Finance & Operations Assignment

VerifiedAdded on 2021/06/16

|20

|5485

|41

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE & OPERATIONS

Finance & Operations

Name of the Student:

Name of the University:

Authors Note:

Finance & Operations

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE & OPERATIONS

1

Table of Contents

Introduction:...............................................................................................................................2

a) Evaluating the operating and regulatory factor to be considered by the board:....................2

b) Estimating the income and expenditure projections for the first 4 years incorporating and

regulatory cost for the proposal:................................................................................................5

c) Critical evaluation of the financial worth of current proposal and an alternative evaluation

including all cost and revenue deemed appropriate:..................................................................9

d) Detailed and fully evaluated conclusion with clear recommendation is provided to the

board:........................................................................................................................................14

Conclusion:..............................................................................................................................15

Reference and Bibliography:....................................................................................................17

1

Table of Contents

Introduction:...............................................................................................................................2

a) Evaluating the operating and regulatory factor to be considered by the board:....................2

b) Estimating the income and expenditure projections for the first 4 years incorporating and

regulatory cost for the proposal:................................................................................................5

c) Critical evaluation of the financial worth of current proposal and an alternative evaluation

including all cost and revenue deemed appropriate:..................................................................9

d) Detailed and fully evaluated conclusion with clear recommendation is provided to the

board:........................................................................................................................................14

Conclusion:..............................................................................................................................15

Reference and Bibliography:....................................................................................................17

FINANCE & OPERATIONS

2

Introduction:

The overall assessment is mainly conducted to understand the financial performance

of New Life Training Plc, when implementing new proposal for the business. The evaluation

on different levels of cost and income that is incurred by New Life Training Plc is adequately

understood in the statement, which could help in detecting the overall financial performance

of the organisation. In addition, the company current utilises a bespoke training centre, which

provides compulsory franchise training, evening sessions for East London School and Private

lettings of facilities group. Furthermore, the use of investment appraisal techniques is mainly

utilised in identifying the overall financial ability of the current proposal made for New Life

Training Plc. Moreover, relevant evaluation of operational and regularity factors is

conducted, which could help the board to improve operations of the company. Estimating the

income and expenditure projects for the first 4 years, while incorporating the relevant

regulatory cost incurred by the proposal. Additionally, the critical evaluation of financial

worth of current proposal and alternative evaluation is depicted in the assessment. The use of

investment approach techniques such as NPV, ARR, IRR and payback period are conducted

to identify viability of the investment. Lastly, adequate recommendations are provided, which

could help in improving the level of profits from operations that could be generated by New

Life Training Plc.

a) Evaluating the operating and regulatory factor to be considered by the board:

The UK government has relative and regulations that needs to be imposed by the

training centre before commencing their operations. this relevant regulations relatively help

in reducing the excessive burden on centres, while minimising the unethical measures taken

by the businesses (GOV.UK 2018). The overall operating and regulatory factors that needs to

2

Introduction:

The overall assessment is mainly conducted to understand the financial performance

of New Life Training Plc, when implementing new proposal for the business. The evaluation

on different levels of cost and income that is incurred by New Life Training Plc is adequately

understood in the statement, which could help in detecting the overall financial performance

of the organisation. In addition, the company current utilises a bespoke training centre, which

provides compulsory franchise training, evening sessions for East London School and Private

lettings of facilities group. Furthermore, the use of investment appraisal techniques is mainly

utilised in identifying the overall financial ability of the current proposal made for New Life

Training Plc. Moreover, relevant evaluation of operational and regularity factors is

conducted, which could help the board to improve operations of the company. Estimating the

income and expenditure projects for the first 4 years, while incorporating the relevant

regulatory cost incurred by the proposal. Additionally, the critical evaluation of financial

worth of current proposal and alternative evaluation is depicted in the assessment. The use of

investment approach techniques such as NPV, ARR, IRR and payback period are conducted

to identify viability of the investment. Lastly, adequate recommendations are provided, which

could help in improving the level of profits from operations that could be generated by New

Life Training Plc.

a) Evaluating the operating and regulatory factor to be considered by the board:

The UK government has relative and regulations that needs to be imposed by the

training centre before commencing their operations. this relevant regulations relatively help

in reducing the excessive burden on centres, while minimising the unethical measures taken

by the businesses (GOV.UK 2018). The overall operating and regulatory factors that needs to

FINANCE & OPERATIONS

3

be considered by the board before opening the overall bespoke training centre are depicted as

follows.

Bespoke Training Centre needs to have adequate staff for supporting its classes and

teaching sessions.

The training centre also needs to have highly educated tutors to support the level of

training that will be provided to the students our customers.

Adequate level of infrastructure needs to be implemented in the centre to support the level

of activities that is intended by the organisation.

The relevant regulations Such a safety and security need to be maintained by the

organisation before commencing the overall project.

Environmental condition for the training centre:

The overall location of the training centre that is intended to be in East London

relatively indicates the overall competition that will be faced by the organisation in the

location. the training centre would have intense competition from different other competitors

who provide he spoke training services to both the franchise and the students. Furthermore,

the above relevant regulations need to be followed by the overall organisation to effectively

comments their operations and improve the level of profitability that could be generated from

the training centre. Additionally, the evaluation also indicates that there is adequate level of

franchise near the location of East London which could allow the organisation to effectively

improve its profitability. the demand from franchise and students is relatively rising in UK

due to the intense competition in the market. students are willing to take extra lessons to

increase their grades which would eventually help them in long run. On the other hand,

franchise companies are utilising bespoke training centres for training their individuals

employees for improving their productivity (Sun, Liu and Zhou 2017).

3

be considered by the board before opening the overall bespoke training centre are depicted as

follows.

Bespoke Training Centre needs to have adequate staff for supporting its classes and

teaching sessions.

The training centre also needs to have highly educated tutors to support the level of

training that will be provided to the students our customers.

Adequate level of infrastructure needs to be implemented in the centre to support the level

of activities that is intended by the organisation.

The relevant regulations Such a safety and security need to be maintained by the

organisation before commencing the overall project.

Environmental condition for the training centre:

The overall location of the training centre that is intended to be in East London

relatively indicates the overall competition that will be faced by the organisation in the

location. the training centre would have intense competition from different other competitors

who provide he spoke training services to both the franchise and the students. Furthermore,

the above relevant regulations need to be followed by the overall organisation to effectively

comments their operations and improve the level of profitability that could be generated from

the training centre. Additionally, the evaluation also indicates that there is adequate level of

franchise near the location of East London which could allow the organisation to effectively

improve its profitability. the demand from franchise and students is relatively rising in UK

due to the intense competition in the market. students are willing to take extra lessons to

increase their grades which would eventually help them in long run. On the other hand,

franchise companies are utilising bespoke training centres for training their individuals

employees for improving their productivity (Sun, Liu and Zhou 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE & OPERATIONS

4

The evaluation also indicates that there is adequate possibility for the new project to

generate higher rate of returns due to the large customer base in East London. The evaluation

also indicate that Increment and customer base would eventually allow the new project to

conduct adequate sales, which could generate higher revenues from the operations. In

addition, the environmental evaluation also states the possibility of higher competition level

by the organisation, which will directly affect its operational capability (Heald 2015).

Applying operational management theory:

The operational Management Theory can be implemented for improving the level of

profit that could be generated from the new project. the Operation Management Theory

directly focuses on the expenses incurred by the organisation to commence its operations. the

new project a relatively utilizes the tutor fees and other overhead expenses to commenced

business. However, the ignorance of electricity cost and other rental cost would directly have

an impact on future performance of the organisation. The operational Management Theory

relatively focuses on the services that is provided by the new project, which will directly

affect its capability to support different operations. In this context, Bird and Brown (2016)

stated that with the help of operational management theories organisations are able to

evaluate their current expenses on raw materials and reduced their expenses to improve the

profitability.

The operational management accounting theory can only be implemented on the

tutors and cleaning stuff that is maintained by bespoke training centre. The evaluation of the

operation would eventually help in detecting the viability of the expenses incurred by the

project. From the evaluation of the activities it could be understood that during the initial use

the in-hiring process of tutors and administrators and not needed adequately due to the low

activity of sessions conducted by the organisation. Therefore, reduction in number of tutors

4

The evaluation also indicates that there is adequate possibility for the new project to

generate higher rate of returns due to the large customer base in East London. The evaluation

also indicate that Increment and customer base would eventually allow the new project to

conduct adequate sales, which could generate higher revenues from the operations. In

addition, the environmental evaluation also states the possibility of higher competition level

by the organisation, which will directly affect its operational capability (Heald 2015).

Applying operational management theory:

The operational Management Theory can be implemented for improving the level of

profit that could be generated from the new project. the Operation Management Theory

directly focuses on the expenses incurred by the organisation to commence its operations. the

new project a relatively utilizes the tutor fees and other overhead expenses to commenced

business. However, the ignorance of electricity cost and other rental cost would directly have

an impact on future performance of the organisation. The operational Management Theory

relatively focuses on the services that is provided by the new project, which will directly

affect its capability to support different operations. In this context, Bird and Brown (2016)

stated that with the help of operational management theories organisations are able to

evaluate their current expenses on raw materials and reduced their expenses to improve the

profitability.

The operational management accounting theory can only be implemented on the

tutors and cleaning stuff that is maintained by bespoke training centre. The evaluation of the

operation would eventually help in detecting the viability of the expenses incurred by the

project. From the evaluation of the activities it could be understood that during the initial use

the in-hiring process of tutors and administrators and not needed adequately due to the low

activity of sessions conducted by the organisation. Therefore, reduction in number of tutors

FINANCE & OPERATIONS

5

would be beneficial for the company. However, the increment and sessions could be seen

from 2nd year of the operation, therefore adequate addition to the tutors and administration

needs to be conducted by the organisation. Hence, applying the operational management

theory could eventually help the company to maximize the profit and minimise any kind of

expenses on operations of the new project

b) Estimating the income and expenditure projections for the first 4 years incorporating

and regulatory cost for the proposal:

There is different level of finance source, which could be used by New Life Training

Plc for financing the proposal for opening bespoke training centre. In addition, choosing the

relevant sources of finance is essential for the company, as helps in minimising the overall

finance cost and maximises its profitability. Abbasi and Abbasi (2017) stated that with the

identification of adequate finance source organisations able to determine whether to accept

the proposal or rejected due to the lack of adequate capital. On the other hand, Ismai et al.

(2018) argued that the results obtained from investment appraisal techniques could be wrong

due to the wrong assumption of revenues, expenses, and discounting factor of the proposed

project. New Life Training Plc can evaluate the following sources of finance for supporting

the expenses of their new project.

External Source of Finance:

Mortgage:

The use of mortgages could be helpful for the organization to acquire the required

level of funds from external sources to support its new project. this fund acquiring would

eventually consist of interest payments which is a relatively lower due to the mortgaging of

5

would be beneficial for the company. However, the increment and sessions could be seen

from 2nd year of the operation, therefore adequate addition to the tutors and administration

needs to be conducted by the organisation. Hence, applying the operational management

theory could eventually help the company to maximize the profit and minimise any kind of

expenses on operations of the new project

b) Estimating the income and expenditure projections for the first 4 years incorporating

and regulatory cost for the proposal:

There is different level of finance source, which could be used by New Life Training

Plc for financing the proposal for opening bespoke training centre. In addition, choosing the

relevant sources of finance is essential for the company, as helps in minimising the overall

finance cost and maximises its profitability. Abbasi and Abbasi (2017) stated that with the

identification of adequate finance source organisations able to determine whether to accept

the proposal or rejected due to the lack of adequate capital. On the other hand, Ismai et al.

(2018) argued that the results obtained from investment appraisal techniques could be wrong

due to the wrong assumption of revenues, expenses, and discounting factor of the proposed

project. New Life Training Plc can evaluate the following sources of finance for supporting

the expenses of their new project.

External Source of Finance:

Mortgage:

The use of mortgages could be helpful for the organization to acquire the required

level of funds from external sources to support its new project. this fund acquiring would

eventually consist of interest payments which is a relatively lower due to the mortgaging of

FINANCE & OPERATIONS

6

lands by the organization. This source of fund could only be acquired if the value of land is

adequate and consistent with amount of the loan.

Share Issue:

The second method that could be used by the organisation is issuing shares, which is

relatively helpful in generating the required level of funds to support its business idea.

However, the extensive issue of shares would eventually increase its supply in the market,

while demands remains the same, which relevantly hampers its share price valuation (Su and

Lu 2015).

Bank Long-term Loan:

The last external source of finance that could be used by the organisation is Bank long

term loans, which relatively provides the lowest finance caused due to the longevity of the

loan period. Bank long term loans are relatively provided to organisations which have

adequately portrayed a positive financial balance over the fiscal years and achievable to

support the finance cost incurred from the loan process. Bank loan are provided with a fixed

interest rate which relatively reduces the net profits of the organisation.

Internal Source of Finance:

Sales of existing assets:

The second internal source of finance could be from the sale of existing assets, which

might allow the company to acquire the required funds for the investment. The sale of

existing assets would only allow the organization to acquire the funds, which will be

generated from the current value of the assets. However, the asset selling procedure is not

viable for an organization, as it would reduce its total assets capacity and hamper its

operational viability (Bangemann 2017).

6

lands by the organization. This source of fund could only be acquired if the value of land is

adequate and consistent with amount of the loan.

Share Issue:

The second method that could be used by the organisation is issuing shares, which is

relatively helpful in generating the required level of funds to support its business idea.

However, the extensive issue of shares would eventually increase its supply in the market,

while demands remains the same, which relevantly hampers its share price valuation (Su and

Lu 2015).

Bank Long-term Loan:

The last external source of finance that could be used by the organisation is Bank long

term loans, which relatively provides the lowest finance caused due to the longevity of the

loan period. Bank long term loans are relatively provided to organisations which have

adequately portrayed a positive financial balance over the fiscal years and achievable to

support the finance cost incurred from the loan process. Bank loan are provided with a fixed

interest rate which relatively reduces the net profits of the organisation.

Internal Source of Finance:

Sales of existing assets:

The second internal source of finance could be from the sale of existing assets, which

might allow the company to acquire the required funds for the investment. The sale of

existing assets would only allow the organization to acquire the funds, which will be

generated from the current value of the assets. However, the asset selling procedure is not

viable for an organization, as it would reduce its total assets capacity and hamper its

operational viability (Bangemann 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE & OPERATIONS

7

Retained profits:

The major internal source that could be used by the organisation is retained profit,

which is accumulated throughout the years for investing in new business opportunities. The

use of retained earnings would eventually help the organization to nullify the finance cost, as

the company’s cash balance will finance the whole investment amount. However, the retained

income of an organisation is never high, due to the extensive dividend and market condition

of the organisation. Nevertheless, after the evaluation of New Life Training PLC current

retained earnings it could be identified that the company has adequate cash balance to support

the proposal, which could help in increasing net income of the organisation (Vlcek 2018).

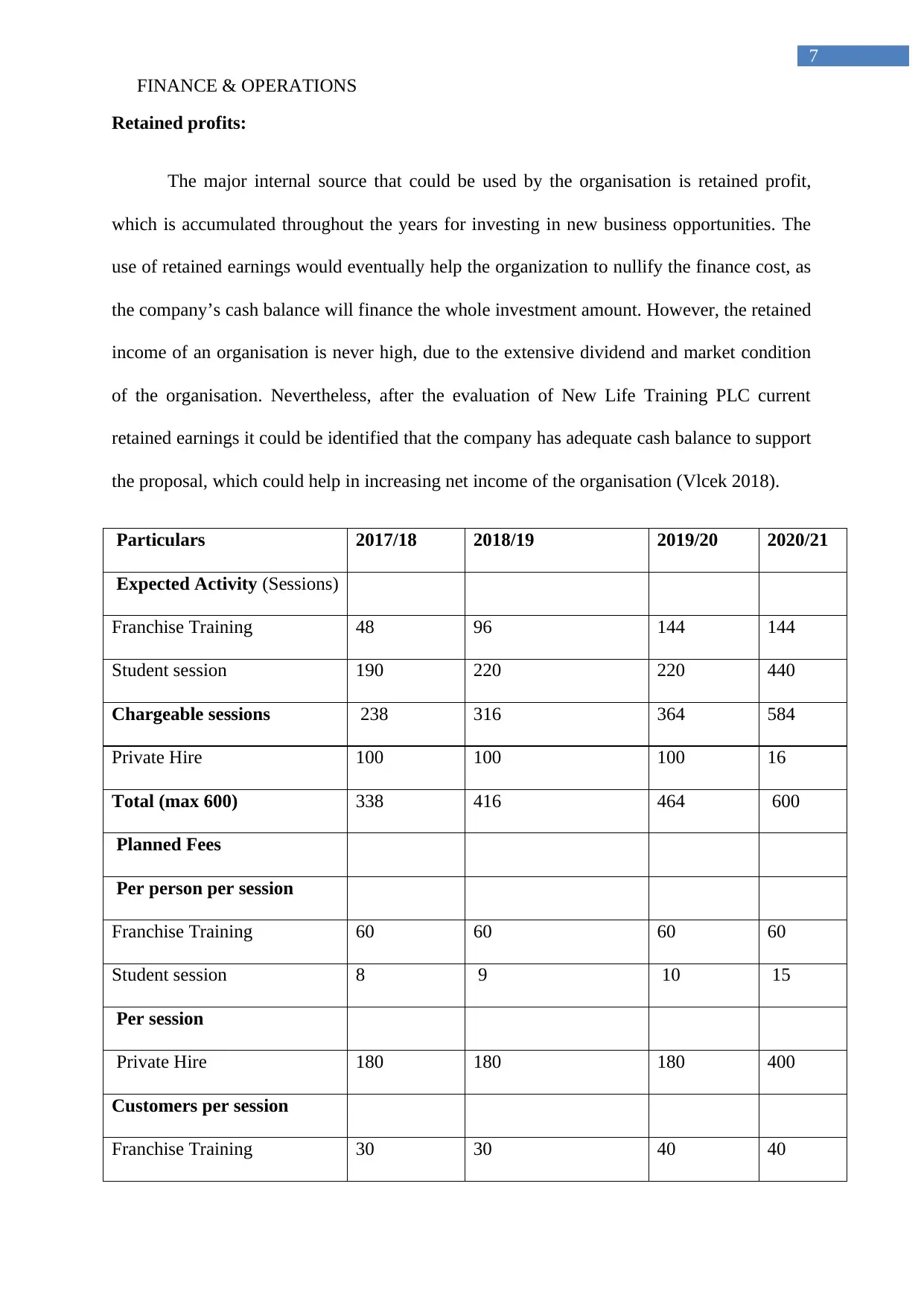

Particulars 2017/18 2018/19 2019/20 2020/21

Expected Activity (Sessions)

Franchise Training 48 96 144 144

Student session 190 220 220 440

Chargeable sessions 238 316 364 584

Private Hire 100 100 100 16

Total (max 600) 338 416 464 600

Planned Fees

Per person per session

Franchise Training 60 60 60 60

Student session 8 9 10 15

Per session

Private Hire 180 180 180 400

Customers per session

Franchise Training 30 30 40 40

7

Retained profits:

The major internal source that could be used by the organisation is retained profit,

which is accumulated throughout the years for investing in new business opportunities. The

use of retained earnings would eventually help the organization to nullify the finance cost, as

the company’s cash balance will finance the whole investment amount. However, the retained

income of an organisation is never high, due to the extensive dividend and market condition

of the organisation. Nevertheless, after the evaluation of New Life Training PLC current

retained earnings it could be identified that the company has adequate cash balance to support

the proposal, which could help in increasing net income of the organisation (Vlcek 2018).

Particulars 2017/18 2018/19 2019/20 2020/21

Expected Activity (Sessions)

Franchise Training 48 96 144 144

Student session 190 220 220 440

Chargeable sessions 238 316 364 584

Private Hire 100 100 100 16

Total (max 600) 338 416 464 600

Planned Fees

Per person per session

Franchise Training 60 60 60 60

Student session 8 9 10 15

Per session

Private Hire 180 180 180 400

Customers per session

Franchise Training 30 30 40 40

FINANCE & OPERATIONS

8

Student session 20 20 20 20

From the overall evaluation of above table, income that is generated by the company

could eventually help in generating high level of profits. In addition, the segregation of

different level of activities that will be conducted by the proposed project is mainly provided

adequately. Furthermore, the pricing, number of customers and session that will be conducted

by the new proposed business is adequate, which will provide higher returns from

investment. The anticipation of rising revenue from the operations will eventually help in

supporting the level of profits that could be generated form operations. Changes in current

operations of the business could eventually help in generating high level of profits from

operations, which might help in improving the level of returns from investment. The changes

in expected activity can be conducted by reducing private hire and student session, while

increasing franchise training could eventually help in improving the level of profits from

operations. The increment in overall franchising training could eventually help in generating

high level of returns from investment (Larder, Sippel and Argent 2017).

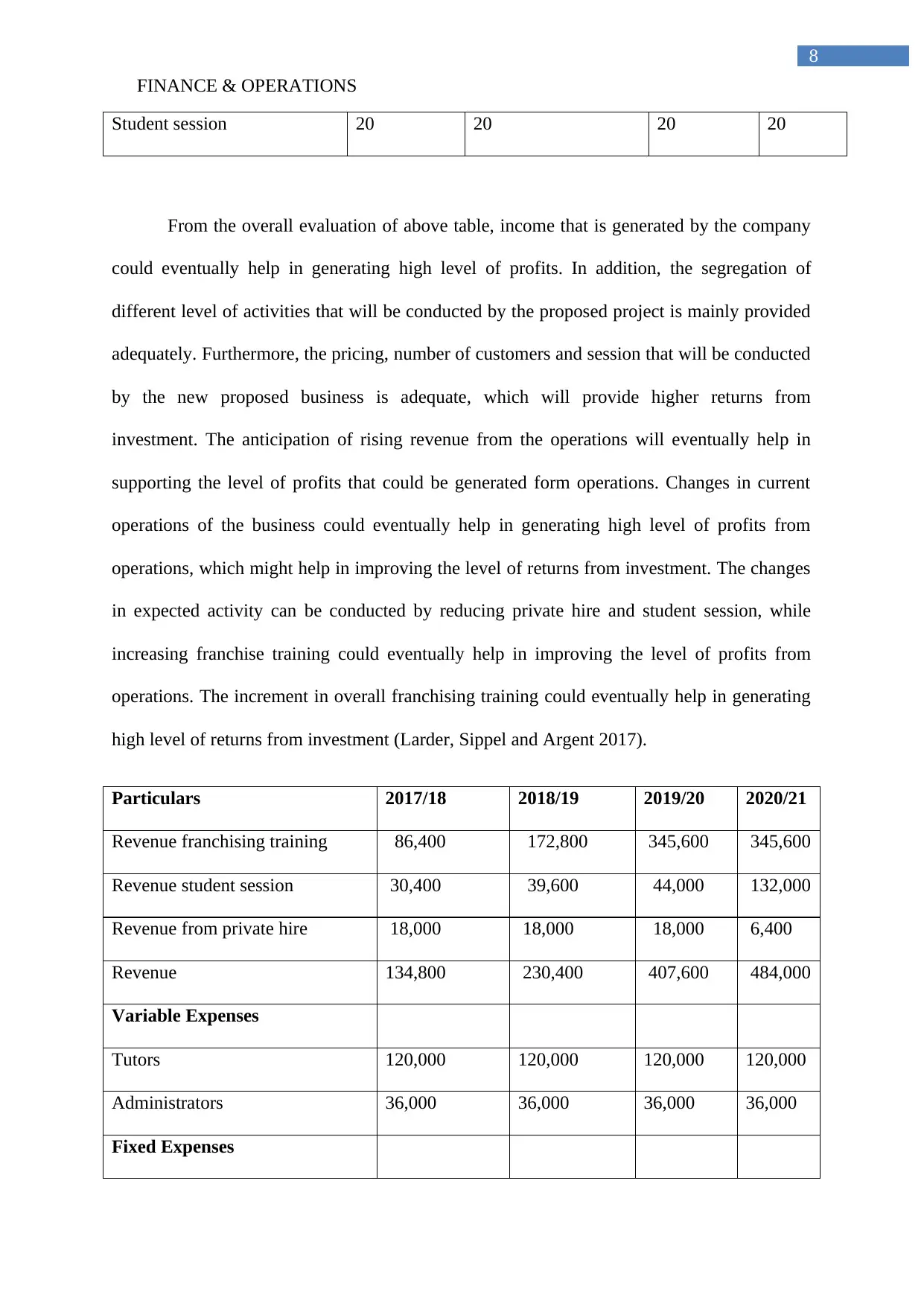

Particulars 2017/18 2018/19 2019/20 2020/21

Revenue franchising training 86,400 172,800 345,600 345,600

Revenue student session 30,400 39,600 44,000 132,000

Revenue from private hire 18,000 18,000 18,000 6,400

Revenue 134,800 230,400 407,600 484,000

Variable Expenses

Tutors 120,000 120,000 120,000 120,000

Administrators 36,000 36,000 36,000 36,000

Fixed Expenses

8

Student session 20 20 20 20

From the overall evaluation of above table, income that is generated by the company

could eventually help in generating high level of profits. In addition, the segregation of

different level of activities that will be conducted by the proposed project is mainly provided

adequately. Furthermore, the pricing, number of customers and session that will be conducted

by the new proposed business is adequate, which will provide higher returns from

investment. The anticipation of rising revenue from the operations will eventually help in

supporting the level of profits that could be generated form operations. Changes in current

operations of the business could eventually help in generating high level of profits from

operations, which might help in improving the level of returns from investment. The changes

in expected activity can be conducted by reducing private hire and student session, while

increasing franchise training could eventually help in improving the level of profits from

operations. The increment in overall franchising training could eventually help in generating

high level of returns from investment (Larder, Sippel and Argent 2017).

Particulars 2017/18 2018/19 2019/20 2020/21

Revenue franchising training 86,400 172,800 345,600 345,600

Revenue student session 30,400 39,600 44,000 132,000

Revenue from private hire 18,000 18,000 18,000 6,400

Revenue 134,800 230,400 407,600 484,000

Variable Expenses

Tutors 120,000 120,000 120,000 120,000

Administrators 36,000 36,000 36,000 36,000

Fixed Expenses

FINANCE & OPERATIONS

9

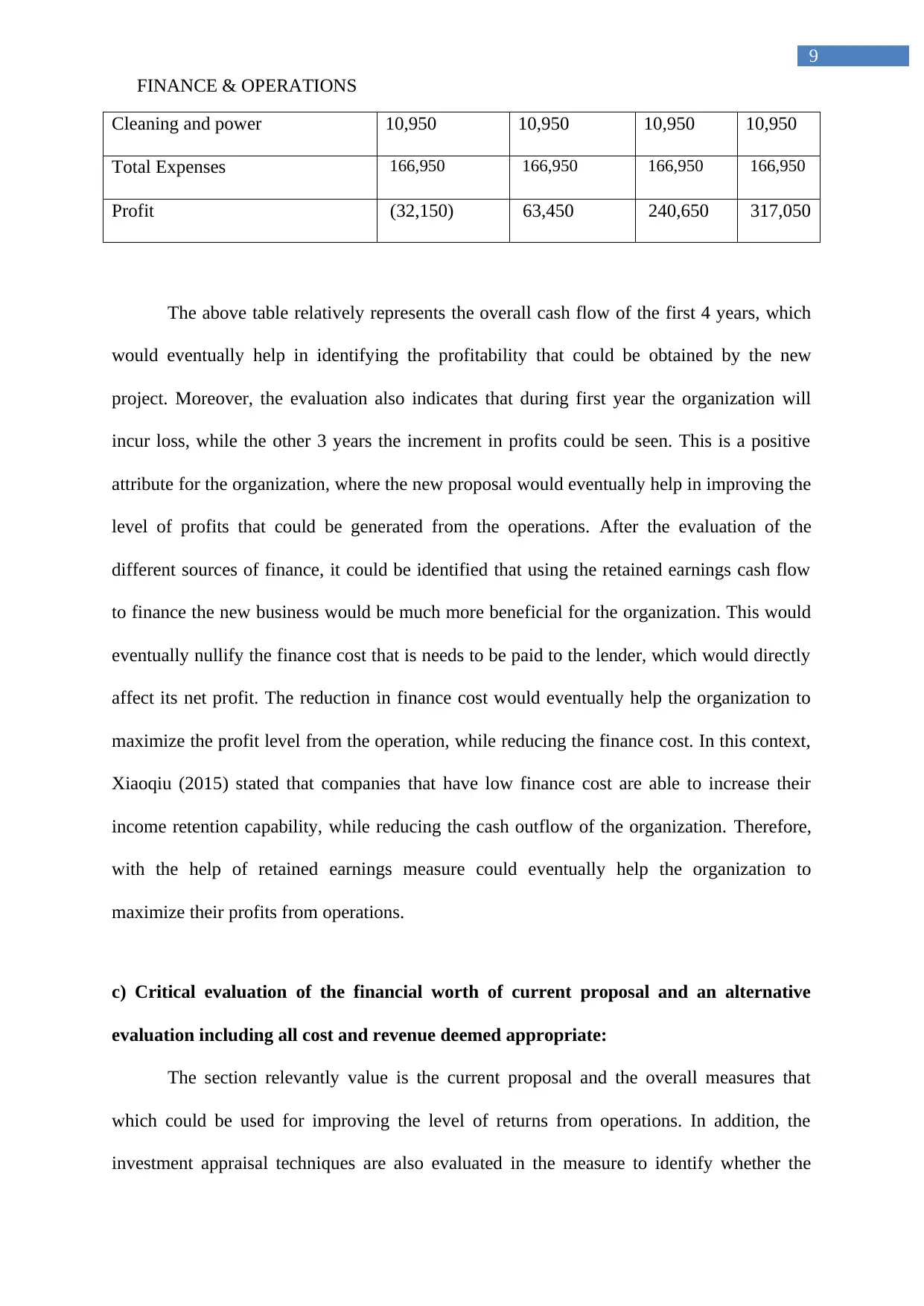

Cleaning and power 10,950 10,950 10,950 10,950

Total Expenses 166,950 166,950 166,950 166,950

Profit (32,150) 63,450 240,650 317,050

The above table relatively represents the overall cash flow of the first 4 years, which

would eventually help in identifying the profitability that could be obtained by the new

project. Moreover, the evaluation also indicates that during first year the organization will

incur loss, while the other 3 years the increment in profits could be seen. This is a positive

attribute for the organization, where the new proposal would eventually help in improving the

level of profits that could be generated from the operations. After the evaluation of the

different sources of finance, it could be identified that using the retained earnings cash flow

to finance the new business would be much more beneficial for the organization. This would

eventually nullify the finance cost that is needs to be paid to the lender, which would directly

affect its net profit. The reduction in finance cost would eventually help the organization to

maximize the profit level from the operation, while reducing the finance cost. In this context,

Xiaoqiu (2015) stated that companies that have low finance cost are able to increase their

income retention capability, while reducing the cash outflow of the organization. Therefore,

with the help of retained earnings measure could eventually help the organization to

maximize their profits from operations.

c) Critical evaluation of the financial worth of current proposal and an alternative

evaluation including all cost and revenue deemed appropriate:

The section relevantly value is the current proposal and the overall measures that

which could be used for improving the level of returns from operations. In addition, the

investment appraisal techniques are also evaluated in the measure to identify whether the

9

Cleaning and power 10,950 10,950 10,950 10,950

Total Expenses 166,950 166,950 166,950 166,950

Profit (32,150) 63,450 240,650 317,050

The above table relatively represents the overall cash flow of the first 4 years, which

would eventually help in identifying the profitability that could be obtained by the new

project. Moreover, the evaluation also indicates that during first year the organization will

incur loss, while the other 3 years the increment in profits could be seen. This is a positive

attribute for the organization, where the new proposal would eventually help in improving the

level of profits that could be generated from the operations. After the evaluation of the

different sources of finance, it could be identified that using the retained earnings cash flow

to finance the new business would be much more beneficial for the organization. This would

eventually nullify the finance cost that is needs to be paid to the lender, which would directly

affect its net profit. The reduction in finance cost would eventually help the organization to

maximize the profit level from the operation, while reducing the finance cost. In this context,

Xiaoqiu (2015) stated that companies that have low finance cost are able to increase their

income retention capability, while reducing the cash outflow of the organization. Therefore,

with the help of retained earnings measure could eventually help the organization to

maximize their profits from operations.

c) Critical evaluation of the financial worth of current proposal and an alternative

evaluation including all cost and revenue deemed appropriate:

The section relevantly value is the current proposal and the overall measures that

which could be used for improving the level of returns from operations. In addition, the

investment appraisal techniques are also evaluated in the measure to identify whether the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE & OPERATIONS

10

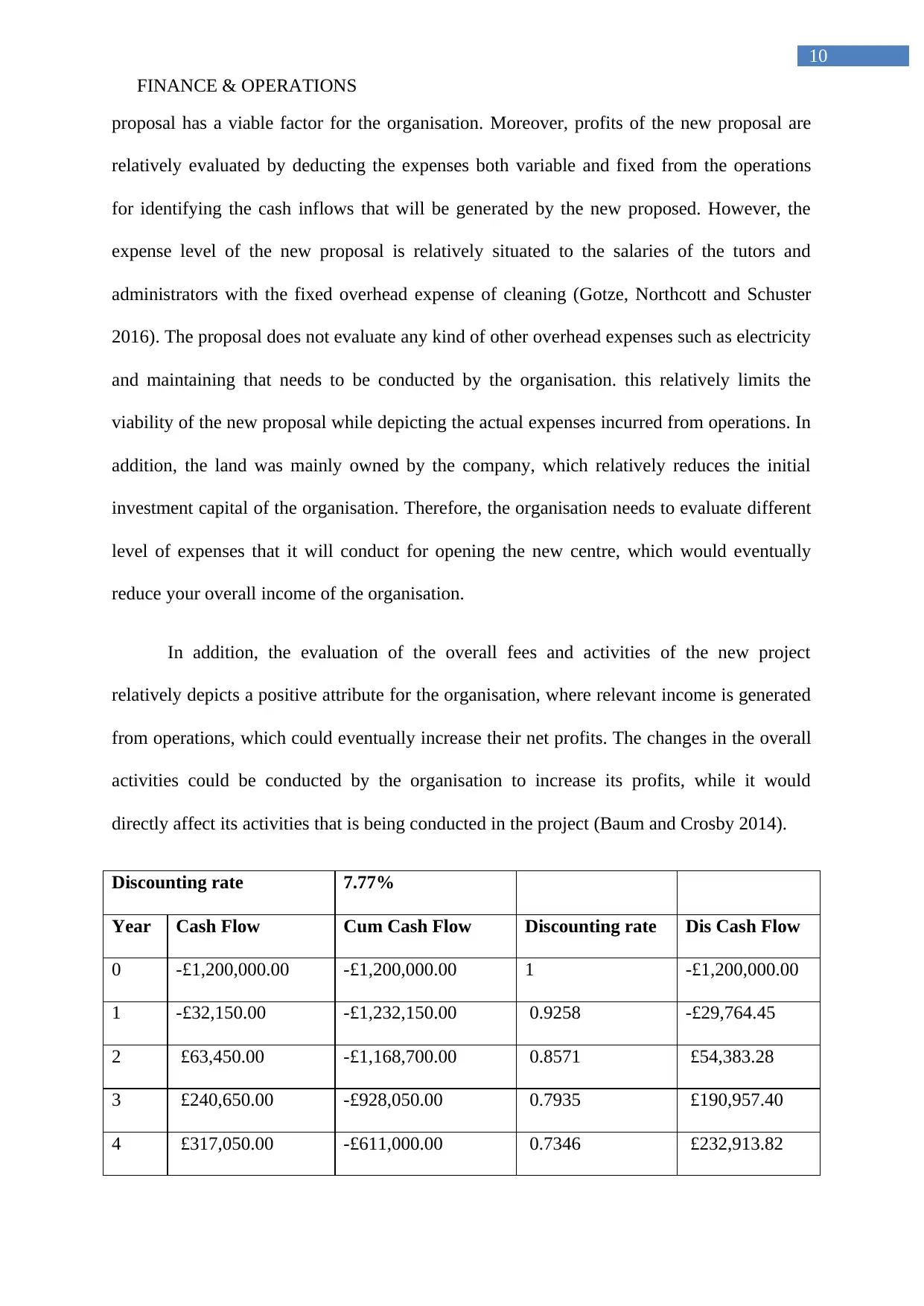

proposal has a viable factor for the organisation. Moreover, profits of the new proposal are

relatively evaluated by deducting the expenses both variable and fixed from the operations

for identifying the cash inflows that will be generated by the new proposed. However, the

expense level of the new proposal is relatively situated to the salaries of the tutors and

administrators with the fixed overhead expense of cleaning (Gotze, Northcott and Schuster

2016). The proposal does not evaluate any kind of other overhead expenses such as electricity

and maintaining that needs to be conducted by the organisation. this relatively limits the

viability of the new proposal while depicting the actual expenses incurred from operations. In

addition, the land was mainly owned by the company, which relatively reduces the initial

investment capital of the organisation. Therefore, the organisation needs to evaluate different

level of expenses that it will conduct for opening the new centre, which would eventually

reduce your overall income of the organisation.

In addition, the evaluation of the overall fees and activities of the new project

relatively depicts a positive attribute for the organisation, where relevant income is generated

from operations, which could eventually increase their net profits. The changes in the overall

activities could be conducted by the organisation to increase its profits, while it would

directly affect its activities that is being conducted in the project (Baum and Crosby 2014).

Discounting rate 7.77%

Year Cash Flow Cum Cash Flow Discounting rate Dis Cash Flow

0 -£1,200,000.00 -£1,200,000.00 1 -£1,200,000.00

1 -£32,150.00 -£1,232,150.00 0.9258 -£29,764.45

2 £63,450.00 -£1,168,700.00 0.8571 £54,383.28

3 £240,650.00 -£928,050.00 0.7935 £190,957.40

4 £317,050.00 -£611,000.00 0.7346 £232,913.82

10

proposal has a viable factor for the organisation. Moreover, profits of the new proposal are

relatively evaluated by deducting the expenses both variable and fixed from the operations

for identifying the cash inflows that will be generated by the new proposed. However, the

expense level of the new proposal is relatively situated to the salaries of the tutors and

administrators with the fixed overhead expense of cleaning (Gotze, Northcott and Schuster

2016). The proposal does not evaluate any kind of other overhead expenses such as electricity

and maintaining that needs to be conducted by the organisation. this relatively limits the

viability of the new proposal while depicting the actual expenses incurred from operations. In

addition, the land was mainly owned by the company, which relatively reduces the initial

investment capital of the organisation. Therefore, the organisation needs to evaluate different

level of expenses that it will conduct for opening the new centre, which would eventually

reduce your overall income of the organisation.

In addition, the evaluation of the overall fees and activities of the new project

relatively depicts a positive attribute for the organisation, where relevant income is generated

from operations, which could eventually increase their net profits. The changes in the overall

activities could be conducted by the organisation to increase its profits, while it would

directly affect its activities that is being conducted in the project (Baum and Crosby 2014).

Discounting rate 7.77%

Year Cash Flow Cum Cash Flow Discounting rate Dis Cash Flow

0 -£1,200,000.00 -£1,200,000.00 1 -£1,200,000.00

1 -£32,150.00 -£1,232,150.00 0.9258 -£29,764.45

2 £63,450.00 -£1,168,700.00 0.8571 £54,383.28

3 £240,650.00 -£928,050.00 0.7935 £190,957.40

4 £317,050.00 -£611,000.00 0.7346 £232,913.82

FINANCE & OPERATIONS

11

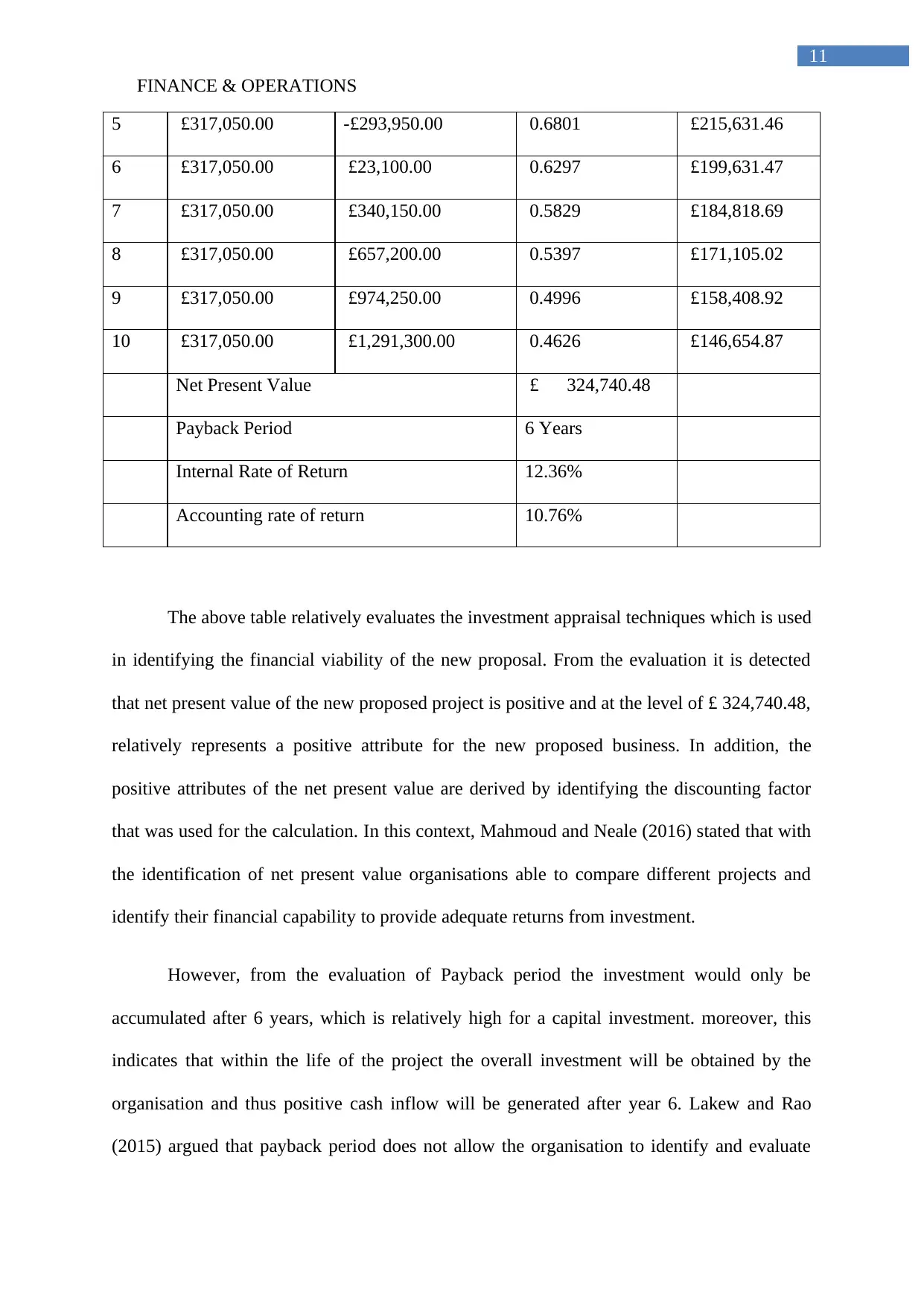

5 £317,050.00 -£293,950.00 0.6801 £215,631.46

6 £317,050.00 £23,100.00 0.6297 £199,631.47

7 £317,050.00 £340,150.00 0.5829 £184,818.69

8 £317,050.00 £657,200.00 0.5397 £171,105.02

9 £317,050.00 £974,250.00 0.4996 £158,408.92

10 £317,050.00 £1,291,300.00 0.4626 £146,654.87

Net Present Value £ 324,740.48

Payback Period 6 Years

Internal Rate of Return 12.36%

Accounting rate of return 10.76%

The above table relatively evaluates the investment appraisal techniques which is used

in identifying the financial viability of the new proposal. From the evaluation it is detected

that net present value of the new proposed project is positive and at the level of £ 324,740.48,

relatively represents a positive attribute for the new proposed business. In addition, the

positive attributes of the net present value are derived by identifying the discounting factor

that was used for the calculation. In this context, Mahmoud and Neale (2016) stated that with

the identification of net present value organisations able to compare different projects and

identify their financial capability to provide adequate returns from investment.

However, from the evaluation of Payback period the investment would only be

accumulated after 6 years, which is relatively high for a capital investment. moreover, this

indicates that within the life of the project the overall investment will be obtained by the

organisation and thus positive cash inflow will be generated after year 6. Lakew and Rao

(2015) argued that payback period does not allow the organisation to identify and evaluate

11

5 £317,050.00 -£293,950.00 0.6801 £215,631.46

6 £317,050.00 £23,100.00 0.6297 £199,631.47

7 £317,050.00 £340,150.00 0.5829 £184,818.69

8 £317,050.00 £657,200.00 0.5397 £171,105.02

9 £317,050.00 £974,250.00 0.4996 £158,408.92

10 £317,050.00 £1,291,300.00 0.4626 £146,654.87

Net Present Value £ 324,740.48

Payback Period 6 Years

Internal Rate of Return 12.36%

Accounting rate of return 10.76%

The above table relatively evaluates the investment appraisal techniques which is used

in identifying the financial viability of the new proposal. From the evaluation it is detected

that net present value of the new proposed project is positive and at the level of £ 324,740.48,

relatively represents a positive attribute for the new proposed business. In addition, the

positive attributes of the net present value are derived by identifying the discounting factor

that was used for the calculation. In this context, Mahmoud and Neale (2016) stated that with

the identification of net present value organisations able to compare different projects and

identify their financial capability to provide adequate returns from investment.

However, from the evaluation of Payback period the investment would only be

accumulated after 6 years, which is relatively high for a capital investment. moreover, this

indicates that within the life of the project the overall investment will be obtained by the

organisation and thus positive cash inflow will be generated after year 6. Lakew and Rao

(2015) argued that payback period does not allow the organisation to identify and evaluate

FINANCE & OPERATIONS

12

cash inflows based on time value, which are relatively reduces the viability of the investment

appraisal technique. nevertheless, for the evaluation and illustrating purposes payback period

can be used to portray the minimum time needed by the project to return the invested amount

of the company.

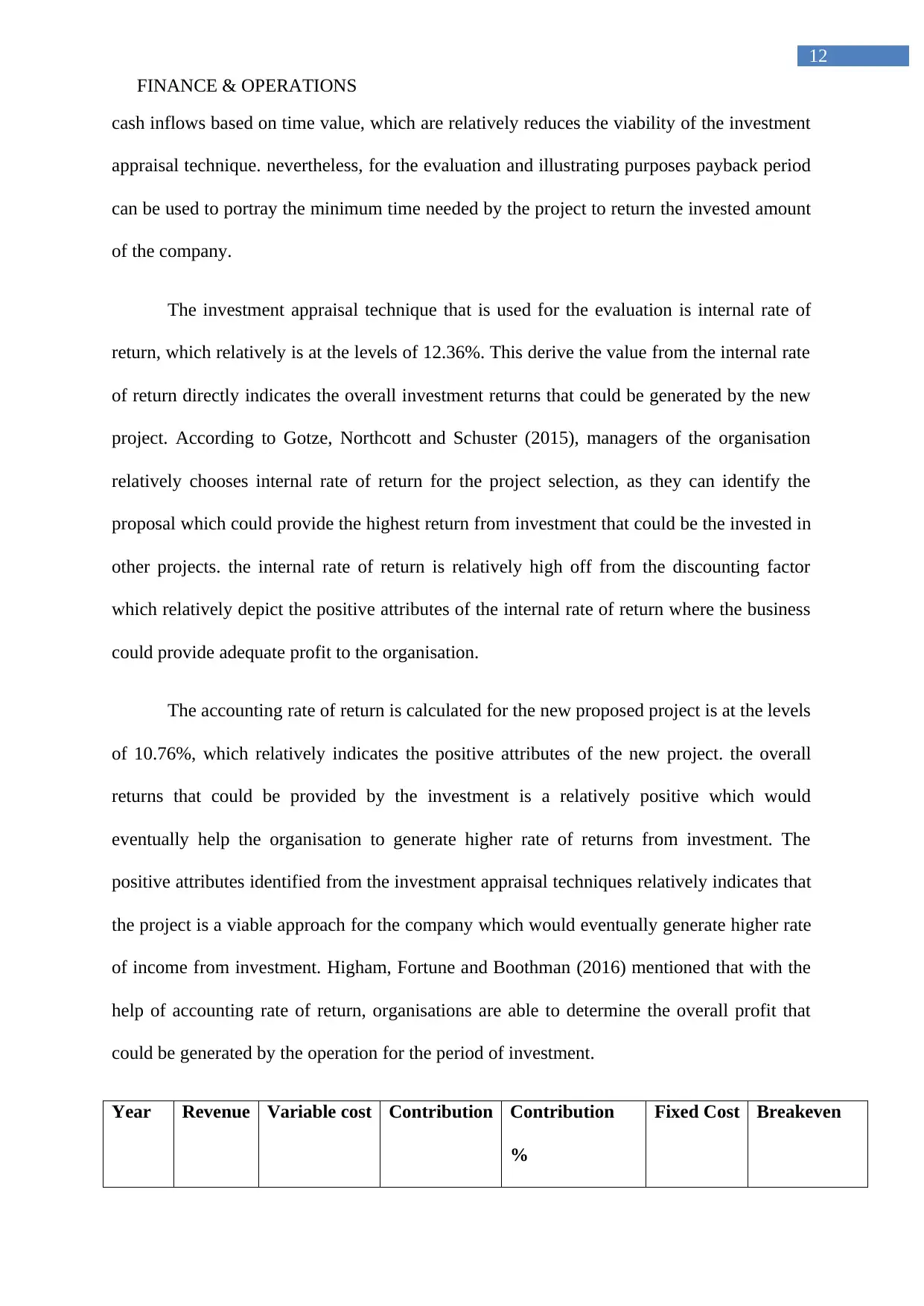

The investment appraisal technique that is used for the evaluation is internal rate of

return, which relatively is at the levels of 12.36%. This derive the value from the internal rate

of return directly indicates the overall investment returns that could be generated by the new

project. According to Gotze, Northcott and Schuster (2015), managers of the organisation

relatively chooses internal rate of return for the project selection, as they can identify the

proposal which could provide the highest return from investment that could be the invested in

other projects. the internal rate of return is relatively high off from the discounting factor

which relatively depict the positive attributes of the internal rate of return where the business

could provide adequate profit to the organisation.

The accounting rate of return is calculated for the new proposed project is at the levels

of 10.76%, which relatively indicates the positive attributes of the new project. the overall

returns that could be provided by the investment is a relatively positive which would

eventually help the organisation to generate higher rate of returns from investment. The

positive attributes identified from the investment appraisal techniques relatively indicates that

the project is a viable approach for the company which would eventually generate higher rate

of income from investment. Higham, Fortune and Boothman (2016) mentioned that with the

help of accounting rate of return, organisations are able to determine the overall profit that

could be generated by the operation for the period of investment.

Year Revenue Variable cost Contribution Contribution

%

Fixed Cost Breakeven

12

cash inflows based on time value, which are relatively reduces the viability of the investment

appraisal technique. nevertheless, for the evaluation and illustrating purposes payback period

can be used to portray the minimum time needed by the project to return the invested amount

of the company.

The investment appraisal technique that is used for the evaluation is internal rate of

return, which relatively is at the levels of 12.36%. This derive the value from the internal rate

of return directly indicates the overall investment returns that could be generated by the new

project. According to Gotze, Northcott and Schuster (2015), managers of the organisation

relatively chooses internal rate of return for the project selection, as they can identify the

proposal which could provide the highest return from investment that could be the invested in

other projects. the internal rate of return is relatively high off from the discounting factor

which relatively depict the positive attributes of the internal rate of return where the business

could provide adequate profit to the organisation.

The accounting rate of return is calculated for the new proposed project is at the levels

of 10.76%, which relatively indicates the positive attributes of the new project. the overall

returns that could be provided by the investment is a relatively positive which would

eventually help the organisation to generate higher rate of returns from investment. The

positive attributes identified from the investment appraisal techniques relatively indicates that

the project is a viable approach for the company which would eventually generate higher rate

of income from investment. Higham, Fortune and Boothman (2016) mentioned that with the

help of accounting rate of return, organisations are able to determine the overall profit that

could be generated by the operation for the period of investment.

Year Revenue Variable cost Contribution Contribution

%

Fixed Cost Breakeven

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE & OPERATIONS

13

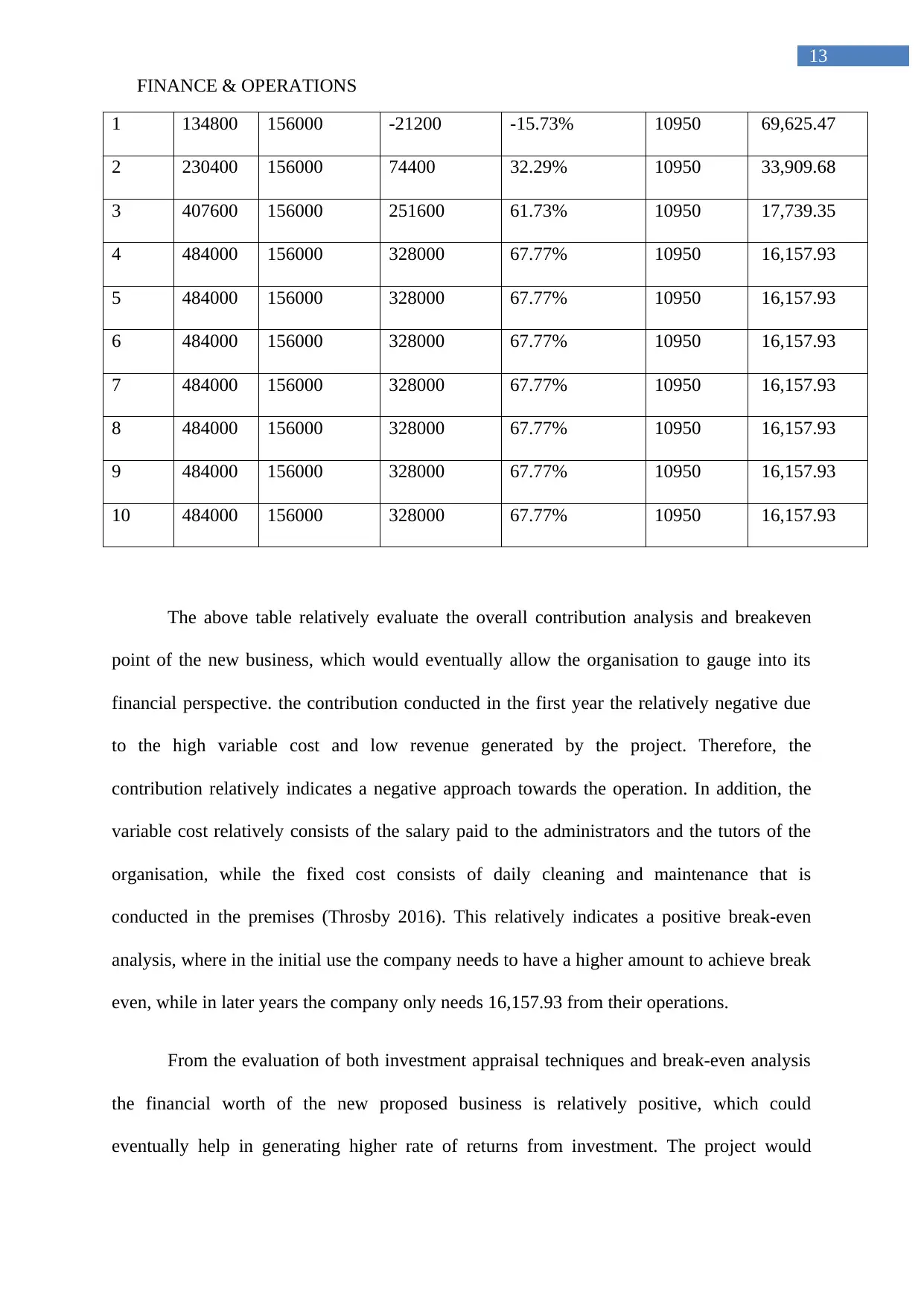

1 134800 156000 -21200 -15.73% 10950 69,625.47

2 230400 156000 74400 32.29% 10950 33,909.68

3 407600 156000 251600 61.73% 10950 17,739.35

4 484000 156000 328000 67.77% 10950 16,157.93

5 484000 156000 328000 67.77% 10950 16,157.93

6 484000 156000 328000 67.77% 10950 16,157.93

7 484000 156000 328000 67.77% 10950 16,157.93

8 484000 156000 328000 67.77% 10950 16,157.93

9 484000 156000 328000 67.77% 10950 16,157.93

10 484000 156000 328000 67.77% 10950 16,157.93

The above table relatively evaluate the overall contribution analysis and breakeven

point of the new business, which would eventually allow the organisation to gauge into its

financial perspective. the contribution conducted in the first year the relatively negative due

to the high variable cost and low revenue generated by the project. Therefore, the

contribution relatively indicates a negative approach towards the operation. In addition, the

variable cost relatively consists of the salary paid to the administrators and the tutors of the

organisation, while the fixed cost consists of daily cleaning and maintenance that is

conducted in the premises (Throsby 2016). This relatively indicates a positive break-even

analysis, where in the initial use the company needs to have a higher amount to achieve break

even, while in later years the company only needs 16,157.93 from their operations.

From the evaluation of both investment appraisal techniques and break-even analysis

the financial worth of the new proposed business is relatively positive, which could

eventually help in generating higher rate of returns from investment. The project would

13

1 134800 156000 -21200 -15.73% 10950 69,625.47

2 230400 156000 74400 32.29% 10950 33,909.68

3 407600 156000 251600 61.73% 10950 17,739.35

4 484000 156000 328000 67.77% 10950 16,157.93

5 484000 156000 328000 67.77% 10950 16,157.93

6 484000 156000 328000 67.77% 10950 16,157.93

7 484000 156000 328000 67.77% 10950 16,157.93

8 484000 156000 328000 67.77% 10950 16,157.93

9 484000 156000 328000 67.77% 10950 16,157.93

10 484000 156000 328000 67.77% 10950 16,157.93

The above table relatively evaluate the overall contribution analysis and breakeven

point of the new business, which would eventually allow the organisation to gauge into its

financial perspective. the contribution conducted in the first year the relatively negative due

to the high variable cost and low revenue generated by the project. Therefore, the

contribution relatively indicates a negative approach towards the operation. In addition, the

variable cost relatively consists of the salary paid to the administrators and the tutors of the

organisation, while the fixed cost consists of daily cleaning and maintenance that is

conducted in the premises (Throsby 2016). This relatively indicates a positive break-even

analysis, where in the initial use the company needs to have a higher amount to achieve break

even, while in later years the company only needs 16,157.93 from their operations.

From the evaluation of both investment appraisal techniques and break-even analysis

the financial worth of the new proposed business is relatively positive, which could

eventually help in generating higher rate of returns from investment. The project would

FINANCE & OPERATIONS

14

provide a higher cash inflow to the organisation, which food increase the firm value in future.

The alternative cash inflow is relatively not needed for the new proposed business, as the

overall investment amount was used by the detailed income which does not have any kind of

Finance cost. moreover, the building was prepared for the land of the organisation, which

reduces the purchasing price of the land. therefore, it could be understood that there is no

alternative cost incurred by the organisation to commence the new business (Laird and

Venables 2017).

d) Detailed and fully evaluated conclusion with clear recommendation is provided to the

board:

From the evaluation of all the relevant financial and regulatory perspective the

investments that will be conducted in the new proposed business is Deemed to be viable. The

New Life Training PLC would eventually improve their profitability by opening the Bespoke

Training Centre, which will relatively have a positive cash inflow for the organisation. The

evaluation also indicated that implementation of the new bespoke Training Centre would

eventually allow the organisation to improve its future profits, while increasing the overall

firm value. Furthermore, after revaluation of all the relevant sources of finance it could be

identified that using retained income for the purpose of Financing the project would be much

beneficial for organisation. the company relevantly has adequate retained income to support

the expenditure on the particular project which would eventually help in minimising the

overall finance cost which will income by New Life Training PLC. therefore, selection of the

retained income for commencing the project is an adequate measurement which could

eventually allow the organisation to maximize its profitability in long run. Furthermore,

adequate regulatory Framework needs to be considered by the organisation while

14

provide a higher cash inflow to the organisation, which food increase the firm value in future.

The alternative cash inflow is relatively not needed for the new proposed business, as the

overall investment amount was used by the detailed income which does not have any kind of

Finance cost. moreover, the building was prepared for the land of the organisation, which

reduces the purchasing price of the land. therefore, it could be understood that there is no

alternative cost incurred by the organisation to commence the new business (Laird and

Venables 2017).

d) Detailed and fully evaluated conclusion with clear recommendation is provided to the

board:

From the evaluation of all the relevant financial and regulatory perspective the

investments that will be conducted in the new proposed business is Deemed to be viable. The

New Life Training PLC would eventually improve their profitability by opening the Bespoke

Training Centre, which will relatively have a positive cash inflow for the organisation. The

evaluation also indicated that implementation of the new bespoke Training Centre would

eventually allow the organisation to improve its future profits, while increasing the overall

firm value. Furthermore, after revaluation of all the relevant sources of finance it could be

identified that using retained income for the purpose of Financing the project would be much

beneficial for organisation. the company relevantly has adequate retained income to support

the expenditure on the particular project which would eventually help in minimising the

overall finance cost which will income by New Life Training PLC. therefore, selection of the

retained income for commencing the project is an adequate measurement which could

eventually allow the organisation to maximize its profitability in long run. Furthermore,

adequate regulatory Framework needs to be considered by the organisation while

FINANCE & OPERATIONS

15

implementing the project. the training Centre needs to follow adequate Regulations that is

laid down by the UK Government for starting the overall project.

The positive attributes of the income that will be generated from the project a

relatively indicates its viability to effectively generate higher rate of return from investments.

The overall investment appraisal techniques such as net present value, payback period,

internal rate of return, and accounting rate of return provides a positive attribute of the new

project. this relatively indicates that according to the investment appraisal technique the

project would provide a higher rate of returns for the company which would eventually

improve its future income. Furthermore, the positive attribute would also help New Life

Training Plc to generate adequate returns from the bespoke training centre. Moreover, the

breakeven analysis also contributes to the positive attributes of river new project, where the

initial stage relatively needed extra income while the later stage provided of lower breakeven

point for the organisation. the minimum of 16,157.93 needs to be obtained by the new project

for getting no profit no loss, which is relatively achievable in the current scenario.

Therefore, it could be assumed that the project is relatively viable and could allow the

organisation to generate higher rate of returns from investment. Hence, the organisation could

effectively utilise the new bespoke Training Centre for increasing its revenue in future and

generate higher rate of returns from investment. The analysis of different regulations, sources

of finance and investment appraisal techniques relatively indicated a positive attribute for the

new business. this mainly indicates that the organisation should continue with the new project

for improving it firm value in near future. However, reduction in relevant expenses and

changes in sessions activities could eventually help the organisation to improve its current

profitability and generate higher rate of returns from investment.

15

implementing the project. the training Centre needs to follow adequate Regulations that is

laid down by the UK Government for starting the overall project.

The positive attributes of the income that will be generated from the project a

relatively indicates its viability to effectively generate higher rate of return from investments.

The overall investment appraisal techniques such as net present value, payback period,

internal rate of return, and accounting rate of return provides a positive attribute of the new

project. this relatively indicates that according to the investment appraisal technique the

project would provide a higher rate of returns for the company which would eventually

improve its future income. Furthermore, the positive attribute would also help New Life

Training Plc to generate adequate returns from the bespoke training centre. Moreover, the

breakeven analysis also contributes to the positive attributes of river new project, where the

initial stage relatively needed extra income while the later stage provided of lower breakeven

point for the organisation. the minimum of 16,157.93 needs to be obtained by the new project

for getting no profit no loss, which is relatively achievable in the current scenario.

Therefore, it could be assumed that the project is relatively viable and could allow the

organisation to generate higher rate of returns from investment. Hence, the organisation could

effectively utilise the new bespoke Training Centre for increasing its revenue in future and

generate higher rate of returns from investment. The analysis of different regulations, sources

of finance and investment appraisal techniques relatively indicated a positive attribute for the

new business. this mainly indicates that the organisation should continue with the new project

for improving it firm value in near future. However, reduction in relevant expenses and

changes in sessions activities could eventually help the organisation to improve its current

profitability and generate higher rate of returns from investment.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE & OPERATIONS

16

Conclusion:

After evaluating the overall financial perspective of the new project with the help of

investment appraisal techniques and break-even analysis it could be identified that the project

is relatively viable. In addition, after evaluating the prospects of the new business the

organisation could generate high rate of returns from investment, while reducing the overall

expenses from operations. The evaluation of both regulatory and operational Framework that

is needed by the organisation is effectively evaluated reassessment, which would eventually

improve the operation is capability of the new project. Furthermore, the evaluation on Cost

and revenue perspective of the new project is conducted, which relatively indicates positive

here for the proposal. However, changes in the revenue section is determined, which could

eventually improve the cash inflow of the organisation. On the other hand, the changes on

expenses also proposed, which would eventually incur by the project while increasing the

cash outflow. However, from the evaluation of all different levels of operations that could be

identified that the project is a viable option for the company is Effectively analyzed in the

assessment. Hence, from the valuation it could be identified that Investments in the new

project would eventually provide fruitful returns for the organization, while improving their

retained income.

16

Conclusion:

After evaluating the overall financial perspective of the new project with the help of

investment appraisal techniques and break-even analysis it could be identified that the project

is relatively viable. In addition, after evaluating the prospects of the new business the

organisation could generate high rate of returns from investment, while reducing the overall

expenses from operations. The evaluation of both regulatory and operational Framework that

is needed by the organisation is effectively evaluated reassessment, which would eventually

improve the operation is capability of the new project. Furthermore, the evaluation on Cost

and revenue perspective of the new project is conducted, which relatively indicates positive

here for the proposal. However, changes in the revenue section is determined, which could

eventually improve the cash inflow of the organisation. On the other hand, the changes on

expenses also proposed, which would eventually incur by the project while increasing the

cash outflow. However, from the evaluation of all different levels of operations that could be

identified that the project is a viable option for the company is Effectively analyzed in the

assessment. Hence, from the valuation it could be identified that Investments in the new

project would eventually provide fruitful returns for the organization, while improving their

retained income.

FINANCE & OPERATIONS

17

Reference and Bibliography:

Abbasi, W.A. and Abbasi, Z.W.D.A., 2017. Supply Chain Finance: Generation and Growth

of New Financing Approach. Journal of Finance, 5(2), pp.50-57.

Alkaraan, F., 2015. Strategic investment decision-making perspectives. In Advances in

Mergers and Acquisitions (pp. 53-66). Emerald Group Publishing Limited.

Australia, C., 2017. Submission to the Finance and Public Administration References

Committee Inquiry on the operation, effectiveness, and consequences of the Public

Governance, Performance and Accountability (Location of Corporate Commonwealth

Entities) Order 2016.

Bangemann, T.O., 2017. Definition of shared services. In Shared Services in Finance and

Accounting (pp. 28-32). Routledge.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Bird, N. and Brown, J., 2016. International climate finance: Principles for European support

to developing countries. European Development Co-operation to 2020 Working paper No. 6.

Bonn: European Association of Development Research and Training Institutes (EADI).

Business.hsbc.co.uk. (2018). Small Business Loan: Business Banking: HSBC UK . [online]

Available at: https://www.business.hsbc.co.uk/1/2/business-banking/business-loans-and-

finance/small-business-loan/ [Accessed 8 May 2018].

Clarke, D. and Broby, D., 2017, October. How to foster co-operation between the Scottish

and Irish Asset Management industries: Scottish and Irish finance initiative. In Scottish and

Irish Finance Initiative Conference.

17

Reference and Bibliography:

Abbasi, W.A. and Abbasi, Z.W.D.A., 2017. Supply Chain Finance: Generation and Growth

of New Financing Approach. Journal of Finance, 5(2), pp.50-57.

Alkaraan, F., 2015. Strategic investment decision-making perspectives. In Advances in

Mergers and Acquisitions (pp. 53-66). Emerald Group Publishing Limited.

Australia, C., 2017. Submission to the Finance and Public Administration References

Committee Inquiry on the operation, effectiveness, and consequences of the Public

Governance, Performance and Accountability (Location of Corporate Commonwealth

Entities) Order 2016.

Bangemann, T.O., 2017. Definition of shared services. In Shared Services in Finance and

Accounting (pp. 28-32). Routledge.

Baum, A.E. and Crosby, N., 2014. Property investment appraisal. John Wiley & Sons.

Bird, N. and Brown, J., 2016. International climate finance: Principles for European support

to developing countries. European Development Co-operation to 2020 Working paper No. 6.

Bonn: European Association of Development Research and Training Institutes (EADI).

Business.hsbc.co.uk. (2018). Small Business Loan: Business Banking: HSBC UK . [online]

Available at: https://www.business.hsbc.co.uk/1/2/business-banking/business-loans-and-

finance/small-business-loan/ [Accessed 8 May 2018].

Clarke, D. and Broby, D., 2017, October. How to foster co-operation between the Scottish

and Irish Asset Management industries: Scottish and Irish finance initiative. In Scottish and

Irish Finance Initiative Conference.

FINANCE & OPERATIONS

18

Crosby, N. and Henneberry, J., 2016. Financialisation, the valuation of investment property

and the urban built environment in the UK. Urban Studies, 53(7), pp.1424-1441.

DeBoeuf, D., Lee, H., Johnson, D. and Masharuev, M., 2018. Purchasing power return, a new

paradigm of capital investment appraisal. Managerial Finance, (just-accepted), pp.00-00.

Götze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal (pp. 105-159). Springer, Berlin, Heidelberg.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

GOV.UK. (2018). Rates and allowances: Corporation Tax. [online] Available at:

https://www.gov.uk/government/publications/rates-and-allowances-corporation-tax/rates-

and-allowances-corporation-tax [Accessed 8 May 2018].

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Harris, E.P., Northcott, D., Elmassri, M.M. and Huikku, J., 2016. Theorising strategic

investment decision-making using strong structuration theory. Accounting, Auditing &

Accountability Journal, 29(7), pp.1177-1203.

Heald, D., 2015. Oral Evidence for ‘Review of the Operation of the Barnett Formula’by the

Committee for Finance and Personnel of the Northern Ireland Assembly, 11 February 2015.

Higham, A.P., Fortune, C. and Boothman, J.C., 2016. Sustainability and investment appraisal

for housing regeneration projects. Structural Survey, 34(2), pp.150-167.

Ismail, K., Talib, Y.A., Salleh, N. and Japri, A., 2018. Critical Success Factors in Operation

Phase of Private Finance Initiative (PFI) Projects. International Journal of Academic

Research in Business and Social Sciences, 8(1), pp.878-888.

18

Crosby, N. and Henneberry, J., 2016. Financialisation, the valuation of investment property

and the urban built environment in the UK. Urban Studies, 53(7), pp.1424-1441.

DeBoeuf, D., Lee, H., Johnson, D. and Masharuev, M., 2018. Purchasing power return, a new

paradigm of capital investment appraisal. Managerial Finance, (just-accepted), pp.00-00.

Götze, U., Northcott, D. and Schuster, P., 2015. Selected Further Applications of Investment

Appraisal Methods. In Investment Appraisal (pp. 105-159). Springer, Berlin, Heidelberg.

Gotze, U., Northcott, D. and Schuster, P., 2016. INVESTMENT APPRAISAL. SPRINGER-

VERLAG BERLIN AN.

GOV.UK. (2018). Rates and allowances: Corporation Tax. [online] Available at:

https://www.gov.uk/government/publications/rates-and-allowances-corporation-tax/rates-

and-allowances-corporation-tax [Accessed 8 May 2018].

Harris, E., 2017. Strategic project risk appraisal and management. Routledge.

Harris, E.P., Northcott, D., Elmassri, M.M. and Huikku, J., 2016. Theorising strategic

investment decision-making using strong structuration theory. Accounting, Auditing &

Accountability Journal, 29(7), pp.1177-1203.

Heald, D., 2015. Oral Evidence for ‘Review of the Operation of the Barnett Formula’by the

Committee for Finance and Personnel of the Northern Ireland Assembly, 11 February 2015.

Higham, A.P., Fortune, C. and Boothman, J.C., 2016. Sustainability and investment appraisal

for housing regeneration projects. Structural Survey, 34(2), pp.150-167.

Ismail, K., Talib, Y.A., Salleh, N. and Japri, A., 2018. Critical Success Factors in Operation

Phase of Private Finance Initiative (PFI) Projects. International Journal of Academic

Research in Business and Social Sciences, 8(1), pp.878-888.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE & OPERATIONS

19

Kafuku, J.M., Saman, M.Z.M., Sharif, S. and Zakuan, N., 2015. Investment decision issues

from remanufacturing system perspective: literature review and further research. Procedia

CIRP, 26, pp.589-594.

Khiyon, N.A. and Mohamed, S.F., 2015. Life Cycle Costing Of Mechanical and Electrical

Services for Private Finance Initiatives Projects in Malaysia. International Journal of

Tomography & Simulation™, 28(3), pp.96-103.

Laird, J.J. and Venables, A.J., 2017. Transport investment and economic performance: A

framework for project appraisal. Transport Policy, 56, pp.1-11.

Lakew, D.M. and Rao, D.P., 2015. Financial Appraisal of Long Term Investment Projects:

Evidence from Ethiopia. Asian Journal of Research in Business Economics and

Management, 5(2), pp.1-16.

Larder, N., Sippel, S.R. and Argent, N., 2017. The redefined role of finance in Australian

agriculture. Australian Geographer, pp.1-22.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol, 5(3).

Lu, L. and Li, C., 2017. Delay-induced oscillation phenomenon of a delayed finance model in

enterprise operation. Advances in Difference Equations, 2017(1), p.173.

Mahmoud, O. and Neale, B., 2016. Managerial judgment factors and the real options

approach in the investment appraisal process: evidence from UK automotive

firms. International Journal of Business and Social Science, 7(5), pp.71-84.

Su, Y. and Lu, N., 2015. Simulation of Game Model for Supply Chain Finance Credit Risk

Based on Multi-Agent. Open Journal of Social Sciences, 3(01), p.31.

19

Kafuku, J.M., Saman, M.Z.M., Sharif, S. and Zakuan, N., 2015. Investment decision issues

from remanufacturing system perspective: literature review and further research. Procedia

CIRP, 26, pp.589-594.

Khiyon, N.A. and Mohamed, S.F., 2015. Life Cycle Costing Of Mechanical and Electrical

Services for Private Finance Initiatives Projects in Malaysia. International Journal of

Tomography & Simulation™, 28(3), pp.96-103.

Laird, J.J. and Venables, A.J., 2017. Transport investment and economic performance: A

framework for project appraisal. Transport Policy, 56, pp.1-11.

Lakew, D.M. and Rao, D.P., 2015. Financial Appraisal of Long Term Investment Projects:

Evidence from Ethiopia. Asian Journal of Research in Business Economics and

Management, 5(2), pp.1-16.

Larder, N., Sippel, S.R. and Argent, N., 2017. The redefined role of finance in Australian

agriculture. Australian Geographer, pp.1-22.

Lindvall, N. and Larsson, A., 2017. Investment Appraisal in the Public Sector–Incorporating

Flexibility and Environmental Impact. Journal of Advanced Management Science Vol, 5(3).

Lu, L. and Li, C., 2017. Delay-induced oscillation phenomenon of a delayed finance model in

enterprise operation. Advances in Difference Equations, 2017(1), p.173.

Mahmoud, O. and Neale, B., 2016. Managerial judgment factors and the real options

approach in the investment appraisal process: evidence from UK automotive

firms. International Journal of Business and Social Science, 7(5), pp.71-84.

Su, Y. and Lu, N., 2015. Simulation of Game Model for Supply Chain Finance Credit Risk

Based on Multi-Agent. Open Journal of Social Sciences, 3(01), p.31.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.