Finance Project: Financial Planning, Risk, and Investment Analysis

VerifiedAdded on 2020/06/05

|12

|2429

|25

Project

AI Summary

This finance project delves into various aspects of personal finance, starting with an analysis of a Lifetime ISA, exploring its benefits and maximum contribution limits. It then calculates the maximum loan amount Mark and Spencer can borrow based on their affordability. The project further assesses the value of an annuity and savings over a three-year period. It then examines the advantages and disadvantages of interest-only mortgages. The assignment then addresses potential risks Mark and Spencer may face and explores the difference between real and nominal values, calculating both for a house and mortgage. The project analyzes short-term and long-term assets and liabilities, calculates net worth, gearing, and current asset ratios, and provides interpretations of the financial performance. Part B of the project discusses risks associated with retirement and suggests strategies for financial security, including the importance of savings, investment in various funds, and the potential of annuity products. The project concludes by highlighting various ways retirees can mitigate risks, such as through part-time work, investment in insurance, and adapting to inflation.

Finance Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1.1 Saving and investment in Lifetime ISA.................................................................................3

1.2 Maximum loan amount..........................................................................................................3

1.3 Value of annuity.....................................................................................................................4

1.4 Value of saving......................................................................................................................5

1.5 Advantage and disadvantage of interest only mortgage........................................................5

1.6 Risks that Mark and Spencer may face..................................................................................5

QUESTION 2..................................................................................................................................5

2.1 Difference between real and nominal value...........................................................................5

2.2 (A). Calculation of nominal value of the house and mortgage with interpretation...............6

(B). Calculation of real value of the house and mortgage with interpretation.............................6

2.3 Short-term and long-term assets and liabilities......................................................................6

2.4 Net worth, gearing and current assets ratio............................................................................7

2.5 Reasons..................................................................................................................................8

PART B...........................................................................................................................................8

REFERENCES..............................................................................................................................10

1.1 Saving and investment in Lifetime ISA.................................................................................3

1.2 Maximum loan amount..........................................................................................................3

1.3 Value of annuity.....................................................................................................................4

1.4 Value of saving......................................................................................................................5

1.5 Advantage and disadvantage of interest only mortgage........................................................5

1.6 Risks that Mark and Spencer may face..................................................................................5

QUESTION 2..................................................................................................................................5

2.1 Difference between real and nominal value...........................................................................5

2.2 (A). Calculation of nominal value of the house and mortgage with interpretation...............6

(B). Calculation of real value of the house and mortgage with interpretation.............................6

2.3 Short-term and long-term assets and liabilities......................................................................6

2.4 Net worth, gearing and current assets ratio............................................................................7

2.5 Reasons..................................................................................................................................8

PART B...........................................................................................................................................8

REFERENCES..............................................................................................................................10

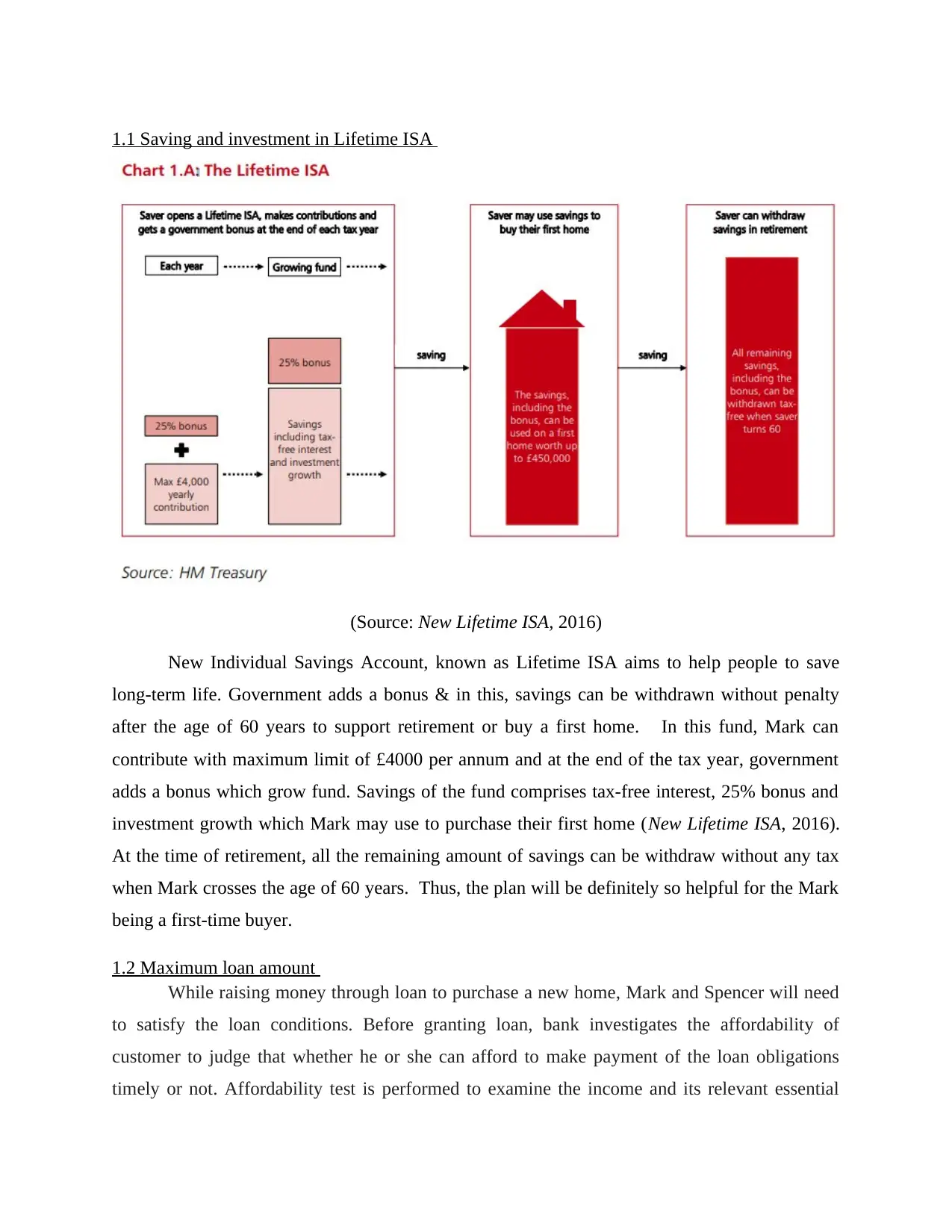

1.1 Saving and investment in Lifetime ISA

(Source: New Lifetime ISA, 2016)

New Individual Savings Account, known as Lifetime ISA aims to help people to save

long-term life. Government adds a bonus & in this, savings can be withdrawn without penalty

after the age of 60 years to support retirement or buy a first home. In this fund, Mark can

contribute with maximum limit of £4000 per annum and at the end of the tax year, government

adds a bonus which grow fund. Savings of the fund comprises tax-free interest, 25% bonus and

investment growth which Mark may use to purchase their first home (New Lifetime ISA, 2016).

At the time of retirement, all the remaining amount of savings can be withdraw without any tax

when Mark crosses the age of 60 years. Thus, the plan will be definitely so helpful for the Mark

being a first-time buyer.

1.2 Maximum loan amount

While raising money through loan to purchase a new home, Mark and Spencer will need

to satisfy the loan conditions. Before granting loan, bank investigates the affordability of

customer to judge that whether he or she can afford to make payment of the loan obligations

timely or not. Affordability test is performed to examine the income and its relevant essential

(Source: New Lifetime ISA, 2016)

New Individual Savings Account, known as Lifetime ISA aims to help people to save

long-term life. Government adds a bonus & in this, savings can be withdrawn without penalty

after the age of 60 years to support retirement or buy a first home. In this fund, Mark can

contribute with maximum limit of £4000 per annum and at the end of the tax year, government

adds a bonus which grow fund. Savings of the fund comprises tax-free interest, 25% bonus and

investment growth which Mark may use to purchase their first home (New Lifetime ISA, 2016).

At the time of retirement, all the remaining amount of savings can be withdraw without any tax

when Mark crosses the age of 60 years. Thus, the plan will be definitely so helpful for the Mark

being a first-time buyer.

1.2 Maximum loan amount

While raising money through loan to purchase a new home, Mark and Spencer will need

to satisfy the loan conditions. Before granting loan, bank investigates the affordability of

customer to judge that whether he or she can afford to make payment of the loan obligations

timely or not. Affordability test is performed to examine the income and its relevant essential

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

spending so as to determine the net availability of money that Mark and Spencer can utilize to

pay-off their mortgage. Broker performed affordability test and found that Mark & Spencer

could pay £900 per month and the loan period is 25-year at 4% APR.

Calculation of maximum amount that can be borrow

Rate=4 % /number of month∈a year

¿ 4 % /12=0.33 %

Number of period of payment =25 years∗12 months

¿ 300 months

Maximum affordable payment=GBP 900 /month

Borrowing amount =Present value( 0.33 % , 300 ,900)

¿ £ 170,507.23

It means that Mark and Spencer would be able to borrow £170,000 by paying monthly

payment worth £900 to the mortgage and can use it to purchase own home.

1.3 Value of annuity

Mark and Spencer require a jointly lump sum of £18,500 to cover the deposit and other

relevant cost to buy a sort of home they want. Although Spencer has a saving of £9,000 which is

expected to grow to £9,250 half-share whereas Mark just can afford £250 each month and obtain

return of 2% per annum through an Ordinary Cash ISA. The amount of these savings after 3 year

can be computed as follows:

FV of annuity

= C*[(1+i)n-1/i]

Interest rate per annum = 2%/12 =

= £250*[(1+0.17%)-1/0.17%]

= £250*37.09

pay-off their mortgage. Broker performed affordability test and found that Mark & Spencer

could pay £900 per month and the loan period is 25-year at 4% APR.

Calculation of maximum amount that can be borrow

Rate=4 % /number of month∈a year

¿ 4 % /12=0.33 %

Number of period of payment =25 years∗12 months

¿ 300 months

Maximum affordable payment=GBP 900 /month

Borrowing amount =Present value( 0.33 % , 300 ,900)

¿ £ 170,507.23

It means that Mark and Spencer would be able to borrow £170,000 by paying monthly

payment worth £900 to the mortgage and can use it to purchase own home.

1.3 Value of annuity

Mark and Spencer require a jointly lump sum of £18,500 to cover the deposit and other

relevant cost to buy a sort of home they want. Although Spencer has a saving of £9,000 which is

expected to grow to £9,250 half-share whereas Mark just can afford £250 each month and obtain

return of 2% per annum through an Ordinary Cash ISA. The amount of these savings after 3 year

can be computed as follows:

FV of annuity

= C*[(1+i)n-1/i]

Interest rate per annum = 2%/12 =

= £250*[(1+0.17%)-1/0.17%]

= £250*37.09

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £9,272.5

Thus, after 3-year, the saving of £250 per month will become £9,272.5 and by this, they

both will have a joint saving worth £18,500.

1.4 Value of saving

Spencer’s value of saving after 3 year = 9000*(1+2%)^3

= £9,550

Mark’s value of savings = £250*12*3 = £9000

1.5 Advantage and disadvantage of interest only mortgage

Advantage of interest only mortgage

Need to pay only interest on the loan for a particular or specified period of time hence

reduces minimum repayments

Disadvantage of interest only mortgage

It is not suitable option for owner occupier and at the end of the interest only period, both

the principles inclusive interest needs to be paid which may be outside the affordability of Mark

(Calabro, 2017).

1.6 Risks that Mark and Spencer may face

Three risks waiting for three years to buy a home

The risk of higher rate of interest tends to increase the cost of borrowing and makes

mortgage more expensive and costlier.

High demand in the future leads to climb prices to an upper extent as a result; cost of

home buying will be greater.

Lack of supply or inventory shortage in the housing market in future may increase price.

QUESTION 2

2.1 Difference between real and nominal value

The difference between nominal and real value is real value is adjusted for inflation

whereas it is not so with the nominal value as these are not adjusted considering the prevailing

Thus, after 3-year, the saving of £250 per month will become £9,272.5 and by this, they

both will have a joint saving worth £18,500.

1.4 Value of saving

Spencer’s value of saving after 3 year = 9000*(1+2%)^3

= £9,550

Mark’s value of savings = £250*12*3 = £9000

1.5 Advantage and disadvantage of interest only mortgage

Advantage of interest only mortgage

Need to pay only interest on the loan for a particular or specified period of time hence

reduces minimum repayments

Disadvantage of interest only mortgage

It is not suitable option for owner occupier and at the end of the interest only period, both

the principles inclusive interest needs to be paid which may be outside the affordability of Mark

(Calabro, 2017).

1.6 Risks that Mark and Spencer may face

Three risks waiting for three years to buy a home

The risk of higher rate of interest tends to increase the cost of borrowing and makes

mortgage more expensive and costlier.

High demand in the future leads to climb prices to an upper extent as a result; cost of

home buying will be greater.

Lack of supply or inventory shortage in the housing market in future may increase price.

QUESTION 2

2.1 Difference between real and nominal value

The difference between nominal and real value is real value is adjusted for inflation

whereas it is not so with the nominal value as these are not adjusted considering the prevailing

inflation rate. Thus, nominal value simply present fixed value of an item whilst real value

expresses the market value by incorporating the price changes in the market. Hence, fluctuating

the market price level changes differentiate both nominal and real market value. Thus, it can be

said that nominal value is also known as book value which is not required to calculate every

year.

2.2 (A). Calculation of nominal value of the house and mortgage with interpretation

Here, the nominal value of the house and mortgage will be remain same to £150,000 and

£140,000 in February 2018 and it will not be adjusted by the general price inflation as well as

house price inflation @ 2% and 4.2% respectively. The value is disregards to the market changes

and expresses its face value that is similar to the value in February 2011.

(B). Calculation of real value of the house and mortgage with interpretation

Real value of house = £150,000 * (1+4.2%)^7

= £200,062.3

Real value of mortgage: £140,000 * (1+2%)^7

£160,816

2.3 Short-term and long-term assets and liabilities

Short-term assets are the assets that are available for a short period usually one year like

debtors, inventory and other. On contrary, short-term liabilities are the liabilities which need to

paid within one year period.

Long-term assets are used for a long-lasting life includes property, plant, machinery and

others whereas long-term liabilities includes those components that firm will pay after a long-

period such as long-term debt loan.

Feb-11 Feb-18

Current assets

Cash ISA £5,000 £1,000

Current account £0 £100

expresses the market value by incorporating the price changes in the market. Hence, fluctuating

the market price level changes differentiate both nominal and real market value. Thus, it can be

said that nominal value is also known as book value which is not required to calculate every

year.

2.2 (A). Calculation of nominal value of the house and mortgage with interpretation

Here, the nominal value of the house and mortgage will be remain same to £150,000 and

£140,000 in February 2018 and it will not be adjusted by the general price inflation as well as

house price inflation @ 2% and 4.2% respectively. The value is disregards to the market changes

and expresses its face value that is similar to the value in February 2011.

(B). Calculation of real value of the house and mortgage with interpretation

Real value of house = £150,000 * (1+4.2%)^7

= £200,062.3

Real value of mortgage: £140,000 * (1+2%)^7

£160,816

2.3 Short-term and long-term assets and liabilities

Short-term assets are the assets that are available for a short period usually one year like

debtors, inventory and other. On contrary, short-term liabilities are the liabilities which need to

paid within one year period.

Long-term assets are used for a long-lasting life includes property, plant, machinery and

others whereas long-term liabilities includes those components that firm will pay after a long-

period such as long-term debt loan.

Feb-11 Feb-18

Current assets

Cash ISA £5,000 £1,000

Current account £0 £100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash ISA £5,000 £1,000

Long-term assets

House £150,000 £150,000

Total assets £160,000 £152,100

Current liabilities

Overdraft £1,000 £0

Credit card £1,000 £2,000

Non-current liabilities

Unsecured debt due for repayment in

January 2019

£5,000 £5000

Loan mortgage £140,000 £140,000

Total liabilities £147,000 £147,000

Net assets £13,000 £5,100

Equity (B/F) £12,900 £5200

Net profit /loss for the current year £100 (£100)

In the given case, overdraft and credit card is short-term liabilities whereas unsecured

debt that is due for repayment in January 2019 and mortgage are long-term liabilities. In contrast,

cash ISA, current account is short-term assets and house is an example of long-term assets.

2.4 Net worth, gearing and current assets ratio

Net worth of £13,000 fallen to £5,100 because of declined in the total assets value

whereas total liabilities remain constant. It shows adverse performance of the business enterprise

due to substantial decline in the value of assets.

Current ratio = current assets/current liabilities

Long-term assets

House £150,000 £150,000

Total assets £160,000 £152,100

Current liabilities

Overdraft £1,000 £0

Credit card £1,000 £2,000

Non-current liabilities

Unsecured debt due for repayment in

January 2019

£5,000 £5000

Loan mortgage £140,000 £140,000

Total liabilities £147,000 £147,000

Net assets £13,000 £5,100

Equity (B/F) £12,900 £5200

Net profit /loss for the current year £100 (£100)

In the given case, overdraft and credit card is short-term liabilities whereas unsecured

debt that is due for repayment in January 2019 and mortgage are long-term liabilities. In contrast,

cash ISA, current account is short-term assets and house is an example of long-term assets.

2.4 Net worth, gearing and current assets ratio

Net worth of £13,000 fallen to £5,100 because of declined in the total assets value

whereas total liabilities remain constant. It shows adverse performance of the business enterprise

due to substantial decline in the value of assets.

Current ratio = current assets/current liabilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2011 = £10000/£2000 = 5:1

2018 = £2100/£2000 = 1.05:1

CR indicates considerable decline from 5:1 to 1.05:1 that shows that company’s ability to

pay off outside or external short-term obligations came down. It is an adverse indicator to the

business liquidity and indicates possibility of liquidity crunch.

Gearing ratios:

Deb- to-equity ratio = Debt/Equity

2011: 145,000/12,900 = 11.24

2012: 145,000/5200 = 27.88

From the derived outcome, it is seen that company is excessively financed through long-

term debt indicates very high financial risk in the business.

2.5 Reasons

Selling of house would lead to improve its financial position as company will not need to

pay mortgage and increase its cash position which will lead to improve financial status.

However, in the long-run, it may impinge on the long-term financial security because in

future, house price inflation will increase price in long-run, however, by selling today, business

will not get a good price.

PART B

There are number of risks that can be faced by individuals and households with respect to

financial security in retirement. Saving is the most important requirement for all the individuals

and they need to save for many reasons to safeguard unexpected costs, to accumulate money for

the purchase of huge assets and to prepare for retirement. As people age moves towards

retirement, they usually start liquidating stock to generate income to pay their living

expenditures, retirement care, health care and others (Topa, Lunceford and Boyatzis, 2017).

There are multiple ranges of risks that an individual can face in retirement such as unexpected

illness, financial turbulence due to inflation and stock market activities, healthcare and housing

2018 = £2100/£2000 = 1.05:1

CR indicates considerable decline from 5:1 to 1.05:1 that shows that company’s ability to

pay off outside or external short-term obligations came down. It is an adverse indicator to the

business liquidity and indicates possibility of liquidity crunch.

Gearing ratios:

Deb- to-equity ratio = Debt/Equity

2011: 145,000/12,900 = 11.24

2012: 145,000/5200 = 27.88

From the derived outcome, it is seen that company is excessively financed through long-

term debt indicates very high financial risk in the business.

2.5 Reasons

Selling of house would lead to improve its financial position as company will not need to

pay mortgage and increase its cash position which will lead to improve financial status.

However, in the long-run, it may impinge on the long-term financial security because in

future, house price inflation will increase price in long-run, however, by selling today, business

will not get a good price.

PART B

There are number of risks that can be faced by individuals and households with respect to

financial security in retirement. Saving is the most important requirement for all the individuals

and they need to save for many reasons to safeguard unexpected costs, to accumulate money for

the purchase of huge assets and to prepare for retirement. As people age moves towards

retirement, they usually start liquidating stock to generate income to pay their living

expenditures, retirement care, health care and others (Topa, Lunceford and Boyatzis, 2017).

There are multiple ranges of risks that an individual can face in retirement such as unexpected

illness, financial turbulence due to inflation and stock market activities, healthcare and housing

issues, change in government policies and others. Moreover, longevity risks are one of great

concern among retirees. In despite of this, death of spouse can reduce pension benefits or impose

financial burden including medical debts (Lusardi, Michaud and Mitchell, 2017). Further,

unexpected health care requirements, change in housing needs and unforeseen or unpredicted

requirement of the family members can bring sudden financial risks after retirement.

It is essential for the retirees to make proper financial planning so as to prevent various

risks that are subjected with the retirement. There are many opportunities available to the retirees

which they can use to safeguard themselves after retirement. In order to mitigate such kind of

risks, many-times, retirees often plan to supplement their income through employing in an either

a part time or full-time work after retirement (Ampudia and Ehrmann, 2017). In the practical

world, it is also seen that many organization hire elderly age people at their workplace

considering their working experience and stability aspect. However, at the same time, in the

current times, companies success majorly depends on hiring people with extraordinary technical

skills and knowledge hence, employment prospects among older people may vary. Thus, based

on their skills and knowledge, people who have sound knowledge of advanced technologies are

able to work even after the age of retirement while the same opportunity may not exist to other

guise and do not help them in shaping risk (Boisclair, DLusardi and Michaud, 2017).

In addition to this, people always save money so as to have sufficient financial security

for future. In order to save, they invest in many funds like pension fund is one of the most

important fund, in which, people contributes some proportion of their salary which is

accumulated and withdrawn after retirement to meet retiree’s financial requirements (Lusardi

and et.al, 2017). Apart from this, people can save some proportion of their income regularly and

invest in alternative investment opportunities such as annuity which will facilitate them to

mitigate some sort of risks by providing life-time income stream (Gruber, Jensen and Kleven,

2017).

Despite this, to have proper coverage against unexpected health concerns or chronic

illnesses, it is a good option available to retirees to insure their life by investing money in life

insurance policies and long-term care insurance which provides healthcare benefits. Like

Medicare is one of the primary sources of healthcare coverage to meet the unpredictable medical

cost. Furthermore, as inflation is a major concern for every person. Hence, it is better opportunity

concern among retirees. In despite of this, death of spouse can reduce pension benefits or impose

financial burden including medical debts (Lusardi, Michaud and Mitchell, 2017). Further,

unexpected health care requirements, change in housing needs and unforeseen or unpredicted

requirement of the family members can bring sudden financial risks after retirement.

It is essential for the retirees to make proper financial planning so as to prevent various

risks that are subjected with the retirement. There are many opportunities available to the retirees

which they can use to safeguard themselves after retirement. In order to mitigate such kind of

risks, many-times, retirees often plan to supplement their income through employing in an either

a part time or full-time work after retirement (Ampudia and Ehrmann, 2017). In the practical

world, it is also seen that many organization hire elderly age people at their workplace

considering their working experience and stability aspect. However, at the same time, in the

current times, companies success majorly depends on hiring people with extraordinary technical

skills and knowledge hence, employment prospects among older people may vary. Thus, based

on their skills and knowledge, people who have sound knowledge of advanced technologies are

able to work even after the age of retirement while the same opportunity may not exist to other

guise and do not help them in shaping risk (Boisclair, DLusardi and Michaud, 2017).

In addition to this, people always save money so as to have sufficient financial security

for future. In order to save, they invest in many funds like pension fund is one of the most

important fund, in which, people contributes some proportion of their salary which is

accumulated and withdrawn after retirement to meet retiree’s financial requirements (Lusardi

and et.al, 2017). Apart from this, people can save some proportion of their income regularly and

invest in alternative investment opportunities such as annuity which will facilitate them to

mitigate some sort of risks by providing life-time income stream (Gruber, Jensen and Kleven,

2017).

Despite this, to have proper coverage against unexpected health concerns or chronic

illnesses, it is a good option available to retirees to insure their life by investing money in life

insurance policies and long-term care insurance which provides healthcare benefits. Like

Medicare is one of the primary sources of healthcare coverage to meet the unpredictable medical

cost. Furthermore, as inflation is a major concern for every person. Hence, it is better opportunity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for the retirees to invest in equity, home or Treasury-Inflation Protected Securities (TIPS).

Moreover, they must prefer investment in annuity product that incorporates cost of living

adjustment feature which helps to offset against inflation. Annuity offers a guaranteed income to

the people (Billingsley, Gitman & Joehnk, 2016). By all of these ways, retirees can safeguard

themselves with the unexpected illness or issues.

Moreover, they must prefer investment in annuity product that incorporates cost of living

adjustment feature which helps to offset against inflation. Annuity offers a guaranteed income to

the people (Billingsley, Gitman & Joehnk, 2016). By all of these ways, retirees can safeguard

themselves with the unexpected illness or issues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Ampudia, M. and Ehrmann, M., 2017. Macroeconomic experiences and risk taking of euro area

households.European Economic Review. 91. pp.146-156.

Billingsley, R., Gitman, L. J., & Joehnk, M. D., 2016. Personal financial planning. Cengage

Learning.

Boisclair, D., Lusardi, A. and Michaud, P. C., 2017. Financial literacy and retirement planning in

Canada. Journal of Pension Economics & Finance. 16(3). pp.277-296.

Calabro, P., 2017. It's about the climb: this financial planning guide uses adventure travel as a

model for getting started. Strategic Finance. 99(3). pp.18-19.

Gruber, J., Jensen, A. and Kleven, H., 2017. Do people respond to the mortage interest

deduction? Quasi-experimental evidence from Denmark. National Bureau of Economic

Research. No. w23600.

Lusardi, A. and et.al, 2017. Visual tools and narratives: New ways to improve financial

literacy. Journal of Pension Economics & Finance. 16(3). pp.297-323.

Lusardi, A., Michaud, P. C. and Mitchell, O. S., 2017. Optimal financial knowledge and wealth

inequality. Journal of Political Economy. 125(2). pp.431-477.

Topa, G., Lunceford, G. and Boyatzis, R.E.D., 2017. Financial planning for retirement: A

psychosocial perspective. Frontiers in Psychology. 8. p.2338.

Online

New Lifetime ISA. 2016. [PDF]. Available through: <

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/508176/

Lifetime_ISA_final.pdf>.

Symond, J., 2014. Pros and cons of an interest only loan. [Online]. Available through: <

https://www.aussie.com.au/blog/dear-john-what-are-the-pros-and-cons-of-an-interest-only-

home-loan-3/>.

Books and Journals

Ampudia, M. and Ehrmann, M., 2017. Macroeconomic experiences and risk taking of euro area

households.European Economic Review. 91. pp.146-156.

Billingsley, R., Gitman, L. J., & Joehnk, M. D., 2016. Personal financial planning. Cengage

Learning.

Boisclair, D., Lusardi, A. and Michaud, P. C., 2017. Financial literacy and retirement planning in

Canada. Journal of Pension Economics & Finance. 16(3). pp.277-296.

Calabro, P., 2017. It's about the climb: this financial planning guide uses adventure travel as a

model for getting started. Strategic Finance. 99(3). pp.18-19.

Gruber, J., Jensen, A. and Kleven, H., 2017. Do people respond to the mortage interest

deduction? Quasi-experimental evidence from Denmark. National Bureau of Economic

Research. No. w23600.

Lusardi, A. and et.al, 2017. Visual tools and narratives: New ways to improve financial

literacy. Journal of Pension Economics & Finance. 16(3). pp.297-323.

Lusardi, A., Michaud, P. C. and Mitchell, O. S., 2017. Optimal financial knowledge and wealth

inequality. Journal of Political Economy. 125(2). pp.431-477.

Topa, G., Lunceford, G. and Boyatzis, R.E.D., 2017. Financial planning for retirement: A

psychosocial perspective. Frontiers in Psychology. 8. p.2338.

Online

New Lifetime ISA. 2016. [PDF]. Available through: <

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/508176/

Lifetime_ISA_final.pdf>.

Symond, J., 2014. Pros and cons of an interest only loan. [Online]. Available through: <

https://www.aussie.com.au/blog/dear-john-what-are-the-pros-and-cons-of-an-interest-only-

home-loan-3/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.