Accounting: Business Transactions, Financial Statements, Fundamental Principles

Added on 2022-11-25

26 Pages4285 Words155 Views

ACCOUNTING

TABLE OF CONTENTS

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................16

SCENARIO 2............................................................................................................................................17

Question 1.............................................................................................................................................17

Question 2.............................................................................................................................................18

Question 3.............................................................................................................................................19

Question 4.............................................................................................................................................19

Question 5.............................................................................................................................................21

CONCLUSION.........................................................................................................................................23

REFERENCES..........................................................................................................................................24

INTRODUCTION.......................................................................................................................................3

SCENARIO 1..............................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................4

Question 3.............................................................................................................................................11

Question 4.............................................................................................................................................12

Question 5.............................................................................................................................................13

Question 6.............................................................................................................................................15

Question 7.............................................................................................................................................16

SCENARIO 2............................................................................................................................................17

Question 1.............................................................................................................................................17

Question 2.............................................................................................................................................18

Question 3.............................................................................................................................................19

Question 4.............................................................................................................................................19

Question 5.............................................................................................................................................21

CONCLUSION.........................................................................................................................................23

REFERENCES..........................................................................................................................................24

INTRODUCTION

Financial Accounting (FA) is procedure of utilizing monetary information through

making summarization of related data to gain deeper insights about firm’s liquidity position. In

present era, it is crucial for company to have efficient FA procedure to derive significant

information to get competitive advantages. The current study is based on providing important

regarding concepts like business transaction, accounting principles, journal entries, ledger, trial

balance, financial reports & statements, cash flow, bank reconciliation, control & suspense

account, etc. To get deeper insights about the same related calculations will be provided in the

systematic format .

SCENARIO 1

Question 1

Business Transaction is related with an economic activity which is recorded in

accounting system. There are different forms of business transaction that are important to

recorded for analyzing, evaluating and controlling monetary position. In order to have

sustainability company conducts different kinds of transaction that are related to internal

and external practices. It includes, cash & credit purchase, sales, raising funds,

expenditure regarding interest, tax, salaries, etc. For having accurate estimation of

company position it becomes essential for organization to record all types of business

transactions.

Single entry presents one sided organizational picture that is unable to track all

transactions as it records business activities partially. On the other side, double entry

system is based on fundamental accounting principle that helps company take all aspects

transactions into consideration (Siagian, 2020). It becomes difficult to identify the errors

through single entry system as compared to double. Assessing financial position with

help of double entry book keeping system it become convenient.

Trial Balance (TB) is combined worksheet that comprises all ledgers’ balances which is

done once the reporting period. For ensuring book keeping accuracy through equalizing

debit & credit balance TB is prepared. It is utilized for various purposes such as

preparation of financial statements, identifying & rectifying errors, formulation of audit

Financial Accounting (FA) is procedure of utilizing monetary information through

making summarization of related data to gain deeper insights about firm’s liquidity position. In

present era, it is crucial for company to have efficient FA procedure to derive significant

information to get competitive advantages. The current study is based on providing important

regarding concepts like business transaction, accounting principles, journal entries, ledger, trial

balance, financial reports & statements, cash flow, bank reconciliation, control & suspense

account, etc. To get deeper insights about the same related calculations will be provided in the

systematic format .

SCENARIO 1

Question 1

Business Transaction is related with an economic activity which is recorded in

accounting system. There are different forms of business transaction that are important to

recorded for analyzing, evaluating and controlling monetary position. In order to have

sustainability company conducts different kinds of transaction that are related to internal

and external practices. It includes, cash & credit purchase, sales, raising funds,

expenditure regarding interest, tax, salaries, etc. For having accurate estimation of

company position it becomes essential for organization to record all types of business

transactions.

Single entry presents one sided organizational picture that is unable to track all

transactions as it records business activities partially. On the other side, double entry

system is based on fundamental accounting principle that helps company take all aspects

transactions into consideration (Siagian, 2020). It becomes difficult to identify the errors

through single entry system as compared to double. Assessing financial position with

help of double entry book keeping system it become convenient.

Trial Balance (TB) is combined worksheet that comprises all ledgers’ balances which is

done once the reporting period. For ensuring book keeping accuracy through equalizing

debit & credit balance TB is prepared. It is utilized for various purposes such as

preparation of financial statements, identifying & rectifying errors, formulation of audit

reports, strategic decision making, comparative analysis, etc. These all provides

assistance in assessing arithmetical accuracy of organization.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

assistance in assessing arithmetical accuracy of organization.

Question 2

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

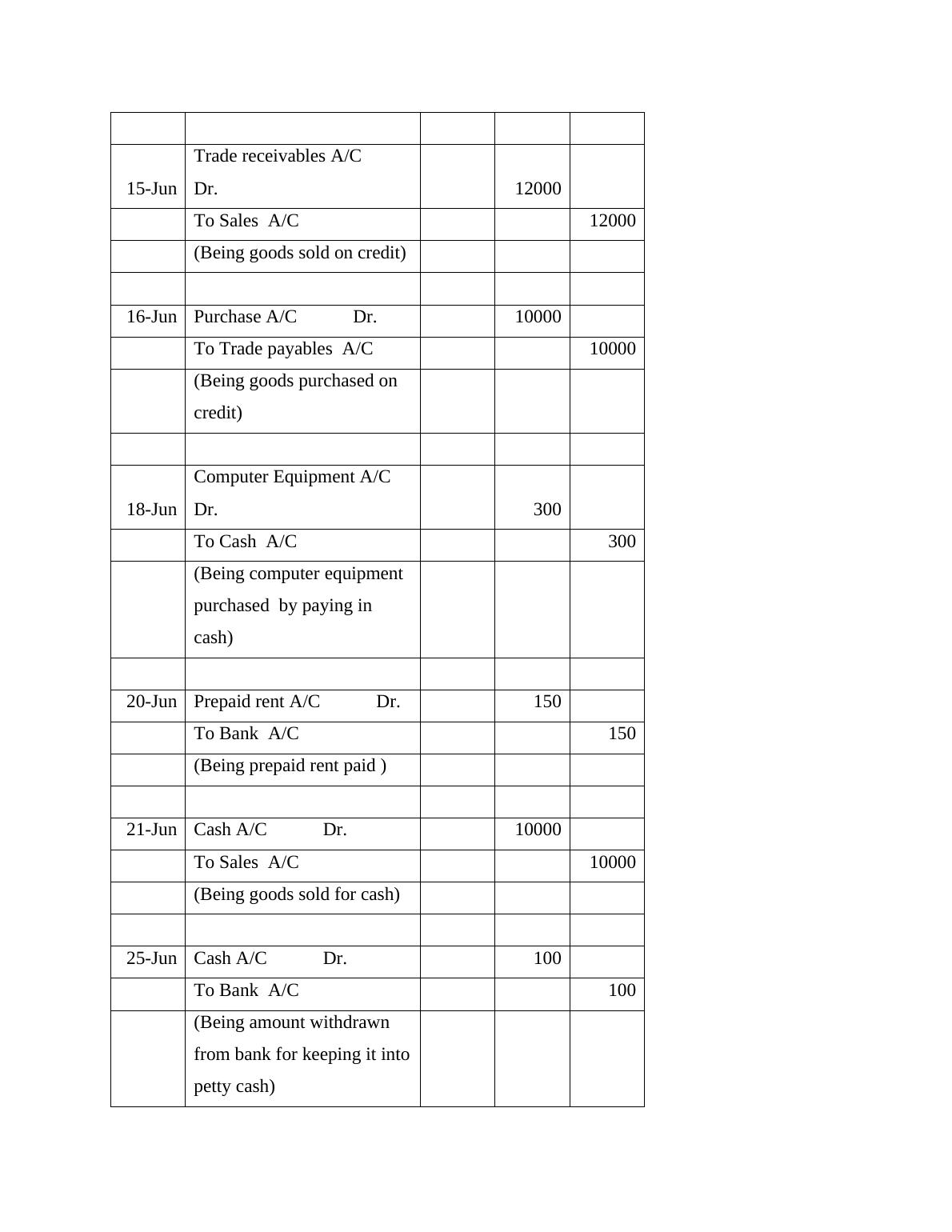

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

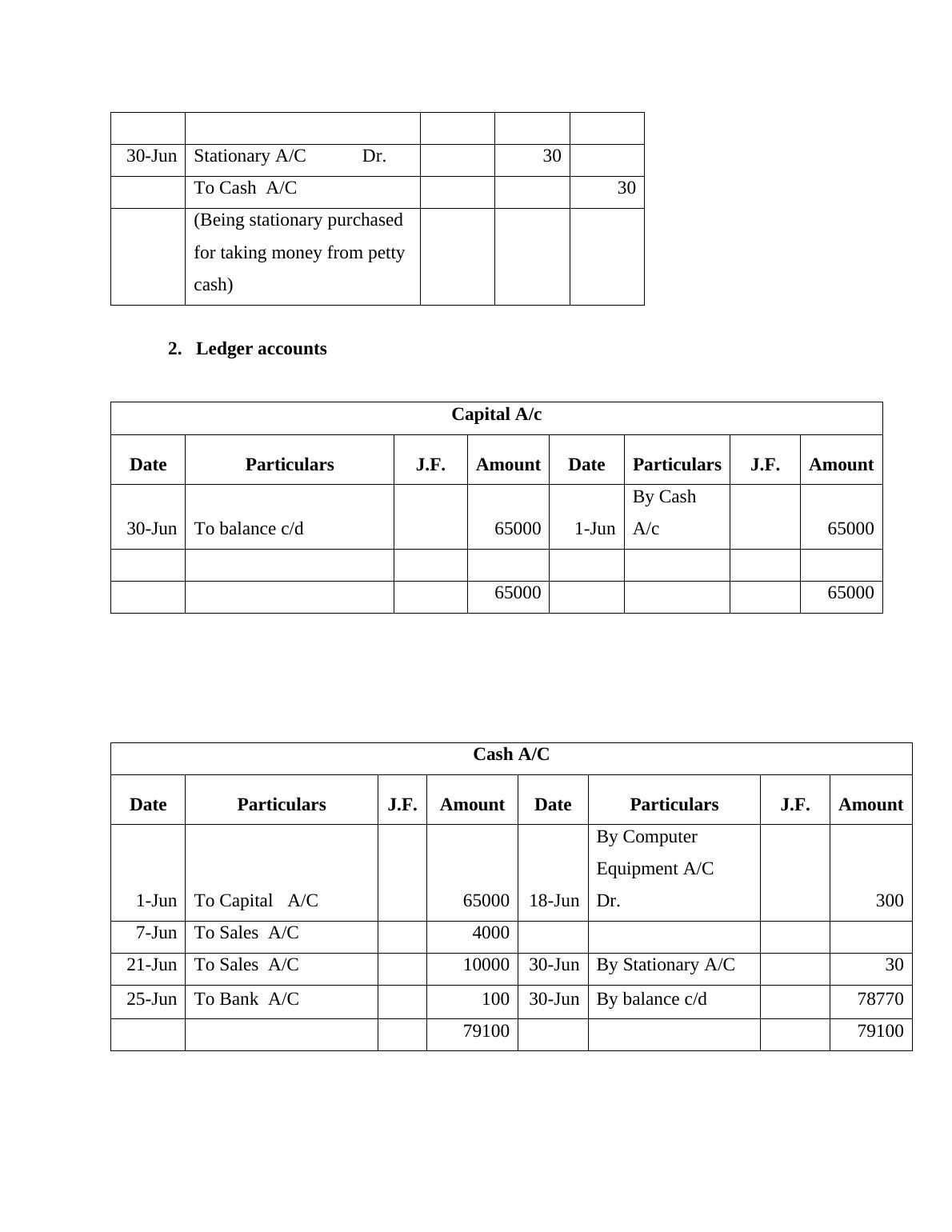

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Financial Accounting: Concepts and Principleslg...

|25

|4323

|68

Financial Accounting Projectlg...

|10

|2071

|369

Financial Accounting Assignment Solutionlg...

|12

|1352

|66

Different Types of Business Transactions and Accounting Principleslg...

|29

|4091

|320

P4 Preparation of financial accounts for sole trader and limited companylg...

|13

|1961

|172

FINANCIAL ACCOUNTING TABLE OF CONTENTSlg...

|18

|3952

|92