Financial Analysis: Cost of Capital for Aust Capital Supplies Report

VerifiedAdded on 2020/06/03

|9

|1027

|44

Report

AI Summary

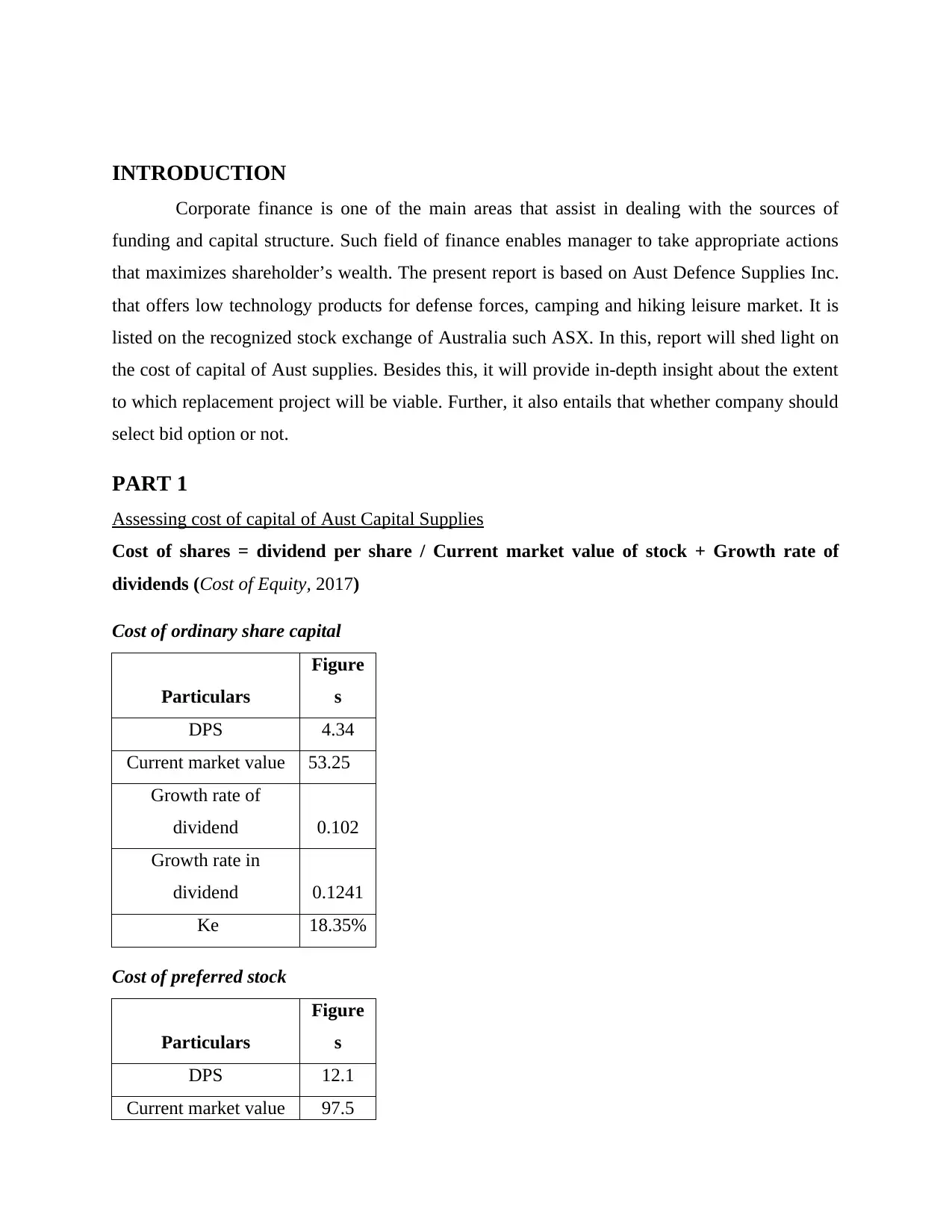

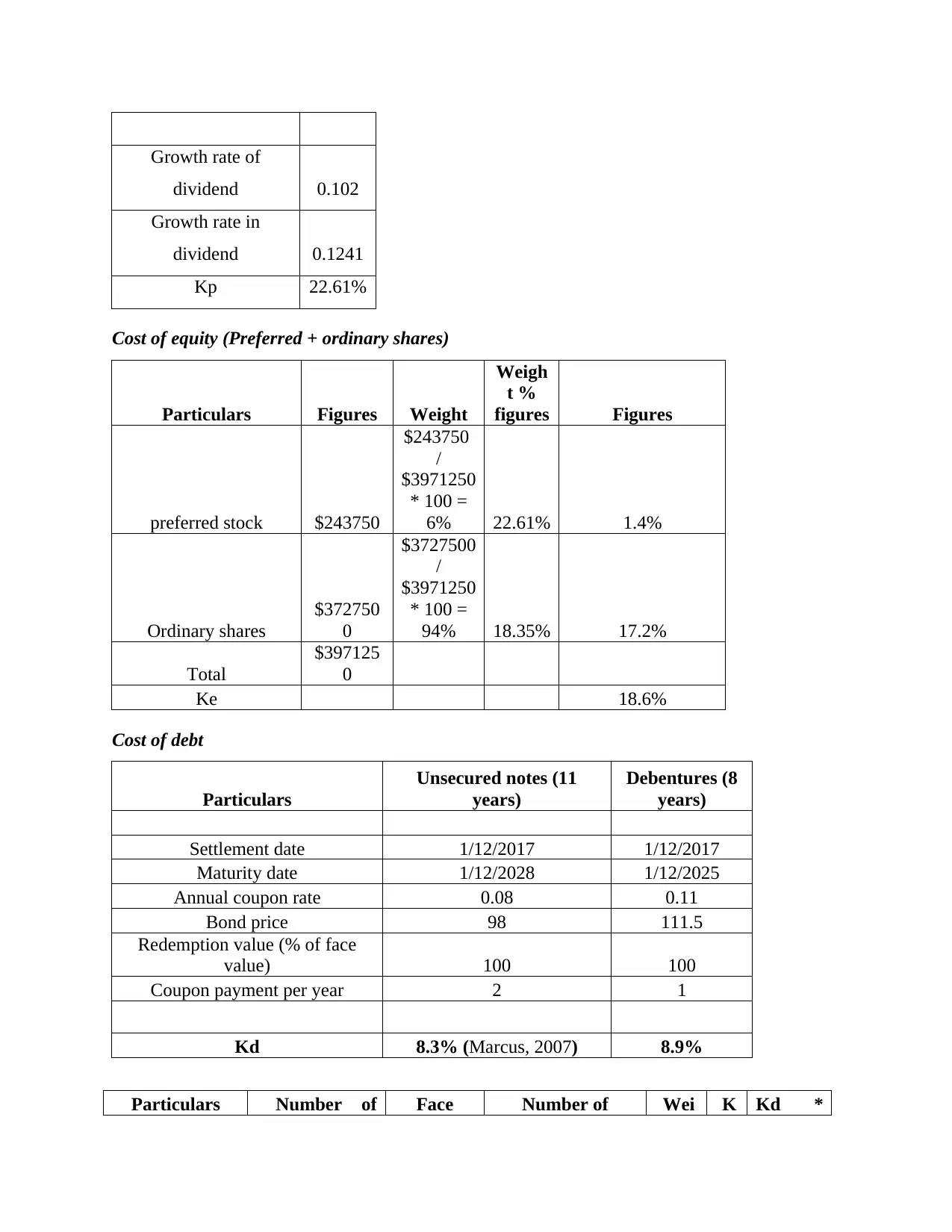

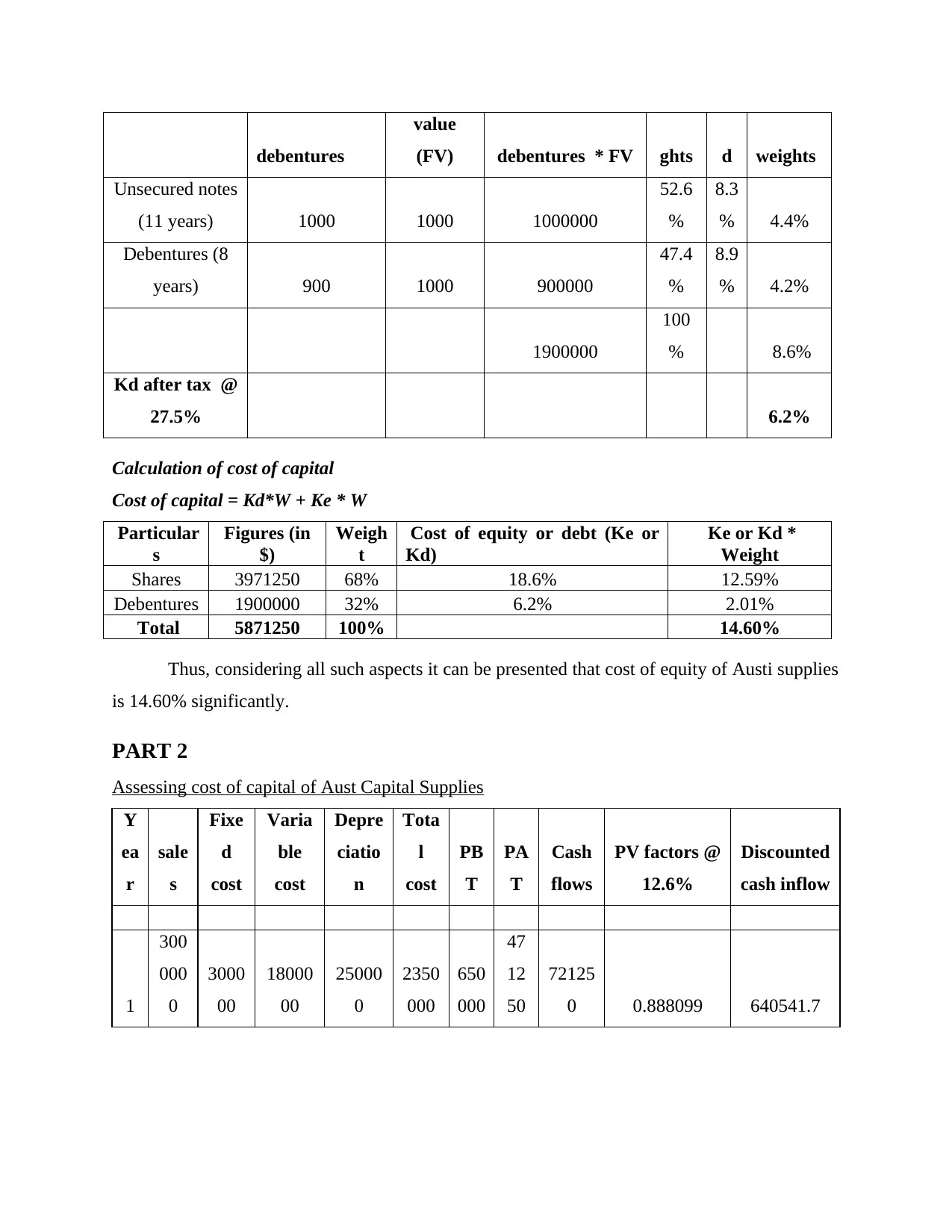

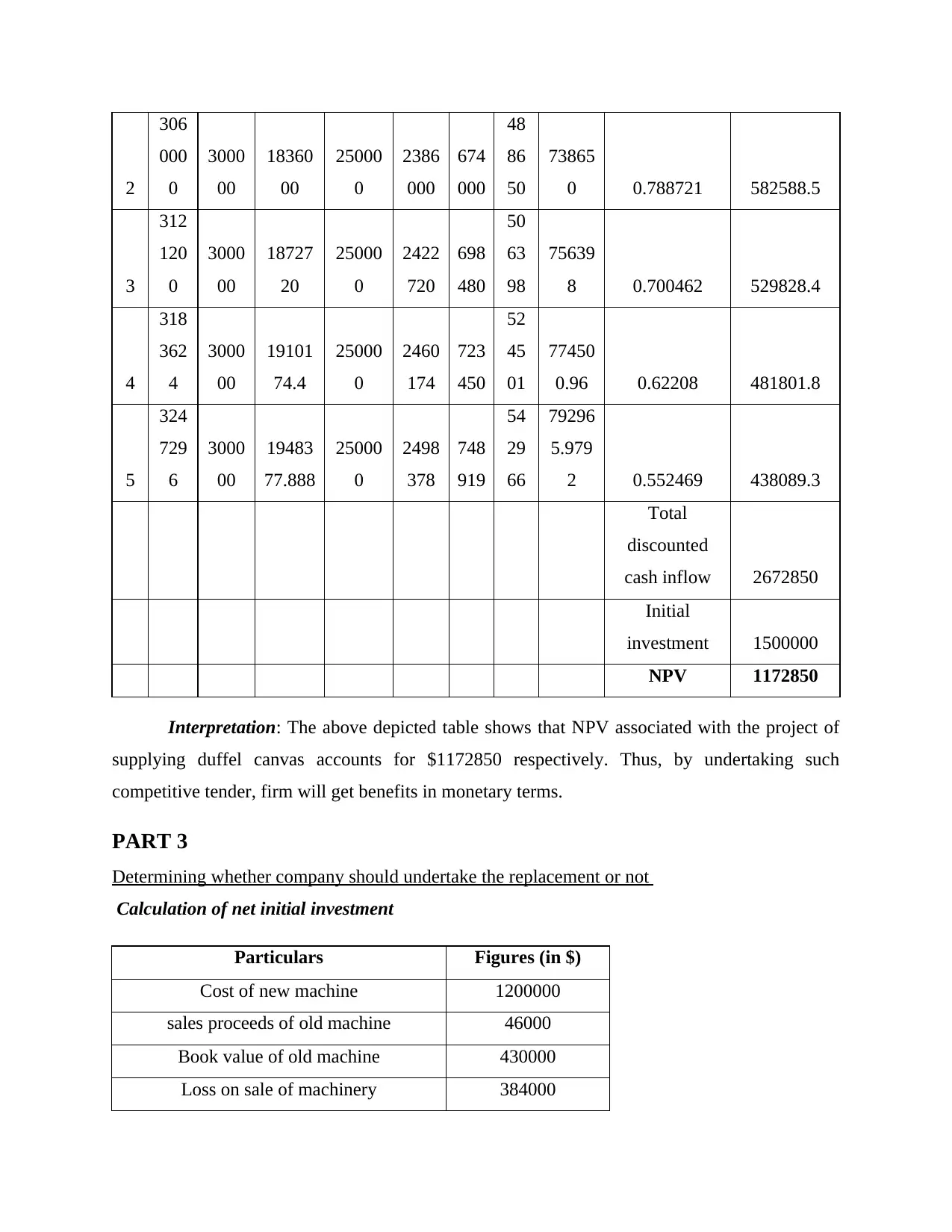

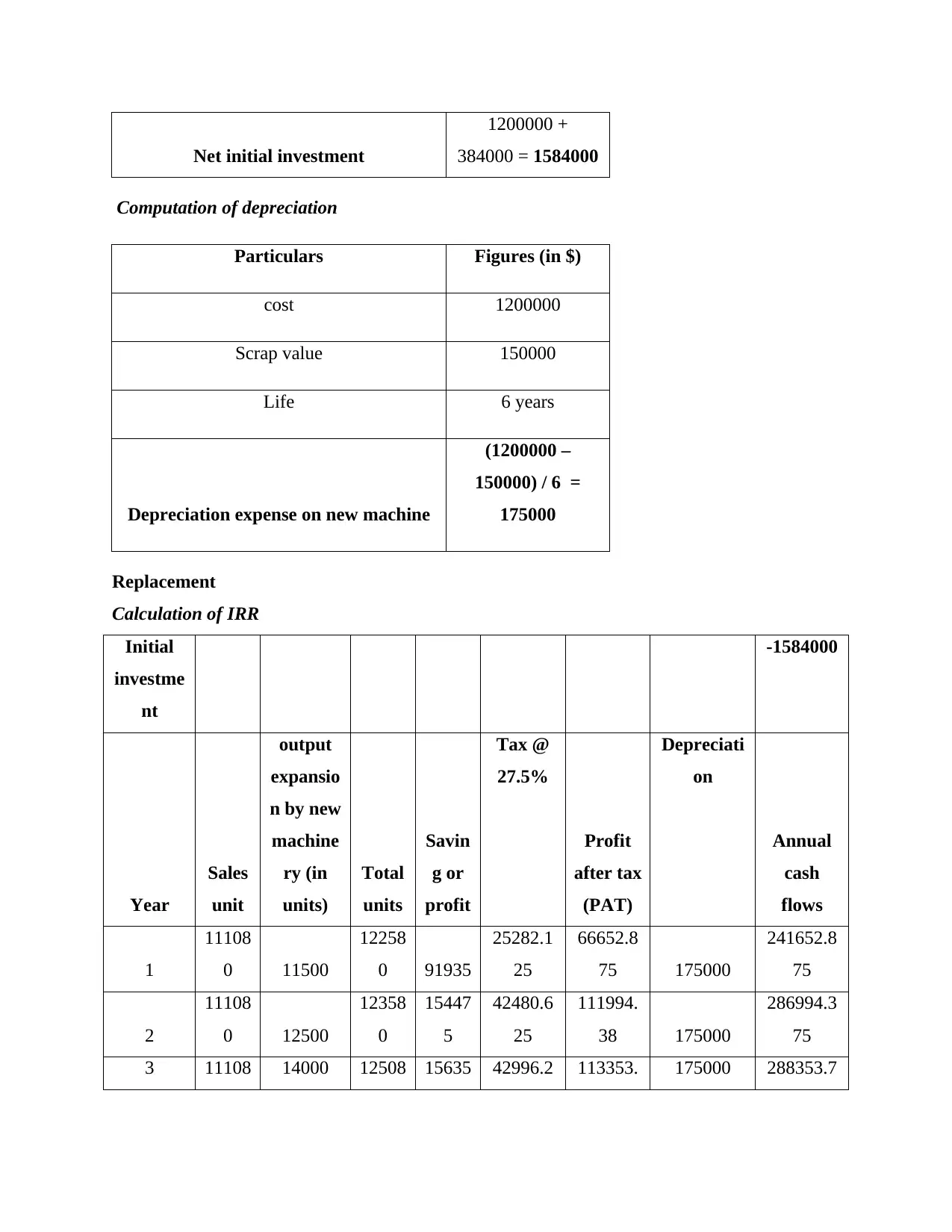

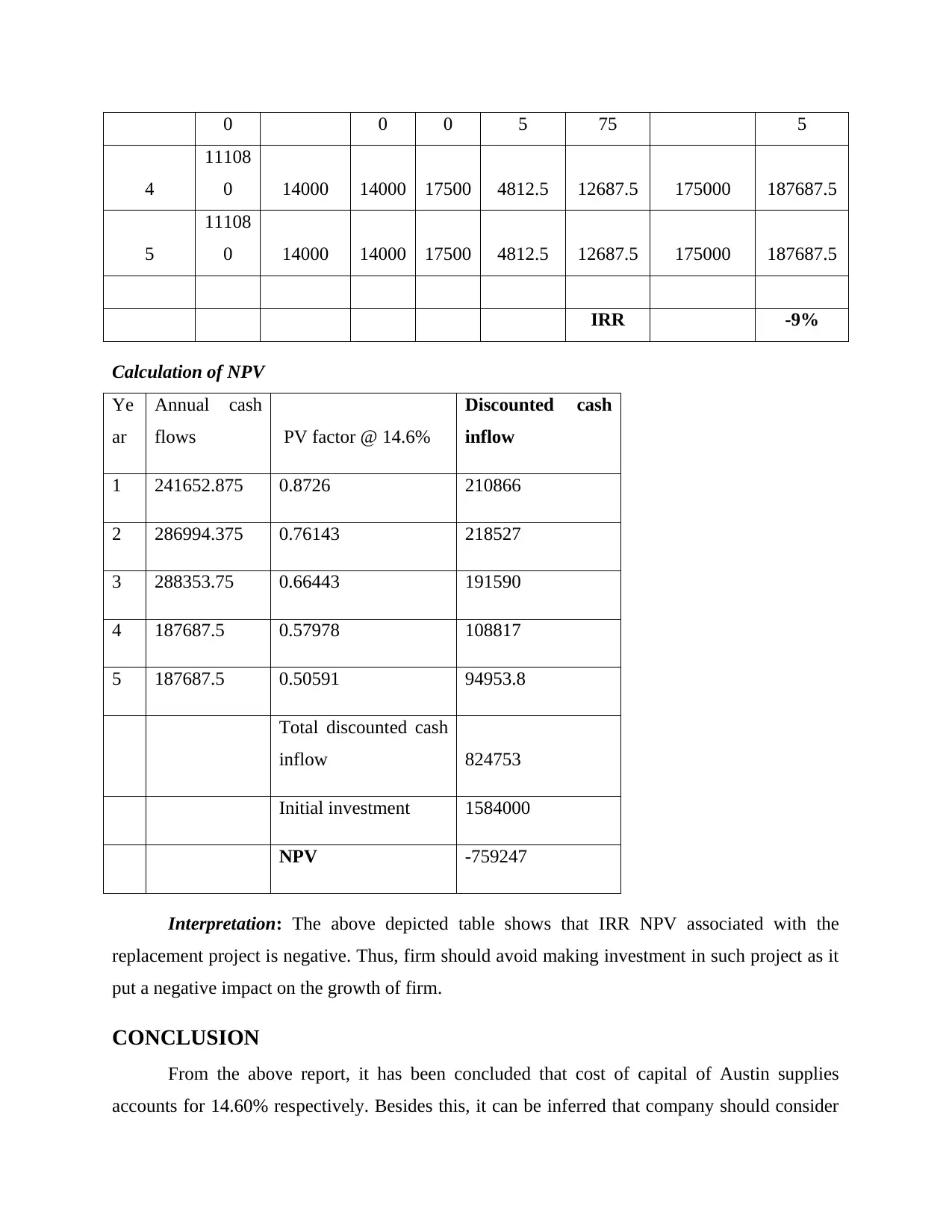

This report provides a comprehensive financial analysis of Aust Capital Supplies, focusing on its cost of capital and investment decisions. The analysis begins by calculating the cost of equity, preferred stock, and debt, ultimately determining the weighted average cost of capital (WACC) to be 14.60%. The report then evaluates a potential tender project, calculating the Net Present Value (NPV) to be $1,172,850, indicating its financial viability. Finally, the report assesses a replacement project, calculating the Net Initial Investment, Internal Rate of Return (IRR), and NPV. The negative NPV and IRR suggest that the company should not undertake the replacement strategy. The report concludes that Aust Capital Supplies should proceed with the tender project and avoid the replacement strategy, based on the financial metrics derived from the analysis.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.