Accounting: Business Transactions, Financial Statements, Fundamental Principles

VerifiedAdded on 2022/11/25

|26

|4285

|155

AI Summary

This document provides an introduction to financial accounting and covers topics such as business transactions, financial statements, and fundamental principles in accounting. It includes scenarios with questions and answers, as well as examples of journal entries and ledger accounts. The document also includes an income statement and a statement of financial position. The subject is accounting, and the course code and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................16

SCENARIO 2............................................................................................................................................17

Question 1.............................................................................................................................................17

Question 2.............................................................................................................................................18

Question 3.............................................................................................................................................19

Question 4.............................................................................................................................................19

Question 5.............................................................................................................................................21

CONCLUSION.........................................................................................................................................23

REFERENCES..........................................................................................................................................24

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................16

SCENARIO 2............................................................................................................................................17

Question 1.............................................................................................................................................17

Question 2.............................................................................................................................................18

Question 3.............................................................................................................................................19

Question 4.............................................................................................................................................19

Question 5.............................................................................................................................................21

CONCLUSION.........................................................................................................................................23

REFERENCES..........................................................................................................................................24

INTRODUCTION

Financial Accounting (FA) is procedure of utilizing monetary information through

making summarization of related data to gain deeper insights about firm’s liquidity position. In

present era, it is crucial for company to have efficient FA procedure to derive significant

information to get competitive advantages. The current study is based on providing important

regarding concepts like business transaction, accounting principles, journal entries, ledger, trial

balance, financial reports & statements, cash flow, bank reconciliation, control & suspense

account, etc. To get deeper insights about the same related calculations will be provided in the

systematic format .

SCENARIO 1

Question 1

Business Transaction is related with an economic activity which is recorded in

accounting system. There are different forms of business transaction that are important to

recorded for analyzing, evaluating and controlling monetary position. In order to have

sustainability company conducts different kinds of transaction that are related to internal

and external practices. It includes, cash & credit purchase, sales, raising funds,

expenditure regarding interest, tax, salaries, etc. For having accurate estimation of

company position it becomes essential for organization to record all types of business

transactions.

Single entry presents one sided organizational picture that is unable to track all

transactions as it records business activities partially. On the other side, double entry

system is based on fundamental accounting principle that helps company take all aspects

transactions into consideration (Siagian, 2020). It becomes difficult to identify the errors

through single entry system as compared to double. Assessing financial position with

help of double entry book keeping system it become convenient.

Trial Balance (TB) is combined worksheet that comprises all ledgers’ balances which is

done once the reporting period. For ensuring book keeping accuracy through equalizing

debit & credit balance TB is prepared. It is utilized for various purposes such as

preparation of financial statements, identifying & rectifying errors, formulation of audit

Financial Accounting (FA) is procedure of utilizing monetary information through

making summarization of related data to gain deeper insights about firm’s liquidity position. In

present era, it is crucial for company to have efficient FA procedure to derive significant

information to get competitive advantages. The current study is based on providing important

regarding concepts like business transaction, accounting principles, journal entries, ledger, trial

balance, financial reports & statements, cash flow, bank reconciliation, control & suspense

account, etc. To get deeper insights about the same related calculations will be provided in the

systematic format .

SCENARIO 1

Question 1

Business Transaction is related with an economic activity which is recorded in

accounting system. There are different forms of business transaction that are important to

recorded for analyzing, evaluating and controlling monetary position. In order to have

sustainability company conducts different kinds of transaction that are related to internal

and external practices. It includes, cash & credit purchase, sales, raising funds,

expenditure regarding interest, tax, salaries, etc. For having accurate estimation of

company position it becomes essential for organization to record all types of business

transactions.

Single entry presents one sided organizational picture that is unable to track all

transactions as it records business activities partially. On the other side, double entry

system is based on fundamental accounting principle that helps company take all aspects

transactions into consideration (Siagian, 2020). It becomes difficult to identify the errors

through single entry system as compared to double. Assessing financial position with

help of double entry book keeping system it become convenient.

Trial Balance (TB) is combined worksheet that comprises all ledgers’ balances which is

done once the reporting period. For ensuring book keeping accuracy through equalizing

debit & credit balance TB is prepared. It is utilized for various purposes such as

preparation of financial statements, identifying & rectifying errors, formulation of audit

reports, strategic decision making, comparative analysis, etc. These all provides

assistance in assessing arithmetical accuracy of organization.

Question 2

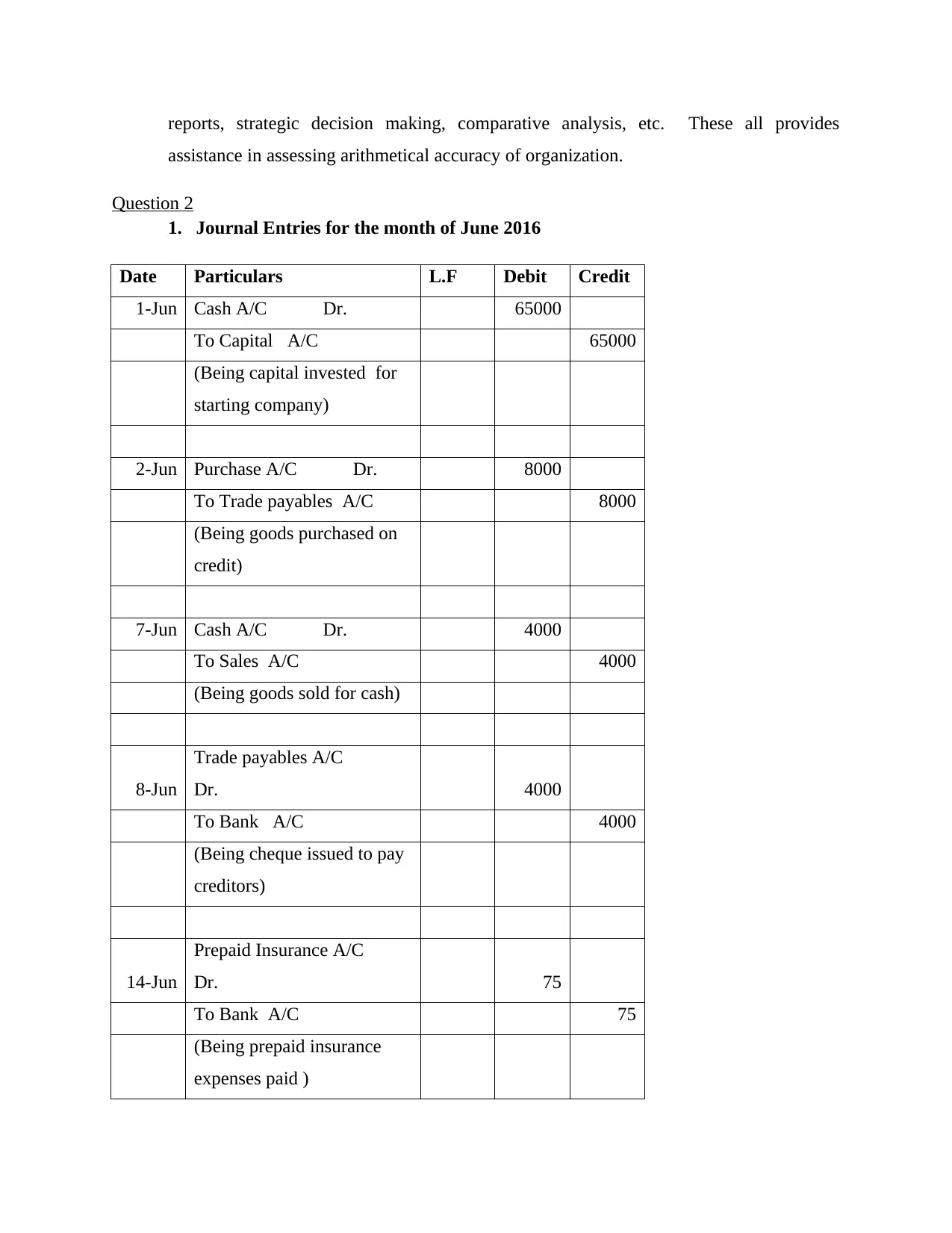

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

assistance in assessing arithmetical accuracy of organization.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

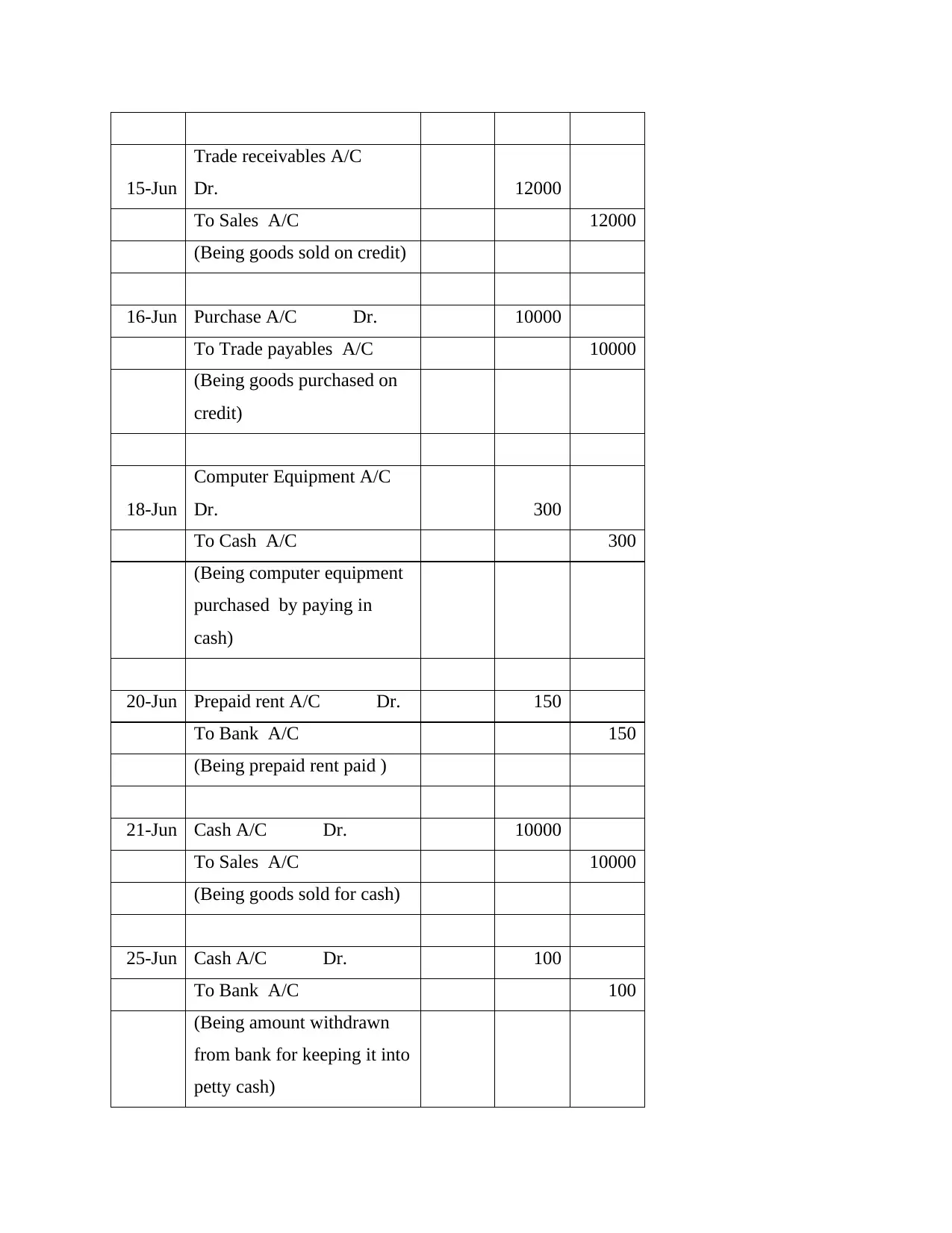

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

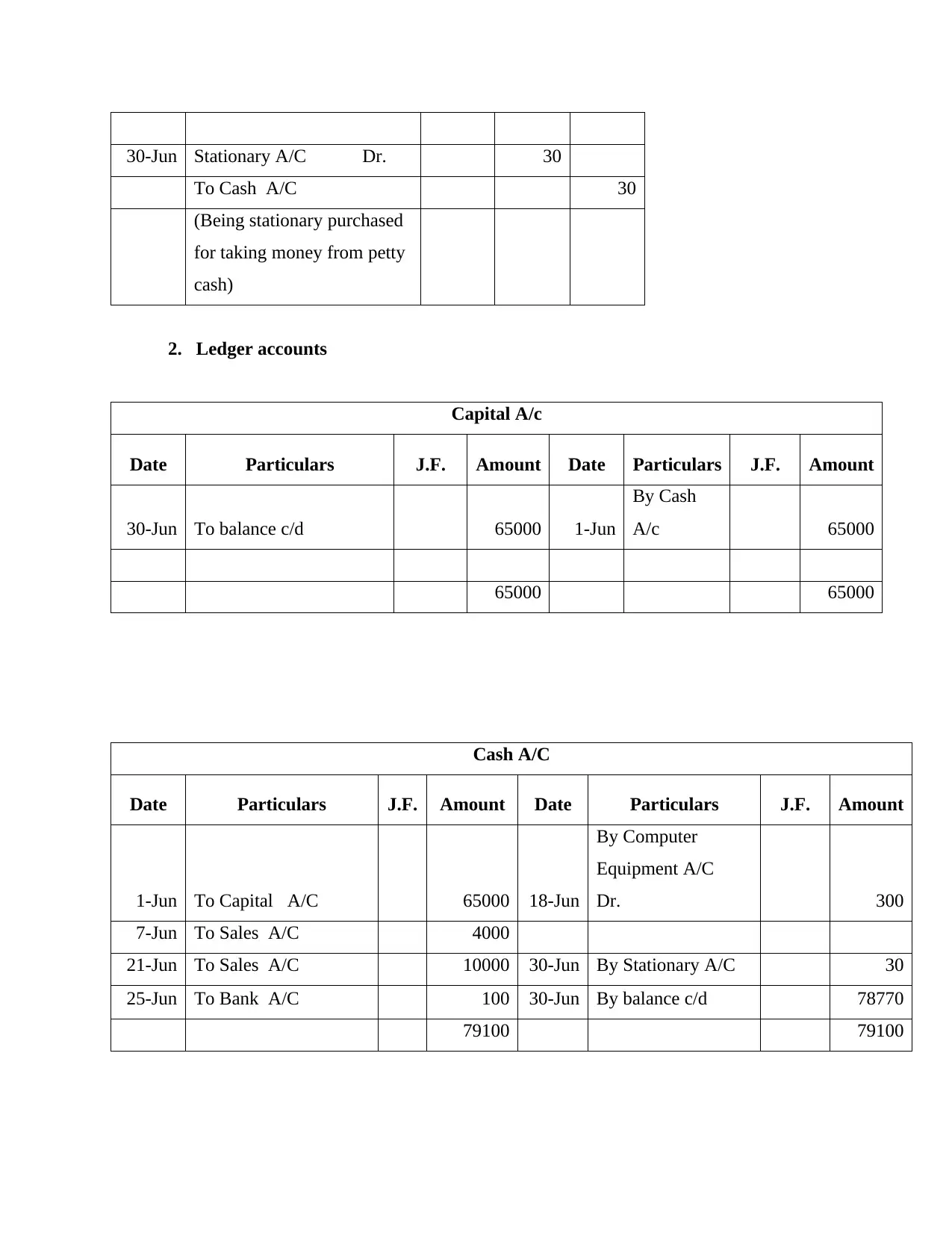

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

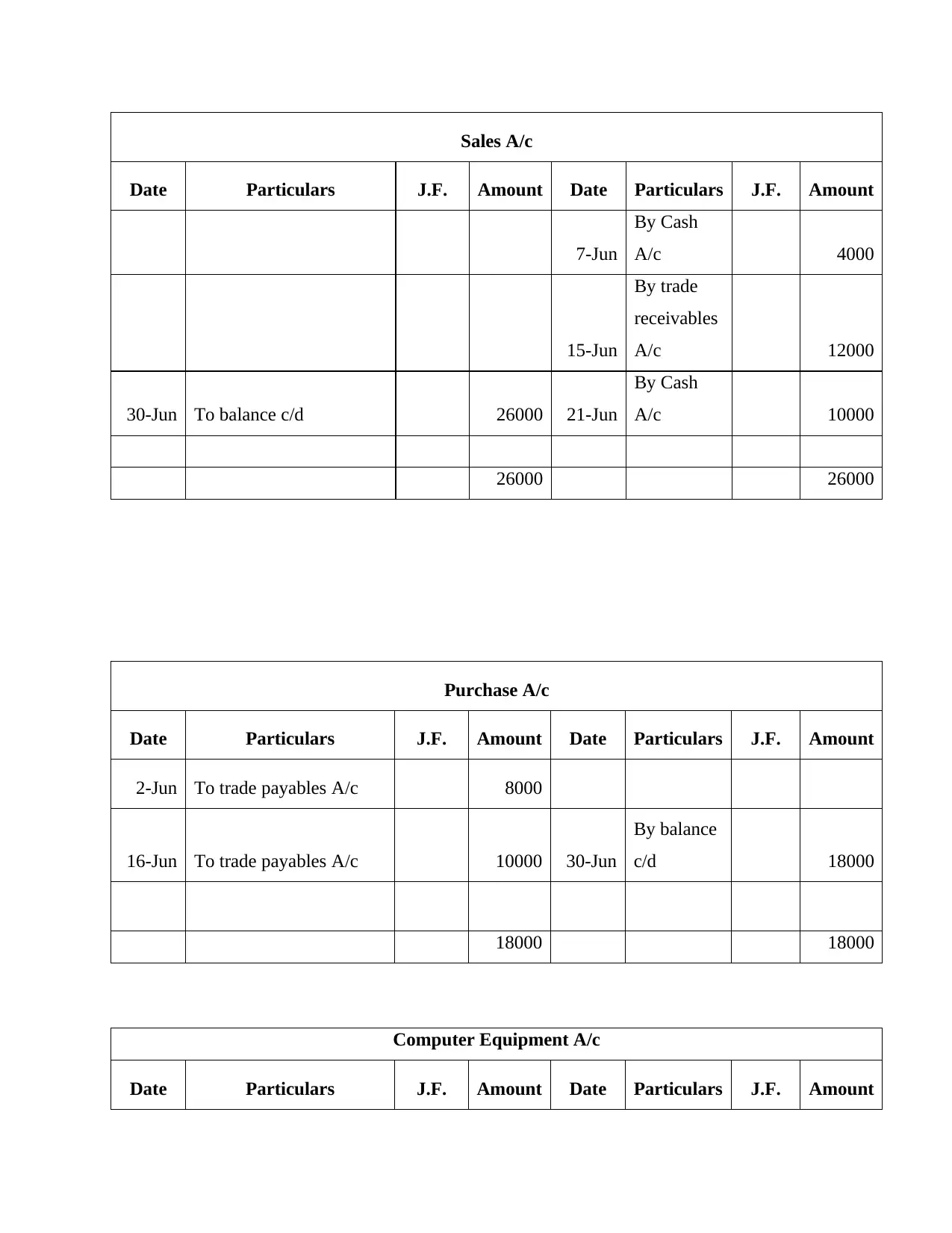

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

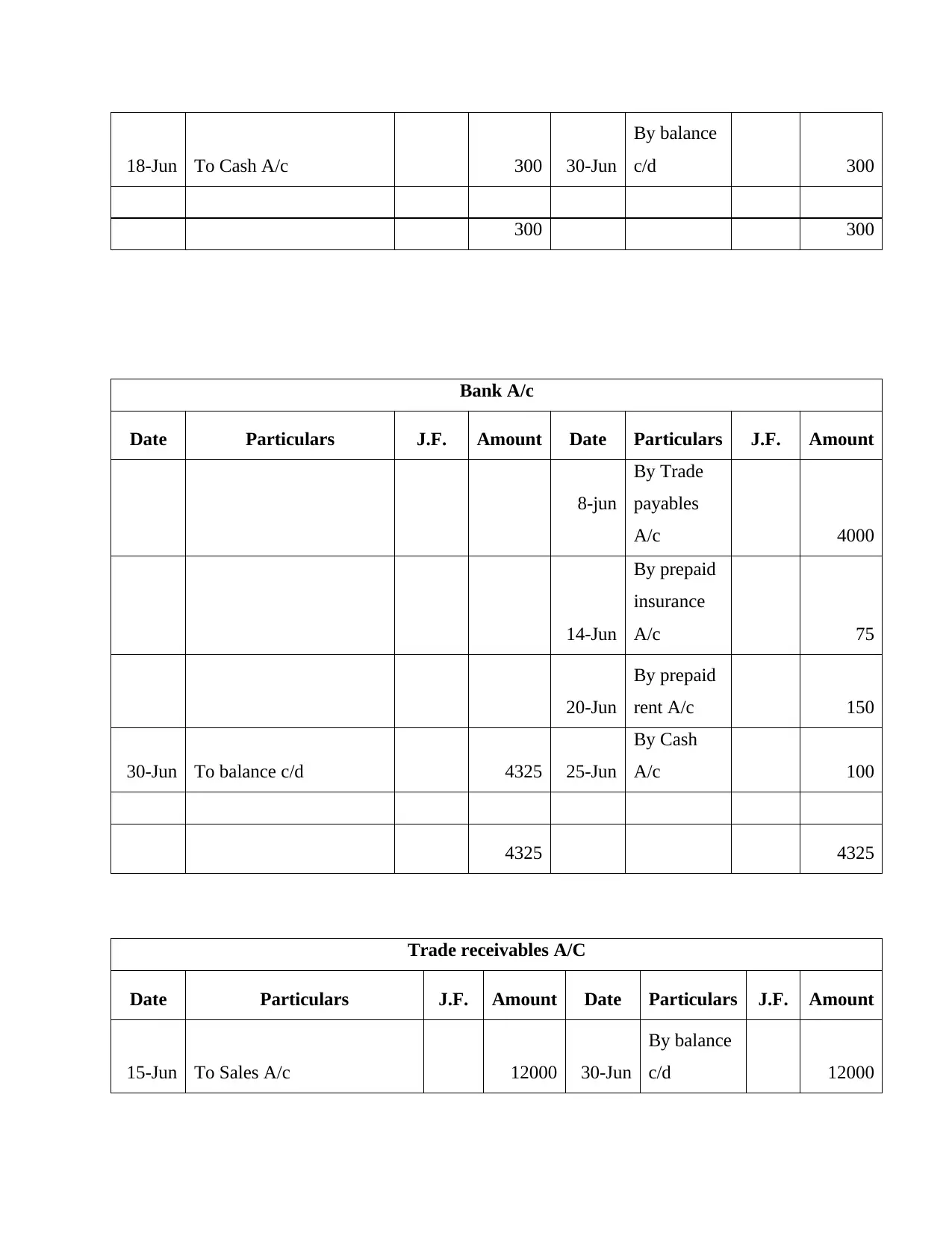

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

By balance

c/d 300

300 300

Bank A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

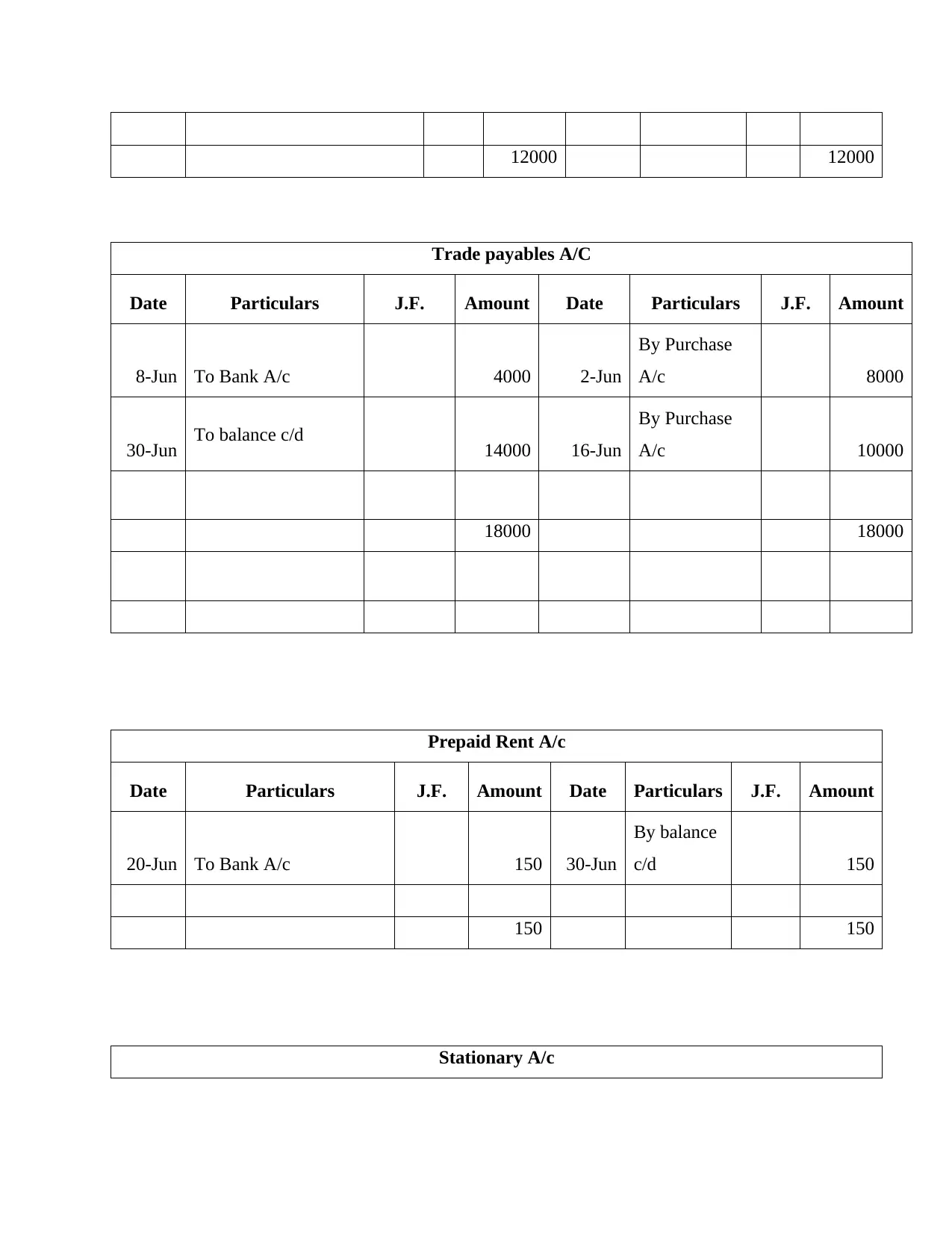

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

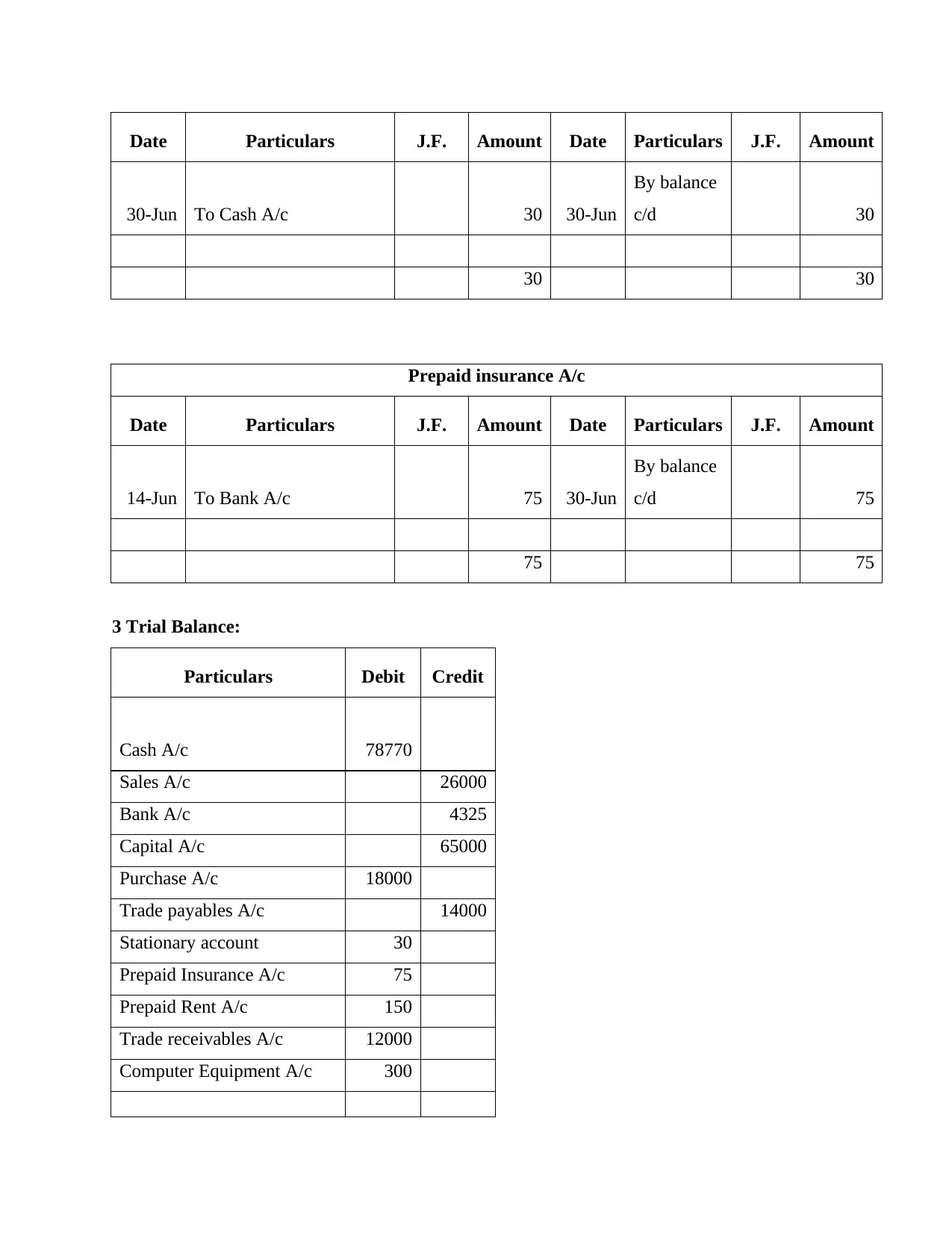

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Total 109325 109325

Question 3

There are various situations in which financial statements and reports are utilized

interchangeably but they are different from each other. Financial Reports (FR) are broader term

that comprises varying forms that are widely taken into consideration for providing essential

information to public. There has been significant utilization of reports by stakeholders in order to

take various important business decisions for accomplishing a particular purpose. Financial

Statements (FS) is narrow term as compared to financial reports as it is one of the reports that lie

under the umbrella. It becomes crucial for company to have accurate reports with appropriate

time based so that company can take significant decisions (Financial Statements vs. Financial

Reports – What’s the Difference? 2021). Having appropriate financial reports helps in attaining

effective performance through actual identification of business position. FS comprises income

statement, balance sheet, change in equity statement, cash flow, etc. whose purpose is to provide

information about cash flows, results of operations, etc. It aids company to get ability to generate

revenue, profits, etc to analyze the trend. Estimation of liquidity with helps of financial

positioning statement become possible to identify suitable course of actions. With help of

financial statement company becomes able to provide reliable & validate data that is significant

for several stakeholders in order to take strategic decisions. Various types of cash, credit, tax, etc.

decisions can be taken for getting desirable position in industry.

There are various parties of internal as well external business environment which utilizes

financial statements for attaining specified objective. Investment analyst uses Fs to make

appropriate decisions through analyzing each aspect related to their client’s objective of having

high return so that they can take proper decisions. Lenders are another party which comprises

financial institutions, banks, etc that provide loan to entity so having fair evaluation of

company’s liquidity, paying capacity these refer financial statements to avoid unfavorable

situation. Rating agencies can make judgment on operational and financing position of entity to

get data regarding making decisions that giving credit will be beneficial or not (Garbowski and

Question 3

There are various situations in which financial statements and reports are utilized

interchangeably but they are different from each other. Financial Reports (FR) are broader term

that comprises varying forms that are widely taken into consideration for providing essential

information to public. There has been significant utilization of reports by stakeholders in order to

take various important business decisions for accomplishing a particular purpose. Financial

Statements (FS) is narrow term as compared to financial reports as it is one of the reports that lie

under the umbrella. It becomes crucial for company to have accurate reports with appropriate

time based so that company can take significant decisions (Financial Statements vs. Financial

Reports – What’s the Difference? 2021). Having appropriate financial reports helps in attaining

effective performance through actual identification of business position. FS comprises income

statement, balance sheet, change in equity statement, cash flow, etc. whose purpose is to provide

information about cash flows, results of operations, etc. It aids company to get ability to generate

revenue, profits, etc to analyze the trend. Estimation of liquidity with helps of financial

positioning statement become possible to identify suitable course of actions. With help of

financial statement company becomes able to provide reliable & validate data that is significant

for several stakeholders in order to take strategic decisions. Various types of cash, credit, tax, etc.

decisions can be taken for getting desirable position in industry.

There are various parties of internal as well external business environment which utilizes

financial statements for attaining specified objective. Investment analyst uses Fs to make

appropriate decisions through analyzing each aspect related to their client’s objective of having

high return so that they can take proper decisions. Lenders are another party which comprises

financial institutions, banks, etc that provide loan to entity so having fair evaluation of

company’s liquidity, paying capacity these refer financial statements to avoid unfavorable

situation. Rating agencies can make judgment on operational and financing position of entity to

get data regarding making decisions that giving credit will be beneficial or not (Garbowski and

et.al., 2019.). Management of organization uses prepared financial statements to get information

of actual performance so that it can recognize lacking functional areas in turn improvement

actions can be taken. Employees needs mentioned financial information to make decisions

regarding their future career that firm will be able to provide them growth opportunities or not.

Employee involvement and productivity can be increased through making understanding these

critical data. Suppliers, customers, etc are other users that give emphasis on financial statements

to take important decisions.

Question 4

Accounting fundamental principles are universally applicable and provides accurate

working pattern to organization. The following mentioned are fundamental principles of

accounting:

Full disclosure principle

This is concerned with making assurance that organization should provide all essential

information to public so that full transparency can be maintained. It is basically related with

publishing all financial statements of company for making stakeholders capable of understanding

each business policy, structure, profits, performance efficiency so that it can avoid any legal

obligation.

Accrual principle

It is accounting principle requires company to record all its transaction in the time period

in which they are incurred. This is combination of two principles revenue recognition &

matching principle (Warren, Jonick and Schneider, 2020). It is utilized to make proper evaluation

of business position through estimating all related transaction with that specified period.

Matching principle

This principles is concerned with recording expenses in same period when the revenue is

earned. There should be accurate pair of expenses with revenue through executing accrual

fundamental principle of accounting. In addition to this, having fairer picture of company

becomes possible through implementing it. It helps in making evaluation how much expenses are

of actual performance so that it can recognize lacking functional areas in turn improvement

actions can be taken. Employees needs mentioned financial information to make decisions

regarding their future career that firm will be able to provide them growth opportunities or not.

Employee involvement and productivity can be increased through making understanding these

critical data. Suppliers, customers, etc are other users that give emphasis on financial statements

to take important decisions.

Question 4

Accounting fundamental principles are universally applicable and provides accurate

working pattern to organization. The following mentioned are fundamental principles of

accounting:

Full disclosure principle

This is concerned with making assurance that organization should provide all essential

information to public so that full transparency can be maintained. It is basically related with

publishing all financial statements of company for making stakeholders capable of understanding

each business policy, structure, profits, performance efficiency so that it can avoid any legal

obligation.

Accrual principle

It is accounting principle requires company to record all its transaction in the time period

in which they are incurred. This is combination of two principles revenue recognition &

matching principle (Warren, Jonick and Schneider, 2020). It is utilized to make proper evaluation

of business position through estimating all related transaction with that specified period.

Matching principle

This principles is concerned with recording expenses in same period when the revenue is

earned. There should be accurate pair of expenses with revenue through executing accrual

fundamental principle of accounting. In addition to this, having fairer picture of company

becomes possible through implementing it. It helps in making evaluation how much expenses are

incurred to earn revenue. These is one of the crucial principle of accounting that need to be taken

into consideration for deriving smooth functioning.

Ongoing principle

It is an underlying assumption regarding preparation of financial statements with

intention of making operational activity for longer duration. This is crucial to implement as it

allows company to make stakeholders aware about stability of company. Continuing operations

shows the ability shows the ability of company to fulfill requirements of stakeholders.

Revenue Recognition Principle

Revenue recognition principle is stipulated with how and when revenue is to be

recognized. In addition to this, particular fundamental principle utilizes accrual accounting and

states that revenue are recognized when realized and earned not when it is received (Drake,

Quinn and Thornock, 2017). Uniform framework is obtained through executing revenue

recognition accounting principle.

Conservatism Principle

It is policy of anticipating possible future losses but not future gains for understate rather

than overstate assets & net income. It is principle for lower of cost for getting current market

value for getting guidance.

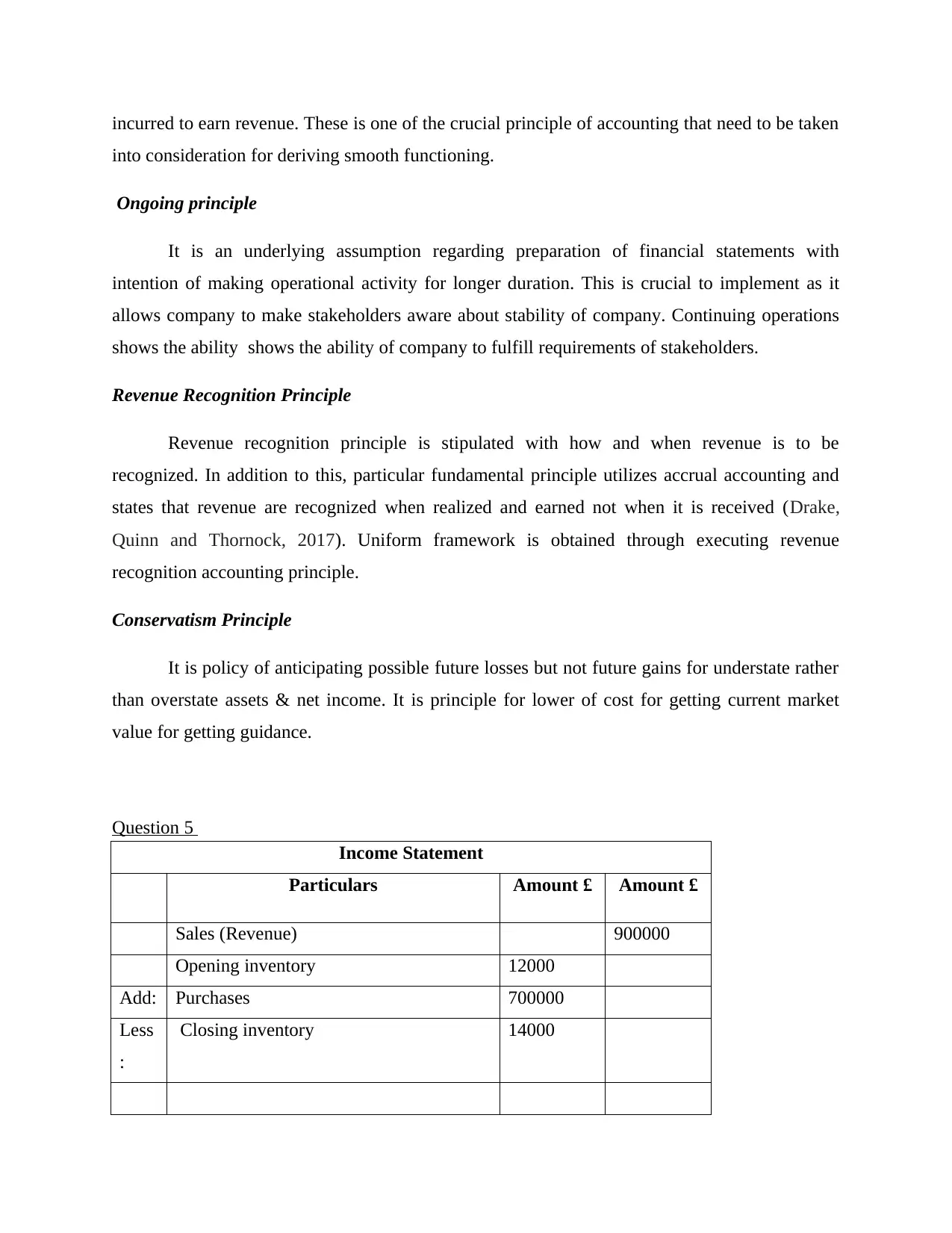

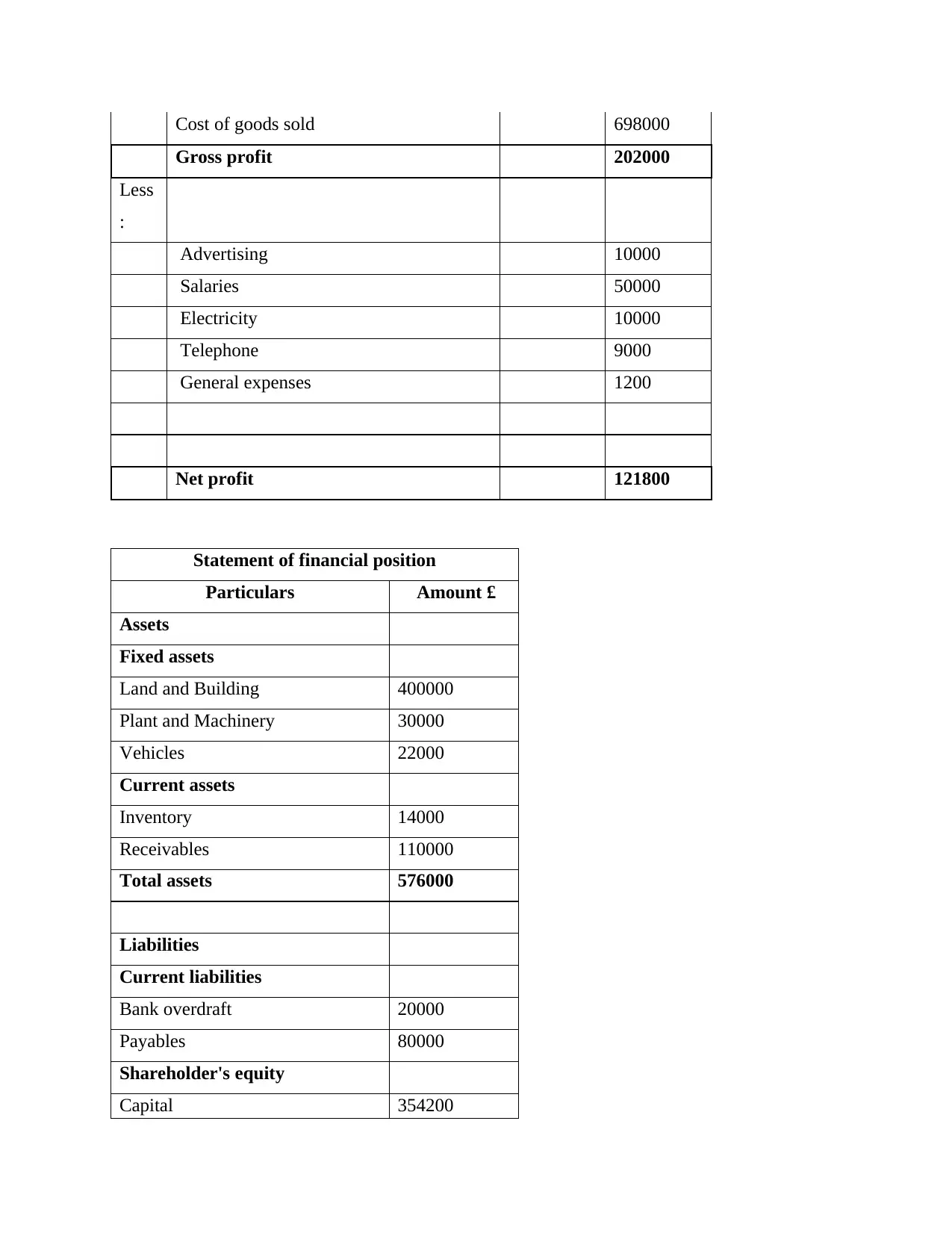

Question 5

Income Statement

Particulars Amount £ Amount £

Sales (Revenue) 900000

Opening inventory 12000

Add: Purchases 700000

Less

:

Closing inventory 14000

into consideration for deriving smooth functioning.

Ongoing principle

It is an underlying assumption regarding preparation of financial statements with

intention of making operational activity for longer duration. This is crucial to implement as it

allows company to make stakeholders aware about stability of company. Continuing operations

shows the ability shows the ability of company to fulfill requirements of stakeholders.

Revenue Recognition Principle

Revenue recognition principle is stipulated with how and when revenue is to be

recognized. In addition to this, particular fundamental principle utilizes accrual accounting and

states that revenue are recognized when realized and earned not when it is received (Drake,

Quinn and Thornock, 2017). Uniform framework is obtained through executing revenue

recognition accounting principle.

Conservatism Principle

It is policy of anticipating possible future losses but not future gains for understate rather

than overstate assets & net income. It is principle for lower of cost for getting current market

value for getting guidance.

Question 5

Income Statement

Particulars Amount £ Amount £

Sales (Revenue) 900000

Opening inventory 12000

Add: Purchases 700000

Less

:

Closing inventory 14000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of goods sold 698000

Gross profit 202000

Less

:

Advertising 10000

Salaries 50000

Electricity 10000

Telephone 9000

General expenses 1200

Net profit 121800

Statement of financial position

Particulars Amount £

Assets

Fixed assets

Land and Building 400000

Plant and Machinery 30000

Vehicles 22000

Current assets

Inventory 14000

Receivables 110000

Total assets 576000

Liabilities

Current liabilities

Bank overdraft 20000

Payables 80000

Shareholder's equity

Capital 354200

Gross profit 202000

Less

:

Advertising 10000

Salaries 50000

Electricity 10000

Telephone 9000

General expenses 1200

Net profit 121800

Statement of financial position

Particulars Amount £

Assets

Fixed assets

Land and Building 400000

Plant and Machinery 30000

Vehicles 22000

Current assets

Inventory 14000

Receivables 110000

Total assets 576000

Liabilities

Current liabilities

Bank overdraft 20000

Payables 80000

Shareholder's equity

Capital 354200

Profit 121800

Total liabilities 576000

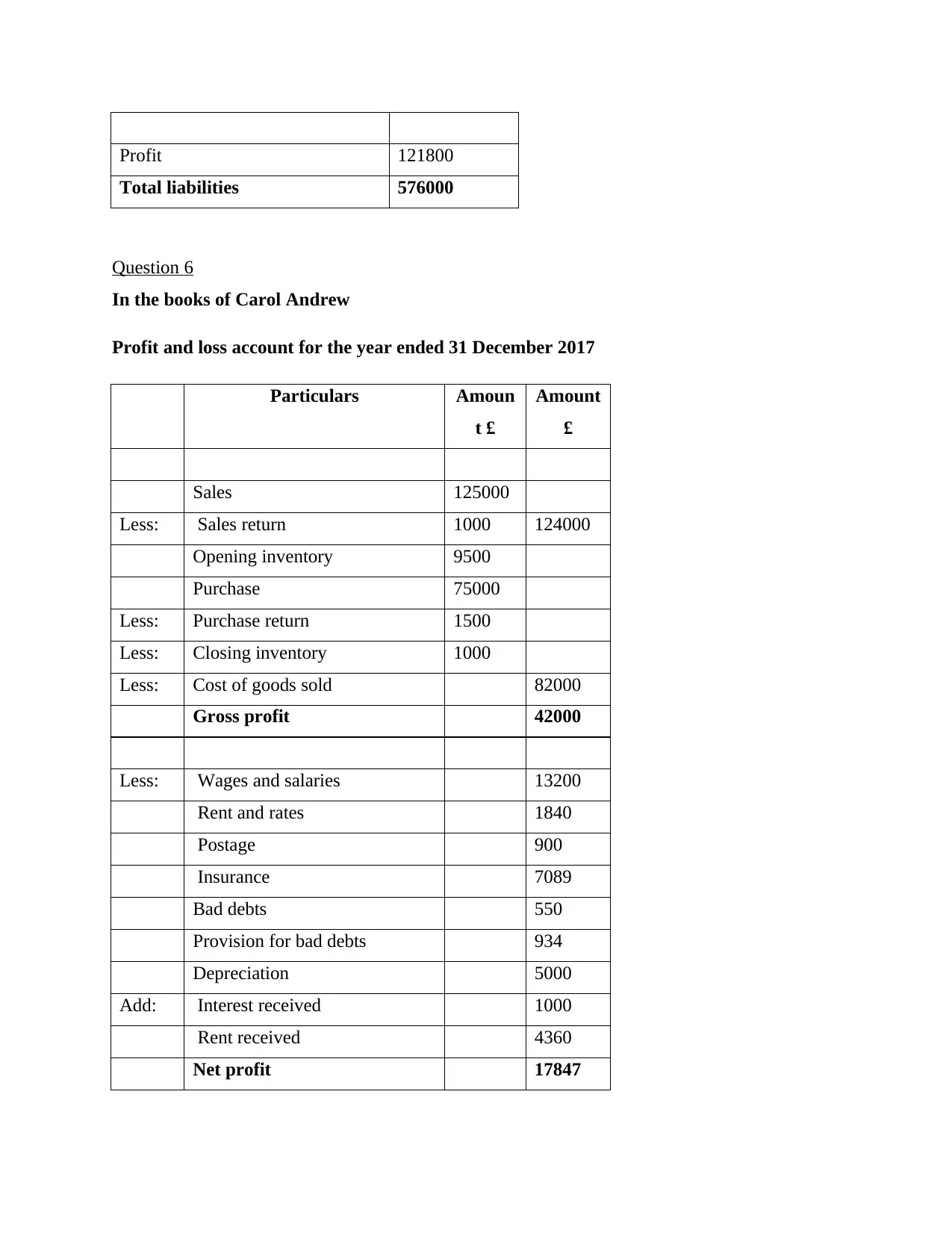

Question 6

In the books of Carol Andrew

Profit and loss account for the year ended 31 December 2017

Particulars Amoun

t £

Amount

£

Sales 125000

Less: Sales return 1000 124000

Opening inventory 9500

Purchase 75000

Less: Purchase return 1500

Less: Closing inventory 1000

Less: Cost of goods sold 82000

Gross profit 42000

Less: Wages and salaries 13200

Rent and rates 1840

Postage 900

Insurance 7089

Bad debts 550

Provision for bad debts 934

Depreciation 5000

Add: Interest received 1000

Rent received 4360

Net profit 17847

Total liabilities 576000

Question 6

In the books of Carol Andrew

Profit and loss account for the year ended 31 December 2017

Particulars Amoun

t £

Amount

£

Sales 125000

Less: Sales return 1000 124000

Opening inventory 9500

Purchase 75000

Less: Purchase return 1500

Less: Closing inventory 1000

Less: Cost of goods sold 82000

Gross profit 42000

Less: Wages and salaries 13200

Rent and rates 1840

Postage 900

Insurance 7089

Bad debts 550

Provision for bad debts 934

Depreciation 5000

Add: Interest received 1000

Rent received 4360

Net profit 17847

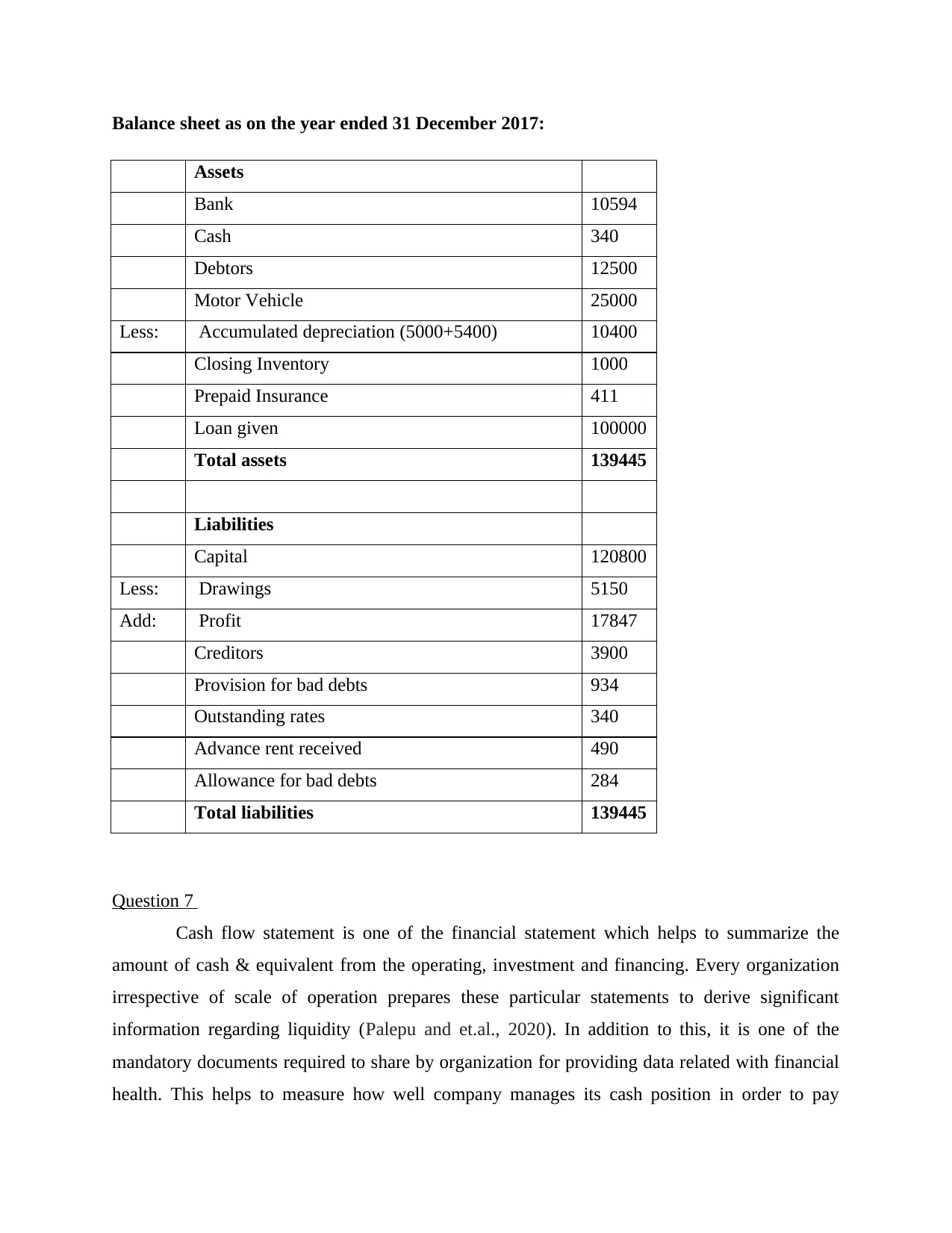

Balance sheet as on the year ended 31 December 2017:

Assets

Bank 10594

Cash 340

Debtors 12500

Motor Vehicle 25000

Less: Accumulated depreciation (5000+5400) 10400

Closing Inventory 1000

Prepaid Insurance 411

Loan given 100000

Total assets 139445

Liabilities

Capital 120800

Less: Drawings 5150

Add: Profit 17847

Creditors 3900

Provision for bad debts 934

Outstanding rates 340

Advance rent received 490

Allowance for bad debts 284

Total liabilities 139445

Question 7

Cash flow statement is one of the financial statement which helps to summarize the

amount of cash & equivalent from the operating, investment and financing. Every organization

irrespective of scale of operation prepares these particular statements to derive significant

information regarding liquidity (Palepu and et.al., 2020). In addition to this, it is one of the

mandatory documents required to share by organization for providing data related with financial

health. This helps to measure how well company manages its cash position in order to pay

Assets

Bank 10594

Cash 340

Debtors 12500

Motor Vehicle 25000

Less: Accumulated depreciation (5000+5400) 10400

Closing Inventory 1000

Prepaid Insurance 411

Loan given 100000

Total assets 139445

Liabilities

Capital 120800

Less: Drawings 5150

Add: Profit 17847

Creditors 3900

Provision for bad debts 934

Outstanding rates 340

Advance rent received 490

Allowance for bad debts 284

Total liabilities 139445

Question 7

Cash flow statement is one of the financial statement which helps to summarize the

amount of cash & equivalent from the operating, investment and financing. Every organization

irrespective of scale of operation prepares these particular statements to derive significant

information regarding liquidity (Palepu and et.al., 2020). In addition to this, it is one of the

mandatory documents required to share by organization for providing data related with financial

health. This helps to measure how well company manages its cash position in order to pay

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

obligations. It provides investor deep insights about financial footing of company so that

accurate decision regarding investment can be taken. Operational efficiency is as well can be

assessed through giving emphasis on cash flow statement. It is basically obtained from three

segments operations, financing and investing that segmentation is widely utilized by stakeholders

for taking strategic decision.

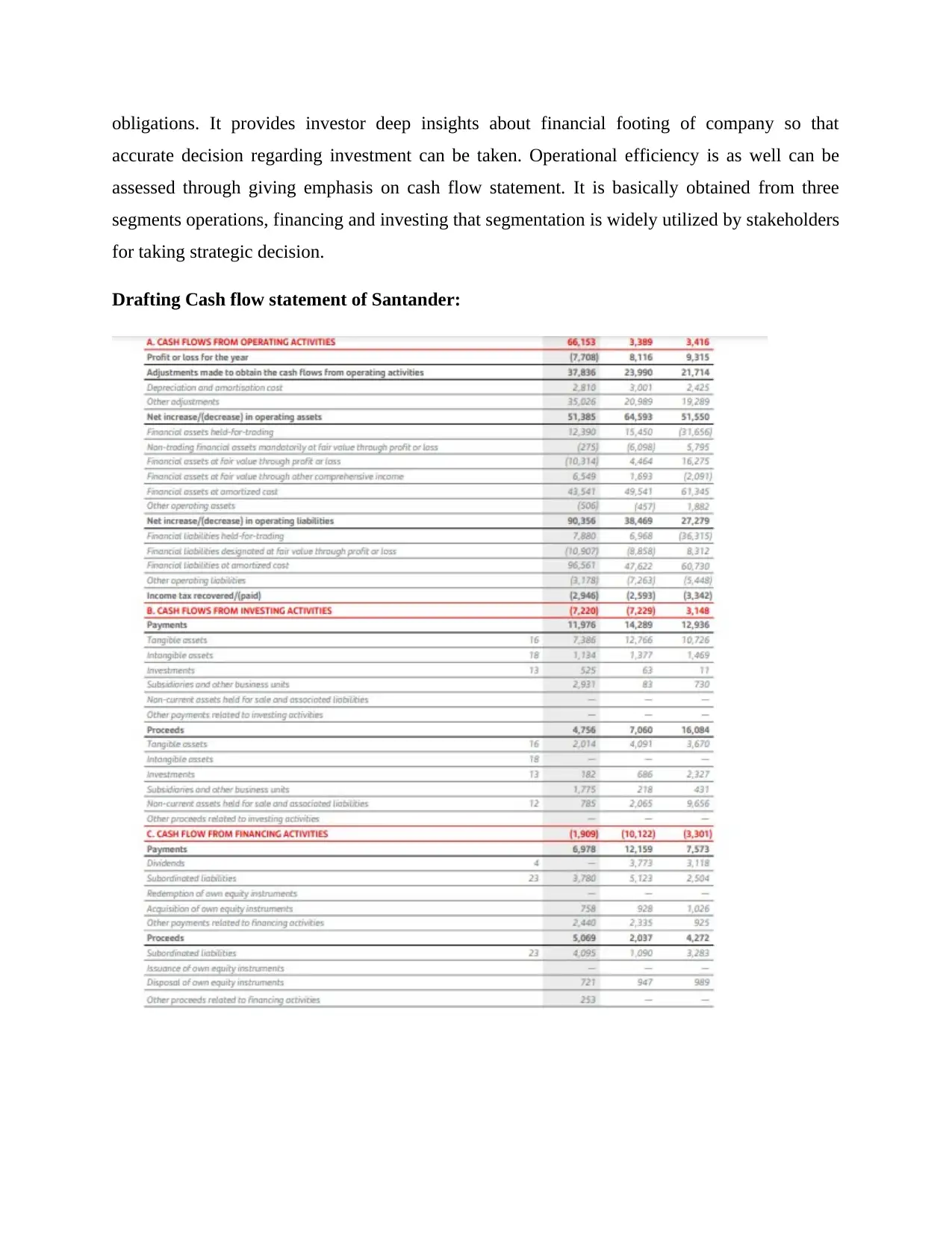

Drafting Cash flow statement of Santander:

accurate decision regarding investment can be taken. Operational efficiency is as well can be

assessed through giving emphasis on cash flow statement. It is basically obtained from three

segments operations, financing and investing that segmentation is widely utilized by stakeholders

for taking strategic decision.

Drafting Cash flow statement of Santander:

SCENARIO 2

Question 1

Bank Reconciliation is summary of banking that matches its balance of bank account

with financial records. It is basically prepared on periodically basis to determine the exact

balance. There are various purposes for which it is prepared and compared with official

statements to accomplish the objective of getting fair details. Identifying errors with help of bank

reconciliation becomes possible (Othman, Laswad and Berkahn, 2020). There are many

situations in which balances of both statement differs that represents errors and mistakes in any

of them. BRS provides assistance in recording transaction so that detecting errors can become

possible. Errors like addition, subtraction, missed payment, etc are some of type of mistakes that

can be obtained with help of bank reconciliation. Investigating interest & other fees related to

bank services utilization can be determined. In addition to this, detecting variety of frauds to

prevent organization’s fund from employees by removing situation of falsifying books &

reconciliation (Sunarya, Nurhaeni and Haris, 2017). It provides opportunity to avoid scenario

that can adversely impact success of company. The reason behind it is that there are many

circumstances in which making payments in order to sustain credibility and trustworthiness

among stakeholder becomes essential. BRS enable company to get information regarding

receivables so that unwanted awkward situations can be avoided. Having efficient organizational

process with ability to maintain significant relationship with stakeholders becomes possible by

executing BRS in company. It is not mandatory to formulate but implementing this specified

method is always beneficial.

It is systematic procedure which is widely taken into consideration to derive objective of

matching both opening balance of bank statement and specified column in cash book. Comparing

this statement enables company to identify missed entry so that necessary adjustment in it can be

made. It is concerned with providing emphasis on several areas like credit, debit side, spotting

errors, rectifying, matching balances of specified statements, etc. BRS process with focusing on

all these helps in avoiding unnecessary penalties with identifying discrepancies at initial stage

(Porter and Norton, 2017). All these steps assist in getting efficient BRS so that company can

obtain efficiency for getting desirable position.

Question 1

Bank Reconciliation is summary of banking that matches its balance of bank account

with financial records. It is basically prepared on periodically basis to determine the exact

balance. There are various purposes for which it is prepared and compared with official

statements to accomplish the objective of getting fair details. Identifying errors with help of bank

reconciliation becomes possible (Othman, Laswad and Berkahn, 2020). There are many

situations in which balances of both statement differs that represents errors and mistakes in any

of them. BRS provides assistance in recording transaction so that detecting errors can become

possible. Errors like addition, subtraction, missed payment, etc are some of type of mistakes that

can be obtained with help of bank reconciliation. Investigating interest & other fees related to

bank services utilization can be determined. In addition to this, detecting variety of frauds to

prevent organization’s fund from employees by removing situation of falsifying books &

reconciliation (Sunarya, Nurhaeni and Haris, 2017). It provides opportunity to avoid scenario

that can adversely impact success of company. The reason behind it is that there are many

circumstances in which making payments in order to sustain credibility and trustworthiness

among stakeholder becomes essential. BRS enable company to get information regarding

receivables so that unwanted awkward situations can be avoided. Having efficient organizational

process with ability to maintain significant relationship with stakeholders becomes possible by

executing BRS in company. It is not mandatory to formulate but implementing this specified

method is always beneficial.

It is systematic procedure which is widely taken into consideration to derive objective of

matching both opening balance of bank statement and specified column in cash book. Comparing

this statement enables company to identify missed entry so that necessary adjustment in it can be

made. It is concerned with providing emphasis on several areas like credit, debit side, spotting

errors, rectifying, matching balances of specified statements, etc. BRS process with focusing on

all these helps in avoiding unnecessary penalties with identifying discrepancies at initial stage

(Porter and Norton, 2017). All these steps assist in getting efficient BRS so that company can

obtain efficiency for getting desirable position.

Question 2

Control Account is summarized form in general ledger which can as well be referred as

adjustment account. The details regarding control account is found in corresponding subsidiary

ledger. It keeps clean of details but contains accurate balance for preparation of financial

statements. In further manner tracking control account with help of subsidiary ledger (What is a

Control Account? 2021). In addition to this, control account is widely taken into practice for

account receivable & payable. The ending balance of subsidiary ledger with control account

should match in order to check accuracy. It is based on daily basis which is commonly used by

large organization. Small organizations takes the general ledger account with linking in

subsidiary account. It comprises total credit of sales, for day, total collection from customers,

return, allowances and many more. It provides mechanism for checking errors & fraud at early

stage.

In financial management control account play crucial role through detecting mistakes so

that clean and detailed information can be attained through this. Providing correct data for

formulating financial statements is another important played by control account (Sutopo and

et.al., 2018). It helps in checking balance of each account before positing it into primary

statement. Control account as well speed up the process of management accounts as deeper

insights through getting balance information before positing can be derived. Avoiding irrelevant

data for effective strategy formulation through saving time by giving emphasis on crucial

information becomes possible through implementing control account in process. Specialized

work via segregating divisions also enable to prepare profit & loss account, balance sheet ,etc.

become possible. These are the contribution of control account in financial management.

Question 3

Suspense Account is utilized to record unclassified transaction that temporarily holds

entries for continuing organizational. This types of account in found in general ledger for

holding discrepancies information utile its actual account is identified. There are numerous

situations in which suspense account is formulated which includes preparation of trail balance,

company has received partial payments, unclassified transactions, etc. It is opened to carry

transaction until it is transferred to its transferred to original account. Accounting books are

made organized through accurately posting all transactions. It helps in avoiding mistakes like

Control Account is summarized form in general ledger which can as well be referred as

adjustment account. The details regarding control account is found in corresponding subsidiary

ledger. It keeps clean of details but contains accurate balance for preparation of financial

statements. In further manner tracking control account with help of subsidiary ledger (What is a

Control Account? 2021). In addition to this, control account is widely taken into practice for

account receivable & payable. The ending balance of subsidiary ledger with control account

should match in order to check accuracy. It is based on daily basis which is commonly used by

large organization. Small organizations takes the general ledger account with linking in

subsidiary account. It comprises total credit of sales, for day, total collection from customers,

return, allowances and many more. It provides mechanism for checking errors & fraud at early

stage.

In financial management control account play crucial role through detecting mistakes so

that clean and detailed information can be attained through this. Providing correct data for

formulating financial statements is another important played by control account (Sutopo and

et.al., 2018). It helps in checking balance of each account before positing it into primary

statement. Control account as well speed up the process of management accounts as deeper

insights through getting balance information before positing can be derived. Avoiding irrelevant

data for effective strategy formulation through saving time by giving emphasis on crucial

information becomes possible through implementing control account in process. Specialized

work via segregating divisions also enable to prepare profit & loss account, balance sheet ,etc.

become possible. These are the contribution of control account in financial management.

Question 3

Suspense Account is utilized to record unclassified transaction that temporarily holds

entries for continuing organizational. This types of account in found in general ledger for

holding discrepancies information utile its actual account is identified. There are numerous

situations in which suspense account is formulated which includes preparation of trail balance,

company has received partial payments, unclassified transactions, etc. It is opened to carry

transaction until it is transferred to its transferred to original account. Accounting books are

made organized through accurately posting all transactions. It helps in avoiding mistakes like

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

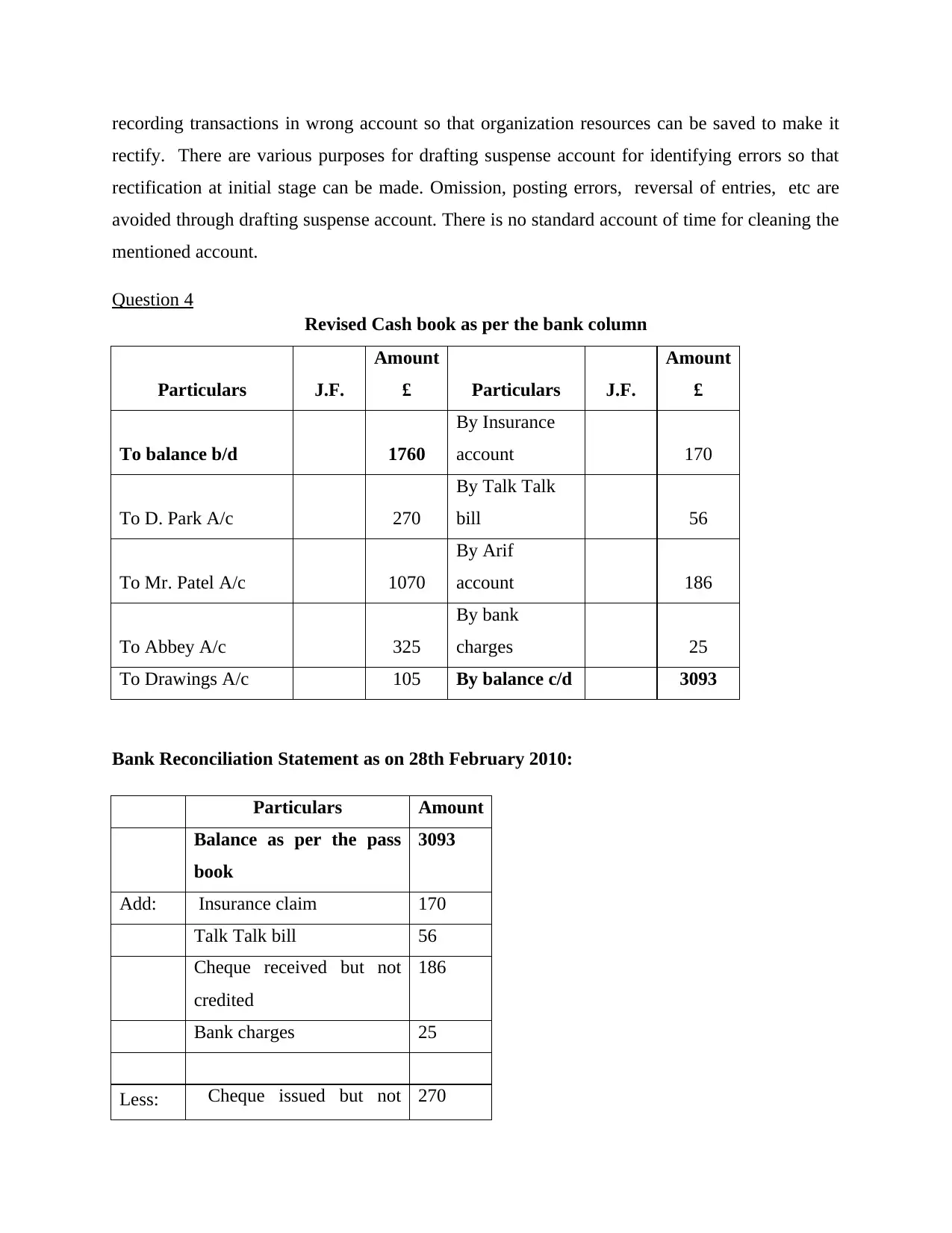

recording transactions in wrong account so that organization resources can be saved to make it

rectify. There are various purposes for drafting suspense account for identifying errors so that

rectification at initial stage can be made. Omission, posting errors, reversal of entries, etc are

avoided through drafting suspense account. There is no standard account of time for cleaning the

mentioned account.

Question 4

Revised Cash book as per the bank column

Particulars J.F.

Amount

£ Particulars J.F.

Amount

£

To balance b/d 1760

By Insurance

account 170

To D. Park A/c 270

By Talk Talk

bill 56

To Mr. Patel A/c 1070

By Arif

account 186

To Abbey A/c 325

By bank

charges 25

To Drawings A/c 105 By balance c/d 3093

Bank Reconciliation Statement as on 28th February 2010:

Particulars Amount

Balance as per the pass

book

3093

Add: Insurance claim 170

Talk Talk bill 56

Cheque received but not

credited

186

Bank charges 25

Less: Cheque issued but not 270

rectify. There are various purposes for drafting suspense account for identifying errors so that

rectification at initial stage can be made. Omission, posting errors, reversal of entries, etc are

avoided through drafting suspense account. There is no standard account of time for cleaning the

mentioned account.

Question 4

Revised Cash book as per the bank column

Particulars J.F.

Amount

£ Particulars J.F.

Amount

£

To balance b/d 1760

By Insurance

account 170

To D. Park A/c 270

By Talk Talk

bill 56

To Mr. Patel A/c 1070

By Arif

account 186

To Abbey A/c 325

By bank

charges 25

To Drawings A/c 105 By balance c/d 3093

Bank Reconciliation Statement as on 28th February 2010:

Particulars Amount

Balance as per the pass

book

3093

Add: Insurance claim 170

Talk Talk bill 56

Cheque received but not

credited

186

Bank charges 25

Less: Cheque issued but not 270

presented for payment

Transfer to bank directly 1070

Dividend received by

Abbey bank

325

Drawings not recorded 105

Balance as per Cash book 1760

Direct Debit

It is particular procedure in which one person’s gives instruction in advance to another

for making transaction related with collecting amount directly through withdrawing from

payer’s account (Osadchy and et.al., 2018). This is utilized for recurring payments such as utility

bills, credit cards, etc. It is completely different from standing order

Standing order

This is considered with giving instruction by bank account holder to their bank to pay

money at regular basis to another’s account. It is used to make payments like rent, utility bills,

interest, etc. Standing order is useful in situations of regular payments which are to be made in

certain parties.

Bank Charges

Bank charges are fees which are charged by bank from the accountholder in respect of

utilizing its services like fund transfer, collection & clearance of cheque, etc.

Dis honor cheque

It is related with the situation where bank denies passing cheque due to low funds,

incorrect message, etc. in addition to this, it is also informed to both parties and also penalty is

charged.

Question 5

a) Journal entries

Transfer to bank directly 1070

Dividend received by

Abbey bank

325

Drawings not recorded 105

Balance as per Cash book 1760

Direct Debit

It is particular procedure in which one person’s gives instruction in advance to another

for making transaction related with collecting amount directly through withdrawing from

payer’s account (Osadchy and et.al., 2018). This is utilized for recurring payments such as utility

bills, credit cards, etc. It is completely different from standing order

Standing order

This is considered with giving instruction by bank account holder to their bank to pay

money at regular basis to another’s account. It is used to make payments like rent, utility bills,

interest, etc. Standing order is useful in situations of regular payments which are to be made in

certain parties.

Bank Charges

Bank charges are fees which are charged by bank from the accountholder in respect of

utilizing its services like fund transfer, collection & clearance of cheque, etc.

Dis honor cheque

It is related with the situation where bank denies passing cheque due to low funds,

incorrect message, etc. in addition to this, it is also informed to both parties and also penalty is

charged.

Question 5

a) Journal entries

Particulars

L.F

. Debit Credit

L.F

. Debit Credit

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

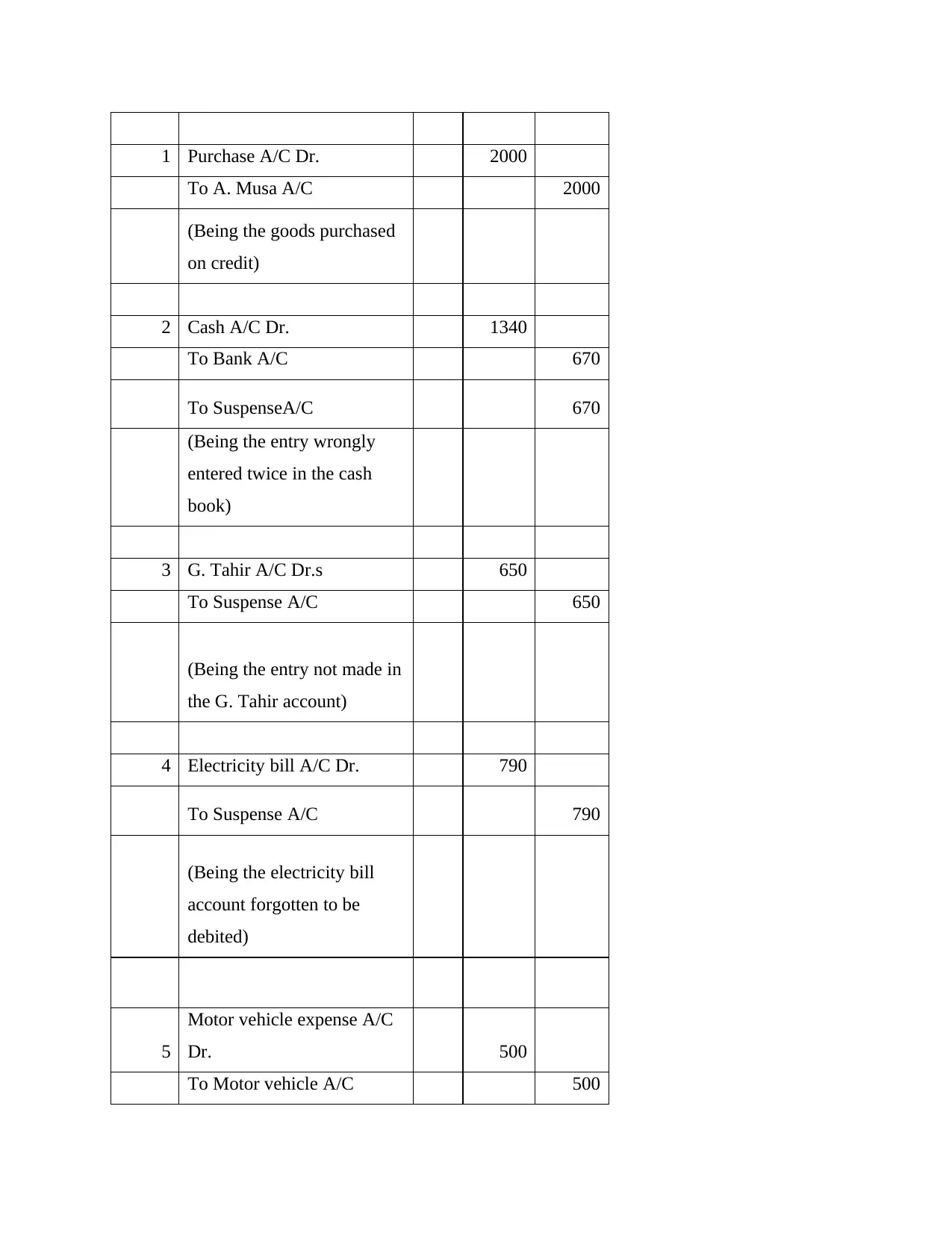

1 Purchase A/C Dr. 2000

To A. Musa A/C 2000

(Being the goods purchased

on credit)

2 Cash A/C Dr. 1340

To Bank A/C 670

To SuspenseA/C 670

(Being the entry wrongly

entered twice in the cash

book)

3 G. Tahir A/C Dr.s 650

To Suspense A/C 650

(Being the entry not made in

the G. Tahir account)

4 Electricity bill A/C Dr. 790

To Suspense A/C 790

(Being the electricity bill

account forgotten to be

debited)

5

Motor vehicle expense A/C

Dr. 500

To Motor vehicle A/C 500

To A. Musa A/C 2000

(Being the goods purchased

on credit)

2 Cash A/C Dr. 1340

To Bank A/C 670

To SuspenseA/C 670

(Being the entry wrongly

entered twice in the cash

book)

3 G. Tahir A/C Dr.s 650

To Suspense A/C 650

(Being the entry not made in

the G. Tahir account)

4 Electricity bill A/C Dr. 790

To Suspense A/C 790

(Being the electricity bill

account forgotten to be

debited)

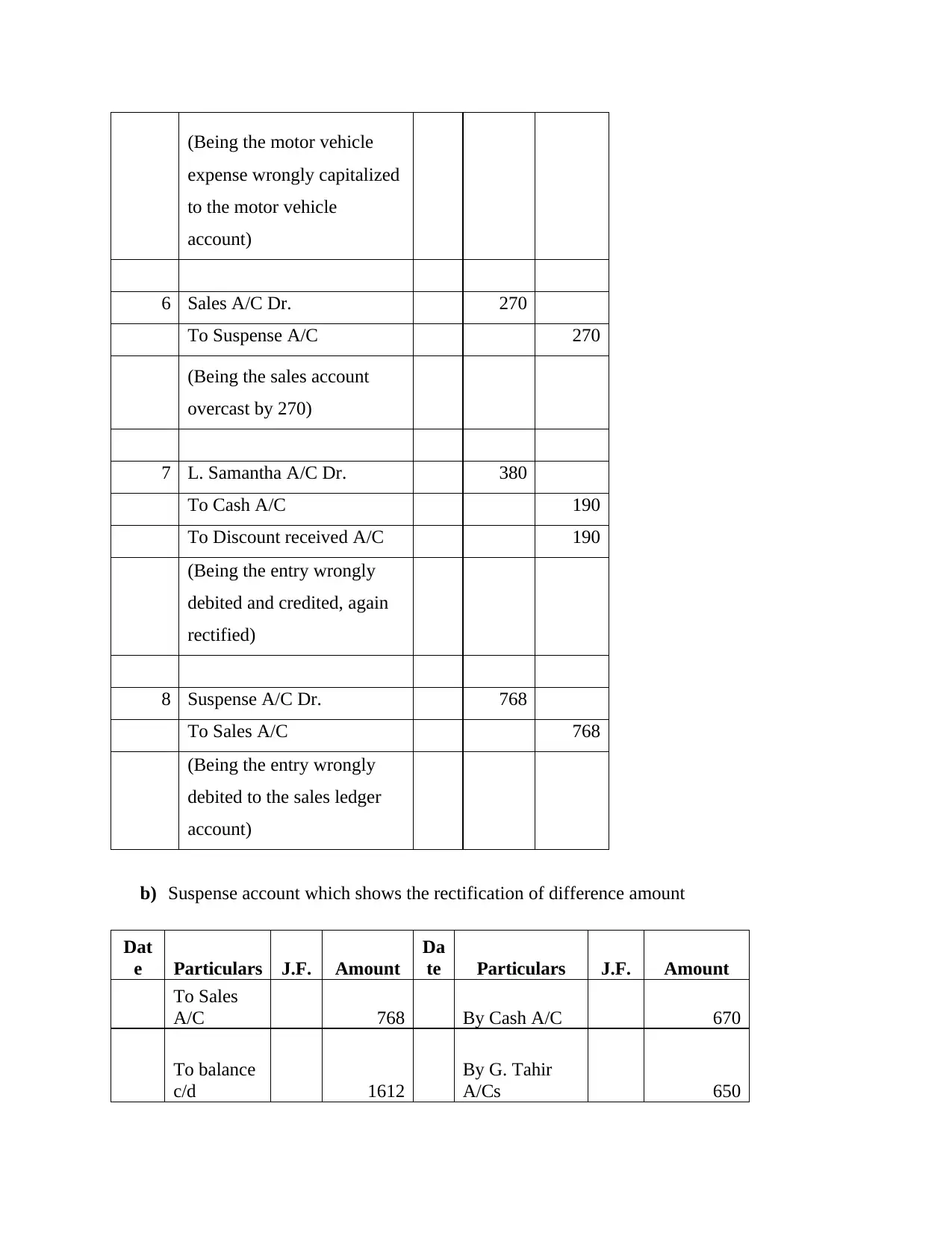

5

Motor vehicle expense A/C

Dr. 500

To Motor vehicle A/C 500

(Being the motor vehicle

expense wrongly capitalized

to the motor vehicle

account)

6 Sales A/C Dr. 270

To Suspense A/C 270

(Being the sales account

overcast by 270)

7 L. Samantha A/C Dr. 380

To Cash A/C 190

To Discount received A/C 190

(Being the entry wrongly

debited and credited, again

rectified)

8 Suspense A/C Dr. 768

To Sales A/C 768

(Being the entry wrongly

debited to the sales ledger

account)

b) Suspense account which shows the rectification of difference amount

Dat

e Particulars J.F. Amount

Da

te Particulars J.F. Amount

To Sales

A/C 768 By Cash A/C 670

To balance

c/d 1612

By G. Tahir

A/Cs 650

expense wrongly capitalized

to the motor vehicle

account)

6 Sales A/C Dr. 270

To Suspense A/C 270

(Being the sales account

overcast by 270)

7 L. Samantha A/C Dr. 380

To Cash A/C 190

To Discount received A/C 190

(Being the entry wrongly

debited and credited, again

rectified)

8 Suspense A/C Dr. 768

To Sales A/C 768

(Being the entry wrongly

debited to the sales ledger

account)

b) Suspense account which shows the rectification of difference amount

Dat

e Particulars J.F. Amount

Da

te Particulars J.F. Amount

To Sales

A/C 768 By Cash A/C 670

To balance

c/d 1612

By G. Tahir

A/Cs 650

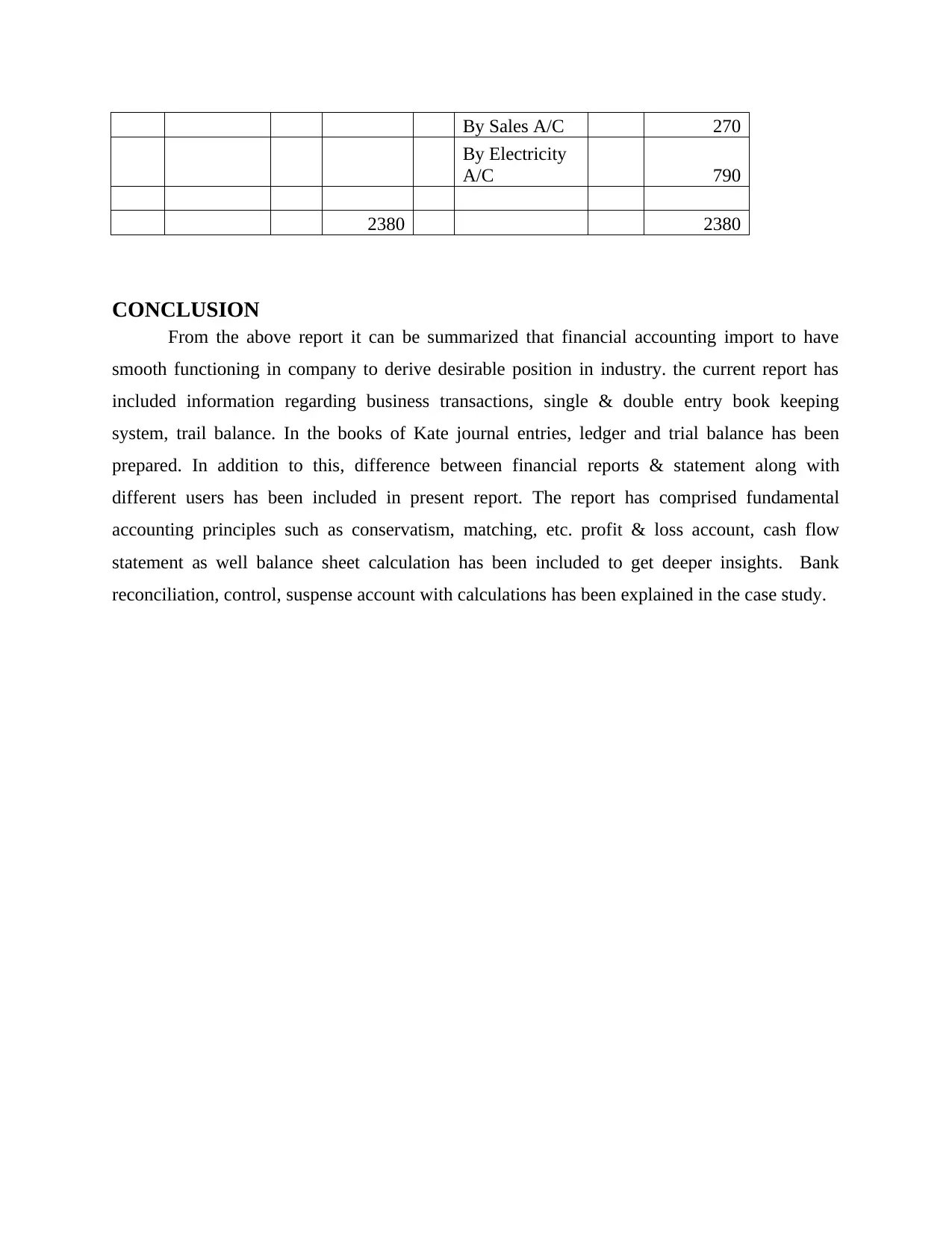

By Sales A/C 270

By Electricity

A/C 790

2380 2380

CONCLUSION

From the above report it can be summarized that financial accounting import to have

smooth functioning in company to derive desirable position in industry. the current report has

included information regarding business transactions, single & double entry book keeping

system, trail balance. In the books of Kate journal entries, ledger and trial balance has been

prepared. In addition to this, difference between financial reports & statement along with

different users has been included in present report. The report has comprised fundamental

accounting principles such as conservatism, matching, etc. profit & loss account, cash flow

statement as well balance sheet calculation has been included to get deeper insights. Bank

reconciliation, control, suspense account with calculations has been explained in the case study.

By Electricity

A/C 790

2380 2380

CONCLUSION

From the above report it can be summarized that financial accounting import to have

smooth functioning in company to derive desirable position in industry. the current report has

included information regarding business transactions, single & double entry book keeping

system, trail balance. In the books of Kate journal entries, ledger and trial balance has been

prepared. In addition to this, difference between financial reports & statement along with

different users has been included in present report. The report has comprised fundamental

accounting principles such as conservatism, matching, etc. profit & loss account, cash flow

statement as well balance sheet calculation has been included to get deeper insights. Bank

reconciliation, control, suspense account with calculations has been explained in the case study.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from

EDGAR. Accounting Horizons. 31(3). pp.55-68.

Garbowski, M. and et.al., 2019. Financial accounting of E-business enterprises. Academy of

Accounting and Financial Studies Journal. 23. pp.1-5.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Othman, R., Laswad, F. and Berkahn, M., 2020. Financial CRIM Es in small businesses: causes

and consequences. Journal of Financial Crime.

Palepu, K.G and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Porter, G. A. and Norton, C. L., 2017. Using financial accounting information: the alternative to

debits and credits. Cengage Learning.

Siagian, A. O., 2020. Contribution of Inventory Accounting Systems in Improving Inventory

Internal Control. Journal of Social Science. 1(2). pp.1-6.s

Sunarya, P.A., Nurhaeni, T. and Haris, H., 2017. Bank Reconciliation Process Efficiency Using

Online Web Based Accounting System 2.0 in Companies. Aptisi

Transactions on Management. 1(2). pp.124-129.

Sutopo, B. and et.al., 2018. Sustainability Reporting and value relevance of financial

statements. Sustainability, 10(3), p.678.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Online

Financial Statements vs. Financial Reports – What’s the Difference? 2021. [Online]. Available

through:< https://www.fyisoft.com/financial-statements-vs-financial-

reports/>

What is a Control Account? 2021. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/4/control-account>

Books and Journals

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from

EDGAR. Accounting Horizons. 31(3). pp.55-68.

Garbowski, M. and et.al., 2019. Financial accounting of E-business enterprises. Academy of

Accounting and Financial Studies Journal. 23. pp.1-5.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Othman, R., Laswad, F. and Berkahn, M., 2020. Financial CRIM Es in small businesses: causes

and consequences. Journal of Financial Crime.

Palepu, K.G and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Porter, G. A. and Norton, C. L., 2017. Using financial accounting information: the alternative to

debits and credits. Cengage Learning.

Siagian, A. O., 2020. Contribution of Inventory Accounting Systems in Improving Inventory

Internal Control. Journal of Social Science. 1(2). pp.1-6.s

Sunarya, P.A., Nurhaeni, T. and Haris, H., 2017. Bank Reconciliation Process Efficiency Using

Online Web Based Accounting System 2.0 in Companies. Aptisi

Transactions on Management. 1(2). pp.124-129.

Sutopo, B. and et.al., 2018. Sustainability Reporting and value relevance of financial

statements. Sustainability, 10(3), p.678.

Warren, C. S., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

Online

Financial Statements vs. Financial Reports – What’s the Difference? 2021. [Online]. Available

through:< https://www.fyisoft.com/financial-statements-vs-financial-

reports/>

What is a Control Account? 2021. [Online]. Available through:

<https://www.accountingtools.com/articles/2017/5/4/control-account>

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.