iMBA Finance Winter 2019: BAE Systems Financial Analysis Report

VerifiedAdded on 2023/01/17

|11

|2354

|55

Report

AI Summary

This finance report provides a detailed analysis of BAE Systems' financial performance for the year 2018. It begins with an introduction to financial management and its importance. The main body of the report includes a comprehensive financial analysis, assessing profitability, liquidity, efficiency, and gearing ratios. It also discusses the limitations of ratio analysis. The report then delves into company valuation, exploring asset-based valuation, dividend valuation methods, and the PE ratio, followed by a critical examination of the valuation methodologies. Furthermore, the report examines the capital structure of Absolute plc, calculating the cost of convertible bonds, cost of equity, and weighted average cost of capital (WACC), along with the difficulties in calculating WACC. The report concludes by summarizing the key findings and emphasizing the importance of financial statements in decision-making and the need for optimal capital structure. The analysis is supported by numerical examples and interpretations of the financial data.

FINANCE MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

CONCLUSION................................................................................................................................1

REFERENCES................................................................................................................................2

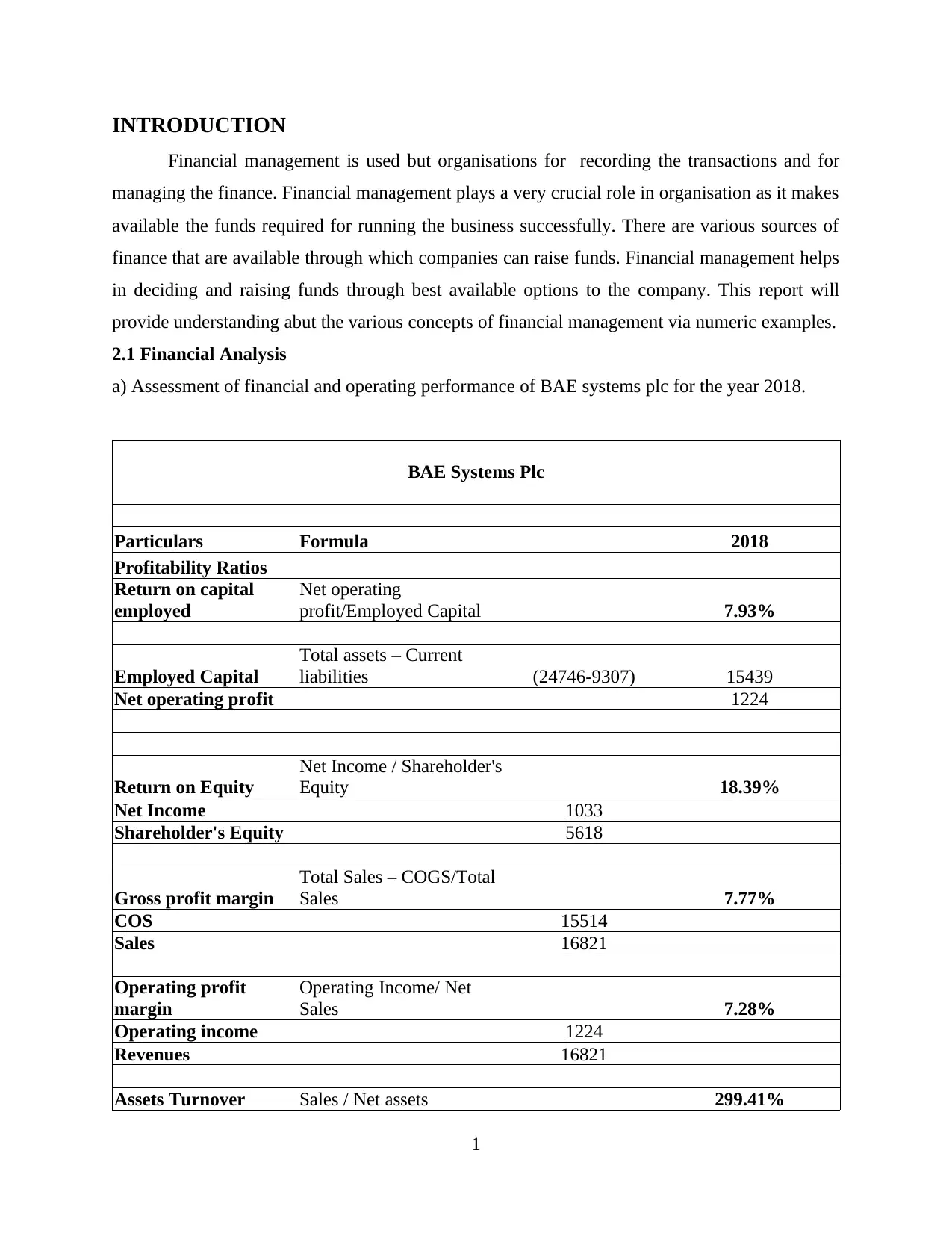

INTRODUCTION

Financial management is used but organisations for recording the transactions and for

managing the finance. Financial management plays a very crucial role in organisation as it makes

available the funds required for running the business successfully. There are various sources of

finance that are available through which companies can raise funds. Financial management helps

in deciding and raising funds through best available options to the company. This report will

provide understanding abut the various concepts of financial management via numeric examples.

2.1 Financial Analysis

a) Assessment of financial and operating performance of BAE systems plc for the year 2018.

BAE Systems Plc

Particulars Formula 2018

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 7.93%

Employed Capital

Total assets – Current

liabilities (24746-9307) 15439

Net operating profit 1224

Return on Equity

Net Income / Shareholder's

Equity 18.39%

Net Income 1033

Shareholder's Equity 5618

Gross profit margin

Total Sales – COGS/Total

Sales 7.77%

COS 15514

Sales 16821

Operating profit

margin

Operating Income/ Net

Sales 7.28%

Operating income 1224

Revenues 16821

Assets Turnover Sales / Net assets 299.41%

1

Financial management is used but organisations for recording the transactions and for

managing the finance. Financial management plays a very crucial role in organisation as it makes

available the funds required for running the business successfully. There are various sources of

finance that are available through which companies can raise funds. Financial management helps

in deciding and raising funds through best available options to the company. This report will

provide understanding abut the various concepts of financial management via numeric examples.

2.1 Financial Analysis

a) Assessment of financial and operating performance of BAE systems plc for the year 2018.

BAE Systems Plc

Particulars Formula 2018

Profitability Ratios

Return on capital

employed

Net operating

profit/Employed Capital 7.93%

Employed Capital

Total assets – Current

liabilities (24746-9307) 15439

Net operating profit 1224

Return on Equity

Net Income / Shareholder's

Equity 18.39%

Net Income 1033

Shareholder's Equity 5618

Gross profit margin

Total Sales – COGS/Total

Sales 7.77%

COS 15514

Sales 16821

Operating profit

margin

Operating Income/ Net

Sales 7.28%

Operating income 1224

Revenues 16821

Assets Turnover Sales / Net assets 299.41%

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

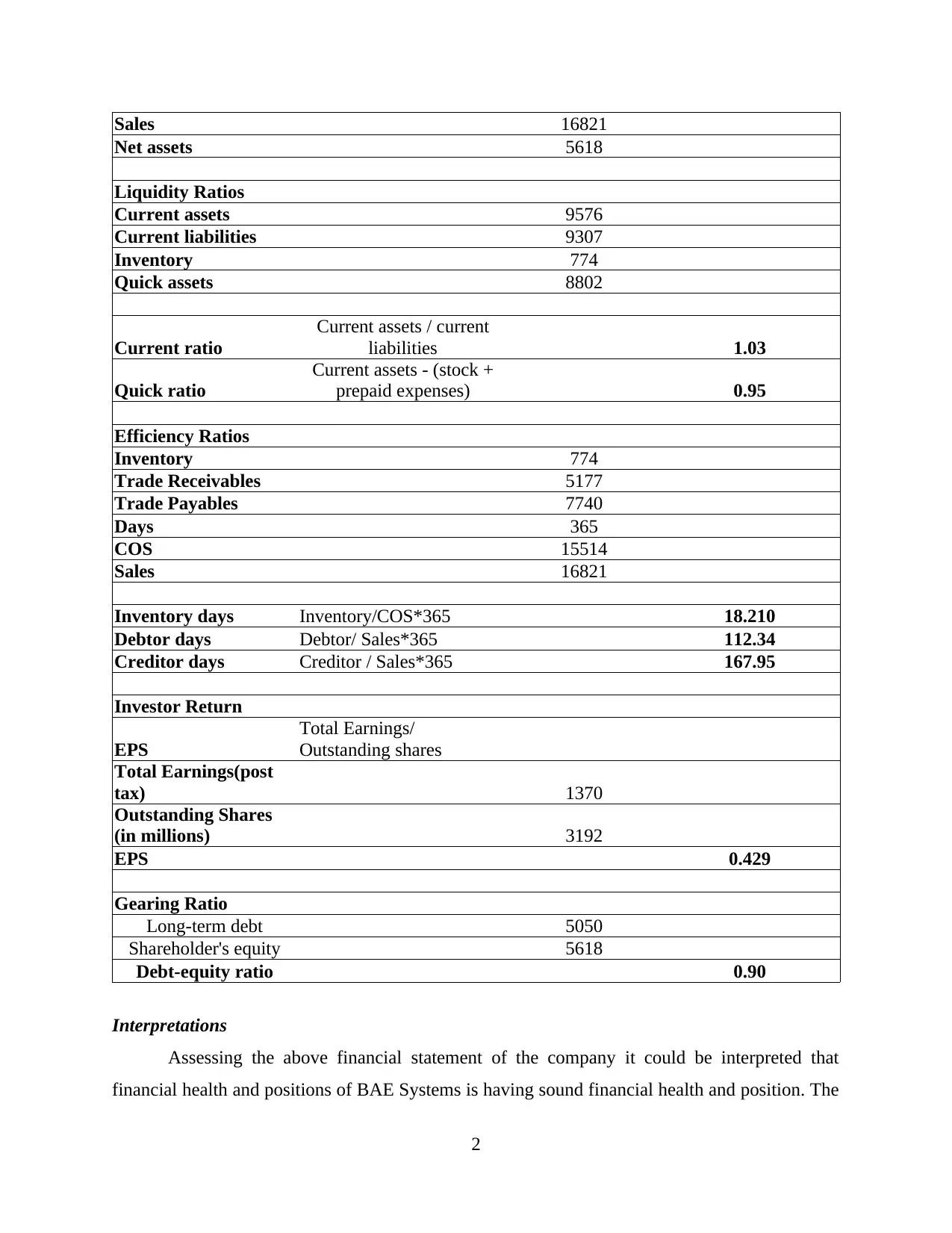

Sales 16821

Net assets 5618

Liquidity Ratios

Current assets 9576

Current liabilities 9307

Inventory 774

Quick assets 8802

Current ratio

Current assets / current

liabilities 1.03

Quick ratio

Current assets - (stock +

prepaid expenses) 0.95

Efficiency Ratios

Inventory 774

Trade Receivables 5177

Trade Payables 7740

Days 365

COS 15514

Sales 16821

Inventory days Inventory/COS*365 18.210

Debtor days Debtor/ Sales*365 112.34

Creditor days Creditor / Sales*365 167.95

Investor Return

EPS

Total Earnings/

Outstanding shares

Total Earnings(post

tax) 1370

Outstanding Shares

(in millions) 3192

EPS 0.429

Gearing Ratio

Long-term debt 5050

Shareholder's equity 5618

Debt-equity ratio 0.90

Interpretations

Assessing the above financial statement of the company it could be interpreted that

financial health and positions of BAE Systems is having sound financial health and position. The

2

Net assets 5618

Liquidity Ratios

Current assets 9576

Current liabilities 9307

Inventory 774

Quick assets 8802

Current ratio

Current assets / current

liabilities 1.03

Quick ratio

Current assets - (stock +

prepaid expenses) 0.95

Efficiency Ratios

Inventory 774

Trade Receivables 5177

Trade Payables 7740

Days 365

COS 15514

Sales 16821

Inventory days Inventory/COS*365 18.210

Debtor days Debtor/ Sales*365 112.34

Creditor days Creditor / Sales*365 167.95

Investor Return

EPS

Total Earnings/

Outstanding shares

Total Earnings(post

tax) 1370

Outstanding Shares

(in millions) 3192

EPS 0.429

Gearing Ratio

Long-term debt 5050

Shareholder's equity 5618

Debt-equity ratio 0.90

Interpretations

Assessing the above financial statement of the company it could be interpreted that

financial health and positions of BAE Systems is having sound financial health and position. The

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability of company is sound return on capital employed of company is 7.93% and return

over equity is 18.39% that means company is giving high return to its investors. Operating

efficiency of company can be analysed using operating margin of company that is around

7.28%.the returns of company could be increased using effective strategies in the business.

Liquidity position of company is less than the standards of 2:1. that shows company does

not have enough assets to meet its short term obligations in comparison to its competitors. Debt

to equity ration of company is also high. Company should adopt for addressing the pension fund

because the company is having retirement obligations which is affecting the financial structure of

company. Therefore company before maximising shareholders wealth should focus over

addressing the pension concern.

b) Limitations of ratio analysis

following are the limitations of using ratio analysis.

Companies make year end changes in the financial statements for improving the ratios, is

such cases ratio proves to be window dressing.

Ratio analysis ignores price level changes due to inflations as several rations are

calculated using the historical costs. They also overlook the changes occurring between

price levels in the period.

Qualitative aspects of the firm affecting the financial performance are ignored and only

monetary aspects are considered.

Ratios do not have any standard definitions. So ratios may be calculated using different

formulas by different firms. Example some firm do not consider bank over drafts in

calculating the current ratios.

Ratios can not be used for resolving financial problems of company. They are not

providing any actual solutions to company for improvement of the performance.

2.2 Company valuation

(a)

Asset based valuation

It is the one of the most important method of asset valuation under which from assets

liability amount is subtracted. Remaining amount indicate firm capability or financial capacity

3

over equity is 18.39% that means company is giving high return to its investors. Operating

efficiency of company can be analysed using operating margin of company that is around

7.28%.the returns of company could be increased using effective strategies in the business.

Liquidity position of company is less than the standards of 2:1. that shows company does

not have enough assets to meet its short term obligations in comparison to its competitors. Debt

to equity ration of company is also high. Company should adopt for addressing the pension fund

because the company is having retirement obligations which is affecting the financial structure of

company. Therefore company before maximising shareholders wealth should focus over

addressing the pension concern.

b) Limitations of ratio analysis

following are the limitations of using ratio analysis.

Companies make year end changes in the financial statements for improving the ratios, is

such cases ratio proves to be window dressing.

Ratio analysis ignores price level changes due to inflations as several rations are

calculated using the historical costs. They also overlook the changes occurring between

price levels in the period.

Qualitative aspects of the firm affecting the financial performance are ignored and only

monetary aspects are considered.

Ratios do not have any standard definitions. So ratios may be calculated using different

formulas by different firms. Example some firm do not consider bank over drafts in

calculating the current ratios.

Ratios can not be used for resolving financial problems of company. They are not

providing any actual solutions to company for improvement of the performance.

2.2 Company valuation

(a)

Asset based valuation

It is the one of the most important method of asset valuation under which from assets

liability amount is subtracted. Remaining amount indicate firm capability or financial capacity

3

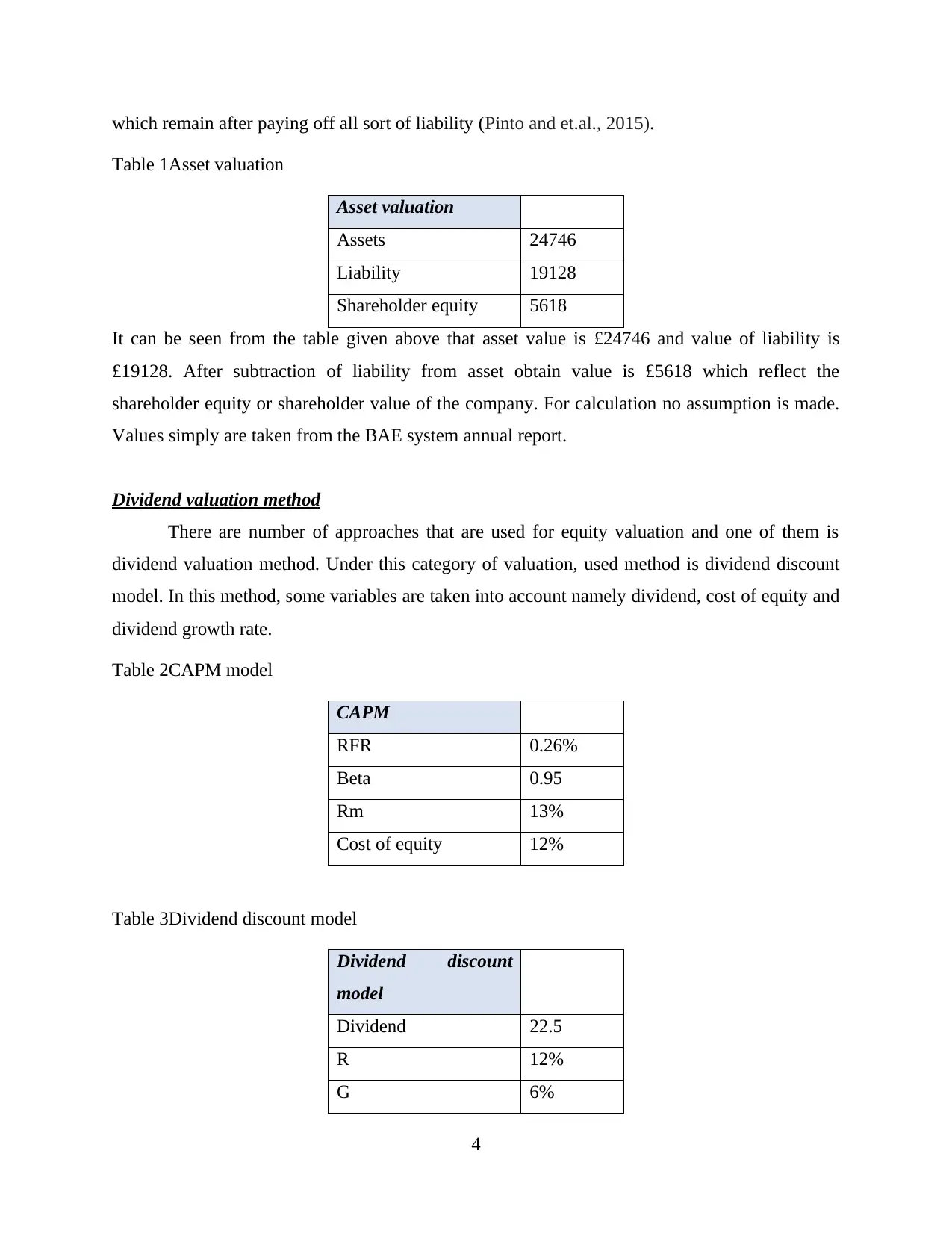

which remain after paying off all sort of liability (Pinto and et.al., 2015).

Table 1Asset valuation

Asset valuation

Assets 24746

Liability 19128

Shareholder equity 5618

It can be seen from the table given above that asset value is £24746 and value of liability is

£19128. After subtraction of liability from asset obtain value is £5618 which reflect the

shareholder equity or shareholder value of the company. For calculation no assumption is made.

Values simply are taken from the BAE system annual report.

Dividend valuation method

There are number of approaches that are used for equity valuation and one of them is

dividend valuation method. Under this category of valuation, used method is dividend discount

model. In this method, some variables are taken into account namely dividend, cost of equity and

dividend growth rate.

Table 2CAPM model

CAPM

RFR 0.26%

Beta 0.95

Rm 13%

Cost of equity 12%

Table 3Dividend discount model

Dividend discount

model

Dividend 22.5

R 12%

G 6%

4

Table 1Asset valuation

Asset valuation

Assets 24746

Liability 19128

Shareholder equity 5618

It can be seen from the table given above that asset value is £24746 and value of liability is

£19128. After subtraction of liability from asset obtain value is £5618 which reflect the

shareholder equity or shareholder value of the company. For calculation no assumption is made.

Values simply are taken from the BAE system annual report.

Dividend valuation method

There are number of approaches that are used for equity valuation and one of them is

dividend valuation method. Under this category of valuation, used method is dividend discount

model. In this method, some variables are taken into account namely dividend, cost of equity and

dividend growth rate.

Table 2CAPM model

CAPM

RFR 0.26%

Beta 0.95

Rm 13%

Cost of equity 12%

Table 3Dividend discount model

Dividend discount

model

Dividend 22.5

R 12%

G 6%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

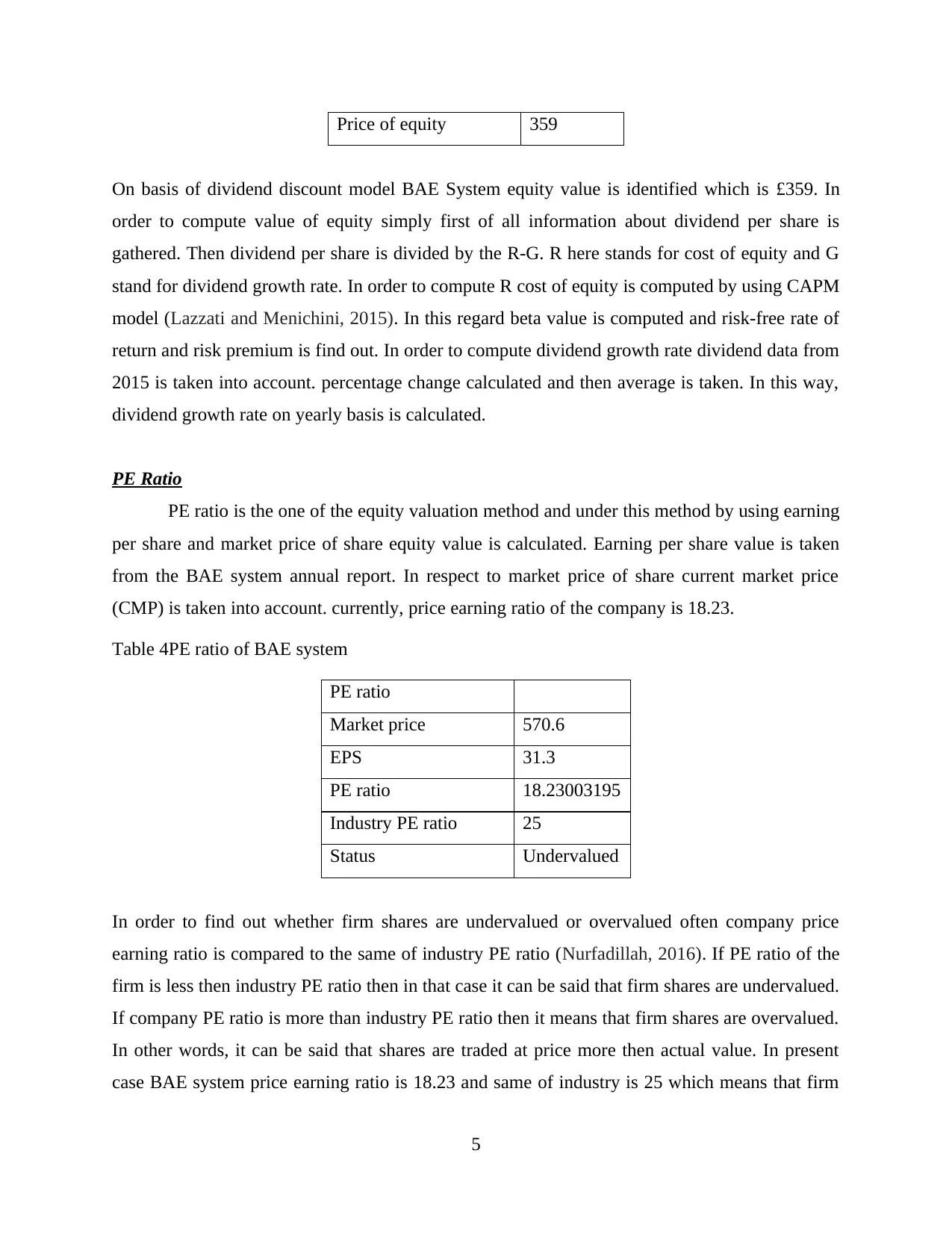

Price of equity 359

On basis of dividend discount model BAE System equity value is identified which is £359. In

order to compute value of equity simply first of all information about dividend per share is

gathered. Then dividend per share is divided by the R-G. R here stands for cost of equity and G

stand for dividend growth rate. In order to compute R cost of equity is computed by using CAPM

model (Lazzati and Menichini, 2015). In this regard beta value is computed and risk-free rate of

return and risk premium is find out. In order to compute dividend growth rate dividend data from

2015 is taken into account. percentage change calculated and then average is taken. In this way,

dividend growth rate on yearly basis is calculated.

PE Ratio

PE ratio is the one of the equity valuation method and under this method by using earning

per share and market price of share equity value is calculated. Earning per share value is taken

from the BAE system annual report. In respect to market price of share current market price

(CMP) is taken into account. currently, price earning ratio of the company is 18.23.

Table 4PE ratio of BAE system

PE ratio

Market price 570.6

EPS 31.3

PE ratio 18.23003195

Industry PE ratio 25

Status Undervalued

In order to find out whether firm shares are undervalued or overvalued often company price

earning ratio is compared to the same of industry PE ratio (Nurfadillah, 2016). If PE ratio of the

firm is less then industry PE ratio then in that case it can be said that firm shares are undervalued.

If company PE ratio is more than industry PE ratio then it means that firm shares are overvalued.

In other words, it can be said that shares are traded at price more then actual value. In present

case BAE system price earning ratio is 18.23 and same of industry is 25 which means that firm

5

On basis of dividend discount model BAE System equity value is identified which is £359. In

order to compute value of equity simply first of all information about dividend per share is

gathered. Then dividend per share is divided by the R-G. R here stands for cost of equity and G

stand for dividend growth rate. In order to compute R cost of equity is computed by using CAPM

model (Lazzati and Menichini, 2015). In this regard beta value is computed and risk-free rate of

return and risk premium is find out. In order to compute dividend growth rate dividend data from

2015 is taken into account. percentage change calculated and then average is taken. In this way,

dividend growth rate on yearly basis is calculated.

PE Ratio

PE ratio is the one of the equity valuation method and under this method by using earning

per share and market price of share equity value is calculated. Earning per share value is taken

from the BAE system annual report. In respect to market price of share current market price

(CMP) is taken into account. currently, price earning ratio of the company is 18.23.

Table 4PE ratio of BAE system

PE ratio

Market price 570.6

EPS 31.3

PE ratio 18.23003195

Industry PE ratio 25

Status Undervalued

In order to find out whether firm shares are undervalued or overvalued often company price

earning ratio is compared to the same of industry PE ratio (Nurfadillah, 2016). If PE ratio of the

firm is less then industry PE ratio then in that case it can be said that firm shares are undervalued.

If company PE ratio is more than industry PE ratio then it means that firm shares are overvalued.

In other words, it can be said that shares are traded at price more then actual value. In present

case BAE system price earning ratio is 18.23 and same of industry is 25 which means that firm

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shares are undervalued and available at cheaper price. Thus, investors must make purchase of the

company shares.

(b) Critical examination of the valuation methodology

PE ratio is the one of the most important valuation technique and it have its own positive

and negative sides. Significance of the PE ratio method is that it reflects whether company shares

are undervalued or overvalued. It assists investors in making more wise investment decisions

(Paul., 2012). Usually, if any share, price is high investors assume it dearer and if share price is

low then investors think that it is cheaper. PE ratio show investors a different picture and indicate

that high price does not mean share is dearer, it may be highly undervalued and can generate

better investment opportunity. Limitation of PE ratio is that if company manipulate its earnings

then in that case earning per share will show wrong value and due to this reason price earning

ratio will do valuation in wrong manner. In respect to dividend discount model main merit is that

its concept is connected to the ground reality (Ivanovski, Ivanovska and Narasanov, 2015). Many

analysts prefer to use model because business is a perpetual entity and it will remain in existence.

Hence, if investor invest today it will receive dividend payment in future time period

consistently. Thus, value of the firm is value of perpetual never ending stream of dividends that

the buyer intends to receive later with the passage of time. Thus, there is no subjectivity in this

model. Negative side of this model is that it is hard task to make accurate projection in this

approach. Main merit of asset-based valuation method is that it is easy to apply and reflect the

portion of asset that remain for shareholders after paying off all liabilities of the business

(Küpper and Pedell, 2016). Demerit of this method is that valuation of intangible assets is hard

task. Moreover, during asset revaluation lots of factors need to be taken into account to

accurately estimate asset value.

2.3 Capital structure

a) Cost of convertible bonds for Absolute plc

Tax rate 19%

Interest rate 8%

Cost of

debt 6.48%

6

company shares.

(b) Critical examination of the valuation methodology

PE ratio is the one of the most important valuation technique and it have its own positive

and negative sides. Significance of the PE ratio method is that it reflects whether company shares

are undervalued or overvalued. It assists investors in making more wise investment decisions

(Paul., 2012). Usually, if any share, price is high investors assume it dearer and if share price is

low then investors think that it is cheaper. PE ratio show investors a different picture and indicate

that high price does not mean share is dearer, it may be highly undervalued and can generate

better investment opportunity. Limitation of PE ratio is that if company manipulate its earnings

then in that case earning per share will show wrong value and due to this reason price earning

ratio will do valuation in wrong manner. In respect to dividend discount model main merit is that

its concept is connected to the ground reality (Ivanovski, Ivanovska and Narasanov, 2015). Many

analysts prefer to use model because business is a perpetual entity and it will remain in existence.

Hence, if investor invest today it will receive dividend payment in future time period

consistently. Thus, value of the firm is value of perpetual never ending stream of dividends that

the buyer intends to receive later with the passage of time. Thus, there is no subjectivity in this

model. Negative side of this model is that it is hard task to make accurate projection in this

approach. Main merit of asset-based valuation method is that it is easy to apply and reflect the

portion of asset that remain for shareholders after paying off all liabilities of the business

(Küpper and Pedell, 2016). Demerit of this method is that valuation of intangible assets is hard

task. Moreover, during asset revaluation lots of factors need to be taken into account to

accurately estimate asset value.

2.3 Capital structure

a) Cost of convertible bonds for Absolute plc

Tax rate 19%

Interest rate 8%

Cost of

debt 6.48%

6

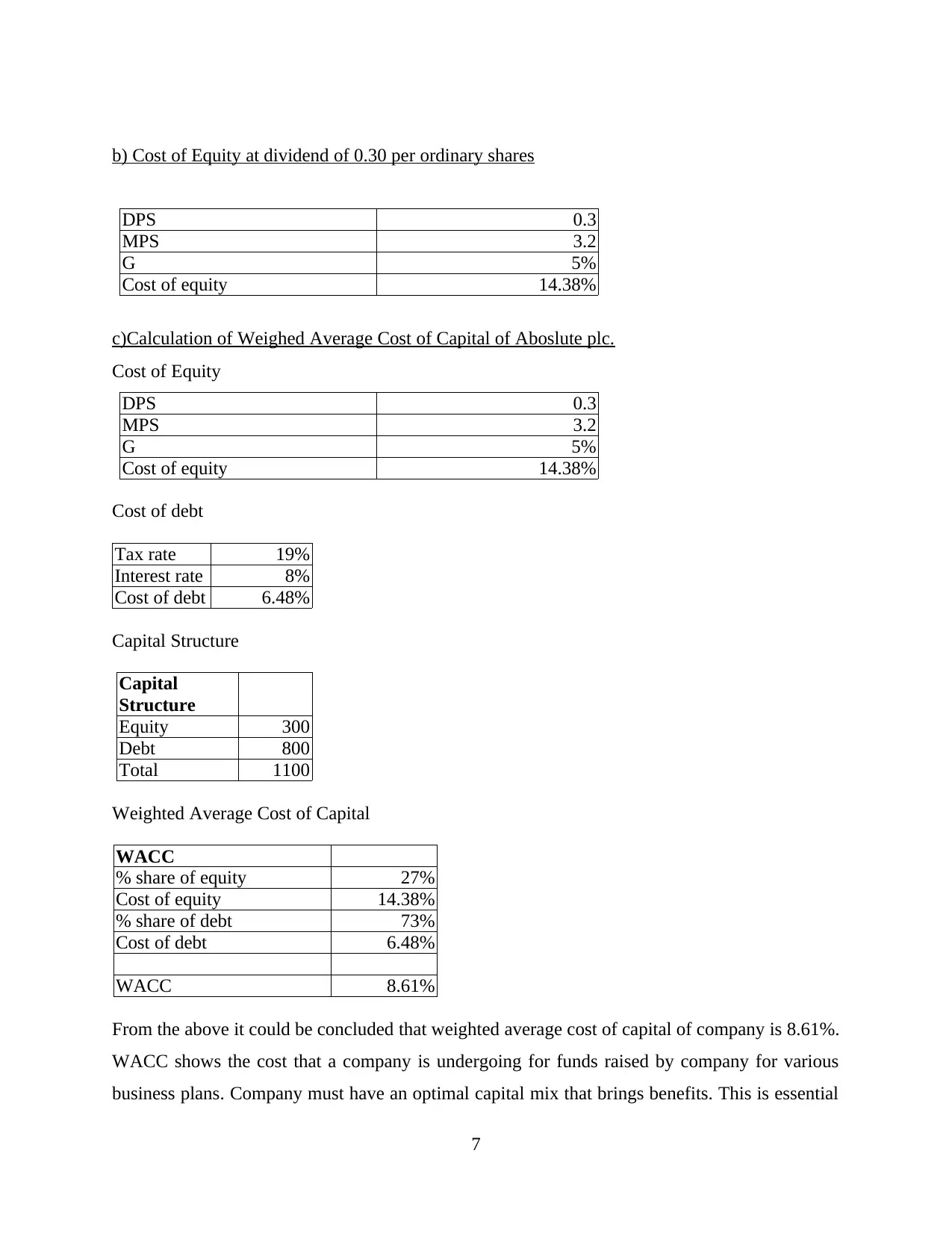

b) Cost of Equity at dividend of 0.30 per ordinary shares

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

c)Calculation of Weighed Average Cost of Capital of Aboslute plc.

Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

WACC

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

WACC 8.61%

From the above it could be concluded that weighted average cost of capital of company is 8.61%.

WACC shows the cost that a company is undergoing for funds raised by company for various

business plans. Company must have an optimal capital mix that brings benefits. This is essential

7

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

c)Calculation of Weighed Average Cost of Capital of Aboslute plc.

Cost of Equity

DPS 0.3

MPS 3.2

G 5%

Cost of equity 14.38%

Cost of debt

Tax rate 19%

Interest rate 8%

Cost of debt 6.48%

Capital Structure

Capital

Structure

Equity 300

Debt 800

Total 1100

Weighted Average Cost of Capital

WACC

% share of equity 27%

Cost of equity 14.38%

% share of debt 73%

Cost of debt 6.48%

WACC 8.61%

From the above it could be concluded that weighted average cost of capital of company is 8.61%.

WACC shows the cost that a company is undergoing for funds raised by company for various

business plans. Company must have an optimal capital mix that brings benefits. This is essential

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for the management to ensure the cost of funds raised by company are adequate. For minimising

the cost of capital companies should have appropriate mix of debt and equity.

d) Difficulties that are experinced in calculating the WACC.

The calculation of WACC is straightforward in theory as compared to theory, because of the

following reason.

there are different methods used while estimating the cost of equity, such that Dividend

discount model and CAPM model. At that time, user aces problem especially related to

one of the variable is an estimate and it is not so easy.

WACC model is a forward looking measure and the entire calculations are based on the

expected returns, not in the historical returns. Therefore, for the equity also, the market

value is consider rather than book value.

However, it is critically analyzed that while calculating WACC, there are different term

used such that risk- free bonds that is further used to determine the cost of debts and it is

not always actually matched the terms of the company's debt and as a result, it is consider

difficult to use practically.

In addition to this, the analyst also needs to include the lease in the debt and they also use

the long term borrowing rates as the cost of debts for this and in turn, it is quite difficult

to calculate. Therefore, it is consider as a challenge to use WACC especially in

calculation.

Further, if the company's structure is complex then it gets more difficult to calculate.

WACC because it requires a long calculation and in turn it consumes lot of time. That is

why, using this WACC is consider one of the most simplest method for theory rather to

use practically.

CONCLUSION

From the above study it could be concluded that the financial statements of company have an

importance in making decisions in market. The companies can enhance the business by making

effective strategies. The financial analysis of company is essential for decision making.

Valuation of the company could be done using various methods. Companies have to ensure that

the capital structure of the company is optimum having lowest cost.

8

the cost of capital companies should have appropriate mix of debt and equity.

d) Difficulties that are experinced in calculating the WACC.

The calculation of WACC is straightforward in theory as compared to theory, because of the

following reason.

there are different methods used while estimating the cost of equity, such that Dividend

discount model and CAPM model. At that time, user aces problem especially related to

one of the variable is an estimate and it is not so easy.

WACC model is a forward looking measure and the entire calculations are based on the

expected returns, not in the historical returns. Therefore, for the equity also, the market

value is consider rather than book value.

However, it is critically analyzed that while calculating WACC, there are different term

used such that risk- free bonds that is further used to determine the cost of debts and it is

not always actually matched the terms of the company's debt and as a result, it is consider

difficult to use practically.

In addition to this, the analyst also needs to include the lease in the debt and they also use

the long term borrowing rates as the cost of debts for this and in turn, it is quite difficult

to calculate. Therefore, it is consider as a challenge to use WACC especially in

calculation.

Further, if the company's structure is complex then it gets more difficult to calculate.

WACC because it requires a long calculation and in turn it consumes lot of time. That is

why, using this WACC is consider one of the most simplest method for theory rather to

use practically.

CONCLUSION

From the above study it could be concluded that the financial statements of company have an

importance in making decisions in market. The companies can enhance the business by making

effective strategies. The financial analysis of company is essential for decision making.

Valuation of the company could be done using various methods. Companies have to ensure that

the capital structure of the company is optimum having lowest cost.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Küpper, H.U. and Pedell, B., 2016. Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy. 40. pp.88-103.

Lazzati, N. and Menichini, A.A., 2015. A dynamic approach to the dividend discount

model. Review of Pacific Basin Financial Markets and Policies. 18(03). p.1550018.

Nurfadillah, M., 2016. ANALISIS PENGARUH EARNING PER SHARE, DEBT TO EQUITY

RATIO DAN RETURN ON EQUITY TERHADAP HARGA SAHAM PT UNILEVER

INDONESIA Tbk. Jurnal Manajemen dan Akuntansi. 12(1).

Pinto, J.E., Henry, E., Robinson, T.R. and Stowe, J.D., 2015. Equity asset valuation. John Wiley

& Sons.

Online

Paul., P., 2012. [Online]. Price to earnings ratio significance, usage and limitations. Available

through:< https://www.paulasset.com/articles/price-to-earning-ratio-significance/>.

9

Books and Journals

Küpper, H.U. and Pedell, B., 2016. Which asset valuation and depreciation method should be

used for regulated utilities? An analytical and simulation-based comparison. Utilities

Policy. 40. pp.88-103.

Lazzati, N. and Menichini, A.A., 2015. A dynamic approach to the dividend discount

model. Review of Pacific Basin Financial Markets and Policies. 18(03). p.1550018.

Nurfadillah, M., 2016. ANALISIS PENGARUH EARNING PER SHARE, DEBT TO EQUITY

RATIO DAN RETURN ON EQUITY TERHADAP HARGA SAHAM PT UNILEVER

INDONESIA Tbk. Jurnal Manajemen dan Akuntansi. 12(1).

Pinto, J.E., Henry, E., Robinson, T.R. and Stowe, J.D., 2015. Equity asset valuation. John Wiley

& Sons.

Online

Paul., P., 2012. [Online]. Price to earnings ratio significance, usage and limitations. Available

through:< https://www.paulasset.com/articles/price-to-earning-ratio-significance/>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.