Finance Management: Key Reports and Metrics

VerifiedAdded on 2023/06/18

|14

|3221

|341

AI Summary

This article discusses the importance of finance management in an organization's growth and the key financial reports and metrics used in finance management. It covers the concept of finance management, its relevance, and the significance of financial planning. The article also explains the three most important financial statements, income statements, balance sheets, and cash flow statements, and their importance. Additionally, it covers the three most common financial ratios, profitability ratios, liquidity ratios, and leverage ratios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

3005

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Section 1: The notion of finance managing is defined and discussed, as well as the relevance

of fiscal administration................................................................................................................1

Section 2: The key fiscal reports are described and discussed, as well as the usage of metrics in

fiscal administration.....................................................................................................................2

Section 3: Using the template provided:......................................................................................7

Section 3: According on the ratio assessment findings, characterise the corporation's

competitiveness, solvency, and effectiveness using the case study data.....................................8

Section 4: Utilizing instances from the research study, describe and analyze the strategies that

this company could employ to enhance its fiscal efficiency.......................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Appendices....................................................................................................................................11

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Section 1: The notion of finance managing is defined and discussed, as well as the relevance

of fiscal administration................................................................................................................1

Section 2: The key fiscal reports are described and discussed, as well as the usage of metrics in

fiscal administration.....................................................................................................................2

Section 3: Using the template provided:......................................................................................7

Section 3: According on the ratio assessment findings, characterise the corporation's

competitiveness, solvency, and effectiveness using the case study data.....................................8

Section 4: Utilizing instances from the research study, describe and analyze the strategies that

this company could employ to enhance its fiscal efficiency.......................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Appendices....................................................................................................................................11

INTRODUCTION

Enterprise administration is divided into various phases, each of which is referred to as fiscal

administration. Preparing, preparing or coordinating, leading, and administering or supervising

diverse accounting corporate operations are all included in these phases or responsibilities

(Foyeke, Olusola and Aderemi, 2016). The procurement and use of the organization's resources

are examples of such actions. Finance managerial tasks are tightly linked to the divisions of

advertising, manufacturing, and personnel relations. Investing and budgetary selections, the

appropriate balance of fiscal assets and asset framework, and payout plans and actions are only a

few of the main fiscal choices made during the fiscal administration procedure. Among the most

critical aspects of every corporate enterprise is finance managing. The ability to administer

corporate funds is critical for beginning a firm or growing an established one.

MAIN BODY

Section 1: The notion of finance managing is defined and discussed, as well as the relevance of

fiscal administration

Concept: Finance administration is a term that encompasses the responsibilities of

effectively managing and regulating an organization's fiscal assets. Finance executives, for

instance, supervise the intake and route of working capital in the company in a manner which

benefits the company.

The significance of finance administration: Fiscal leadership is among the most important

factors in an organization's growth. The following are among some of the reasons why fiscal

managing is so important:

Enhancing fiscal wellness: The circulation of money within an institution is critical to

the smooth execution of corporate activities and the corporation's economic wellbeing.

The presence of a working capital imbalance as contrasted to pre-estimated amounts

could adversely impair the firm's commercial activities and image. For instance, a key

customer's request might not have been completed since the company can't afford to

spend for the basic resources needed to make the customer request. Account receivable

and payables are essential components of good money administration. By properly

recovering and repaying off its obligations in a brief amount of span, the institution could

strengthen its liquid assets and credit worthiness (Henager and Cude, 2016).

Enterprise administration is divided into various phases, each of which is referred to as fiscal

administration. Preparing, preparing or coordinating, leading, and administering or supervising

diverse accounting corporate operations are all included in these phases or responsibilities

(Foyeke, Olusola and Aderemi, 2016). The procurement and use of the organization's resources

are examples of such actions. Finance managerial tasks are tightly linked to the divisions of

advertising, manufacturing, and personnel relations. Investing and budgetary selections, the

appropriate balance of fiscal assets and asset framework, and payout plans and actions are only a

few of the main fiscal choices made during the fiscal administration procedure. Among the most

critical aspects of every corporate enterprise is finance managing. The ability to administer

corporate funds is critical for beginning a firm or growing an established one.

MAIN BODY

Section 1: The notion of finance managing is defined and discussed, as well as the relevance of

fiscal administration

Concept: Finance administration is a term that encompasses the responsibilities of

effectively managing and regulating an organization's fiscal assets. Finance executives, for

instance, supervise the intake and route of working capital in the company in a manner which

benefits the company.

The significance of finance administration: Fiscal leadership is among the most important

factors in an organization's growth. The following are among some of the reasons why fiscal

managing is so important:

Enhancing fiscal wellness: The circulation of money within an institution is critical to

the smooth execution of corporate activities and the corporation's economic wellbeing.

The presence of a working capital imbalance as contrasted to pre-estimated amounts

could adversely impair the firm's commercial activities and image. For instance, a key

customer's request might not have been completed since the company can't afford to

spend for the basic resources needed to make the customer request. Account receivable

and payables are essential components of good money administration. By properly

recovering and repaying off its obligations in a brief amount of span, the institution could

strengthen its liquid assets and credit worthiness (Henager and Cude, 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Finance Managing Assists in Fiscal Planning: Finance administration assists in

forecasting the current industry and evaluating the corporate growth in reference to that

marketplace. A cash plan is often utilized as a quality indicator. The administration

would be capable to innovate and develop the finest and more suitable fiscal strategies

and programs by evaluating the variances in estimates. It would aid the organisation in

better preparing for the unknown, as well as improving its efficiency and effectiveness.

Finance Administration Could Assist the Firm in Making Proper Selections and

Preparing Reliable Monetary Statements: Finance managing could assist the business

in making suitable selections and preparing reliable financial statements in a prompt and

structured way. As a consequence, the corporation's satisfaction and efficiency would

increase, and the firm's earnings condition would strengthen.

Allow for optimum financing activities: Many start-ups require mortgages and

receivables from bigger corporations or rich individuals in order to correctly support their

activities until they reach an initial capital expenditure. The corporation's development

would necessitate an increase in investment. Finance managerial skills would assist the

organisation in determining the appropriate origins and combination of cash to establish

an appropriate resource framework. This guarantees that their finances are utilized well

and that no money is wasted (Kwilinskyi, Shteingauz and Maslov, 2020).

Section 2: The key fiscal reports are described and discussed, as well as the usage of metrics in

fiscal administration

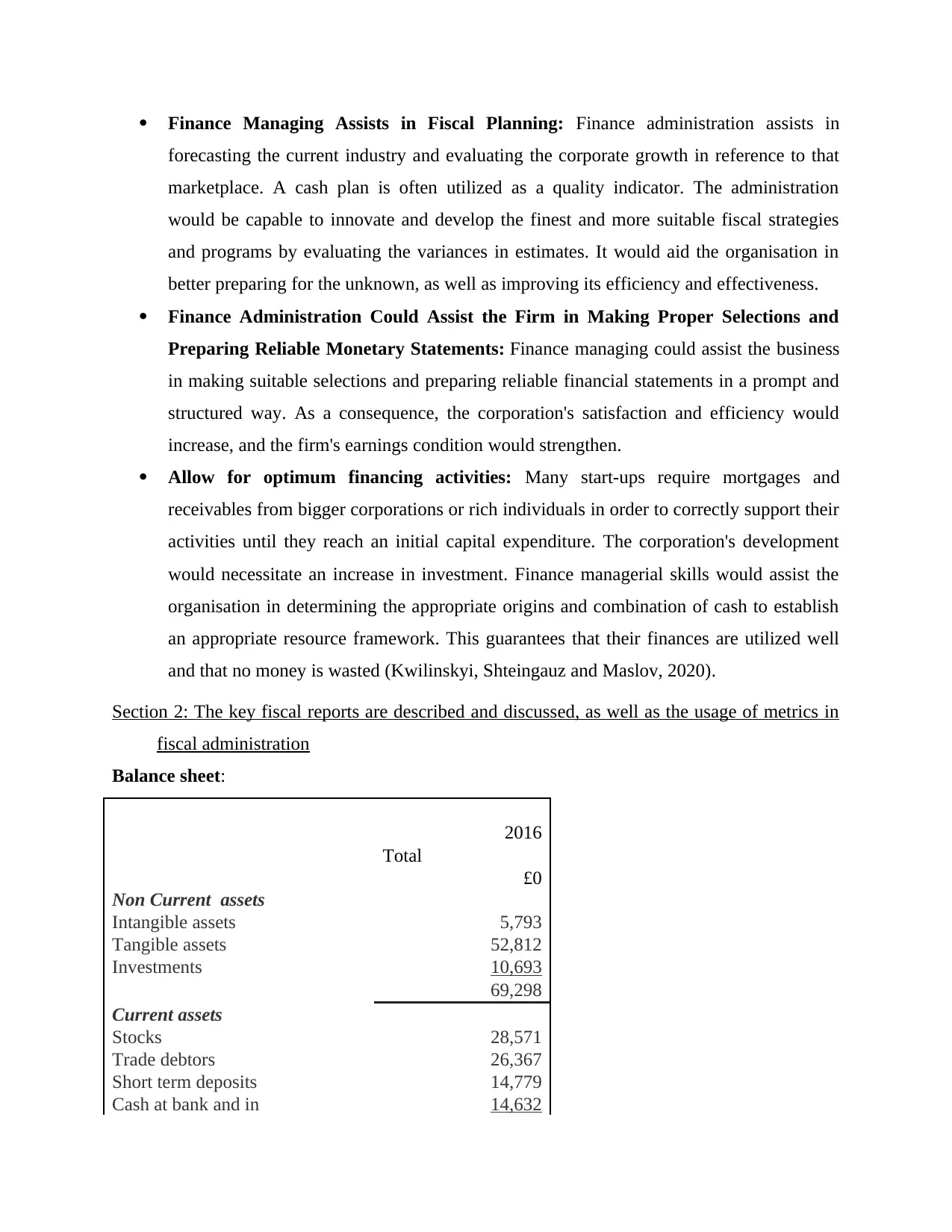

Balance sheet:

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in 14,632

forecasting the current industry and evaluating the corporate growth in reference to that

marketplace. A cash plan is often utilized as a quality indicator. The administration

would be capable to innovate and develop the finest and more suitable fiscal strategies

and programs by evaluating the variances in estimates. It would aid the organisation in

better preparing for the unknown, as well as improving its efficiency and effectiveness.

Finance Administration Could Assist the Firm in Making Proper Selections and

Preparing Reliable Monetary Statements: Finance managing could assist the business

in making suitable selections and preparing reliable financial statements in a prompt and

structured way. As a consequence, the corporation's satisfaction and efficiency would

increase, and the firm's earnings condition would strengthen.

Allow for optimum financing activities: Many start-ups require mortgages and

receivables from bigger corporations or rich individuals in order to correctly support their

activities until they reach an initial capital expenditure. The corporation's development

would necessitate an increase in investment. Finance managerial skills would assist the

organisation in determining the appropriate origins and combination of cash to establish

an appropriate resource framework. This guarantees that their finances are utilized well

and that no money is wasted (Kwilinskyi, Shteingauz and Maslov, 2020).

Section 2: The key fiscal reports are described and discussed, as well as the usage of metrics in

fiscal administration

Balance sheet:

2016

Total

£0

Non Current assets

Intangible assets 5,793

Tangible assets 52,812

Investments 10,693

69,298

Current assets

Stocks 28,571

Trade debtors 26,367

Short term deposits 14,779

Cash at bank and in 14,632

hand

84,349

Current liabilities

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

84,349

Current liabilities

Bank loans and

overdrafts 9,610

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585

Other creditors

including tax and social

security

4,562

37,928

working capital 46,421

Total assets less

current liabilities 1,15,719

Non Current

Liabilities

Bank loans and

overdrafts 16,506

Other Liabilities 7,304

23,810

Provisions for

liabilities 8,094

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322

Retained earnings 43,057

Total equity 83,802

Business Review:

2016 20

15 Change

£’000 £’000 %

Turnover (continuing operations) 1,89,711 1,79,58

7

5.60

%

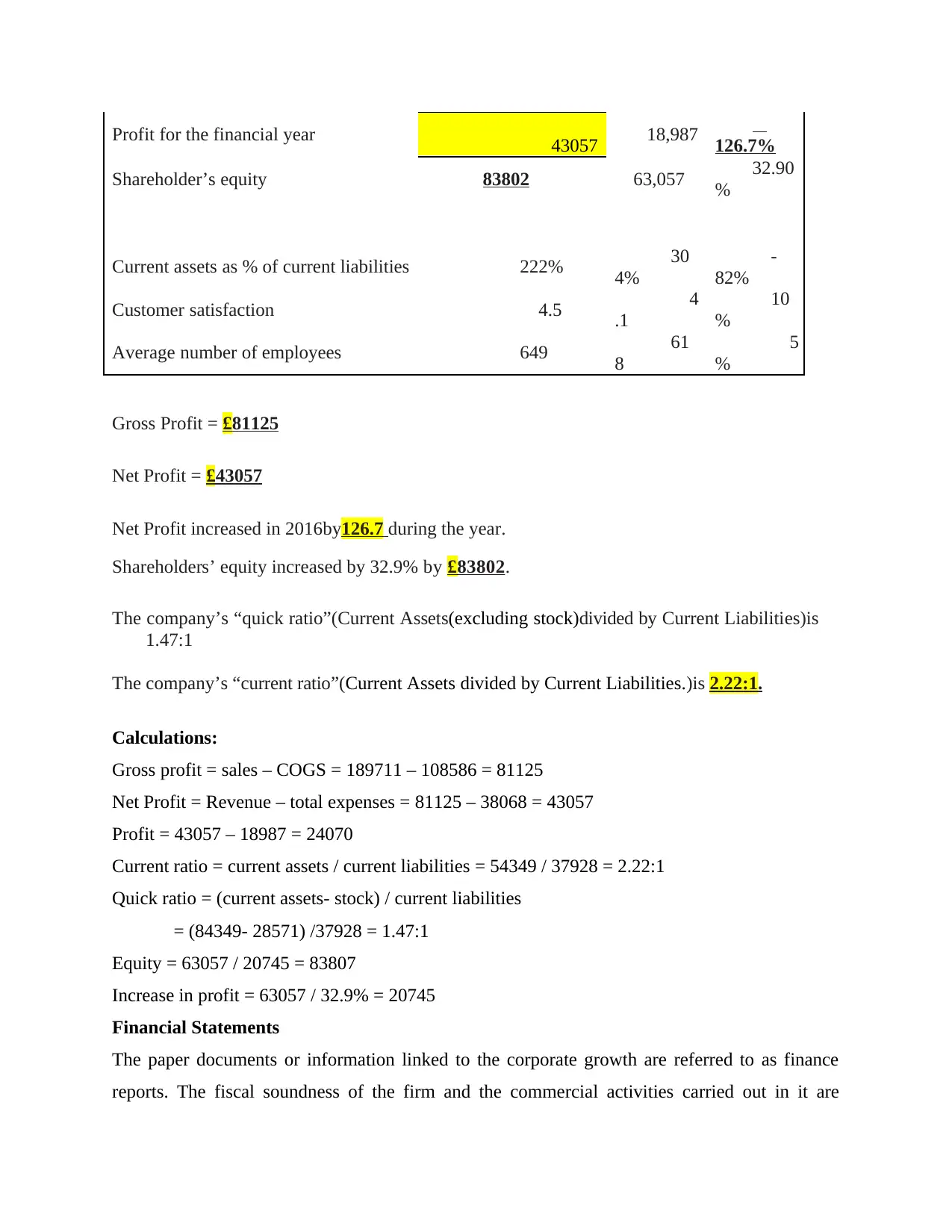

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802 63,057 32.90

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio”(Current Assets(excluding stock)divided by Current Liabilities)is

1.47:1

The company’s “current ratio”(Current Assets divided by Current Liabilities.)is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

Financial Statements

The paper documents or information linked to the corporate growth are referred to as finance

reports. The fiscal soundness of the firm and the commercial activities carried out in it are

Shareholder’s equity 83802 63,057 32.90

%

Current assets as % of current liabilities 222% 30

4%

-

82%

Customer satisfaction 4.5 4

.1

10

%

Average number of employees 649 61

8

5

%

Gross Profit = £81125

Net Profit = £43057

Net Profit increased in 2016by126.7 during the year.

Shareholders’ equity increased by 32.9% by £83802.

The company’s “quick ratio”(Current Assets(excluding stock)divided by Current Liabilities)is

1.47:1

The company’s “current ratio”(Current Assets divided by Current Liabilities.)is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

Financial Statements

The paper documents or information linked to the corporate growth are referred to as finance

reports. The fiscal soundness of the firm and the commercial activities carried out in it are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reflected in such documents. Corporate attorneys, external examiners, governmental

organizations, and others typically examine and evaluate such reports. These are conducted to

validate the corporation's trustworthiness and the correctness of its financial reports for purposes

of finance, taxation, and investing (Levy, Bouheni and Ammi, 2018). The revenue report,

balancing report, and money circulation assertion are the three most important financial

statements. The following fiscal reports are addressed in detail:

Income Statements: A corporation's income statement tracks and analyzes all of its

expenditures and earnings. The goal of this assertion is to determine if the business is

making a net gain or a net deficit as a consequence of its selling. If the corporation's

earnings from activities surpasses its expenditures, then that would create money or

profitability. But at the other side, if the corporation's expenditure exceeds its income

from activities, it would incur a net deficit. Selling or Earnings from Activities,

Operational costs, and Non-operating expenditure are all factors in calculating an income

summary. Every one of the expenses of the products supplied are included in selling. The

costs of running a business, such as administrative expenses, advertising costs, and so on,

are included in capital expenditures. Non-operating expenditures are expenditures that are

unrelated to selling, such as income payments on mortgages and receivables, one-time

expenditures, and so on (Ivanovich, 2020).

The income statement is calculated using the following equation:

Revenue – Expenses = Net Income

Balance Sheet: A balance sheet is usually of an organization's main significant fiscal

reports. This declaration must be prepared since it reflects the firm's general fiscal status

and shows the organization's corporate profits and losses. The resources of the

corporation typically have included the tools and infrastructure, as well as its inventory,

acquisitions, liquid assets, and working capital, among other things. Long-term

borrowing and advancements, money owing to lenders or collections accruals, and other

obligations are typically included in the firmy's debt. Along with its obligations, the

balance sheet usually contains the stockholder ownership, such as Investors' Holdings or

Equitable, bank overdrafts, and other items. Following the production of the balance

sheet, it must be said that the resources of the business are equivalent to the ownership

and obligations of the firm.

organizations, and others typically examine and evaluate such reports. These are conducted to

validate the corporation's trustworthiness and the correctness of its financial reports for purposes

of finance, taxation, and investing (Levy, Bouheni and Ammi, 2018). The revenue report,

balancing report, and money circulation assertion are the three most important financial

statements. The following fiscal reports are addressed in detail:

Income Statements: A corporation's income statement tracks and analyzes all of its

expenditures and earnings. The goal of this assertion is to determine if the business is

making a net gain or a net deficit as a consequence of its selling. If the corporation's

earnings from activities surpasses its expenditures, then that would create money or

profitability. But at the other side, if the corporation's expenditure exceeds its income

from activities, it would incur a net deficit. Selling or Earnings from Activities,

Operational costs, and Non-operating expenditure are all factors in calculating an income

summary. Every one of the expenses of the products supplied are included in selling. The

costs of running a business, such as administrative expenses, advertising costs, and so on,

are included in capital expenditures. Non-operating expenditures are expenditures that are

unrelated to selling, such as income payments on mortgages and receivables, one-time

expenditures, and so on (Ivanovich, 2020).

The income statement is calculated using the following equation:

Revenue – Expenses = Net Income

Balance Sheet: A balance sheet is usually of an organization's main significant fiscal

reports. This declaration must be prepared since it reflects the firm's general fiscal status

and shows the organization's corporate profits and losses. The resources of the

corporation typically have included the tools and infrastructure, as well as its inventory,

acquisitions, liquid assets, and working capital, among other things. Long-term

borrowing and advancements, money owing to lenders or collections accruals, and other

obligations are typically included in the firmy's debt. Along with its obligations, the

balance sheet usually contains the stockholder ownership, such as Investors' Holdings or

Equitable, bank overdrafts, and other items. Following the production of the balance

sheet, it must be said that the resources of the business are equivalent to the ownership

and obligations of the firm.

The following is the method utilized to prepare the firm's balance sheet:

Liabilities + Shareholders' Equity = Assets

Cash Flow Statement: The cash flow statement, is generated so that managers could

comprehend and assess if the business could produce sufficient cash through different

economic processes to pay off obligations, finance services, and reinvest. The cash flow

summary represents the corporation's fiscal status since it reveals the pattern of cash flow

and if working capitals have been used efficiently. Running operations, structured

finance, and interest expenses are the 3 major elements of a cash flow statement (Sheedy,

Griffin and Barbour, 2017).

o CFS's operating endeavors include all uses and suppliers of cash resources derived from

commercial processes such as goods and commodity sales. Instances include bills

receipts and payments, inventories, amortization, compensation and payroll, and so forth.

o The use and origins of funds from the firm's long holdings are included in investing

operations. Credits or advancements issued or obtained, the acquisition and selling of

marketable securities, and so on are examples.

o Money acquired from creditors and businesses, as well as income distributions given to

stockholders, are examples of finance operations. Funding operations include the sale of

stocks and bonds, the repayment of borrowing, and the distribution of profits.

Financial Ratios

Financial metrics aid in the analysis of a corporation's outcomes in general of solvency,

competitiveness, and effectiveness. Such metrics are typically used to evaluate a company's total

fiscal status to its rivals'. In essence, proportions are time-oriented, therefore it could be used to

track a corporation's progress over the years. The following are 3 of the most common fiscal

ratios:

Profitability Ratios: Profitability Proportions, often referred as Return on Investment

(ROI) proportions, are used to assess an organizational value based on its profitability. A bigger

profitability usually suggests that the firm is in excellent fiscal shape and performing well. Total

Revenue Margins, Net Income Margin, and Return on Capital are the three most used

performance metrics (Shoup, 2017). After calculating the revenue margins created on selling, the

total revenue margins reveal the corporation's production and trading productivity and

Liabilities + Shareholders' Equity = Assets

Cash Flow Statement: The cash flow statement, is generated so that managers could

comprehend and assess if the business could produce sufficient cash through different

economic processes to pay off obligations, finance services, and reinvest. The cash flow

summary represents the corporation's fiscal status since it reveals the pattern of cash flow

and if working capitals have been used efficiently. Running operations, structured

finance, and interest expenses are the 3 major elements of a cash flow statement (Sheedy,

Griffin and Barbour, 2017).

o CFS's operating endeavors include all uses and suppliers of cash resources derived from

commercial processes such as goods and commodity sales. Instances include bills

receipts and payments, inventories, amortization, compensation and payroll, and so forth.

o The use and origins of funds from the firm's long holdings are included in investing

operations. Credits or advancements issued or obtained, the acquisition and selling of

marketable securities, and so on are examples.

o Money acquired from creditors and businesses, as well as income distributions given to

stockholders, are examples of finance operations. Funding operations include the sale of

stocks and bonds, the repayment of borrowing, and the distribution of profits.

Financial Ratios

Financial metrics aid in the analysis of a corporation's outcomes in general of solvency,

competitiveness, and effectiveness. Such metrics are typically used to evaluate a company's total

fiscal status to its rivals'. In essence, proportions are time-oriented, therefore it could be used to

track a corporation's progress over the years. The following are 3 of the most common fiscal

ratios:

Profitability Ratios: Profitability Proportions, often referred as Return on Investment

(ROI) proportions, are used to assess an organizational value based on its profitability. A bigger

profitability usually suggests that the firm is in excellent fiscal shape and performing well. Total

Revenue Margins, Net Income Margin, and Return on Capital are the three most used

performance metrics (Shoup, 2017). After calculating the revenue margins created on selling, the

total revenue margins reveal the corporation's production and trading productivity and

performance. The net income margins are a measure of a firm's corporate performance. The

return on investment (ROI) is a metric that shows how efficient a firm has used its funds.

Liquidity Ratios: Liquidity Ratios are used to determine a firm's potential to discharge

its obligations and commitments. If the business can create sufficient currency capital to support

all of its expenditures or doesn't even have sufficient short-term resources to fulfil its short-term

obligations and responsibilities, it may experience fiscal difficulties. The Current Ratio and the

Quick Ratio are the 2 most important liquidity metrics. The current ratio measures a

corporation's capacity to properly pay down its short-term loans. A least of 2:1 is the criterion for

this proportion. The quick or acid-test ratio is a more stringent way of determining a

corporation's capacity to repay down present or short-term obligations. The optimal proportion

for this combination is one to one (Wang, Dou and Jia, 2016).

Leverage Ratios: The potential of a corporation to pay down its long-term debts is

measured by leverage metrics. Such metrics examine and evaluate the corporation's dependence

on borrowing and advancements to finance its activities. Debt Ratio and Debt-Equity Ratio are

two of the most widely utilised leverage ratios. The debt ratio shows how much of a firm's

capitalization is financed via borrowing. The debt-to-equity ratio compares how much of a

corporation's capitalization is financed by loans vs how much is financed by its investors and

proprietors.

Section 3: Using the template provided:

Net profit margin = 43057 / 189711 * 100

= 22.69%

Gross profit margin= 81125 / 189711 * 100

= 42.76%

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

return on investment (ROI) is a metric that shows how efficient a firm has used its funds.

Liquidity Ratios: Liquidity Ratios are used to determine a firm's potential to discharge

its obligations and commitments. If the business can create sufficient currency capital to support

all of its expenditures or doesn't even have sufficient short-term resources to fulfil its short-term

obligations and responsibilities, it may experience fiscal difficulties. The Current Ratio and the

Quick Ratio are the 2 most important liquidity metrics. The current ratio measures a

corporation's capacity to properly pay down its short-term loans. A least of 2:1 is the criterion for

this proportion. The quick or acid-test ratio is a more stringent way of determining a

corporation's capacity to repay down present or short-term obligations. The optimal proportion

for this combination is one to one (Wang, Dou and Jia, 2016).

Leverage Ratios: The potential of a corporation to pay down its long-term debts is

measured by leverage metrics. Such metrics examine and evaluate the corporation's dependence

on borrowing and advancements to finance its activities. Debt Ratio and Debt-Equity Ratio are

two of the most widely utilised leverage ratios. The debt ratio shows how much of a firm's

capitalization is financed via borrowing. The debt-to-equity ratio compares how much of a

corporation's capitalization is financed by loans vs how much is financed by its investors and

proprietors.

Section 3: Using the template provided:

Net profit margin = 43057 / 189711 * 100

= 22.69%

Gross profit margin= 81125 / 189711 * 100

= 42.76%

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Section 3: According on the ratio assessment findings, characterise the corporation's

competitiveness, solvency, and effectiveness using the case study data

On the foundation of its Ratio Review, the corporation's revenue, productivity, and

solvency have also been remarked on it after thorough collection of the information provided in

the Case Study included in Appendix.

Profitability

The net income increased towards the ending of the year 2015, increasing from £18,987

to £43,057 in the following season. Following an examination of the firm's earnings parameters,

it was discovered that perhaps the total revenue margins is 42.8 percent and the net income

margins is 22.7 percent. The corporation's competitiveness might be said to be significant

because the net income margins has increased (Bouveret, 2018).

Liquidity

After examining the corporation's current and quick metrics, the current ratio is 2.22:1,

which is greater than the industry standard of 2:1. This demonstrates that the corporation's

stability is superior than those of other identical businesses. The corporation's excellent stability

could be seen in the Quick ratio, which would be 1.47:1, which would be greater than the

industry mean of 1:1.

Efficiency

Asset turnover is a good indicator of a firm's productivity. For each and every £1 spent, the

proprietors gain £2.26. It is clear that it invests its financial funds wisely, as its investors and

proprietors had received a return on investment of over 226 percent.

Section 4: Utilizing instances from the research study, describe and analyze the strategies that

this company could employ to enhance its fiscal efficiency

Even though the organisation has already been operating quickly and successfully,

administration could evaluate several features and difficulties in order to enhance its

effectiveness. The following are among the approaches which the corporation could pursue:

Marketing Tactic: A corporation could design an appropriate advertising mix to increase

communications and effectiveness in the advertising of the items and operations. This would

increase the corporation's revenue by increasing its market share.

Credit Policies: The firm's credit regulations could be revised and tightened. This will

shorten the time it takes to recover a loan from a customer. This would also assist the firm's

competitiveness, solvency, and effectiveness using the case study data

On the foundation of its Ratio Review, the corporation's revenue, productivity, and

solvency have also been remarked on it after thorough collection of the information provided in

the Case Study included in Appendix.

Profitability

The net income increased towards the ending of the year 2015, increasing from £18,987

to £43,057 in the following season. Following an examination of the firm's earnings parameters,

it was discovered that perhaps the total revenue margins is 42.8 percent and the net income

margins is 22.7 percent. The corporation's competitiveness might be said to be significant

because the net income margins has increased (Bouveret, 2018).

Liquidity

After examining the corporation's current and quick metrics, the current ratio is 2.22:1,

which is greater than the industry standard of 2:1. This demonstrates that the corporation's

stability is superior than those of other identical businesses. The corporation's excellent stability

could be seen in the Quick ratio, which would be 1.47:1, which would be greater than the

industry mean of 1:1.

Efficiency

Asset turnover is a good indicator of a firm's productivity. For each and every £1 spent, the

proprietors gain £2.26. It is clear that it invests its financial funds wisely, as its investors and

proprietors had received a return on investment of over 226 percent.

Section 4: Utilizing instances from the research study, describe and analyze the strategies that

this company could employ to enhance its fiscal efficiency

Even though the organisation has already been operating quickly and successfully,

administration could evaluate several features and difficulties in order to enhance its

effectiveness. The following are among the approaches which the corporation could pursue:

Marketing Tactic: A corporation could design an appropriate advertising mix to increase

communications and effectiveness in the advertising of the items and operations. This would

increase the corporation's revenue by increasing its market share.

Credit Policies: The firm's credit regulations could be revised and tightened. This will

shorten the time it takes to recover a loan from a customer. This would also assist the firm's

financial position, allowing it to deposit its very own resources back into the business. As a

result, the company's debt-to-equity proportion would improve (Eka, 2018).

Conclusion

The principles and significance of the different fiscal reports were the subject of this

research. The many forms of profitability metrics have also been examined and debated.

Analyses and suggestions for the business in the research study have also been made depending

on such profitability metrics. Additional suggestions were provided to assist the organisation in

improving and enhancing its fiscal place in the industry. In the Appendices, there are further

instances of information collection and presentation that have been constructed and evaluated

using suitable calculations.

result, the company's debt-to-equity proportion would improve (Eka, 2018).

Conclusion

The principles and significance of the different fiscal reports were the subject of this

research. The many forms of profitability metrics have also been examined and debated.

Analyses and suggestions for the business in the research study have also been made depending

on such profitability metrics. Additional suggestions were provided to assist the organisation in

improving and enhancing its fiscal place in the industry. In the Appendices, there are further

instances of information collection and presentation that have been constructed and evaluated

using suitable calculations.

References

Books and journals

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Henager, R. and Cude, B.J., 2016. Financial Literacy and Long-and Short-Term Financial

Behavior in Different Age Groups. Journal of Financial Counseling and Planning,

27(1), pp.3-19.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Sheedy, E.A., Griffin, B. and Barbour, J.P., 2017. A framework and measure for examining risk

climate in financial institutions. Journal of Business and Psychology. 32(1). pp.101-116.

Shoup, C., 2017. Public finance. Routledge.

Wang, Q., Dou, J. and Jia, S., 2016. A meta-analytic review of corporate social responsibility

and corporate financial performance: The moderating effect of contextual

factors. Business & Society. 55(8). pp.1083-1121.

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Books and journals

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Henager, R. and Cude, B.J., 2016. Financial Literacy and Long-and Short-Term Financial

Behavior in Different Age Groups. Journal of Financial Counseling and Planning,

27(1), pp.3-19.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for

ensuring effective functioning of the residential real estate market.

Levy, A., Bouheni, F.B. and Ammi, C., 2018. Financial management: USGAAP and IFRS

Standards. John Wiley & Sons.

Ivanovich, K.K., 2020. About some questions of classification of institutional conditions

determining the structure of doing business in Uzbekistan. South Asian Journal of

Marketing & Management Research. 10(5). pp.17-28.

Sheedy, E.A., Griffin, B. and Barbour, J.P., 2017. A framework and measure for examining risk

climate in financial institutions. Journal of Business and Psychology. 32(1). pp.101-116.

Shoup, C., 2017. Public finance. Routledge.

Wang, Q., Dou, J. and Jia, S., 2016. A meta-analytic review of corporate social responsibility

and corporate financial performance: The moderating effect of contextual

factors. Business & Society. 55(8). pp.1083-1121.

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Eka, H., 2018. Corporate finance and firm value in the Indonesian manufacturing

companies. BUSINESS STUDIES. 11(2). pp.113-127.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

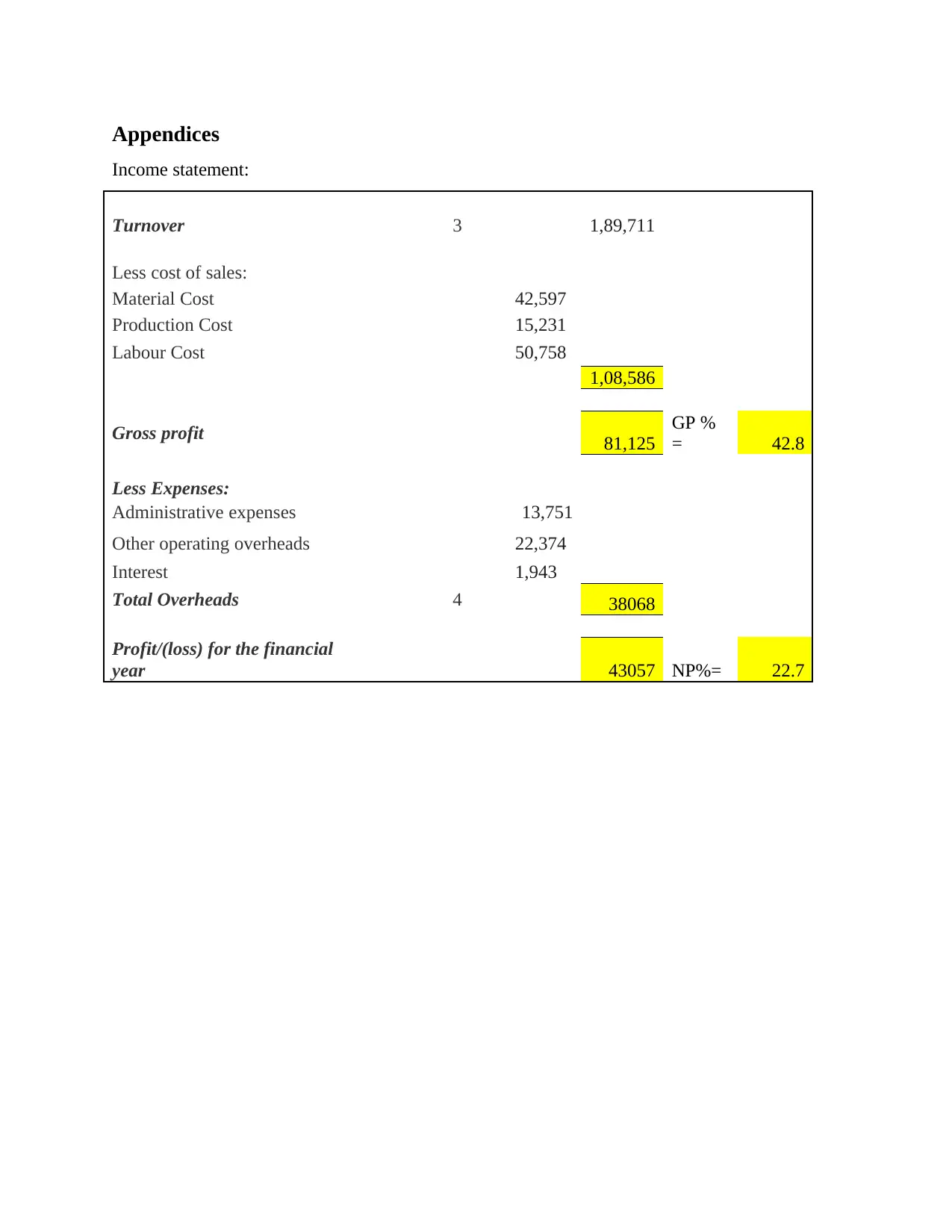

Appendices

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

Income statement:

Turnover 3 1,89,711

Less cost of sales:

Material Cost 42,597

Production Cost 15,231

Labour Cost 50,758

1,08,586

Gross profit 81,125

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751

Other operating overheads 22,374

Interest 1,943

Total Overheads 4 38068

Profit/(loss) for the financial

year 43057 NP%= 22.7

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.