P1: Double entry bookkeeping system of debits and credits

Added on 2021-01-03

16 Pages1395 Words327 Views

Financial Accounting Part 1

TABLE OF CONTENTSTable of Contents.............................................................................................................................2INTRODUCTION...........................................................................................................................1TASK 1............................................................................................................................................1P1: Double entry bookkeeping system of debits and credits..................................................1P2: Preparation of trail balance..............................................................................................6TASK 2............................................................................................................................................7P3: Formulation of financial statements.................................................................................7P4: Preparation of financial statements for sole trader and limited companies.....................8CONCLUSION..............................................................................................................................13REFERENCES..............................................................................................................................14

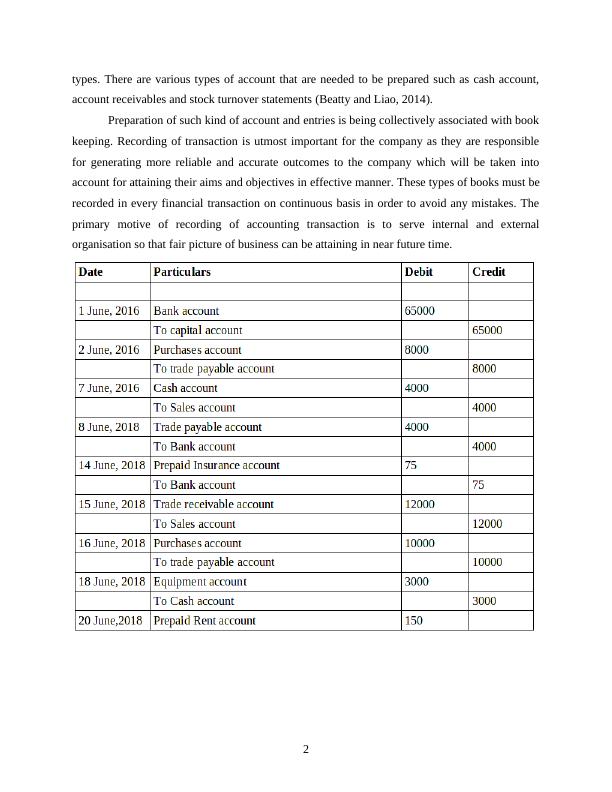

INTRODUCTIONFinance is considered as life blood of the company. Most of the time an organisation usedto prefer resources utilisation by the help of using numerous funds and capital. Financialaccounting is an important area of finance that is concerned with overall summary, analysis andreporting of different types of transactions those are done in an accounting period. This projectpart provides specific information about use of double entry bookkeeping system as well aspreparation of trail balances by the help of balance off rules to finish the ledger. Apart from this,preparation of final account is also being done by adjusting accruals, depreciation andprepayments (Edwards, 2013). Understanding of several final accounts that are prepared bythrough using different types of organisation is done accordingly. TASK 1P1: Double entry bookkeeping system of debits and creditsIn every business organisation, it is vital for them to make use of various accounting dealthat are done during the period of time. Double entry system of accounting means that allbusiness transaction used to get involve into two accounts. Like for example, in case companyborrows certain amount of money from their bank, the company’s overall cash account wouldhave enhanced and its liability of loans must be payable by the parties. In case of double entrysystem which is equal value of funds that always transferred from one statements to another.Accountants can use debit and credit terms in order to determine, whether the money is beingtransferred from the account books (Weil, Schipper and Francis, 2013). This has been stated invarious ways that have multiple effectives of the statements, the total value entered on left sideof an account must be equal to the total amount mentioned at the right side of column. It iscomplete system of book-keeping that is having two aspects for each transaction. In order tomake analysis of various financial statements those are prepared by the company accountantneed to first record journal entry of the transactions and then after go on to make trail balance. Journal entries: It refers to be the logging system of accountancy that which helps torecord each and every transaction those are associated with cash or credit. The financial managerneed to consider various transactions and every data must be related to debit and credit amount.The total of debit and credit must be equal at both the side. All those accounting transactions thatare recorded into the journal are sorted before posted into the ledger books as per their nature and1

types. There are various types of account that are needed to be prepared such as cash account,account receivables and stock turnover statements (Beatty and Liao, 2014). Preparation of such kind of account and entries is being collectively associated with bookkeeping. Recording of transaction is utmost important for the company as they are responsiblefor generating more reliable and accurate outcomes to the company which will be taken intoaccount for attaining their aims and objectives in effective manner. These types of books must berecorded in every financial transaction on continuous basis in order to avoid any mistakes. Theprimary motive of recording of accounting transaction is to serve internal and externalorganisation so that fair picture of business can be attaining in near future time. 2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting INTRODUCTION 1 TASK 11 Question 1 2 7 TASK 29 Question 1 2 7 CONCLUSION 11 REFERENCES 12 INTRODUCTIONlg...

|14

|1243

|343

Assignment on Financial Accounting (PDF)lg...

|15

|1177

|294

Double Entry Bookkeeping System Doclg...

|15

|1056

|150

(solved) Analysis of Financial Statementslg...

|16

|1265

|309

Financial Accounting Part 1 Introductionlg...

|17

|1393

|275

Financial Accounting: Transactions, Bookkeeping, Journal Entries, Financial Reports, Principleslg...

|25

|4870

|184