Finance Project 2

VerifiedAdded on 2022/12/27

|9

|1247

|1

AI Summary

This document discusses the potential benefits of treasury centralisation, such as holistic cash management and combating payment abuse. It also explores how a business can minimise problems for subsidiaries arising from treasury centralisation. Additionally, it provides insights into the financial state and performance of a company, including return on capital employed, operating profit margin, current ratio, and more. The document also examines the difference between actual and budgeted costs and revenue, and the reasons behind the difference.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Finance Project 2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

PART A...........................................................................................................................................1

(a) Potential benefits of treasury centralisation ..........................................................................1

(b) How the business proposes to minimise any potential problems for the subsidiaries that

might arise because of treasury centralisation?...........................................................................1

PART B............................................................................................................................................2

Evolute financial state and performance.....................................................................................2

(b) Company consider stick exchange listing.............................................................................4

PART C............................................................................................................................................5

(a) Were actual costs higher than they should have been to procedure and sell 8200 Darcy's?. 5

(b) Was actual revenue satisfactory from the scale of 8200 Darcy's? ........................................5

(c) Reason for the difference in profit between actual profit and budgeted profit?....................5

REFERENCES................................................................................................................................7

PART A...........................................................................................................................................1

(a) Potential benefits of treasury centralisation ..........................................................................1

(b) How the business proposes to minimise any potential problems for the subsidiaries that

might arise because of treasury centralisation?...........................................................................1

PART B............................................................................................................................................2

Evolute financial state and performance.....................................................................................2

(b) Company consider stick exchange listing.............................................................................4

PART C............................................................................................................................................5

(a) Were actual costs higher than they should have been to procedure and sell 8200 Darcy's?. 5

(b) Was actual revenue satisfactory from the scale of 8200 Darcy's? ........................................5

(c) Reason for the difference in profit between actual profit and budgeted profit?....................5

REFERENCES................................................................................................................................7

PART A

(a) Potential benefits of treasury centralisation

Treasury centralisation is a system of financial management that applied by the most of

the business entities in which financial, cash management, foreign exchange decisions and

controlled by unique team. There are mentioned some benefits of treasury centralisation in

context of BHP that are mentioned below:

1. Holistic cash management: It helps to provide a complete view of bank balances, short

term liquidity requirements and long term cash forecasts. It allows for optimizations of

banking relationships and increase of return on cash by payment factory structure cash

pooling, netting and target balance management.

2. A close eye on payment abuse: Currently, international cybercriminals are increasingly

targeting corporate payment procedure due to cash flows out of business. Through

treasury centralisation aware about cash flow and able to effectively combat fraudsters

and keep close eye on payment abuse. Centralizing outgoing payments factory or an in

house bank and harmonizing all related procedure in order top enhance transparency of

cash flow and take holistic approach for managing the risks.

3. The advantage of centralised treasury system to integrate reporting and accounting area

and achieve all detailed, accurate and up to date information about company cash position

and associate risk. Such elements are helping in preparing strategies to get rid of from

risks and find out various resources of accounts information.

(b) How the business proposes to minimise any potential problems for the subsidiaries that might

arise because of treasury centralisation?

BHP is an Australian registered multinational organisation that conduct their subsidiaries

around 33 nations like Europe, US and may others, These subsidiaries are traditionally allowed a

big amount of autonomy and proposing to centralise of different management operations of

group treasury. As a result it impact on the business in positive and negative manner. There are

arising different problems such as:

Liquidity risk: It is a main risk that faced by the subsidiaries for enough fund and

continue their operational activities by economic cycle and enough funds for strategic

1

(a) Potential benefits of treasury centralisation

Treasury centralisation is a system of financial management that applied by the most of

the business entities in which financial, cash management, foreign exchange decisions and

controlled by unique team. There are mentioned some benefits of treasury centralisation in

context of BHP that are mentioned below:

1. Holistic cash management: It helps to provide a complete view of bank balances, short

term liquidity requirements and long term cash forecasts. It allows for optimizations of

banking relationships and increase of return on cash by payment factory structure cash

pooling, netting and target balance management.

2. A close eye on payment abuse: Currently, international cybercriminals are increasingly

targeting corporate payment procedure due to cash flows out of business. Through

treasury centralisation aware about cash flow and able to effectively combat fraudsters

and keep close eye on payment abuse. Centralizing outgoing payments factory or an in

house bank and harmonizing all related procedure in order top enhance transparency of

cash flow and take holistic approach for managing the risks.

3. The advantage of centralised treasury system to integrate reporting and accounting area

and achieve all detailed, accurate and up to date information about company cash position

and associate risk. Such elements are helping in preparing strategies to get rid of from

risks and find out various resources of accounts information.

(b) How the business proposes to minimise any potential problems for the subsidiaries that might

arise because of treasury centralisation?

BHP is an Australian registered multinational organisation that conduct their subsidiaries

around 33 nations like Europe, US and may others, These subsidiaries are traditionally allowed a

big amount of autonomy and proposing to centralise of different management operations of

group treasury. As a result it impact on the business in positive and negative manner. There are

arising different problems such as:

Liquidity risk: It is a main risk that faced by the subsidiaries for enough fund and

continue their operational activities by economic cycle and enough funds for strategic

1

opportunities. As with this risk treasury must find an effective balance between risk and require

cost for proper management of risk.

Solution: For this require to prepare cash management in which identify short term liquidity risk

and do not approve excessive cash for any activity.

Operational risk: Treasury centralisation is mainly not responsible for the business

procedure like sales, procurement and manufacturing. As a result it becomes reason of operation

risk and covers all procedure like arranging all solid and holistic expertise, policies and

procedures.

Solution: For mitigate this risk require to balance all the procedures of business and cost to find

the most effective solutions for business.

Credit risk: It is mainly focused on treasuries and liable for the counterparties like

banks. When BHP centralised treasury so it impact on subsidiaries and manage the credit risk of

commercial counter parties like customers and vendors.

Solution: For manage this risk by credit insurance and credit default swaps and managed with

strong credit policies and procedure.

PART B

Evolute financial state and performance

2

cost for proper management of risk.

Solution: For this require to prepare cash management in which identify short term liquidity risk

and do not approve excessive cash for any activity.

Operational risk: Treasury centralisation is mainly not responsible for the business

procedure like sales, procurement and manufacturing. As a result it becomes reason of operation

risk and covers all procedure like arranging all solid and holistic expertise, policies and

procedures.

Solution: For mitigate this risk require to balance all the procedures of business and cost to find

the most effective solutions for business.

Credit risk: It is mainly focused on treasuries and liable for the counterparties like

banks. When BHP centralised treasury so it impact on subsidiaries and manage the credit risk of

commercial counter parties like customers and vendors.

Solution: For manage this risk by credit insurance and credit default swaps and managed with

strong credit policies and procedure.

PART B

Evolute financial state and performance

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

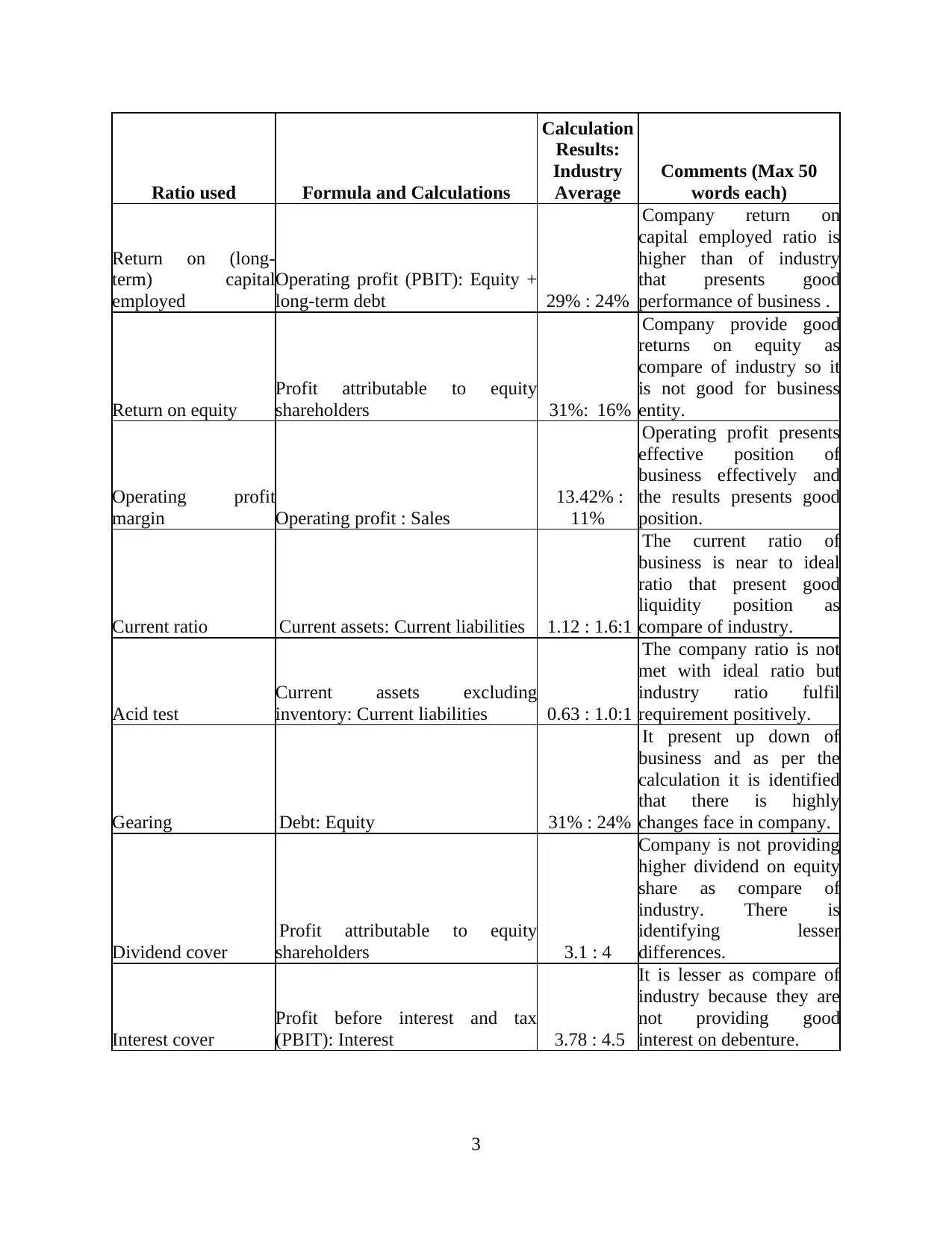

Ratio used Formula and Calculations

Calculation

Results:

Industry

Average

Comments (Max 50

words each)

Return on (long-

term) capital

employed

Operating profit (PBIT): Equity +

long-term debt 29% : 24%

Company return on

capital employed ratio is

higher than of industry

that presents good

performance of business .

Return on equity

Profit attributable to equity

shareholders 31%: 16%

Company provide good

returns on equity as

compare of industry so it

is not good for business

entity.

Operating profit

margin Operating profit : Sales

13.42% :

11%

Operating profit presents

effective position of

business effectively and

the results presents good

position.

Current ratio Current assets: Current liabilities 1.12 : 1.6:1

The current ratio of

business is near to ideal

ratio that present good

liquidity position as

compare of industry.

Acid test

Current assets excluding

inventory: Current liabilities 0.63 : 1.0:1

The company ratio is not

met with ideal ratio but

industry ratio fulfil

requirement positively.

Gearing Debt: Equity 31% : 24%

It present up down of

business and as per the

calculation it is identified

that there is highly

changes face in company.

Dividend cover

Profit attributable to equity

shareholders 3.1 : 4

Company is not providing

higher dividend on equity

share as compare of

industry. There is

identifying lesser

differences.

Interest cover

Profit before interest and tax

(PBIT): Interest 3.78 : 4.5

It is lesser as compare of

industry because they are

not providing good

interest on debenture.

3

Calculation

Results:

Industry

Average

Comments (Max 50

words each)

Return on (long-

term) capital

employed

Operating profit (PBIT): Equity +

long-term debt 29% : 24%

Company return on

capital employed ratio is

higher than of industry

that presents good

performance of business .

Return on equity

Profit attributable to equity

shareholders 31%: 16%

Company provide good

returns on equity as

compare of industry so it

is not good for business

entity.

Operating profit

margin Operating profit : Sales

13.42% :

11%

Operating profit presents

effective position of

business effectively and

the results presents good

position.

Current ratio Current assets: Current liabilities 1.12 : 1.6:1

The current ratio of

business is near to ideal

ratio that present good

liquidity position as

compare of industry.

Acid test

Current assets excluding

inventory: Current liabilities 0.63 : 1.0:1

The company ratio is not

met with ideal ratio but

industry ratio fulfil

requirement positively.

Gearing Debt: Equity 31% : 24%

It present up down of

business and as per the

calculation it is identified

that there is highly

changes face in company.

Dividend cover

Profit attributable to equity

shareholders 3.1 : 4

Company is not providing

higher dividend on equity

share as compare of

industry. There is

identifying lesser

differences.

Interest cover

Profit before interest and tax

(PBIT): Interest 3.78 : 4.5

It is lesser as compare of

industry because they are

not providing good

interest on debenture.

3

(b) Company consider stick exchange listing

Listing will allows a business to raise capital in broad market area in regard of their

shares and debentures. Along with expand existing business and set up new business easily.

Moreover, it supports in fund acquisition, provide a exit strategy for founders of business and

also for early stage investors.

4

Listing will allows a business to raise capital in broad market area in regard of their

shares and debentures. Along with expand existing business and set up new business easily.

Moreover, it supports in fund acquisition, provide a exit strategy for founders of business and

also for early stage investors.

4

PART C

(a) Were actual costs higher than they should have been to procedure and sell 8200 Darcy's?

Yes actual cost is higher than for manufacturing and selling procedure. When compare

results of actual and budgeted profits so it is getting that organization is not properly utilized

their resources so it impact on the profit. Along with it is increasing total overhead that reduce

profitability. For this require to product manufacture in less cost and proper utilize all the

resources.

(b) Was actual revenue satisfactory from the scale of 8200 Darcy's?

Yes, actual revenue is satisfactory from the scale of 8200 Darcy because after increasing

production unit in actual company generate more profitability. Thus, it presents good position of

business and generate 3200 more profitability in actual as compare of budgeted profit.

(c) Reason for the difference in profit between actual profit and budgeted profit?

The main reason between actual and budgeted profit that in budgeted calculation produce

7500 units and in actual produce 8200 units. In budgeted production cost of material and labour

take is less so it presents less overhead. On the other side in actual unit calculation take higher

cost that impact on the profitability in large manner.

5

(a) Were actual costs higher than they should have been to procedure and sell 8200 Darcy's?

Yes actual cost is higher than for manufacturing and selling procedure. When compare

results of actual and budgeted profits so it is getting that organization is not properly utilized

their resources so it impact on the profit. Along with it is increasing total overhead that reduce

profitability. For this require to product manufacture in less cost and proper utilize all the

resources.

(b) Was actual revenue satisfactory from the scale of 8200 Darcy's?

Yes, actual revenue is satisfactory from the scale of 8200 Darcy because after increasing

production unit in actual company generate more profitability. Thus, it presents good position of

business and generate 3200 more profitability in actual as compare of budgeted profit.

(c) Reason for the difference in profit between actual profit and budgeted profit?

The main reason between actual and budgeted profit that in budgeted calculation produce

7500 units and in actual produce 8200 units. In budgeted production cost of material and labour

take is less so it presents less overhead. On the other side in actual unit calculation take higher

cost that impact on the profitability in large manner.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

REFERENCES

Books and Journals

7

Books and Journals

7

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.