Research on Financial Account Principle

Added on 2020-06-05

31 Pages4090 Words137 Views

Financial Account Principle

Table of ContentsINTRODUCTION...........................................................................................................................3Report to Line Manager...............................................................................................................4Client 1.............................................................................................................................................6A. Preparation of Journal entries.................................................................................................6B. Ledger accounts ......................................................................................................................8C. Trial balance..........................................................................................................................16Client 2...........................................................................................................................................17A. Statement of Profit and Loss.................................................................................................17B. Preparing balance sheet of Peter piper .................................................................................18Client 3...........................................................................................................................................20A. Producing Income statement.................................................................................................20B. Preparing Statement of Financial Position ...........................................................................21C. Consistency and Prudency concepts.....................................................................................26D. Outlining purpose of depreciation.........................................................................................27Client 4...........................................................................................................................................28A. Preparation of Bank Reconciliation Statement ....................................................................28B. Causes of varying bank records with accounting books.......................................................29C. Producing Bank Reconciliation Statement............................................................................29Client 5...........................................................................................................................................29A. Sales ledger control account and Purchase ledger control account......................................29B. Explaining meaning of control account................................................................................30Client 6...........................................................................................................................................31A. Meaning and features of suspense account...........................................................................31

B. Drafting trial balance.............................................................................................................31C. Preparing journal entries.......................................................................................................32D. Differentiating suspense and clearing account......................................................................32CONCLUSION..............................................................................................................................33REFERENCES..............................................................................................................................34INTRODUCTIONAccounting plays crucial role in the company to prepare final accounts in effectivemanner. Present report deals with preparation of financial statements of 6 clients and showingfinancial position. Moreover, accounting principles and concepts are discussed in the report.Accounting guidelines issued by various professional bodies are explained as well. Furthermore,trial balance and ledger accounts are prepared for the clients. Moreover, sales and purchaseledger control both are produced. Thus, it can be said that financial accounting principlesprovides way to produce correct financial statements of the business.

Report to Line ManagerTo: Line ManagerSubject: Importance of accounting regulations and concepts in the business and variousconcepts for achieving growth of company.Define financial accounting: - Financial accounting is a financial statement of a company. Infinancial statement we include income statement and balance sheet of the company. It is theprocess of recording, summarising, classifying and interpreting the financial statement of acompany. Financial accounting is the accounting activities of the company and it’s apreparation of profit and loss accounts and balance sheet of a company. Company issue theirfinancial statement time to time and assess the statement regularly (Warren and Jones, 2018).The main purpose of financial accounting is to forecast for the company, how to earn moreprofits in future. Financial statement include cash flow, income statement, balance sheet,retained earnings. In income statements include revenue and expenses of the company. Cashflow include operating, investing and financing activities of the company. Balance sheet is astatement of financial year it include assets, liabilities, capital equity etc. Financial statementalso shows the financial condition of a company. There are some principle regarding financialaccounting that is company report should be easy to understand and credible and comparable.Financial accounting follow the common rules which is accounting standards. Financialaccounting is differ from managerial accounting and its forecast the financial reports of thecompany and this reports shows to the stakeholders, regulators of the company.The IASB(International Accounting Standards Board) objective is to provide financial information toinvestor, shareholders and lenders. And then decision involves buying, selling, or holdingequity and to provide loans from credit.Explain regulation relating to financial accounting: - The main purpose of financialaccounting is to forecast for the company. In the financial accounting prepared profit and lossstatement and statement of financial position of partnership to examine. The accountingstandards are designed for betterment of financial accounting. In accounting standards includewhat transaction should be shown in financial statement (Mullinova, 2016). The main purposeof creating accounts standards is to define proper accounting practice with in legal framework.The necessity of accounting regulation is when an individual choose to start a business. Theneed for accounting standards only becomes apparent when the key characteristics of thevarious mediums through which business venture can be carried. Financial accountingfocusses on the following areas that is identification and recording of financial information. Infinancial accounting the activities should be reported. In this include clarity, accuracymaterialistic data which helps in better to judge a report. Financial statement are preparedunder regulatory framework. First is professional regulation, in this its outline thatrecommended methods that can be used to value inventory and to provide guidance on wheninventory should be recognised. The next international regulation, in this the main aim of theIASC was to promote the company worldwide and compare consistency in financialstatements with other companies. ISAB main aim is to establish open participatory andtransparent due process, collaborate globally for standard setting community and to connectwith investors, regulators, business leaders and the global accountancy profession at everystage of process. The ISAB has full control on developing and set its own technical aspects.Describe accounting rules and principles: - The rules and concepts that govern inaccounting. The main purpose of accounting principle is the accounting is based on legalistic

accounting which is detailed or complicated. If any company distribute their financialstatements to the shareholder or to the public so its required to follow generally acceptedaccounting principle for preparing financial statements (Libby, 2017). Some basic accountingprinciple are:-The business as a single entity concept:- The business is a single entity . Business allactivities are treated separately .A business can run long after the existence of its owner.The specific currency principle: - All country have their own currency. Some companieswho conduct business in foreign currencies ant then convert the currencies in prevalentexchange rate of currency.The specific time period principle: - Financial statement prepare in a specific time period. Inincome statement there is start date and end date. And balance sheet is prepare on a certaindate.The Historical Cost Principle: - The prices which is items were bought and sold its valuationis done in financial statements. The real value may changes in inflation and recession time.The Full Disclosure Principle: - This principle focuses on all accounting scandals in news nowdays. And company should reveal all the relevant aspects of the functioning.The Recognition Principle: - In this principle companies reveals their income and expenses inthe same time period in which they were accrued.The Non-Death Principle of Businesses:-In this principle businesses will continue to function eternally and have no end date as such.The Matching Principle: - In this principle the accrual system of accounting should be used forevery debit there should be credit.The Principle of Materiality: - the report should be materialistic and accurate. There areinaccuracy in records of financial accounting so the company note judge the right and not toforecast (KHAJAVI and EBRAHIMI, 2017).The Principle of Conservative Accounting: - In this principle expenses are recordedimmediately but incomes are recorded only when it comes in cash.Explain the conventions and concepts relating to consistency and material disclosure:-Conventions includes those customs or tradition which is help the accountants while preparingthe accounting statements. Some accounting conventions are:-Convention of disclosure: - The term disclosure only implies that there is information whichis material to all which is invested in company. It implies that accounts should be prepared thatall material information is clearly disclosed to the reader. The idea behind this convention isthat nobody can misuse the reports of a company. Convention of materiality: - In this convention only those items should recorded which issignificant and insignificant items should be ignored. This is used because of accounting willbe over burden. An item material for one concern may be immaterial for another (EBRAHIMI,TALEBNIA, VAKILIFARD and NIKOUMARAM, 2017).Convention of consistency: - This convention implies that accounting practices should remainunchanged from one year to another. Consistency does not mean inflexibility. If introductionof innovative techniques and changes become necessary, the change and its effect should beclear.

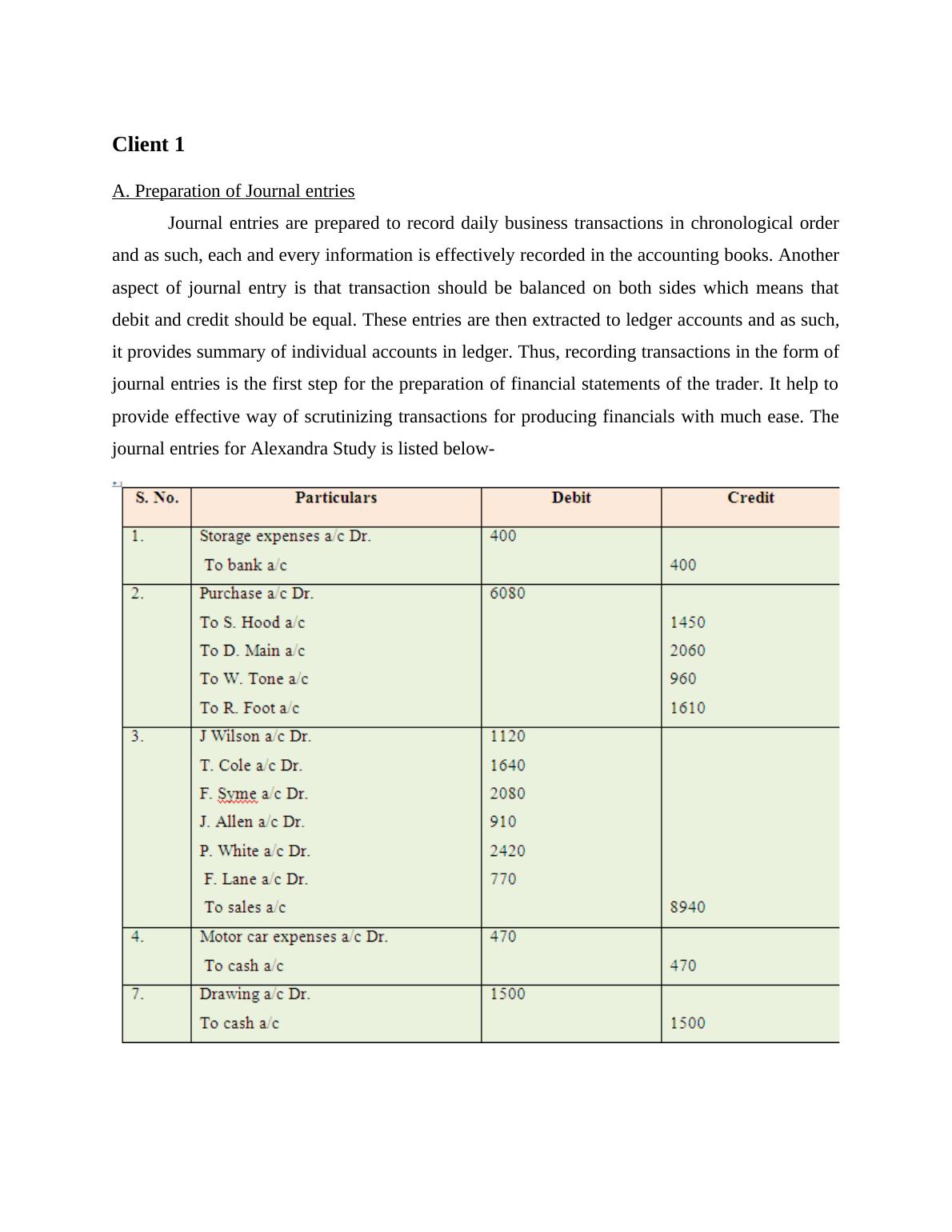

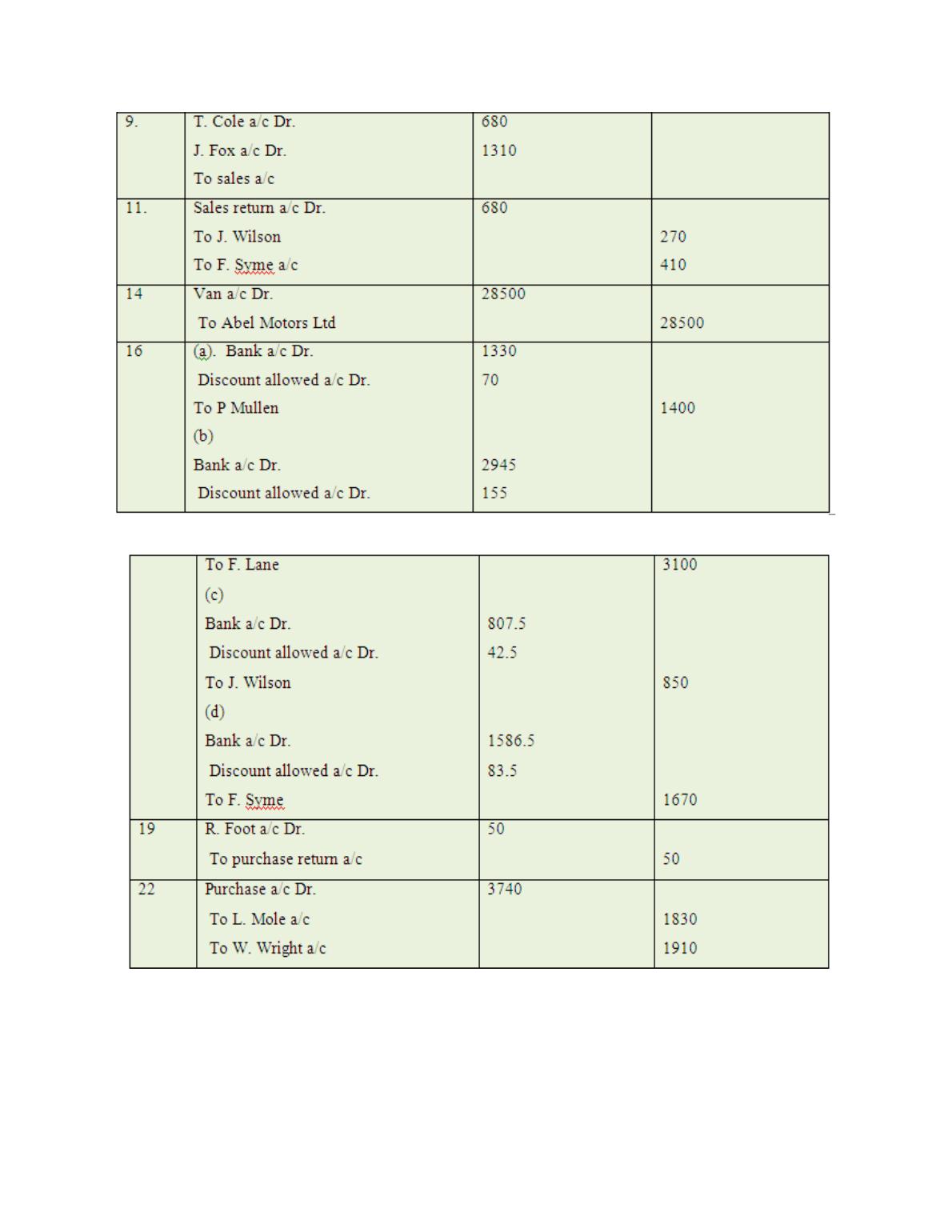

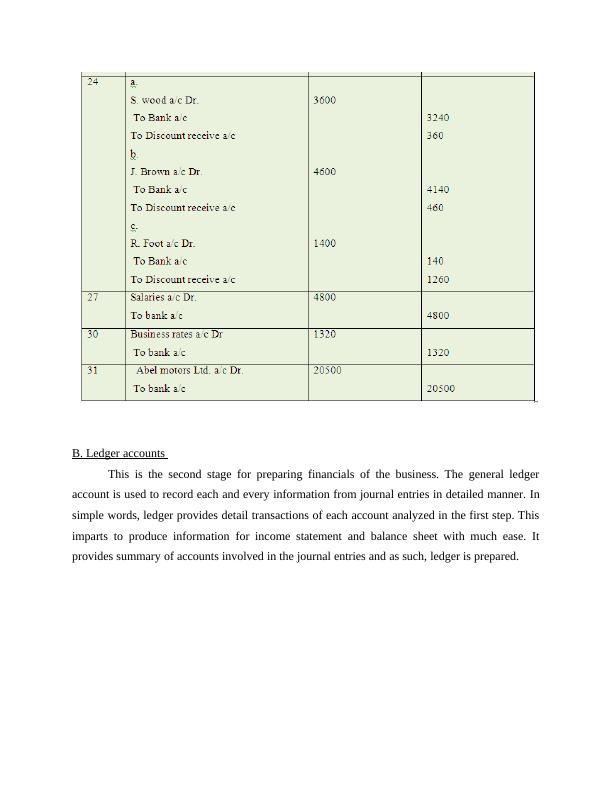

Client 1A. Preparation of Journal entriesJournal entries are prepared to record daily business transactions in chronological orderand as such, each and every information is effectively recorded in the accounting books. Anotheraspect of journal entry is that transaction should be balanced on both sides which means thatdebit and credit should be equal. These entries are then extracted to ledger accounts and as such,it provides summary of individual accounts in ledger. Thus, recording transactions in the form ofjournal entries is the first step for the preparation of financial statements of the trader. It help toprovide effective way of scrutinizing transactions for producing financials with much ease. Thejournal entries for Alexandra Study is listed below-

B. Ledger accounts This is the second stage for preparing financials of the business. The general ledgeraccount is used to record each and every information from journal entries in detailed manner. Insimple words, ledger provides detail transactions of each account analyzed in the first step. Thisimparts to produce information for income statement and balance sheet with much ease. Itprovides summary of accounts involved in the journal entries and as such, ledger is prepared.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting Principles: Assignmentlg...

|40

|3645

|142

Assignment on Financial Accounting pdflg...

|47

|5713

|177

Importance of Accounting in Preparation of Financial Statements - Reportlg...

|34

|4240

|26

Accounting Principles and Ruleslg...

|39

|4332

|322

Financial Accounting Principles and Conceptslg...

|38

|3915

|73

Financial Accounting & Principles Assignmentlg...

|37

|2902

|88