Finance Portfolio Management

VerifiedAdded on 2023/03/20

|12

|2430

|77

AI Summary

This report provides information about investment strategies and portfolio management in finance. It covers topics such as calculating returns, variances, and correlations for stocks and index, analyzing portfolio performance and risk, and detecting limitations of the analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE PORTFOLIO MANAGEMENT

Finance Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Finance Portfolio Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE PORTFOLIO MANAGEMENT

1

Table of Contents

Introduction:...............................................................................................................................2

Part 1:.........................................................................................................................................2

a. Calculating the discrete return, arithmetic return and geometric returns for the stock:.........2

b. Calculating the variance returns of each stock with covariance and correlation coefficients:

....................................................................................................................................................3

c. Comparing the results, while indicating about the events that took place during the period:3

Part 2:.........................................................................................................................................4

a. Computing the weekly rate of return and variance of an equally weighted portfolio:...........4

b. Examining and comparing the pattern of the returns of the portfolio with those of the

individual stocks and stock index, while comparing the variances:..........................................5

Part 3:.........................................................................................................................................5

a. Converting the yields to weekly numbers:.............................................................................5

b. Computing beta and Jensen’s Alpha for each stock:.............................................................6

c. Calculating total risk of the portfolio, while partitioning the risk on the basis of systematic

and unsystematic risk:................................................................................................................6

d. Commenting on the stock and portfolio performance:..........................................................7

Part 4: Indicating how useful was the analysis, while detecting the limitations of the analysis7

Conclusion:................................................................................................................................8

References and Bibliography:....................................................................................................9

1

Table of Contents

Introduction:...............................................................................................................................2

Part 1:.........................................................................................................................................2

a. Calculating the discrete return, arithmetic return and geometric returns for the stock:.........2

b. Calculating the variance returns of each stock with covariance and correlation coefficients:

....................................................................................................................................................3

c. Comparing the results, while indicating about the events that took place during the period:3

Part 2:.........................................................................................................................................4

a. Computing the weekly rate of return and variance of an equally weighted portfolio:...........4

b. Examining and comparing the pattern of the returns of the portfolio with those of the

individual stocks and stock index, while comparing the variances:..........................................5

Part 3:.........................................................................................................................................5

a. Converting the yields to weekly numbers:.............................................................................5

b. Computing beta and Jensen’s Alpha for each stock:.............................................................6

c. Calculating total risk of the portfolio, while partitioning the risk on the basis of systematic

and unsystematic risk:................................................................................................................6

d. Commenting on the stock and portfolio performance:..........................................................7

Part 4: Indicating how useful was the analysis, while detecting the limitations of the analysis7

Conclusion:................................................................................................................................8

References and Bibliography:....................................................................................................9

FINANCE PORTFOLIO MANAGEMENT

2

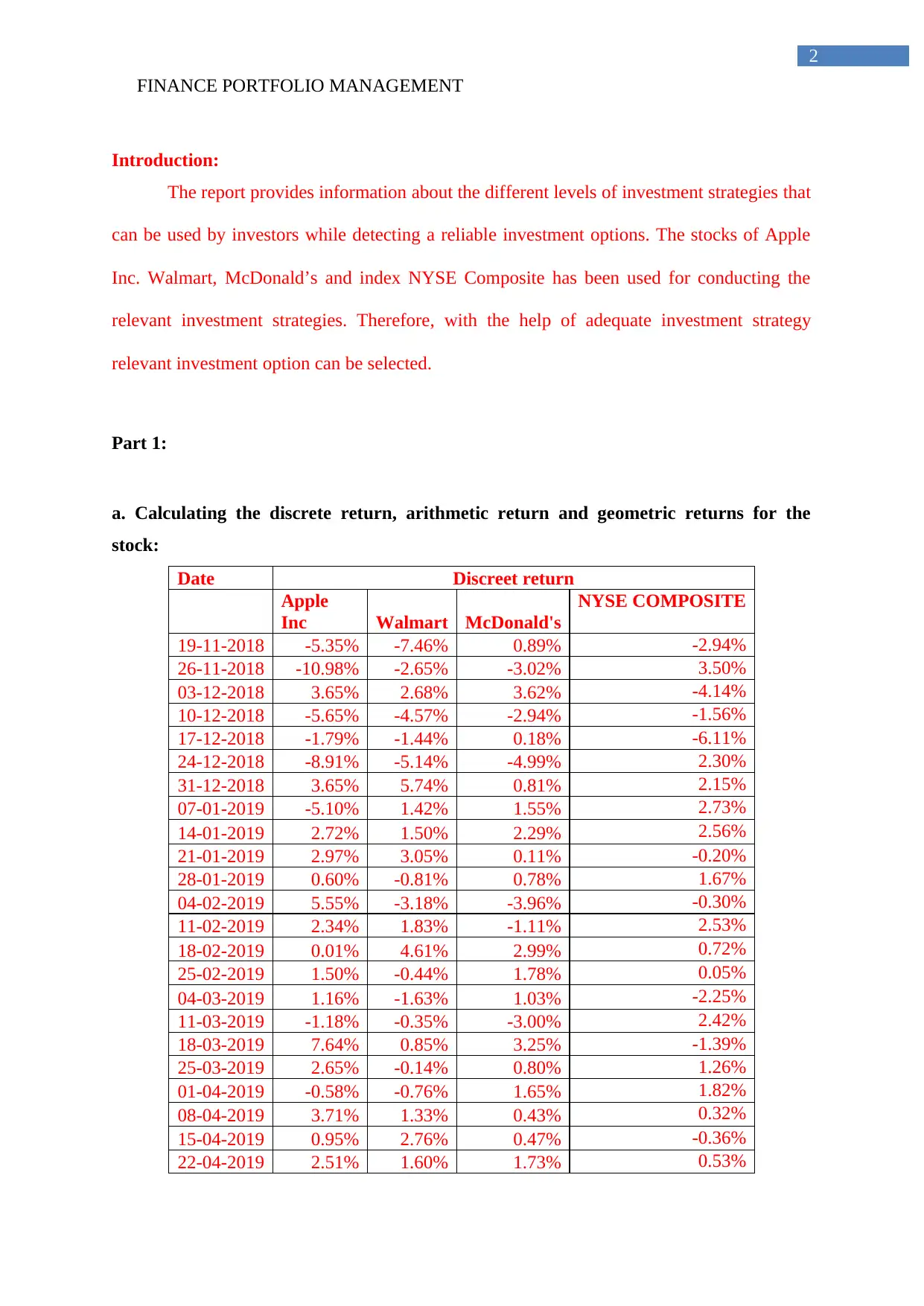

Introduction:

The report provides information about the different levels of investment strategies that

can be used by investors while detecting a reliable investment options. The stocks of Apple

Inc. Walmart, McDonald’s and index NYSE Composite has been used for conducting the

relevant investment strategies. Therefore, with the help of adequate investment strategy

relevant investment option can be selected.

Part 1:

a. Calculating the discrete return, arithmetic return and geometric returns for the

stock:

Date Discreet return

Apple

Inc Walmart McDonald's

NYSE COMPOSITE

19-11-2018 -5.35% -7.46% 0.89% -2.94%

26-11-2018 -10.98% -2.65% -3.02% 3.50%

03-12-2018 3.65% 2.68% 3.62% -4.14%

10-12-2018 -5.65% -4.57% -2.94% -1.56%

17-12-2018 -1.79% -1.44% 0.18% -6.11%

24-12-2018 -8.91% -5.14% -4.99% 2.30%

31-12-2018 3.65% 5.74% 0.81% 2.15%

07-01-2019 -5.10% 1.42% 1.55% 2.73%

14-01-2019 2.72% 1.50% 2.29% 2.56%

21-01-2019 2.97% 3.05% 0.11% -0.20%

28-01-2019 0.60% -0.81% 0.78% 1.67%

04-02-2019 5.55% -3.18% -3.96% -0.30%

11-02-2019 2.34% 1.83% -1.11% 2.53%

18-02-2019 0.01% 4.61% 2.99% 0.72%

25-02-2019 1.50% -0.44% 1.78% 0.05%

04-03-2019 1.16% -1.63% 1.03% -2.25%

11-03-2019 -1.18% -0.35% -3.00% 2.42%

18-03-2019 7.64% 0.85% 3.25% -1.39%

25-03-2019 2.65% -0.14% 0.80% 1.26%

01-04-2019 -0.58% -0.76% 1.65% 1.82%

08-04-2019 3.71% 1.33% 0.43% 0.32%

15-04-2019 0.95% 2.76% 0.47% -0.36%

22-04-2019 2.51% 1.60% 1.73% 0.53%

2

Introduction:

The report provides information about the different levels of investment strategies that

can be used by investors while detecting a reliable investment options. The stocks of Apple

Inc. Walmart, McDonald’s and index NYSE Composite has been used for conducting the

relevant investment strategies. Therefore, with the help of adequate investment strategy

relevant investment option can be selected.

Part 1:

a. Calculating the discrete return, arithmetic return and geometric returns for the

stock:

Date Discreet return

Apple

Inc Walmart McDonald's

NYSE COMPOSITE

19-11-2018 -5.35% -7.46% 0.89% -2.94%

26-11-2018 -10.98% -2.65% -3.02% 3.50%

03-12-2018 3.65% 2.68% 3.62% -4.14%

10-12-2018 -5.65% -4.57% -2.94% -1.56%

17-12-2018 -1.79% -1.44% 0.18% -6.11%

24-12-2018 -8.91% -5.14% -4.99% 2.30%

31-12-2018 3.65% 5.74% 0.81% 2.15%

07-01-2019 -5.10% 1.42% 1.55% 2.73%

14-01-2019 2.72% 1.50% 2.29% 2.56%

21-01-2019 2.97% 3.05% 0.11% -0.20%

28-01-2019 0.60% -0.81% 0.78% 1.67%

04-02-2019 5.55% -3.18% -3.96% -0.30%

11-02-2019 2.34% 1.83% -1.11% 2.53%

18-02-2019 0.01% 4.61% 2.99% 0.72%

25-02-2019 1.50% -0.44% 1.78% 0.05%

04-03-2019 1.16% -1.63% 1.03% -2.25%

11-03-2019 -1.18% -0.35% -3.00% 2.42%

18-03-2019 7.64% 0.85% 3.25% -1.39%

25-03-2019 2.65% -0.14% 0.80% 1.26%

01-04-2019 -0.58% -0.76% 1.65% 1.82%

08-04-2019 3.71% 1.33% 0.43% 0.32%

15-04-2019 0.95% 2.76% 0.47% -0.36%

22-04-2019 2.51% 1.60% 1.73% 0.53%

FINANCE PORTFOLIO MANAGEMENT

3

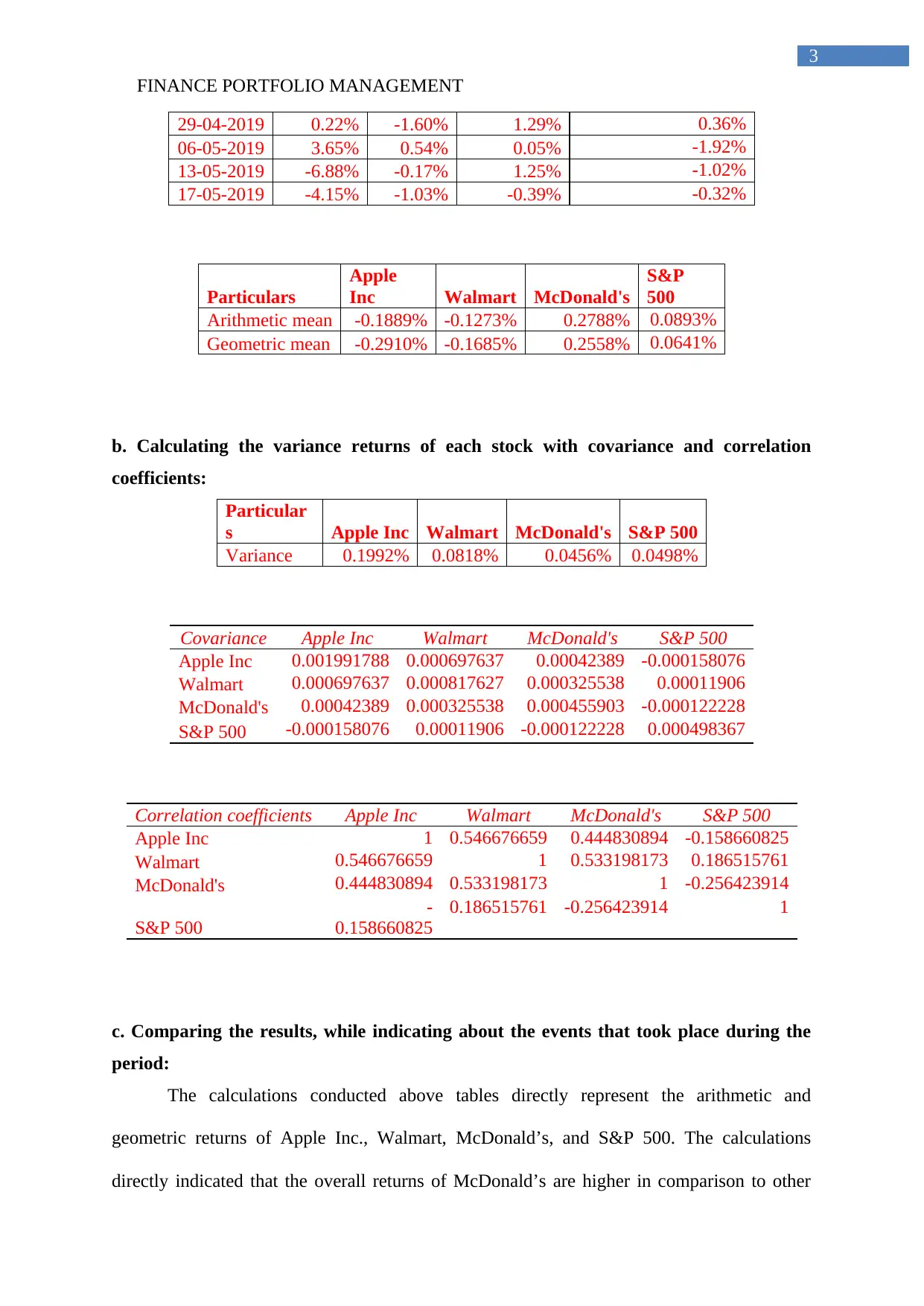

29-04-2019 0.22% -1.60% 1.29% 0.36%

06-05-2019 3.65% 0.54% 0.05% -1.92%

13-05-2019 -6.88% -0.17% 1.25% -1.02%

17-05-2019 -4.15% -1.03% -0.39% -0.32%

Particulars

Apple

Inc Walmart McDonald's

S&P

500

Arithmetic mean -0.1889% -0.1273% 0.2788% 0.0893%

Geometric mean -0.2910% -0.1685% 0.2558% 0.0641%

b. Calculating the variance returns of each stock with covariance and correlation

coefficients:

Particular

s Apple Inc Walmart McDonald's S&P 500

Variance 0.1992% 0.0818% 0.0456% 0.0498%

Covariance Apple Inc Walmart McDonald's S&P 500

Apple Inc 0.001991788 0.000697637 0.00042389 -0.000158076

Walmart 0.000697637 0.000817627 0.000325538 0.00011906

McDonald's 0.00042389 0.000325538 0.000455903 -0.000122228

S&P 500 -0.000158076 0.00011906 -0.000122228 0.000498367

Correlation coefficients Apple Inc Walmart McDonald's S&P 500

Apple Inc 1 0.546676659 0.444830894 -0.158660825

Walmart 0.546676659 1 0.533198173 0.186515761

McDonald's 0.444830894 0.533198173 1 -0.256423914

S&P 500

-

0.158660825

0.186515761 -0.256423914 1

c. Comparing the results, while indicating about the events that took place during the

period:

The calculations conducted above tables directly represent the arithmetic and

geometric returns of Apple Inc., Walmart, McDonald’s, and S&P 500. The calculations

directly indicated that the overall returns of McDonald’s are higher in comparison to other

3

29-04-2019 0.22% -1.60% 1.29% 0.36%

06-05-2019 3.65% 0.54% 0.05% -1.92%

13-05-2019 -6.88% -0.17% 1.25% -1.02%

17-05-2019 -4.15% -1.03% -0.39% -0.32%

Particulars

Apple

Inc Walmart McDonald's

S&P

500

Arithmetic mean -0.1889% -0.1273% 0.2788% 0.0893%

Geometric mean -0.2910% -0.1685% 0.2558% 0.0641%

b. Calculating the variance returns of each stock with covariance and correlation

coefficients:

Particular

s Apple Inc Walmart McDonald's S&P 500

Variance 0.1992% 0.0818% 0.0456% 0.0498%

Covariance Apple Inc Walmart McDonald's S&P 500

Apple Inc 0.001991788 0.000697637 0.00042389 -0.000158076

Walmart 0.000697637 0.000817627 0.000325538 0.00011906

McDonald's 0.00042389 0.000325538 0.000455903 -0.000122228

S&P 500 -0.000158076 0.00011906 -0.000122228 0.000498367

Correlation coefficients Apple Inc Walmart McDonald's S&P 500

Apple Inc 1 0.546676659 0.444830894 -0.158660825

Walmart 0.546676659 1 0.533198173 0.186515761

McDonald's 0.444830894 0.533198173 1 -0.256423914

S&P 500

-

0.158660825

0.186515761 -0.256423914 1

c. Comparing the results, while indicating about the events that took place during the

period:

The calculations conducted above tables directly represent the arithmetic and

geometric returns of Apple Inc., Walmart, McDonald’s, and S&P 500. The calculations

directly indicated that the overall returns of McDonald’s are higher in comparison to other

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE PORTFOLIO MANAGEMENT

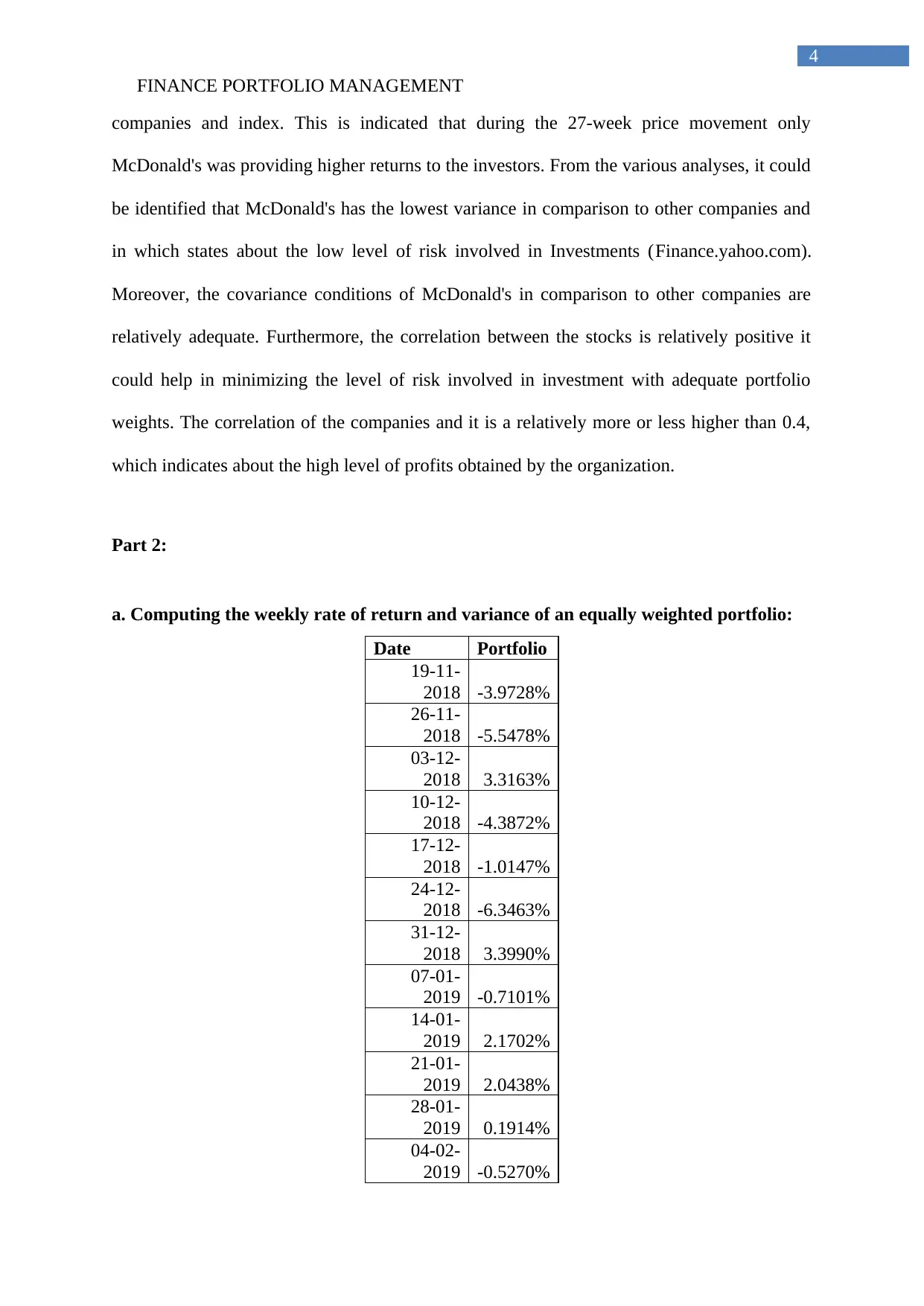

4

companies and index. This is indicated that during the 27-week price movement only

McDonald's was providing higher returns to the investors. From the various analyses, it could

be identified that McDonald's has the lowest variance in comparison to other companies and

in which states about the low level of risk involved in Investments (Finance.yahoo.com).

Moreover, the covariance conditions of McDonald's in comparison to other companies are

relatively adequate. Furthermore, the correlation between the stocks is relatively positive it

could help in minimizing the level of risk involved in investment with adequate portfolio

weights. The correlation of the companies and it is a relatively more or less higher than 0.4,

which indicates about the high level of profits obtained by the organization.

Part 2:

a. Computing the weekly rate of return and variance of an equally weighted portfolio:

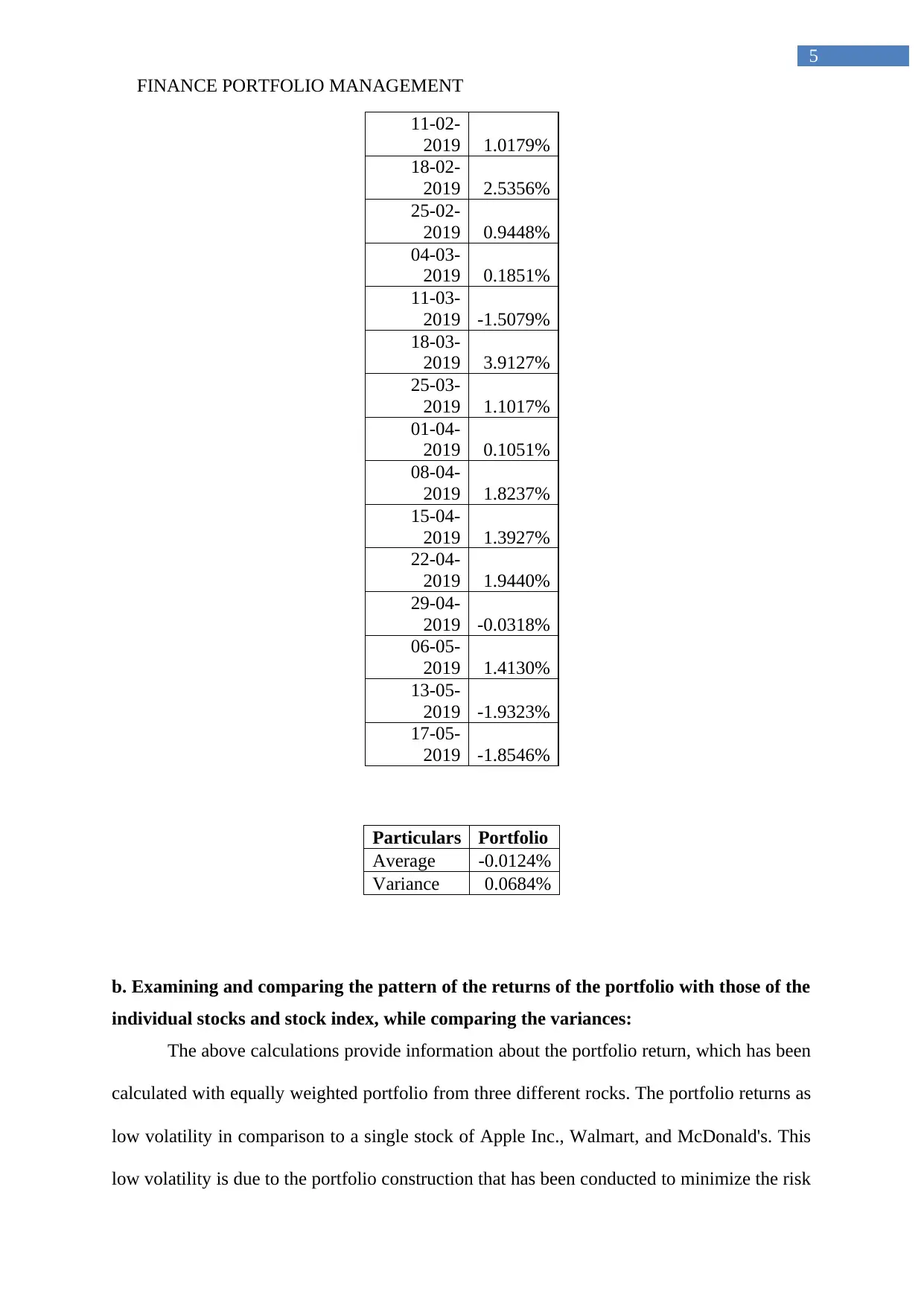

Date Portfolio

19-11-

2018 -3.9728%

26-11-

2018 -5.5478%

03-12-

2018 3.3163%

10-12-

2018 -4.3872%

17-12-

2018 -1.0147%

24-12-

2018 -6.3463%

31-12-

2018 3.3990%

07-01-

2019 -0.7101%

14-01-

2019 2.1702%

21-01-

2019 2.0438%

28-01-

2019 0.1914%

04-02-

2019 -0.5270%

4

companies and index. This is indicated that during the 27-week price movement only

McDonald's was providing higher returns to the investors. From the various analyses, it could

be identified that McDonald's has the lowest variance in comparison to other companies and

in which states about the low level of risk involved in Investments (Finance.yahoo.com).

Moreover, the covariance conditions of McDonald's in comparison to other companies are

relatively adequate. Furthermore, the correlation between the stocks is relatively positive it

could help in minimizing the level of risk involved in investment with adequate portfolio

weights. The correlation of the companies and it is a relatively more or less higher than 0.4,

which indicates about the high level of profits obtained by the organization.

Part 2:

a. Computing the weekly rate of return and variance of an equally weighted portfolio:

Date Portfolio

19-11-

2018 -3.9728%

26-11-

2018 -5.5478%

03-12-

2018 3.3163%

10-12-

2018 -4.3872%

17-12-

2018 -1.0147%

24-12-

2018 -6.3463%

31-12-

2018 3.3990%

07-01-

2019 -0.7101%

14-01-

2019 2.1702%

21-01-

2019 2.0438%

28-01-

2019 0.1914%

04-02-

2019 -0.5270%

FINANCE PORTFOLIO MANAGEMENT

5

11-02-

2019 1.0179%

18-02-

2019 2.5356%

25-02-

2019 0.9448%

04-03-

2019 0.1851%

11-03-

2019 -1.5079%

18-03-

2019 3.9127%

25-03-

2019 1.1017%

01-04-

2019 0.1051%

08-04-

2019 1.8237%

15-04-

2019 1.3927%

22-04-

2019 1.9440%

29-04-

2019 -0.0318%

06-05-

2019 1.4130%

13-05-

2019 -1.9323%

17-05-

2019 -1.8546%

Particulars Portfolio

Average -0.0124%

Variance 0.0684%

b. Examining and comparing the pattern of the returns of the portfolio with those of the

individual stocks and stock index, while comparing the variances:

The above calculations provide information about the portfolio return, which has been

calculated with equally weighted portfolio from three different rocks. The portfolio returns as

low volatility in comparison to a single stock of Apple Inc., Walmart, and McDonald's. This

low volatility is due to the portfolio construction that has been conducted to minimize the risk

5

11-02-

2019 1.0179%

18-02-

2019 2.5356%

25-02-

2019 0.9448%

04-03-

2019 0.1851%

11-03-

2019 -1.5079%

18-03-

2019 3.9127%

25-03-

2019 1.1017%

01-04-

2019 0.1051%

08-04-

2019 1.8237%

15-04-

2019 1.3927%

22-04-

2019 1.9440%

29-04-

2019 -0.0318%

06-05-

2019 1.4130%

13-05-

2019 -1.9323%

17-05-

2019 -1.8546%

Particulars Portfolio

Average -0.0124%

Variance 0.0684%

b. Examining and comparing the pattern of the returns of the portfolio with those of the

individual stocks and stock index, while comparing the variances:

The above calculations provide information about the portfolio return, which has been

calculated with equally weighted portfolio from three different rocks. The portfolio returns as

low volatility in comparison to a single stock of Apple Inc., Walmart, and McDonald's. This

low volatility is due to the portfolio construction that has been conducted to minimize the risk

FINANCE PORTFOLIO MANAGEMENT

6

and improve returns from the investment. For single stock, it could be identified that the

overall variance is a relatively high which indicates about the risk involved in investment.

However, the portfolio variance is relatively low in comparison to other stocks listed in the

above table, which is due to the adequate diversification that has been conducted to nullify

the relevant impact from capital market. Hence, with diversify portfolio investors can reduce

the risk and losses from stock market (Wsj.com).

Part 3:

a. Converting the yields to weekly numbers:

Particulars Value

Treasury bill 2.46%

Risk free rate 1.23%

b. Computing beta and Jensen’s Alpha for each stock:

Excess returns

Date Apple Inc Walmart McDonald's NYSE COMPOSITE Portfolio

19-11-

2018 -6.5804% -8.6855% -0.3426%

-4.1657%

-5.2028%

26-11-

2018 -12.2050% -3.8812% -4.2472%

2.2703%

-6.7778%

03-12-

2018 2.4208% 1.4514% 2.3868%

-5.3690%

2.0863%

10-12-

2018 -6.8801% -5.7973% -4.1741%

-2.7921%

-5.6172%

17-12-

2018 -3.0165% -2.6679% -1.0496%

-7.3424%

-2.2447%

24-12-

2018 -10.1435% -6.3688% -6.2166%

1.0724%

-7.5763%

31-12-

2018 2.4189% 4.5086% -0.4204%

0.9168%

2.1690%

07-01-

2019 -6.3315% 0.1919% 0.3193%

1.4984%

-1.9401%

14-01-

2019 1.4882% 0.2683% 1.0641%

1.3338%

0.9402%

21-01-

2019 1.7446% 1.8172% -1.1203%

-1.4318%

0.8138%

6

and improve returns from the investment. For single stock, it could be identified that the

overall variance is a relatively high which indicates about the risk involved in investment.

However, the portfolio variance is relatively low in comparison to other stocks listed in the

above table, which is due to the adequate diversification that has been conducted to nullify

the relevant impact from capital market. Hence, with diversify portfolio investors can reduce

the risk and losses from stock market (Wsj.com).

Part 3:

a. Converting the yields to weekly numbers:

Particulars Value

Treasury bill 2.46%

Risk free rate 1.23%

b. Computing beta and Jensen’s Alpha for each stock:

Excess returns

Date Apple Inc Walmart McDonald's NYSE COMPOSITE Portfolio

19-11-

2018 -6.5804% -8.6855% -0.3426%

-4.1657%

-5.2028%

26-11-

2018 -12.2050% -3.8812% -4.2472%

2.2703%

-6.7778%

03-12-

2018 2.4208% 1.4514% 2.3868%

-5.3690%

2.0863%

10-12-

2018 -6.8801% -5.7973% -4.1741%

-2.7921%

-5.6172%

17-12-

2018 -3.0165% -2.6679% -1.0496%

-7.3424%

-2.2447%

24-12-

2018 -10.1435% -6.3688% -6.2166%

1.0724%

-7.5763%

31-12-

2018 2.4189% 4.5086% -0.4204%

0.9168%

2.1690%

07-01-

2019 -6.3315% 0.1919% 0.3193%

1.4984%

-1.9401%

14-01-

2019 1.4882% 0.2683% 1.0641%

1.3338%

0.9402%

21-01-

2019 1.7446% 1.8172% -1.1203%

-1.4318%

0.8138%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE PORTFOLIO MANAGEMENT

7

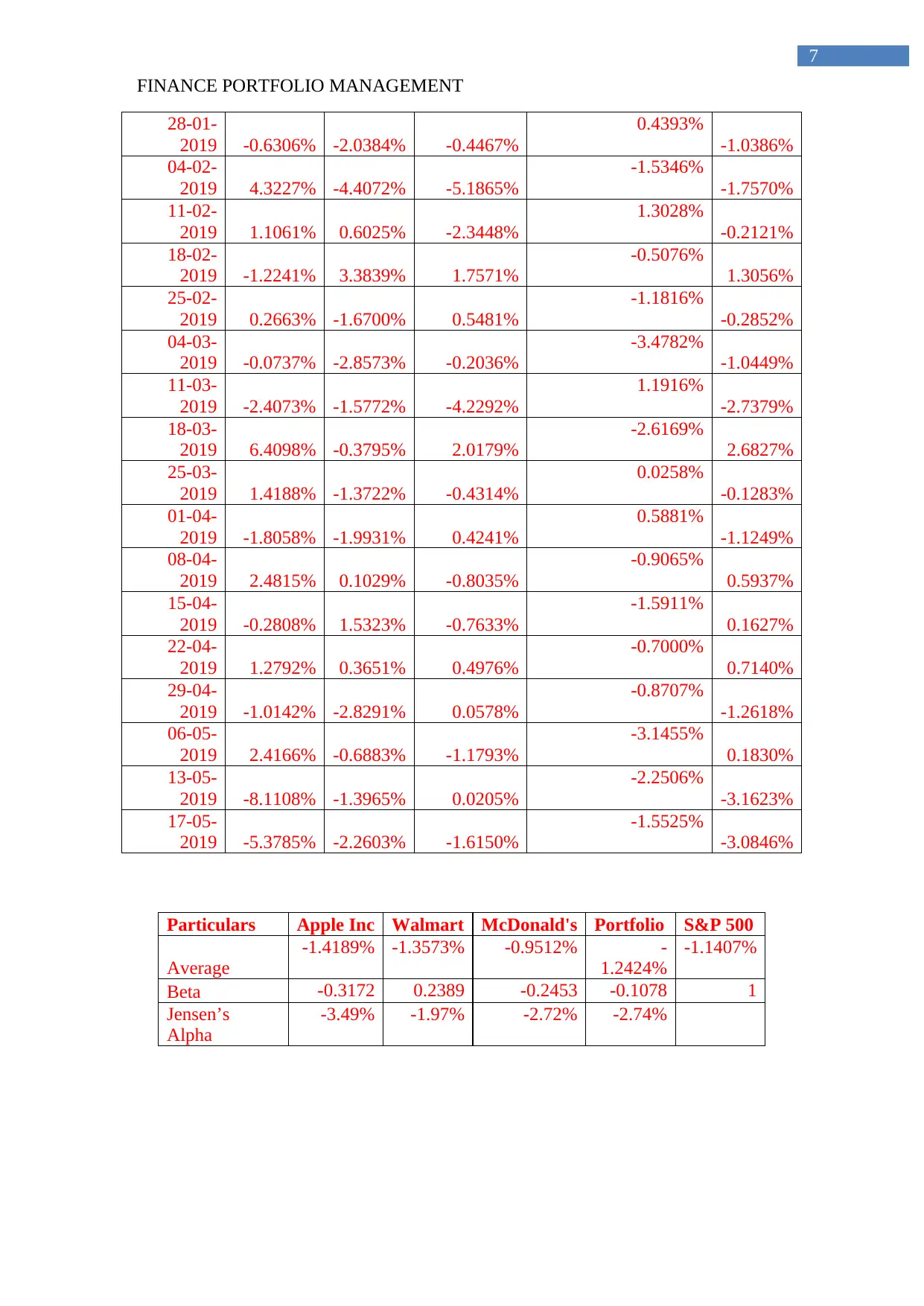

28-01-

2019 -0.6306% -2.0384% -0.4467%

0.4393%

-1.0386%

04-02-

2019 4.3227% -4.4072% -5.1865%

-1.5346%

-1.7570%

11-02-

2019 1.1061% 0.6025% -2.3448%

1.3028%

-0.2121%

18-02-

2019 -1.2241% 3.3839% 1.7571%

-0.5076%

1.3056%

25-02-

2019 0.2663% -1.6700% 0.5481%

-1.1816%

-0.2852%

04-03-

2019 -0.0737% -2.8573% -0.2036%

-3.4782%

-1.0449%

11-03-

2019 -2.4073% -1.5772% -4.2292%

1.1916%

-2.7379%

18-03-

2019 6.4098% -0.3795% 2.0179%

-2.6169%

2.6827%

25-03-

2019 1.4188% -1.3722% -0.4314%

0.0258%

-0.1283%

01-04-

2019 -1.8058% -1.9931% 0.4241%

0.5881%

-1.1249%

08-04-

2019 2.4815% 0.1029% -0.8035%

-0.9065%

0.5937%

15-04-

2019 -0.2808% 1.5323% -0.7633%

-1.5911%

0.1627%

22-04-

2019 1.2792% 0.3651% 0.4976%

-0.7000%

0.7140%

29-04-

2019 -1.0142% -2.8291% 0.0578%

-0.8707%

-1.2618%

06-05-

2019 2.4166% -0.6883% -1.1793%

-3.1455%

0.1830%

13-05-

2019 -8.1108% -1.3965% 0.0205%

-2.2506%

-3.1623%

17-05-

2019 -5.3785% -2.2603% -1.6150%

-1.5525%

-3.0846%

Particulars Apple Inc Walmart McDonald's Portfolio S&P 500

Average

-1.4189% -1.3573% -0.9512% -

1.2424%

-1.1407%

Beta -0.3172 0.2389 -0.2453 -0.1078 1

Jensen’s

Alpha

-3.49% -1.97% -2.72% -2.74%

7

28-01-

2019 -0.6306% -2.0384% -0.4467%

0.4393%

-1.0386%

04-02-

2019 4.3227% -4.4072% -5.1865%

-1.5346%

-1.7570%

11-02-

2019 1.1061% 0.6025% -2.3448%

1.3028%

-0.2121%

18-02-

2019 -1.2241% 3.3839% 1.7571%

-0.5076%

1.3056%

25-02-

2019 0.2663% -1.6700% 0.5481%

-1.1816%

-0.2852%

04-03-

2019 -0.0737% -2.8573% -0.2036%

-3.4782%

-1.0449%

11-03-

2019 -2.4073% -1.5772% -4.2292%

1.1916%

-2.7379%

18-03-

2019 6.4098% -0.3795% 2.0179%

-2.6169%

2.6827%

25-03-

2019 1.4188% -1.3722% -0.4314%

0.0258%

-0.1283%

01-04-

2019 -1.8058% -1.9931% 0.4241%

0.5881%

-1.1249%

08-04-

2019 2.4815% 0.1029% -0.8035%

-0.9065%

0.5937%

15-04-

2019 -0.2808% 1.5323% -0.7633%

-1.5911%

0.1627%

22-04-

2019 1.2792% 0.3651% 0.4976%

-0.7000%

0.7140%

29-04-

2019 -1.0142% -2.8291% 0.0578%

-0.8707%

-1.2618%

06-05-

2019 2.4166% -0.6883% -1.1793%

-3.1455%

0.1830%

13-05-

2019 -8.1108% -1.3965% 0.0205%

-2.2506%

-3.1623%

17-05-

2019 -5.3785% -2.2603% -1.6150%

-1.5525%

-3.0846%

Particulars Apple Inc Walmart McDonald's Portfolio S&P 500

Average

-1.4189% -1.3573% -0.9512% -

1.2424%

-1.1407%

Beta -0.3172 0.2389 -0.2453 -0.1078 1

Jensen’s

Alpha

-3.49% -1.97% -2.72% -2.74%

FINANCE PORTFOLIO MANAGEMENT

8

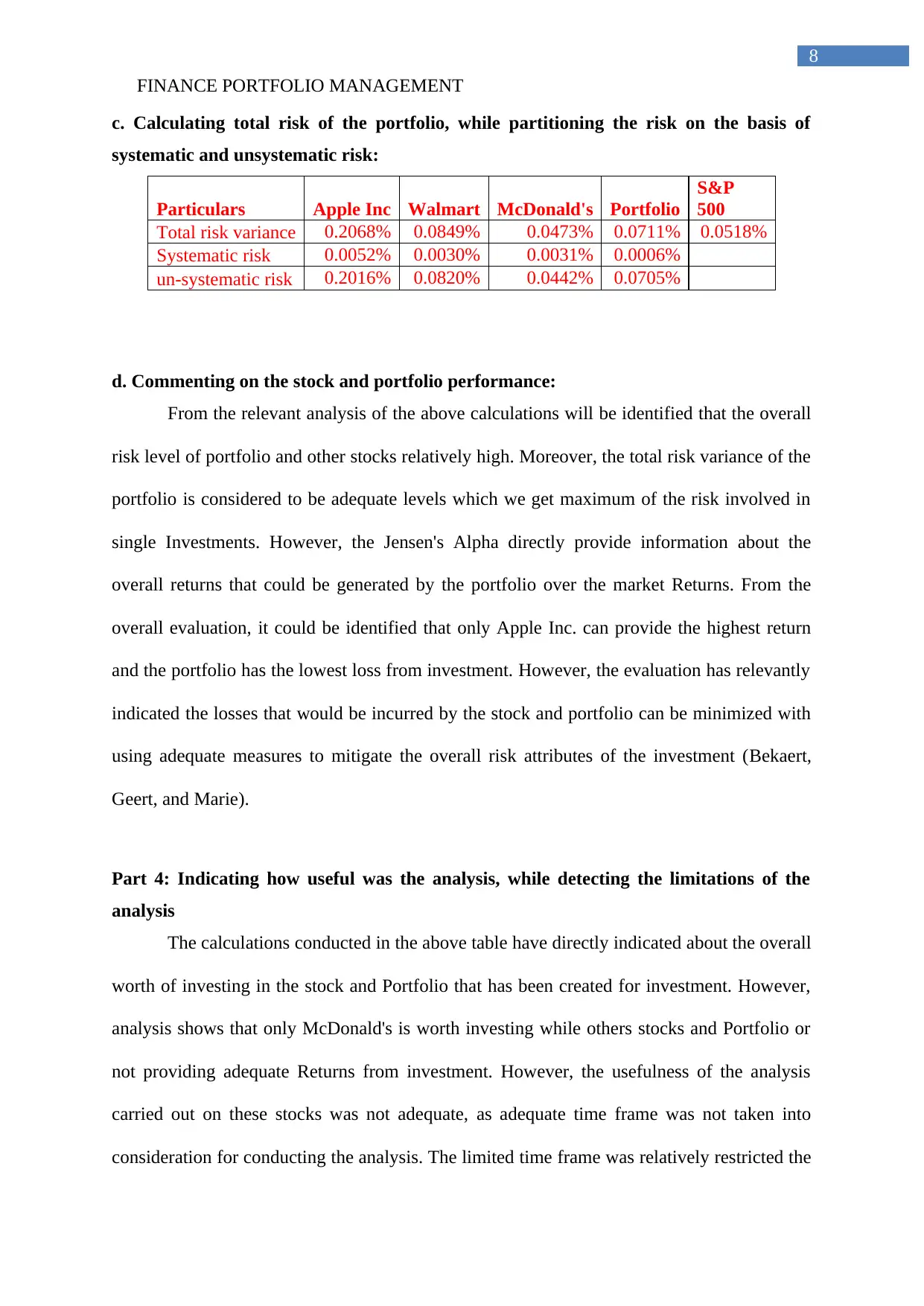

c. Calculating total risk of the portfolio, while partitioning the risk on the basis of

systematic and unsystematic risk:

Particulars Apple Inc Walmart McDonald's Portfolio

S&P

500

Total risk variance 0.2068% 0.0849% 0.0473% 0.0711% 0.0518%

Systematic risk 0.0052% 0.0030% 0.0031% 0.0006%

un-systematic risk 0.2016% 0.0820% 0.0442% 0.0705%

d. Commenting on the stock and portfolio performance:

From the relevant analysis of the above calculations will be identified that the overall

risk level of portfolio and other stocks relatively high. Moreover, the total risk variance of the

portfolio is considered to be adequate levels which we get maximum of the risk involved in

single Investments. However, the Jensen's Alpha directly provide information about the

overall returns that could be generated by the portfolio over the market Returns. From the

overall evaluation, it could be identified that only Apple Inc. can provide the highest return

and the portfolio has the lowest loss from investment. However, the evaluation has relevantly

indicated the losses that would be incurred by the stock and portfolio can be minimized with

using adequate measures to mitigate the overall risk attributes of the investment (Bekaert,

Geert, and Marie).

Part 4: Indicating how useful was the analysis, while detecting the limitations of the

analysis

The calculations conducted in the above table have directly indicated about the overall

worth of investing in the stock and Portfolio that has been created for investment. However,

analysis shows that only McDonald's is worth investing while others stocks and Portfolio or

not providing adequate Returns from investment. However, the usefulness of the analysis

carried out on these stocks was not adequate, as adequate time frame was not taken into

consideration for conducting the analysis. The limited time frame was relatively restricted the

8

c. Calculating total risk of the portfolio, while partitioning the risk on the basis of

systematic and unsystematic risk:

Particulars Apple Inc Walmart McDonald's Portfolio

S&P

500

Total risk variance 0.2068% 0.0849% 0.0473% 0.0711% 0.0518%

Systematic risk 0.0052% 0.0030% 0.0031% 0.0006%

un-systematic risk 0.2016% 0.0820% 0.0442% 0.0705%

d. Commenting on the stock and portfolio performance:

From the relevant analysis of the above calculations will be identified that the overall

risk level of portfolio and other stocks relatively high. Moreover, the total risk variance of the

portfolio is considered to be adequate levels which we get maximum of the risk involved in

single Investments. However, the Jensen's Alpha directly provide information about the

overall returns that could be generated by the portfolio over the market Returns. From the

overall evaluation, it could be identified that only Apple Inc. can provide the highest return

and the portfolio has the lowest loss from investment. However, the evaluation has relevantly

indicated the losses that would be incurred by the stock and portfolio can be minimized with

using adequate measures to mitigate the overall risk attributes of the investment (Bekaert,

Geert, and Marie).

Part 4: Indicating how useful was the analysis, while detecting the limitations of the

analysis

The calculations conducted in the above table have directly indicated about the overall

worth of investing in the stock and Portfolio that has been created for investment. However,

analysis shows that only McDonald's is worth investing while others stocks and Portfolio or

not providing adequate Returns from investment. However, the usefulness of the analysis

carried out on these stocks was not adequate, as adequate time frame was not taken into

consideration for conducting the analysis. The limited time frame was relatively restricted the

FINANCE PORTFOLIO MANAGEMENT

9

overall analysis of the stocks and detection of the risk and return involved in investments.

The major limitations were the time restrictions and the overall use of weekly returns for

analyzing the stocks risk and return attributes. Therefore, on the basis of the limitations no

investment should be conducted by investors, as the analysis failed to operate and capture the

risk and return attributes of a stock and portfolio (Fedsearch.org). Moreover, relevant changes

in the analysis could have been made, where the time frame of the analysis could increase to

more than two to three years, as it might help in protecting the actual risk and return

conditions of stock.

Conclusion:

The overall assessment directly evaluates different level of strategies such as Total

risk and Jensen Alpha to derive the adequate investment options. From the overall

calculation, it can be detected that only McDonald is a viable investment options in

comparison to other stock and portfolio. However, the limitations of the study have relevantly

restricted the viability of the analysis, which can be conducted for detecting the investment

option.

9

overall analysis of the stocks and detection of the risk and return involved in investments.

The major limitations were the time restrictions and the overall use of weekly returns for

analyzing the stocks risk and return attributes. Therefore, on the basis of the limitations no

investment should be conducted by investors, as the analysis failed to operate and capture the

risk and return attributes of a stock and portfolio (Fedsearch.org). Moreover, relevant changes

in the analysis could have been made, where the time frame of the analysis could increase to

more than two to three years, as it might help in protecting the actual risk and return

conditions of stock.

Conclusion:

The overall assessment directly evaluates different level of strategies such as Total

risk and Jensen Alpha to derive the adequate investment options. From the overall

calculation, it can be detected that only McDonald is a viable investment options in

comparison to other stock and portfolio. However, the limitations of the study have relevantly

restricted the viability of the analysis, which can be conducted for detecting the investment

option.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE PORTFOLIO MANAGEMENT

10

References and Bibliography:

Bekaert, Geert, and Marie Hoerova. "The VIX, the variance premium and stock market

volatility." Journal of Econometrics183, no. 2 (2014): 181-192.

Cremers, Martijn, Michael Halling, and David Weinbaum. "Aggregate jump and volatility

risk in the cross‐section of stock returns." The Journal of Finance 70, no. 2 (2015): 577-614.

Diaz, Elena Maria, Juan Carlos Molero, and Fernando Perez de Gracia. "Oil price volatility

and stock returns in the G7 economies." Energy Economics 54 (2016): 417-430.

Economy.com Analytics, Moody's. 2019. "United States Treasury Bills: 26-Week - High

Rate | Moody's Analytics". Economy.Com. Accessed May 20 2019.

https://www.economy.com/united-states/treasury-bills-26-week-high-rate.

Fedsearch.org. 2019. Fedsearch.Org. Accessed May 20 2019.

https://www.fedsearch.org/board_public/search?text=treasury+bill&Search=.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/WMT/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/AAPL/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/MCD/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

10

References and Bibliography:

Bekaert, Geert, and Marie Hoerova. "The VIX, the variance premium and stock market

volatility." Journal of Econometrics183, no. 2 (2014): 181-192.

Cremers, Martijn, Michael Halling, and David Weinbaum. "Aggregate jump and volatility

risk in the cross‐section of stock returns." The Journal of Finance 70, no. 2 (2015): 577-614.

Diaz, Elena Maria, Juan Carlos Molero, and Fernando Perez de Gracia. "Oil price volatility

and stock returns in the G7 economies." Energy Economics 54 (2016): 417-430.

Economy.com Analytics, Moody's. 2019. "United States Treasury Bills: 26-Week - High

Rate | Moody's Analytics". Economy.Com. Accessed May 20 2019.

https://www.economy.com/united-states/treasury-bills-26-week-high-rate.

Fedsearch.org. 2019. Fedsearch.Org. Accessed May 20 2019.

https://www.fedsearch.org/board_public/search?text=treasury+bill&Search=.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/WMT/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/AAPL/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

Finance.yahoo.com. 2019. Finance.Yahoo.Com. Accessed May 20 2019.

https://finance.yahoo.com/quote/MCD/history?

period1=1541010600&period2=1558290600&interval=1wk&filter=history&frequency=1wk.

FINANCE PORTFOLIO MANAGEMENT

11

Finance.yahoo.com. 2019. Yahoo is now part of Oath. [online] Available at:

https://finance.yahoo.com/quote/%5ENYA/history?

period1=1541961000&period2=1558377000&interval=1wk&filter=history&frequency=1wk

[Accessed 20 May 2019].

Wsj.com. 2019. Wsj.Com. Accessed May 20 2019.

http://www.wsj.com/mdc/public/page/2_3020-moneyrate.html.

11

Finance.yahoo.com. 2019. Yahoo is now part of Oath. [online] Available at:

https://finance.yahoo.com/quote/%5ENYA/history?

period1=1541961000&period2=1558377000&interval=1wk&filter=history&frequency=1wk

[Accessed 20 May 2019].

Wsj.com. 2019. Wsj.Com. Accessed May 20 2019.

http://www.wsj.com/mdc/public/page/2_3020-moneyrate.html.

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.