Financial Accounting

Added on 2022-12-27

14 Pages2916 Words416 Views

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note

FINANCIAL ACCOUNTING

1

Table of Contents

Answer to Question 1................................................................................................................2

Answer to Question 2................................................................................................................2

Working Notes.......................................................................................................................2

Consolidated Financial Statement of P CO...........................................................................3

Answer to Question 3................................................................................................................4

Purpose of Preparing Consolidated Financial Statements.....................................................4

Non-Controlling Interest.......................................................................................................4

Principles of Consolidated Financial Statements..................................................................5

Consolidated Financial Statement.........................................................................................6

Answer to Question 4................................................................................................................6

Translation of Foreign Currency...........................................................................................7

Answer to Question 5................................................................................................................8

Approaches for Corporate Reporting....................................................................................8

Integrated Reporting Framework..........................................................................................9

Analysis of the Article.........................................................................................................10

Reference.................................................................................................................................12

1

Table of Contents

Answer to Question 1................................................................................................................2

Answer to Question 2................................................................................................................2

Working Notes.......................................................................................................................2

Consolidated Financial Statement of P CO...........................................................................3

Answer to Question 3................................................................................................................4

Purpose of Preparing Consolidated Financial Statements.....................................................4

Non-Controlling Interest.......................................................................................................4

Principles of Consolidated Financial Statements..................................................................5

Consolidated Financial Statement.........................................................................................6

Answer to Question 4................................................................................................................6

Translation of Foreign Currency...........................................................................................7

Answer to Question 5................................................................................................................8

Approaches for Corporate Reporting....................................................................................8

Integrated Reporting Framework..........................................................................................9

Analysis of the Article.........................................................................................................10

Reference.................................................................................................................................12

FINANCIAL ACCOUNTING

2

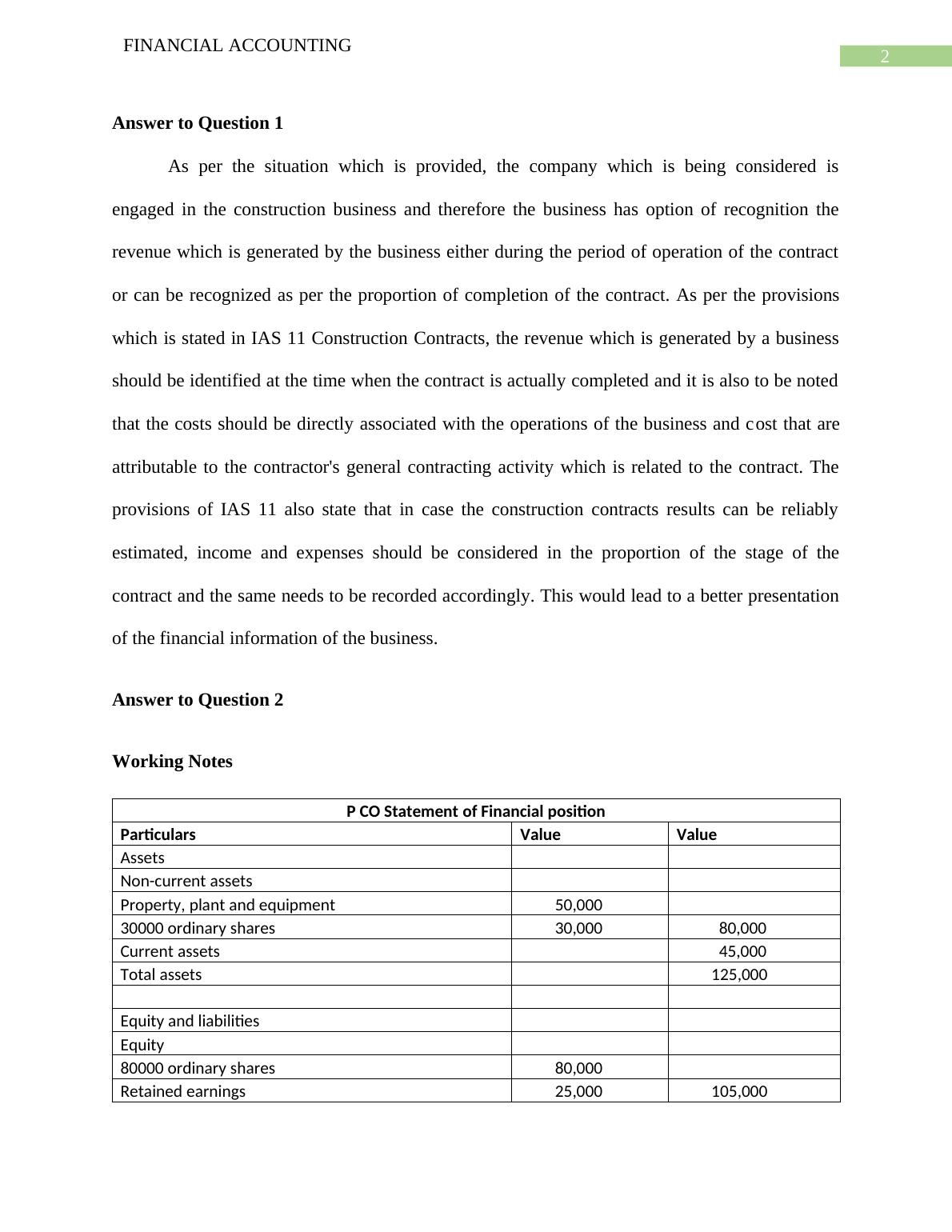

Answer to Question 1

As per the situation which is provided, the company which is being considered is

engaged in the construction business and therefore the business has option of recognition the

revenue which is generated by the business either during the period of operation of the contract

or can be recognized as per the proportion of completion of the contract. As per the provisions

which is stated in IAS 11 Construction Contracts, the revenue which is generated by a business

should be identified at the time when the contract is actually completed and it is also to be noted

that the costs should be directly associated with the operations of the business and cost that are

attributable to the contractor's general contracting activity which is related to the contract. The

provisions of IAS 11 also state that in case the construction contracts results can be reliably

estimated, income and expenses should be considered in the proportion of the stage of the

contract and the same needs to be recorded accordingly. This would lead to a better presentation

of the financial information of the business.

Answer to Question 2

Working Notes

P CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 50,000

30000 ordinary shares 30,000 80,000

Current assets 45,000

Total assets 125,000

Equity and liabilities

Equity

80000 ordinary shares 80,000

Retained earnings 25,000 105,000

2

Answer to Question 1

As per the situation which is provided, the company which is being considered is

engaged in the construction business and therefore the business has option of recognition the

revenue which is generated by the business either during the period of operation of the contract

or can be recognized as per the proportion of completion of the contract. As per the provisions

which is stated in IAS 11 Construction Contracts, the revenue which is generated by a business

should be identified at the time when the contract is actually completed and it is also to be noted

that the costs should be directly associated with the operations of the business and cost that are

attributable to the contractor's general contracting activity which is related to the contract. The

provisions of IAS 11 also state that in case the construction contracts results can be reliably

estimated, income and expenses should be considered in the proportion of the stage of the

contract and the same needs to be recorded accordingly. This would lead to a better presentation

of the financial information of the business.

Answer to Question 2

Working Notes

P CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 50,000

30000 ordinary shares 30,000 80,000

Current assets 45,000

Total assets 125,000

Equity and liabilities

Equity

80000 ordinary shares 80,000

Retained earnings 25,000 105,000

FINANCIAL ACCOUNTING

3

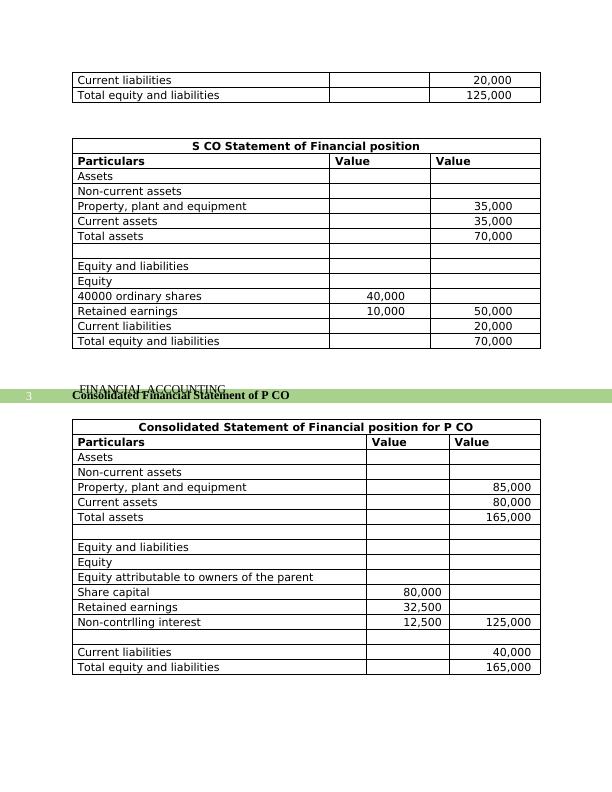

Current liabilities 20,000

Total equity and liabilities 125,000

S CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 35,000

Current assets 35,000

Total assets 70,000

Equity and liabilities

Equity

40000 ordinary shares 40,000

Retained earnings 10,000 50,000

Current liabilities 20,000

Total equity and liabilities 70,000

Consolidated Financial Statement of P CO

Consolidated Statement of Financial position for P CO

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 85,000

Current assets 80,000

Total assets 165,000

Equity and liabilities

Equity

Equity attributable to owners of the parent

Share capital 80,000

Retained earnings 32,500

Non-contrlling interest 12,500 125,000

Current liabilities 40,000

Total equity and liabilities 165,000

3

Current liabilities 20,000

Total equity and liabilities 125,000

S CO Statement of Financial position

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 35,000

Current assets 35,000

Total assets 70,000

Equity and liabilities

Equity

40000 ordinary shares 40,000

Retained earnings 10,000 50,000

Current liabilities 20,000

Total equity and liabilities 70,000

Consolidated Financial Statement of P CO

Consolidated Statement of Financial position for P CO

Particulars Value Value

Assets

Non-current assets

Property, plant and equipment 85,000

Current assets 80,000

Total assets 165,000

Equity and liabilities

Equity

Equity attributable to owners of the parent

Share capital 80,000

Retained earnings 32,500

Non-contrlling interest 12,500 125,000

Current liabilities 40,000

Total equity and liabilities 165,000

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Advanced Financial Accounting Theorylg...

|8

|898

|24

Financial Statements and Variance Analysis for Non-Profit Organizationslg...

|12

|600

|344

Financial Performance Evaluation of DP World and PSA Internationalslg...

|14

|3285

|490

Financial Accounting: Consolidated Statement of Financial Position and Relevance, Reliability, and Comparability of Financial Informationlg...

|12

|3642

|435

Importance of Professional Ethics in Accountinglg...

|13

|3940

|29

COMPANY ACCOUNTING.lg...

|7

|493

|1