Finance Project 2: Cost Analysis and Break-Even Point Analysis

VerifiedAdded on 2020/07/23

|9

|1264

|31

Project

AI Summary

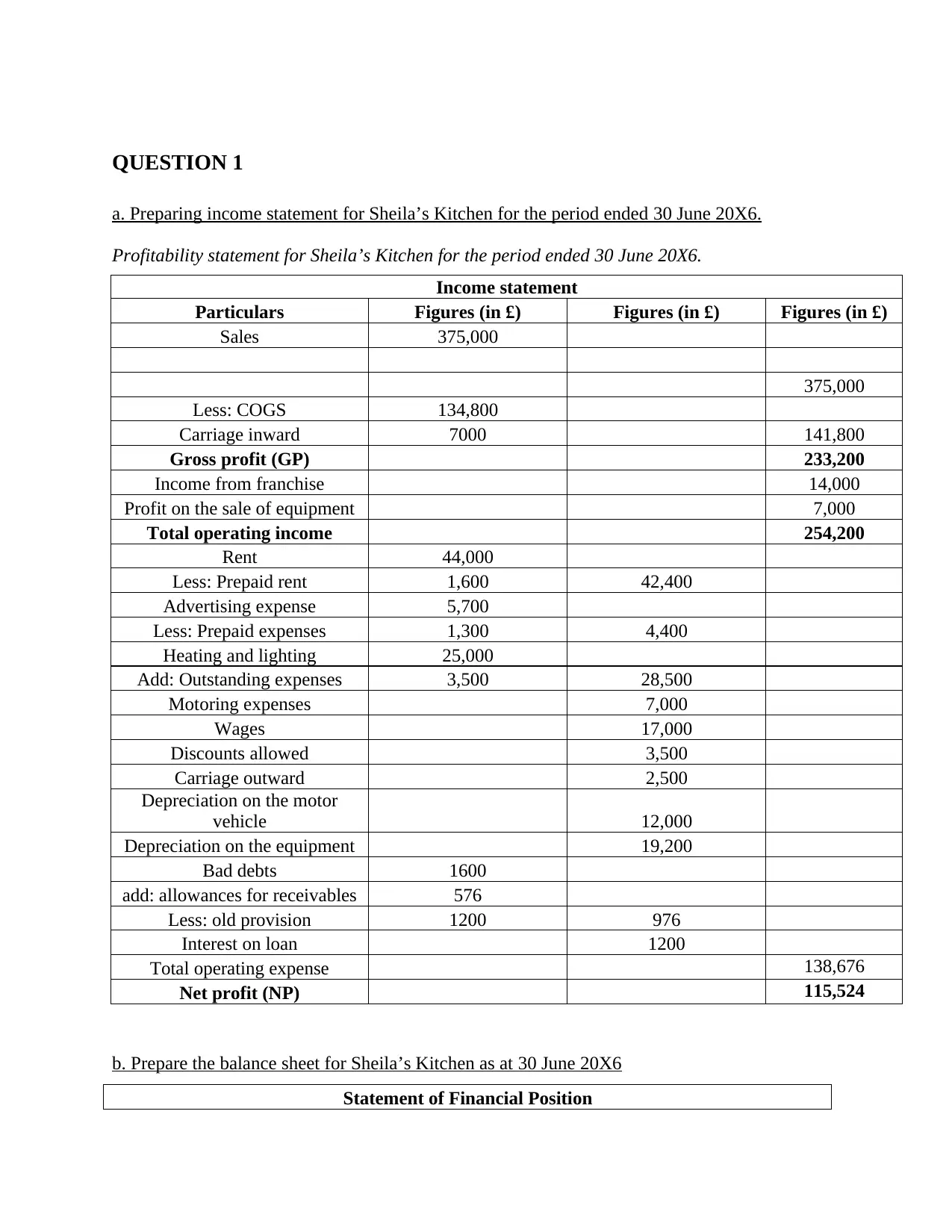

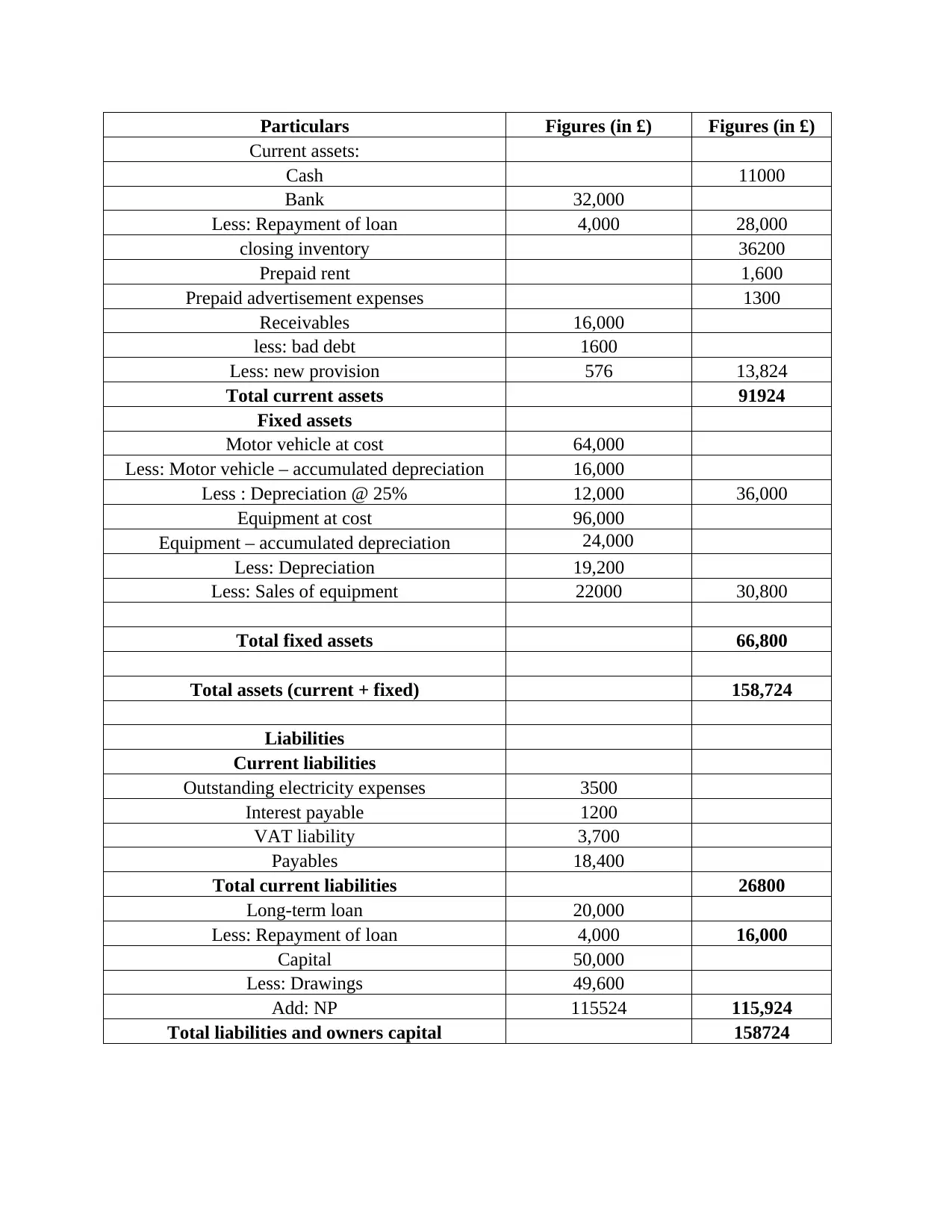

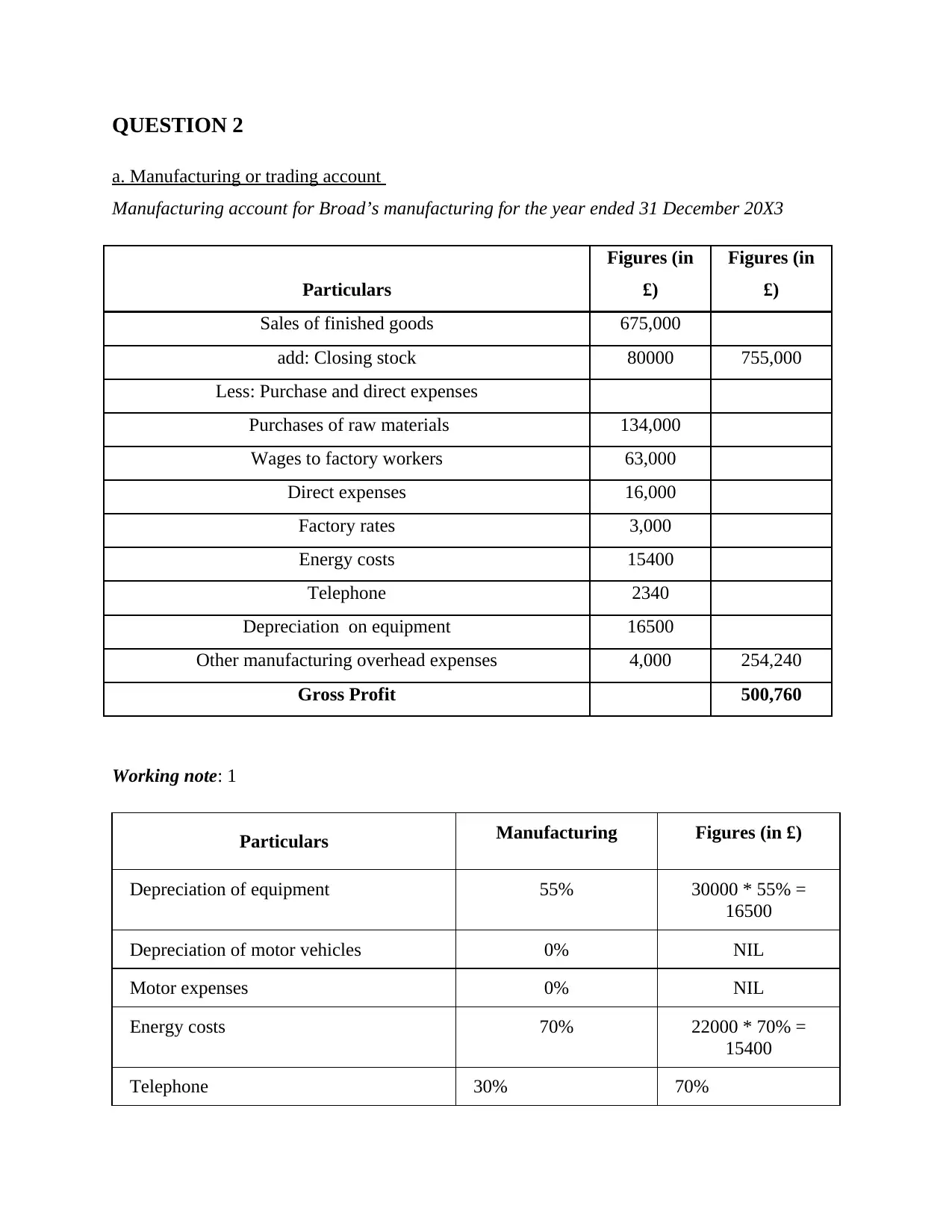

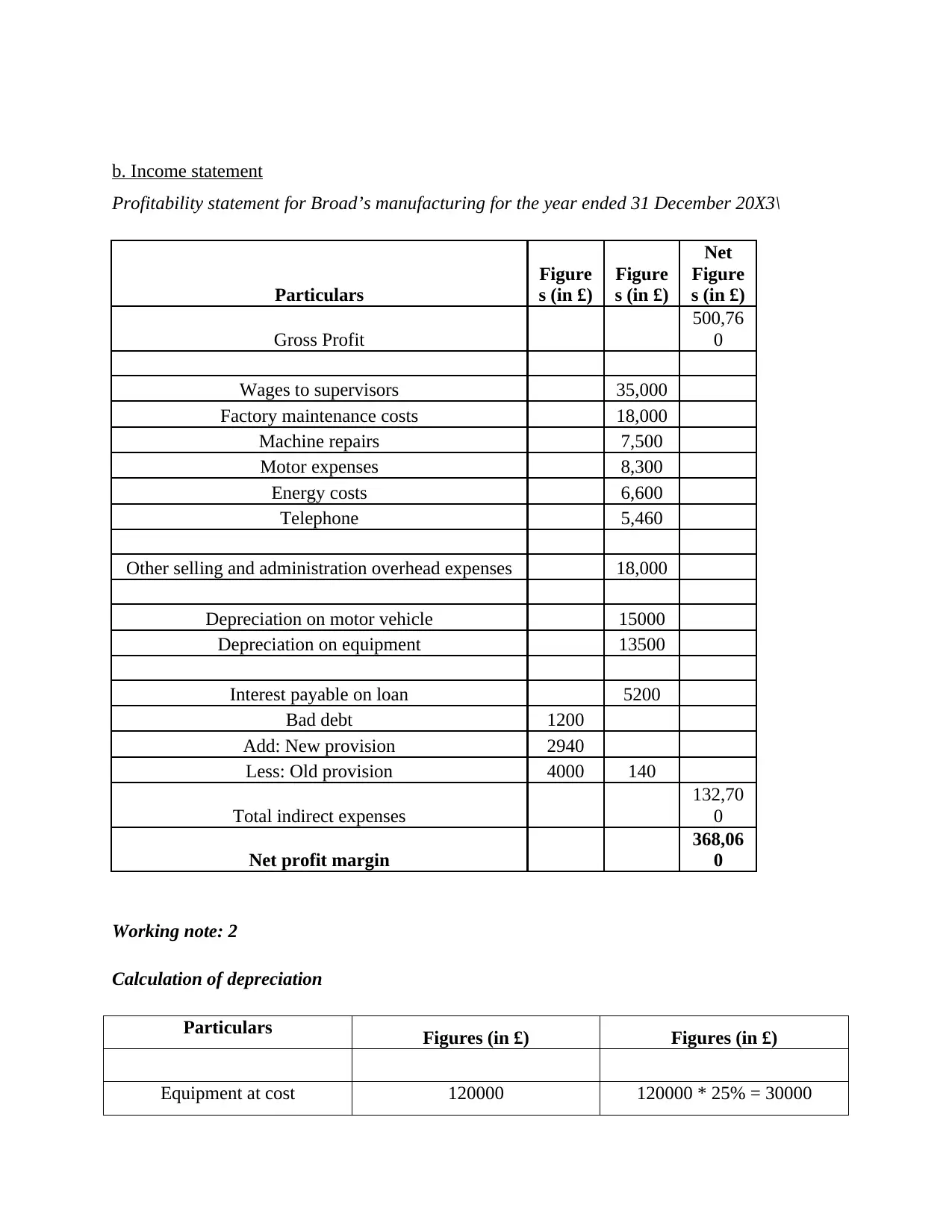

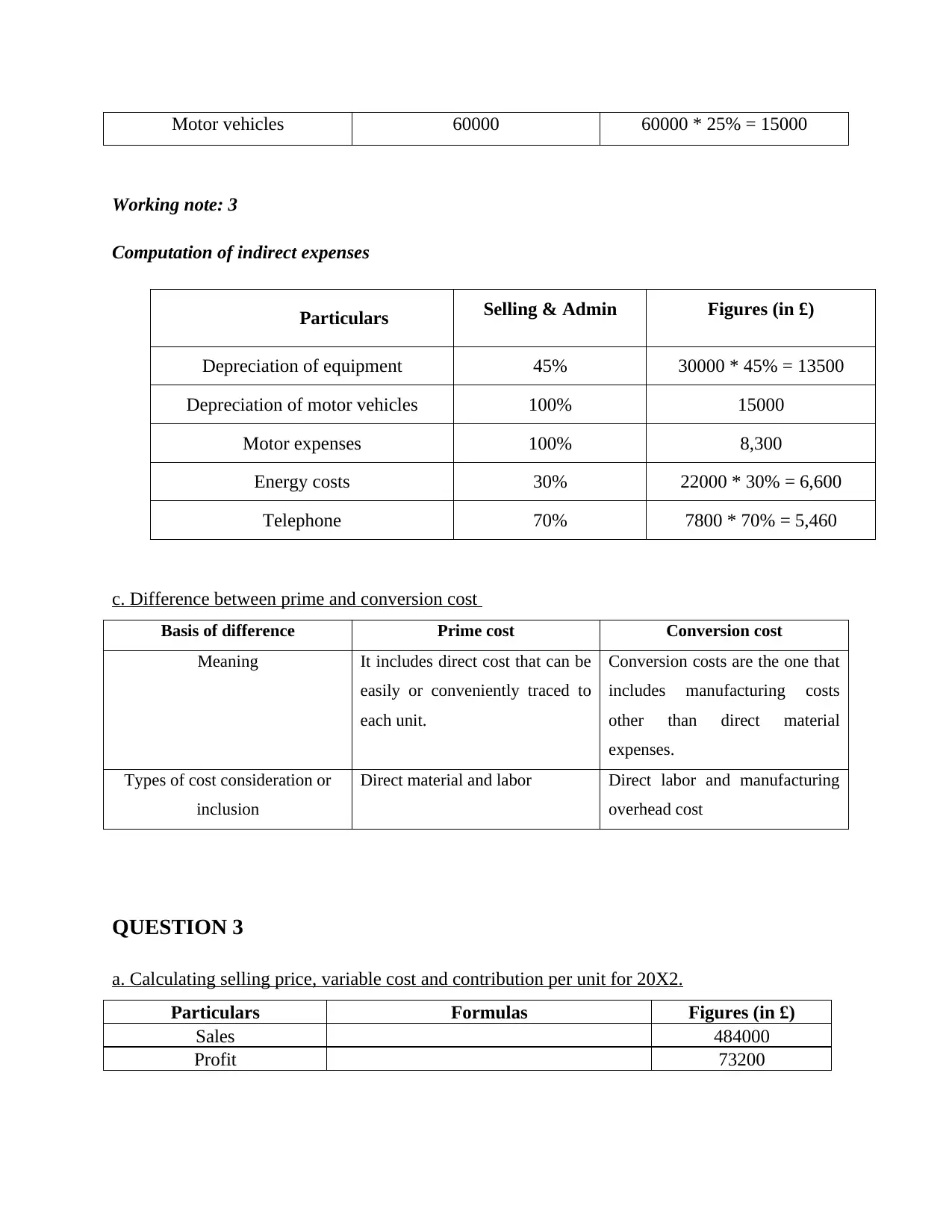

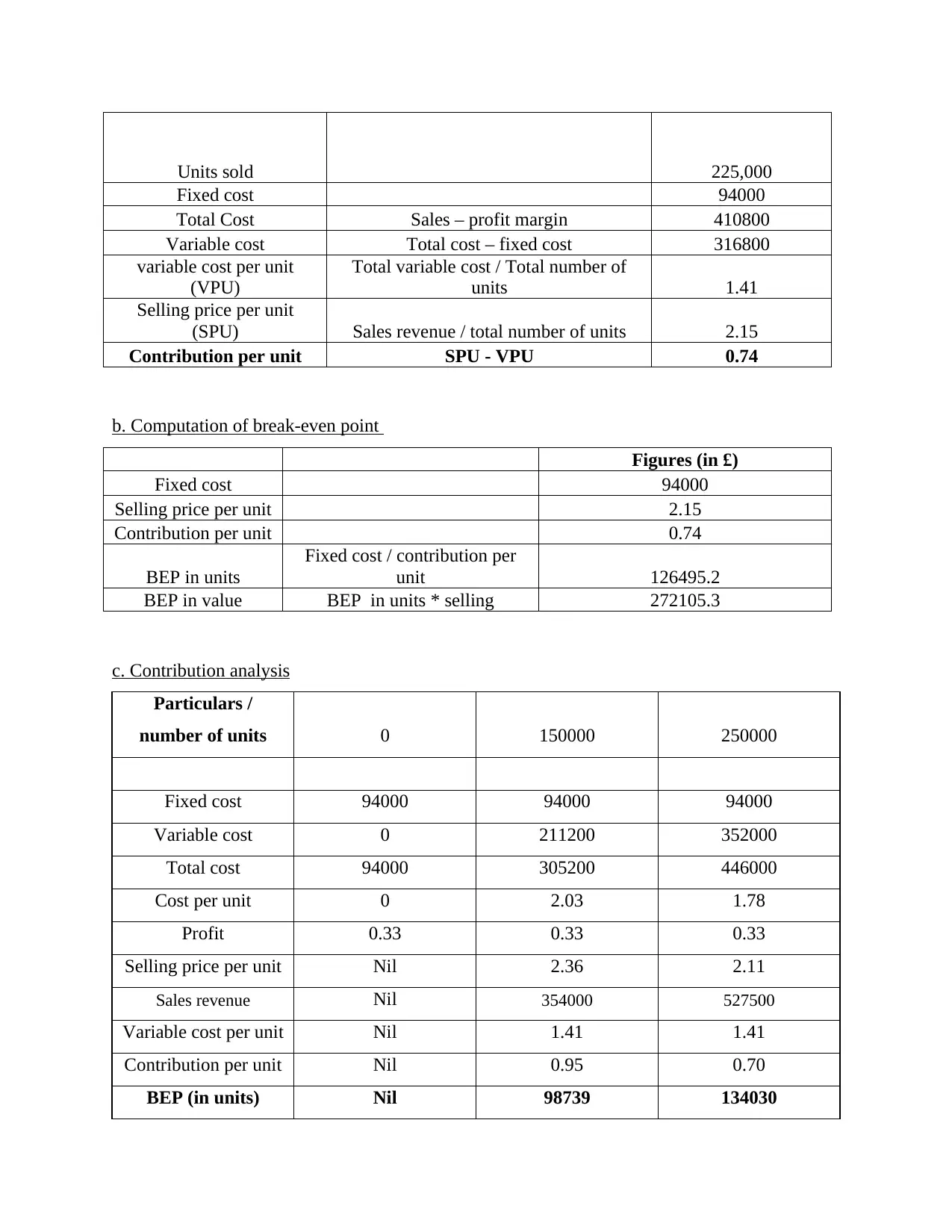

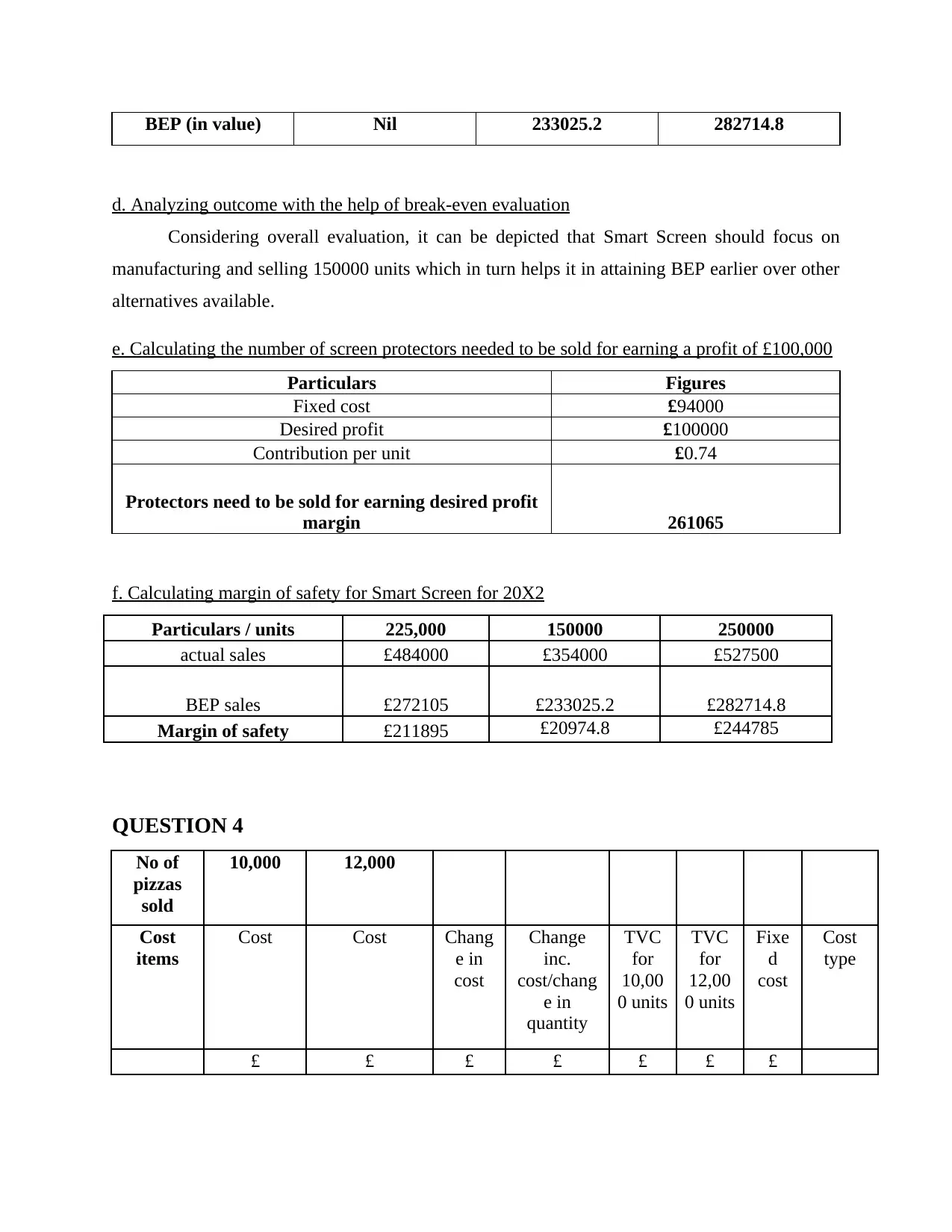

This finance project provides a detailed financial analysis for two different scenarios: Sheila's Kitchen and Broad's manufacturing. The project begins with the preparation of income statements and balance sheets for Sheila's Kitchen, followed by a manufacturing account and income statement for Broad's manufacturing. It includes calculations for the break-even point, contribution margin, and margin of safety, along with an analysis of the impact of different production levels on profitability. The project also explores the difference between prime and conversion costs and calculates the number of units needed to achieve a desired profit. Finally, the project analyzes variable and fixed costs related to pizza production and their impact on cost per unit.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.