Financial Analysis: EOQ, Investment Appraisal, Ratios & Governance

VerifiedAdded on 2023/06/17

|15

|4054

|364

Report

AI Summary

This report provides a comprehensive analysis of various financial techniques, including Economic Order Quantity (EOQ) for inventory management, investment appraisal methods such as payback period and Accounting Rate of Return (ARR), and financial ratio analysis for performance evaluation. It critically evaluates the EOQ model and Just-In-Time (JIT) approach for inventory management, offering recommendations for their implementation. The report also advises on investment decisions, comparing options using payback period and ARR, and discusses the advantages and disadvantages of different investment appraisal techniques. Furthermore, it explores the role of organizations in the international regulatory framework for accounting and the role of the audit committee in corporate governance. This analysis aims to provide a thorough understanding of financial management principles and their practical applications.

INTRODUCTION TO

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

(a) Calculation of Economic Order Quantity (EOQ) of hard plastic..........................................3

(b) Calculation of total annual cost of hard plastic.....................................................................3

(c) Critical evaluation of EOQ model as a part of Inventories management..............................4

(d)................................................................................................................................................4

QUESTION: 2.................................................................................................................................5

a. Calculation of payback period for option A and option B......................................................5

b. Calculation of Accounting rate of return for Option A and Option B....................................6

c. Critical evaluation of Accounting Rate of Return technique..................................................8

d. Advising senior executive team over the comments made.....................................................8

QUESTION 3...................................................................................................................................9

(a) Calculation of Financial Ratios.............................................................................................9

(b)..............................................................................................................................................11

QUESTION: 4...............................................................................................................................12

a. Role of organizations in the International regulatory framework for accounting.................12

b. Role of audit committee in corporate governance................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

(a) Calculation of Economic Order Quantity (EOQ) of hard plastic..........................................3

(b) Calculation of total annual cost of hard plastic.....................................................................3

(c) Critical evaluation of EOQ model as a part of Inventories management..............................4

(d)................................................................................................................................................4

QUESTION: 2.................................................................................................................................5

a. Calculation of payback period for option A and option B......................................................5

b. Calculation of Accounting rate of return for Option A and Option B....................................6

c. Critical evaluation of Accounting Rate of Return technique..................................................8

d. Advising senior executive team over the comments made.....................................................8

QUESTION 3...................................................................................................................................9

(a) Calculation of Financial Ratios.............................................................................................9

(b)..............................................................................................................................................11

QUESTION: 4...............................................................................................................................12

a. Role of organizations in the International regulatory framework for accounting.................12

b. Role of audit committee in corporate governance................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

In the present report, various financial techniques will be applied that is useful in

different circumstances such inventory management techniques, investment appraisal techniques

and ratio analysis technique for performance evaluation. Also, discussion pertaining to corporate

governance has been done by highlighting the role of different international regulatory

framework for accounting and audit committee.

QUESTION 1

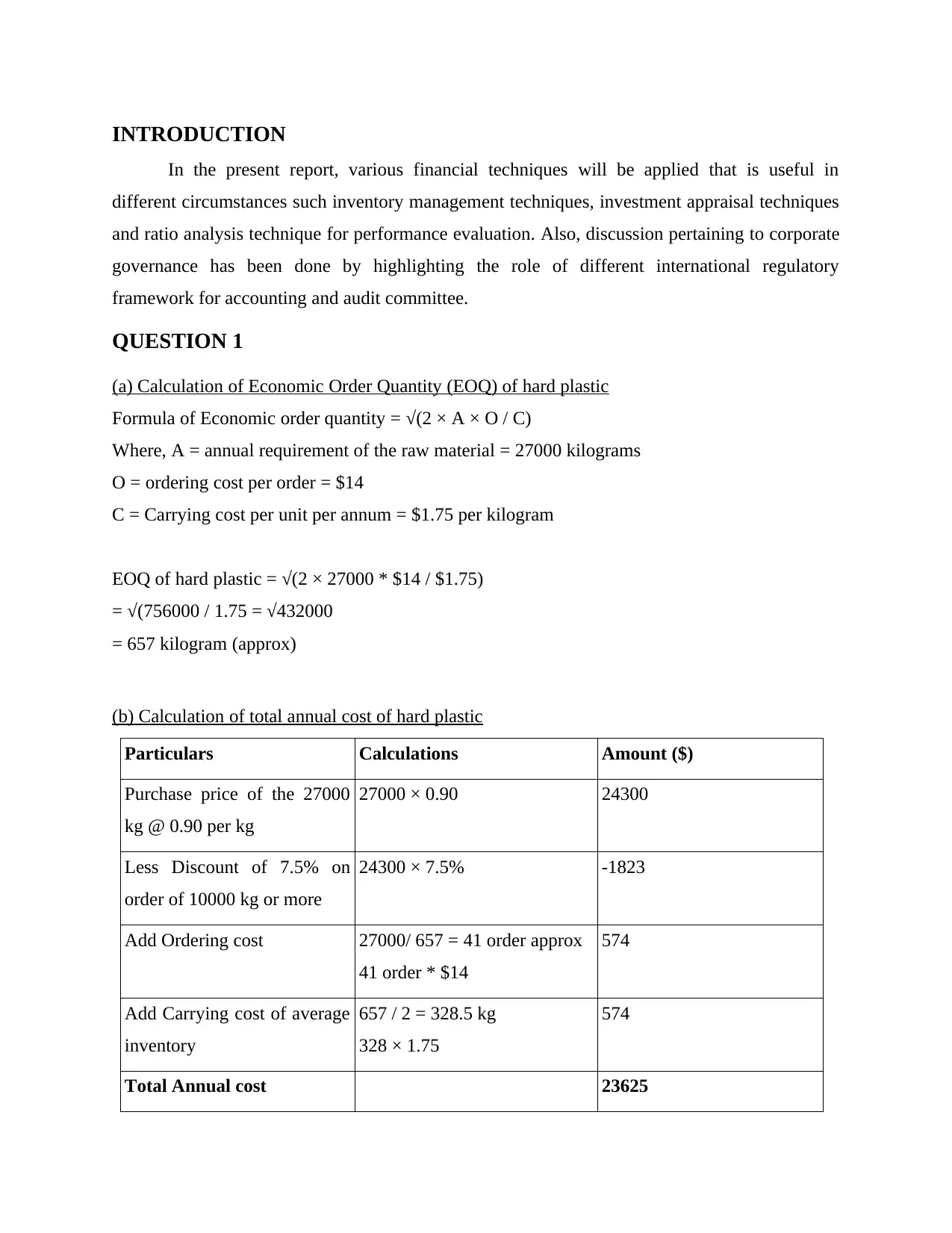

(a) Calculation of Economic Order Quantity (EOQ) of hard plastic

Formula of Economic order quantity = √(2 × A × O / C)

Where, A = annual requirement of the raw material = 27000 kilograms

O = ordering cost per order = $14

C = Carrying cost per unit per annum = $1.75 per kilogram

EOQ of hard plastic = √(2 × 27000 * $14 / $1.75)

= √(756000 / 1.75 = √432000

= 657 kilogram (approx)

(b) Calculation of total annual cost of hard plastic

Particulars Calculations Amount ($)

Purchase price of the 27000

kg @ 0.90 per kg

27000 × 0.90 24300

Less Discount of 7.5% on

order of 10000 kg or more

24300 × 7.5% -1823

Add Ordering cost 27000/ 657 = 41 order approx

41 order * $14

574

Add Carrying cost of average

inventory

657 / 2 = 328.5 kg

328 × 1.75

574

Total Annual cost 23625

In the present report, various financial techniques will be applied that is useful in

different circumstances such inventory management techniques, investment appraisal techniques

and ratio analysis technique for performance evaluation. Also, discussion pertaining to corporate

governance has been done by highlighting the role of different international regulatory

framework for accounting and audit committee.

QUESTION 1

(a) Calculation of Economic Order Quantity (EOQ) of hard plastic

Formula of Economic order quantity = √(2 × A × O / C)

Where, A = annual requirement of the raw material = 27000 kilograms

O = ordering cost per order = $14

C = Carrying cost per unit per annum = $1.75 per kilogram

EOQ of hard plastic = √(2 × 27000 * $14 / $1.75)

= √(756000 / 1.75 = √432000

= 657 kilogram (approx)

(b) Calculation of total annual cost of hard plastic

Particulars Calculations Amount ($)

Purchase price of the 27000

kg @ 0.90 per kg

27000 × 0.90 24300

Less Discount of 7.5% on

order of 10000 kg or more

24300 × 7.5% -1823

Add Ordering cost 27000/ 657 = 41 order approx

41 order * $14

574

Add Carrying cost of average

inventory

657 / 2 = 328.5 kg

328 × 1.75

574

Total Annual cost 23625

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

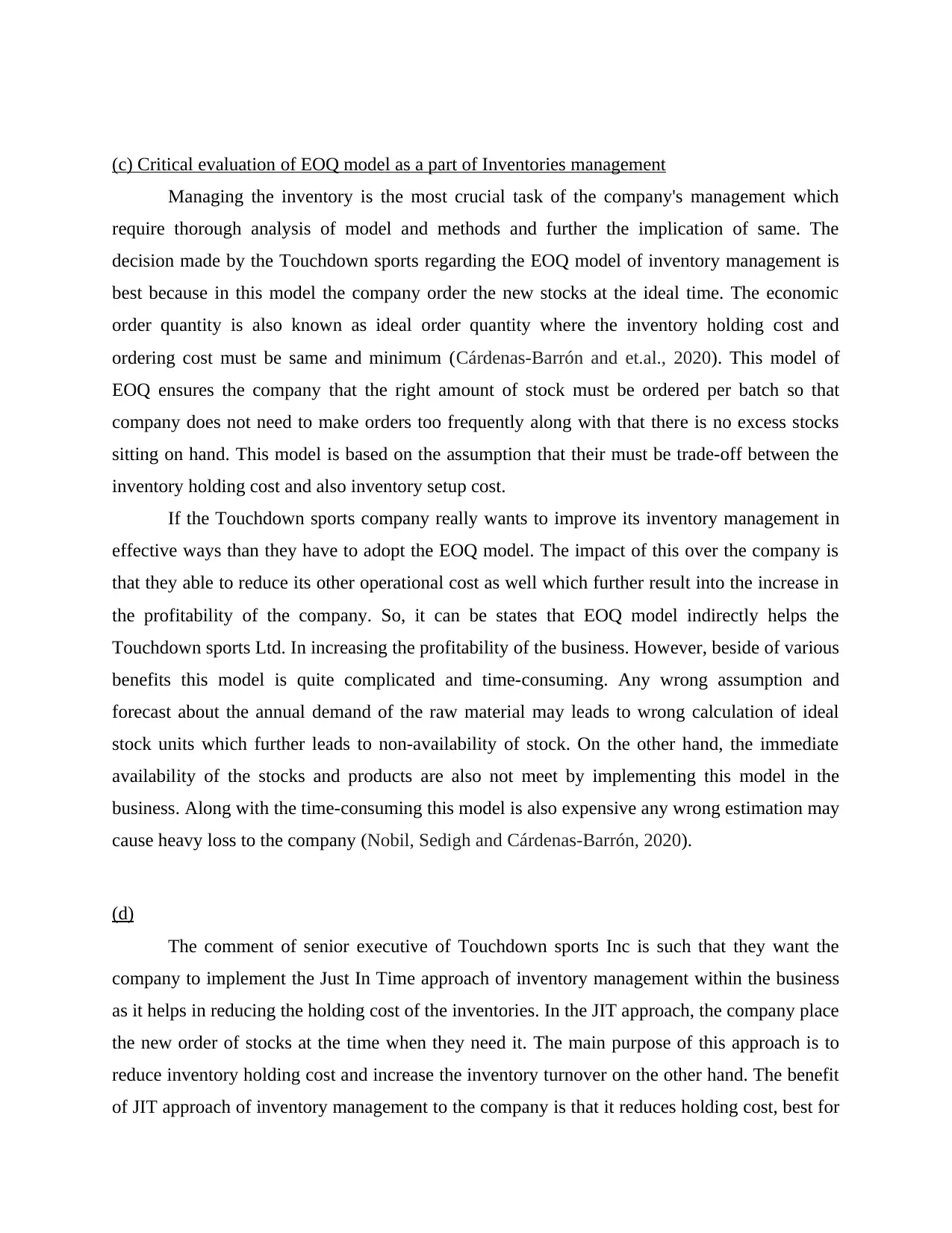

(c) Critical evaluation of EOQ model as a part of Inventories management

Managing the inventory is the most crucial task of the company's management which

require thorough analysis of model and methods and further the implication of same. The

decision made by the Touchdown sports regarding the EOQ model of inventory management is

best because in this model the company order the new stocks at the ideal time. The economic

order quantity is also known as ideal order quantity where the inventory holding cost and

ordering cost must be same and minimum (Cárdenas-Barrón and et.al., 2020). This model of

EOQ ensures the company that the right amount of stock must be ordered per batch so that

company does not need to make orders too frequently along with that there is no excess stocks

sitting on hand. This model is based on the assumption that their must be trade-off between the

inventory holding cost and also inventory setup cost.

If the Touchdown sports company really wants to improve its inventory management in

effective ways than they have to adopt the EOQ model. The impact of this over the company is

that they able to reduce its other operational cost as well which further result into the increase in

the profitability of the company. So, it can be states that EOQ model indirectly helps the

Touchdown sports Ltd. In increasing the profitability of the business. However, beside of various

benefits this model is quite complicated and time-consuming. Any wrong assumption and

forecast about the annual demand of the raw material may leads to wrong calculation of ideal

stock units which further leads to non-availability of stock. On the other hand, the immediate

availability of the stocks and products are also not meet by implementing this model in the

business. Along with the time-consuming this model is also expensive any wrong estimation may

cause heavy loss to the company (Nobil, Sedigh and Cárdenas-Barrón, 2020).

(d)

The comment of senior executive of Touchdown sports Inc is such that they want the

company to implement the Just In Time approach of inventory management within the business

as it helps in reducing the holding cost of the inventories. In the JIT approach, the company place

the new order of stocks at the time when they need it. The main purpose of this approach is to

reduce inventory holding cost and increase the inventory turnover on the other hand. The benefit

of JIT approach of inventory management to the company is that it reduces holding cost, best for

Managing the inventory is the most crucial task of the company's management which

require thorough analysis of model and methods and further the implication of same. The

decision made by the Touchdown sports regarding the EOQ model of inventory management is

best because in this model the company order the new stocks at the ideal time. The economic

order quantity is also known as ideal order quantity where the inventory holding cost and

ordering cost must be same and minimum (Cárdenas-Barrón and et.al., 2020). This model of

EOQ ensures the company that the right amount of stock must be ordered per batch so that

company does not need to make orders too frequently along with that there is no excess stocks

sitting on hand. This model is based on the assumption that their must be trade-off between the

inventory holding cost and also inventory setup cost.

If the Touchdown sports company really wants to improve its inventory management in

effective ways than they have to adopt the EOQ model. The impact of this over the company is

that they able to reduce its other operational cost as well which further result into the increase in

the profitability of the company. So, it can be states that EOQ model indirectly helps the

Touchdown sports Ltd. In increasing the profitability of the business. However, beside of various

benefits this model is quite complicated and time-consuming. Any wrong assumption and

forecast about the annual demand of the raw material may leads to wrong calculation of ideal

stock units which further leads to non-availability of stock. On the other hand, the immediate

availability of the stocks and products are also not meet by implementing this model in the

business. Along with the time-consuming this model is also expensive any wrong estimation may

cause heavy loss to the company (Nobil, Sedigh and Cárdenas-Barrón, 2020).

(d)

The comment of senior executive of Touchdown sports Inc is such that they want the

company to implement the Just In Time approach of inventory management within the business

as it helps in reducing the holding cost of the inventories. In the JIT approach, the company place

the new order of stocks at the time when they need it. The main purpose of this approach is to

reduce inventory holding cost and increase the inventory turnover on the other hand. The benefit

of JIT approach of inventory management to the company is that it reduces holding cost, best for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

waste elimination or reduction along with is also best for smaller investment. But on the other

hand, implementation of this approach at the time of high demand of products will cause risk of

running out of stock. It is because their can be delay arises in the stock receivables which further

leads to delay in production of products and the delivery of same to the ultimate customers (Liu

and et.al., 2020). The risk of over dependency on the supplier for the stocks order is also arises

which leads to delay in the fulfilment of customers expectations. It also required more planning

of stock demands.

On the basis of above analysis of the JIT approach, it is advisable to the Touchdown

Sports Inc. that they have to adopt and implement the Just in Time approach within the business

at the time of low demand or average demand of shoulder pad and other sports equipment. But in

the month of July, August, September and December it is advisable to the company that they

have to continue with the EOQ model only. It helps the company in reducing the unnecessary

holding cost and wastage of hard plastic (Yan and et.al., 2020). While on the other hand, it is

also best for meeting the high demand of products in peak time.

QUESTION: 2

a. Calculation of payback period for option A and option B

Calculation of Payback Period for Option A

Year Cash flows Cumulative cash flows

Initial Investment -51000

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 43010 55610

From the above calculations, the payback period for the option A would be as follows:

4 years + [(51000 – 12600 / 43010) × 12]

= 4 + 0.8 = 4.8 years or 4 years and 8 months.

hand, implementation of this approach at the time of high demand of products will cause risk of

running out of stock. It is because their can be delay arises in the stock receivables which further

leads to delay in production of products and the delivery of same to the ultimate customers (Liu

and et.al., 2020). The risk of over dependency on the supplier for the stocks order is also arises

which leads to delay in the fulfilment of customers expectations. It also required more planning

of stock demands.

On the basis of above analysis of the JIT approach, it is advisable to the Touchdown

Sports Inc. that they have to adopt and implement the Just in Time approach within the business

at the time of low demand or average demand of shoulder pad and other sports equipment. But in

the month of July, August, September and December it is advisable to the company that they

have to continue with the EOQ model only. It helps the company in reducing the unnecessary

holding cost and wastage of hard plastic (Yan and et.al., 2020). While on the other hand, it is

also best for meeting the high demand of products in peak time.

QUESTION: 2

a. Calculation of payback period for option A and option B

Calculation of Payback Period for Option A

Year Cash flows Cumulative cash flows

Initial Investment -51000

1 3200 3200

2 3300 6500

3 3100 9600

4 3000 12600

5 43010 55610

From the above calculations, the payback period for the option A would be as follows:

4 years + [(51000 – 12600 / 43010) × 12]

= 4 + 0.8 = 4.8 years or 4 years and 8 months.

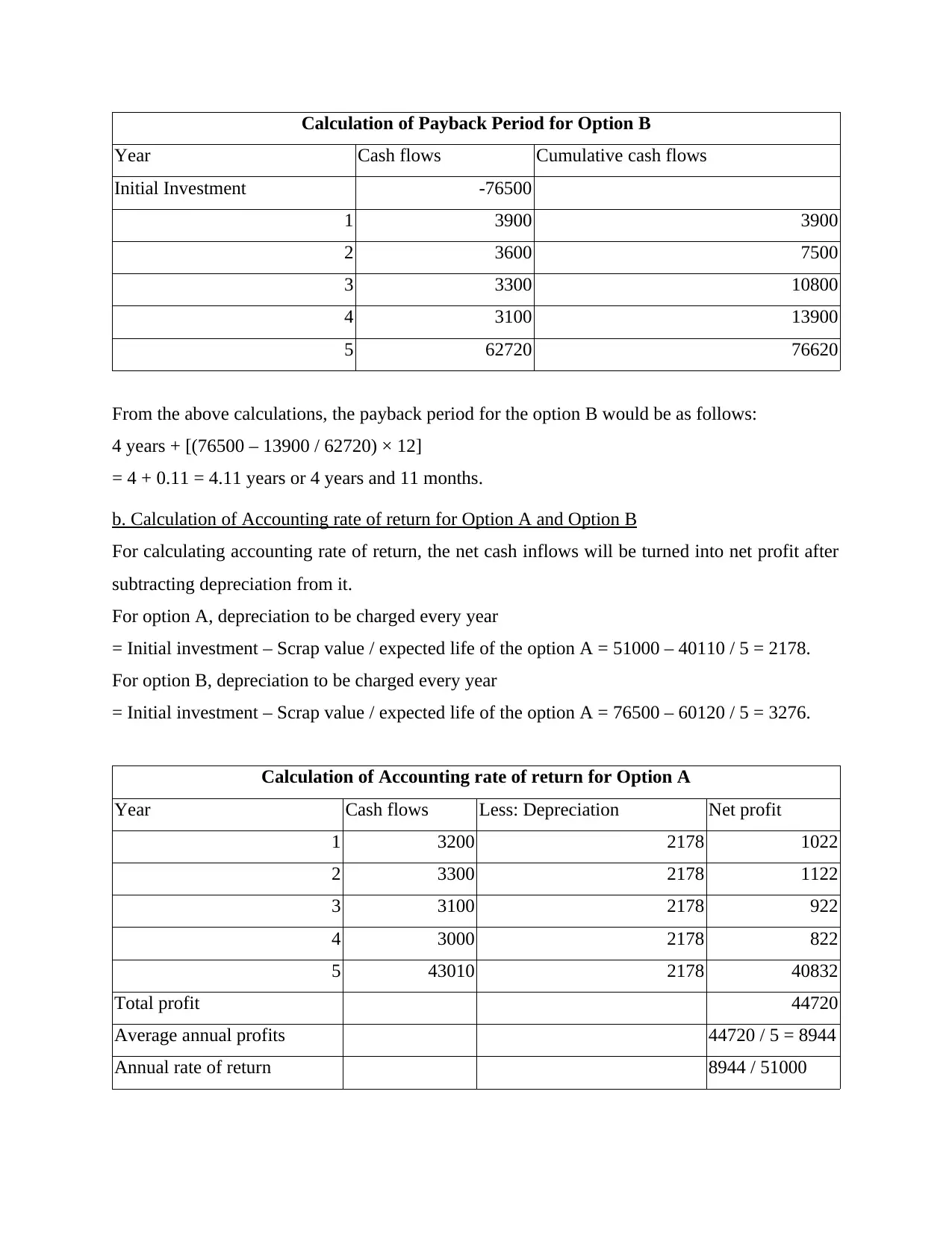

Calculation of Payback Period for Option B

Year Cash flows Cumulative cash flows

Initial Investment -76500

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 62720 76620

From the above calculations, the payback period for the option B would be as follows:

4 years + [(76500 – 13900 / 62720) × 12]

= 4 + 0.11 = 4.11 years or 4 years and 11 months.

b. Calculation of Accounting rate of return for Option A and Option B

For calculating accounting rate of return, the net cash inflows will be turned into net profit after

subtracting depreciation from it.

For option A, depreciation to be charged every year

= Initial investment – Scrap value / expected life of the option A = 51000 – 40110 / 5 = 2178.

For option B, depreciation to be charged every year

= Initial investment – Scrap value / expected life of the option A = 76500 – 60120 / 5 = 3276.

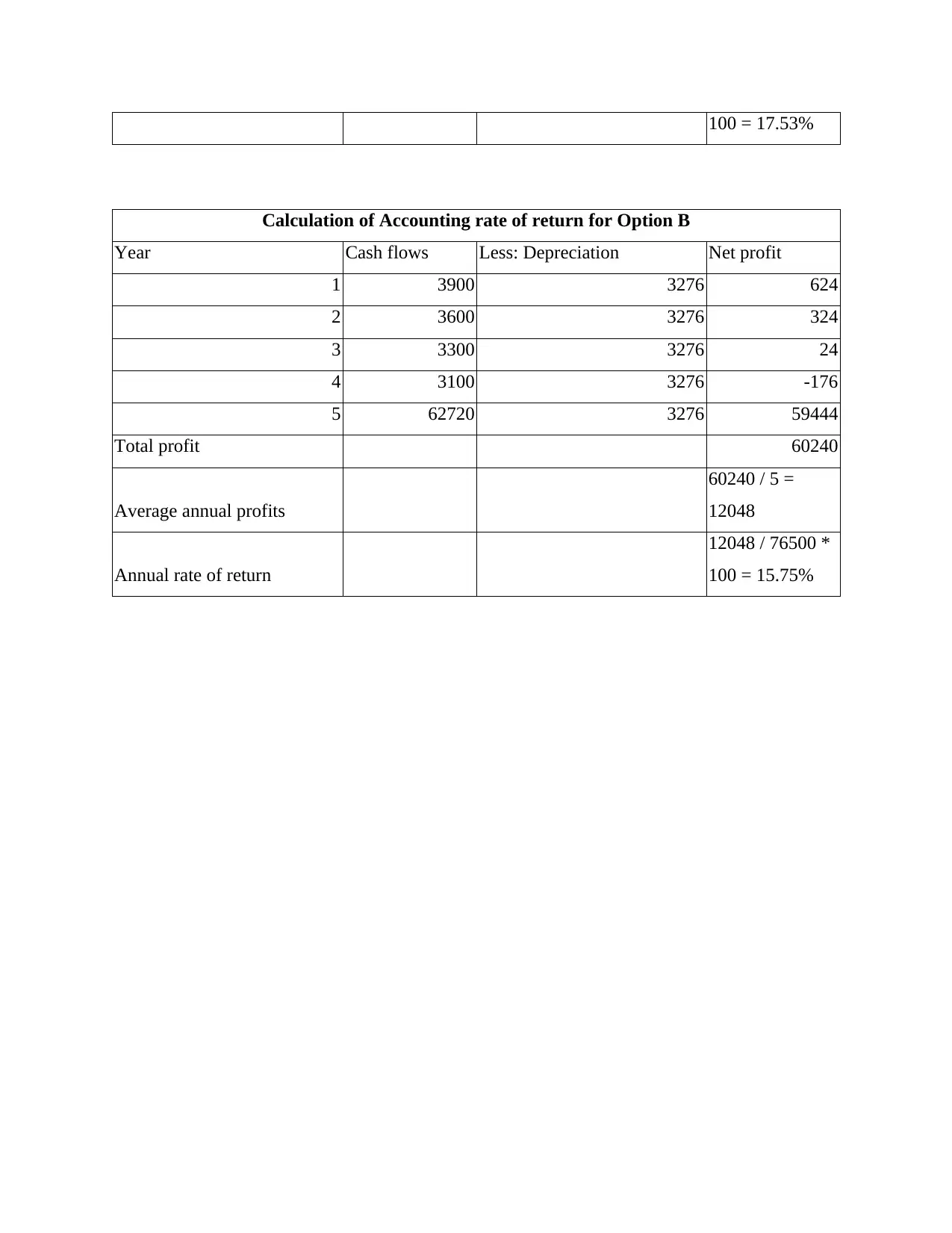

Calculation of Accounting rate of return for Option A

Year Cash flows Less: Depreciation Net profit

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 43010 2178 40832

Total profit 44720

Average annual profits 44720 / 5 = 8944

Annual rate of return 8944 / 51000

Year Cash flows Cumulative cash flows

Initial Investment -76500

1 3900 3900

2 3600 7500

3 3300 10800

4 3100 13900

5 62720 76620

From the above calculations, the payback period for the option B would be as follows:

4 years + [(76500 – 13900 / 62720) × 12]

= 4 + 0.11 = 4.11 years or 4 years and 11 months.

b. Calculation of Accounting rate of return for Option A and Option B

For calculating accounting rate of return, the net cash inflows will be turned into net profit after

subtracting depreciation from it.

For option A, depreciation to be charged every year

= Initial investment – Scrap value / expected life of the option A = 51000 – 40110 / 5 = 2178.

For option B, depreciation to be charged every year

= Initial investment – Scrap value / expected life of the option A = 76500 – 60120 / 5 = 3276.

Calculation of Accounting rate of return for Option A

Year Cash flows Less: Depreciation Net profit

1 3200 2178 1022

2 3300 2178 1122

3 3100 2178 922

4 3000 2178 822

5 43010 2178 40832

Total profit 44720

Average annual profits 44720 / 5 = 8944

Annual rate of return 8944 / 51000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

100 = 17.53%

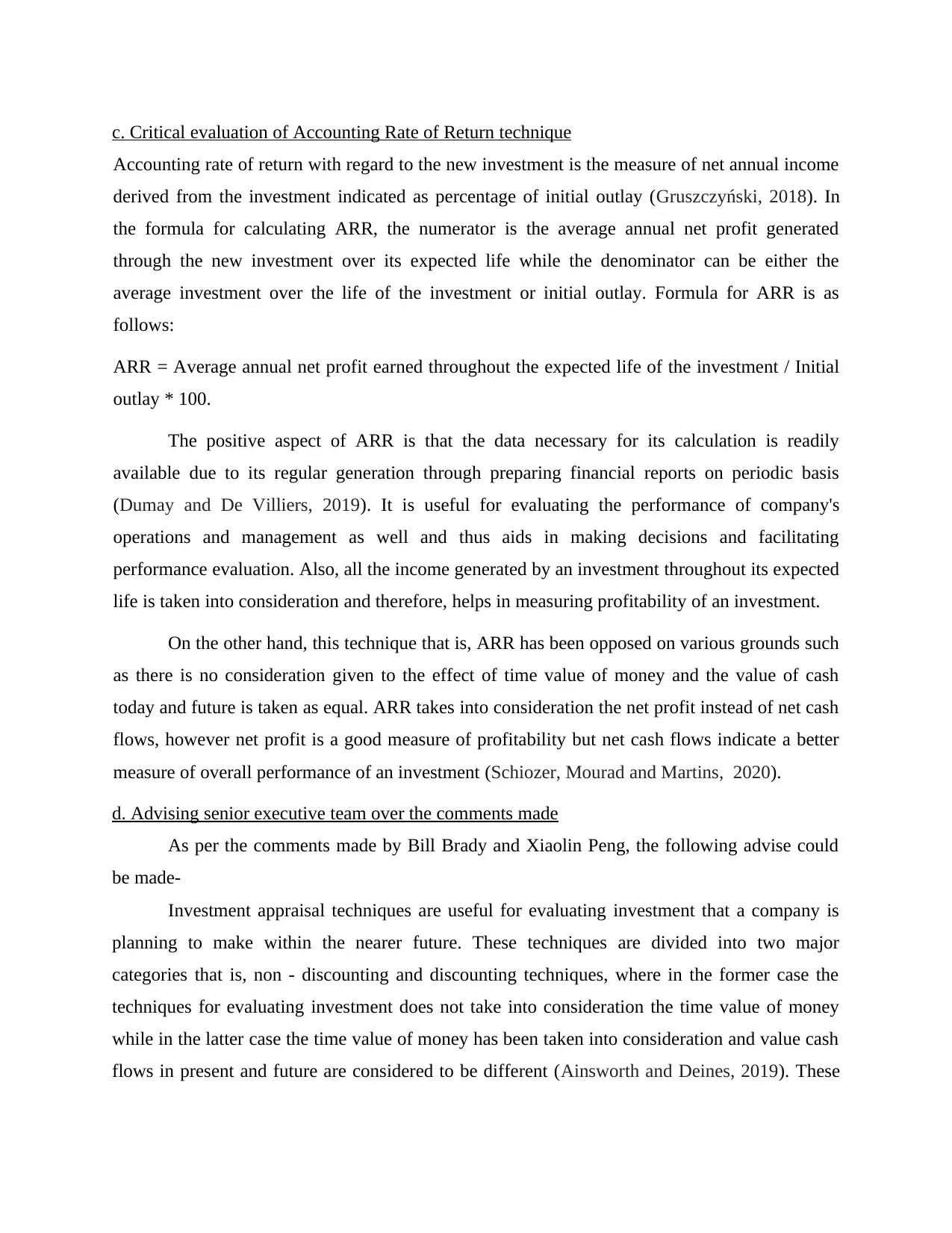

Calculation of Accounting rate of return for Option B

Year Cash flows Less: Depreciation Net profit

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 62720 3276 59444

Total profit 60240

Average annual profits

60240 / 5 =

12048

Annual rate of return

12048 / 76500 *

100 = 15.75%

Calculation of Accounting rate of return for Option B

Year Cash flows Less: Depreciation Net profit

1 3900 3276 624

2 3600 3276 324

3 3300 3276 24

4 3100 3276 -176

5 62720 3276 59444

Total profit 60240

Average annual profits

60240 / 5 =

12048

Annual rate of return

12048 / 76500 *

100 = 15.75%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Critical evaluation of Accounting Rate of Return technique

Accounting rate of return with regard to the new investment is the measure of net annual income

derived from the investment indicated as percentage of initial outlay (Gruszczyński, 2018). In

the formula for calculating ARR, the numerator is the average annual net profit generated

through the new investment over its expected life while the denominator can be either the

average investment over the life of the investment or initial outlay. Formula for ARR is as

follows:

ARR = Average annual net profit earned throughout the expected life of the investment / Initial

outlay * 100.

The positive aspect of ARR is that the data necessary for its calculation is readily

available due to its regular generation through preparing financial reports on periodic basis

(Dumay and De Villiers, 2019). It is useful for evaluating the performance of company's

operations and management as well and thus aids in making decisions and facilitating

performance evaluation. Also, all the income generated by an investment throughout its expected

life is taken into consideration and therefore, helps in measuring profitability of an investment.

On the other hand, this technique that is, ARR has been opposed on various grounds such

as there is no consideration given to the effect of time value of money and the value of cash

today and future is taken as equal. ARR takes into consideration the net profit instead of net cash

flows, however net profit is a good measure of profitability but net cash flows indicate a better

measure of overall performance of an investment (Schiozer, Mourad and Martins, 2020).

d. Advising senior executive team over the comments made

As per the comments made by Bill Brady and Xiaolin Peng, the following advise could

be made-

Investment appraisal techniques are useful for evaluating investment that a company is

planning to make within the nearer future. These techniques are divided into two major

categories that is, non - discounting and discounting techniques, where in the former case the

techniques for evaluating investment does not take into consideration the time value of money

while in the latter case the time value of money has been taken into consideration and value cash

flows in present and future are considered to be different (Ainsworth and Deines, 2019). These

Accounting rate of return with regard to the new investment is the measure of net annual income

derived from the investment indicated as percentage of initial outlay (Gruszczyński, 2018). In

the formula for calculating ARR, the numerator is the average annual net profit generated

through the new investment over its expected life while the denominator can be either the

average investment over the life of the investment or initial outlay. Formula for ARR is as

follows:

ARR = Average annual net profit earned throughout the expected life of the investment / Initial

outlay * 100.

The positive aspect of ARR is that the data necessary for its calculation is readily

available due to its regular generation through preparing financial reports on periodic basis

(Dumay and De Villiers, 2019). It is useful for evaluating the performance of company's

operations and management as well and thus aids in making decisions and facilitating

performance evaluation. Also, all the income generated by an investment throughout its expected

life is taken into consideration and therefore, helps in measuring profitability of an investment.

On the other hand, this technique that is, ARR has been opposed on various grounds such

as there is no consideration given to the effect of time value of money and the value of cash

today and future is taken as equal. ARR takes into consideration the net profit instead of net cash

flows, however net profit is a good measure of profitability but net cash flows indicate a better

measure of overall performance of an investment (Schiozer, Mourad and Martins, 2020).

d. Advising senior executive team over the comments made

As per the comments made by Bill Brady and Xiaolin Peng, the following advise could

be made-

Investment appraisal techniques are useful for evaluating investment that a company is

planning to make within the nearer future. These techniques are divided into two major

categories that is, non - discounting and discounting techniques, where in the former case the

techniques for evaluating investment does not take into consideration the time value of money

while in the latter case the time value of money has been taken into consideration and value cash

flows in present and future are considered to be different (Ainsworth and Deines, 2019). These

techniques are helpful in increasing shareholder's return and thus ensures that the most profitable

and best technique could be selected.

It is necessary to select the best investment through evaluating investment through

different techniques by including both non-discounting and discounting as the combination of

these techniques is advisable to the senior executive of the company to facilitate evaluation of

investment performance both in terms of present and future (Torrebruno, 2020).

The various non-discounting techniques of evaluating investment performance are

payback period and accounting rate of return (ARR). On the other hand, the discounting

techniques of evaluating investment performance are Net present value (NPV), Internal rate of

return (IRR), Discounted payback period and Modified internal rate of return (MIRR)

(Bangemann, 2017). All these different techniques have various advantages and disadvantages,

for instance; Internal rate of return have the following advantages and disadvantages.

Advantages of IRR are as follows:

As IRR is the discounting techniques of investment evaluation, it takes into consideration

the time value of money, so that the value of cash flows can be derived for both present

and future.

All the cash flows associated with the investment occupying throughout the life of an

investment is taken into consideration. Also, it aids in achieving the goal of maximising

the wealth of shareholders.

Disadvantages of IRR are as follows:

The process of determining IRR becomes difficult when there are more than one cash

outflows involved in the expected life of investment, as there will be more than one IRR

and interpreting it becomes quite difficult.

IRR is not useful when there is more than one investment and also they are having

different patterns of inflows and outflows.

QUESTION 3

(a) Calculation of Financial Ratios

Gross Profit margin:

Formula = Gross Profit / Net sales * 100

2019 = 1313 / 3495 × 100 = 38%

and best technique could be selected.

It is necessary to select the best investment through evaluating investment through

different techniques by including both non-discounting and discounting as the combination of

these techniques is advisable to the senior executive of the company to facilitate evaluation of

investment performance both in terms of present and future (Torrebruno, 2020).

The various non-discounting techniques of evaluating investment performance are

payback period and accounting rate of return (ARR). On the other hand, the discounting

techniques of evaluating investment performance are Net present value (NPV), Internal rate of

return (IRR), Discounted payback period and Modified internal rate of return (MIRR)

(Bangemann, 2017). All these different techniques have various advantages and disadvantages,

for instance; Internal rate of return have the following advantages and disadvantages.

Advantages of IRR are as follows:

As IRR is the discounting techniques of investment evaluation, it takes into consideration

the time value of money, so that the value of cash flows can be derived for both present

and future.

All the cash flows associated with the investment occupying throughout the life of an

investment is taken into consideration. Also, it aids in achieving the goal of maximising

the wealth of shareholders.

Disadvantages of IRR are as follows:

The process of determining IRR becomes difficult when there are more than one cash

outflows involved in the expected life of investment, as there will be more than one IRR

and interpreting it becomes quite difficult.

IRR is not useful when there is more than one investment and also they are having

different patterns of inflows and outflows.

QUESTION 3

(a) Calculation of Financial Ratios

Gross Profit margin:

Formula = Gross Profit / Net sales * 100

2019 = 1313 / 3495 × 100 = 38%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assets Usage ratio:

Formula = Net Sales / Total Assets

2019 = 3495 / 3812 = 0.92

Current Ratio:

Formula = Current Assets / Current Liabilities

Current assets = Inventory + Trade receivable + Short term investment + Cash at bank

Current liabilities = Trade payables + Bank overdraft + Taxation

2018 = (102 + 315 + 0 + 1) / (119 + 98 + 285)

= 418 / 502 = 0.83

2019 = (150 + 1010 + 75 + 452) / (289 + 143 + 312)

= 1687 / 744 = 2.27

Acid Test Ratio:

Formula = (Current assets – Inventory) / Current Liabilities

2018 = (418 – 102) / 502

= 316 / 502 = 0.63

2019 = (1687 – 150) / 744

= 1537/ 744 = 2.07

Inventories holding period:

Formula = (Inventory / Cost of goods sold) * 365 days

2019 = 150 / 2182 × 365 days = 25 days approx.

Debt to Equity Ratio:

Formula = Total Debt/ Total Equity

Total Debt = Current liabilities + non-current liabilities

2018 = 502 + 50 = 552

2019 = 744 + 170 = 914

Total equity = share capital + share premium account + revaluation surplus + retained earnings

Formula = Net Sales / Total Assets

2019 = 3495 / 3812 = 0.92

Current Ratio:

Formula = Current Assets / Current Liabilities

Current assets = Inventory + Trade receivable + Short term investment + Cash at bank

Current liabilities = Trade payables + Bank overdraft + Taxation

2018 = (102 + 315 + 0 + 1) / (119 + 98 + 285)

= 418 / 502 = 0.83

2019 = (150 + 1010 + 75 + 452) / (289 + 143 + 312)

= 1687 / 744 = 2.27

Acid Test Ratio:

Formula = (Current assets – Inventory) / Current Liabilities

2018 = (418 – 102) / 502

= 316 / 502 = 0.63

2019 = (1687 – 150) / 744

= 1537/ 744 = 2.07

Inventories holding period:

Formula = (Inventory / Cost of goods sold) * 365 days

2019 = 150 / 2182 × 365 days = 25 days approx.

Debt to Equity Ratio:

Formula = Total Debt/ Total Equity

Total Debt = Current liabilities + non-current liabilities

2018 = 502 + 50 = 552

2019 = 744 + 170 = 914

Total equity = share capital + share premium account + revaluation surplus + retained earnings

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2018 = 1550 + 150 + 51 + 200 = 1951

2019 = 1950 + 260 + 70 + 618 = 2898

Ratios:

2018 = 552 / 1951 = 0.28

2019 = 914 / 2898 = 0.32

(b)

Importance of considering users of financial statement while doing financial statement

analysis:

While doing the financial statement analysis, it is crucial for the company that they must

consider the internal and external stakeholder perspective as well. It is because they are the one

that need to make decision regarding investment. The users of financial statement mainly review

the ratio analysis section of the annual report in order to make the decision regarding investment.

Thus, it is crucial for the company that they must calculate all ratios and further compare it in

order to identify their own current performance with past years or with the competitors. Financial

statement analysis plays significant role in the life of the users of financial statement because on

the basis of this user can deduce and identify company efficiency, performance, competitiveness

and prospects (Gjoni-Karameta and et.al., 2021). The users of FS involve customers who uses

the analysis of ratios in order to identify whether the company are providing goods at high price

or low price as compared to the cost of goods sold.

On the other hand, the employees and shareholders of the company uses financial

statement to identify and analyse profitability position of the business. It is because if the profit

of the business is high the employees will get higher salary and shareholders will get higher

dividend. Thus, it is important for the company that while doing financial statement and ratio

analysis of the business they have to consider the users or key stakeholders as well. The financial

statement involve the income statement, balance sheet, cash flow statement and statement of

change in equity which are basically result of the double-entry system of the business (Kerezsi,

Tarnóczi and Fenyves, 2018). The liquidity and leverage position of the company is understands

by the users by using the capital structure and identify whether to buy debt or equity share of the

business.

2019 = 1950 + 260 + 70 + 618 = 2898

Ratios:

2018 = 552 / 1951 = 0.28

2019 = 914 / 2898 = 0.32

(b)

Importance of considering users of financial statement while doing financial statement

analysis:

While doing the financial statement analysis, it is crucial for the company that they must

consider the internal and external stakeholder perspective as well. It is because they are the one

that need to make decision regarding investment. The users of financial statement mainly review

the ratio analysis section of the annual report in order to make the decision regarding investment.

Thus, it is crucial for the company that they must calculate all ratios and further compare it in

order to identify their own current performance with past years or with the competitors. Financial

statement analysis plays significant role in the life of the users of financial statement because on

the basis of this user can deduce and identify company efficiency, performance, competitiveness

and prospects (Gjoni-Karameta and et.al., 2021). The users of FS involve customers who uses

the analysis of ratios in order to identify whether the company are providing goods at high price

or low price as compared to the cost of goods sold.

On the other hand, the employees and shareholders of the company uses financial

statement to identify and analyse profitability position of the business. It is because if the profit

of the business is high the employees will get higher salary and shareholders will get higher

dividend. Thus, it is important for the company that while doing financial statement and ratio

analysis of the business they have to consider the users or key stakeholders as well. The financial

statement involve the income statement, balance sheet, cash flow statement and statement of

change in equity which are basically result of the double-entry system of the business (Kerezsi,

Tarnóczi and Fenyves, 2018). The liquidity and leverage position of the company is understands

by the users by using the capital structure and identify whether to buy debt or equity share of the

business.

The future expansion of the company is depends upon its creditors and investors and if

they fail to consider them they it may lead to heavy loss and discloser of business. Stakeholders

also analyse the annual report of the company to identify whether the business are operating in

ethical manner or not (Gulin, Hladika and Mićin, 2017). The government analysis the FS to

identify whether the tax paid by the company is correct or not. Thus, it is crucial for the company

that they have to make sure that their profits are real without any manipulation or window

dressing.

QUESTION: 4

a. Role of organizations in the International regulatory framework for accounting

Role of IFRS foundations

To develop globally accepted financial reporting standards which require transparent,

high quality and comparable information in financial statements and reports to aid

investors, participants of global capital markets and other users who make economic

decisions on the basis of financial statement information (Abdullah, 2018).

To ensure the application and use of these standards. To facilitate and promote the adoption of IFRS.

Role of IFRS Advisory Council

It provides a forum for IASB in an attempt to consult a range of interested parties who

are getting affected by the work of IASB in order to-

1. to extend suggestions to board on its priorities and decisions.

2. Informing board regarding the views of individual and organizations of its standard

setting project (Habib and Hasan, 2019).

3. Give advice to trustees or board.

Role of IASB

IASB has the role of fulfilling technical matters of IFRS foundation.

Discretely develop technical agenda in consultation with public and trustees.

Prepare IFRS & exposure drafts as the due process states in the constitution. Issues and approves interpretations issued by IFRS interpretations committee.

Role of IFRS interpretations committee

they fail to consider them they it may lead to heavy loss and discloser of business. Stakeholders

also analyse the annual report of the company to identify whether the business are operating in

ethical manner or not (Gulin, Hladika and Mićin, 2017). The government analysis the FS to

identify whether the tax paid by the company is correct or not. Thus, it is crucial for the company

that they have to make sure that their profits are real without any manipulation or window

dressing.

QUESTION: 4

a. Role of organizations in the International regulatory framework for accounting

Role of IFRS foundations

To develop globally accepted financial reporting standards which require transparent,

high quality and comparable information in financial statements and reports to aid

investors, participants of global capital markets and other users who make economic

decisions on the basis of financial statement information (Abdullah, 2018).

To ensure the application and use of these standards. To facilitate and promote the adoption of IFRS.

Role of IFRS Advisory Council

It provides a forum for IASB in an attempt to consult a range of interested parties who

are getting affected by the work of IASB in order to-

1. to extend suggestions to board on its priorities and decisions.

2. Informing board regarding the views of individual and organizations of its standard

setting project (Habib and Hasan, 2019).

3. Give advice to trustees or board.

Role of IASB

IASB has the role of fulfilling technical matters of IFRS foundation.

Discretely develop technical agenda in consultation with public and trustees.

Prepare IFRS & exposure drafts as the due process states in the constitution. Issues and approves interpretations issued by IFRS interpretations committee.

Role of IFRS interpretations committee

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.