The Regulatory Environment and Financial Reporting

Prepare a 2 page newsletter summarizing changes and developments in the financial reporting environment from 1 December 2018 to 31 March 2019.

7 Pages848 Words75 Views

Added on 2023-01-13

About This Document

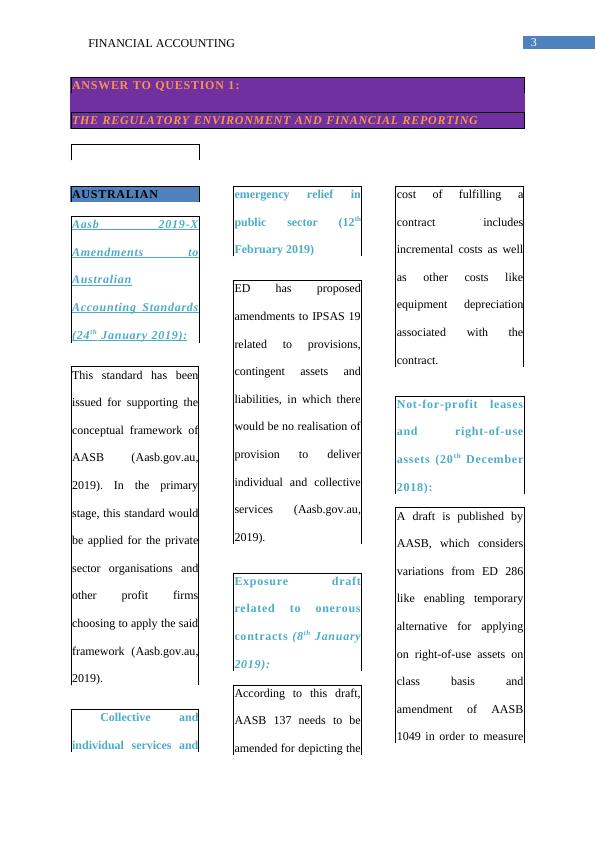

This document provides an overview of the regulatory environment and financial reporting in the field of financial accounting. It discusses the amendments to Australian accounting standards, including the proposed amendments to IPSAS 19 and the changes in funding liabilities. It also explores the usefulness of special purpose financial statements and the impact of IFRS 16 on leasing. The document includes references for further reading.

The Regulatory Environment and Financial Reporting

Prepare a 2 page newsletter summarizing changes and developments in the financial reporting environment from 1 December 2018 to 31 March 2019.

Added on 2023-01-13

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

The Regulatory Environment for Financial Reporting

|6

|835

|56

Accounting and Financial Management

|9

|1494

|98

Advanced Financial Accounting

|8

|1542

|92

IFRS 16 Leases: Implications for Lessor and Lessee

|10

|1947

|210

Changes in Accounting Standard by AASB from 1 December 2018 to 31 March 2019

|8

|1575

|34

Newsletter and Financial Statements

|7

|1407

|310