finance

11 Pages3055 Words23 Views

Added on 2023-01-05

About This Document

need in 4 hours

finance

Added on 2023-01-05

ShareRelated Documents

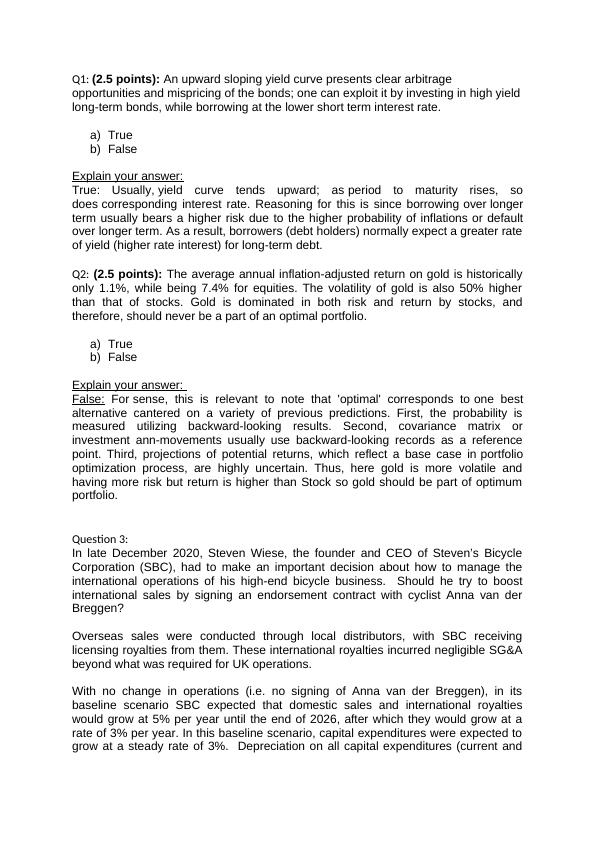

Q1: (2.5 points): An upward sloping yield curve presents clear arbitrage

opportunities and mispricing of the bonds; one can exploit it by investing in high yield

long-term bonds, while borrowing at the lower short term interest rate.

a) True

b) False

Explain your answer:

True: Usually, yield curve tends upward; as period to maturity rises, so

does corresponding interest rate. Reasoning for this is since borrowing over longer

term usually bears a higher risk due to the higher probability of inflations or default

over longer term. As a result, borrowers (debt holders) normally expect a greater rate

of yield (higher rate interest) for long-term debt.

Q2: (2.5 points): The average annual inflation-adjusted return on gold is historically

only 1.1%, while being 7.4% for equities. The volatility of gold is also 50% higher

than that of stocks. Gold is dominated in both risk and return by stocks, and

therefore, should never be a part of an optimal portfolio.

a) True

b) False

Explain your answer:

False: For sense, this is relevant to note that 'optimal' corresponds to one best

alternative cantered on a variety of previous predictions. First, the probability is

measured utilizing backward-looking results. Second, covariance matrix or

investment ann-movements usually use backward-looking records as a reference

point. Third, projections of potential returns, which reflect a base case in portfolio

optimization process, are highly uncertain. Thus, here gold is more volatile and

having more risk but return is higher than Stock so gold should be part of optimum

portfolio.

Question 3:

In late December 2020, Steven Wiese, the founder and CEO of Steven’s Bicycle

Corporation (SBC), had to make an important decision about how to manage the

international operations of his high-end bicycle business. Should he try to boost

international sales by signing an endorsement contract with cyclist Anna van der

Breggen?

Overseas sales were conducted through local distributors, with SBC receiving

licensing royalties from them. These international royalties incurred negligible SG&A

beyond what was required for UK operations.

With no change in operations (i.e. no signing of Anna van der Breggen), in its

baseline scenario SBC expected that domestic sales and international royalties

would grow at 5% per year until the end of 2026, after which they would grow at a

rate of 3% per year. In this baseline scenario, capital expenditures were expected to

grow at a steady rate of 3%. Depreciation on all capital expenditures (current and

opportunities and mispricing of the bonds; one can exploit it by investing in high yield

long-term bonds, while borrowing at the lower short term interest rate.

a) True

b) False

Explain your answer:

True: Usually, yield curve tends upward; as period to maturity rises, so

does corresponding interest rate. Reasoning for this is since borrowing over longer

term usually bears a higher risk due to the higher probability of inflations or default

over longer term. As a result, borrowers (debt holders) normally expect a greater rate

of yield (higher rate interest) for long-term debt.

Q2: (2.5 points): The average annual inflation-adjusted return on gold is historically

only 1.1%, while being 7.4% for equities. The volatility of gold is also 50% higher

than that of stocks. Gold is dominated in both risk and return by stocks, and

therefore, should never be a part of an optimal portfolio.

a) True

b) False

Explain your answer:

False: For sense, this is relevant to note that 'optimal' corresponds to one best

alternative cantered on a variety of previous predictions. First, the probability is

measured utilizing backward-looking results. Second, covariance matrix or

investment ann-movements usually use backward-looking records as a reference

point. Third, projections of potential returns, which reflect a base case in portfolio

optimization process, are highly uncertain. Thus, here gold is more volatile and

having more risk but return is higher than Stock so gold should be part of optimum

portfolio.

Question 3:

In late December 2020, Steven Wiese, the founder and CEO of Steven’s Bicycle

Corporation (SBC), had to make an important decision about how to manage the

international operations of his high-end bicycle business. Should he try to boost

international sales by signing an endorsement contract with cyclist Anna van der

Breggen?

Overseas sales were conducted through local distributors, with SBC receiving

licensing royalties from them. These international royalties incurred negligible SG&A

beyond what was required for UK operations.

With no change in operations (i.e. no signing of Anna van der Breggen), in its

baseline scenario SBC expected that domestic sales and international royalties

would grow at 5% per year until the end of 2026, after which they would grow at a

rate of 3% per year. In this baseline scenario, capital expenditures were expected to

grow at a steady rate of 3%. Depreciation on all capital expenditures (current and

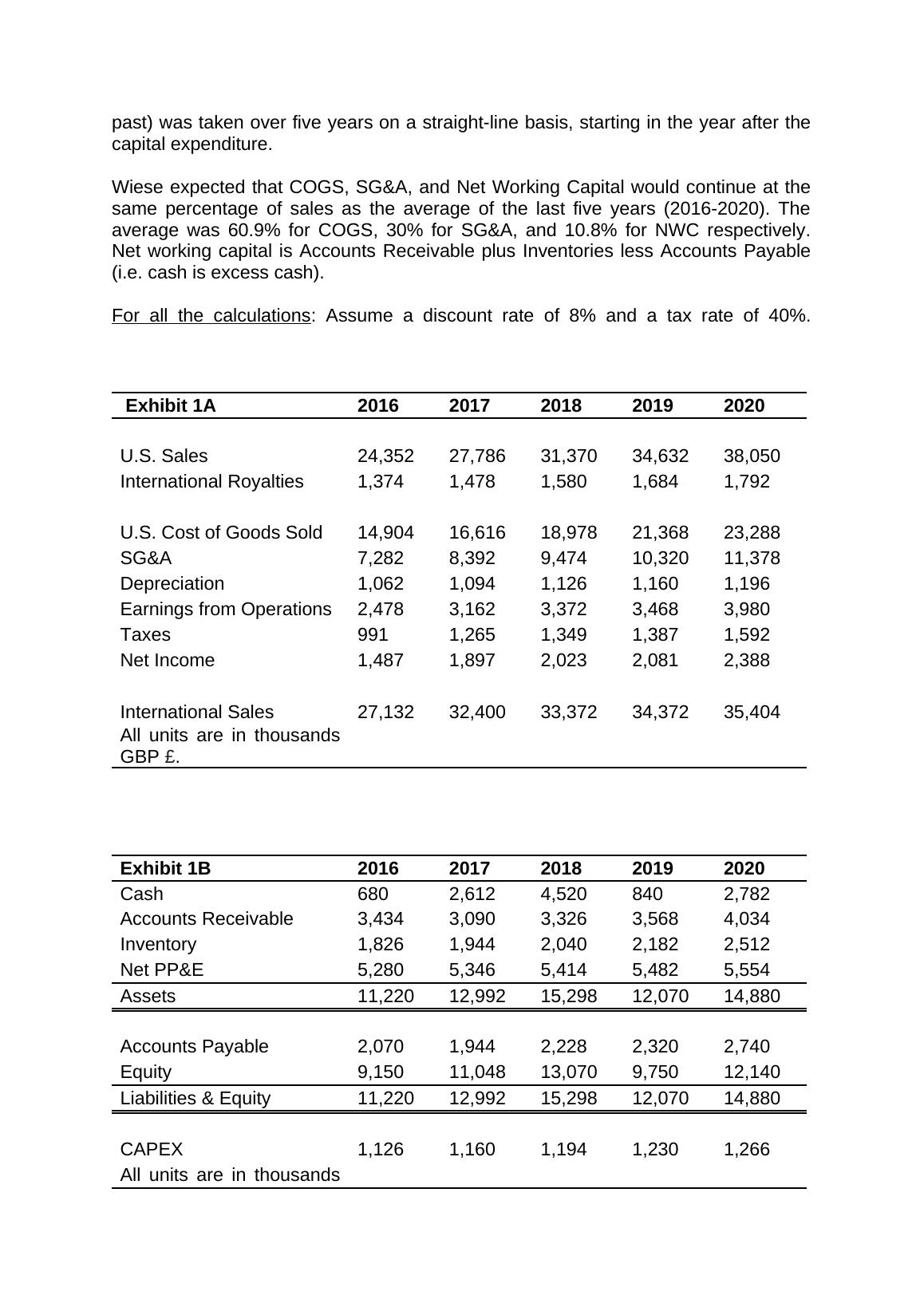

past) was taken over five years on a straight-line basis, starting in the year after the

capital expenditure.

Wiese expected that COGS, SG&A, and Net Working Capital would continue at the

same percentage of sales as the average of the last five years (2016-2020). The

average was 60.9% for COGS, 30% for SG&A, and 10.8% for NWC respectively.

Net working capital is Accounts Receivable plus Inventories less Accounts Payable

(i.e. cash is excess cash).

For all the calculations: Assume a discount rate of 8% and a tax rate of 40%.

Exhibit 1A 2016 2017 2018 2019 2020

U.S. Sales 24,352 27,786 31,370 34,632 38,050

International Royalties 1,374 1,478 1,580 1,684 1,792

U.S. Cost of Goods Sold 14,904 16,616 18,978 21,368 23,288

SG&A 7,282 8,392 9,474 10,320 11,378

Depreciation 1,062 1,094 1,126 1,160 1,196

Earnings from Operations 2,478 3,162 3,372 3,468 3,980

Taxes 991 1,265 1,349 1,387 1,592

Net Income 1,487 1,897 2,023 2,081 2,388

International Sales 27,132 32,400 33,372 34,372 35,404

All units are in thousands

GBP £.

Exhibit 1B 2016 2017 2018 2019 2020

Cash 680 2,612 4,520 840 2,782

Accounts Receivable 3,434 3,090 3,326 3,568 4,034

Inventory 1,826 1,944 2,040 2,182 2,512

Net PP&E 5,280 5,346 5,414 5,482 5,554

Assets 11,220 12,992 15,298 12,070 14,880

Accounts Payable 2,070 1,944 2,228 2,320 2,740

Equity 9,150 11,048 13,070 9,750 12,140

Liabilities & Equity 11,220 12,992 15,298 12,070 14,880

CAPEX 1,126 1,160 1,194 1,230 1,266

All units are in thousands

capital expenditure.

Wiese expected that COGS, SG&A, and Net Working Capital would continue at the

same percentage of sales as the average of the last five years (2016-2020). The

average was 60.9% for COGS, 30% for SG&A, and 10.8% for NWC respectively.

Net working capital is Accounts Receivable plus Inventories less Accounts Payable

(i.e. cash is excess cash).

For all the calculations: Assume a discount rate of 8% and a tax rate of 40%.

Exhibit 1A 2016 2017 2018 2019 2020

U.S. Sales 24,352 27,786 31,370 34,632 38,050

International Royalties 1,374 1,478 1,580 1,684 1,792

U.S. Cost of Goods Sold 14,904 16,616 18,978 21,368 23,288

SG&A 7,282 8,392 9,474 10,320 11,378

Depreciation 1,062 1,094 1,126 1,160 1,196

Earnings from Operations 2,478 3,162 3,372 3,468 3,980

Taxes 991 1,265 1,349 1,387 1,592

Net Income 1,487 1,897 2,023 2,081 2,388

International Sales 27,132 32,400 33,372 34,372 35,404

All units are in thousands

GBP £.

Exhibit 1B 2016 2017 2018 2019 2020

Cash 680 2,612 4,520 840 2,782

Accounts Receivable 3,434 3,090 3,326 3,568 4,034

Inventory 1,826 1,944 2,040 2,182 2,512

Net PP&E 5,280 5,346 5,414 5,482 5,554

Assets 11,220 12,992 15,298 12,070 14,880

Accounts Payable 2,070 1,944 2,228 2,320 2,740

Equity 9,150 11,048 13,070 9,750 12,140

Liabilities & Equity 11,220 12,992 15,298 12,070 14,880

CAPEX 1,126 1,160 1,194 1,230 1,266

All units are in thousands

GBP £.

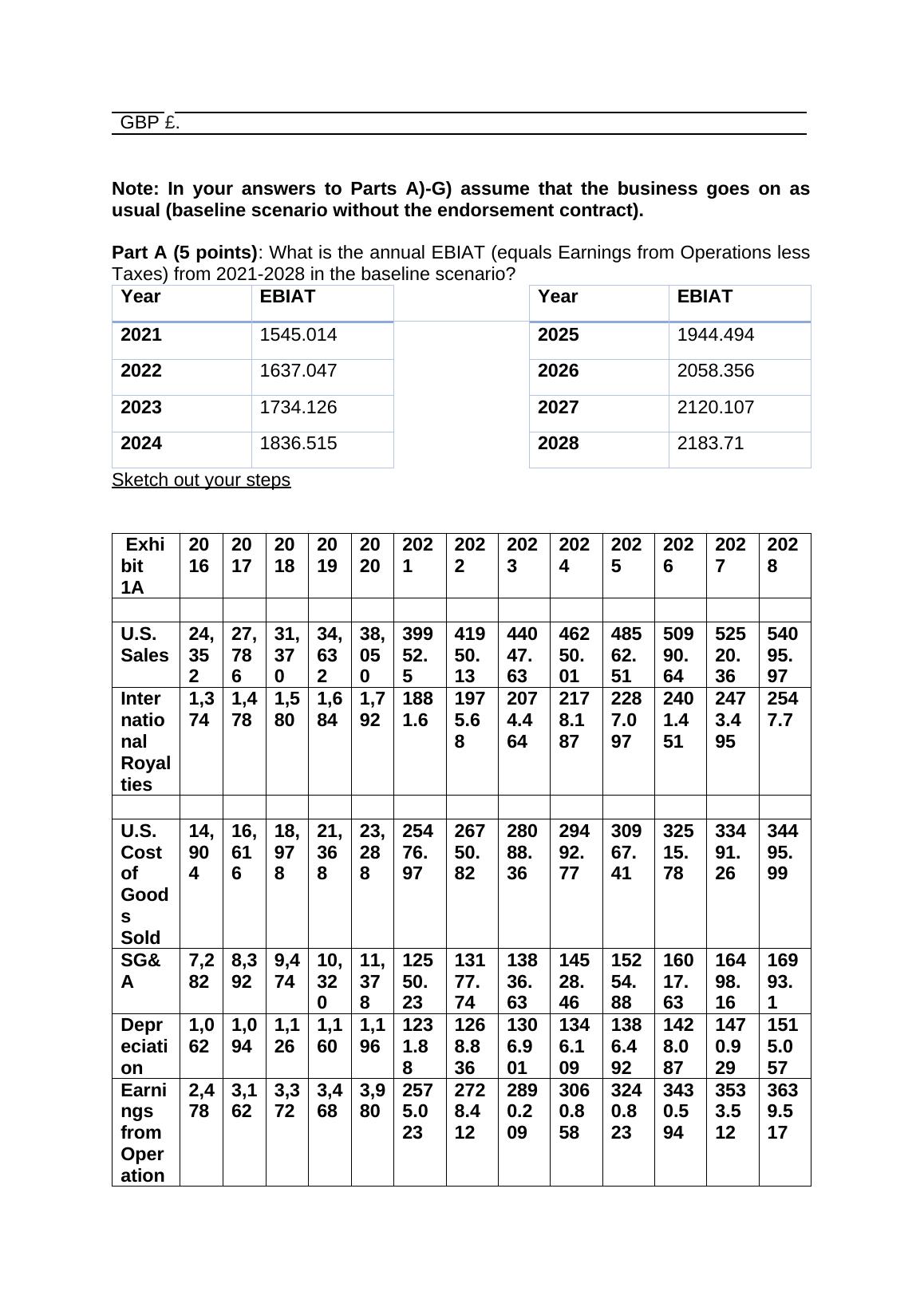

Note: In your answers to Parts A)-G) assume that the business goes on as

usual (baseline scenario without the endorsement contract).

Part A (5 points): What is the annual EBIAT (equals Earnings from Operations less

Taxes) from 2021-2028 in the baseline scenario?

Year EBIAT Year EBIAT

2021 1545.014 2025 1944.494

2022 1637.047 2026 2058.356

2023 1734.126 2027 2120.107

2024 1836.515 2028 2183.71

Sketch out your steps

Exhi

bit

1A

20

16

20

17

20

18

20

19

20

20

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

U.S.

Sales

24,

35

2

27,

78

6

31,

37

0

34,

63

2

38,

05

0

399

52.

5

419

50.

13

440

47.

63

462

50.

01

485

62.

51

509

90.

64

525

20.

36

540

95.

97

Inter

natio

nal

Royal

ties

1,3

74

1,4

78

1,5

80

1,6

84

1,7

92

188

1.6

197

5.6

8

207

4.4

64

217

8.1

87

228

7.0

97

240

1.4

51

247

3.4

95

254

7.7

U.S.

Cost

of

Good

s

Sold

14,

90

4

16,

61

6

18,

97

8

21,

36

8

23,

28

8

254

76.

97

267

50.

82

280

88.

36

294

92.

77

309

67.

41

325

15.

78

334

91.

26

344

95.

99

SG&

A

7,2

82

8,3

92

9,4

74

10,

32

0

11,

37

8

125

50.

23

131

77.

74

138

36.

63

145

28.

46

152

54.

88

160

17.

63

164

98.

16

169

93.

1

Depr

eciati

on

1,0

62

1,0

94

1,1

26

1,1

60

1,1

96

123

1.8

8

126

8.8

36

130

6.9

01

134

6.1

09

138

6.4

92

142

8.0

87

147

0.9

29

151

5.0

57

Earni

ngs

from

Oper

ation

2,4

78

3,1

62

3,3

72

3,4

68

3,9

80

257

5.0

23

272

8.4

12

289

0.2

09

306

0.8

58

324

0.8

23

343

0.5

94

353

3.5

12

363

9.5

17

Note: In your answers to Parts A)-G) assume that the business goes on as

usual (baseline scenario without the endorsement contract).

Part A (5 points): What is the annual EBIAT (equals Earnings from Operations less

Taxes) from 2021-2028 in the baseline scenario?

Year EBIAT Year EBIAT

2021 1545.014 2025 1944.494

2022 1637.047 2026 2058.356

2023 1734.126 2027 2120.107

2024 1836.515 2028 2183.71

Sketch out your steps

Exhi

bit

1A

20

16

20

17

20

18

20

19

20

20

202

1

202

2

202

3

202

4

202

5

202

6

202

7

202

8

U.S.

Sales

24,

35

2

27,

78

6

31,

37

0

34,

63

2

38,

05

0

399

52.

5

419

50.

13

440

47.

63

462

50.

01

485

62.

51

509

90.

64

525

20.

36

540

95.

97

Inter

natio

nal

Royal

ties

1,3

74

1,4

78

1,5

80

1,6

84

1,7

92

188

1.6

197

5.6

8

207

4.4

64

217

8.1

87

228

7.0

97

240

1.4

51

247

3.4

95

254

7.7

U.S.

Cost

of

Good

s

Sold

14,

90

4

16,

61

6

18,

97

8

21,

36

8

23,

28

8

254

76.

97

267

50.

82

280

88.

36

294

92.

77

309

67.

41

325

15.

78

334

91.

26

344

95.

99

SG&

A

7,2

82

8,3

92

9,4

74

10,

32

0

11,

37

8

125

50.

23

131

77.

74

138

36.

63

145

28.

46

152

54.

88

160

17.

63

164

98.

16

169

93.

1

Depr

eciati

on

1,0

62

1,0

94

1,1

26

1,1

60

1,1

96

123

1.8

8

126

8.8

36

130

6.9

01

134

6.1

09

138

6.4

92

142

8.0

87

147

0.9

29

151

5.0

57

Earni

ngs

from

Oper

ation

2,4

78

3,1

62

3,3

72

3,4

68

3,9

80

257

5.0

23

272

8.4

12

289

0.2

09

306

0.8

58

324

0.8

23

343

0.5

94

353

3.5

12

363

9.5

17

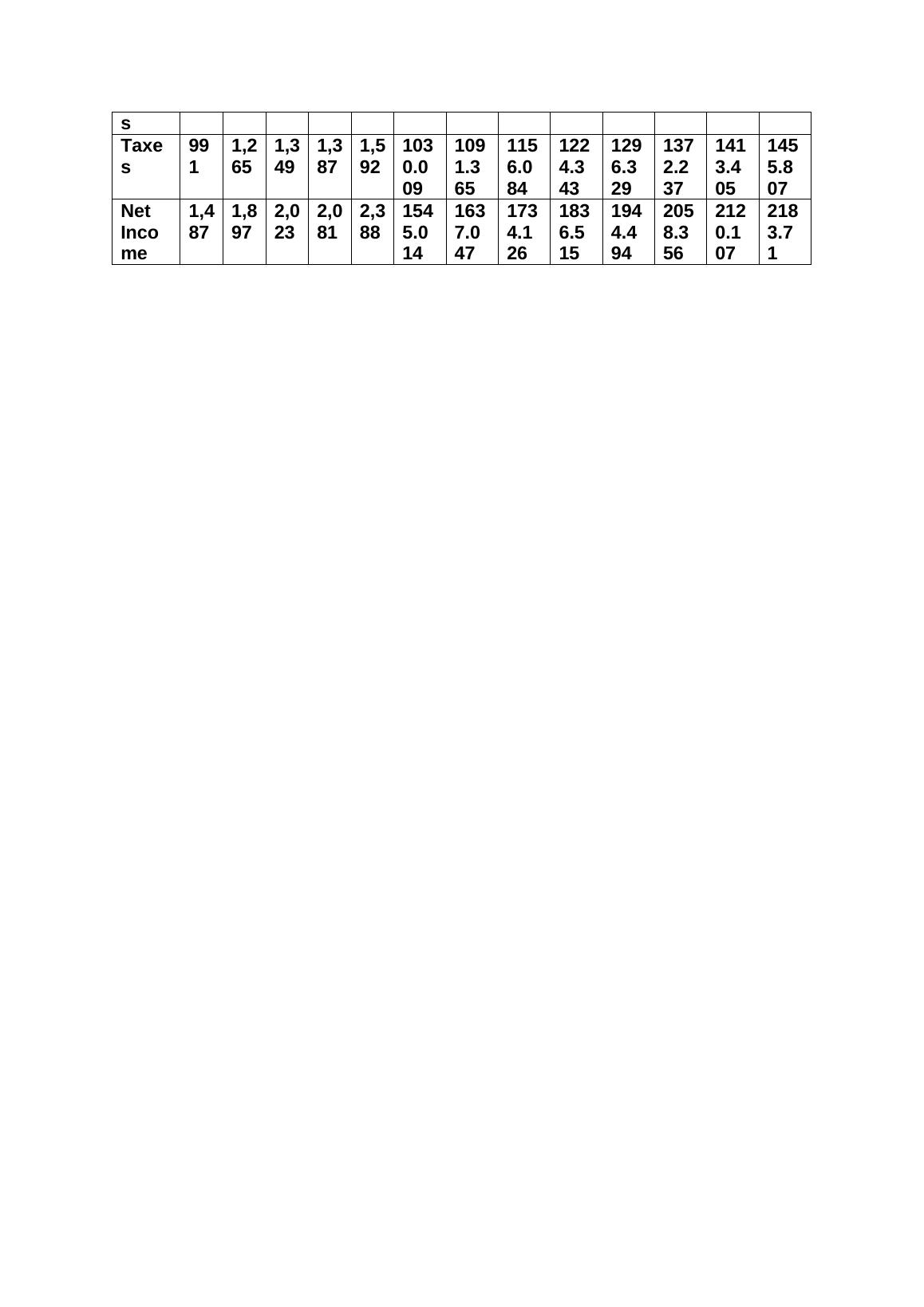

s

Taxe

s

99

1

1,2

65

1,3

49

1,3

87

1,5

92

103

0.0

09

109

1.3

65

115

6.0

84

122

4.3

43

129

6.3

29

137

2.2

37

141

3.4

05

145

5.8

07

Net

Inco

me

1,4

87

1,8

97

2,0

23

2,0

81

2,3

88

154

5.0

14

163

7.0

47

173

4.1

26

183

6.5

15

194

4.4

94

205

8.3

56

212

0.1

07

218

3.7

1

Taxe

s

99

1

1,2

65

1,3

49

1,3

87

1,5

92

103

0.0

09

109

1.3

65

115

6.0

84

122

4.3

43

129

6.3

29

137

2.2

37

141

3.4

05

145

5.8

07

Net

Inco

me

1,4

87

1,8

97

2,0

23

2,0

81

2,3

88

154

5.0

14

163

7.0

47

173

4.1

26

183

6.5

15

194

4.4

94

205

8.3

56

212

0.1

07

218

3.7

1

End of preview

Want to access all the pages? Upload your documents or become a member.