Financial Performance Evaluation of DP World and PSA Internationals

VerifiedAdded on 2023/06/10

|14

|3285

|490

AI Summary

This report evaluates the financial performance of DP World and PSA Internationals using key financial ratios such as profitability, solvency, efficiency and capital structure. The report includes the computation of key financial ratios, analysis of the same and cross-sectional analysis with industry averages.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Author’s Note:

Finance

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

FINANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Part 1............................................................................................................................................2

Part 2............................................................................................................................................3

Answer to Question 2......................................................................................................................4

Introduction..................................................................................................................................4

Calculation of Key Financial Ratios............................................................................................5

Analysis of Key Financial Ratios for both Companies...............................................................6

Cross Sectional Analysis of Financial Ratios............................................................................10

Conclusion and Recommendations............................................................................................11

Reference.......................................................................................................................................12

FINANCE

Table of Contents

Answer to Question 1......................................................................................................................2

Part 1............................................................................................................................................2

Part 2............................................................................................................................................3

Answer to Question 2......................................................................................................................4

Introduction..................................................................................................................................4

Calculation of Key Financial Ratios............................................................................................5

Analysis of Key Financial Ratios for both Companies...............................................................6

Cross Sectional Analysis of Financial Ratios............................................................................10

Conclusion and Recommendations............................................................................................11

Reference.......................................................................................................................................12

2

FINANCE

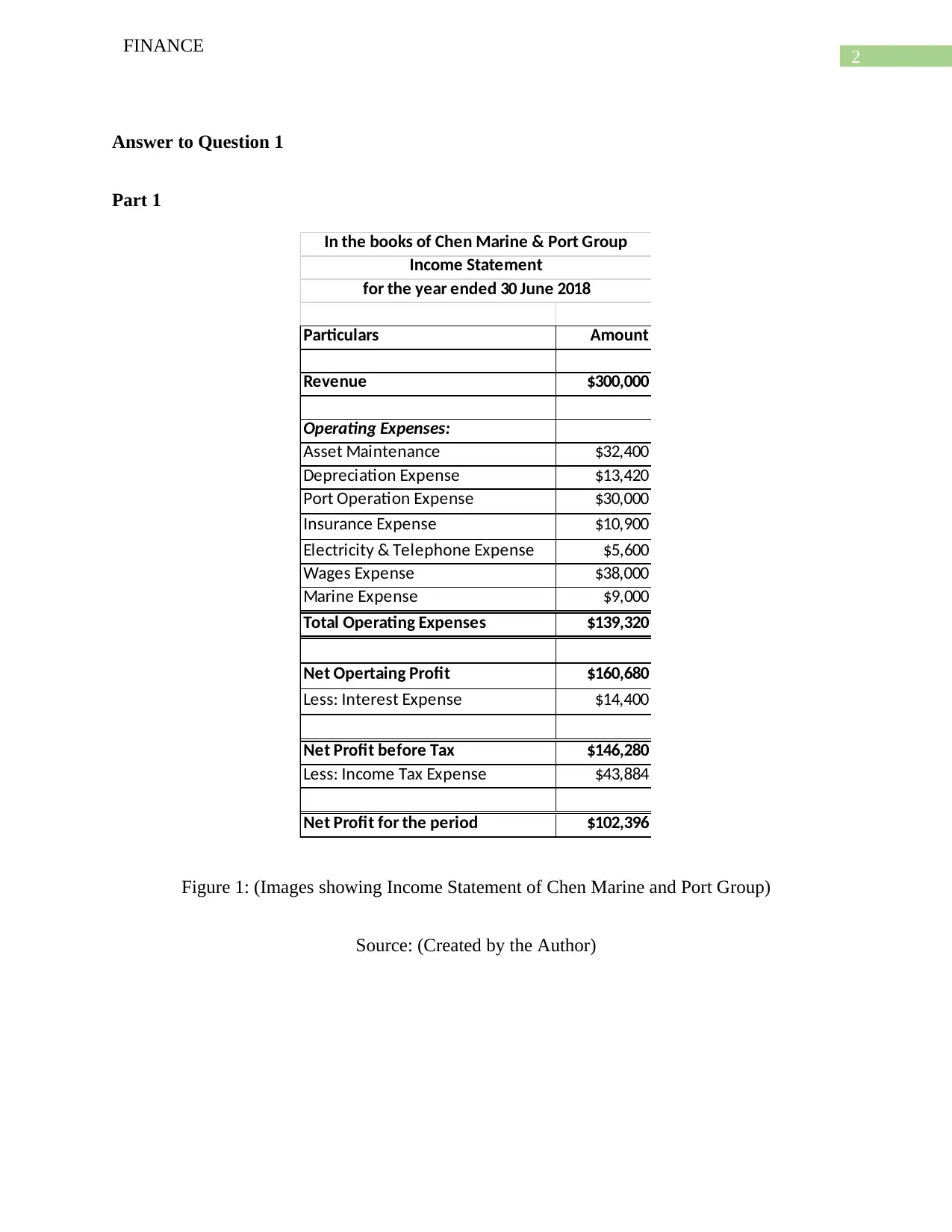

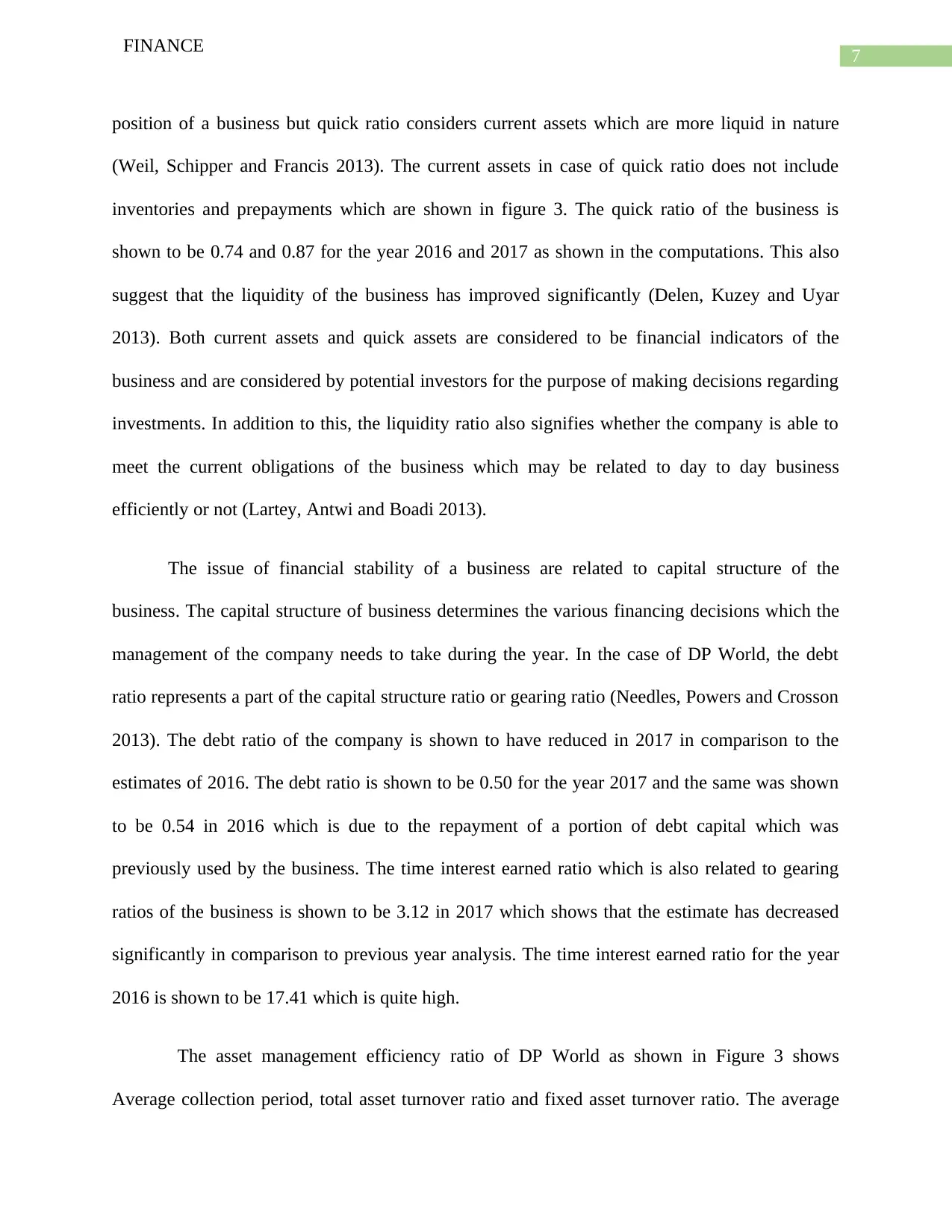

Answer to Question 1

Part 1

Particulars Amount

Revenue $300,000

Operating Expenses:

Asset Maintenance $32,400

Depreciation Expense $13,420

Port Operation Expense $30,000

Insurance Expense $10,900

Electricity & Telephone Expense $5,600

Wages Expense $38,000

Marine Expense $9,000

Total Operating Expenses $139,320

Net Opertaing Profit $160,680

Less: Interest Expense $14,400

Net Profit before Tax $146,280

Less: Income Tax Expense $43,884

Net Profit for the period $102,396

In the books of Chen Marine & Port Group

Income Statement

for the year ended 30 June 2018

Figure 1: (Images showing Income Statement of Chen Marine and Port Group)

Source: (Created by the Author)

FINANCE

Answer to Question 1

Part 1

Particulars Amount

Revenue $300,000

Operating Expenses:

Asset Maintenance $32,400

Depreciation Expense $13,420

Port Operation Expense $30,000

Insurance Expense $10,900

Electricity & Telephone Expense $5,600

Wages Expense $38,000

Marine Expense $9,000

Total Operating Expenses $139,320

Net Opertaing Profit $160,680

Less: Interest Expense $14,400

Net Profit before Tax $146,280

Less: Income Tax Expense $43,884

Net Profit for the period $102,396

In the books of Chen Marine & Port Group

Income Statement

for the year ended 30 June 2018

Figure 1: (Images showing Income Statement of Chen Marine and Port Group)

Source: (Created by the Author)

3

FINANCE

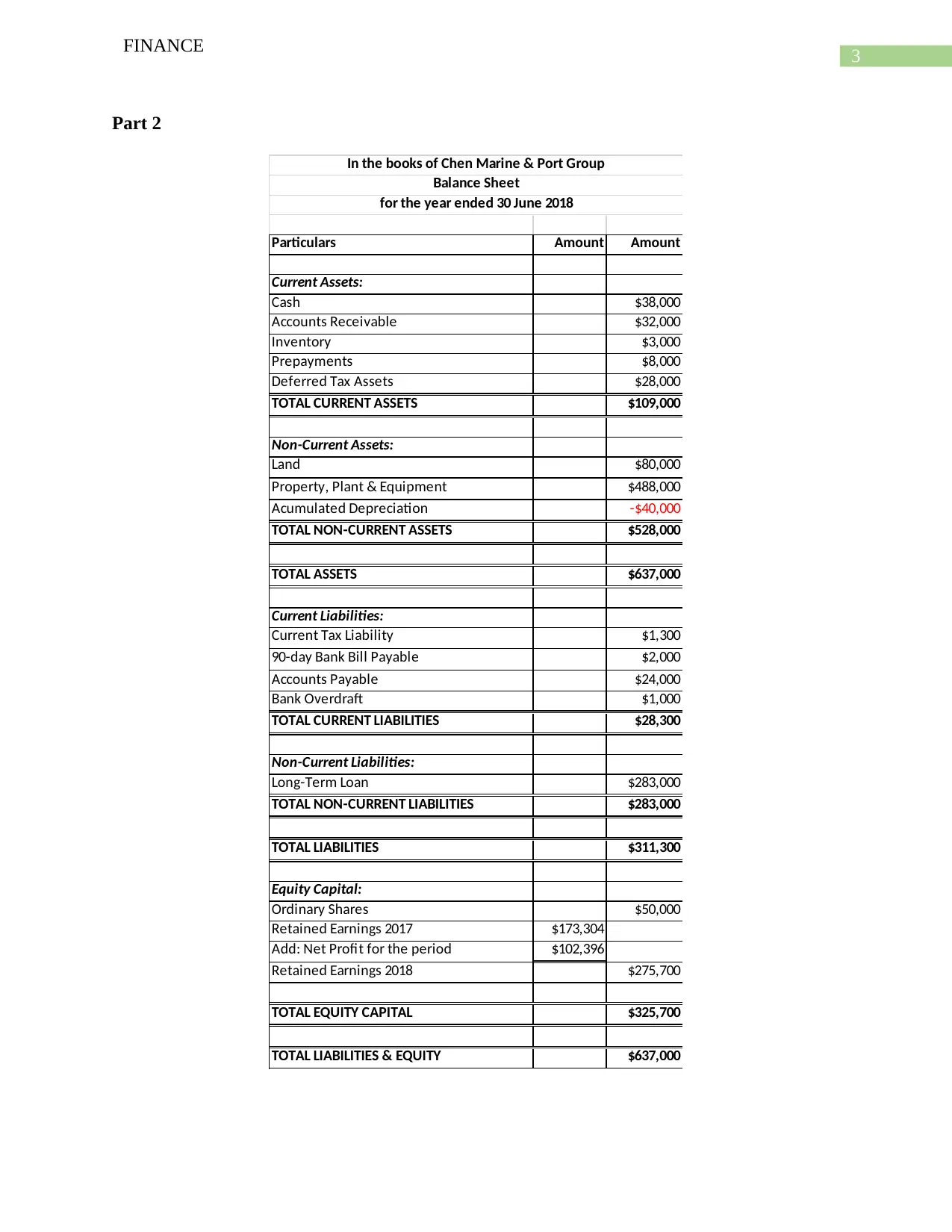

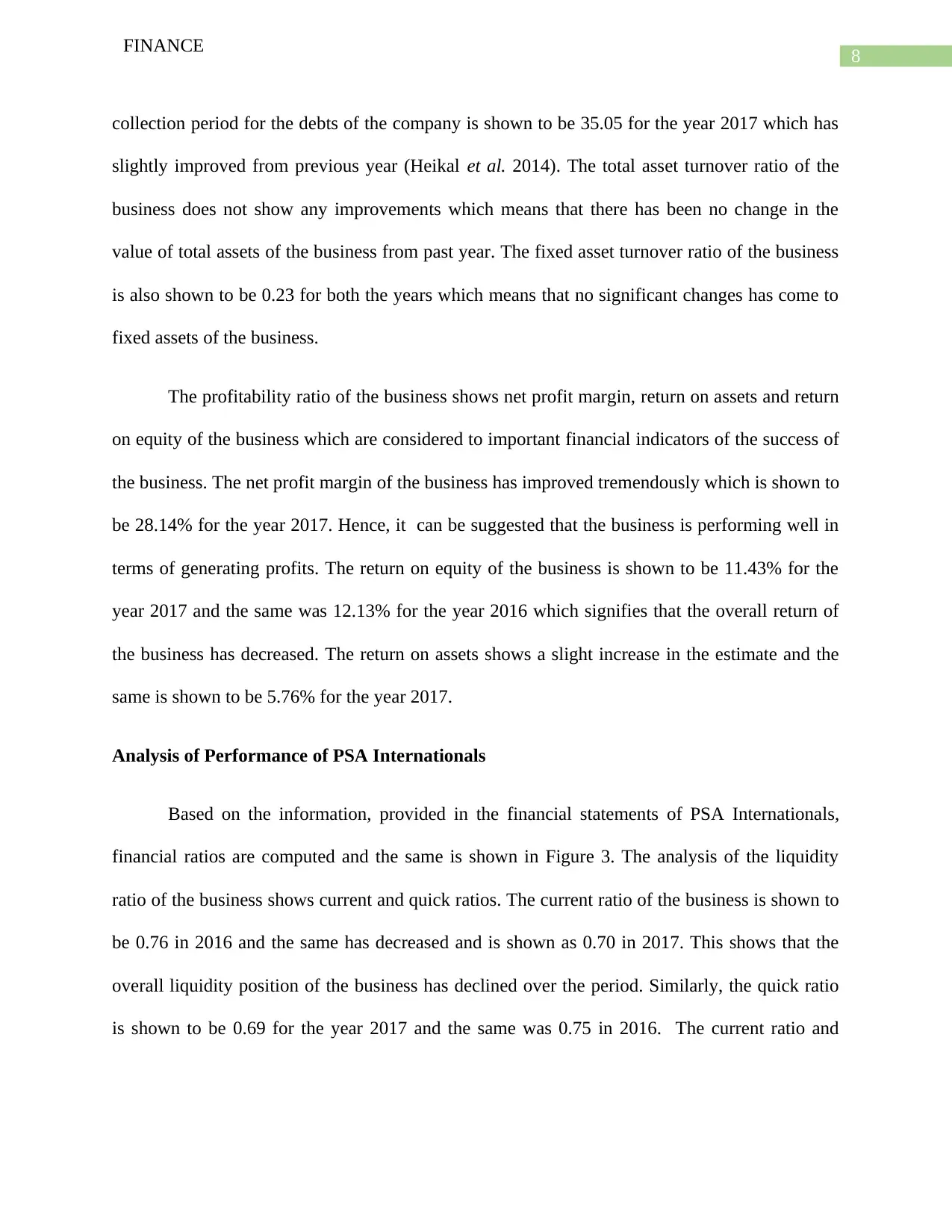

Part 2

Particulars Amount Amount

Current Assets:

Cash $38,000

Accounts Receivable $32,000

Inventory $3,000

Prepayments $8,000

Deferred Tax Assets $28,000

TOTAL CURRENT ASSETS $109,000

Non-Current Assets:

Land $80,000

Property, Plant & Equipment $488,000

Acumulated Depreciation -$40,000

TOTAL NON-CURRENT ASSETS $528,000

TOTAL ASSETS $637,000

Current Liabilities:

Current Tax Liability $1,300

90-day Bank Bill Payable $2,000

Accounts Payable $24,000

Bank Overdraft $1,000

TOTAL CURRENT LIABILITIES $28,300

Non-Current Liabilities:

Long-Term Loan $283,000

TOTAL NON-CURRENT LIABILITIES $283,000

TOTAL LIABILITIES $311,300

Equity Capital:

Ordinary Shares $50,000

Retained Earnings 2017 $173,304

Add: Net Profit for the period $102,396

Retained Earnings 2018 $275,700

TOTAL EQUITY CAPITAL $325,700

TOTAL LIABILITIES & EQUITY $637,000

In the books of Chen Marine & Port Group

Balance Sheet

for the year ended 30 June 2018

FINANCE

Part 2

Particulars Amount Amount

Current Assets:

Cash $38,000

Accounts Receivable $32,000

Inventory $3,000

Prepayments $8,000

Deferred Tax Assets $28,000

TOTAL CURRENT ASSETS $109,000

Non-Current Assets:

Land $80,000

Property, Plant & Equipment $488,000

Acumulated Depreciation -$40,000

TOTAL NON-CURRENT ASSETS $528,000

TOTAL ASSETS $637,000

Current Liabilities:

Current Tax Liability $1,300

90-day Bank Bill Payable $2,000

Accounts Payable $24,000

Bank Overdraft $1,000

TOTAL CURRENT LIABILITIES $28,300

Non-Current Liabilities:

Long-Term Loan $283,000

TOTAL NON-CURRENT LIABILITIES $283,000

TOTAL LIABILITIES $311,300

Equity Capital:

Ordinary Shares $50,000

Retained Earnings 2017 $173,304

Add: Net Profit for the period $102,396

Retained Earnings 2018 $275,700

TOTAL EQUITY CAPITAL $325,700

TOTAL LIABILITIES & EQUITY $637,000

In the books of Chen Marine & Port Group

Balance Sheet

for the year ended 30 June 2018

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

FINANCE

Figure 2: (Images showing Balance Sheet of Chen Marine and Port Group)

Source: (Created by the Author)

Answer to Question 2

Introduction

The primary objective of this report is to evaluate the financial performance of two

companies which are DP World and PSA Internationals. The report will be including key

financial ratios and analyzing the same for the purpose of identifying different areas of

performance for the businesses such as profitability, solvency, efficiency and capital structure.

DP World is engaged in the business of operating ports and was established in the year

2005 by merging of Dubai Ports Authority and Dubai Ports International. The company had

purchased numerous ports in USA but the same were sold shortly afterwards due to the

controversy which arose. PSA Internationals is also in engaged in the operations of port

operations and is considered to be one of the largest port operators of the country. The

assessment will be considering the financial information of these companies from the annual

report for recent years for computing key financial ratios of the business.

FINANCE

Figure 2: (Images showing Balance Sheet of Chen Marine and Port Group)

Source: (Created by the Author)

Answer to Question 2

Introduction

The primary objective of this report is to evaluate the financial performance of two

companies which are DP World and PSA Internationals. The report will be including key

financial ratios and analyzing the same for the purpose of identifying different areas of

performance for the businesses such as profitability, solvency, efficiency and capital structure.

DP World is engaged in the business of operating ports and was established in the year

2005 by merging of Dubai Ports Authority and Dubai Ports International. The company had

purchased numerous ports in USA but the same were sold shortly afterwards due to the

controversy which arose. PSA Internationals is also in engaged in the operations of port

operations and is considered to be one of the largest port operators of the country. The

assessment will be considering the financial information of these companies from the annual

report for recent years for computing key financial ratios of the business.

5

FINANCE

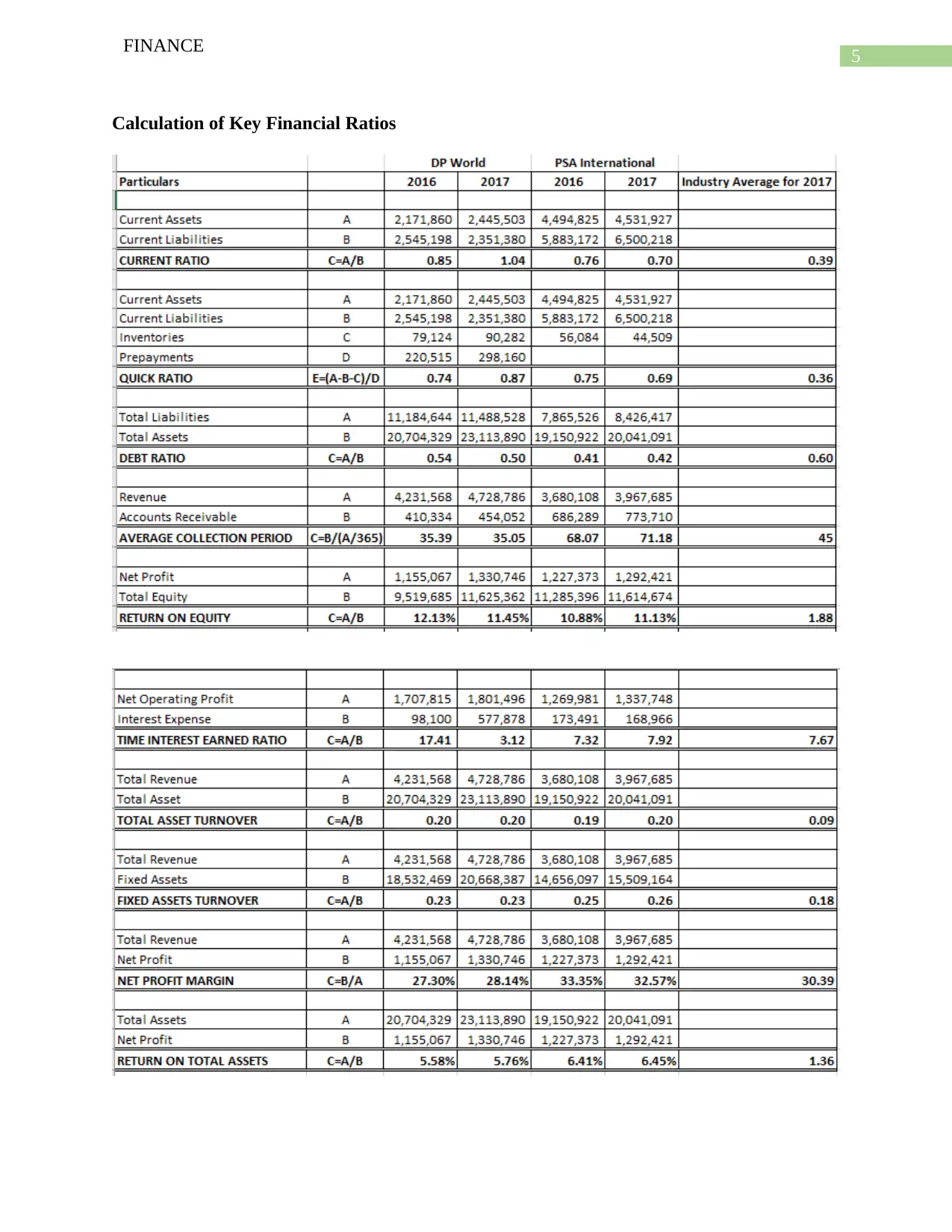

Calculation of Key Financial Ratios

FINANCE

Calculation of Key Financial Ratios

6

FINANCE

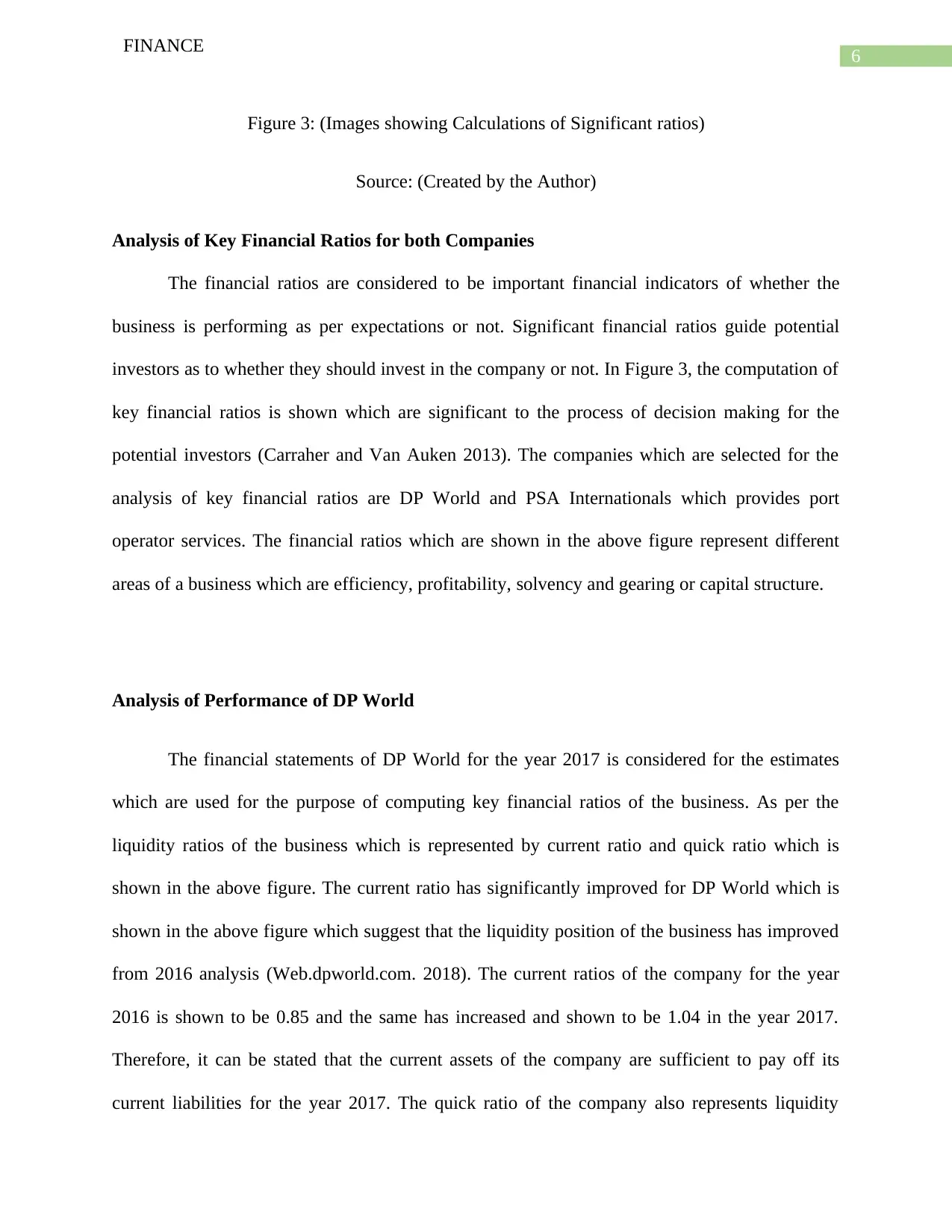

Figure 3: (Images showing Calculations of Significant ratios)

Source: (Created by the Author)

Analysis of Key Financial Ratios for both Companies

The financial ratios are considered to be important financial indicators of whether the

business is performing as per expectations or not. Significant financial ratios guide potential

investors as to whether they should invest in the company or not. In Figure 3, the computation of

key financial ratios is shown which are significant to the process of decision making for the

potential investors (Carraher and Van Auken 2013). The companies which are selected for the

analysis of key financial ratios are DP World and PSA Internationals which provides port

operator services. The financial ratios which are shown in the above figure represent different

areas of a business which are efficiency, profitability, solvency and gearing or capital structure.

Analysis of Performance of DP World

The financial statements of DP World for the year 2017 is considered for the estimates

which are used for the purpose of computing key financial ratios of the business. As per the

liquidity ratios of the business which is represented by current ratio and quick ratio which is

shown in the above figure. The current ratio has significantly improved for DP World which is

shown in the above figure which suggest that the liquidity position of the business has improved

from 2016 analysis (Web.dpworld.com. 2018). The current ratios of the company for the year

2016 is shown to be 0.85 and the same has increased and shown to be 1.04 in the year 2017.

Therefore, it can be stated that the current assets of the company are sufficient to pay off its

current liabilities for the year 2017. The quick ratio of the company also represents liquidity

FINANCE

Figure 3: (Images showing Calculations of Significant ratios)

Source: (Created by the Author)

Analysis of Key Financial Ratios for both Companies

The financial ratios are considered to be important financial indicators of whether the

business is performing as per expectations or not. Significant financial ratios guide potential

investors as to whether they should invest in the company or not. In Figure 3, the computation of

key financial ratios is shown which are significant to the process of decision making for the

potential investors (Carraher and Van Auken 2013). The companies which are selected for the

analysis of key financial ratios are DP World and PSA Internationals which provides port

operator services. The financial ratios which are shown in the above figure represent different

areas of a business which are efficiency, profitability, solvency and gearing or capital structure.

Analysis of Performance of DP World

The financial statements of DP World for the year 2017 is considered for the estimates

which are used for the purpose of computing key financial ratios of the business. As per the

liquidity ratios of the business which is represented by current ratio and quick ratio which is

shown in the above figure. The current ratio has significantly improved for DP World which is

shown in the above figure which suggest that the liquidity position of the business has improved

from 2016 analysis (Web.dpworld.com. 2018). The current ratios of the company for the year

2016 is shown to be 0.85 and the same has increased and shown to be 1.04 in the year 2017.

Therefore, it can be stated that the current assets of the company are sufficient to pay off its

current liabilities for the year 2017. The quick ratio of the company also represents liquidity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCE

position of a business but quick ratio considers current assets which are more liquid in nature

(Weil, Schipper and Francis 2013). The current assets in case of quick ratio does not include

inventories and prepayments which are shown in figure 3. The quick ratio of the business is

shown to be 0.74 and 0.87 for the year 2016 and 2017 as shown in the computations. This also

suggest that the liquidity of the business has improved significantly (Delen, Kuzey and Uyar

2013). Both current assets and quick assets are considered to be financial indicators of the

business and are considered by potential investors for the purpose of making decisions regarding

investments. In addition to this, the liquidity ratio also signifies whether the company is able to

meet the current obligations of the business which may be related to day to day business

efficiently or not (Lartey, Antwi and Boadi 2013).

The issue of financial stability of a business are related to capital structure of the

business. The capital structure of business determines the various financing decisions which the

management of the company needs to take during the year. In the case of DP World, the debt

ratio represents a part of the capital structure ratio or gearing ratio (Needles, Powers and Crosson

2013). The debt ratio of the company is shown to have reduced in 2017 in comparison to the

estimates of 2016. The debt ratio is shown to be 0.50 for the year 2017 and the same was shown

to be 0.54 in 2016 which is due to the repayment of a portion of debt capital which was

previously used by the business. The time interest earned ratio which is also related to gearing

ratios of the business is shown to be 3.12 in 2017 which shows that the estimate has decreased

significantly in comparison to previous year analysis. The time interest earned ratio for the year

2016 is shown to be 17.41 which is quite high.

The asset management efficiency ratio of DP World as shown in Figure 3 shows

Average collection period, total asset turnover ratio and fixed asset turnover ratio. The average

FINANCE

position of a business but quick ratio considers current assets which are more liquid in nature

(Weil, Schipper and Francis 2013). The current assets in case of quick ratio does not include

inventories and prepayments which are shown in figure 3. The quick ratio of the business is

shown to be 0.74 and 0.87 for the year 2016 and 2017 as shown in the computations. This also

suggest that the liquidity of the business has improved significantly (Delen, Kuzey and Uyar

2013). Both current assets and quick assets are considered to be financial indicators of the

business and are considered by potential investors for the purpose of making decisions regarding

investments. In addition to this, the liquidity ratio also signifies whether the company is able to

meet the current obligations of the business which may be related to day to day business

efficiently or not (Lartey, Antwi and Boadi 2013).

The issue of financial stability of a business are related to capital structure of the

business. The capital structure of business determines the various financing decisions which the

management of the company needs to take during the year. In the case of DP World, the debt

ratio represents a part of the capital structure ratio or gearing ratio (Needles, Powers and Crosson

2013). The debt ratio of the company is shown to have reduced in 2017 in comparison to the

estimates of 2016. The debt ratio is shown to be 0.50 for the year 2017 and the same was shown

to be 0.54 in 2016 which is due to the repayment of a portion of debt capital which was

previously used by the business. The time interest earned ratio which is also related to gearing

ratios of the business is shown to be 3.12 in 2017 which shows that the estimate has decreased

significantly in comparison to previous year analysis. The time interest earned ratio for the year

2016 is shown to be 17.41 which is quite high.

The asset management efficiency ratio of DP World as shown in Figure 3 shows

Average collection period, total asset turnover ratio and fixed asset turnover ratio. The average

8

FINANCE

collection period for the debts of the company is shown to be 35.05 for the year 2017 which has

slightly improved from previous year (Heikal et al. 2014). The total asset turnover ratio of the

business does not show any improvements which means that there has been no change in the

value of total assets of the business from past year. The fixed asset turnover ratio of the business

is also shown to be 0.23 for both the years which means that no significant changes has come to

fixed assets of the business.

The profitability ratio of the business shows net profit margin, return on assets and return

on equity of the business which are considered to important financial indicators of the success of

the business. The net profit margin of the business has improved tremendously which is shown to

be 28.14% for the year 2017. Hence, it can be suggested that the business is performing well in

terms of generating profits. The return on equity of the business is shown to be 11.43% for the

year 2017 and the same was 12.13% for the year 2016 which signifies that the overall return of

the business has decreased. The return on assets shows a slight increase in the estimate and the

same is shown to be 5.76% for the year 2017.

Analysis of Performance of PSA Internationals

Based on the information, provided in the financial statements of PSA Internationals,

financial ratios are computed and the same is shown in Figure 3. The analysis of the liquidity

ratio of the business shows current and quick ratios. The current ratio of the business is shown to

be 0.76 in 2016 and the same has decreased and is shown as 0.70 in 2017. This shows that the

overall liquidity position of the business has declined over the period. Similarly, the quick ratio

is shown to be 0.69 for the year 2017 and the same was 0.75 in 2016. The current ratio and

FINANCE

collection period for the debts of the company is shown to be 35.05 for the year 2017 which has

slightly improved from previous year (Heikal et al. 2014). The total asset turnover ratio of the

business does not show any improvements which means that there has been no change in the

value of total assets of the business from past year. The fixed asset turnover ratio of the business

is also shown to be 0.23 for both the years which means that no significant changes has come to

fixed assets of the business.

The profitability ratio of the business shows net profit margin, return on assets and return

on equity of the business which are considered to important financial indicators of the success of

the business. The net profit margin of the business has improved tremendously which is shown to

be 28.14% for the year 2017. Hence, it can be suggested that the business is performing well in

terms of generating profits. The return on equity of the business is shown to be 11.43% for the

year 2017 and the same was 12.13% for the year 2016 which signifies that the overall return of

the business has decreased. The return on assets shows a slight increase in the estimate and the

same is shown to be 5.76% for the year 2017.

Analysis of Performance of PSA Internationals

Based on the information, provided in the financial statements of PSA Internationals,

financial ratios are computed and the same is shown in Figure 3. The analysis of the liquidity

ratio of the business shows current and quick ratios. The current ratio of the business is shown to

be 0.76 in 2016 and the same has decreased and is shown as 0.70 in 2017. This shows that the

overall liquidity position of the business has declined over the period. Similarly, the quick ratio

is shown to be 0.69 for the year 2017 and the same was 0.75 in 2016. The current ratio and

9

FINANCE

quick ratio of the business both shows decrease which suggest that the liquidity position of the

business has decreased slightly (Globalpsa.com. 2018).

The gearing ratio of the business is showing debt of the business and also has equity

capital in the capital mix of the business. The debt ratio of the business has increased to 0.42 in

2017 and the same is shown to be 0.41 in 2016. The debt ratio suggest that the borrowings of the

business has increased in the current year. The Time interest earned ratio of the business for the

year 2017 is shown to be 7.92 which is more than previous year estimate (Al Karim and Alam

2013). Therefore, this signifies that the business has taken additional loan for financing the

activities of the business.

The asset management ratios signifies that the efficiency of the business to manage the

return which can be generated. The average collection period which is computed in figure 3

shows that the same has become higher which is not acceptable for the company. This signifies

that the funds of the business will be blocked for additional number of days. The total asset

turnover ratio and fixed asset turnover ratio shows that both have increased slightly from the

estimates of previous year which is represent that the company has made certain additions to the

assets of the business during the year.

The profitability ratio of the company shows net profit margin, return on assets and return

on equity for the business. All three of these ratios are considered to be financial indicators of the

success of the business (Louis, Seret and Baesens 2013). The net profit margin of the company is

shown to be 32.57% which is significant lower than the estimate of 2016 which is shown to be

33.35%. This shows that there is a fall in the profits of the business. It is an unfavorable sign for

the business. The return on equity, generated by the business is shown to be higher in 2017

FINANCE

quick ratio of the business both shows decrease which suggest that the liquidity position of the

business has decreased slightly (Globalpsa.com. 2018).

The gearing ratio of the business is showing debt of the business and also has equity

capital in the capital mix of the business. The debt ratio of the business has increased to 0.42 in

2017 and the same is shown to be 0.41 in 2016. The debt ratio suggest that the borrowings of the

business has increased in the current year. The Time interest earned ratio of the business for the

year 2017 is shown to be 7.92 which is more than previous year estimate (Al Karim and Alam

2013). Therefore, this signifies that the business has taken additional loan for financing the

activities of the business.

The asset management ratios signifies that the efficiency of the business to manage the

return which can be generated. The average collection period which is computed in figure 3

shows that the same has become higher which is not acceptable for the company. This signifies

that the funds of the business will be blocked for additional number of days. The total asset

turnover ratio and fixed asset turnover ratio shows that both have increased slightly from the

estimates of previous year which is represent that the company has made certain additions to the

assets of the business during the year.

The profitability ratio of the company shows net profit margin, return on assets and return

on equity for the business. All three of these ratios are considered to be financial indicators of the

success of the business (Louis, Seret and Baesens 2013). The net profit margin of the company is

shown to be 32.57% which is significant lower than the estimate of 2016 which is shown to be

33.35%. This shows that there is a fall in the profits of the business. It is an unfavorable sign for

the business. The return on equity, generated by the business is shown to be higher in 2017

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

FINANCE

which suggest that the business meets the expectation of the shareholders. The company has

provided 6.45% return on assets during the year 2017 which is slightly higher than the estimate

of 2016.

Cross Sectional Analysis of Financial Ratios

Cross sectional analysis of the financial ratios requires comparison of the results which

are computed in figure 3 with the industry averages which is also shown in figure 3. The current

ratio of both DP World and PSA Internationals is more than the industry average which is shown

to be 0.39 (Law and Singh 2014). This signifies that both the companies have better liquidity

position than most of the companies in the industry (Trujillo‐Ponce 2013). The current ratio of

DP World is better than PSA International as shown in figure 3. The quick ratio for both the

company also shows a similar result as in the case of current ratios.

The gearing ratio which consist of debt ratio shows that the both the company does not

uses as much debt capital as compared to other business in the industry. This can differ from

business to business in accordance to the Capital structure of the business (Adrian, Etula and

Muir 2014). The efficient ratio is represented by receivable collection period and total asset

turnover ratio and fixed asset turnover ratio. The average collection period for most of the

businesses is shown to be better than the DP World and PSA International. The total asset

turnover ratio and fixed asset turnover ratio of DP World and PSA International is better than the

industry average which is shown in figure 3.

The profitability ratio of the business consists of net profit margin, return on equity and

return on total asset. The net profit margin of DP World is lower than the industry average which

is shown to be 28.14% and the industry average is shown to be 30.39%. However, the net profit

FINANCE

which suggest that the business meets the expectation of the shareholders. The company has

provided 6.45% return on assets during the year 2017 which is slightly higher than the estimate

of 2016.

Cross Sectional Analysis of Financial Ratios

Cross sectional analysis of the financial ratios requires comparison of the results which

are computed in figure 3 with the industry averages which is also shown in figure 3. The current

ratio of both DP World and PSA Internationals is more than the industry average which is shown

to be 0.39 (Law and Singh 2014). This signifies that both the companies have better liquidity

position than most of the companies in the industry (Trujillo‐Ponce 2013). The current ratio of

DP World is better than PSA International as shown in figure 3. The quick ratio for both the

company also shows a similar result as in the case of current ratios.

The gearing ratio which consist of debt ratio shows that the both the company does not

uses as much debt capital as compared to other business in the industry. This can differ from

business to business in accordance to the Capital structure of the business (Adrian, Etula and

Muir 2014). The efficient ratio is represented by receivable collection period and total asset

turnover ratio and fixed asset turnover ratio. The average collection period for most of the

businesses is shown to be better than the DP World and PSA International. The total asset

turnover ratio and fixed asset turnover ratio of DP World and PSA International is better than the

industry average which is shown in figure 3.

The profitability ratio of the business consists of net profit margin, return on equity and

return on total asset. The net profit margin of DP World is lower than the industry average which

is shown to be 28.14% and the industry average is shown to be 30.39%. However, the net profit

11

FINANCE

margin of PSA International is better than the industry average which shows that PSA

International is more profitable in nature (Han, Yang and Zhou 2013). The return on assets of the

business of both the companies is better than the industry average which shows that the

companies are better than most of the companies in the industry.

Conclusion and Recommendations

As per the significant ratios which are computed in figure 3, the liquidity position of DP

World is relatively higher than that of PSA Internationals which is clearly indicated by the

current ratio and quick ratio of the business. The debt ratio of the business also shows that DP

World is better leveraged considering the capital structure of the business as compared to the

business of PSA Internationals (Chandra 2017). In most cases, better leveraged firms have higher

chances to achieve growth and development and also improve profitability of the company in the

long-run. Therefore, the business of DP World looks more favorable from the point of view of

leverage in comparison to business of PSA Internationals.

The asset management ratios which are represented by total asset turnover ratio and fixed

asset turnover ratio is also shown to be better for DP World which signifies that the business is

able to utilize the assets to its full capacity and thereby generate appropriate revenues from the

same. The collection period for debtors in case of DP World is also lower than business of PSA

Internationals which shows a better debtor management policy of the business and also a better

collection policy as well.

The profitability ratio reveals that the net profit margin of business of PSA Internationals

is much better than DP World which is an indication of better sales or better cost control policy

of the business (Tan 2013). The current market condition reveals that the business of DP World

FINANCE

margin of PSA International is better than the industry average which shows that PSA

International is more profitable in nature (Han, Yang and Zhou 2013). The return on assets of the

business of both the companies is better than the industry average which shows that the

companies are better than most of the companies in the industry.

Conclusion and Recommendations

As per the significant ratios which are computed in figure 3, the liquidity position of DP

World is relatively higher than that of PSA Internationals which is clearly indicated by the

current ratio and quick ratio of the business. The debt ratio of the business also shows that DP

World is better leveraged considering the capital structure of the business as compared to the

business of PSA Internationals (Chandra 2017). In most cases, better leveraged firms have higher

chances to achieve growth and development and also improve profitability of the company in the

long-run. Therefore, the business of DP World looks more favorable from the point of view of

leverage in comparison to business of PSA Internationals.

The asset management ratios which are represented by total asset turnover ratio and fixed

asset turnover ratio is also shown to be better for DP World which signifies that the business is

able to utilize the assets to its full capacity and thereby generate appropriate revenues from the

same. The collection period for debtors in case of DP World is also lower than business of PSA

Internationals which shows a better debtor management policy of the business and also a better

collection policy as well.

The profitability ratio reveals that the net profit margin of business of PSA Internationals

is much better than DP World which is an indication of better sales or better cost control policy

of the business (Tan 2013). The current market condition reveals that the business of DP World

12

FINANCE

is better than the business of PSA Internationals as the former is undergoing growth and

development and is recognizable in the industry. The company DP World is a result of a merger

and thereby is financially quite established. Therefore it is recommended that investors invests in

the business of DP World as the company looks more financially secure with better liquidity

position, return on equity and assets, average net profits, better efficiency.

Reference

Adrian, T., Etula, E. and Muir, T., 2014. Financial intermediaries and the cross‐section of asset

returns. The Journal of Finance, 69(6), pp.2557-2596.

Al Karim, R. and Alam, T., 2013. An evaluation of financial performance of private commercial

banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), p.65.

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Globalpsa.com. 2018. [online] Available at:

https://www.globalpsa.com/wp-content/uploads/AR2017.pdf [Accessed 25 Aug. 2018].

Han, Y., Yang, K. and Zhou, G., 2013. A new anomaly: The cross-sectional profitability of

technical analysis. Journal of Financial and Quantitative Analysis, 48(5), pp.1433-1461.

FINANCE

is better than the business of PSA Internationals as the former is undergoing growth and

development and is recognizable in the industry. The company DP World is a result of a merger

and thereby is financially quite established. Therefore it is recommended that investors invests in

the business of DP World as the company looks more financially secure with better liquidity

position, return on equity and assets, average net profits, better efficiency.

Reference

Adrian, T., Etula, E. and Muir, T., 2014. Financial intermediaries and the cross‐section of asset

returns. The Journal of Finance, 69(6), pp.2557-2596.

Al Karim, R. and Alam, T., 2013. An evaluation of financial performance of private commercial

banks in Bangladesh: Ratio analysis. Journal of Business Studies Quarterly, 5(2), p.65.

Carraher, S. and Van Auken, H., 2013. The use of financial statements for decision making by

small firms. Journal of Small Business & Entrepreneurship, 26(3), pp.323-336.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Globalpsa.com. 2018. [online] Available at:

https://www.globalpsa.com/wp-content/uploads/AR2017.pdf [Accessed 25 Aug. 2018].

Han, Y., Yang, K. and Zhou, G., 2013. A new anomaly: The cross-sectional profitability of

technical analysis. Journal of Financial and Quantitative Analysis, 48(5), pp.1433-1461.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

FINANCE

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock Exchange. International

Journal of Academic Research in Business and Social Sciences, 4(12), p.101.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social Science, 4(3).

Law, S.H. and Singh, N., 2014. Does too much finance harm economic growth?. Journal of

Banking & Finance, 41, pp.36-44.

Louis, P., Seret, A. and Baesens, B., 2013. Financial efficiency and social impact of

microfinance institutions using self-organizing maps. World Development, 46, pp.197-210.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Tan, L., 2013. Creditor control rights, state of nature verification, and financial reporting

conservatism. Journal of Accounting and Economics, 55(1), pp.1-22.

Trujillo‐Ponce, A., 2013. What determines the profitability of banks? Evidence from

Spain. Accounting & Finance, 53(2), pp.561-586.

Web.dpworld.com. 2018. [online] Available at:

http://web.dpworld.com/wp-content/uploads/2014/05/DPWORLD_AR.pdf [Accessed 25 Aug.

2018].

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

FINANCE

Heikal, M., Khaddafi, M. and Ummah, A., 2014. Influence analysis of return on assets (ROA),

return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock Exchange. International

Journal of Academic Research in Business and Social Sciences, 4(12), p.101.

Lartey, V.C., Antwi, S. and Boadi, E.K., 2013. The relationship between liquidity and

profitability of listed banks in Ghana. International Journal of Business and Social Science, 4(3).

Law, S.H. and Singh, N., 2014. Does too much finance harm economic growth?. Journal of

Banking & Finance, 41, pp.36-44.

Louis, P., Seret, A. and Baesens, B., 2013. Financial efficiency and social impact of

microfinance institutions using self-organizing maps. World Development, 46, pp.197-210.

Needles, B.E., Powers, M. and Crosson, S.V., 2013. Financial and managerial accounting.

Cengage Learning.

Tan, L., 2013. Creditor control rights, state of nature verification, and financial reporting

conservatism. Journal of Accounting and Economics, 55(1), pp.1-22.

Trujillo‐Ponce, A., 2013. What determines the profitability of banks? Evidence from

Spain. Accounting & Finance, 53(2), pp.561-586.

Web.dpworld.com. 2018. [online] Available at:

http://web.dpworld.com/wp-content/uploads/2014/05/DPWORLD_AR.pdf [Accessed 25 Aug.

2018].

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.