Financial Accounting Assignment Solution: Comprehensive Analysis

VerifiedAdded on 2022/11/24

|27

|4911

|421

Homework Assignment

AI Summary

This financial accounting assignment solution provides a detailed analysis of various concepts. The introduction covers financial accounting's role in generating financial information. Question 1 defines different types of business transactions, including cash, credit, internal, and external transactions, along with explanations of single and double-entry bookkeeping, and the importance of a trial balance. Question 2 provides journal entries for various transactions and ledger accounts, while Question 3 differentiates between financial statements and financial reports. Question 4 discusses key accounting principles such as economic entity, going concern, cost, full disclosure, revenue recognition, and matching principles. Question 5 presents profit and loss calculations and balance sheet preparation. The second part of the solution includes scenario-based questions, with Question 1 focusing on bank reconciliation, Question 2 on control accounts, Question 3 on the suspense account, Question 4 on preparing an updated cash book and bank reconciliation statement, and Question 5 on journal entries. The assignment covers a wide range of financial accounting topics, providing a comprehensive understanding of the subject.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................11

Principles of accounting.........................................................................................................................11

QUESTION 5...............................................................................................................................................12

Calculation.............................................................................................................................................12

QUESTION 6...............................................................................................................................................14

Profit and Loss Account.........................................................................................................................14

QUESTION 7...............................................................................................................................................15

Cash flow statement..............................................................................................................................15

SCENARIO 2...............................................................................................................................................17

QUESTION 1...............................................................................................................................................17

Bank Reconciliation...............................................................................................................................17

QUESTION 2...............................................................................................................................................18

Control accounts....................................................................................................................................18

QUESTION 3...............................................................................................................................................19

Suspense Account..................................................................................................................................19

QUESTION 4...............................................................................................................................................20

(a) Required to prepare updated cash book and bank reconciliation statement..................................20

QUESTION 5...............................................................................................................................................22

Journal entries.......................................................................................................................................22

CONCLUSION.............................................................................................................................................24

REFERENCES..............................................................................................................................................25

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

Different types of business transaction...................................................................................................3

QUESTION 2.................................................................................................................................................5

Calculation...............................................................................................................................................5

QUESTION 3...............................................................................................................................................10

Different between financial statement and financial report.................................................................10

QUESTION 4...............................................................................................................................................11

Principles of accounting.........................................................................................................................11

QUESTION 5...............................................................................................................................................12

Calculation.............................................................................................................................................12

QUESTION 6...............................................................................................................................................14

Profit and Loss Account.........................................................................................................................14

QUESTION 7...............................................................................................................................................15

Cash flow statement..............................................................................................................................15

SCENARIO 2...............................................................................................................................................17

QUESTION 1...............................................................................................................................................17

Bank Reconciliation...............................................................................................................................17

QUESTION 2...............................................................................................................................................18

Control accounts....................................................................................................................................18

QUESTION 3...............................................................................................................................................19

Suspense Account..................................................................................................................................19

QUESTION 4...............................................................................................................................................20

(a) Required to prepare updated cash book and bank reconciliation statement..................................20

QUESTION 5...............................................................................................................................................22

Journal entries.......................................................................................................................................22

CONCLUSION.............................................................................................................................................24

REFERENCES..............................................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting includes generating financial information for internal business

workers, lenders, borrowers, and consumers that detail a firm's activities and general financial

viability. Financial accounting is generating detailed updates of a firm's assets, whether monthly,

weekly, or annually. It's crucial to remember, nevertheless, that such assessments aren't intended

to communicate a certain point of view or judgment well about firm. They should only be used to

convey facts that external stakeholders of the statements may use to form their own judgments

more about financial viability of the firm (Kholid, Alvian and Tumewang, 2020).

This report categorized into two parts in which first part included various numerical

questions based on profit and loss account. Along with discuss various topics like business

transactions, principle of accounting and cash flow statement. In the second part define about the

suspense account, control account and bank reconciliation statement in broad manner.

QUESTION 1

Different types of business transaction

A transfer of goods can be characterized as a trade (also known as a commercial

transaction or a monetary transaction). It is the trade of services or products at a fixed rate in a

commercial setting. Each activity affects a company's financial situation and, as a result, should

be documented in the accounting records. The deal might be between two people who have been

involved in commerce and doing it for mutually profit, or between a commercial entity and a

consumer, such as a small store.

Cash transaction: A cash transaction happens when money is collected or maximum efficacy at

the moment the processing takes place. It's worth noting that when a payment is received with a

bank card or a cheque, the transactions is also regarded to be a cash deal. For example, buying of

furnishings for money, selling of products for money, settlement to a creditors by cheque, and so

on are instances of financial transactions.

Credit transaction: A credit transaction happens whenever a repayment or revenue earned is not

implemented directly at the moment the action is performed but is delayed to a future stage.

Financial accounting includes generating financial information for internal business

workers, lenders, borrowers, and consumers that detail a firm's activities and general financial

viability. Financial accounting is generating detailed updates of a firm's assets, whether monthly,

weekly, or annually. It's crucial to remember, nevertheless, that such assessments aren't intended

to communicate a certain point of view or judgment well about firm. They should only be used to

convey facts that external stakeholders of the statements may use to form their own judgments

more about financial viability of the firm (Kholid, Alvian and Tumewang, 2020).

This report categorized into two parts in which first part included various numerical

questions based on profit and loss account. Along with discuss various topics like business

transactions, principle of accounting and cash flow statement. In the second part define about the

suspense account, control account and bank reconciliation statement in broad manner.

QUESTION 1

Different types of business transaction

A transfer of goods can be characterized as a trade (also known as a commercial

transaction or a monetary transaction). It is the trade of services or products at a fixed rate in a

commercial setting. Each activity affects a company's financial situation and, as a result, should

be documented in the accounting records. The deal might be between two people who have been

involved in commerce and doing it for mutually profit, or between a commercial entity and a

consumer, such as a small store.

Cash transaction: A cash transaction happens when money is collected or maximum efficacy at

the moment the processing takes place. It's worth noting that when a payment is received with a

bank card or a cheque, the transactions is also regarded to be a cash deal. For example, buying of

furnishings for money, selling of products for money, settlement to a creditors by cheque, and so

on are instances of financial transactions.

Credit transaction: A credit transaction happens whenever a repayment or revenue earned is not

implemented directly at the moment the action is performed but is delayed to a future stage.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Internal transaction: Internal services contain no third parties. Most operations do not include

the transfer of money across 2 people, but the event that occurs as a result of the trade is

quantifiable in cash form and has an influence on the company's financial condition. Inflation of

marketable securities and recognizing the loss of property due to fire, for illustration, are

instances of such activities (Tingey-Holyoak and et.al, 2020).

External transaction: External interactions are those in which a company trades money with

3rd parties. Those activities that aren't inside are typically referred to as external transactions.

These are the routine activities that a company conducts on a constant basis. Acquisition of

products and services, sale of goods to consumers, acquisition of marketable securities for

company use, payments of rental to owner, payments of gas, electric, or property taxes, payment

of salary to workers are all examples of external transactions. Outside payments often make up a

substantial percentage of any business's operations.

Define single entry book keeping:

In a single-entry accounting system, the record must be made just once from either the direct

debit row. This approach is most often employed by small firms who just need to keep track of

the fundamentals like money, accounts outstanding, accounts payable, and so on. Only if the

company transactions are relatively basic and the quantity is very low, this sort of technology is

regarded insufficient.

Define double entry book keeping:

A double-entry method necessitates entering the same information twice, once in the credit

column and once in debit side of a different account. These are designed to make sure no

submissions are overlooked by accidentally. It's also a more convenient approach to balance the

books. Double-entry accounting necessitates the management of a number of separate accounts.

Every activity that occurs must be recorded in two separate accounts. In one accounts, a debit

would be represented as a credit from another (Belesis, Sorros and Karagiorgos, 2020). Asset,

liability, income, expenditure, and cash payments can all benefit from double-entry accounting.

Explain trial balance and its importance

the transfer of money across 2 people, but the event that occurs as a result of the trade is

quantifiable in cash form and has an influence on the company's financial condition. Inflation of

marketable securities and recognizing the loss of property due to fire, for illustration, are

instances of such activities (Tingey-Holyoak and et.al, 2020).

External transaction: External interactions are those in which a company trades money with

3rd parties. Those activities that aren't inside are typically referred to as external transactions.

These are the routine activities that a company conducts on a constant basis. Acquisition of

products and services, sale of goods to consumers, acquisition of marketable securities for

company use, payments of rental to owner, payments of gas, electric, or property taxes, payment

of salary to workers are all examples of external transactions. Outside payments often make up a

substantial percentage of any business's operations.

Define single entry book keeping:

In a single-entry accounting system, the record must be made just once from either the direct

debit row. This approach is most often employed by small firms who just need to keep track of

the fundamentals like money, accounts outstanding, accounts payable, and so on. Only if the

company transactions are relatively basic and the quantity is very low, this sort of technology is

regarded insufficient.

Define double entry book keeping:

A double-entry method necessitates entering the same information twice, once in the credit

column and once in debit side of a different account. These are designed to make sure no

submissions are overlooked by accidentally. It's also a more convenient approach to balance the

books. Double-entry accounting necessitates the management of a number of separate accounts.

Every activity that occurs must be recorded in two separate accounts. In one accounts, a debit

would be represented as a credit from another (Belesis, Sorros and Karagiorgos, 2020). Asset,

liability, income, expenditure, and cash payments can all benefit from double-entry accounting.

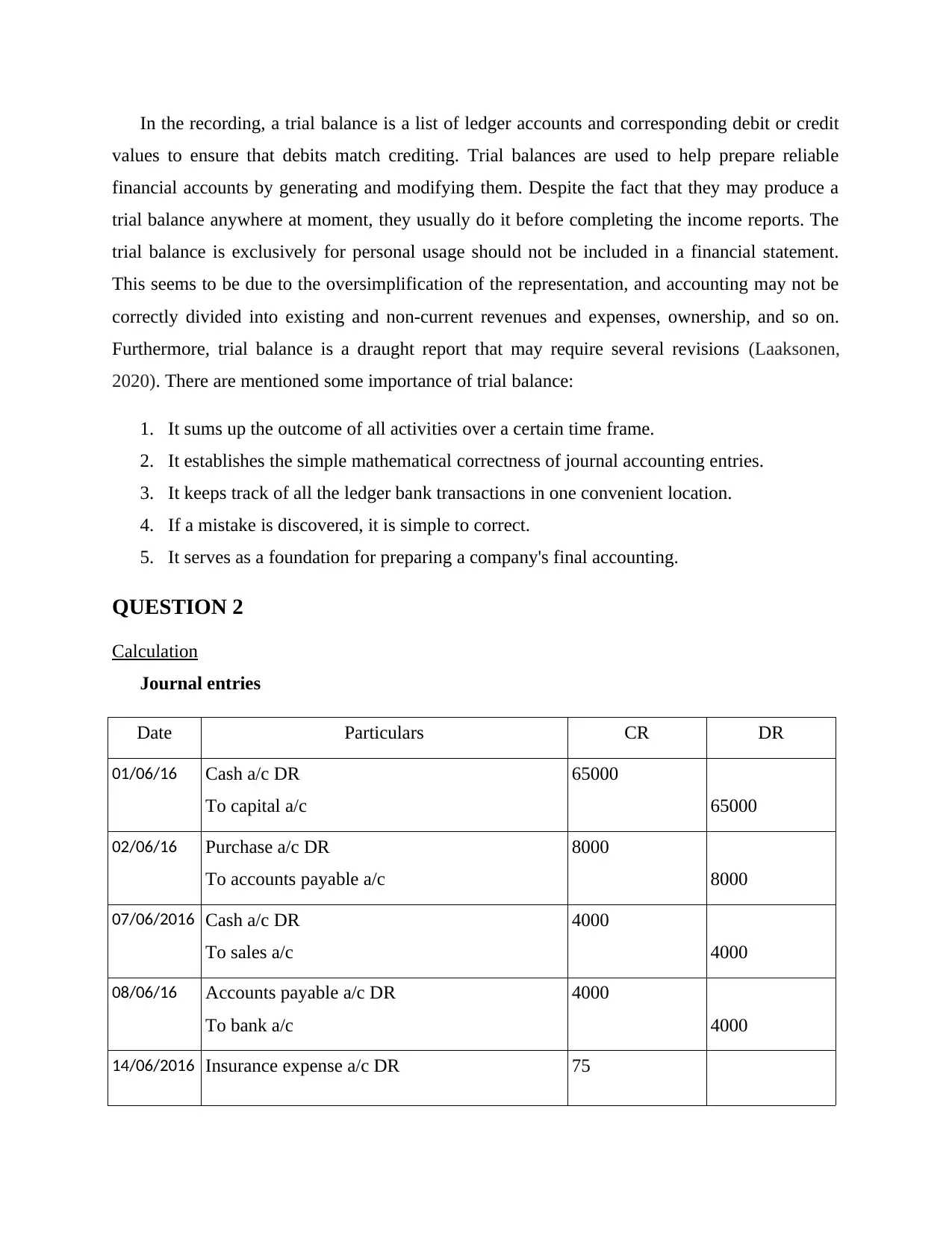

Explain trial balance and its importance

In the recording, a trial balance is a list of ledger accounts and corresponding debit or credit

values to ensure that debits match crediting. Trial balances are used to help prepare reliable

financial accounts by generating and modifying them. Despite the fact that they may produce a

trial balance anywhere at moment, they usually do it before completing the income reports. The

trial balance is exclusively for personal usage should not be included in a financial statement.

This seems to be due to the oversimplification of the representation, and accounting may not be

correctly divided into existing and non-current revenues and expenses, ownership, and so on.

Furthermore, trial balance is a draught report that may require several revisions (Laaksonen,

2020). There are mentioned some importance of trial balance:

1. It sums up the outcome of all activities over a certain time frame.

2. It establishes the simple mathematical correctness of journal accounting entries.

3. It keeps track of all the ledger bank transactions in one convenient location.

4. If a mistake is discovered, it is simple to correct.

5. It serves as a foundation for preparing a company's final accounting.

QUESTION 2

Calculation

Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

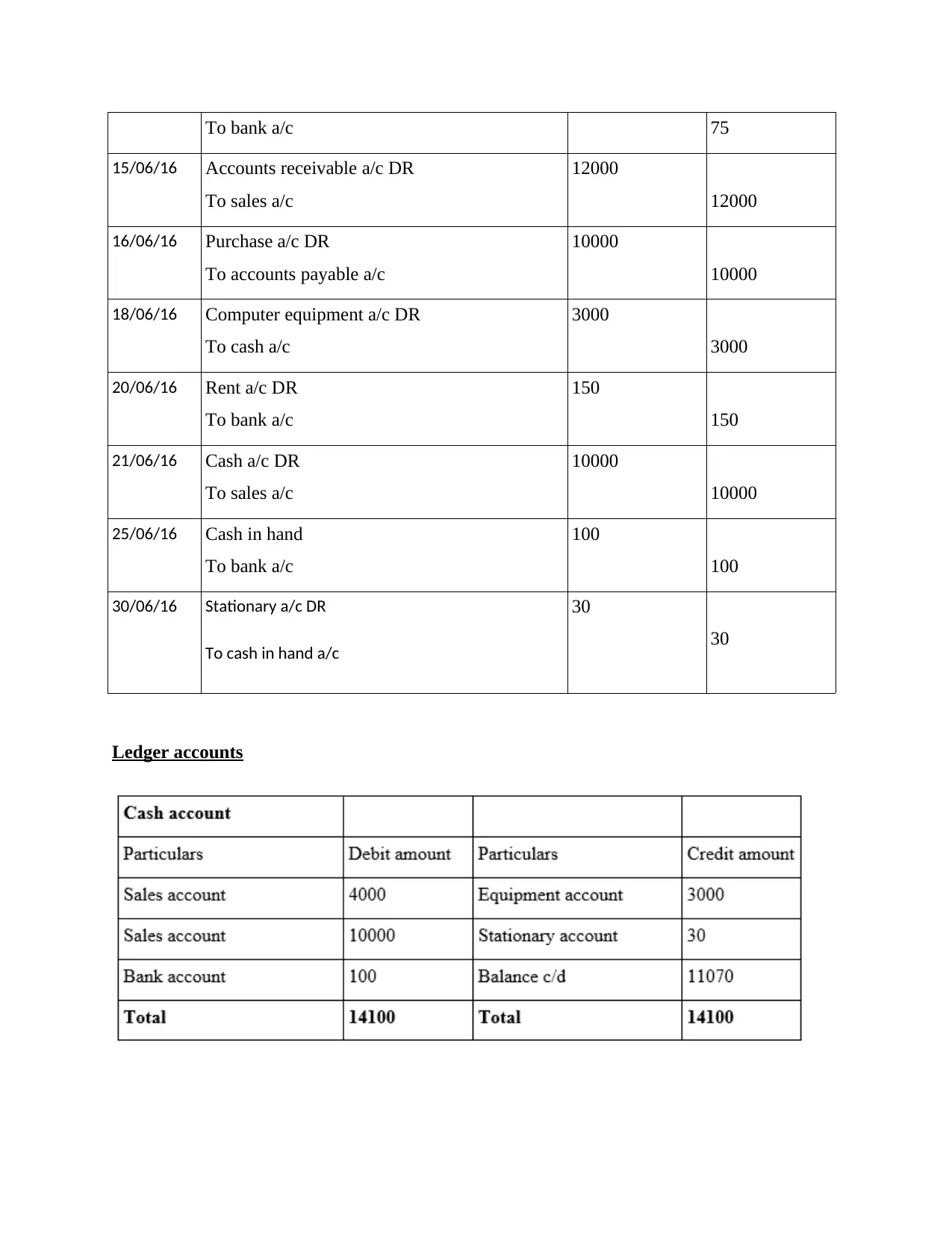

14/06/2016 Insurance expense a/c DR 75

values to ensure that debits match crediting. Trial balances are used to help prepare reliable

financial accounts by generating and modifying them. Despite the fact that they may produce a

trial balance anywhere at moment, they usually do it before completing the income reports. The

trial balance is exclusively for personal usage should not be included in a financial statement.

This seems to be due to the oversimplification of the representation, and accounting may not be

correctly divided into existing and non-current revenues and expenses, ownership, and so on.

Furthermore, trial balance is a draught report that may require several revisions (Laaksonen,

2020). There are mentioned some importance of trial balance:

1. It sums up the outcome of all activities over a certain time frame.

2. It establishes the simple mathematical correctness of journal accounting entries.

3. It keeps track of all the ledger bank transactions in one convenient location.

4. If a mistake is discovered, it is simple to correct.

5. It serves as a foundation for preparing a company's final accounting.

QUESTION 2

Calculation

Journal entries

Date Particulars CR DR

01/06/16 Cash a/c DR

To capital a/c

65000

65000

02/06/16 Purchase a/c DR

To accounts payable a/c

8000

8000

07/06/2016 Cash a/c DR

To sales a/c

4000

4000

08/06/16 Accounts payable a/c DR

To bank a/c

4000

4000

14/06/2016 Insurance expense a/c DR 75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To bank a/c 75

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

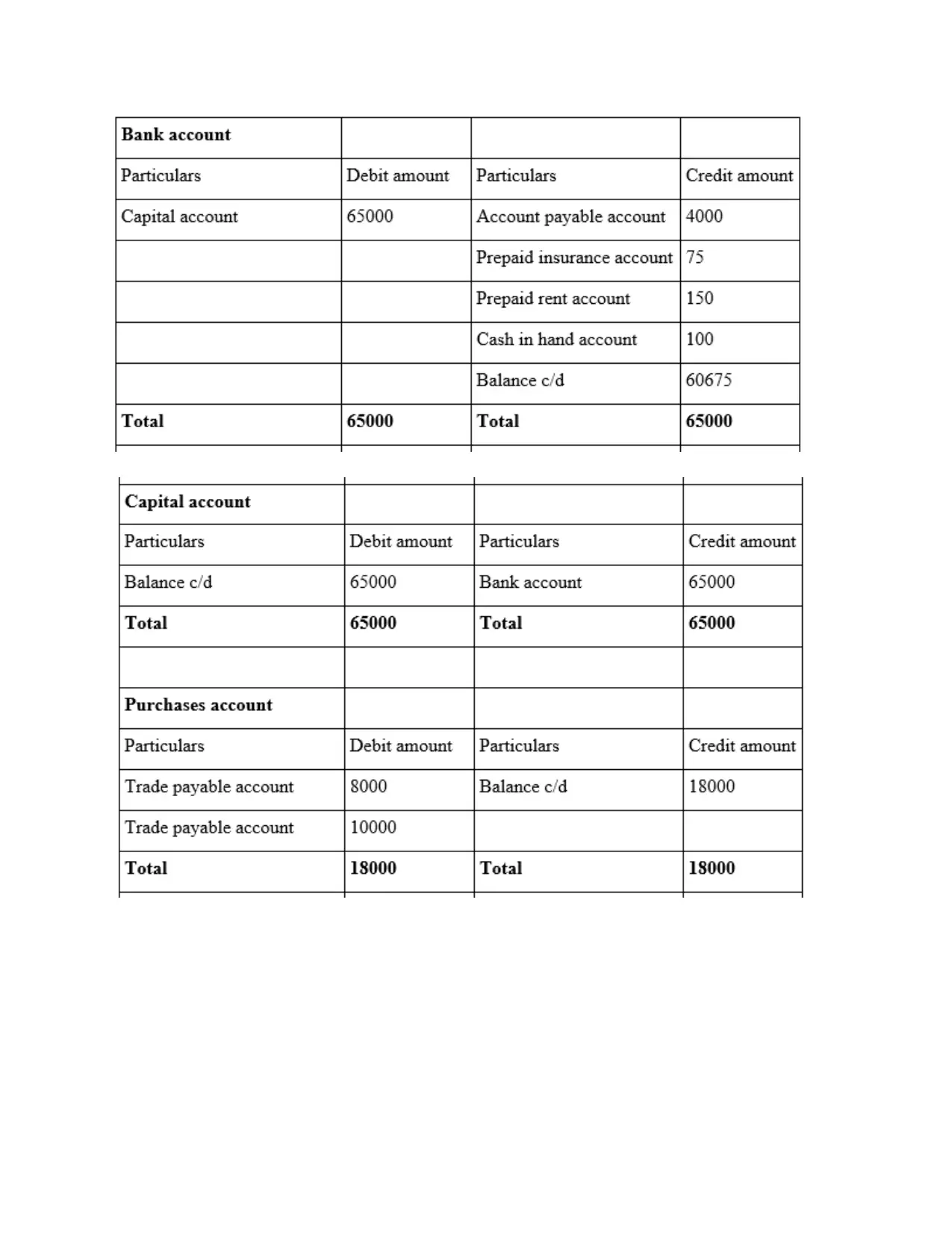

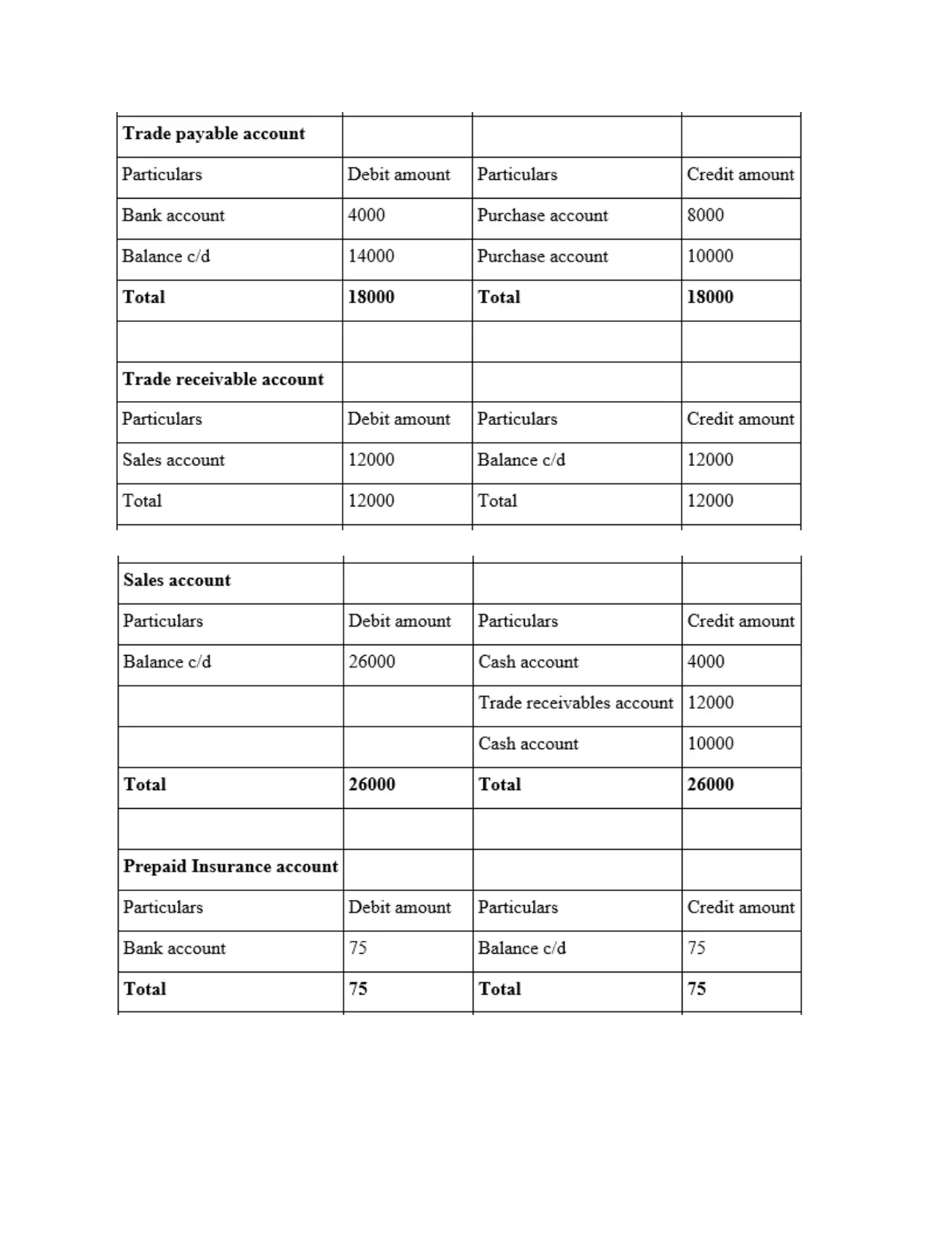

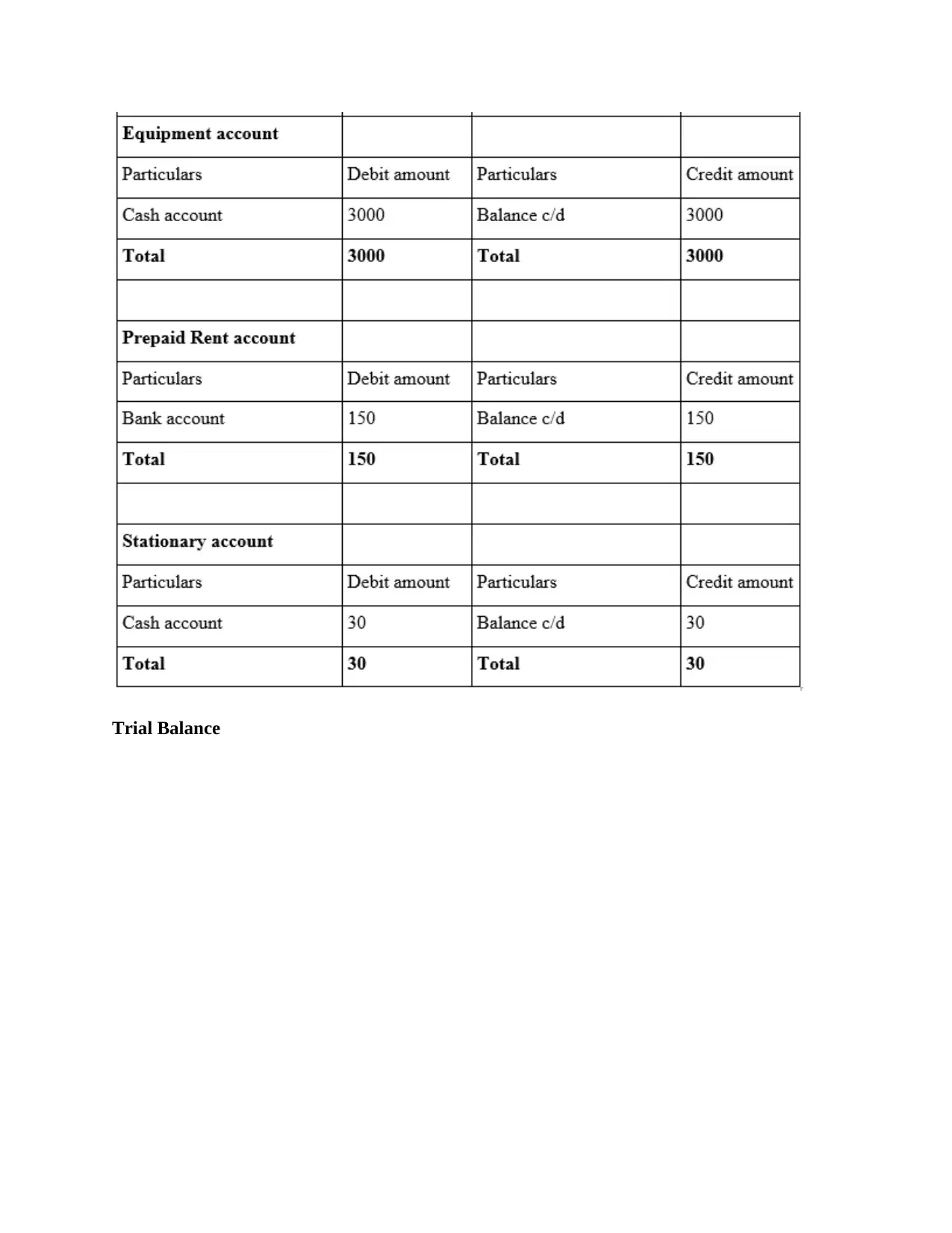

Ledger accounts

15/06/16 Accounts receivable a/c DR

To sales a/c

12000

12000

16/06/16 Purchase a/c DR

To accounts payable a/c

10000

10000

18/06/16 Computer equipment a/c DR

To cash a/c

3000

3000

20/06/16 Rent a/c DR

To bank a/c

150

150

21/06/16 Cash a/c DR

To sales a/c

10000

10000

25/06/16 Cash in hand

To bank a/c

100

100

30/06/16 Stationary a/c DR

To cash in hand a/c

30

30

Ledger accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

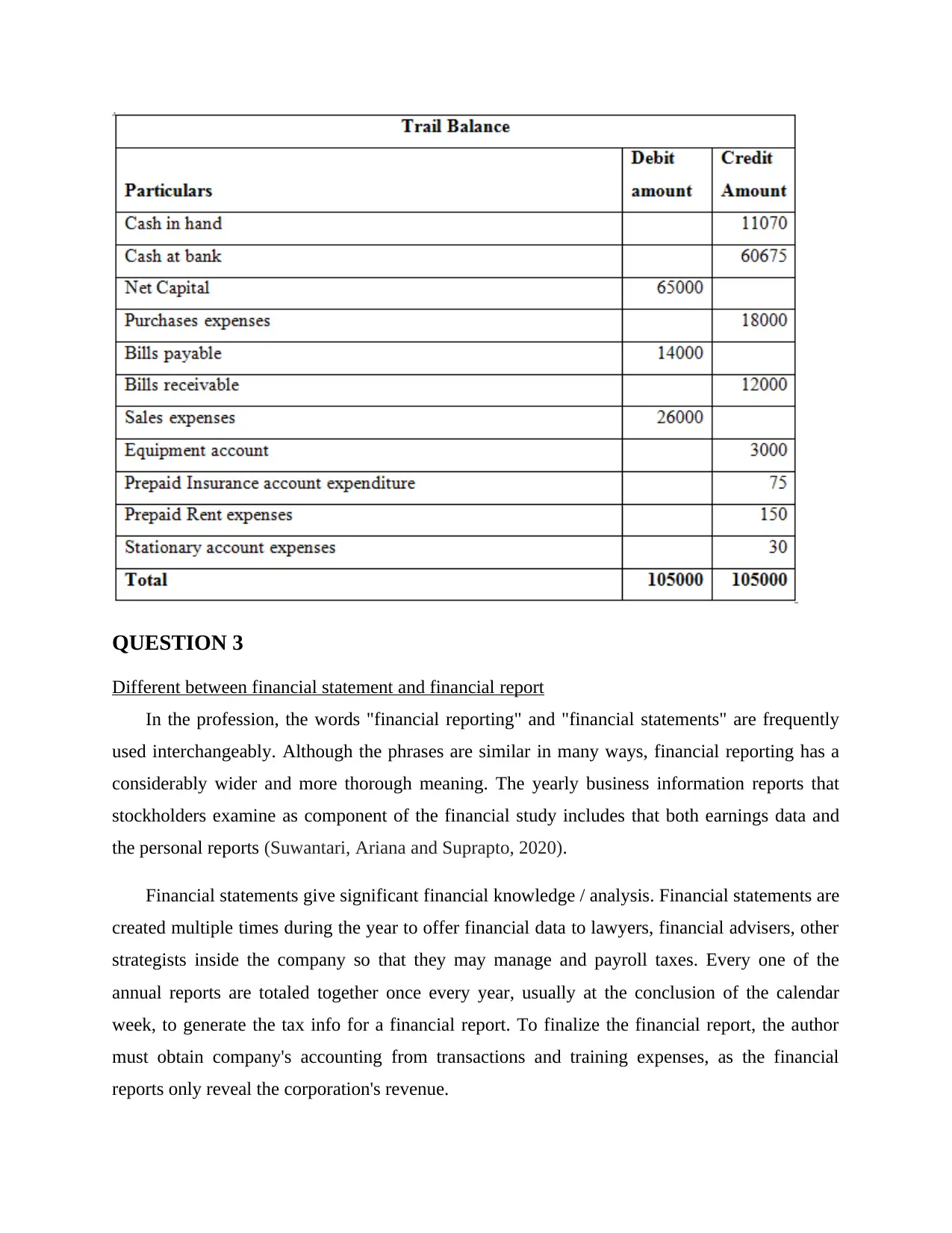

Trial Balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

Different between financial statement and financial report

In the profession, the words "financial reporting" and "financial statements" are frequently

used interchangeably. Although the phrases are similar in many ways, financial reporting has a

considerably wider and more thorough meaning. The yearly business information reports that

stockholders examine as component of the financial study includes that both earnings data and

the personal reports (Suwantari, Ariana and Suprapto, 2020).

Financial statements give significant financial knowledge / analysis. Financial statements are

created multiple times during the year to offer financial data to lawyers, financial advisers, other

strategists inside the company so that they may manage and payroll taxes. Every one of the

annual reports are totaled together once every year, usually at the conclusion of the calendar

week, to generate the tax info for a financial report. To finalize the financial report, the author

must obtain company's accounting from transactions and training expenses, as the financial

reports only reveal the corporation's revenue.

Different between financial statement and financial report

In the profession, the words "financial reporting" and "financial statements" are frequently

used interchangeably. Although the phrases are similar in many ways, financial reporting has a

considerably wider and more thorough meaning. The yearly business information reports that

stockholders examine as component of the financial study includes that both earnings data and

the personal reports (Suwantari, Ariana and Suprapto, 2020).

Financial statements give significant financial knowledge / analysis. Financial statements are

created multiple times during the year to offer financial data to lawyers, financial advisers, other

strategists inside the company so that they may manage and payroll taxes. Every one of the

annual reports are totaled together once every year, usually at the conclusion of the calendar

week, to generate the tax info for a financial report. To finalize the financial report, the author

must obtain company's accounting from transactions and training expenses, as the financial

reports only reveal the corporation's revenue.

Financial reports are used by small businesses to entice new entrants, shares, and employees

to the organization. Shareholders and users may cause shifts in the business's net wealth, cash

flow statements, and an operating capital structure since such financial report is a collection of

various financial statements for a particular period. To put it another way, the owners can follow

all of the capital and cash in the company and see how and why it is used and generated. Every

other year, monetary reviews are conducted to convey the company's earnings and expenditures

for the previous fiscal year. Whereas financial reports are created so that stakeholders, suppliers,

and analysts saw how firm money is spent, a corporation could also use reports to identify assets

and manage its budget. Financial reporting makes use of financial statements to reveal financial

information about a long - term solvency over a span of years (Moy and et.al, 2020).

QUESTION 4

Principles of accounting

The area of bookkeeping is governed by a set of broad principles and ideas. These

fundamental accounting principles and methods serve as the foundation for more comprehensive

and particular accounting regulations. Accounting standards are the norms and criteria that

businesses must adhere to this when preparing financial statements.

Economic entity principle: The auditor maintains all of a sole proprietorship's commercial

dealings distinct from the employee's personal operations. A sole trader and its operator are

regarded one organization for liability purposes, although they are different entities for taxation

purposes.

Going concern: This accounting concept implies that a firm will survive long enough to achieve

its goals and fulfill its obligations, and it will not be liquidated in the nearish term. Unless the

auditor feels the corporation's economic position has been that it will be unable to survive, the

auditor must make this opinion public. The going concern concept permits the business to

postpone part of its which was before costs to accumulated other comprehensive income.

Cost principle: Cost, from the perspective of an accountant, represents the amount invested

whenever a product was first purchased, if that product is sold last week or thirty years earlier.

As a result, the figures on financial reports are known to as historical cost figures. Asset values

are not updated for inflationary for this accounting approach. In reality, asset quantities are not

to the organization. Shareholders and users may cause shifts in the business's net wealth, cash

flow statements, and an operating capital structure since such financial report is a collection of

various financial statements for a particular period. To put it another way, the owners can follow

all of the capital and cash in the company and see how and why it is used and generated. Every

other year, monetary reviews are conducted to convey the company's earnings and expenditures

for the previous fiscal year. Whereas financial reports are created so that stakeholders, suppliers,

and analysts saw how firm money is spent, a corporation could also use reports to identify assets

and manage its budget. Financial reporting makes use of financial statements to reveal financial

information about a long - term solvency over a span of years (Moy and et.al, 2020).

QUESTION 4

Principles of accounting

The area of bookkeeping is governed by a set of broad principles and ideas. These

fundamental accounting principles and methods serve as the foundation for more comprehensive

and particular accounting regulations. Accounting standards are the norms and criteria that

businesses must adhere to this when preparing financial statements.

Economic entity principle: The auditor maintains all of a sole proprietorship's commercial

dealings distinct from the employee's personal operations. A sole trader and its operator are

regarded one organization for liability purposes, although they are different entities for taxation

purposes.

Going concern: This accounting concept implies that a firm will survive long enough to achieve

its goals and fulfill its obligations, and it will not be liquidated in the nearish term. Unless the

auditor feels the corporation's economic position has been that it will be unable to survive, the

auditor must make this opinion public. The going concern concept permits the business to

postpone part of its which was before costs to accumulated other comprehensive income.

Cost principle: Cost, from the perspective of an accountant, represents the amount invested

whenever a product was first purchased, if that product is sold last week or thirty years earlier.

As a result, the figures on financial reports are known to as historical cost figures. Asset values

are not updated for inflationary for this accounting approach. In reality, asset quantities are not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.