Winter 2019 iMBA Finance Report: BAE Systems Financial Analysis

VerifiedAdded on 2023/01/18

|15

|2377

|89

Report

AI Summary

This report presents a comprehensive financial analysis of BAE Systems, a UK-based aerospace company, and compares its performance with its competitor, Airbus SE. The analysis includes an in-depth examination of financial statements, ratio analysis (profitability, liquidity, and investor ratios), and company valuation using asset-based, dividend, and price-earnings methods. The report also explores the limitations of ratio analysis and delves into capital structure considerations, including the cost of debt and equity, and the weighted average cost of capital (WACC). Numerical tasks related to capital structure are provided. The report concludes with an evaluation of BAE System's financial position and offers insights into its strengths and weaknesses. The report uses financial data from 2018.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK...............................................................................................................................................3

Financial Analysis:......................................................................................................................3

Company valuation:....................................................................................................................6

Capital structure:.......................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

TASK...............................................................................................................................................3

Financial Analysis:......................................................................................................................3

Company valuation:....................................................................................................................6

Capital structure:.......................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The term finance is a key aspect for business entities in order to complete different kinds

of activities. In order to analyse need of finance, there are different types of methods and

techniques. Companies produce various number of financial statements to assess their financial

needs (McLean and Zhao, 2014). This study provides financial analysis of corporation BAE

Systems (UK's Aerospace company) along with comparison of performance with competitor

named Airbus SE. Both companies are operating in same industry, BAE is UK's company while

Airbus SE is European international aerospace and defence corporation.

Study also contains practical sum of valuation of respective company and some

numerical task related to capital structure. Moreover, study provides explanation about key

limitation of usage of ratio analysis.

TASK

Financial Analysis:

Financial analysis mainly relates to effective application of financial and numerical

information for assessing corporation's performance in all aspects and provide meaningful

recommendations in relation to ways by which company can improvise existing performance.

Ratio analysis is one of the most useful tool for financial analysis which is purely formula based

(De Mooij, 2012.). This help to make comparison of financial and operating performance of

company with industry standards and competitors. Following is ratio analysis of Company BAE

Systems along with its competitor Airbus SE, as follows:

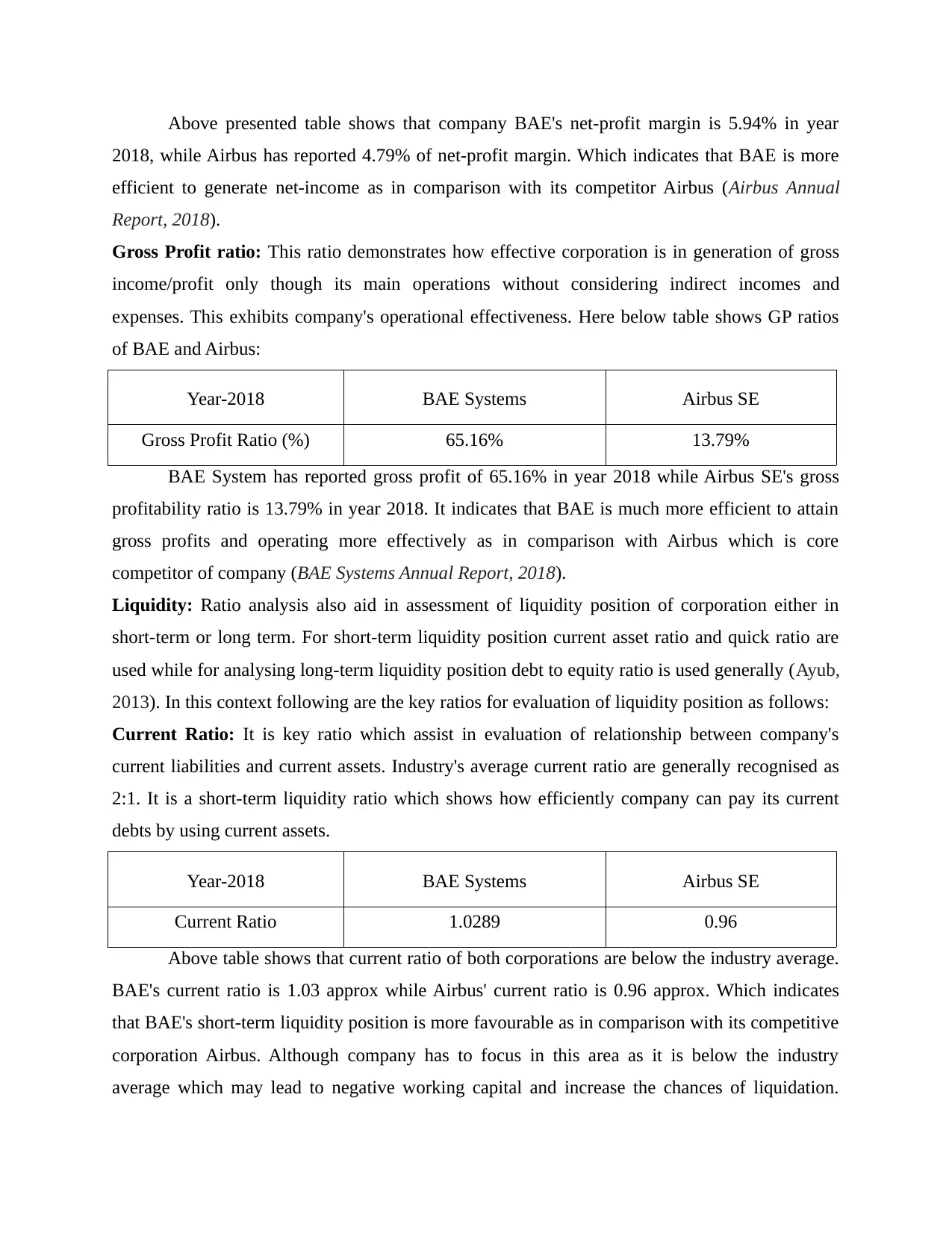

Profitability Criteria: Ratio analysis exhibits corporation's performance in terms of capacity

and efficiency of company to generate profits. It mainly includes net profit ratio and gross profit

ratio, which are analysed below in respect of respective company and its competitor:

Net Profit Ratio: This ratio represents how much profit after providing all expenditures

company has been earned as a specific percentage of total revenue. Net profit margin or ratio

demonstrates how much or what extent company's revenue has been converted into net income.

Year 2018 BAE Systems Airbus SE

Net Profit Margin(%) 5.94% 4.79%

The term finance is a key aspect for business entities in order to complete different kinds

of activities. In order to analyse need of finance, there are different types of methods and

techniques. Companies produce various number of financial statements to assess their financial

needs (McLean and Zhao, 2014). This study provides financial analysis of corporation BAE

Systems (UK's Aerospace company) along with comparison of performance with competitor

named Airbus SE. Both companies are operating in same industry, BAE is UK's company while

Airbus SE is European international aerospace and defence corporation.

Study also contains practical sum of valuation of respective company and some

numerical task related to capital structure. Moreover, study provides explanation about key

limitation of usage of ratio analysis.

TASK

Financial Analysis:

Financial analysis mainly relates to effective application of financial and numerical

information for assessing corporation's performance in all aspects and provide meaningful

recommendations in relation to ways by which company can improvise existing performance.

Ratio analysis is one of the most useful tool for financial analysis which is purely formula based

(De Mooij, 2012.). This help to make comparison of financial and operating performance of

company with industry standards and competitors. Following is ratio analysis of Company BAE

Systems along with its competitor Airbus SE, as follows:

Profitability Criteria: Ratio analysis exhibits corporation's performance in terms of capacity

and efficiency of company to generate profits. It mainly includes net profit ratio and gross profit

ratio, which are analysed below in respect of respective company and its competitor:

Net Profit Ratio: This ratio represents how much profit after providing all expenditures

company has been earned as a specific percentage of total revenue. Net profit margin or ratio

demonstrates how much or what extent company's revenue has been converted into net income.

Year 2018 BAE Systems Airbus SE

Net Profit Margin(%) 5.94% 4.79%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Above presented table shows that company BAE's net-profit margin is 5.94% in year

2018, while Airbus has reported 4.79% of net-profit margin. Which indicates that BAE is more

efficient to generate net-income as in comparison with its competitor Airbus (Airbus Annual

Report, 2018).

Gross Profit ratio: This ratio demonstrates how effective corporation is in generation of gross

income/profit only though its main operations without considering indirect incomes and

expenses. This exhibits company's operational effectiveness. Here below table shows GP ratios

of BAE and Airbus:

Year-2018 BAE Systems Airbus SE

Gross Profit Ratio (%) 65.16% 13.79%

BAE System has reported gross profit of 65.16% in year 2018 while Airbus SE's gross

profitability ratio is 13.79% in year 2018. It indicates that BAE is much more efficient to attain

gross profits and operating more effectively as in comparison with Airbus which is core

competitor of company (BAE Systems Annual Report, 2018).

Liquidity: Ratio analysis also aid in assessment of liquidity position of corporation either in

short-term or long term. For short-term liquidity position current asset ratio and quick ratio are

used while for analysing long-term liquidity position debt to equity ratio is used generally (Ayub,

2013). In this context following are the key ratios for evaluation of liquidity position as follows:

Current Ratio: It is key ratio which assist in evaluation of relationship between company's

current liabilities and current assets. Industry's average current ratio are generally recognised as

2:1. It is a short-term liquidity ratio which shows how efficiently company can pay its current

debts by using current assets.

Year-2018 BAE Systems Airbus SE

Current Ratio 1.0289 0.96

Above table shows that current ratio of both corporations are below the industry average.

BAE's current ratio is 1.03 approx while Airbus' current ratio is 0.96 approx. Which indicates

that BAE's short-term liquidity position is more favourable as in comparison with its competitive

corporation Airbus. Although company has to focus in this area as it is below the industry

average which may lead to negative working capital and increase the chances of liquidation.

2018, while Airbus has reported 4.79% of net-profit margin. Which indicates that BAE is more

efficient to generate net-income as in comparison with its competitor Airbus (Airbus Annual

Report, 2018).

Gross Profit ratio: This ratio demonstrates how effective corporation is in generation of gross

income/profit only though its main operations without considering indirect incomes and

expenses. This exhibits company's operational effectiveness. Here below table shows GP ratios

of BAE and Airbus:

Year-2018 BAE Systems Airbus SE

Gross Profit Ratio (%) 65.16% 13.79%

BAE System has reported gross profit of 65.16% in year 2018 while Airbus SE's gross

profitability ratio is 13.79% in year 2018. It indicates that BAE is much more efficient to attain

gross profits and operating more effectively as in comparison with Airbus which is core

competitor of company (BAE Systems Annual Report, 2018).

Liquidity: Ratio analysis also aid in assessment of liquidity position of corporation either in

short-term or long term. For short-term liquidity position current asset ratio and quick ratio are

used while for analysing long-term liquidity position debt to equity ratio is used generally (Ayub,

2013). In this context following are the key ratios for evaluation of liquidity position as follows:

Current Ratio: It is key ratio which assist in evaluation of relationship between company's

current liabilities and current assets. Industry's average current ratio are generally recognised as

2:1. It is a short-term liquidity ratio which shows how efficiently company can pay its current

debts by using current assets.

Year-2018 BAE Systems Airbus SE

Current Ratio 1.0289 0.96

Above table shows that current ratio of both corporations are below the industry average.

BAE's current ratio is 1.03 approx while Airbus' current ratio is 0.96 approx. Which indicates

that BAE's short-term liquidity position is more favourable as in comparison with its competitive

corporation Airbus. Although company has to focus in this area as it is below the industry

average which may lead to negative working capital and increase the chances of liquidation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company can improve this ratio by restructuring of short-term debts and timely collection of

trade-payables.

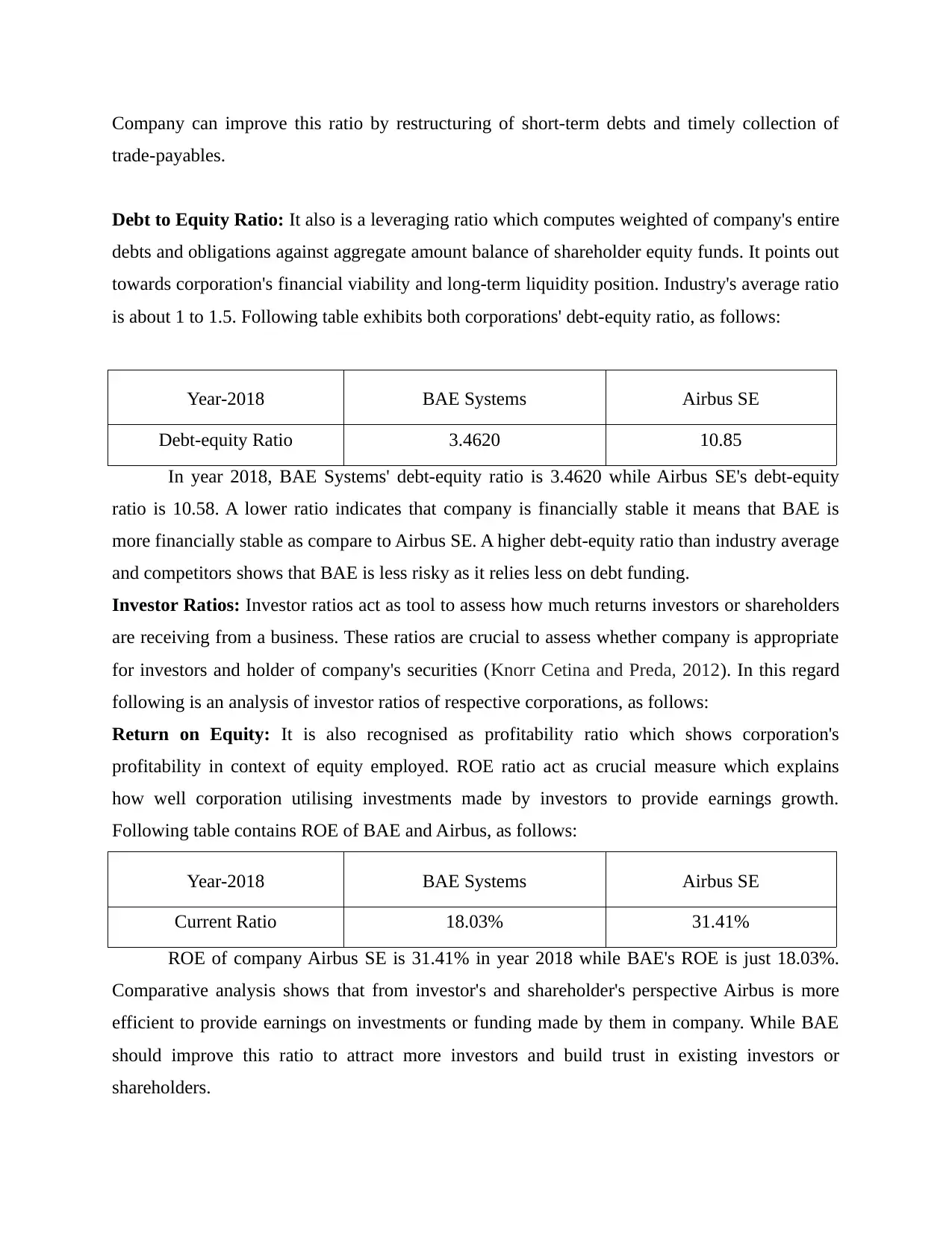

Debt to Equity Ratio: It also is a leveraging ratio which computes weighted of company's entire

debts and obligations against aggregate amount balance of shareholder equity funds. It points out

towards corporation's financial viability and long-term liquidity position. Industry's average ratio

is about 1 to 1.5. Following table exhibits both corporations' debt-equity ratio, as follows:

Year-2018 BAE Systems Airbus SE

Debt-equity Ratio 3.4620 10.85

In year 2018, BAE Systems' debt-equity ratio is 3.4620 while Airbus SE's debt-equity

ratio is 10.58. A lower ratio indicates that company is financially stable it means that BAE is

more financially stable as compare to Airbus SE. A higher debt-equity ratio than industry average

and competitors shows that BAE is less risky as it relies less on debt funding.

Investor Ratios: Investor ratios act as tool to assess how much returns investors or shareholders

are receiving from a business. These ratios are crucial to assess whether company is appropriate

for investors and holder of company's securities (Knorr Cetina and Preda, 2012). In this regard

following is an analysis of investor ratios of respective corporations, as follows:

Return on Equity: It is also recognised as profitability ratio which shows corporation's

profitability in context of equity employed. ROE ratio act as crucial measure which explains

how well corporation utilising investments made by investors to provide earnings growth.

Following table contains ROE of BAE and Airbus, as follows:

Year-2018 BAE Systems Airbus SE

Current Ratio 18.03% 31.41%

ROE of company Airbus SE is 31.41% in year 2018 while BAE's ROE is just 18.03%.

Comparative analysis shows that from investor's and shareholder's perspective Airbus is more

efficient to provide earnings on investments or funding made by them in company. While BAE

should improve this ratio to attract more investors and build trust in existing investors or

shareholders.

trade-payables.

Debt to Equity Ratio: It also is a leveraging ratio which computes weighted of company's entire

debts and obligations against aggregate amount balance of shareholder equity funds. It points out

towards corporation's financial viability and long-term liquidity position. Industry's average ratio

is about 1 to 1.5. Following table exhibits both corporations' debt-equity ratio, as follows:

Year-2018 BAE Systems Airbus SE

Debt-equity Ratio 3.4620 10.85

In year 2018, BAE Systems' debt-equity ratio is 3.4620 while Airbus SE's debt-equity

ratio is 10.58. A lower ratio indicates that company is financially stable it means that BAE is

more financially stable as compare to Airbus SE. A higher debt-equity ratio than industry average

and competitors shows that BAE is less risky as it relies less on debt funding.

Investor Ratios: Investor ratios act as tool to assess how much returns investors or shareholders

are receiving from a business. These ratios are crucial to assess whether company is appropriate

for investors and holder of company's securities (Knorr Cetina and Preda, 2012). In this regard

following is an analysis of investor ratios of respective corporations, as follows:

Return on Equity: It is also recognised as profitability ratio which shows corporation's

profitability in context of equity employed. ROE ratio act as crucial measure which explains

how well corporation utilising investments made by investors to provide earnings growth.

Following table contains ROE of BAE and Airbus, as follows:

Year-2018 BAE Systems Airbus SE

Current Ratio 18.03% 31.41%

ROE of company Airbus SE is 31.41% in year 2018 while BAE's ROE is just 18.03%.

Comparative analysis shows that from investor's and shareholder's perspective Airbus is more

efficient to provide earnings on investments or funding made by them in company. While BAE

should improve this ratio to attract more investors and build trust in existing investors or

shareholders.

(b). Limitations on the usefulness of ratio analysis:

Historical data and Financial Statements limitation: Ratios are generally assessed

through application of figures stated in FS and other historical previous year data. So if there any

error exists or limitation attached with such data or stated figure it will definitely affect the

outcomes of ratio analysis.

Distinct Accounting Policies: Differentiation in application of accounting policies like

depreciation accounting, valuing inventories etc. in different corporation makes it difficult to

make comparison among tow corporations.

Quantitative Analysis: Ratio analysis is an computational approach which involves only

monetary and quantitative data. Sometimes it act as limitation because it consider only

quantitative aspect and lack of consideration of qualitative aspect lead to misleading analysis.

Impact of Inflation: Annual accounts are formulated on periodic basis so there are

timing differences exists among two or more year's accounts. In case inflation arsed between two

periods then the actual prices and effect of inflation are not reliably reflected in accounts. So no.

across the distinct-distinct periods are not so much comparable until adjustments regarding

inflation are not made in accounts (Richards, 2012).

Company valuation:

(a) Valuation of BAE Systems Plc:

Asset Based Valuation: It is type of valuation which primarily emphasises upon corporation's

assets value after subtracting of all external-liabilities. It is simple and widely used method in

which net assets are recognised as value of business normally (Prasad, 2015).

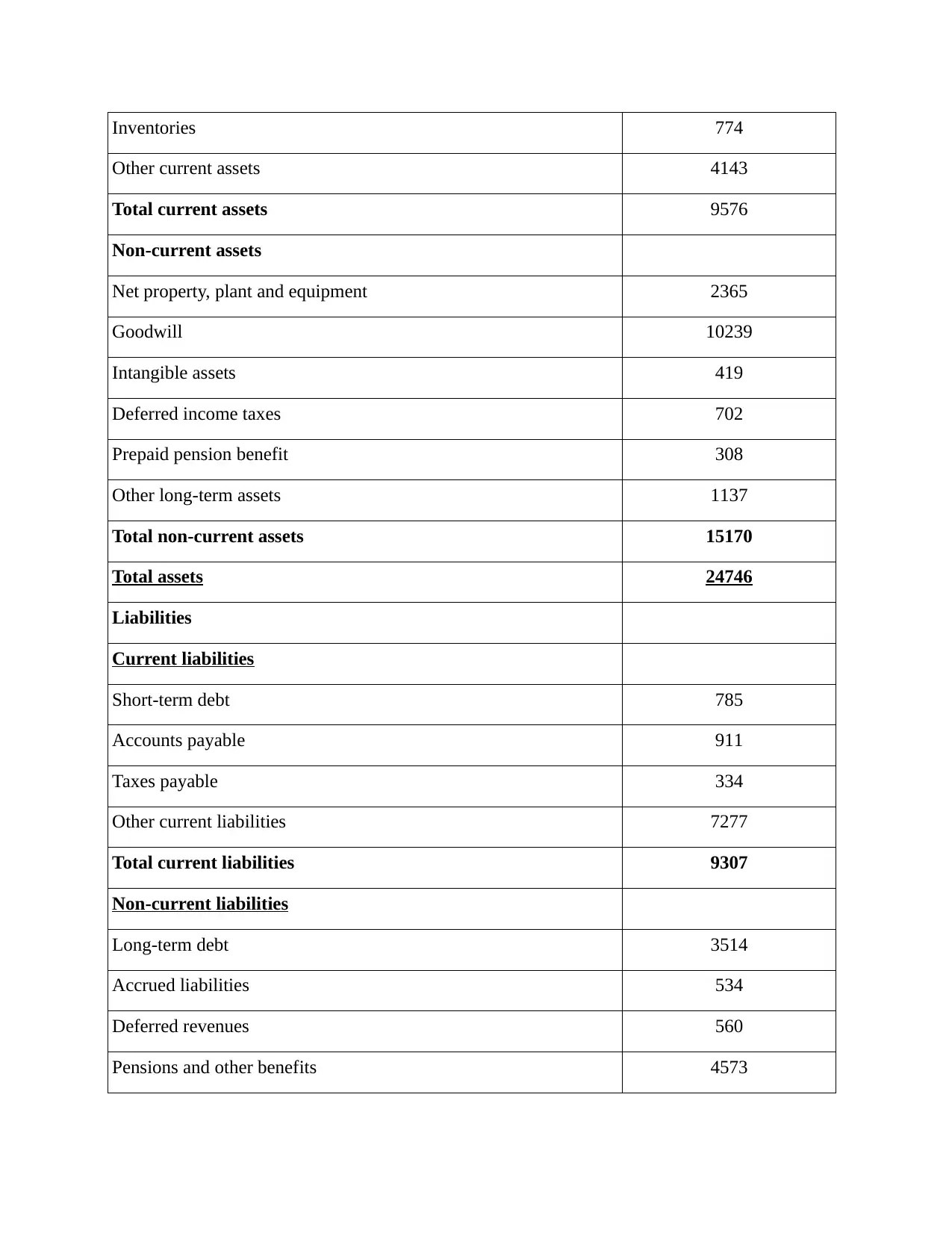

Asset Based Valuation of BAE System Plc

Year-2018 (GBP in

millions)

Assets

Current assets

Cash and cash equivalents 3232

Receivables 1427

Historical data and Financial Statements limitation: Ratios are generally assessed

through application of figures stated in FS and other historical previous year data. So if there any

error exists or limitation attached with such data or stated figure it will definitely affect the

outcomes of ratio analysis.

Distinct Accounting Policies: Differentiation in application of accounting policies like

depreciation accounting, valuing inventories etc. in different corporation makes it difficult to

make comparison among tow corporations.

Quantitative Analysis: Ratio analysis is an computational approach which involves only

monetary and quantitative data. Sometimes it act as limitation because it consider only

quantitative aspect and lack of consideration of qualitative aspect lead to misleading analysis.

Impact of Inflation: Annual accounts are formulated on periodic basis so there are

timing differences exists among two or more year's accounts. In case inflation arsed between two

periods then the actual prices and effect of inflation are not reliably reflected in accounts. So no.

across the distinct-distinct periods are not so much comparable until adjustments regarding

inflation are not made in accounts (Richards, 2012).

Company valuation:

(a) Valuation of BAE Systems Plc:

Asset Based Valuation: It is type of valuation which primarily emphasises upon corporation's

assets value after subtracting of all external-liabilities. It is simple and widely used method in

which net assets are recognised as value of business normally (Prasad, 2015).

Asset Based Valuation of BAE System Plc

Year-2018 (GBP in

millions)

Assets

Current assets

Cash and cash equivalents 3232

Receivables 1427

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventories 774

Other current assets 4143

Total current assets 9576

Non-current assets

Net property, plant and equipment 2365

Goodwill 10239

Intangible assets 419

Deferred income taxes 702

Prepaid pension benefit 308

Other long-term assets 1137

Total non-current assets 15170

Total assets 24746

Liabilities

Current liabilities

Short-term debt 785

Accounts payable 911

Taxes payable 334

Other current liabilities 7277

Total current liabilities 9307

Non-current liabilities

Long-term debt 3514

Accrued liabilities 534

Deferred revenues 560

Pensions and other benefits 4573

Other current assets 4143

Total current assets 9576

Non-current assets

Net property, plant and equipment 2365

Goodwill 10239

Intangible assets 419

Deferred income taxes 702

Prepaid pension benefit 308

Other long-term assets 1137

Total non-current assets 15170

Total assets 24746

Liabilities

Current liabilities

Short-term debt 785

Accounts payable 911

Taxes payable 334

Other current liabilities 7277

Total current liabilities 9307

Non-current liabilities

Long-term debt 3514

Accrued liabilities 534

Deferred revenues 560

Pensions and other benefits 4573

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

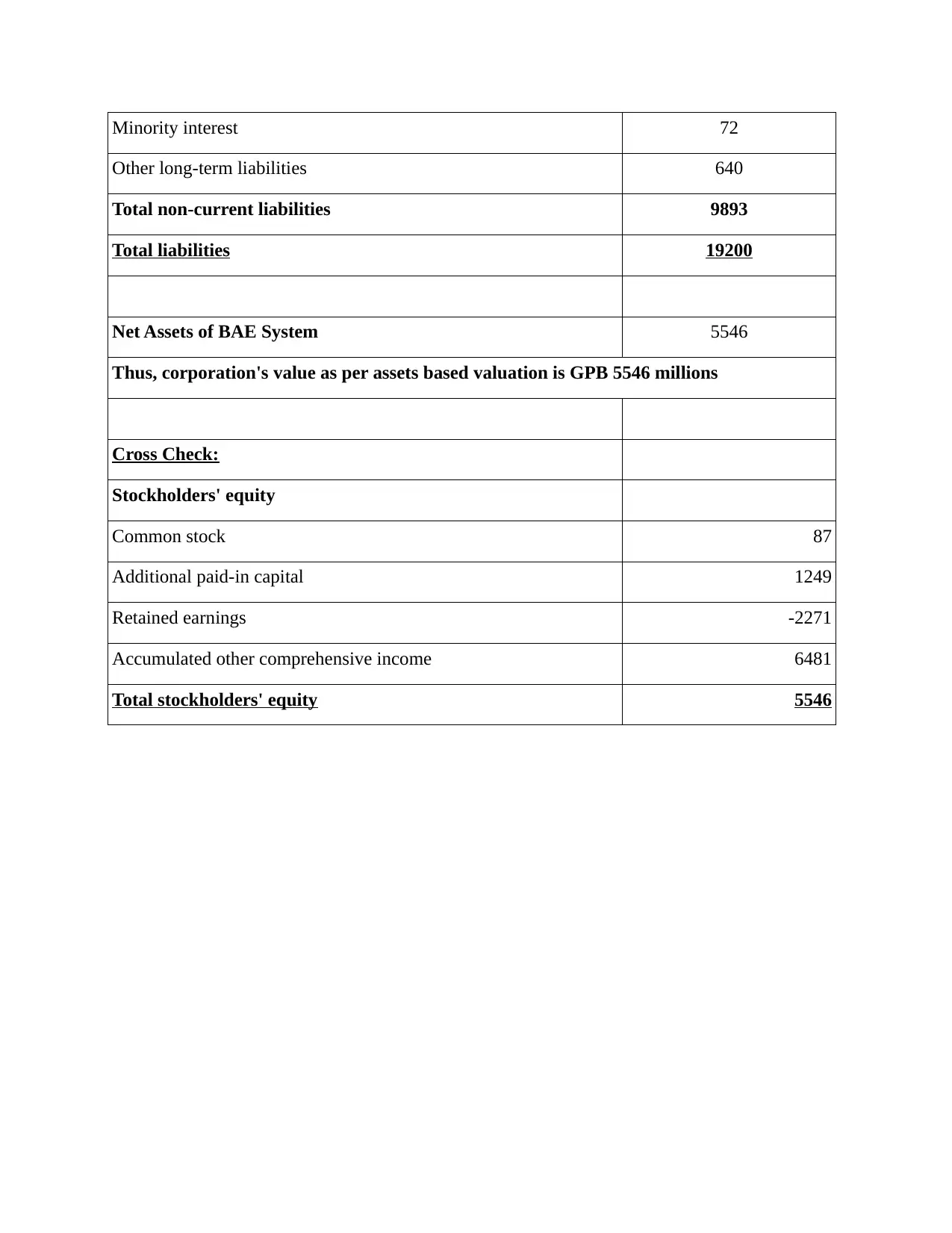

Minority interest 72

Other long-term liabilities 640

Total non-current liabilities 9893

Total liabilities 19200

Net Assets of BAE System 5546

Thus, corporation's value as per assets based valuation is GPB 5546 millions

Cross Check:

Stockholders' equity

Common stock 87

Additional paid-in capital 1249

Retained earnings -2271

Accumulated other comprehensive income 6481

Total stockholders' equity 5546

Other long-term liabilities 640

Total non-current liabilities 9893

Total liabilities 19200

Net Assets of BAE System 5546

Thus, corporation's value as per assets based valuation is GPB 5546 millions

Cross Check:

Stockholders' equity

Common stock 87

Additional paid-in capital 1249

Retained earnings -2271

Accumulated other comprehensive income 6481

Total stockholders' equity 5546

Analysis: Above computation of valuation of BAE System Plc based on Net-asset method shows

that company's net asset valuation is 5546 million while company's aggregate asset amount is

24746 million and total external liabilities are of 19200 million.

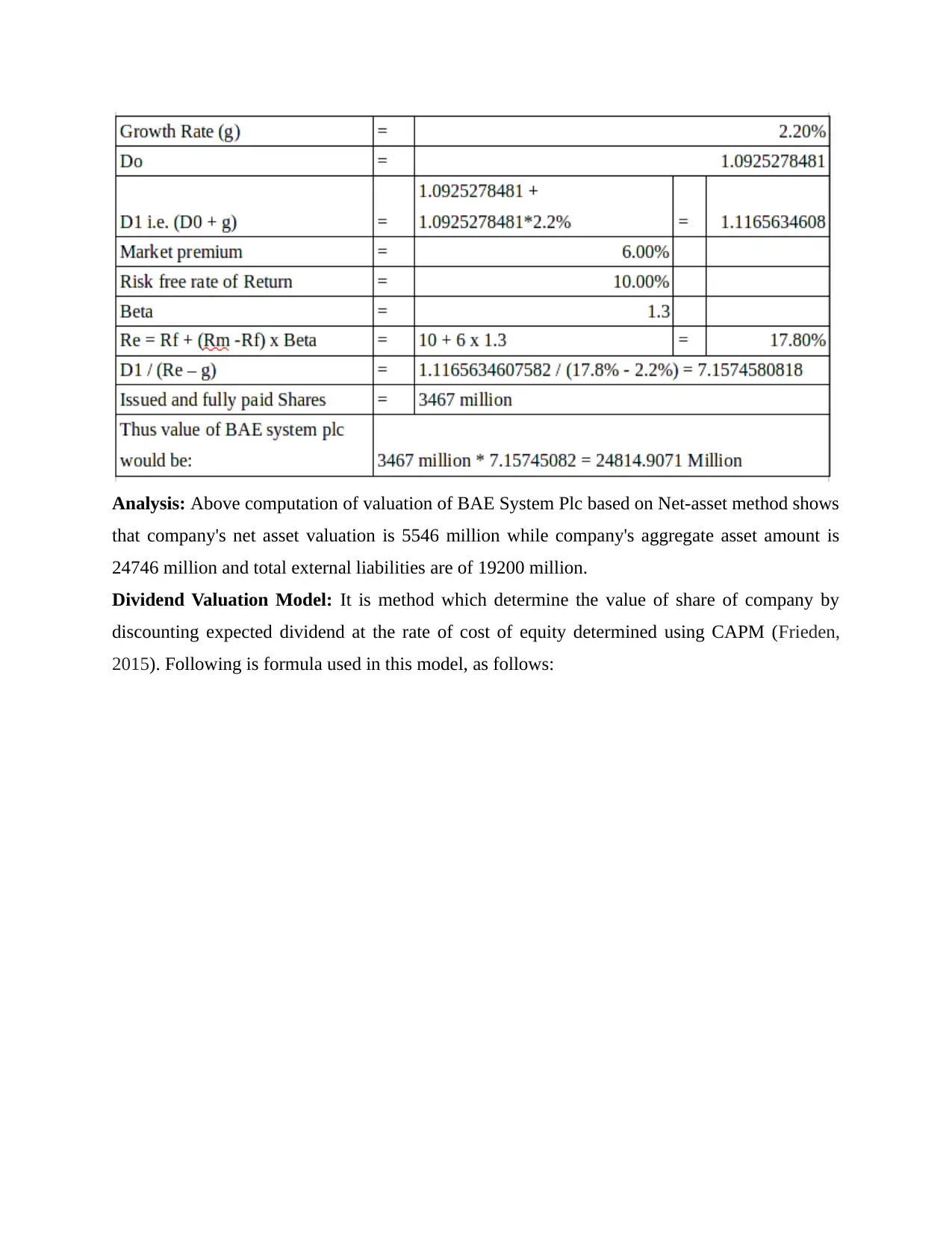

Dividend Valuation Model: It is method which determine the value of share of company by

discounting expected dividend at the rate of cost of equity determined using CAPM (Frieden,

2015). Following is formula used in this model, as follows:

that company's net asset valuation is 5546 million while company's aggregate asset amount is

24746 million and total external liabilities are of 19200 million.

Dividend Valuation Model: It is method which determine the value of share of company by

discounting expected dividend at the rate of cost of equity determined using CAPM (Frieden,

2015). Following is formula used in this model, as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

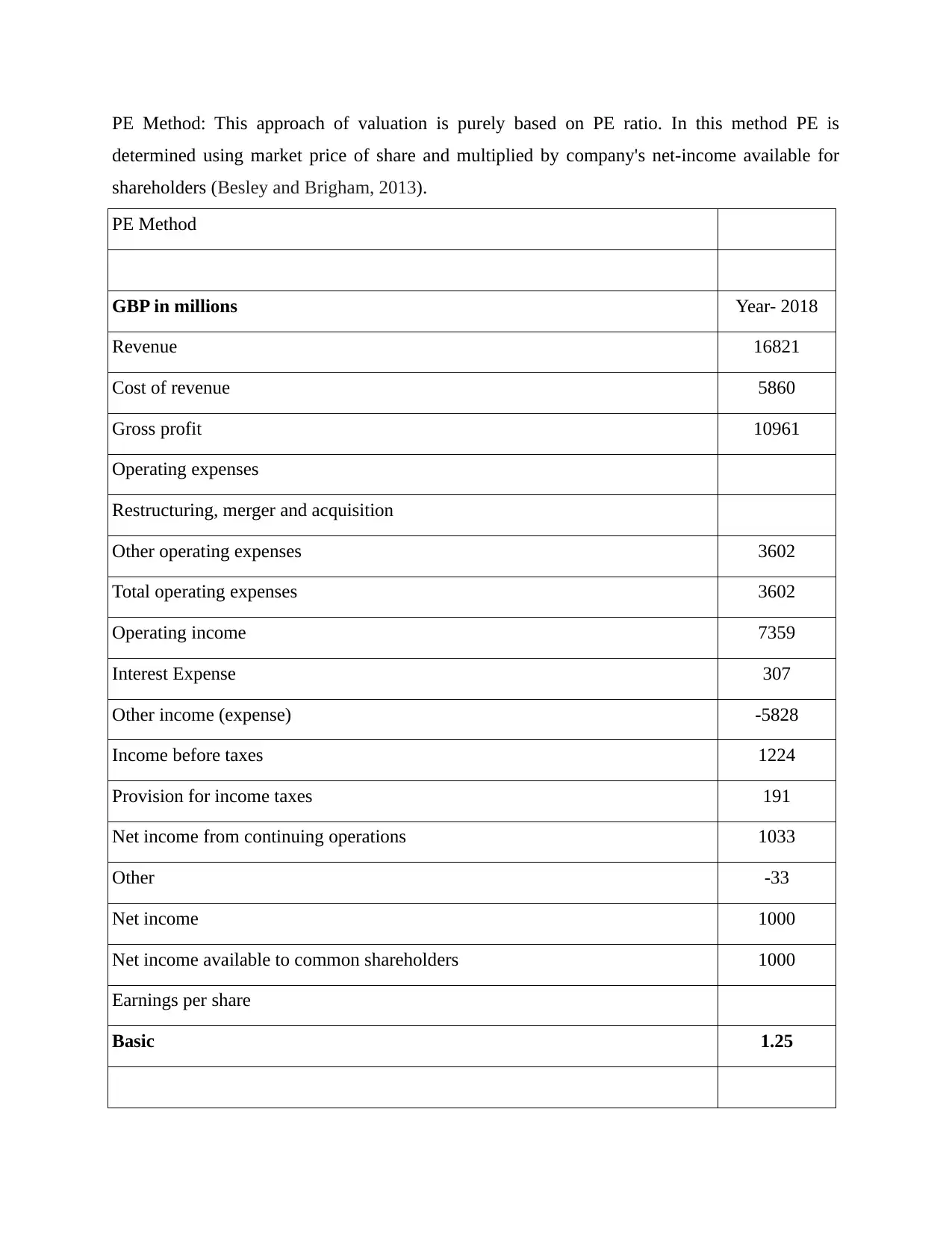

PE Method: This approach of valuation is purely based on PE ratio. In this method PE is

determined using market price of share and multiplied by company's net-income available for

shareholders (Besley and Brigham, 2013).

PE Method

GBP in millions Year- 2018

Revenue 16821

Cost of revenue 5860

Gross profit 10961

Operating expenses

Restructuring, merger and acquisition

Other operating expenses 3602

Total operating expenses 3602

Operating income 7359

Interest Expense 307

Other income (expense) -5828

Income before taxes 1224

Provision for income taxes 191

Net income from continuing operations 1033

Other -33

Net income 1000

Net income available to common shareholders 1000

Earnings per share

Basic 1.25

determined using market price of share and multiplied by company's net-income available for

shareholders (Besley and Brigham, 2013).

PE Method

GBP in millions Year- 2018

Revenue 16821

Cost of revenue 5860

Gross profit 10961

Operating expenses

Restructuring, merger and acquisition

Other operating expenses 3602

Total operating expenses 3602

Operating income 7359

Interest Expense 307

Other income (expense) -5828

Income before taxes 1224

Provision for income taxes 191

Net income from continuing operations 1033

Other -33

Net income 1000

Net income available to common shareholders 1000

Earnings per share

Basic 1.25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

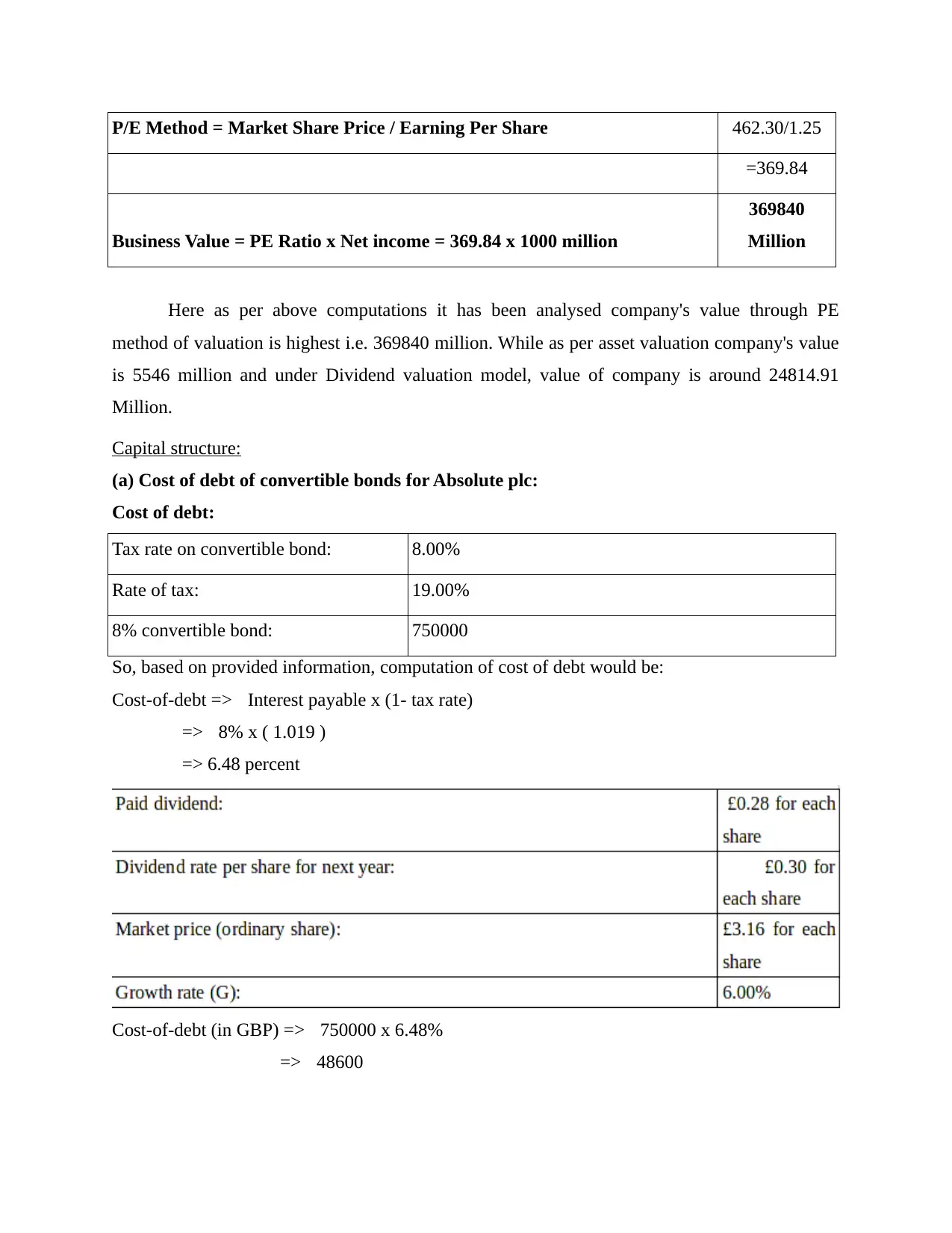

P/E Method = Market Share Price / Earning Per Share 462.30/1.25

=369.84

Business Value = PE Ratio x Net income = 369.84 x 1000 million

369840

Million

Here as per above computations it has been analysed company's value through PE

method of valuation is highest i.e. 369840 million. While as per asset valuation company's value

is 5546 million and under Dividend valuation model, value of company is around 24814.91

Million.

Capital structure:

(a) Cost of debt of convertible bonds for Absolute plc:

Cost of debt:

Tax rate on convertible bond: 8.00%

Rate of tax: 19.00%

8% convertible bond: 750000

So, based on provided information, computation of cost of debt would be:

Cost-of-debt => Interest payable x (1- tax rate)

=> 8% x ( 1.019 )

=> 6.48 percent

Cost-of-debt (in GBP) => 750000 x 6.48%

=> 48600

=369.84

Business Value = PE Ratio x Net income = 369.84 x 1000 million

369840

Million

Here as per above computations it has been analysed company's value through PE

method of valuation is highest i.e. 369840 million. While as per asset valuation company's value

is 5546 million and under Dividend valuation model, value of company is around 24814.91

Million.

Capital structure:

(a) Cost of debt of convertible bonds for Absolute plc:

Cost of debt:

Tax rate on convertible bond: 8.00%

Rate of tax: 19.00%

8% convertible bond: 750000

So, based on provided information, computation of cost of debt would be:

Cost-of-debt => Interest payable x (1- tax rate)

=> 8% x ( 1.019 )

=> 6.48 percent

Cost-of-debt (in GBP) => 750000 x 6.48%

=> 48600

(b) Cost of equity:

So, Cost of equity would be: (Dividend per share / Market price of ordinary share) + g%

= (0.30 / 3.16) + 6 percent

= 9.49 + 6 percent

= 15.49 percent

(c)Weighted average cost of capital:

So, Cost of equity would be: (Dividend per share / Market price of ordinary share) + g%

= (0.30 / 3.16) + 6 percent

= 9.49 + 6 percent

= 15.49 percent

(c)Weighted average cost of capital:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.