Finance Leases: Accounting, Manufacturer/Dealer Lessors & Gali Ltd

VerifiedAdded on 2023/04/23

|9

|1406

|117

Essay

AI Summary

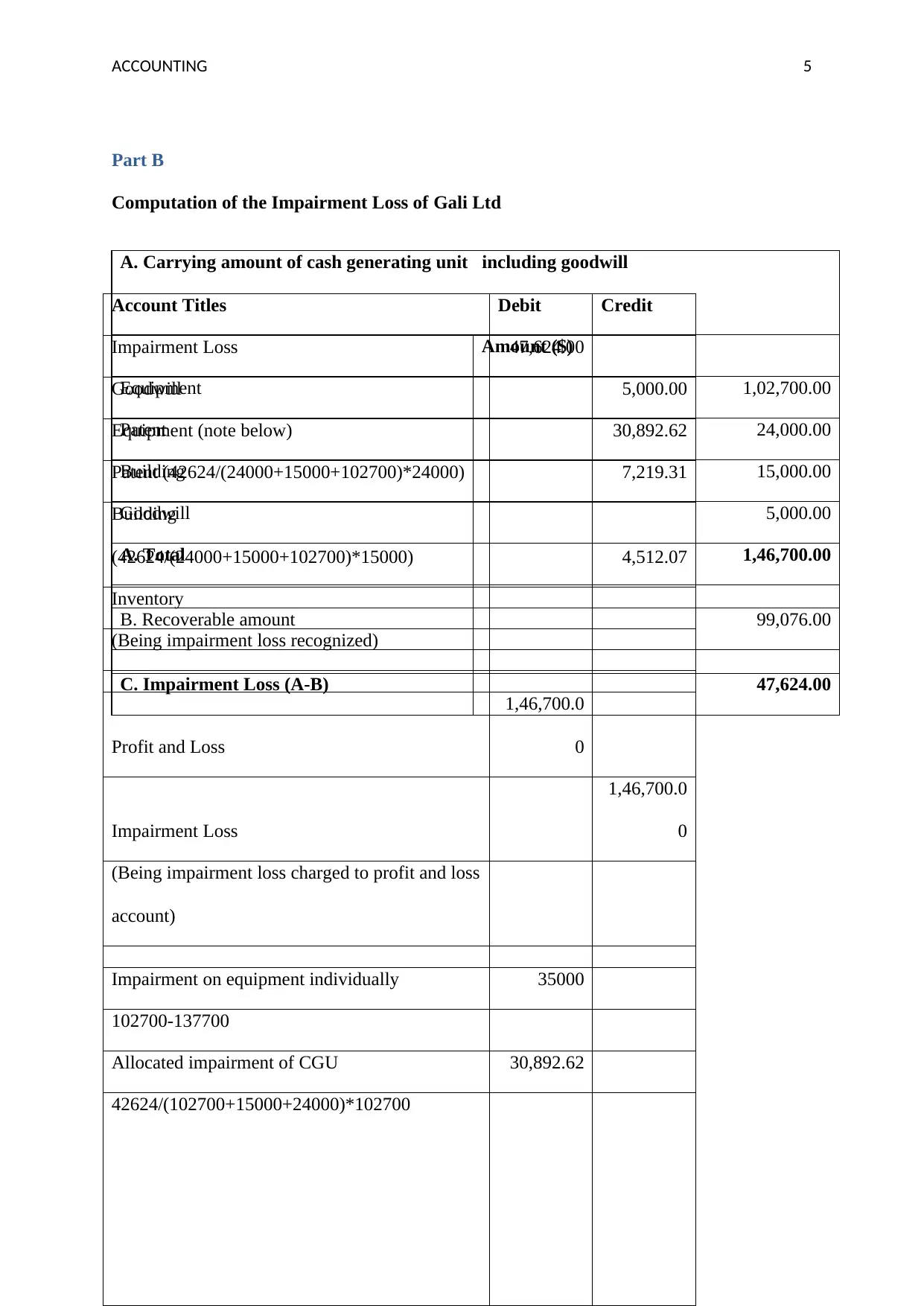

This assignment provides a comprehensive overview of accounting for finance leases by manufacturer or dealer lessors, adhering to AASB 16 standards. It distinguishes between finance and operating leases, highlighting the importance of proper calculation for lessors, focusing on benefits such as ownership preservation, tax advantages, and high profitability. The assignment details the balance sheet, income statement, and cash flow statement treatments for finance leases, emphasizing the impact on assets, liabilities, and working capital. A practical application is presented through a case study of Gali Ltd, demonstrating the computation of impairment loss, including journal entries and asset allocation, ensuring compliance with accounting principles. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.