FINANCE 4 Investment Techniques Investment Techniques

VerifiedAdded on 2022/08/12

|13

|1220

|123

AI Summary

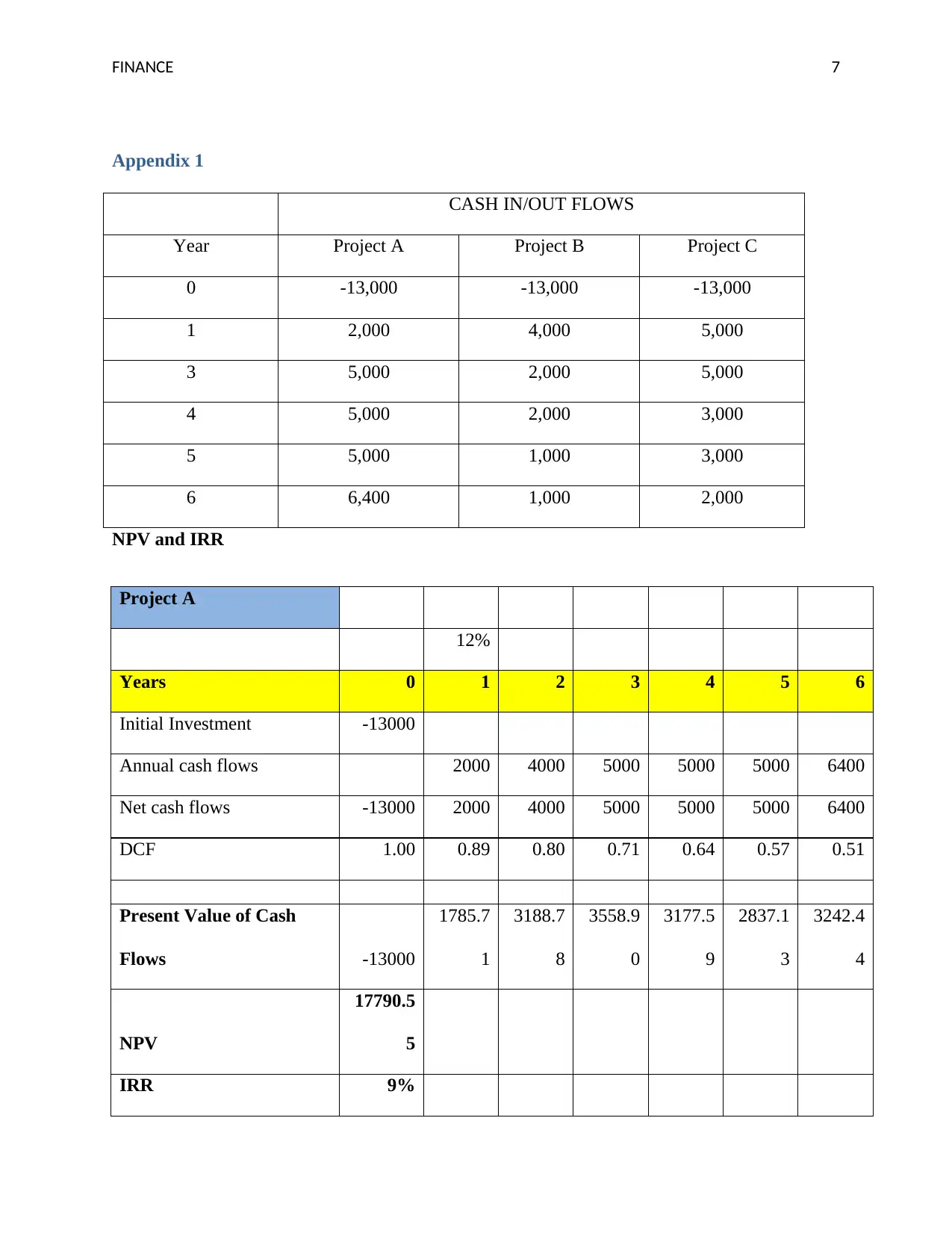

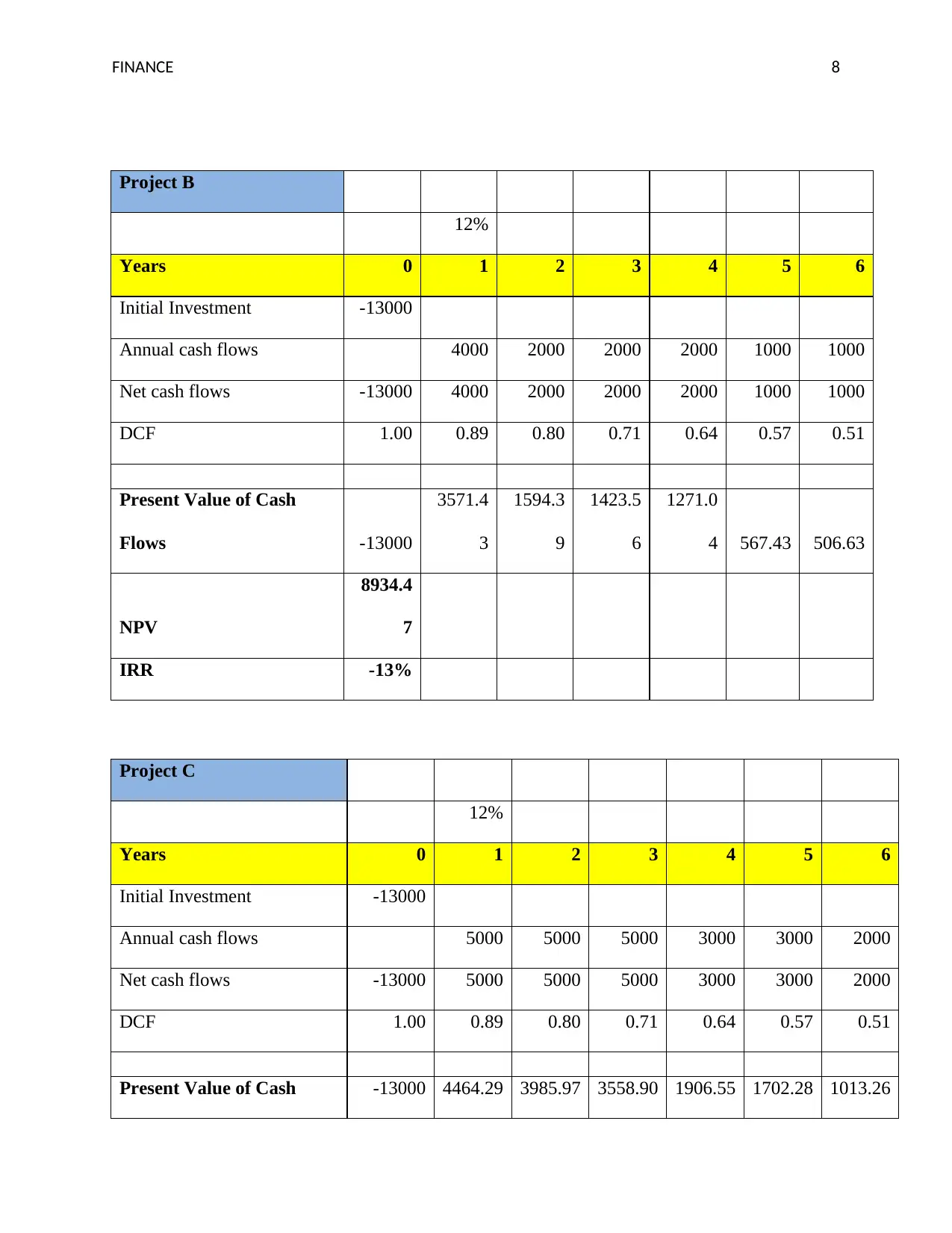

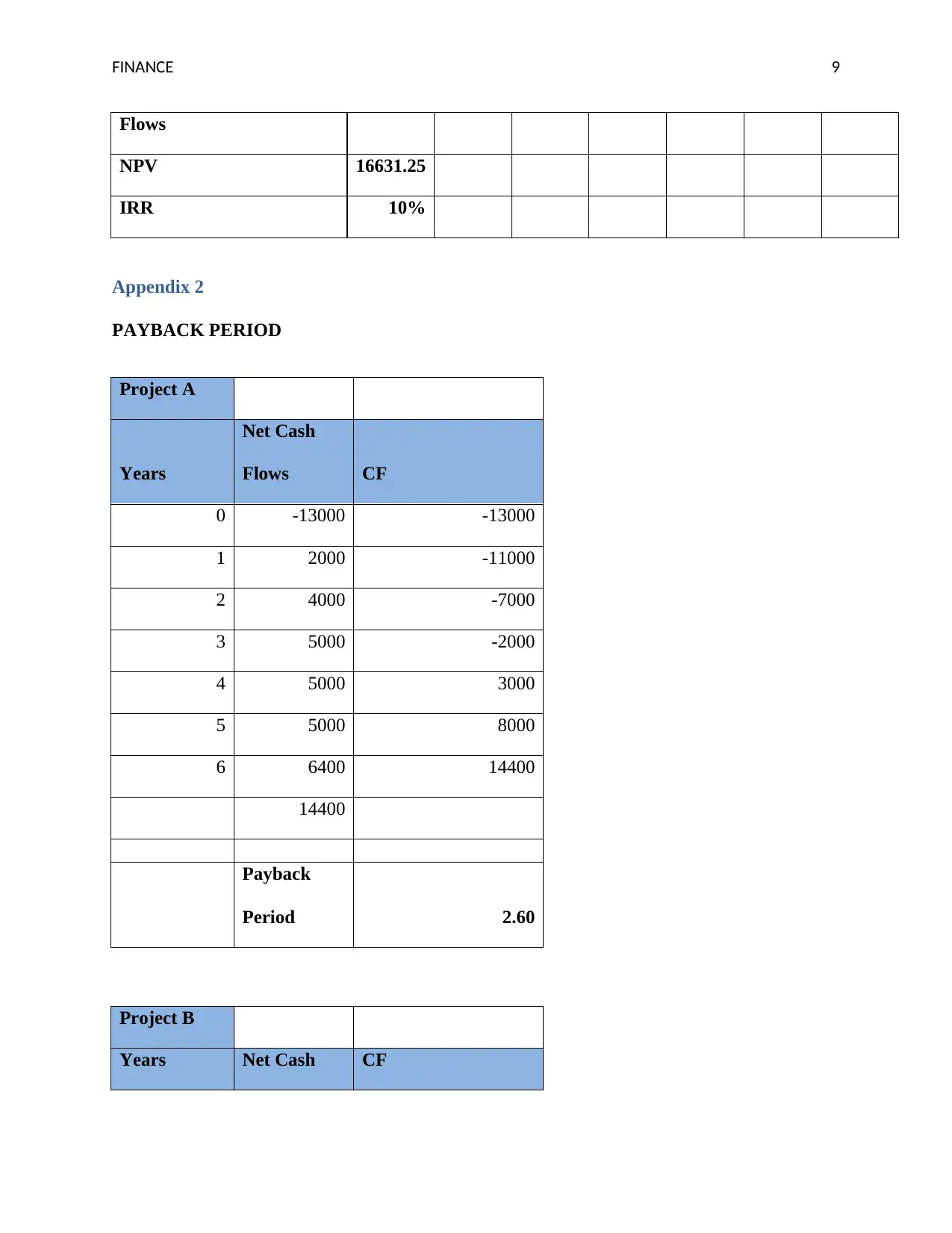

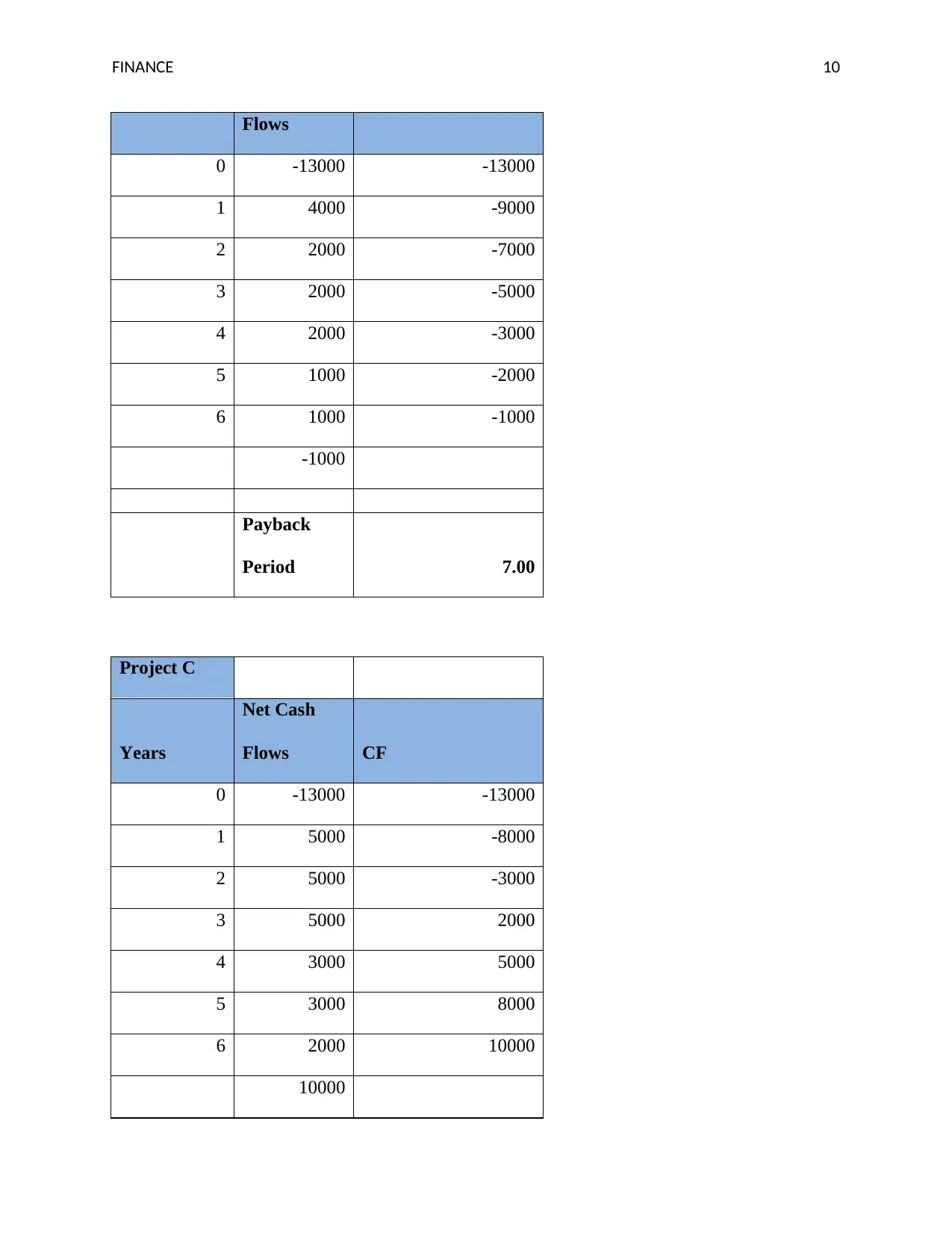

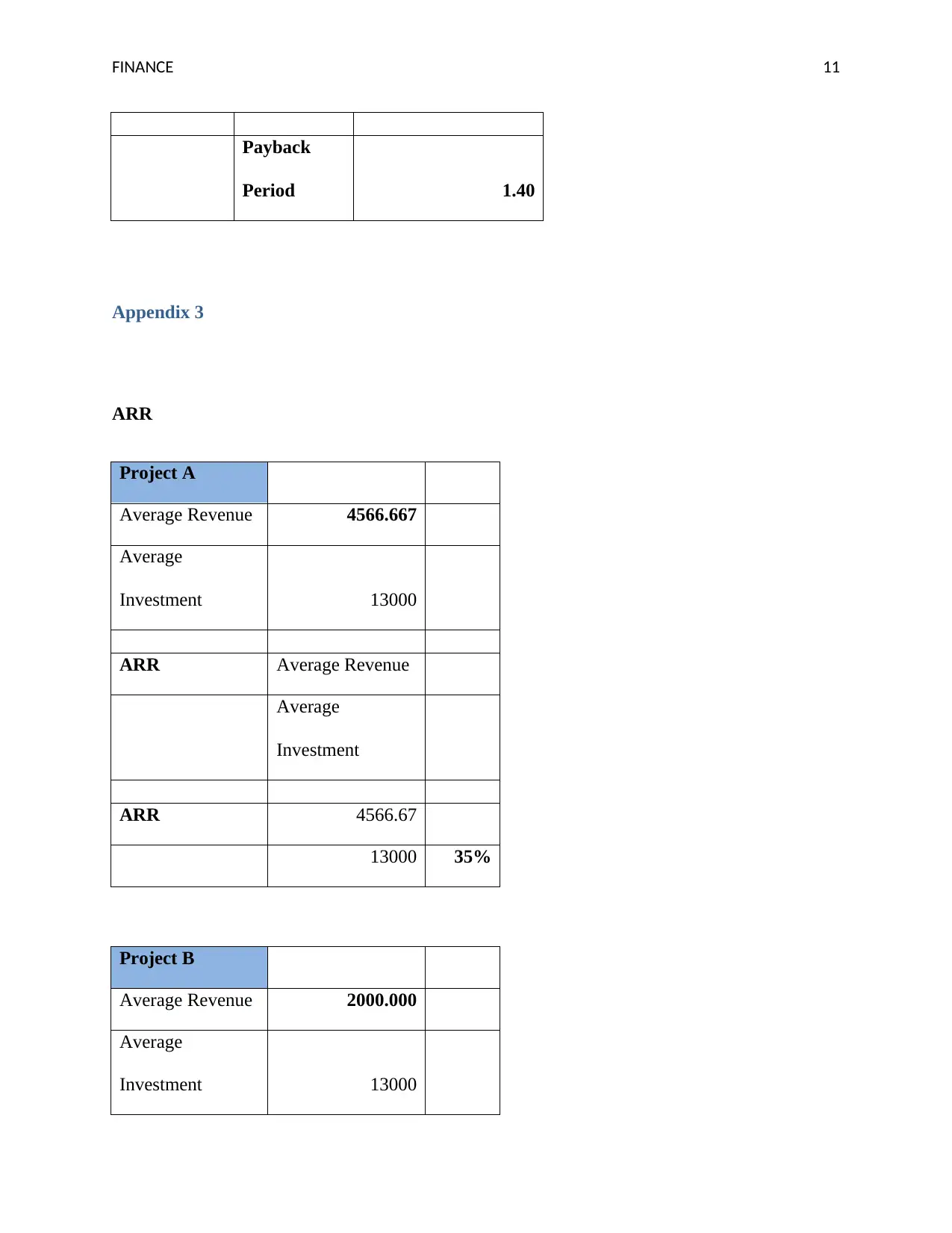

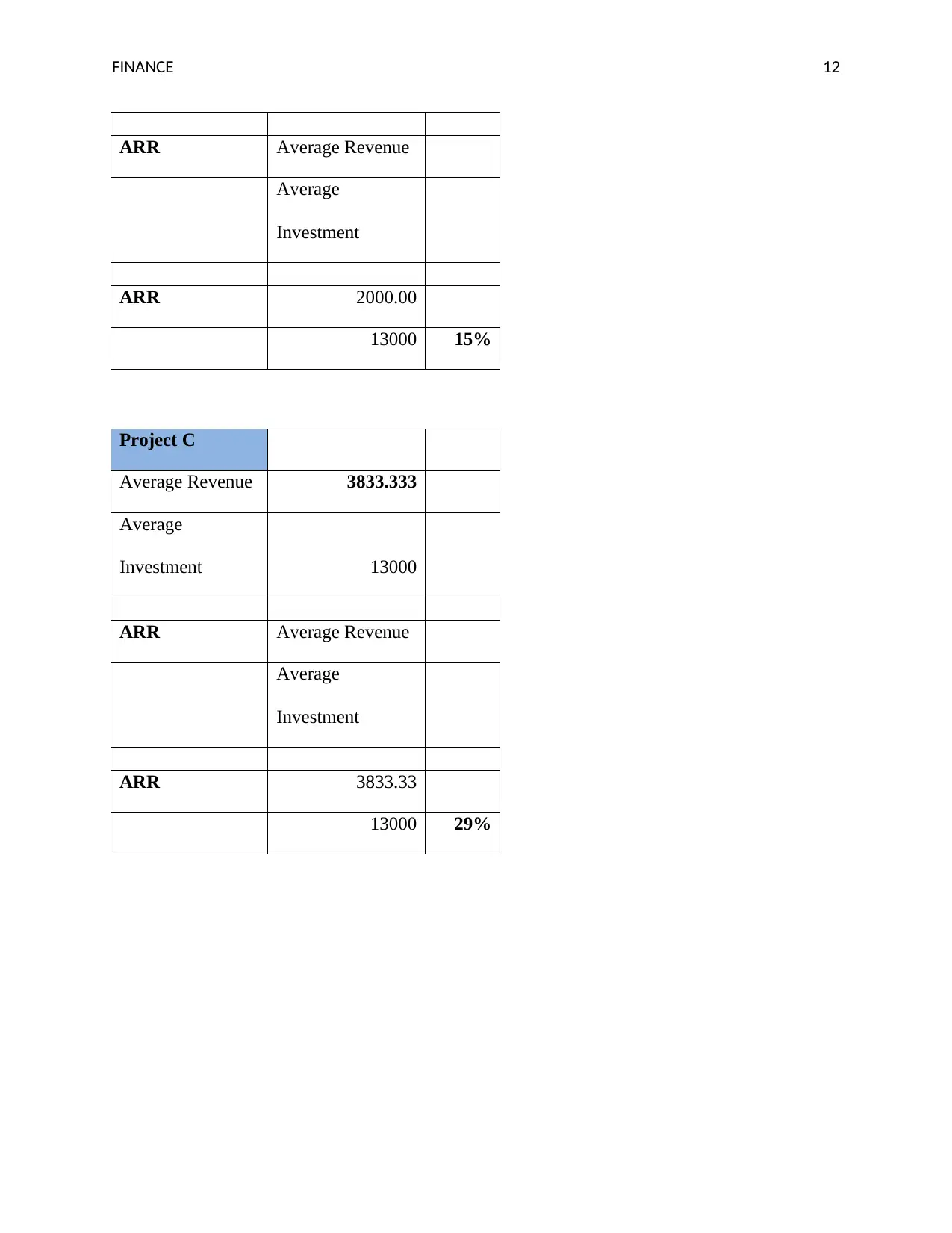

FINANCE 4 Investment Techniques Investment Techniques Contents Purpose of this report 2 Investment Appraisal Techniques 2 ARR (Average Rate of Return) 2 NPV 2 IRR 3 Payback Period 3 Implementation of techniques on projects 4 Recommendations 4 Financing Methods Operating Activities for Sensations Corporation 4 Managing Working Capital 5 Conclusion 5 References 6 Appendix 1 7 Appendix 2 9 Appendix 3 11 Purpose of this report The main aim of this report is to discuss about the investment appraisal techniques. Investment Appraisal Techniques ARR (Average Rate of

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.