao, J., 2021. The misallocation of finance. The Journal of Finance. 76(5).

pp.2359-2407.

Zhang, D., Mohsin, M. and Taghizadeh-Hesary, F., 2022. Does green finance counteract the

climate change mitigation: asymmetric effect of renewable energy investment and

R&D. Energy Economics. 113. p.106183.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.