Finance Assignment: Valuation, Investment, and Production Analysis

VerifiedAdded on 2023/01/07

|7

|1455

|24

Homework Assignment

AI Summary

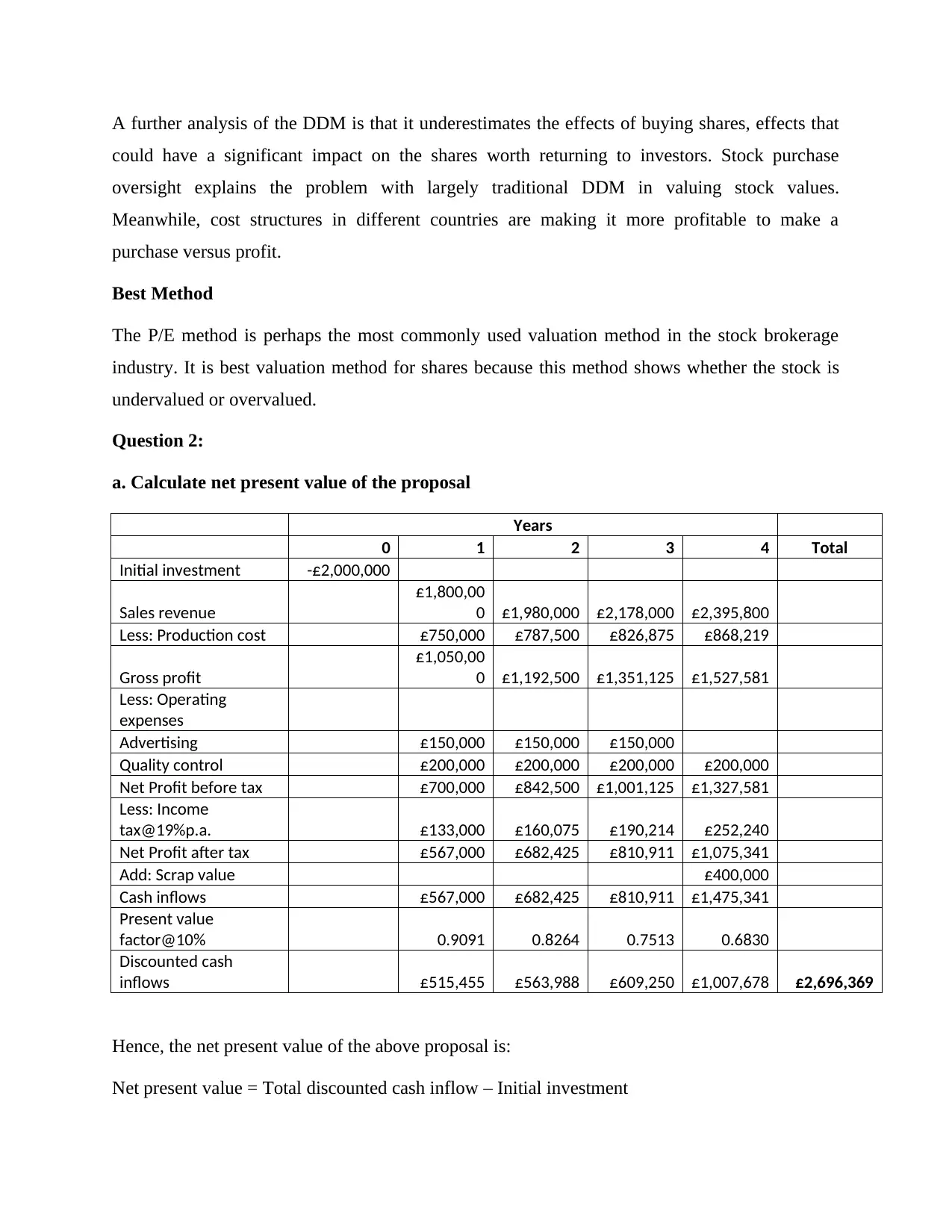

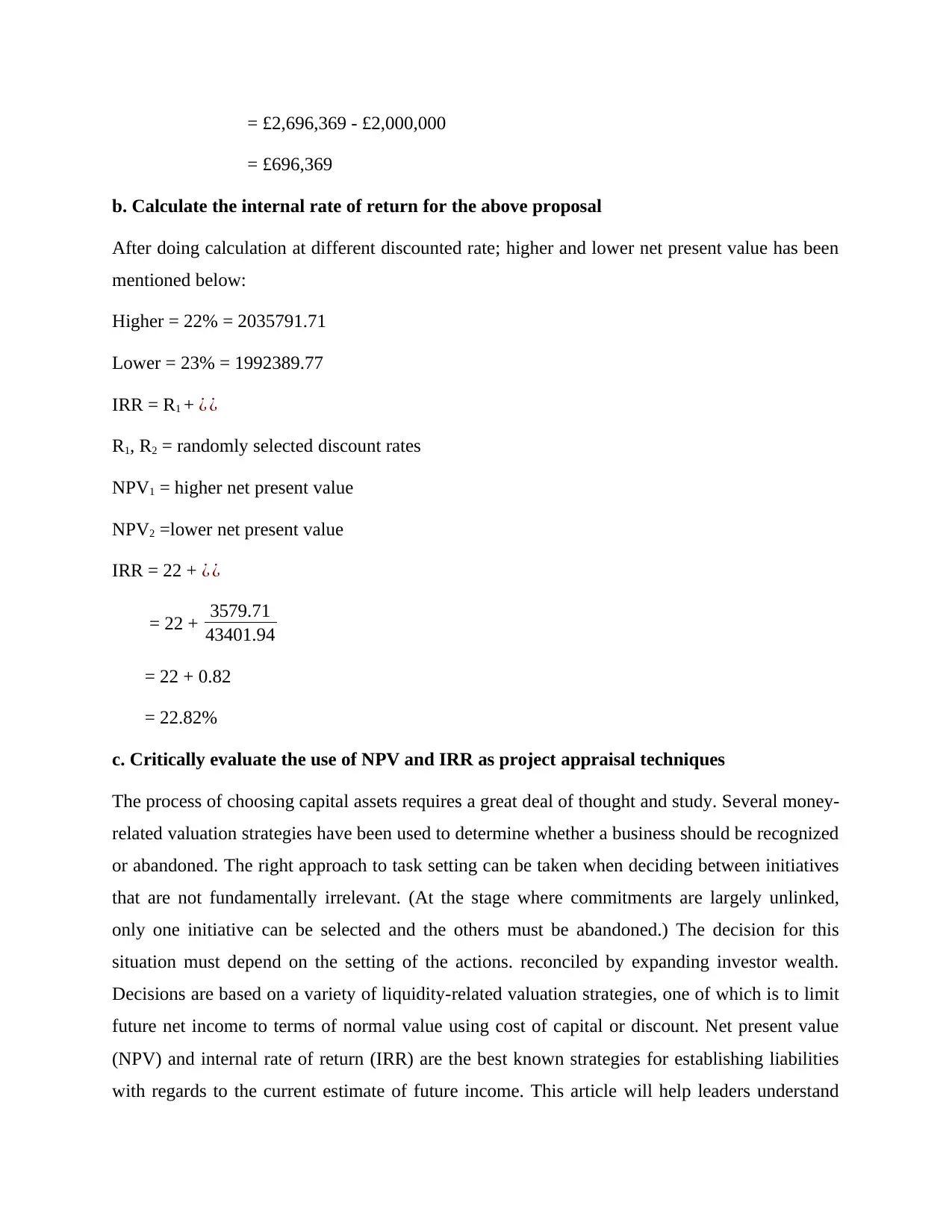

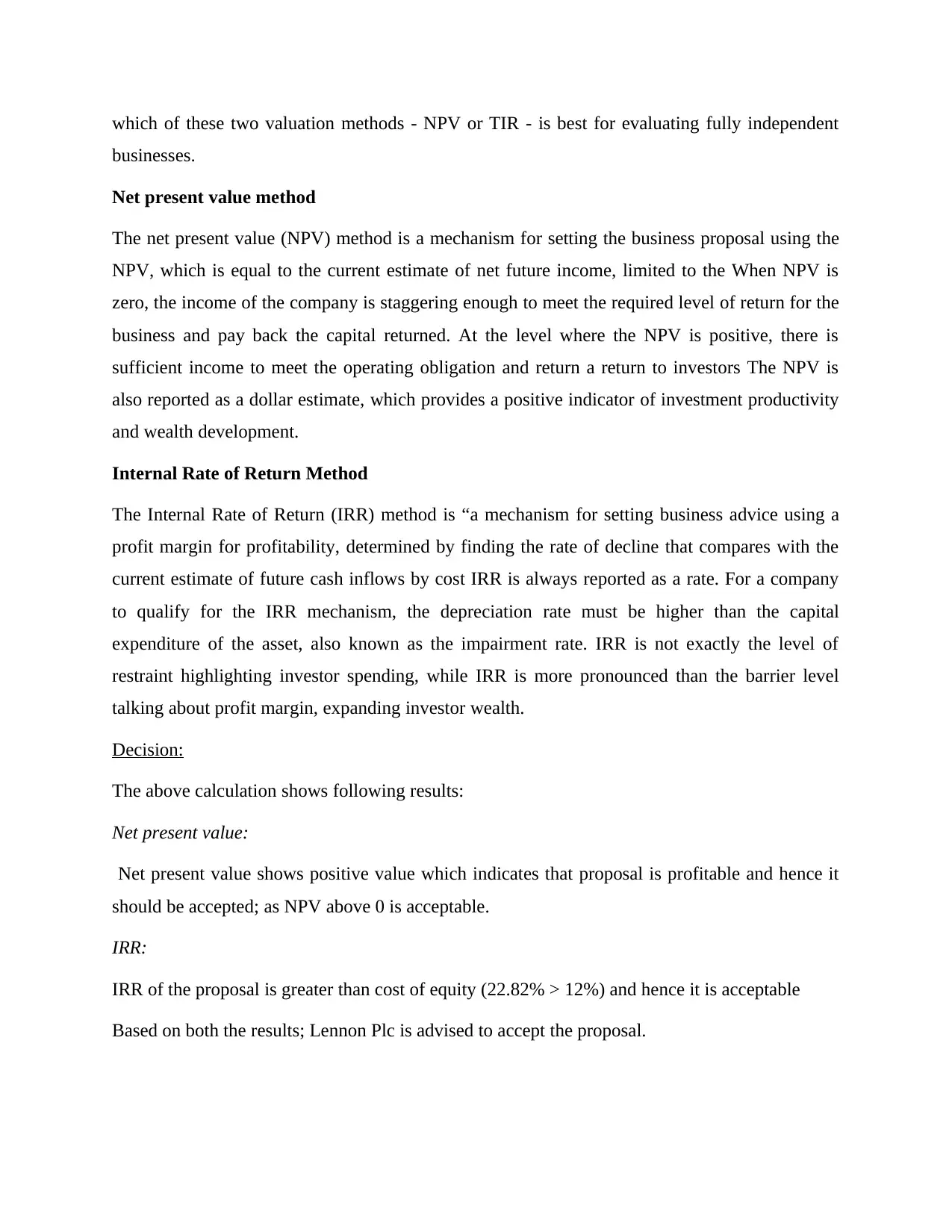

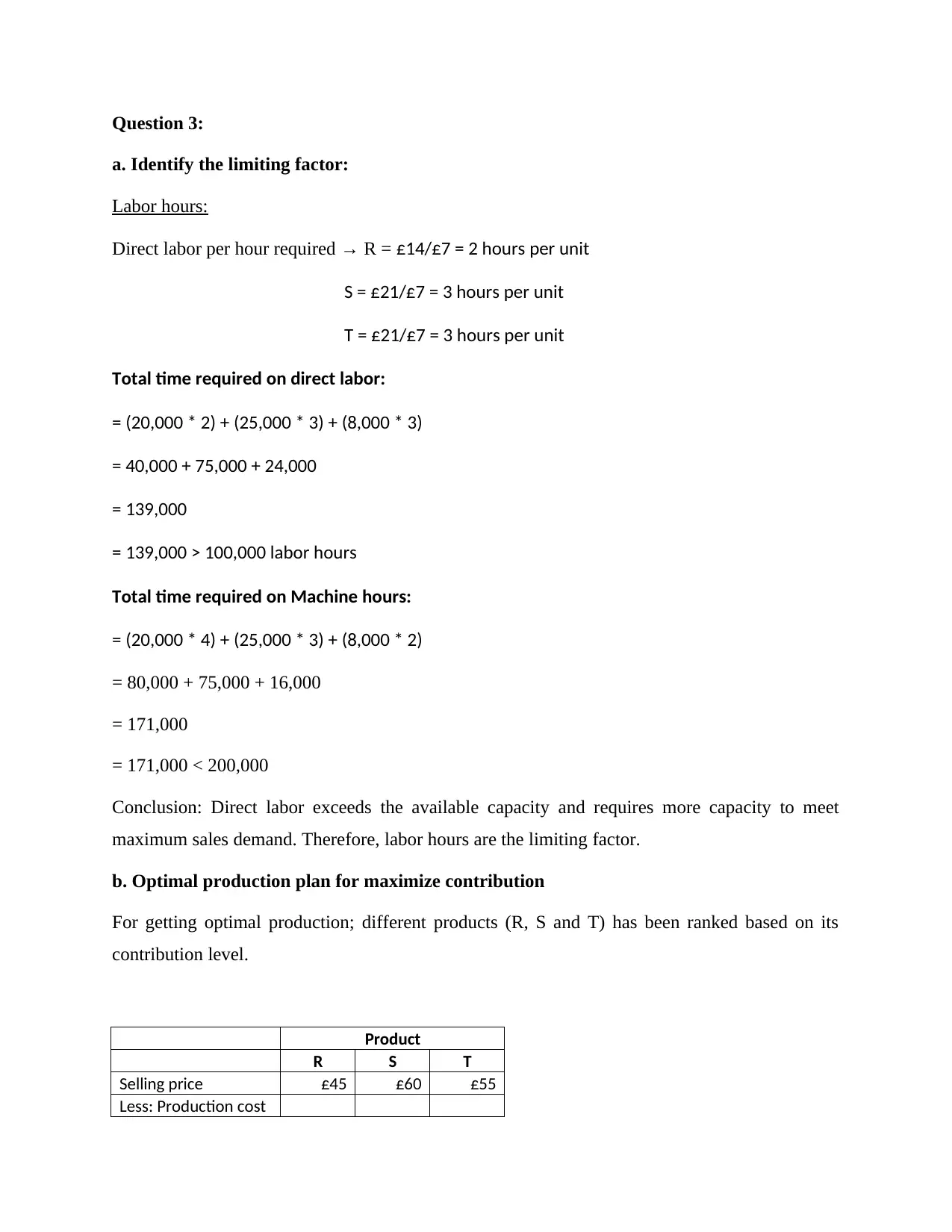

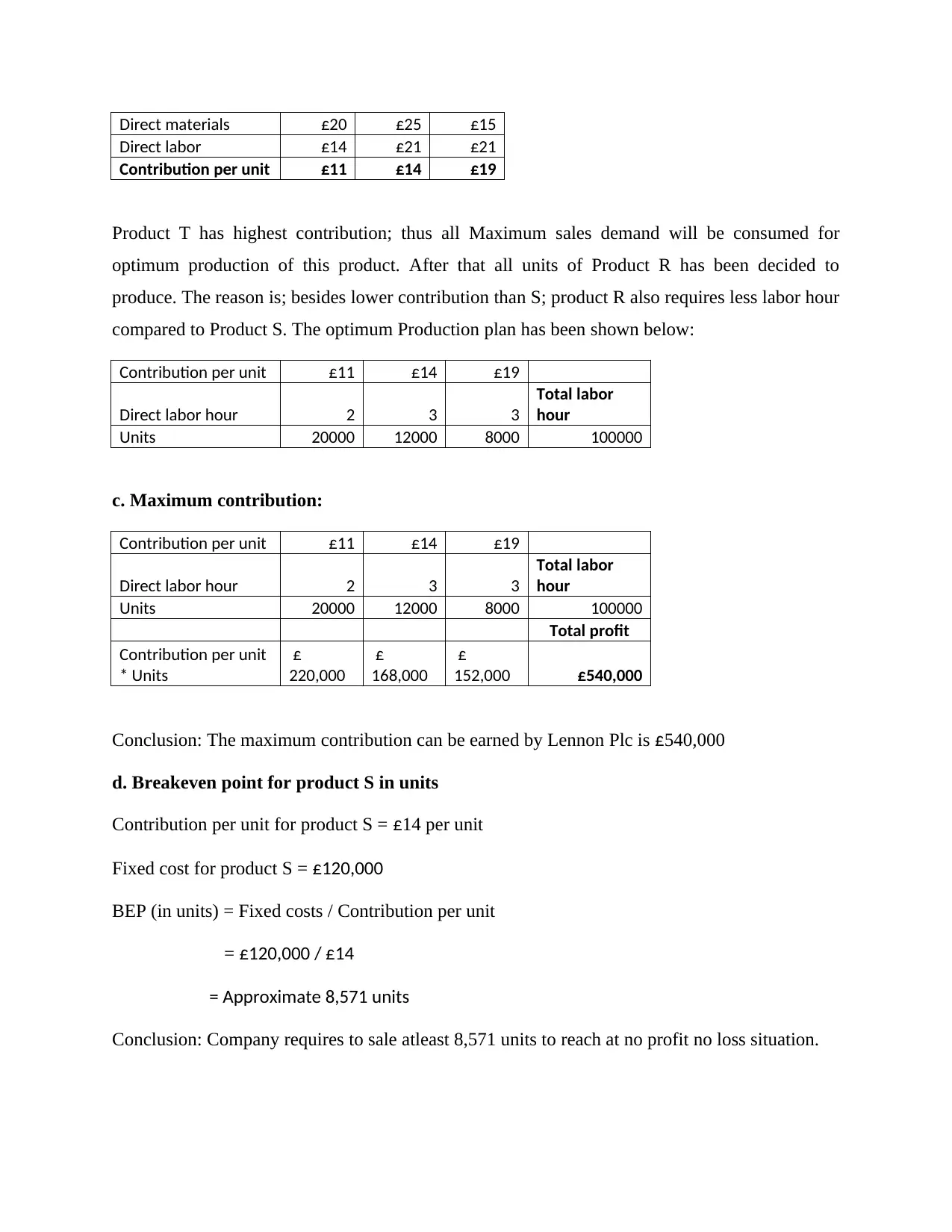

This finance assignment solution addresses three key questions. The first question involves the application of the P/E ratio and the dividend growth model for stock valuation, along with a discussion of the limitations of the dividend growth model. The second question focuses on project appraisal techniques, specifically calculating the Net Present Value (NPV) and Internal Rate of Return (IRR) of a proposed investment, and critically evaluating the use of these methods. The third question delves into production planning, identifying the limiting factor, determining the optimal production plan to maximize contribution, and calculating the breakeven point for a specific product. The solution includes detailed calculations and explanations to support the analysis, providing a comprehensive understanding of the concepts.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.