Finance Portfolio Management

VerifiedAdded on 2023/04/04

|15

|2854

|173

AI Summary

This document provides an in-depth analysis of finance portfolio management, including the construction of stable return and high return portfolios. It explores the application of modern portfolio theory and evaluates the performance of portfolios using various performance measures. The document also discusses the limitations of portfolio management and provides expert guidance on constructing portfolios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running Head: Finance Portfolio Management

Finance Portfolio Management

PC-LE0327

Finance Portfolio Management

PC-LE0327

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction...........................................................................................................................................2

1. Portfolio Construction...................................................................................................................2

2. Application of Modern Portfolio Theory in Portfolio Construction...............................................3

Sharpe Ratio......................................................................................................................................8

Treynor Ratio....................................................................................................................................9

Jensen’s Alpha...................................................................................................................................9

3. Performance of Portfolios in January-February 2019..................................................................12

4. Limitation....................................................................................................................................13

5. Conclusion...................................................................................................................................13

References...........................................................................................................................................14

Appendix.............................................................................................................................................15

1

Introduction...........................................................................................................................................2

1. Portfolio Construction...................................................................................................................2

2. Application of Modern Portfolio Theory in Portfolio Construction...............................................3

Sharpe Ratio......................................................................................................................................8

Treynor Ratio....................................................................................................................................9

Jensen’s Alpha...................................................................................................................................9

3. Performance of Portfolios in January-February 2019..................................................................12

4. Limitation....................................................................................................................................13

5. Conclusion...................................................................................................................................13

References...........................................................................................................................................14

Appendix.............................................................................................................................................15

1

Introduction

At the time of making an investment decision the main motives of the investors are to receive

a higher return on the amount invested and to reduce the risk of loss. Usually, there are

investors who prefer to receive a fixed amount of return on their invested amount which may

include a pensioner, salaried person planning a marriage, education of his son/daughter or

future travel plans (Forbes, 2019). Then, there are people who have the capability of taking

more and more risk to get a good sum of return. Such persons usually have a good amount of

money which usually increases their risk taking capability. The profit or loss on investment

depends highly upon the selection of stocks which ultimately forms a portfolio. There are

certain parameters which are considered at the time of forming a portfolio which includes the

political, economic, environmental etc. factors and the most important parameter which

influences a portfolio is the risk attached with the stock and its sector. The main motive

behind the portfolio construction is nothing but is to diversify this risk at the maximum level.

Apart from this it is always advisable to look both risk return together at the time of

evaluating portfolio.

1. Portfolio Construction

As we know there are two kinds of investors: first those investors who want to get a stable

return from the amount invested and they are usually risk averse and then there are those

investors who love to take risks but expect a higher rate of return from the market.

There are stocks which give a stable return over a period of time and are less volatile. Also,

there are stocks which are highly volatile and give a high return, however the risk in such

stocks are on a higher side. For the investors who believe in taking more risk for a higher rate

of return on their money, they usually opt for such stocks.

At the time of forming stable return portfolio, the betas of individual stocks were considered

and the ones with the lower beta were selected like Admiral Group Plc., Auto Trader Group

Plc. and Pearson Plc. have beta of 0.54, -0.02 and 0.7 respectively. Also, the standard

deviations and returns of the stocks were calculated and the stocks with lowest risk and

lowest returns were chosen for stable return portfolio as shown in Table A.

In case of high return portfolio, the stocks with higher betas were chosen because such

volatile stocks usually give a higher return. The betas for high return portfolio are 1.36, 1.12

2

At the time of making an investment decision the main motives of the investors are to receive

a higher return on the amount invested and to reduce the risk of loss. Usually, there are

investors who prefer to receive a fixed amount of return on their invested amount which may

include a pensioner, salaried person planning a marriage, education of his son/daughter or

future travel plans (Forbes, 2019). Then, there are people who have the capability of taking

more and more risk to get a good sum of return. Such persons usually have a good amount of

money which usually increases their risk taking capability. The profit or loss on investment

depends highly upon the selection of stocks which ultimately forms a portfolio. There are

certain parameters which are considered at the time of forming a portfolio which includes the

political, economic, environmental etc. factors and the most important parameter which

influences a portfolio is the risk attached with the stock and its sector. The main motive

behind the portfolio construction is nothing but is to diversify this risk at the maximum level.

Apart from this it is always advisable to look both risk return together at the time of

evaluating portfolio.

1. Portfolio Construction

As we know there are two kinds of investors: first those investors who want to get a stable

return from the amount invested and they are usually risk averse and then there are those

investors who love to take risks but expect a higher rate of return from the market.

There are stocks which give a stable return over a period of time and are less volatile. Also,

there are stocks which are highly volatile and give a high return, however the risk in such

stocks are on a higher side. For the investors who believe in taking more risk for a higher rate

of return on their money, they usually opt for such stocks.

At the time of forming stable return portfolio, the betas of individual stocks were considered

and the ones with the lower beta were selected like Admiral Group Plc., Auto Trader Group

Plc. and Pearson Plc. have beta of 0.54, -0.02 and 0.7 respectively. Also, the standard

deviations and returns of the stocks were calculated and the stocks with lowest risk and

lowest returns were chosen for stable return portfolio as shown in Table A.

In case of high return portfolio, the stocks with higher betas were chosen because such

volatile stocks usually give a higher return. The betas for high return portfolio are 1.36, 1.12

2

and 0.66 for Ocado, J Sainsbury plc. and Evraz plc. respectively. Also, the stocks with higher

risk and higher returns were considered and we could find the figures in Table A.

In Table A, we could see that the stocks of stable return portfolio have lower return and lower

risk as compared to the stocks of high return portfolio which are having higher return and

higher risk.

Table A: Mean and Standard Deviation of Stocks of Portfolios

Stable Return

Portfolio Mean Standard

Deviation

High Return

Portfolio Mean Standard

Deviation

Admiral 5.57% 18% Ocado 68.42% 61.00%

Auto Trader 23.48% 28% J Sainsbury Plc. 7.98% 25.00%

Pearson Plc. 18.43% 21% Evraz 31.94% 46.27%

2. Application of Modern Portfolio Theory in Portfolio Construction

The theory of modern portfolio was given by Harry Markowitz which got published in the

year 1952 in Journal of Finance. He was the person who actually quantified the way of

forming portfolio at a given level of risk (U.S.News, 2018). The investors use this theory for

maximising their expected return on the formed portfolio. (Hawley and Lukomnik, 2018).

There are certain assumptions on which this theory works, like no transaction costs are

involved in buying/selling the securities, no tax are paid, risk is only considered at the time of

investing in any security, investors are allowed to take any position irrespective of its size and

type because the market is considered to be infinitely liquid, taxes and dividends are not

considered by the investor at the time of making an investment decision, investors are risk

adverse and rational along with the full knowledge of risk involved in the investment etc.

Three Asset Portfolio Formula

Covariance Formula

3

risk and higher returns were considered and we could find the figures in Table A.

In Table A, we could see that the stocks of stable return portfolio have lower return and lower

risk as compared to the stocks of high return portfolio which are having higher return and

higher risk.

Table A: Mean and Standard Deviation of Stocks of Portfolios

Stable Return

Portfolio Mean Standard

Deviation

High Return

Portfolio Mean Standard

Deviation

Admiral 5.57% 18% Ocado 68.42% 61.00%

Auto Trader 23.48% 28% J Sainsbury Plc. 7.98% 25.00%

Pearson Plc. 18.43% 21% Evraz 31.94% 46.27%

2. Application of Modern Portfolio Theory in Portfolio Construction

The theory of modern portfolio was given by Harry Markowitz which got published in the

year 1952 in Journal of Finance. He was the person who actually quantified the way of

forming portfolio at a given level of risk (U.S.News, 2018). The investors use this theory for

maximising their expected return on the formed portfolio. (Hawley and Lukomnik, 2018).

There are certain assumptions on which this theory works, like no transaction costs are

involved in buying/selling the securities, no tax are paid, risk is only considered at the time of

investing in any security, investors are allowed to take any position irrespective of its size and

type because the market is considered to be infinitely liquid, taxes and dividends are not

considered by the investor at the time of making an investment decision, investors are risk

adverse and rational along with the full knowledge of risk involved in the investment etc.

Three Asset Portfolio Formula

Covariance Formula

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

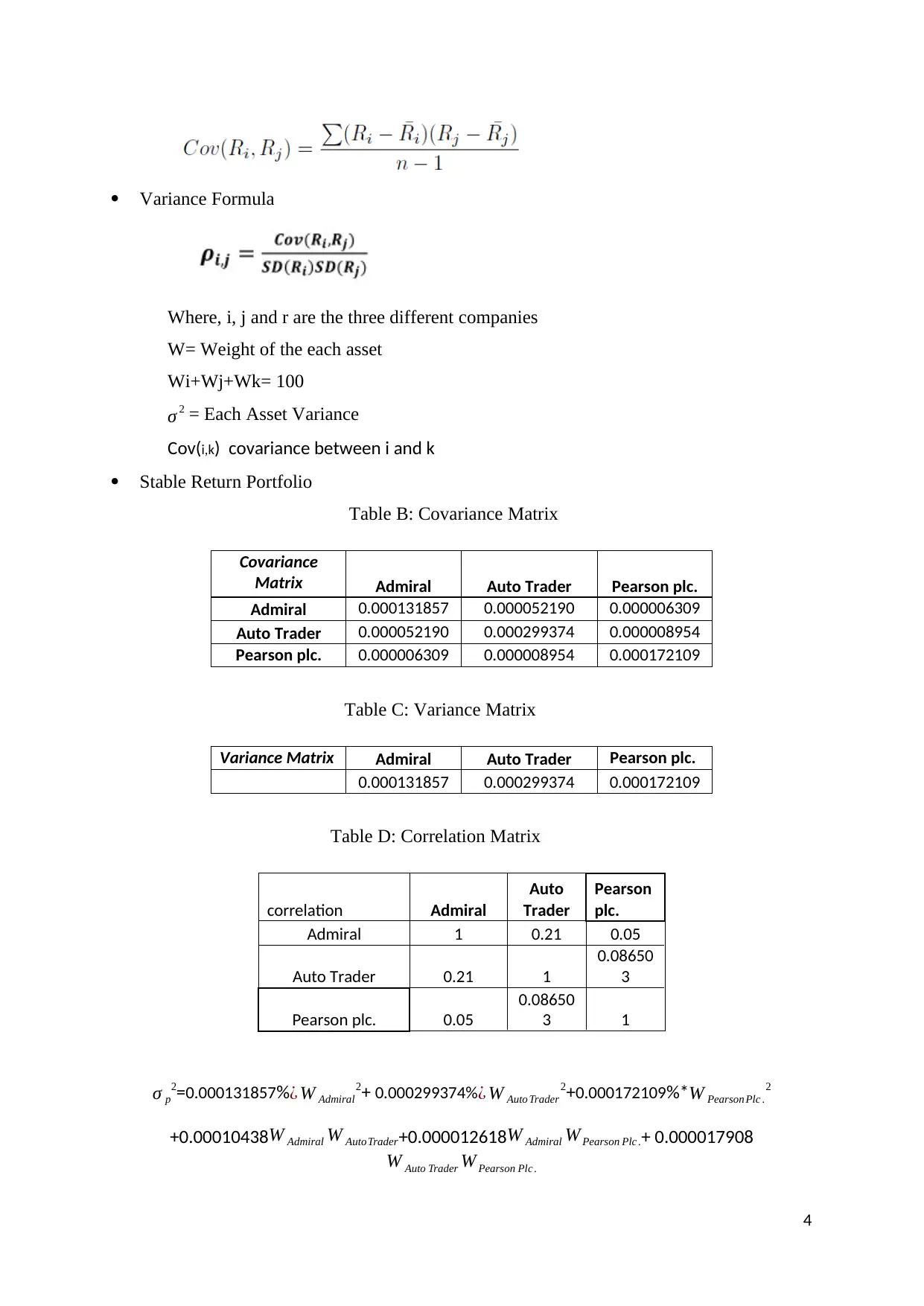

Variance Formula

Where, i, j and r are the three different companies

W= Weight of the each asset

Wi+Wj+Wk= 100

σ 2 = Each Asset Variance

Cov(i,k) covariance between i and k

Stable Return Portfolio

Table B: Covariance Matrix

Covariance

Matrix Admiral Auto Trader Pearson plc.

Admiral 0.000131857 0.000052190 0.000006309

Auto Trader 0.000052190 0.000299374 0.000008954

Pearson plc. 0.000006309 0.000008954 0.000172109

Table C: Variance Matrix

Variance Matrix Admiral Auto Trader Pearson plc.

0.000131857 0.000299374 0.000172109

Table D: Correlation Matrix

correlation Admiral

Auto

Trader

Pearson

plc.

Admiral 1 0.21 0.05

Auto Trader 0.21 1

0.08650

3

Pearson plc. 0.05

0.08650

3 1

σ p

2=0.000131857%¿ W Admiral

2+ 0.000299374% ¿ W Auto Trader

2+0.000172109%*W Pearson Plc .

2

+0.00010438 W Admiral W AutoTrader+0.000012618W Admiral W Pearson Plc .+ 0.000017908

W Auto Trader W Pearson Plc .

4

Where, i, j and r are the three different companies

W= Weight of the each asset

Wi+Wj+Wk= 100

σ 2 = Each Asset Variance

Cov(i,k) covariance between i and k

Stable Return Portfolio

Table B: Covariance Matrix

Covariance

Matrix Admiral Auto Trader Pearson plc.

Admiral 0.000131857 0.000052190 0.000006309

Auto Trader 0.000052190 0.000299374 0.000008954

Pearson plc. 0.000006309 0.000008954 0.000172109

Table C: Variance Matrix

Variance Matrix Admiral Auto Trader Pearson plc.

0.000131857 0.000299374 0.000172109

Table D: Correlation Matrix

correlation Admiral

Auto

Trader

Pearson

plc.

Admiral 1 0.21 0.05

Auto Trader 0.21 1

0.08650

3

Pearson plc. 0.05

0.08650

3 1

σ p

2=0.000131857%¿ W Admiral

2+ 0.000299374% ¿ W Auto Trader

2+0.000172109%*W Pearson Plc .

2

+0.00010438 W Admiral W AutoTrader+0.000012618W Admiral W Pearson Plc .+ 0.000017908

W Auto Trader W Pearson Plc .

4

E ( RStable Return Portfolio ) =5.57 %∗W Admiral+23.48 % W AutoTrader+ 18.43% W Pearson Plc

High Return Portfolio

Table E: Covariance Matrix

Ocado J Sainsbury plc. Evraz

Ocado 0.00147327671 0.00001228977 -0.00000534408

J Sainsbury plc. 0.00001228977 0.00024696506 0.00004465741

Evraz -0.00000534408 0.00004465741 0.00084608739

Table F: Variance Matrix

variance Matrix

Ocado J Sainsbury plc. Evraz

0.0014732767

1 0.00024696506

0.0008460873

9

Table G: Correlation Matrix

correlation Ocado

J

Sainsbur

y plc.

Evraz

Ocado 1 0.11 0.13

J Sainsbury plc 0.11 1

0.09769

4

Evraz 0.13 0.097694 1

σ p

20.00147327671 ¿ W Ocado

2+0.00024696506% ¿ W J Sainsbury plc .

2+0.00084608739%*W Evraz

2

+0.00001228977 W Ocado WJ Sainsbury Plc .+ (-0.00001068816) WOcado W Evraz+ 0.00008931482

W J Sainsbury plc . W Evraz

E ( RHighRetu rn Portfolio ) =68.42%∗W Ocado+7.98 % W J Sainsbury plc .+31.94 % W Evraz

5

High Return Portfolio

Table E: Covariance Matrix

Ocado J Sainsbury plc. Evraz

Ocado 0.00147327671 0.00001228977 -0.00000534408

J Sainsbury plc. 0.00001228977 0.00024696506 0.00004465741

Evraz -0.00000534408 0.00004465741 0.00084608739

Table F: Variance Matrix

variance Matrix

Ocado J Sainsbury plc. Evraz

0.0014732767

1 0.00024696506

0.0008460873

9

Table G: Correlation Matrix

correlation Ocado

J

Sainsbur

y plc.

Evraz

Ocado 1 0.11 0.13

J Sainsbury plc 0.11 1

0.09769

4

Evraz 0.13 0.097694 1

σ p

20.00147327671 ¿ W Ocado

2+0.00024696506% ¿ W J Sainsbury plc .

2+0.00084608739%*W Evraz

2

+0.00001228977 W Ocado WJ Sainsbury Plc .+ (-0.00001068816) WOcado W Evraz+ 0.00008931482

W J Sainsbury plc . W Evraz

E ( RHighRetu rn Portfolio ) =68.42%∗W Ocado+7.98 % W J Sainsbury plc .+31.94 % W Evraz

5

Analysis of weight

Here, the weights of the stable return portfolio and high return portfolio are optimised to

maximise the sharp ratio and both of these optimal portfolios are identified through the

efficient frontiers given under Graph A.

Figure A: Efficient Frontiers

0.005000 0.010000 0.015000 0.020000 0.025000 0.030000 0.035000

-0.15%

-0.10%

-0.05%

0.00%

0.05%

0.10%

0.15%

Efficient frontier for High Return Portfolio

Efficient frontier

Standard Deviation

Returns

0.006000 0.008000 0.010000 0.012000 0.014000 0.016000

-0.15%

-0.10%

-0.05%

0.00%

0.05%

0.10%

Efficient Frontier for Stable Return Portfolio

Efficient Frontier

Standard Deviation

Returns

6

Here, the weights of the stable return portfolio and high return portfolio are optimised to

maximise the sharp ratio and both of these optimal portfolios are identified through the

efficient frontiers given under Graph A.

Figure A: Efficient Frontiers

0.005000 0.010000 0.015000 0.020000 0.025000 0.030000 0.035000

-0.15%

-0.10%

-0.05%

0.00%

0.05%

0.10%

0.15%

Efficient frontier for High Return Portfolio

Efficient frontier

Standard Deviation

Returns

0.006000 0.008000 0.010000 0.012000 0.014000 0.016000

-0.15%

-0.10%

-0.05%

0.00%

0.05%

0.10%

Efficient Frontier for Stable Return Portfolio

Efficient Frontier

Standard Deviation

Returns

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These portfolios are constructed using Markowitz Portfolio Theory. Efficient Frontiers are

constructed to find the combination which maximises the sharp ratio from the number of

weight combinations available for any portfolio. Efficient frontier is created to identify the set

of optimal portfolios that gives the maximum expected return for the given level of risk or the

minimum risk for the defined level of expected return. Now, in Table “H” one can find the

portfolios constructed for the above mentioned types of investors; first for the ones who want

a stable return on their investment and the others who want a higher return on their

investment.

Table H: Stable Returns Portfolio and High Returns Portfolio

Stable Return

Portfolio Sector Weight

s

High Return

Portfolio Sector Weight

s

Admiral Group plc. Financials 6.36 Ocado Group plc. Consumer

Discretionary 50.41%

Auto Trader Group plc. Communication Services 39.26 J Sainsbury plc. Consumer Staples 15.36%

Pearson plc. Communication Services 54.38 Evraz plc. Materials 34.23%

Comparison of Performance of Stable return Portfolio and High return Portfolio

Portfolios performance evaluation is usually conducted to know whether an investment

portfolio had underperformed or outperformed or had performed at par with a considered

benchmark which could be an index. There are various reasons for which performance of the

investment portfolio is evaluated. First, the investors are always keen to know the

performance of the portfolio in which they had invested their funds and accordingly they

manage or revise their portfolio. Second, with the help of the portfolio performance measures

the performance of the portfolio manager is evaluated.

There are usually three ratios which are computed in order to evaluate the performance of

portfolios. These are Sharpe ratios, Treynor ratio and Jensen’s alpha.

Now, let us evaluate the performance of the two portfolios formed for the investors looking

for stable return and for those looking for high return.

Sharpe Ratio

Sharpe ratio computes the excess return earned on per unit of total risk of the investment

portfolio (Morningstar, 2012). Sharpe ratio is calculated with the help of the following

7

constructed to find the combination which maximises the sharp ratio from the number of

weight combinations available for any portfolio. Efficient frontier is created to identify the set

of optimal portfolios that gives the maximum expected return for the given level of risk or the

minimum risk for the defined level of expected return. Now, in Table “H” one can find the

portfolios constructed for the above mentioned types of investors; first for the ones who want

a stable return on their investment and the others who want a higher return on their

investment.

Table H: Stable Returns Portfolio and High Returns Portfolio

Stable Return

Portfolio Sector Weight

s

High Return

Portfolio Sector Weight

s

Admiral Group plc. Financials 6.36 Ocado Group plc. Consumer

Discretionary 50.41%

Auto Trader Group plc. Communication Services 39.26 J Sainsbury plc. Consumer Staples 15.36%

Pearson plc. Communication Services 54.38 Evraz plc. Materials 34.23%

Comparison of Performance of Stable return Portfolio and High return Portfolio

Portfolios performance evaluation is usually conducted to know whether an investment

portfolio had underperformed or outperformed or had performed at par with a considered

benchmark which could be an index. There are various reasons for which performance of the

investment portfolio is evaluated. First, the investors are always keen to know the

performance of the portfolio in which they had invested their funds and accordingly they

manage or revise their portfolio. Second, with the help of the portfolio performance measures

the performance of the portfolio manager is evaluated.

There are usually three ratios which are computed in order to evaluate the performance of

portfolios. These are Sharpe ratios, Treynor ratio and Jensen’s alpha.

Now, let us evaluate the performance of the two portfolios formed for the investors looking

for stable return and for those looking for high return.

Sharpe Ratio

Sharpe ratio computes the excess return earned on per unit of total risk of the investment

portfolio (Morningstar, 2012). Sharpe ratio is calculated with the help of the following

7

formula:

where,

Rp= Portfolio return

Rf=Risk Free rate of return

σp= Portfolio standard deviation

S= Sharpe Ratio

Treynor Ratio

Treynor ratio computes the excess return earned on per unit of systematic risk. Excess return

is also known as risk premium (Benhamou and Guez, 2018). In case of Sharpe ratio, the

standard deviation of portfolio is used as risk parameter and here in case of Treynor ratio the

systematic risk is considered (cleartax, 2018). Systematic risk refers to those risks which

could never be removed or eliminated through diversification. Treynor ratio is calculated

with the help of the following formula:

where,

Rp= Portfolio return

Rf=Risk Free rate of return

ßp = Portfolio beta

T= Treynor Ratio

8

S= Rp-Rf/ σp

T= Rp-Rf/ ßp

where,

Rp= Portfolio return

Rf=Risk Free rate of return

σp= Portfolio standard deviation

S= Sharpe Ratio

Treynor Ratio

Treynor ratio computes the excess return earned on per unit of systematic risk. Excess return

is also known as risk premium (Benhamou and Guez, 2018). In case of Sharpe ratio, the

standard deviation of portfolio is used as risk parameter and here in case of Treynor ratio the

systematic risk is considered (cleartax, 2018). Systematic risk refers to those risks which

could never be removed or eliminated through diversification. Treynor ratio is calculated

with the help of the following formula:

where,

Rp= Portfolio return

Rf=Risk Free rate of return

ßp = Portfolio beta

T= Treynor Ratio

8

S= Rp-Rf/ σp

T= Rp-Rf/ ßp

Jensen’s Alpha

Jensen’s alpha is calculated on the basis of Capital Asset Pricing Model (CAPM). The figure

of alpha denotes by how much amount the average return of portfolio deviates from the

expected return calculated by applying the capital asset pricing model (CAPM) (Dr. Wu,

2007). The expected return calculated through CAPM actually considers risk free rate of

return, systematic risk and market risk premium.

Jensen’s alpha is calculated with the help of the following formula:

where,

Rp= Portfolio return

CAPM= Rf- ßp * (Market return -Rf)

α=Jensen’s Alpha

Performance Measure of Stable Return Portfolio

In Table I, the ratios are computed for evaluating the performance of stable return portfolio

during the time period of January- December 2018. Now, the first thing we could observe

from the figures of these ratios is that all these are positive in number. This shows that the

portfolio is giving an adequate amount of return and has performed really well. Individually,

the positive figure of Sharpe ratio and Treynor ratio of the stable return portfolio shows that

the investor has received some amount of return for the risk taken but it is not considered

good because the return received from the portfolio is below the risk free rate which stands at

0.72%. Lastly, the computed alpha of stable return portfolio has shown that the portfolio had

outperformed the market. Higher alphas are always considered to be good and acceptable.

9

α = Rp- CAPM

Jensen’s alpha is calculated on the basis of Capital Asset Pricing Model (CAPM). The figure

of alpha denotes by how much amount the average return of portfolio deviates from the

expected return calculated by applying the capital asset pricing model (CAPM) (Dr. Wu,

2007). The expected return calculated through CAPM actually considers risk free rate of

return, systematic risk and market risk premium.

Jensen’s alpha is calculated with the help of the following formula:

where,

Rp= Portfolio return

CAPM= Rf- ßp * (Market return -Rf)

α=Jensen’s Alpha

Performance Measure of Stable Return Portfolio

In Table I, the ratios are computed for evaluating the performance of stable return portfolio

during the time period of January- December 2018. Now, the first thing we could observe

from the figures of these ratios is that all these are positive in number. This shows that the

portfolio is giving an adequate amount of return and has performed really well. Individually,

the positive figure of Sharpe ratio and Treynor ratio of the stable return portfolio shows that

the investor has received some amount of return for the risk taken but it is not considered

good because the return received from the portfolio is below the risk free rate which stands at

0.72%. Lastly, the computed alpha of stable return portfolio has shown that the portfolio had

outperformed the market. Higher alphas are always considered to be good and acceptable.

9

α = Rp- CAPM

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table I: Performance measure of Stable Return Portfolio

Performance Measures of Stable Return

Portfolio

Sharpe Ratio 0.15

Treynor Ratio 0.18

Jensen's Ratio 0.25

Performance Measure of High Return Portfolio

In Table J, the ratios are computed for evaluating the performance of high return portfolio.

Now if we look at the performance of high return portfolio then all the three ratios are

positive. Individually, as per Sharpe ratio which considers only the systematic risk, the

portfolio had given the return as expected because the return received is much higher than the

return given by the risk free securities (0.72%). However, as per Treynor ratio, which

considers both systematic risk and unsystematic risk, is not so impressive. Jensen’s alpha of

the company is positive from where we may interpret that this portfolio had performed well.

Considering, Jenson’s alpha and Sharpe ratio of High return portfolio we could see the

potential of the investment portfolio to outperform the market.

Table J: Performance measure of High Return Portfolio

Performance Measures of High Return Portfolio

Sharpe Ratio 1.84

Treynor Ratio 0.42

Jensen's Ratio 0.61

Portfolio Comparison on the basis of Performance Measures

On comparing the two portfolios, we could see from Table K that high return portfolio had

performed much better than the stable return portfolio. Individually, the Sharpe ratio of high

return portfolio is 1.84 where the same ratio of stable return portfolio is only 0.15 which is

very minimal. This means that the systematic risk or market risk is more in high return

portfolio than stable return portfolio as a result of which the investors of high return stock can

10

Performance Measures of Stable Return

Portfolio

Sharpe Ratio 0.15

Treynor Ratio 0.18

Jensen's Ratio 0.25

Performance Measure of High Return Portfolio

In Table J, the ratios are computed for evaluating the performance of high return portfolio.

Now if we look at the performance of high return portfolio then all the three ratios are

positive. Individually, as per Sharpe ratio which considers only the systematic risk, the

portfolio had given the return as expected because the return received is much higher than the

return given by the risk free securities (0.72%). However, as per Treynor ratio, which

considers both systematic risk and unsystematic risk, is not so impressive. Jensen’s alpha of

the company is positive from where we may interpret that this portfolio had performed well.

Considering, Jenson’s alpha and Sharpe ratio of High return portfolio we could see the

potential of the investment portfolio to outperform the market.

Table J: Performance measure of High Return Portfolio

Performance Measures of High Return Portfolio

Sharpe Ratio 1.84

Treynor Ratio 0.42

Jensen's Ratio 0.61

Portfolio Comparison on the basis of Performance Measures

On comparing the two portfolios, we could see from Table K that high return portfolio had

performed much better than the stable return portfolio. Individually, the Sharpe ratio of high

return portfolio is 1.84 where the same ratio of stable return portfolio is only 0.15 which is

very minimal. This means that the systematic risk or market risk is more in high return

portfolio than stable return portfolio as a result of which the investors of high return stock can

10

expect a bigger sum of return. Now, Treynor ratio of high return portfolio is 0.42 and stable

return portfolio is just 0.18. This shows that the investors of high return portfolio can expect a

bigger compensation amount for the taking the risk over those who had invested in stable

return portfolio. Lastly, the Jensen’s alpha of high return portfolio is 100% higher than the

stable return portfolio which shows the potential of high return investment portfolio to

outperform the market.

3. Performance of Portfolios in January-February 2019

We could notice in Table K, that the expected return of high return portfolio is higher than

that of stable return portfolio. As per the portfolio theory, an investor of high return portfolio

always expects a higher return as a reward for taking more risk.

We know, that the portfolio formed for the purpose of getting a stable return possess a lower

risk than the portfolio formed for the getting a higher return. Here too we could see the risk

on higher return portfolio is 2% whereas the risk on stable return portfolio is only 1%.

Table K: Expected return and risk of portfolios

Jan- Feb 2019 Stable Return Portfolio

High Return

Portfolio

Expected return -0.03% 0.29%

Standard Deviation of

portfolio 1% 2%

4. Limitation of the Study

There are 100 companies listed on Financial Times Stock Exchange 100 Index, the reason for

which it was not possible to calculate the return for each of the stock to select high return and

stable return portfolio. Therefore, we calculated the returns of only few stocks to select the

stock for stable return and high return portfolio construction. Here the stocks are not selected

from the different sectors to form the portfolios because the requirement was to form the

portfolios using risk and return concept. Generally, if there is a high correlation between two

or three sectors, then the risk of loss is on a higher side. Say for example, if one sector got

adversely affected by any systematic risk and the companies operating in that sector had to

face a heavy drop in their share prices. In such cases, the other sectors having a positive

correlation with the systematic risk affected sector will also notice a drop in the share prices

11

return portfolio is just 0.18. This shows that the investors of high return portfolio can expect a

bigger compensation amount for the taking the risk over those who had invested in stable

return portfolio. Lastly, the Jensen’s alpha of high return portfolio is 100% higher than the

stable return portfolio which shows the potential of high return investment portfolio to

outperform the market.

3. Performance of Portfolios in January-February 2019

We could notice in Table K, that the expected return of high return portfolio is higher than

that of stable return portfolio. As per the portfolio theory, an investor of high return portfolio

always expects a higher return as a reward for taking more risk.

We know, that the portfolio formed for the purpose of getting a stable return possess a lower

risk than the portfolio formed for the getting a higher return. Here too we could see the risk

on higher return portfolio is 2% whereas the risk on stable return portfolio is only 1%.

Table K: Expected return and risk of portfolios

Jan- Feb 2019 Stable Return Portfolio

High Return

Portfolio

Expected return -0.03% 0.29%

Standard Deviation of

portfolio 1% 2%

4. Limitation of the Study

There are 100 companies listed on Financial Times Stock Exchange 100 Index, the reason for

which it was not possible to calculate the return for each of the stock to select high return and

stable return portfolio. Therefore, we calculated the returns of only few stocks to select the

stock for stable return and high return portfolio construction. Here the stocks are not selected

from the different sectors to form the portfolios because the requirement was to form the

portfolios using risk and return concept. Generally, if there is a high correlation between two

or three sectors, then the risk of loss is on a higher side. Say for example, if one sector got

adversely affected by any systematic risk and the companies operating in that sector had to

face a heavy drop in their share prices. In such cases, the other sectors having a positive

correlation with the systematic risk affected sector will also notice a drop in the share prices

11

because of the same systematic risk. So, at the time of forming portfolio it is always advisable

to include the stocks from different sectors with no correlation between them.

5. Conclusion

So before taking an investment decision each of the stocks, their sectors, risk, return etc. are

properly evaluated in order to avoid the risk of loss. The investors try to diversify their risk

with the help of forming a good portfolio and this concept of forming a portfolio for risk

diversification was given by Harry Markowitz. The investors with a low risk appetite prefer

to invest in a stable risk portfolio and the investors with a high risk appetite go for high risk

portfolio. We chose two separate portfolios for both types of investors wherein we found that

the performance of the portfolio do not solely depends upon the return but it also relies on the

risk. The performance of the portfolios is also measured by the investors with the help of the

tools like Sharpe ratios, Treynor ratio and Jensen’s alpha. These ratios are even used by the

management of the company to access the ability of the portfolio manager. The performance

of the portfolio also depends upon the market condition as a result of which both the

portfolios gave a desirable performance in the year 2018 however the same portfolio

responded in a negative manner in the year 2019. Therefore, portfolio helps in diversifying

the risk however there are certain factors which could never be controlled and thereby risk

cannot be eliminated completely.

12

to include the stocks from different sectors with no correlation between them.

5. Conclusion

So before taking an investment decision each of the stocks, their sectors, risk, return etc. are

properly evaluated in order to avoid the risk of loss. The investors try to diversify their risk

with the help of forming a good portfolio and this concept of forming a portfolio for risk

diversification was given by Harry Markowitz. The investors with a low risk appetite prefer

to invest in a stable risk portfolio and the investors with a high risk appetite go for high risk

portfolio. We chose two separate portfolios for both types of investors wherein we found that

the performance of the portfolio do not solely depends upon the return but it also relies on the

risk. The performance of the portfolios is also measured by the investors with the help of the

tools like Sharpe ratios, Treynor ratio and Jensen’s alpha. These ratios are even used by the

management of the company to access the ability of the portfolio manager. The performance

of the portfolio also depends upon the market condition as a result of which both the

portfolios gave a desirable performance in the year 2018 however the same portfolio

responded in a negative manner in the year 2019. Therefore, portfolio helps in diversifying

the risk however there are certain factors which could never be controlled and thereby risk

cannot be eliminated completely.

12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Benhamou, E., And Guez, B. (2018).Incremental Sharpe and other performance ratios. [Online].

Available 27 May, 2019 https://arxiv.org/pdf/1807.09864.pdf.

Cleartax.(2018). Treynor Ratio: Meaning, calculation, how to use it and more. [Online]. Available 27

May, 2019 https://cleartax.in/s/treynor-ratio.

forbes.com.(2019).8 Strategies That Offer High Return With Low Risk. [Online]. Available 27 May,

2019 https://www.forbes.com/sites/jrose/2016/06/23/8-strategies-that-offer-high-return-with-low-

risk/.

Hawley, J., And Lukomnik, J. (2018).The third, systems stage of corporate governance: Why

institutional investors need to move beyond modern portfolio theory. [Online]. Available 27 May,

2019

https://www.researchgate.net/profile/James_Hawley2/publication/323323162_The_third_systems_

stage_of_corporate_governance_Why_institutional_investors_need_to_move_beyond_modern_po

rtfolio_theory/links/5a8e058daca272c56bc408c8/The-third-systems-stage-of-corporate-

governance-Why-institutional-investors-need-to-move-beyond-modern-portfolio-theory.pdf.

Morningstar.(2012).Are Your Fund’s Returns Worth the Risk?. [Online]. Available 27 May, 2019

https://www.morningstar.in/posts/9320/are-your-funds-returns-worth-the-risk.aspx.

U.S.News.(2018).What is modern portfolio theory?. [Online]. Available 27 May, 2019

https://money.usnews.com/investing/buy-and-hold-strategy/articles/2018-01-12/what-is-modern-

portfolio-theory.

Wu, Y. (2007 Performance Measurement. [Online]. Available 27 May, 2019

https://homepage.univie.ac.at/youchang.wu/5.pdf.

13

Benhamou, E., And Guez, B. (2018).Incremental Sharpe and other performance ratios. [Online].

Available 27 May, 2019 https://arxiv.org/pdf/1807.09864.pdf.

Cleartax.(2018). Treynor Ratio: Meaning, calculation, how to use it and more. [Online]. Available 27

May, 2019 https://cleartax.in/s/treynor-ratio.

forbes.com.(2019).8 Strategies That Offer High Return With Low Risk. [Online]. Available 27 May,

2019 https://www.forbes.com/sites/jrose/2016/06/23/8-strategies-that-offer-high-return-with-low-

risk/.

Hawley, J., And Lukomnik, J. (2018).The third, systems stage of corporate governance: Why

institutional investors need to move beyond modern portfolio theory. [Online]. Available 27 May,

2019

https://www.researchgate.net/profile/James_Hawley2/publication/323323162_The_third_systems_

stage_of_corporate_governance_Why_institutional_investors_need_to_move_beyond_modern_po

rtfolio_theory/links/5a8e058daca272c56bc408c8/The-third-systems-stage-of-corporate-

governance-Why-institutional-investors-need-to-move-beyond-modern-portfolio-theory.pdf.

Morningstar.(2012).Are Your Fund’s Returns Worth the Risk?. [Online]. Available 27 May, 2019

https://www.morningstar.in/posts/9320/are-your-funds-returns-worth-the-risk.aspx.

U.S.News.(2018).What is modern portfolio theory?. [Online]. Available 27 May, 2019

https://money.usnews.com/investing/buy-and-hold-strategy/articles/2018-01-12/what-is-modern-

portfolio-theory.

Wu, Y. (2007 Performance Measurement. [Online]. Available 27 May, 2019

https://homepage.univie.ac.at/youchang.wu/5.pdf.

13

Appendix

14

14

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.