(PDF) Case Examples of Project Evaluations

VerifiedAdded on 2021/05/31

|6

|1278

|54

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

To : CEO, Pinto Limited

From : STUDENT’S NAME

Date : 18TH MAY, 2018

Subject : Evaluation of introduction of new project

This project is made in order to check the feasibility of the project with the help of capital

budgeting technique. The projected cash flows are used to carry out capital budgeting.

Base case analysis:

We have used the data from the market research to perform the capital budgeting process and

calculate different metrics for the proposed project. This analysis will helps us to draw a

conclusion whether to accept the project or reject it (Adelaja, 2015).

Particulars Result Comment

Net present

value

$5,605,81

6

The present value of the future cash flows is calculated

through NPV. It can also be calculated by subtracting present

value of inflow from present value of outflow. The project

should be accepted if the NPV is positive. If the PV of cash

inflow exceeds the outflow then the project shall be accepted.

In the given case, NPV is positive and higher and therefore,

the project should be accepted.

Pay-back

period

2.73 years It is the time in which the investors recover the cost made as

an investment. A lower pay back period is favourable. In the

give case, the payback period is 2.73 years whereas the

investment period is 6 years. Therefore, the project should be

accepted.

Discounted

pay-back

period

3.38 years This is more like the payback period, only the difference is

that the cash flows that are taken in this are discounted cash

flows. This is slightly higher when compared to the payback

period. In the given case, the discounted payback period is

calculated as 3.38 years.

Profitability

Index

1.31 times Profitability index helps the investor to calculate the

profitability of the project on a single dollar invested. The

From : STUDENT’S NAME

Date : 18TH MAY, 2018

Subject : Evaluation of introduction of new project

This project is made in order to check the feasibility of the project with the help of capital

budgeting technique. The projected cash flows are used to carry out capital budgeting.

Base case analysis:

We have used the data from the market research to perform the capital budgeting process and

calculate different metrics for the proposed project. This analysis will helps us to draw a

conclusion whether to accept the project or reject it (Adelaja, 2015).

Particulars Result Comment

Net present

value

$5,605,81

6

The present value of the future cash flows is calculated

through NPV. It can also be calculated by subtracting present

value of inflow from present value of outflow. The project

should be accepted if the NPV is positive. If the PV of cash

inflow exceeds the outflow then the project shall be accepted.

In the given case, NPV is positive and higher and therefore,

the project should be accepted.

Pay-back

period

2.73 years It is the time in which the investors recover the cost made as

an investment. A lower pay back period is favourable. In the

give case, the payback period is 2.73 years whereas the

investment period is 6 years. Therefore, the project should be

accepted.

Discounted

pay-back

period

3.38 years This is more like the payback period, only the difference is

that the cash flows that are taken in this are discounted cash

flows. This is slightly higher when compared to the payback

period. In the given case, the discounted payback period is

calculated as 3.38 years.

Profitability

Index

1.31 times Profitability index helps the investor to calculate the

profitability of the project on a single dollar invested. The

profitability index is 1.31 times. This shows that the project

will earn $1.31 for every $1 invested.

Internal Rate

of return

21.14% The IRR return helps us to determine the actual return on the

investment. The IRR is compared to the required rate of

return and then the final decision is taken. If the IRR exceeds

the required rate of return then the proposal shall be accepted.

In the given case IRR is 21.14% which is exceeding the

required rate of return.

Uncertainty analysis:

We extract a lot of data from the market and carry out research before accepting the ne

project. However, complete data is not available and therefore, many assumption has to be

taken. A detailed study and analysis is carried out (Bierman & Smidt, 2010). The cash flows

as well as the discount rate are based on many assumptions and so it cannot be determined

easily. We know that the economy and the market are dynamic in nature and a small change

in the assumption might have a larger impact. Therefore, the capital budgeting process is

considered to be a risky tool (Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008).

Sensitivity Analysis:

Sensitivity analysis is involved in the process of capital budgeting which helps to know about

the sensitivity of the project when there is a change in any financial factor of the product. In

the give case, the sensitivity analysis is carried out with respect to the change in units of

sales, price of the units and the change in working capital requirement (Peterson & Fabozzi,

2012).

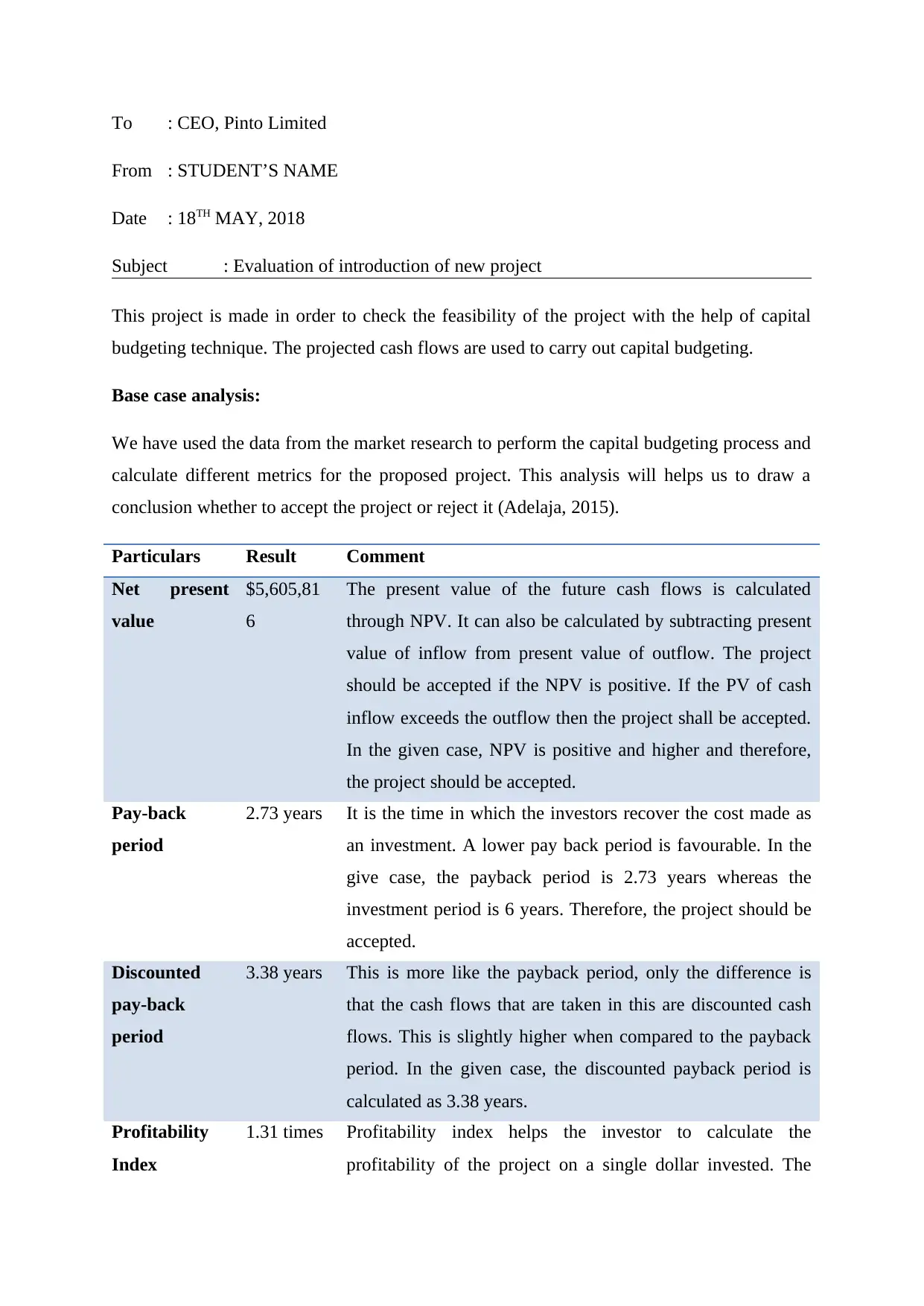

The graph shown below shows the sensitivity analysis with respect of the inputs that are

mentioned above:

will earn $1.31 for every $1 invested.

Internal Rate

of return

21.14% The IRR return helps us to determine the actual return on the

investment. The IRR is compared to the required rate of

return and then the final decision is taken. If the IRR exceeds

the required rate of return then the proposal shall be accepted.

In the given case IRR is 21.14% which is exceeding the

required rate of return.

Uncertainty analysis:

We extract a lot of data from the market and carry out research before accepting the ne

project. However, complete data is not available and therefore, many assumption has to be

taken. A detailed study and analysis is carried out (Bierman & Smidt, 2010). The cash flows

as well as the discount rate are based on many assumptions and so it cannot be determined

easily. We know that the economy and the market are dynamic in nature and a small change

in the assumption might have a larger impact. Therefore, the capital budgeting process is

considered to be a risky tool (Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008).

Sensitivity Analysis:

Sensitivity analysis is involved in the process of capital budgeting which helps to know about

the sensitivity of the project when there is a change in any financial factor of the product. In

the give case, the sensitivity analysis is carried out with respect to the change in units of

sales, price of the units and the change in working capital requirement (Peterson & Fabozzi,

2012).

The graph shown below shows the sensitivity analysis with respect of the inputs that are

mentioned above:

-2% -1% 0% 1% 2%

$4,600,000

$4,800,000

$5,000,000

$5,200,000

$5,400,000

$5,600,000

$5,800,000

$6,000,000

$6,200,000

WACC

Units sold yr1

NWC% yr1 rev

It is evident from the graph mentioned above that the slope of line representing the sensitivity

with respect to the number of units sold is the steepest. This is an indication that the project is

highly sensitive to the number of units that are sold. Therefore, the inputs that are considered

while carrying out sensitivity analysis should be chosen wisely (Rivenbark, Vogt, &

Marlowe, 2009).

Scenario analysis

Scenario analysis is one of the capital budgeting tools which help the investor have an idea of

the outcome of the project under various scenarios (Piper, 2015). The data collected for the

project based on market research are subject to many assumptions. A little change in any

requirement may affect the outcome strongly. Therefore, we conduct scenario analysis which

helps the investor understand the affect of these assumptions on the result (Seitz & Ellison,

2009). We have conducted the analyses based in changes in weighted average cost and

changes in units sold.

Scenario Rate of

return

Units

Sold

NPV Remarks

Optimist 9% 230000 $944679

5

Optimist scenario shows us the outcome of the

project when all the assumptions made come

true. This is not likely to happen since market is

dynamic

Realist 10% 200000 $560581 The realist scenario is the most likely to happen

$4,600,000

$4,800,000

$5,000,000

$5,200,000

$5,400,000

$5,600,000

$5,800,000

$6,000,000

$6,200,000

WACC

Units sold yr1

NWC% yr1 rev

It is evident from the graph mentioned above that the slope of line representing the sensitivity

with respect to the number of units sold is the steepest. This is an indication that the project is

highly sensitive to the number of units that are sold. Therefore, the inputs that are considered

while carrying out sensitivity analysis should be chosen wisely (Rivenbark, Vogt, &

Marlowe, 2009).

Scenario analysis

Scenario analysis is one of the capital budgeting tools which help the investor have an idea of

the outcome of the project under various scenarios (Piper, 2015). The data collected for the

project based on market research are subject to many assumptions. A little change in any

requirement may affect the outcome strongly. Therefore, we conduct scenario analysis which

helps the investor understand the affect of these assumptions on the result (Seitz & Ellison,

2009). We have conducted the analyses based in changes in weighted average cost and

changes in units sold.

Scenario Rate of

return

Units

Sold

NPV Remarks

Optimist 9% 230000 $944679

5

Optimist scenario shows us the outcome of the

project when all the assumptions made come

true. This is not likely to happen since market is

dynamic

Realist 10% 200000 $560581 The realist scenario is the most likely to happen

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

6 scenario as it is based on assumptions which are

mist likely to hold true.

Pessimis

t

11% 170000 $197758

9

The pessimist scenario is the worst case

scenario which is also not likely to occur. This

is the situation when the project fails to hold

true any of the assumptions on which the

outcome was dependent.

Conclusion and Recommendation

The process of capital budgeting helps the company to know about the financial viability of

the project. It helps the company to take a decision whether to accept or to reject a given

proposal. In the given case, we have decided to accept the project because of its higher

expected returns. But this outcome will hold true if the assumptions made were correct. If

there is a change in assumptions then the result might be different than what was expected.

On analysing we have found out that the project will have positive cash flows and returns

from this project are exceeding the cost. Therefore, we can conclude that this project should

be accepted (Shapiro, 2007).

mist likely to hold true.

Pessimis

t

11% 170000 $197758

9

The pessimist scenario is the worst case

scenario which is also not likely to occur. This

is the situation when the project fails to hold

true any of the assumptions on which the

outcome was dependent.

Conclusion and Recommendation

The process of capital budgeting helps the company to know about the financial viability of

the project. It helps the company to take a decision whether to accept or to reject a given

proposal. In the given case, we have decided to accept the project because of its higher

expected returns. But this outcome will hold true if the assumptions made were correct. If

there is a change in assumptions then the result might be different than what was expected.

On analysing we have found out that the project will have positive cash flows and returns

from this project are exceeding the cost. Therefore, we can conclude that this project should

be accepted (Shapiro, 2007).

Bibliography

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital

Budgeting: Financial Appraisal of Investment Projects. Cambridge: Cambridge University

Press.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Piper, M. (2015). Accounting made simple. United States: CreateSpace Pub.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide

for Local Governments. Washington, D.C.: ICMA Press.

Seitz, N., & Ellison, M. (2009). Capital Budgeting and Long-Term Financing Decisions.

New York: Thomson Learning.

Shapiro, A. C. (2007). Capital Budgeting and Investment Analysis. New Jersey: Wiley.

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital

Budgeting: Financial Appraisal of Investment Projects. Cambridge: Cambridge University

Press.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Piper, M. (2015). Accounting made simple. United States: CreateSpace Pub.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide

for Local Governments. Washington, D.C.: ICMA Press.

Seitz, N., & Ellison, M. (2009). Capital Budgeting and Long-Term Financing Decisions.

New York: Thomson Learning.

Shapiro, A. C. (2007). Capital Budgeting and Investment Analysis. New Jersey: Wiley.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.