Capital Structure Analysis Report: DRB-HICOM and Bermaz Auto Berhad

VerifiedAdded on 2022/08/12

|11

|2261

|19

Report

AI Summary

This report provides a detailed analysis of the capital structure of two Malaysian companies, DRB-HICOM and Bermaz Auto Berhad, from 2014 to 2018. The analysis includes an introduction to both companies, followed by the computation and explanation of relevant financial ratios such as the debt-equity ratio, debt-to-total assets ratio, dividend coverage ratio, and interest coverage ratio. The report then offers a comparative analysis of the capital structures of the two companies, highlighting their similarities and differences in terms of financial leverage, asset financing, dividend policies, and interest obligations. The report concludes with a summary of the findings, emphasizing the importance of capital structure in assessing a company's risk profile and future prospects, and the implications of the observed trends for both companies. The report also references the annual reports of the companies and other academic sources to support the analysis.

Running head: FINANCE

Financial Management II

Name of the Student

Name of the University

Author Note

Financial Management II

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Introduction..................................................................................................................................2

Relevant Ratios for capital structure analysis..............................................................................3

Ratio analysis of Bermaz Auto Berhad........................................................................................6

Comparative analysis...................................................................................................................8

Conclusion...................................................................................................................................9

References..................................................................................................................................10

Table of Contents

Introduction..................................................................................................................................2

Relevant Ratios for capital structure analysis..............................................................................3

Ratio analysis of Bermaz Auto Berhad........................................................................................6

Comparative analysis...................................................................................................................8

Conclusion...................................................................................................................................9

References..................................................................................................................................10

2FINANCE

Introduction

The primary purpose of the report is to conduct a thorough analysis of the capital

structure of two companies operating in Malaysia. After analysing the capital structure of both

the companies, a comparative analysis is conducted on both the companies. The companies

selected for this purpose are DRB-HICOM and Bermaz Auto Berhad.

DRB-HICOM is renowned as one of the largest and most diverse conglomerates in

Malaysia. The main businesses of the entity are conducted in the Automotive, Services and

Properties sector. It is a result of the merger between Heavy Industries Corporation of Malaysia

Berhad (HICOM) and Diversified Resources Berhad (DRB) in 2000 (DRB-HICOM, 2020).

. As per the company’s reports, there are around 70 operating companies within the group with a

total employee strength of 56000. The company is well-known across Malaysia for its Properties

business. The most popular brand of the entity is Glenmarie. This brand has become synonymous

with luxury and quality in relation to residential, commercial and hospitality projects nationwide.

Another popular aspect is the Proton City, a township spread across 4000 acres across Malaysia.

Bermaz Auto Berhad is another Malaysian entity which commenced its operations in

2008 after the merger between Bermaz and Mazda Motor Corporation. The core businesses of

the entity include the distribution and retailing of Mazda vehicles and the provision of after sale

services related to the same. Apart from these, the business also includes the distribution of

vehicles through third party branches in Philippines (Bermaz Auto Berhad, 2020). As a part of

conducting the business smoothly, the business is also involved in the local assembly of Mazda

Vehicles through the use of local and imported Mazda-supplied parts. Apart from these, the

entity is also involved in the overseas distribution of vehicles assembled in Malaysia.

Introduction

The primary purpose of the report is to conduct a thorough analysis of the capital

structure of two companies operating in Malaysia. After analysing the capital structure of both

the companies, a comparative analysis is conducted on both the companies. The companies

selected for this purpose are DRB-HICOM and Bermaz Auto Berhad.

DRB-HICOM is renowned as one of the largest and most diverse conglomerates in

Malaysia. The main businesses of the entity are conducted in the Automotive, Services and

Properties sector. It is a result of the merger between Heavy Industries Corporation of Malaysia

Berhad (HICOM) and Diversified Resources Berhad (DRB) in 2000 (DRB-HICOM, 2020).

. As per the company’s reports, there are around 70 operating companies within the group with a

total employee strength of 56000. The company is well-known across Malaysia for its Properties

business. The most popular brand of the entity is Glenmarie. This brand has become synonymous

with luxury and quality in relation to residential, commercial and hospitality projects nationwide.

Another popular aspect is the Proton City, a township spread across 4000 acres across Malaysia.

Bermaz Auto Berhad is another Malaysian entity which commenced its operations in

2008 after the merger between Bermaz and Mazda Motor Corporation. The core businesses of

the entity include the distribution and retailing of Mazda vehicles and the provision of after sale

services related to the same. Apart from these, the business also includes the distribution of

vehicles through third party branches in Philippines (Bermaz Auto Berhad, 2020). As a part of

conducting the business smoothly, the business is also involved in the local assembly of Mazda

Vehicles through the use of local and imported Mazda-supplied parts. Apart from these, the

entity is also involved in the overseas distribution of vehicles assembled in Malaysia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

Relevant Ratios for capital structure analysis

Capital structure ratios of DRB- HICOM

Particulars Formula 2014 2015 2016 2017 2018

Total Debt 71270

63

69097

31

68647

45

62937

75

57851

12

Total Equity 73114

83

75705

86

85024

43

10138

515

10285

872

Debt-Equity Ratio Total Debt/Total Equity 0.974

777

0.912

708

0.807

385

0.620

779

0.562

433

Total Debt 71270

63

69097

31

68647

45

62937

75

57851

12

Total Assets 39753

022

42359

422

42041

503

43847

849

43195

433

Debt to Total Assets

Ratio

Total Debt/Total Assets

Ratio

0.179

284

0.163

121

0.163

285

0.143

537

0.133

929

Earnings per share 0.239

1

0.155

3

-

0.513

5

-0.235 0.257

8

Dividend per share 0.6 0.6 0.2 0.1 0.3

Dividend Coverage Earnings per 0.398 0.258 - -2.35 0.86

Relevant Ratios for capital structure analysis

Capital structure ratios of DRB- HICOM

Particulars Formula 2014 2015 2016 2017 2018

Total Debt 71270

63

69097

31

68647

45

62937

75

57851

12

Total Equity 73114

83

75705

86

85024

43

10138

515

10285

872

Debt-Equity Ratio Total Debt/Total Equity 0.974

777

0.912

708

0.807

385

0.620

779

0.562

433

Total Debt 71270

63

69097

31

68647

45

62937

75

57851

12

Total Assets 39753

022

42359

422

42041

503

43847

849

43195

433

Debt to Total Assets

Ratio

Total Debt/Total Assets

Ratio

0.179

284

0.163

121

0.163

285

0.143

537

0.133

929

Earnings per share 0.239

1

0.155

3

-

0.513

5

-0.235 0.257

8

Dividend per share 0.6 0.6 0.2 0.1 0.3

Dividend Coverage Earnings per 0.398 0.258 - -2.35 0.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

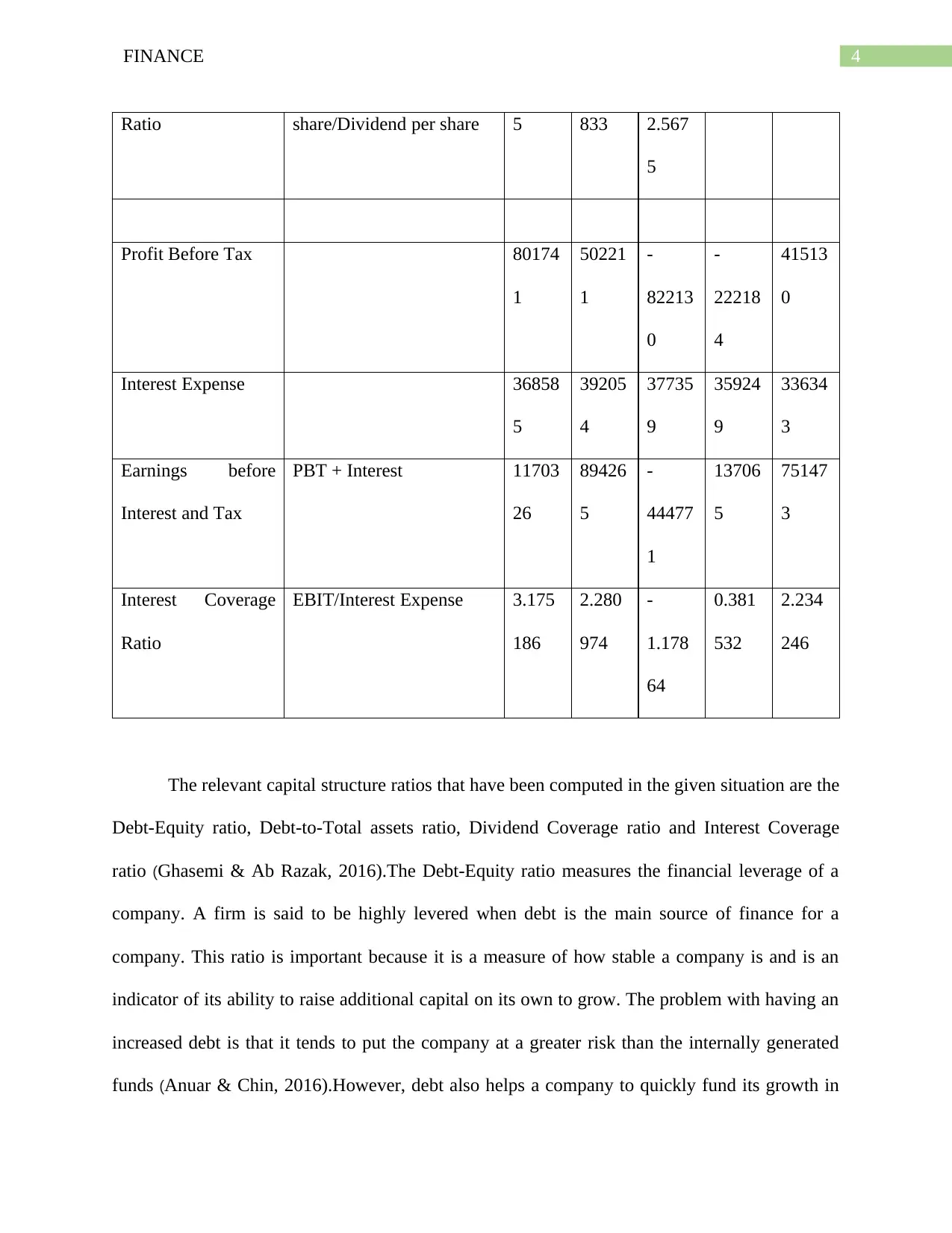

4FINANCE

Ratio share/Dividend per share 5 833 2.567

5

Profit Before Tax 80174

1

50221

1

-

82213

0

-

22218

4

41513

0

Interest Expense 36858

5

39205

4

37735

9

35924

9

33634

3

Earnings before

Interest and Tax

PBT + Interest 11703

26

89426

5

-

44477

1

13706

5

75147

3

Interest Coverage

Ratio

EBIT/Interest Expense 3.175

186

2.280

974

-

1.178

64

0.381

532

2.234

246

The relevant capital structure ratios that have been computed in the given situation are the

Debt-Equity ratio, Debt-to-Total assets ratio, Dividend Coverage ratio and Interest Coverage

ratio (Ghasemi & Ab Razak, 2016).The Debt-Equity ratio measures the financial leverage of a

company. A firm is said to be highly levered when debt is the main source of finance for a

company. This ratio is important because it is a measure of how stable a company is and is an

indicator of its ability to raise additional capital on its own to grow. The problem with having an

increased debt is that it tends to put the company at a greater risk than the internally generated

funds (Anuar & Chin, 2016).However, debt also helps a company to quickly fund its growth in

Ratio share/Dividend per share 5 833 2.567

5

Profit Before Tax 80174

1

50221

1

-

82213

0

-

22218

4

41513

0

Interest Expense 36858

5

39205

4

37735

9

35924

9

33634

3

Earnings before

Interest and Tax

PBT + Interest 11703

26

89426

5

-

44477

1

13706

5

75147

3

Interest Coverage

Ratio

EBIT/Interest Expense 3.175

186

2.280

974

-

1.178

64

0.381

532

2.234

246

The relevant capital structure ratios that have been computed in the given situation are the

Debt-Equity ratio, Debt-to-Total assets ratio, Dividend Coverage ratio and Interest Coverage

ratio (Ghasemi & Ab Razak, 2016).The Debt-Equity ratio measures the financial leverage of a

company. A firm is said to be highly levered when debt is the main source of finance for a

company. This ratio is important because it is a measure of how stable a company is and is an

indicator of its ability to raise additional capital on its own to grow. The problem with having an

increased debt is that it tends to put the company at a greater risk than the internally generated

funds (Anuar & Chin, 2016).However, debt also helps a company to quickly fund its growth in

5FINANCE

the short term. In case of DRB-HCOM, it is evident that the entity was highly levered in 2014

with a ratio as high as 0.97. However, the company has succeeded in reducing its debt as a part

of the capital to 0.56 by 2018. Hence, the company’s risk of going bankrupt has come down

significantly over the past five years. The company has a less risky capital structure in the

present day than it had previously.

The debt to assets ratio is a measure of the total debt that the company has invested when

compared to the total assets owned by it. The main purpose of analysing this ratio is to

understand the amount of assets of a company which were financed by the creditors. While

having a large number of assets is an indicator of a healthy company performance, it cannot be

the case if it is financed by huge amount of debts. In case of DRB-HICOM, the total debt to

assets ratio of the company has always been as low as 10 percent. This is a good sign as the

company can use the debt and assets as a part of the business and not for purchasing new assets.

This is also an indicator of better operational performance on behalf of the company.

The dividend coverage ratio is a measure of the number of times that a company can pay

dividends to its shareholders. A dividend coverage ratio of greater than one suggests that the

company is able to generate enough earnings during the course of a year to pay dividends to the

shareholders at least once (Fitri, Hosen & Muhari, 2016).A DCR of more than two is an indicator

of an extremely efficient performance by the company. A consistently low levels of DCR is a

cause for concern amongst the shareholders because it suggests that the company will not be able

to pay the dividends in the future. In DRB-HICOM’s situation, the company has generated

consistently low levels of DCR. In 2016, the DCR of the company was at its lowest at -2.5. In

2018, this improved to 0.86, but indicates that the company is unable to generate sufficient

the short term. In case of DRB-HCOM, it is evident that the entity was highly levered in 2014

with a ratio as high as 0.97. However, the company has succeeded in reducing its debt as a part

of the capital to 0.56 by 2018. Hence, the company’s risk of going bankrupt has come down

significantly over the past five years. The company has a less risky capital structure in the

present day than it had previously.

The debt to assets ratio is a measure of the total debt that the company has invested when

compared to the total assets owned by it. The main purpose of analysing this ratio is to

understand the amount of assets of a company which were financed by the creditors. While

having a large number of assets is an indicator of a healthy company performance, it cannot be

the case if it is financed by huge amount of debts. In case of DRB-HICOM, the total debt to

assets ratio of the company has always been as low as 10 percent. This is a good sign as the

company can use the debt and assets as a part of the business and not for purchasing new assets.

This is also an indicator of better operational performance on behalf of the company.

The dividend coverage ratio is a measure of the number of times that a company can pay

dividends to its shareholders. A dividend coverage ratio of greater than one suggests that the

company is able to generate enough earnings during the course of a year to pay dividends to the

shareholders at least once (Fitri, Hosen & Muhari, 2016).A DCR of more than two is an indicator

of an extremely efficient performance by the company. A consistently low levels of DCR is a

cause for concern amongst the shareholders because it suggests that the company will not be able

to pay the dividends in the future. In DRB-HICOM’s situation, the company has generated

consistently low levels of DCR. In 2016, the DCR of the company was at its lowest at -2.5. In

2018, this improved to 0.86, but indicates that the company is unable to generate sufficient

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

profits to pay the amounts to its shareholders in the current year. However, this ratio is not

considered as a great indicator of the future risk faced by a company.

The Interest coverage ratio is the measure of a company’s ability to handle the financial

burdens faced by it. It suggests how well a company is able to pay the interest on the debt taken

by it before the payment of taxes (Werne, 2015). As the amount paid on debt is used as a cover

against the taxes paid by the entity, it can be used to reduce the tax burden of the entity.

However, this ratio should also be greater than one to indicate that a company is performing well

in terms of meeting its obligations. In case of DRB-HICOM, the interest coverage ratio has gone

down on a consistent basis from 2014 to 2016. It went up by 0.38 in 2017 and went as high as

2.34 in 2018.

The capital structure analysis of the entity suggests that the company was highly risk

taking in 2014. However, this risk has come down in the recent years and the amount of debt

employed by the entity as a part of its business also came down by a significant margin.

Similarly, the net profit earned by the entity in 2016 and 2017 was also negative. These suggest

that the entity needs to maintain a better profitability for the benefit of the people investing in it.

Ratio analysis of Bermaz Auto Berhad

Particulars Formula 2014 2015 2016 2017 2018

Total Debt 2598

03

2470

16

3858

77

4632

85

3272

35

Total Equity 3543

94

4925

34

5630

14

4923

97

5245

04

profits to pay the amounts to its shareholders in the current year. However, this ratio is not

considered as a great indicator of the future risk faced by a company.

The Interest coverage ratio is the measure of a company’s ability to handle the financial

burdens faced by it. It suggests how well a company is able to pay the interest on the debt taken

by it before the payment of taxes (Werne, 2015). As the amount paid on debt is used as a cover

against the taxes paid by the entity, it can be used to reduce the tax burden of the entity.

However, this ratio should also be greater than one to indicate that a company is performing well

in terms of meeting its obligations. In case of DRB-HICOM, the interest coverage ratio has gone

down on a consistent basis from 2014 to 2016. It went up by 0.38 in 2017 and went as high as

2.34 in 2018.

The capital structure analysis of the entity suggests that the company was highly risk

taking in 2014. However, this risk has come down in the recent years and the amount of debt

employed by the entity as a part of its business also came down by a significant margin.

Similarly, the net profit earned by the entity in 2016 and 2017 was also negative. These suggest

that the entity needs to maintain a better profitability for the benefit of the people investing in it.

Ratio analysis of Bermaz Auto Berhad

Particulars Formula 2014 2015 2016 2017 2018

Total Debt 2598

03

2470

16

3858

77

4632

85

3272

35

Total Equity 3543

94

4925

34

5630

14

4923

97

5245

04

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

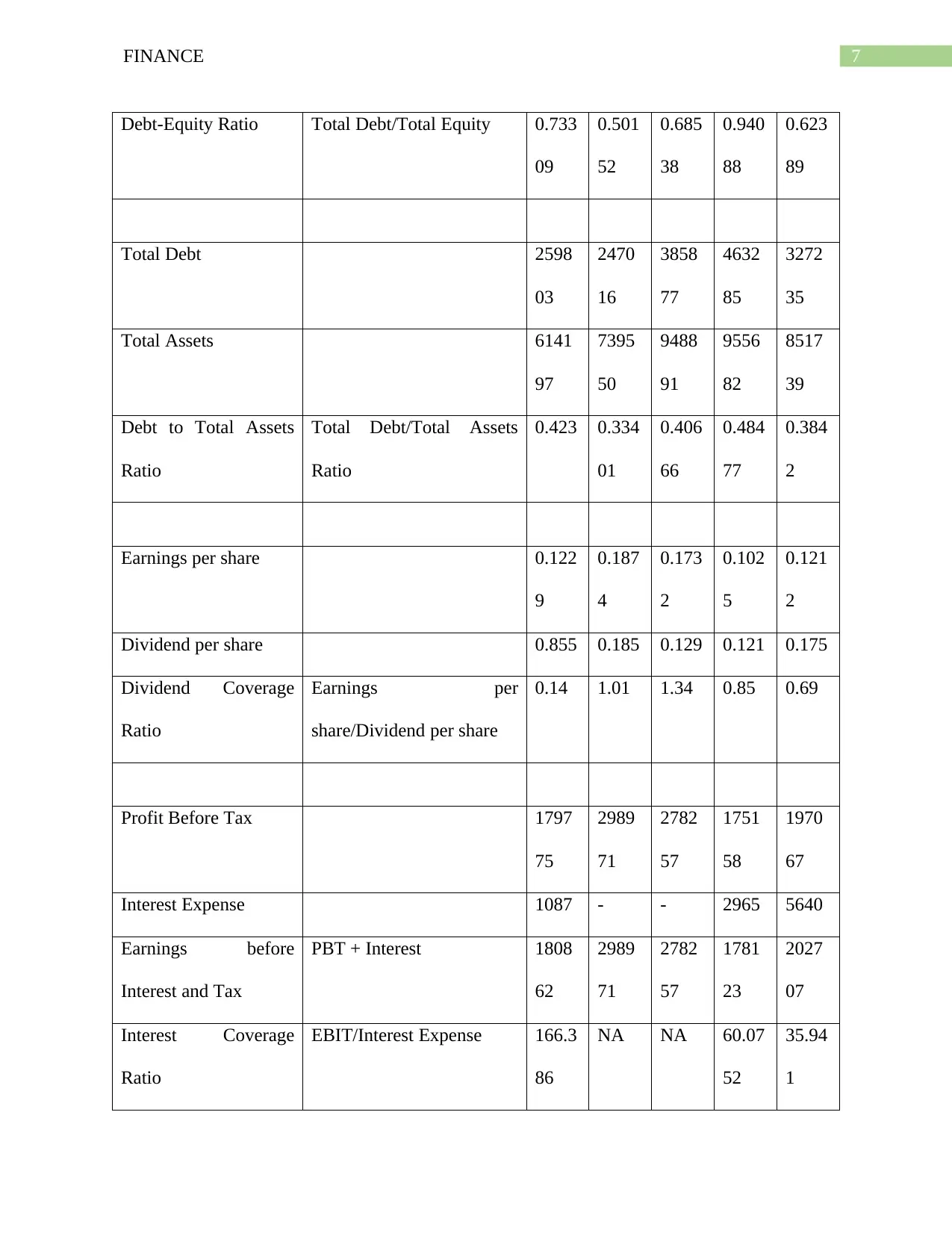

Debt-Equity Ratio Total Debt/Total Equity 0.733

09

0.501

52

0.685

38

0.940

88

0.623

89

Total Debt 2598

03

2470

16

3858

77

4632

85

3272

35

Total Assets 6141

97

7395

50

9488

91

9556

82

8517

39

Debt to Total Assets

Ratio

Total Debt/Total Assets

Ratio

0.423 0.334

01

0.406

66

0.484

77

0.384

2

Earnings per share 0.122

9

0.187

4

0.173

2

0.102

5

0.121

2

Dividend per share 0.855 0.185 0.129 0.121 0.175

Dividend Coverage

Ratio

Earnings per

share/Dividend per share

0.14 1.01 1.34 0.85 0.69

Profit Before Tax 1797

75

2989

71

2782

57

1751

58

1970

67

Interest Expense 1087 - - 2965 5640

Earnings before

Interest and Tax

PBT + Interest 1808

62

2989

71

2782

57

1781

23

2027

07

Interest Coverage

Ratio

EBIT/Interest Expense 166.3

86

NA NA 60.07

52

35.94

1

Debt-Equity Ratio Total Debt/Total Equity 0.733

09

0.501

52

0.685

38

0.940

88

0.623

89

Total Debt 2598

03

2470

16

3858

77

4632

85

3272

35

Total Assets 6141

97

7395

50

9488

91

9556

82

8517

39

Debt to Total Assets

Ratio

Total Debt/Total Assets

Ratio

0.423 0.334

01

0.406

66

0.484

77

0.384

2

Earnings per share 0.122

9

0.187

4

0.173

2

0.102

5

0.121

2

Dividend per share 0.855 0.185 0.129 0.121 0.175

Dividend Coverage

Ratio

Earnings per

share/Dividend per share

0.14 1.01 1.34 0.85 0.69

Profit Before Tax 1797

75

2989

71

2782

57

1751

58

1970

67

Interest Expense 1087 - - 2965 5640

Earnings before

Interest and Tax

PBT + Interest 1808

62

2989

71

2782

57

1781

23

2027

07

Interest Coverage

Ratio

EBIT/Interest Expense 166.3

86

NA NA 60.07

52

35.94

1

8FINANCE

The debt-equity ratio of Bermaz Auto Limited suggests that the entity’s debt-equity ratio

has been fluctuating over the years. It was as high as 0.94088 in 2017 and came down to 0.62389

in 2018. This suggests that the entity is looking to become more stable in terms of its operations.

The total debt to assets ratio of the entity also suggests that the entity is not employing the debt

funds for the purchase of assets. The dividend cover of this entity is also not very high and the

highest ratio in the past five years is 1.34. This indicates that the entity has not levied its focus

sufficiently on the payment of dividends from the earnings made by it in a given financial year.

The interest coverage ratio of the expense in the years 2016 and 2017 was very high as it did not

implement any debt funds on which interest had to be paid as a part of the expenses. However,

the debt funds and interest expenditure by the company have grown in recent years. This

suggests that the entity is looking to quickly expand its business in the short run.

Comparative analysis

In this case, the analysis was conducted between DRB-HICOM and Bermaz Auto Berhad

to compare and contrast the capital structure of both the entities over a period of 5 years. The

analysis suggests that both the entities have a similar structure in terms of employing debt as a

part of the business. The debt-equity ratio of both the entities in 2018 was lower than 0.65. The

debt to asset ratio of DRB-HICOM, however was more than that of Bermaz Auto Berhad in the

year 2018. This means that the assets generated by DRB are more dependent on the availability

of debt funds to be utilised in the business. The Dividend coverage ratio of Bermaz is much

better than that of DRB, which has failed to generate sufficient funds as a part of the distribution

to the shareholders. This also means that the operational stability of DRB is lower. The people

investing in both these entities are also unable to generate sufficient funds necessary to provide

returns to the shareholders. The interest coverage ratio of Bermaz Auto is better than that of

The debt-equity ratio of Bermaz Auto Limited suggests that the entity’s debt-equity ratio

has been fluctuating over the years. It was as high as 0.94088 in 2017 and came down to 0.62389

in 2018. This suggests that the entity is looking to become more stable in terms of its operations.

The total debt to assets ratio of the entity also suggests that the entity is not employing the debt

funds for the purchase of assets. The dividend cover of this entity is also not very high and the

highest ratio in the past five years is 1.34. This indicates that the entity has not levied its focus

sufficiently on the payment of dividends from the earnings made by it in a given financial year.

The interest coverage ratio of the expense in the years 2016 and 2017 was very high as it did not

implement any debt funds on which interest had to be paid as a part of the expenses. However,

the debt funds and interest expenditure by the company have grown in recent years. This

suggests that the entity is looking to quickly expand its business in the short run.

Comparative analysis

In this case, the analysis was conducted between DRB-HICOM and Bermaz Auto Berhad

to compare and contrast the capital structure of both the entities over a period of 5 years. The

analysis suggests that both the entities have a similar structure in terms of employing debt as a

part of the business. The debt-equity ratio of both the entities in 2018 was lower than 0.65. The

debt to asset ratio of DRB-HICOM, however was more than that of Bermaz Auto Berhad in the

year 2018. This means that the assets generated by DRB are more dependent on the availability

of debt funds to be utilised in the business. The Dividend coverage ratio of Bermaz is much

better than that of DRB, which has failed to generate sufficient funds as a part of the distribution

to the shareholders. This also means that the operational stability of DRB is lower. The people

investing in both these entities are also unable to generate sufficient funds necessary to provide

returns to the shareholders. The interest coverage ratio of Bermaz Auto is better than that of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

DRB due to the lack of additional external funds used by the entity. However, in recent years, it

is quite evident that DRB is looking to stabilise itself as a business while Bermaz is looking to

expand its business as a part of its expansion activities.

Conclusion

On the basis of the above discussion, it can be suggested that the capital structure is an

important indicator of the risk profile and future prospects of a business entity. The ratios used to

analyse the same were the debt-equity ratio, debt to total assets ratio, dividend coverage ratio and

the interest coverage ratios of the entity. An analysis of the profiles of the entities suggests that

both of them do not employ huge debts in relation to the equity employed by them as a part of

the business. Similarly, the interest coverage of the entities differs significantly because of the

differences in the external debt funds employed by the company. While Bermaz is looking to

fund its short term growth by employing more debts, DRB is looking to stabilise itself by

reducing the dependence on the excess external funds used by it as a part of the business.

DRB due to the lack of additional external funds used by the entity. However, in recent years, it

is quite evident that DRB is looking to stabilise itself as a business while Bermaz is looking to

expand its business as a part of its expansion activities.

Conclusion

On the basis of the above discussion, it can be suggested that the capital structure is an

important indicator of the risk profile and future prospects of a business entity. The ratios used to

analyse the same were the debt-equity ratio, debt to total assets ratio, dividend coverage ratio and

the interest coverage ratios of the entity. An analysis of the profiles of the entities suggests that

both of them do not employ huge debts in relation to the equity employed by them as a part of

the business. Similarly, the interest coverage of the entities differs significantly because of the

differences in the external debt funds employed by the company. While Bermaz is looking to

fund its short term growth by employing more debts, DRB is looking to stabilise itself by

reducing the dependence on the excess external funds used by it as a part of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

References

Annual Reports – DRB-HICOM Berhad. (2020). Drb-hicom.com. Retrieved 29 February 2020,

from https://www.drb-hicom.com/investors/annual-report/

Anuar, H., & Chin, O. (2016). The development of debt to equity ratio in capital structure model:

A case of micro franchising. Procedia Economics and Finance, 35, 274-280.

Fitri, R. R., Hosen, M. N., & Muhari, S. (2016). Analysis of factors that impact dividend payout

ratio on listed companies at Jakarta islamic index. International Journal of Academic

Research in Accounting, Finance and Management Sciences, 6(2), 87-97.

Ghasemi, M., & Ab Razak, N. H. (2016). The impact of liquidity on the capital structure:

Evidence from Malaysia. International journal of economics and finance, 8(10), 130-139.

Malaysia, N. (2020). Bermaz Auto Berhad. Bauto.com.my. Retrieved 29 February 2020, from

https://www.bauto.com.my/investor-relations.php?p=annual_reports

Werne, J. (2015). An Optimization Of The Liquidity Coverage Ratio.

References

Annual Reports – DRB-HICOM Berhad. (2020). Drb-hicom.com. Retrieved 29 February 2020,

from https://www.drb-hicom.com/investors/annual-report/

Anuar, H., & Chin, O. (2016). The development of debt to equity ratio in capital structure model:

A case of micro franchising. Procedia Economics and Finance, 35, 274-280.

Fitri, R. R., Hosen, M. N., & Muhari, S. (2016). Analysis of factors that impact dividend payout

ratio on listed companies at Jakarta islamic index. International Journal of Academic

Research in Accounting, Finance and Management Sciences, 6(2), 87-97.

Ghasemi, M., & Ab Razak, N. H. (2016). The impact of liquidity on the capital structure:

Evidence from Malaysia. International journal of economics and finance, 8(10), 130-139.

Malaysia, N. (2020). Bermaz Auto Berhad. Bauto.com.my. Retrieved 29 February 2020, from

https://www.bauto.com.my/investor-relations.php?p=annual_reports

Werne, J. (2015). An Optimization Of The Liquidity Coverage Ratio.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.