Tesco Plc Financial Analysis Report: Company Valuation and Capital

VerifiedAdded on 2023/01/06

|14

|2630

|3

Report

AI Summary

This finance report provides a comprehensive analysis of Tesco Plc, a major British retailer. It begins with a comparative financial analysis using ratio analysis, comparing Tesco to its competitors, Morrisons and J Sainsbury. The analysis covers liquidity, solvency, profitability, efficiency, and market prospect ratios, providing insights into each company's financial health. The report then delves into company valuation, employing asset-based valuation, dividend valuation model, and price-earnings (P/E) ratio methods to determine Tesco's value. Finally, the report addresses capital structure, calculating the cost of debt, cost of equity, and weighted average cost of capital (WACC) for Absolute Plc, including a discussion of the limitations of WACC calculations. The report concludes by summarizing the key findings and emphasizing the broad scope and significance of finance in business operations.

Finance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Financial Analysis..................................................................................................................3

Company valuation:................................................................................................................6

Capital structure....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

Financial Analysis..................................................................................................................3

Company valuation:................................................................................................................6

Capital structure....................................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

Introduction

Finance is a broad term used for management of money and investment activities related

to money. It represents process of raising funds for the business operations and their

management (Choi and et.al., 2018). It deals with activities associated with leveraging, debt-

equity, capital market, etc.

Tesco Plc is a British company founded in 1919. It operates as a groceries and general

merchandise retail chain. The stores also provide software and financial services. It offers both

online and offline channels of distribution. The following report contains three major parts. First

part contains assessment of financial and operating performance of Tesco Plc and its two

competitors Morrisons Supermarket Plc and J Sainsbury Plc using comparative ratio analysis.

Second part contains valuation of Tesco through different approaches. Final part consists of

practical questions related to capital structure of Absolute Plc. In it, cost of debt, cost of equity

and weighted average cost of capital is determined.

Task 1

Financial Analysis

Financial analysis refers to the process of using financial information of a company to

assess profitability of businesses, projects or budgets of company. Necessary recommendations

for improvement are made on its basis. Various techniques are used for financial analysis such as

ratio analysis, trend analysis, cash flow and fund flow analysis, etc.

Ratio Analysis - Ratio analysis is a technique of financial analysis which helps

management in gaining insights into company's profitability, liquidity, solvency and efficiency.

It helps management of company in analysing the financial performance and health of company

in comparison to its own historical records as well as competitor's performance (Luo and et.al.,

2016). Financial ratios are grouped in certain categories. Below is the comparative ratio analysis

of Tesco Plc and its two competitors – Morrisons Supermarket Plc and J Sainsbury Plc in above

mentioned categories: Figures are taken from Annual-report of the three companies for period

ending Feb-Mar 2019. Liquidity Ratios – Liquidity refers to a company's capability of converting their assets

into cash. These ratios are fundamental ratios to assess the company's ability to meet its

3

Finance is a broad term used for management of money and investment activities related

to money. It represents process of raising funds for the business operations and their

management (Choi and et.al., 2018). It deals with activities associated with leveraging, debt-

equity, capital market, etc.

Tesco Plc is a British company founded in 1919. It operates as a groceries and general

merchandise retail chain. The stores also provide software and financial services. It offers both

online and offline channels of distribution. The following report contains three major parts. First

part contains assessment of financial and operating performance of Tesco Plc and its two

competitors Morrisons Supermarket Plc and J Sainsbury Plc using comparative ratio analysis.

Second part contains valuation of Tesco through different approaches. Final part consists of

practical questions related to capital structure of Absolute Plc. In it, cost of debt, cost of equity

and weighted average cost of capital is determined.

Task 1

Financial Analysis

Financial analysis refers to the process of using financial information of a company to

assess profitability of businesses, projects or budgets of company. Necessary recommendations

for improvement are made on its basis. Various techniques are used for financial analysis such as

ratio analysis, trend analysis, cash flow and fund flow analysis, etc.

Ratio Analysis - Ratio analysis is a technique of financial analysis which helps

management in gaining insights into company's profitability, liquidity, solvency and efficiency.

It helps management of company in analysing the financial performance and health of company

in comparison to its own historical records as well as competitor's performance (Luo and et.al.,

2016). Financial ratios are grouped in certain categories. Below is the comparative ratio analysis

of Tesco Plc and its two competitors – Morrisons Supermarket Plc and J Sainsbury Plc in above

mentioned categories: Figures are taken from Annual-report of the three companies for period

ending Feb-Mar 2019. Liquidity Ratios – Liquidity refers to a company's capability of converting their assets

into cash. These ratios are fundamental ratios to assess the company's ability to meet its

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

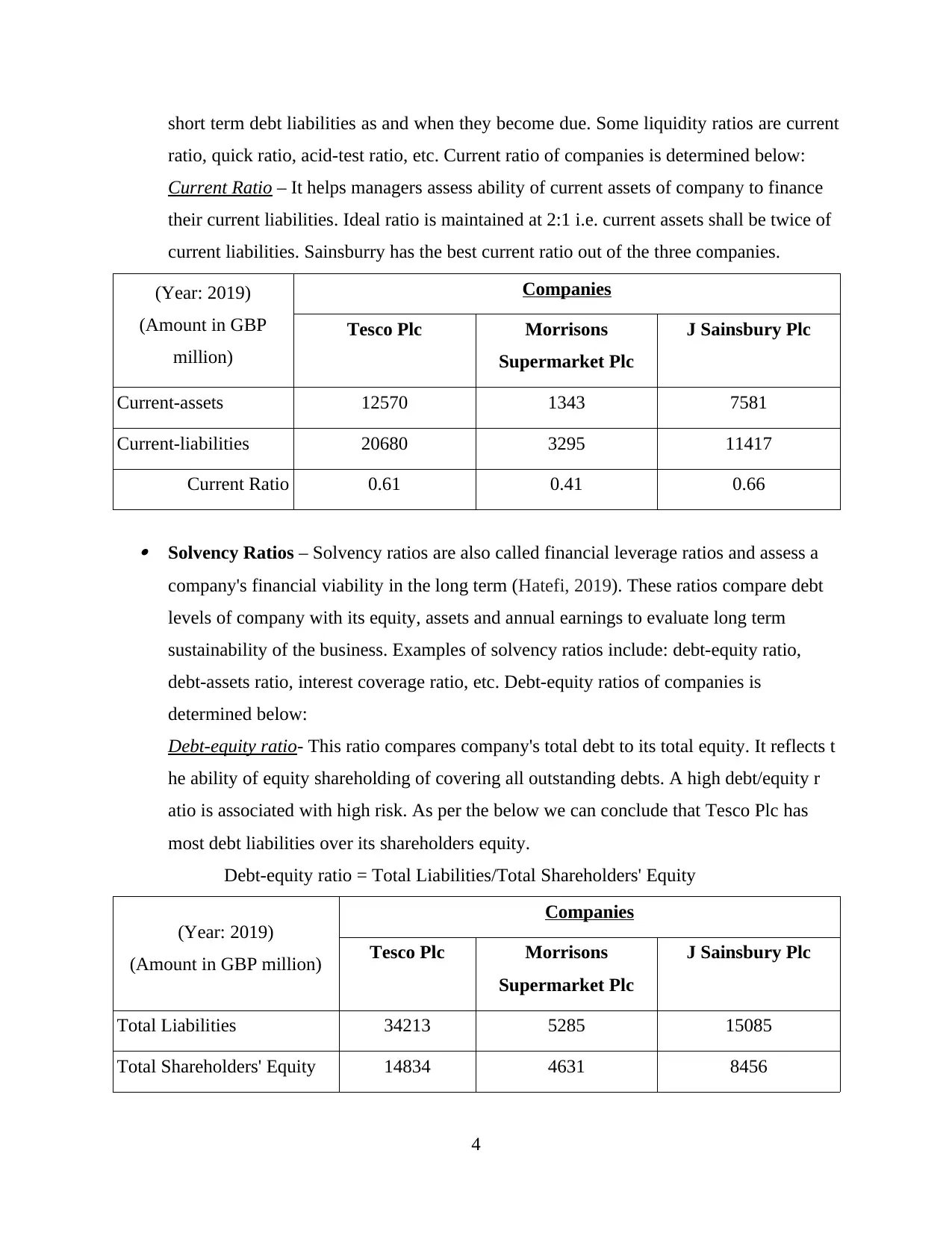

short term debt liabilities as and when they become due. Some liquidity ratios are current

ratio, quick ratio, acid-test ratio, etc. Current ratio of companies is determined below:

Current Ratio – It helps managers assess ability of current assets of company to finance

their current liabilities. Ideal ratio is maintained at 2:1 i.e. current assets shall be twice of

current liabilities. Sainsburry has the best current ratio out of the three companies.

(Year: 2019)

(Amount in GBP

million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Current-assets 12570 1343 7581

Current-liabilities 20680 3295 11417

Current Ratio 0.61 0.41 0.66

Solvency Ratios – Solvency ratios are also called financial leverage ratios and assess a

company's financial viability in the long term (Hatefi, 2019). These ratios compare debt

levels of company with its equity, assets and annual earnings to evaluate long term

sustainability of the business. Examples of solvency ratios include: debt-equity ratio,

debt-assets ratio, interest coverage ratio, etc. Debt-equity ratios of companies is

determined below:

Debt-equity ratio- This ratio compares company's total debt to its total equity. It reflects t

he ability of equity shareholding of covering all outstanding debts. A high debt/equity r

atio is associated with high risk. As per the below we can conclude that Tesco Plc has

most debt liabilities over its shareholders equity.

Debt-equity ratio = Total Liabilities/Total Shareholders' Equity

(Year: 2019)

(Amount in GBP million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Total Liabilities 34213 5285 15085

Total Shareholders' Equity 14834 4631 8456

4

ratio, quick ratio, acid-test ratio, etc. Current ratio of companies is determined below:

Current Ratio – It helps managers assess ability of current assets of company to finance

their current liabilities. Ideal ratio is maintained at 2:1 i.e. current assets shall be twice of

current liabilities. Sainsburry has the best current ratio out of the three companies.

(Year: 2019)

(Amount in GBP

million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Current-assets 12570 1343 7581

Current-liabilities 20680 3295 11417

Current Ratio 0.61 0.41 0.66

Solvency Ratios – Solvency ratios are also called financial leverage ratios and assess a

company's financial viability in the long term (Hatefi, 2019). These ratios compare debt

levels of company with its equity, assets and annual earnings to evaluate long term

sustainability of the business. Examples of solvency ratios include: debt-equity ratio,

debt-assets ratio, interest coverage ratio, etc. Debt-equity ratios of companies is

determined below:

Debt-equity ratio- This ratio compares company's total debt to its total equity. It reflects t

he ability of equity shareholding of covering all outstanding debts. A high debt/equity r

atio is associated with high risk. As per the below we can conclude that Tesco Plc has

most debt liabilities over its shareholders equity.

Debt-equity ratio = Total Liabilities/Total Shareholders' Equity

(Year: 2019)

(Amount in GBP million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Total Liabilities 34213 5285 15085

Total Shareholders' Equity 14834 4631 8456

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

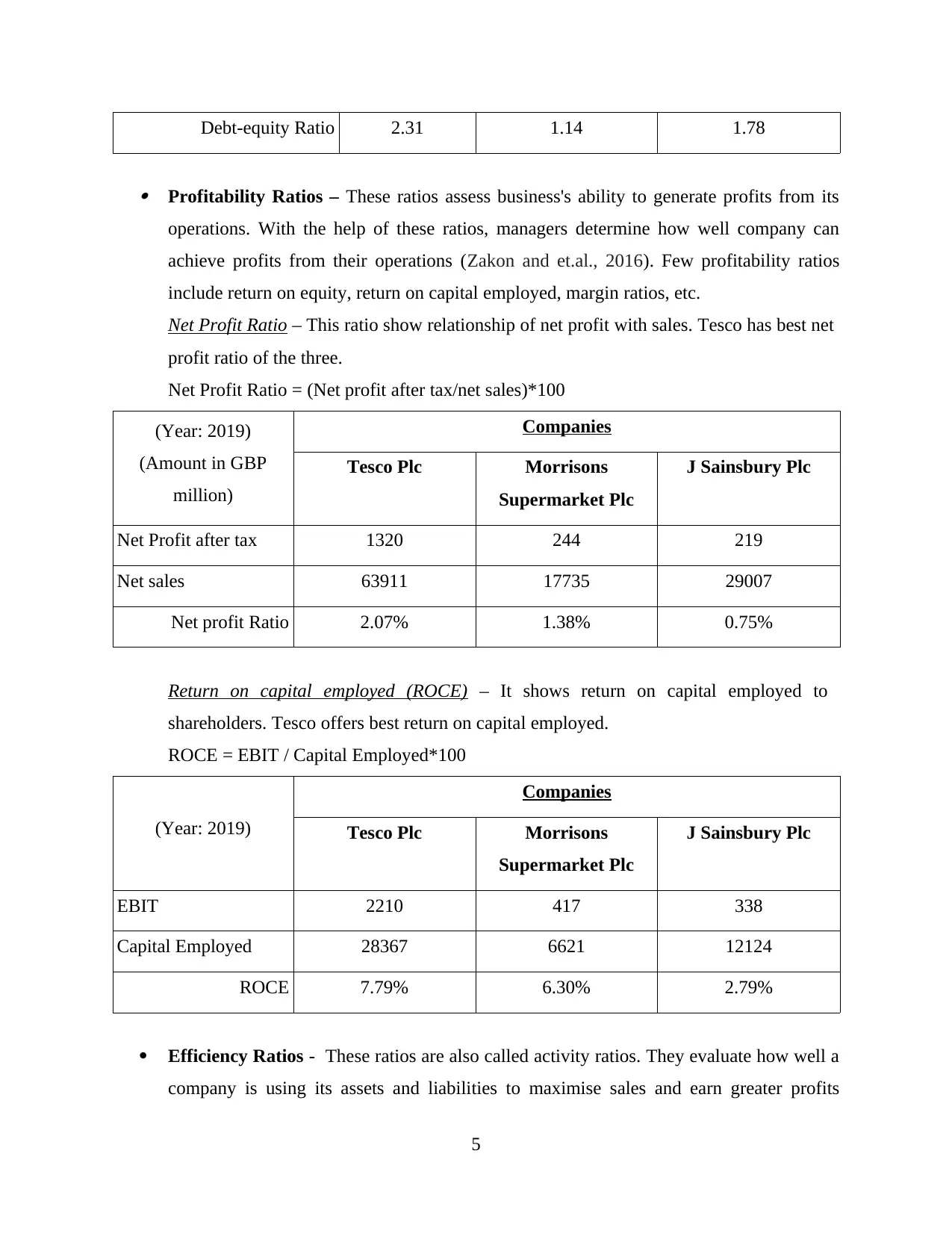

Debt-equity Ratio 2.31 1.14 1.78

Profitability Ratios – These ratios assess business's ability to generate profits from its

operations. With the help of these ratios, managers determine how well company can

achieve profits from their operations (Zakon and et.al., 2016). Few profitability ratios

include return on equity, return on capital employed, margin ratios, etc.

Net Profit Ratio – This ratio show relationship of net profit with sales. Tesco has best net

profit ratio of the three.

Net Profit Ratio = (Net profit after tax/net sales)*100

(Year: 2019)

(Amount in GBP

million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Net Profit after tax 1320 244 219

Net sales 63911 17735 29007

Net profit Ratio 2.07% 1.38% 0.75%

Return on capital employed (ROCE) – It shows return on capital employed to

shareholders. Tesco offers best return on capital employed.

ROCE = EBIT / Capital Employed*100

(Year: 2019)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

EBIT 2210 417 338

Capital Employed 28367 6621 12124

ROCE 7.79% 6.30% 2.79%

Efficiency Ratios - These ratios are also called activity ratios. They evaluate how well a

company is using its assets and liabilities to maximise sales and earn greater profits

5

Profitability Ratios – These ratios assess business's ability to generate profits from its

operations. With the help of these ratios, managers determine how well company can

achieve profits from their operations (Zakon and et.al., 2016). Few profitability ratios

include return on equity, return on capital employed, margin ratios, etc.

Net Profit Ratio – This ratio show relationship of net profit with sales. Tesco has best net

profit ratio of the three.

Net Profit Ratio = (Net profit after tax/net sales)*100

(Year: 2019)

(Amount in GBP

million)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Net Profit after tax 1320 244 219

Net sales 63911 17735 29007

Net profit Ratio 2.07% 1.38% 0.75%

Return on capital employed (ROCE) – It shows return on capital employed to

shareholders. Tesco offers best return on capital employed.

ROCE = EBIT / Capital Employed*100

(Year: 2019)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

EBIT 2210 417 338

Capital Employed 28367 6621 12124

ROCE 7.79% 6.30% 2.79%

Efficiency Ratios - These ratios are also called activity ratios. They evaluate how well a

company is using its assets and liabilities to maximise sales and earn greater profits

5

(Pinto, 2020). Improvement in efficiency ratios refers improvement in revenue

generation. Key efficiency ratios include: inventory turnover ratio, asset turnover ratio,

receivables turnover ratio, etc.

Asset Turnover Ratio – It shows the number of times assets are utilised to convert into

sales.

Asset Turnover Ratio = Net Sales / Average Total Assets

(Year: 2019)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Net sales 63911 17735 29007

Average Total Assets 46965.5 9791.5 22771

Asset Turnover Ratio 1.36 1.81 1.27 Market prospect Ratios – These ratios help investors to predict future performance of

business and their earnings out of it (Bond and et.al., 2017). These earnings are in the

form of high future dividends or higher stock valued. They include price-earning ratio

(P/E Ratio), earning per share (EPS), dividend payout ratio, dividend yield, etc.

Earning per share: It shows earning of the shareholders on each share of the company. In the

following table it is clear that Tesco has better EPS in comparison to its competitors.

(Year: 2019)

Companies

Tesco Plc Morrisons Supermarket Plc J Sainsbury Plc

Basic EPS from

continuing operations

13.65p 10.34p 9.1p

Limitation of usefulness of financial ratio analysis Historical information – Information used in the analysis is based on past results of the

company. Thus, are not true reflection of future company performance. Changes in accounting policies – If a company has significant changes in its accounting

policies, financial metrics used for ratio analysis are rendered incomparable. Ratio

analysis needs to be changed accordingly.

6

generation. Key efficiency ratios include: inventory turnover ratio, asset turnover ratio,

receivables turnover ratio, etc.

Asset Turnover Ratio – It shows the number of times assets are utilised to convert into

sales.

Asset Turnover Ratio = Net Sales / Average Total Assets

(Year: 2019)

Companies

Tesco Plc Morrisons

Supermarket Plc

J Sainsbury Plc

Net sales 63911 17735 29007

Average Total Assets 46965.5 9791.5 22771

Asset Turnover Ratio 1.36 1.81 1.27 Market prospect Ratios – These ratios help investors to predict future performance of

business and their earnings out of it (Bond and et.al., 2017). These earnings are in the

form of high future dividends or higher stock valued. They include price-earning ratio

(P/E Ratio), earning per share (EPS), dividend payout ratio, dividend yield, etc.

Earning per share: It shows earning of the shareholders on each share of the company. In the

following table it is clear that Tesco has better EPS in comparison to its competitors.

(Year: 2019)

Companies

Tesco Plc Morrisons Supermarket Plc J Sainsbury Plc

Basic EPS from

continuing operations

13.65p 10.34p 9.1p

Limitation of usefulness of financial ratio analysis Historical information – Information used in the analysis is based on past results of the

company. Thus, are not true reflection of future company performance. Changes in accounting policies – If a company has significant changes in its accounting

policies, financial metrics used for ratio analysis are rendered incomparable. Ratio

analysis needs to be changed accordingly.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inflationary effects - Inflation changes between two years and it is not reflected in the

ratio analysis. This makes ratio incomparable without making necessary adjustments.

Company valuation:

(a) Valuation of Tesco Plc:

Asset Based Valuation: This approach is based on valuation of net assets. Net assets are

determined by subtracting total liabilities from total assets (Elliott, Hobson and White, 2015).

Asset Based Valuation of Tesco Plc

2018 (in GBP millions)

Assets

Current assets

Cash and cash equivalents 2916

Receivables 1640

Inventories 2617

Loans and advances to customers and banks 4882

Other current assets 515

Total current assets 12570

Non-current assets

Net property, plant and equipment 19023

Goodwill 6264

Investments 740

Deferred income taxes 132

Loans and advances to customers and banks 7868

Other long-term assets 2450

Total non-current assets 36477

Total assets 49047

7

ratio analysis. This makes ratio incomparable without making necessary adjustments.

Company valuation:

(a) Valuation of Tesco Plc:

Asset Based Valuation: This approach is based on valuation of net assets. Net assets are

determined by subtracting total liabilities from total assets (Elliott, Hobson and White, 2015).

Asset Based Valuation of Tesco Plc

2018 (in GBP millions)

Assets

Current assets

Cash and cash equivalents 2916

Receivables 1640

Inventories 2617

Loans and advances to customers and banks 4882

Other current assets 515

Total current assets 12570

Non-current assets

Net property, plant and equipment 19023

Goodwill 6264

Investments 740

Deferred income taxes 132

Loans and advances to customers and banks 7868

Other long-term assets 2450

Total non-current assets 36477

Total assets 49047

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

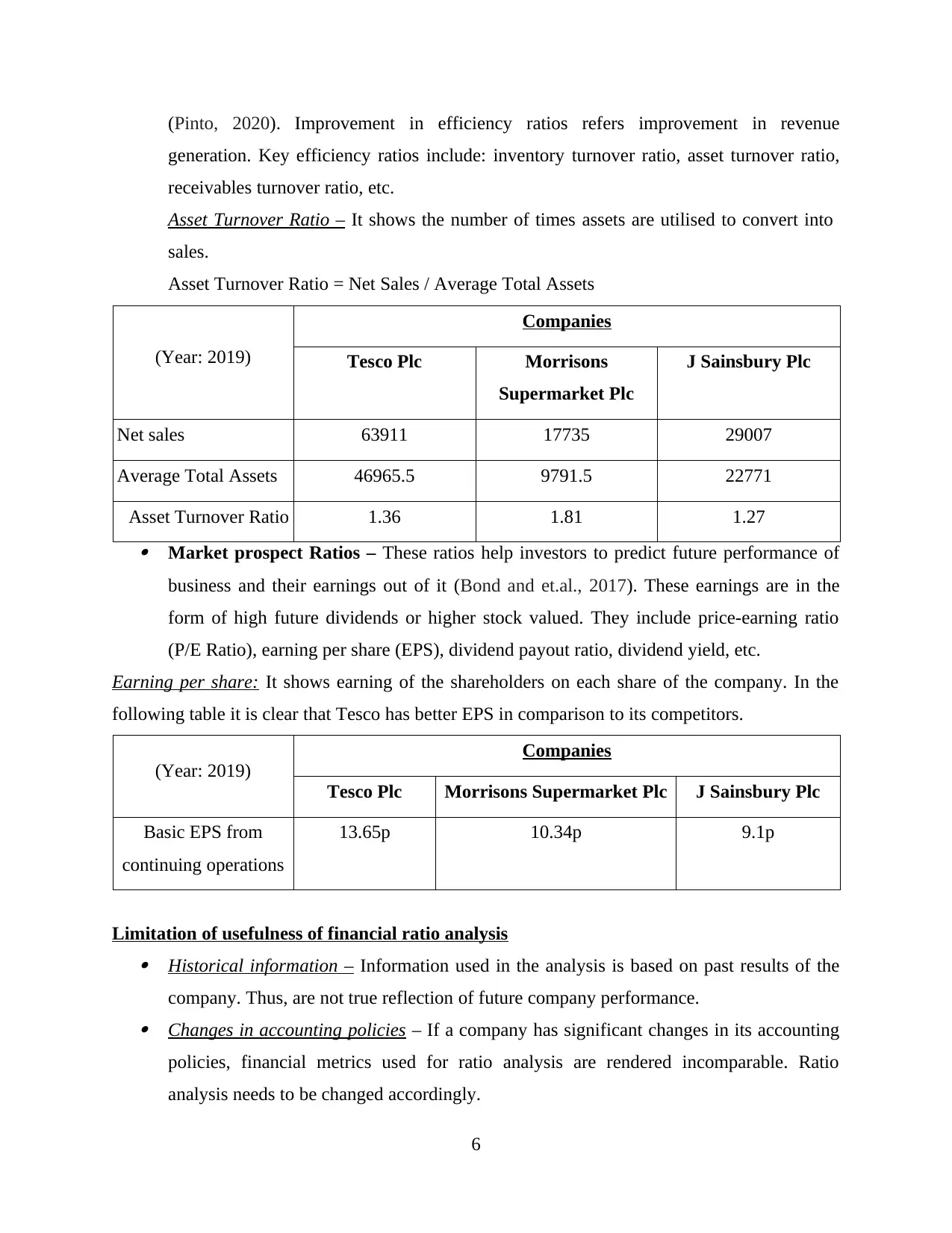

Liabilities

Current liabilities

Borrowings, customer deposits and deposits from banks 10431

Accounts payable 9354

Taxes payable 325

Other current liabilities 570

Total current liabilities 20680

Non-current liabilities

Borrowings, customer deposits and deposits from banks 8969

Trade and other payables 384

Deferred tax liabilities 236

Pensions and other benefits 2808

Other long-term liabilities 1136

Total non-current liabilities 13533

Total liabilities 34213

Net Assets of Tesco Plc 14834

Thus, value as per assets based valuation of Tesco Plc is GBP 14834 millions

Cross Check:

Stockholders' equity

Share Capital 490

Share premium 5165

Retained earnings 5405

8

Current liabilities

Borrowings, customer deposits and deposits from banks 10431

Accounts payable 9354

Taxes payable 325

Other current liabilities 570

Total current liabilities 20680

Non-current liabilities

Borrowings, customer deposits and deposits from banks 8969

Trade and other payables 384

Deferred tax liabilities 236

Pensions and other benefits 2808

Other long-term liabilities 1136

Total non-current liabilities 13533

Total liabilities 34213

Net Assets of Tesco Plc 14834

Thus, value as per assets based valuation of Tesco Plc is GBP 14834 millions

Cross Check:

Stockholders' equity

Share Capital 490

Share premium 5165

Retained earnings 5405

8

All other reserves 3774

Total stockholders' equity 14834

Dividend Valuation Model: It is a quantitative method used to predict value of company's stock

price. It discounts all future dividends to their present value and sum it. It assumes that the

present day price is worth the sum of all its future dividend payments when discounted-back to

present day value.

Growth Rate (g) = 4.00%

Do = 5

D1 i.e. (D0 + g) = 5+4.00% = 5.2

Market premium = 6.00%

Risk free rate of Return = 10.00%

Beta = 1.3

Re = Rf + (Rm -Rf) x Beta = 10 +6 x 1.3 = 17.80%

D1 / (Re – g) = 5.2 / (17.8% - 4%) = 37.68 %

Issued and fully paid Shares = 3467 million

Thus value of Tesco plc would be: 3467 million * 37.68 = 1306 Million

(Values have been assumed to show appropriate calculations)

PE Method: It is a ratio method for valuing a company in terms of market price of its shares in

relation to its earning per share. It is also known as price multiple or earnings multiple.

9

Total stockholders' equity 14834

Dividend Valuation Model: It is a quantitative method used to predict value of company's stock

price. It discounts all future dividends to their present value and sum it. It assumes that the

present day price is worth the sum of all its future dividend payments when discounted-back to

present day value.

Growth Rate (g) = 4.00%

Do = 5

D1 i.e. (D0 + g) = 5+4.00% = 5.2

Market premium = 6.00%

Risk free rate of Return = 10.00%

Beta = 1.3

Re = Rf + (Rm -Rf) x Beta = 10 +6 x 1.3 = 17.80%

D1 / (Re – g) = 5.2 / (17.8% - 4%) = 37.68 %

Issued and fully paid Shares = 3467 million

Thus value of Tesco plc would be: 3467 million * 37.68 = 1306 Million

(Values have been assumed to show appropriate calculations)

PE Method: It is a ratio method for valuing a company in terms of market price of its shares in

relation to its earning per share. It is also known as price multiple or earnings multiple.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

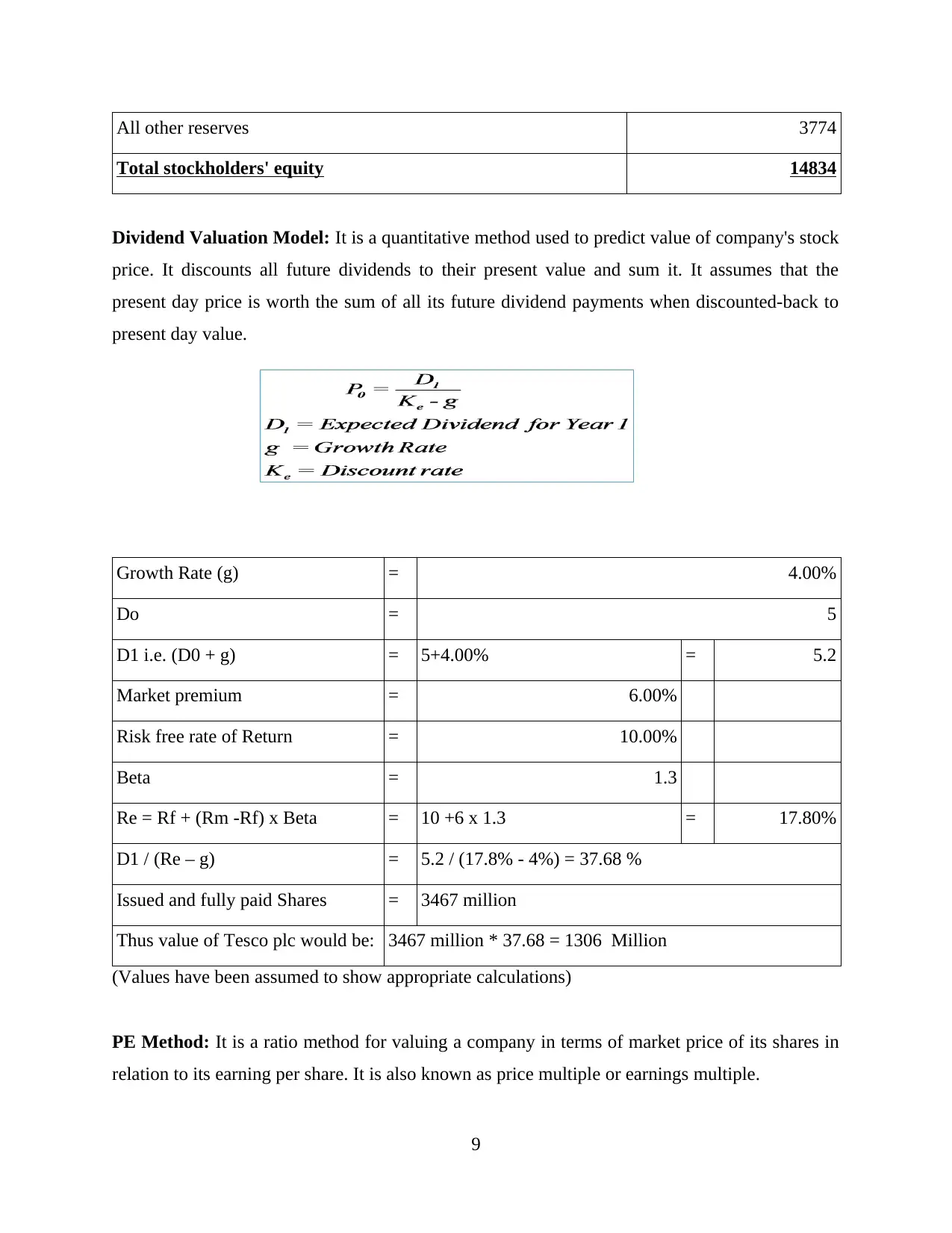

Valuation of Tesco Plc through PE Method

GBP in millions 2018

Sales Receipts 63911

Cost of goods sold -59767

Gross-profit 4144

Operating-expenditures 2075

Aggregate operating expenses -2075

Interest Expenditure -536

Other miscellaneous income 141

PBT 1674

Provision for income-taxes 354

Net-income from continuing operations 1320

Net-income attributable to owners of the parent 1322

Net-income for non-controlling interests -2

Earnings per share

Basic 13.65p

P/E Method = Market Share Price / Earning Per Share 213.6/13.65

=16.97

Business Value = PE Ratio * Net income = 16.97 * 1322 million 22430 Million

Capital structure

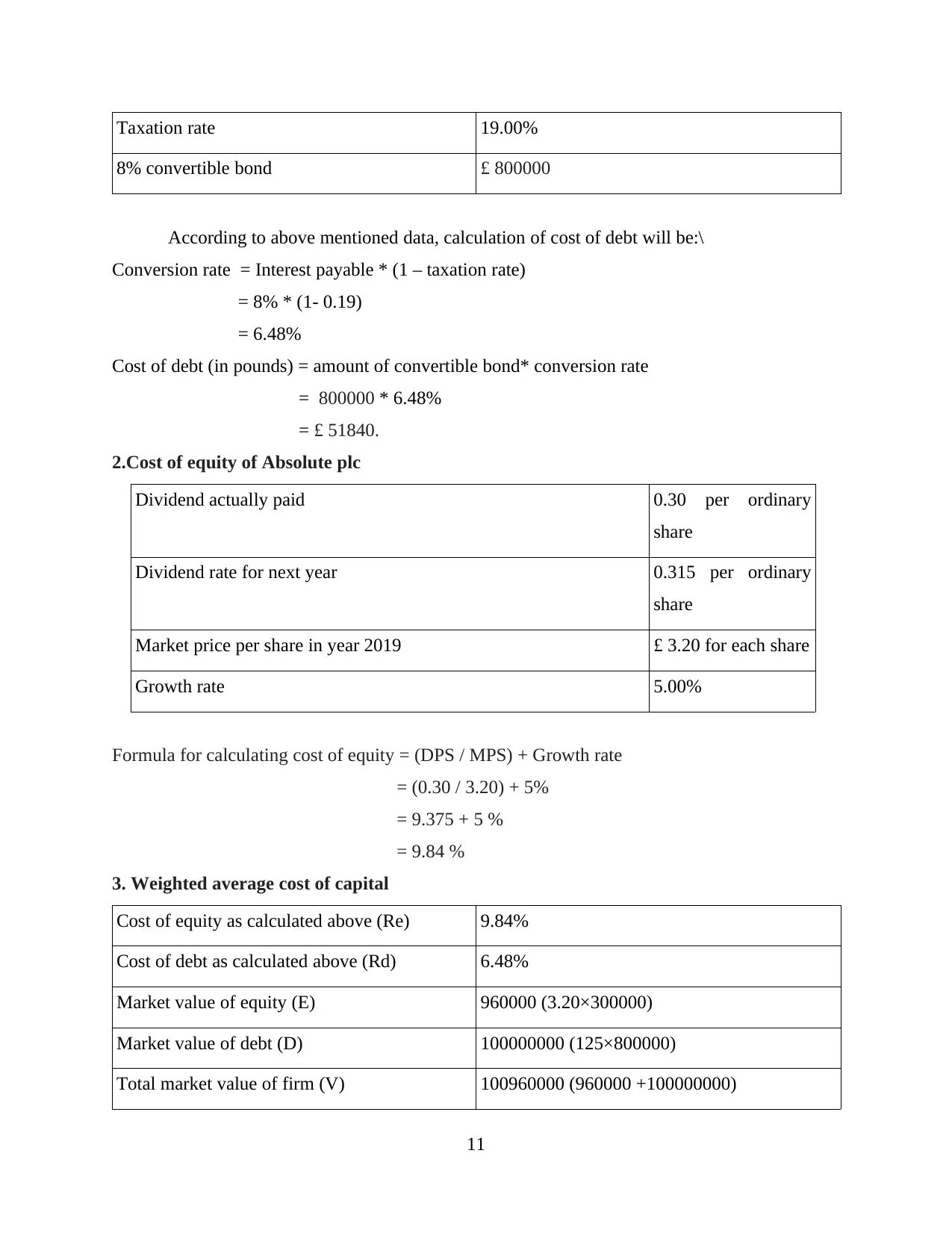

1.Cost of debt of absolute plc

Rate of interest on convertible bond 8.00%

10

GBP in millions 2018

Sales Receipts 63911

Cost of goods sold -59767

Gross-profit 4144

Operating-expenditures 2075

Aggregate operating expenses -2075

Interest Expenditure -536

Other miscellaneous income 141

PBT 1674

Provision for income-taxes 354

Net-income from continuing operations 1320

Net-income attributable to owners of the parent 1322

Net-income for non-controlling interests -2

Earnings per share

Basic 13.65p

P/E Method = Market Share Price / Earning Per Share 213.6/13.65

=16.97

Business Value = PE Ratio * Net income = 16.97 * 1322 million 22430 Million

Capital structure

1.Cost of debt of absolute plc

Rate of interest on convertible bond 8.00%

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation rate 19.00%

8% convertible bond £ 800000

According to above mentioned data, calculation of cost of debt will be:\

Conversion rate = Interest payable * (1 – taxation rate)

= 8% * (1- 0.19)

= 6.48%

Cost of debt (in pounds) = amount of convertible bond* conversion rate

= 800000 * 6.48%

= £ 51840.

2.Cost of equity of Absolute plc

Dividend actually paid 0.30 per ordinary

share

Dividend rate for next year 0.315 per ordinary

share

Market price per share in year 2019 £ 3.20 for each share

Growth rate 5.00%

Formula for calculating cost of equity = (DPS / MPS) + Growth rate

= (0.30 / 3.20) + 5%

= 9.375 + 5 %

= 9.84 %

3. Weighted average cost of capital

Cost of equity as calculated above (Re) 9.84%

Cost of debt as calculated above (Rd) 6.48%

Market value of equity (E) 960000 (3.20×300000)

Market value of debt (D) 100000000 (125×800000)

Total market value of firm (V) 100960000 (960000 +100000000)

11

8% convertible bond £ 800000

According to above mentioned data, calculation of cost of debt will be:\

Conversion rate = Interest payable * (1 – taxation rate)

= 8% * (1- 0.19)

= 6.48%

Cost of debt (in pounds) = amount of convertible bond* conversion rate

= 800000 * 6.48%

= £ 51840.

2.Cost of equity of Absolute plc

Dividend actually paid 0.30 per ordinary

share

Dividend rate for next year 0.315 per ordinary

share

Market price per share in year 2019 £ 3.20 for each share

Growth rate 5.00%

Formula for calculating cost of equity = (DPS / MPS) + Growth rate

= (0.30 / 3.20) + 5%

= 9.375 + 5 %

= 9.84 %

3. Weighted average cost of capital

Cost of equity as calculated above (Re) 9.84%

Cost of debt as calculated above (Rd) 6.48%

Market value of equity (E) 960000 (3.20×300000)

Market value of debt (D) 100000000 (125×800000)

Total market value of firm (V) 100960000 (960000 +100000000)

11

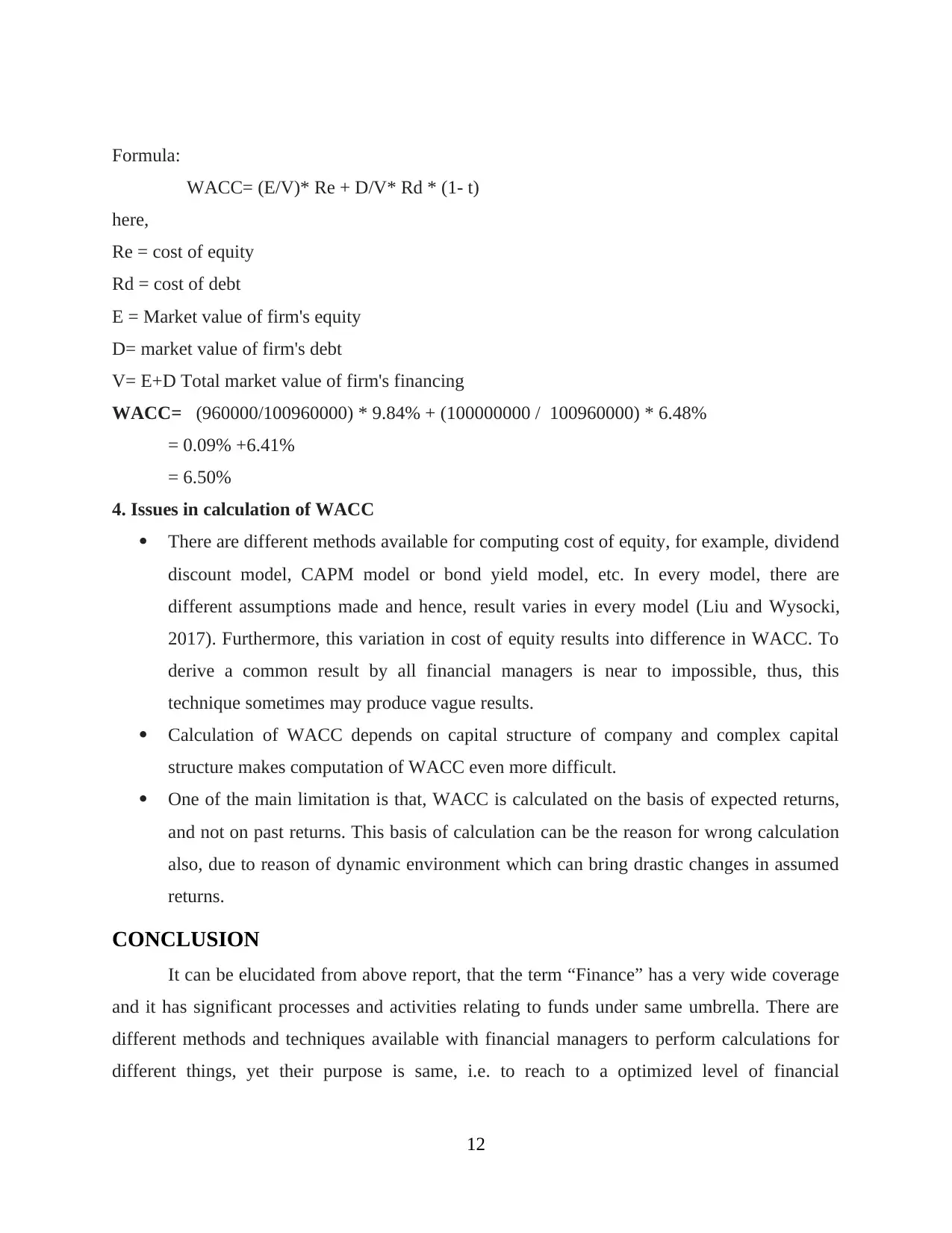

Formula:

WACC= (E/V)* Re + D/V* Rd * (1- t)

here,

Re = cost of equity

Rd = cost of debt

E = Market value of firm's equity

D= market value of firm's debt

V= E+D Total market value of firm's financing

WACC= (960000/100960000) * 9.84% + (100000000 / 100960000) * 6.48%

= 0.09% +6.41%

= 6.50%

4. Issues in calculation of WACC

There are different methods available for computing cost of equity, for example, dividend

discount model, CAPM model or bond yield model, etc. In every model, there are

different assumptions made and hence, result varies in every model (Liu and Wysocki,

2017). Furthermore, this variation in cost of equity results into difference in WACC. To

derive a common result by all financial managers is near to impossible, thus, this

technique sometimes may produce vague results.

Calculation of WACC depends on capital structure of company and complex capital

structure makes computation of WACC even more difficult.

One of the main limitation is that, WACC is calculated on the basis of expected returns,

and not on past returns. This basis of calculation can be the reason for wrong calculation

also, due to reason of dynamic environment which can bring drastic changes in assumed

returns.

CONCLUSION

It can be elucidated from above report, that the term “Finance” has a very wide coverage

and it has significant processes and activities relating to funds under same umbrella. There are

different methods and techniques available with financial managers to perform calculations for

different things, yet their purpose is same, i.e. to reach to a optimized level of financial

12

WACC= (E/V)* Re + D/V* Rd * (1- t)

here,

Re = cost of equity

Rd = cost of debt

E = Market value of firm's equity

D= market value of firm's debt

V= E+D Total market value of firm's financing

WACC= (960000/100960000) * 9.84% + (100000000 / 100960000) * 6.48%

= 0.09% +6.41%

= 6.50%

4. Issues in calculation of WACC

There are different methods available for computing cost of equity, for example, dividend

discount model, CAPM model or bond yield model, etc. In every model, there are

different assumptions made and hence, result varies in every model (Liu and Wysocki,

2017). Furthermore, this variation in cost of equity results into difference in WACC. To

derive a common result by all financial managers is near to impossible, thus, this

technique sometimes may produce vague results.

Calculation of WACC depends on capital structure of company and complex capital

structure makes computation of WACC even more difficult.

One of the main limitation is that, WACC is calculated on the basis of expected returns,

and not on past returns. This basis of calculation can be the reason for wrong calculation

also, due to reason of dynamic environment which can bring drastic changes in assumed

returns.

CONCLUSION

It can be elucidated from above report, that the term “Finance” has a very wide coverage

and it has significant processes and activities relating to funds under same umbrella. There are

different methods and techniques available with financial managers to perform calculations for

different things, yet their purpose is same, i.e. to reach to a optimized level of financial

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.