Financial Accounting Assignment: Case Study Analysis and Report

VerifiedAdded on 2022/11/28

|25

|4323

|68

Homework Assignment

AI Summary

This financial accounting assignment presents a comprehensive analysis of key accounting concepts through two detailed scenarios. The solution includes journal entries, ledger accounts, trial balances, income statements, and balance sheets, providing a deep dive into double-entry bookkeeping, financial statement preparation, and the application of accounting principles. The assignment covers business transactions, the differences between financial reports and statements, and the roles of various stakeholders in financial reporting. It also delves into the fundamental principles of accounting, such as the matching principle, accrual principle, going concern, full disclosure, and revenue recognition, offering a practical understanding of their application. Furthermore, the solution includes a profit and loss account and a balance sheet, demonstrating the practical application of accounting knowledge. This document serves as a valuable resource for students studying financial accounting, offering insights into real-world applications and problem-solving techniques.

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION........................................................................................................... 3

SCENARIO 1................................................................................................................. 3

Question 1.................................................................................................................. 3

Question 2.................................................................................................................. 4

Question 3................................................................................................................ 11

Question 4................................................................................................................ 13

Question 5................................................................................................................ 14

Question 6................................................................................................................ 15

Question 7................................................................................................................ 17

SCENARIO 2............................................................................................................... 18

Question 1................................................................................................................ 18

Question 2................................................................................................................ 19

Question 3................................................................................................................ 20

Question 4................................................................................................................ 21

Question 5................................................................................................................ 22

CONCLUSION............................................................................................................. 25

REFERENCES............................................................................................................. 26

INTRODUCTION........................................................................................................... 3

SCENARIO 1................................................................................................................. 3

Question 1.................................................................................................................. 3

Question 2.................................................................................................................. 4

Question 3................................................................................................................ 11

Question 4................................................................................................................ 13

Question 5................................................................................................................ 14

Question 6................................................................................................................ 15

Question 7................................................................................................................ 17

SCENARIO 2............................................................................................................... 18

Question 1................................................................................................................ 18

Question 2................................................................................................................ 19

Question 3................................................................................................................ 20

Question 4................................................................................................................ 21

Question 5................................................................................................................ 22

CONCLUSION............................................................................................................. 25

REFERENCES............................................................................................................. 26

INTRODUCTION

Financial accounting is the process of recording, analyzing and controlling monetary

information. In current scenario it is essential to implement financial accounting process to drive

important data for decision making. The present report will present various types of essential

concepts like accounting principles, bank reconciliation statement, financial statements, control

& suspense account, etc. It will comprises the calculations like journal entries, ledger account,

trial balance, suspense, bank reconciliation statement, etc to get deeper understanding of mention

concepts. Current case study will involve deep knowledge regarding financial accounting.

SCENARIO 1

Question 1

Business Transactions (BT) are those activities which affect financial position of

organization. There are various types of BT which play crucial role in influencing company

processes. It comprises cash, credit, internal, external which can broadly classified as purchasing

goods, material, services, noncurrent assets, raising funds and paying wages, taxes, interest &

salaries, etc. It becomes essential for company to pay attention on all types of transactions so that

estimation of accurate financial position can be exerted.

Single entry provides one sided view of organizational transaction. In double entry

booking both the aspects of transactions are recorded which provides ability to capture accurate

financial position (Pesci and Girardi, 2021). It makes possible to implement method for error

detection which is not offered by single entry booking. In double entry transaction are recorded

in form of debits and credits.

Trial Balance (TB) is accounting report formulated at the end of financial period so that other

statements can be prepared. Purpose behind creating TB is to permit organization to identify

errors & mistakes so that essential changes through making adjustments can be done. It is

important to prepare as it assist company in decision making regarding budgets, formulating

auditing reports, comparative analysis through identifying mistakes and making adjustments for

rectifying so that arithmetical accuracy can be obtained. Management of firm can balance debt &

credit item by referring the TB. It becomes possible to prepare financial statements by having air

information through trial balance in order to determine actual monetary condition of company.

Financial accounting is the process of recording, analyzing and controlling monetary

information. In current scenario it is essential to implement financial accounting process to drive

important data for decision making. The present report will present various types of essential

concepts like accounting principles, bank reconciliation statement, financial statements, control

& suspense account, etc. It will comprises the calculations like journal entries, ledger account,

trial balance, suspense, bank reconciliation statement, etc to get deeper understanding of mention

concepts. Current case study will involve deep knowledge regarding financial accounting.

SCENARIO 1

Question 1

Business Transactions (BT) are those activities which affect financial position of

organization. There are various types of BT which play crucial role in influencing company

processes. It comprises cash, credit, internal, external which can broadly classified as purchasing

goods, material, services, noncurrent assets, raising funds and paying wages, taxes, interest &

salaries, etc. It becomes essential for company to pay attention on all types of transactions so that

estimation of accurate financial position can be exerted.

Single entry provides one sided view of organizational transaction. In double entry

booking both the aspects of transactions are recorded which provides ability to capture accurate

financial position (Pesci and Girardi, 2021). It makes possible to implement method for error

detection which is not offered by single entry booking. In double entry transaction are recorded

in form of debits and credits.

Trial Balance (TB) is accounting report formulated at the end of financial period so that other

statements can be prepared. Purpose behind creating TB is to permit organization to identify

errors & mistakes so that essential changes through making adjustments can be done. It is

important to prepare as it assist company in decision making regarding budgets, formulating

auditing reports, comparative analysis through identifying mistakes and making adjustments for

rectifying so that arithmetical accuracy can be obtained. Management of firm can balance debt &

credit item by referring the TB. It becomes possible to prepare financial statements by having air

information through trial balance in order to determine actual monetary condition of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Question 2

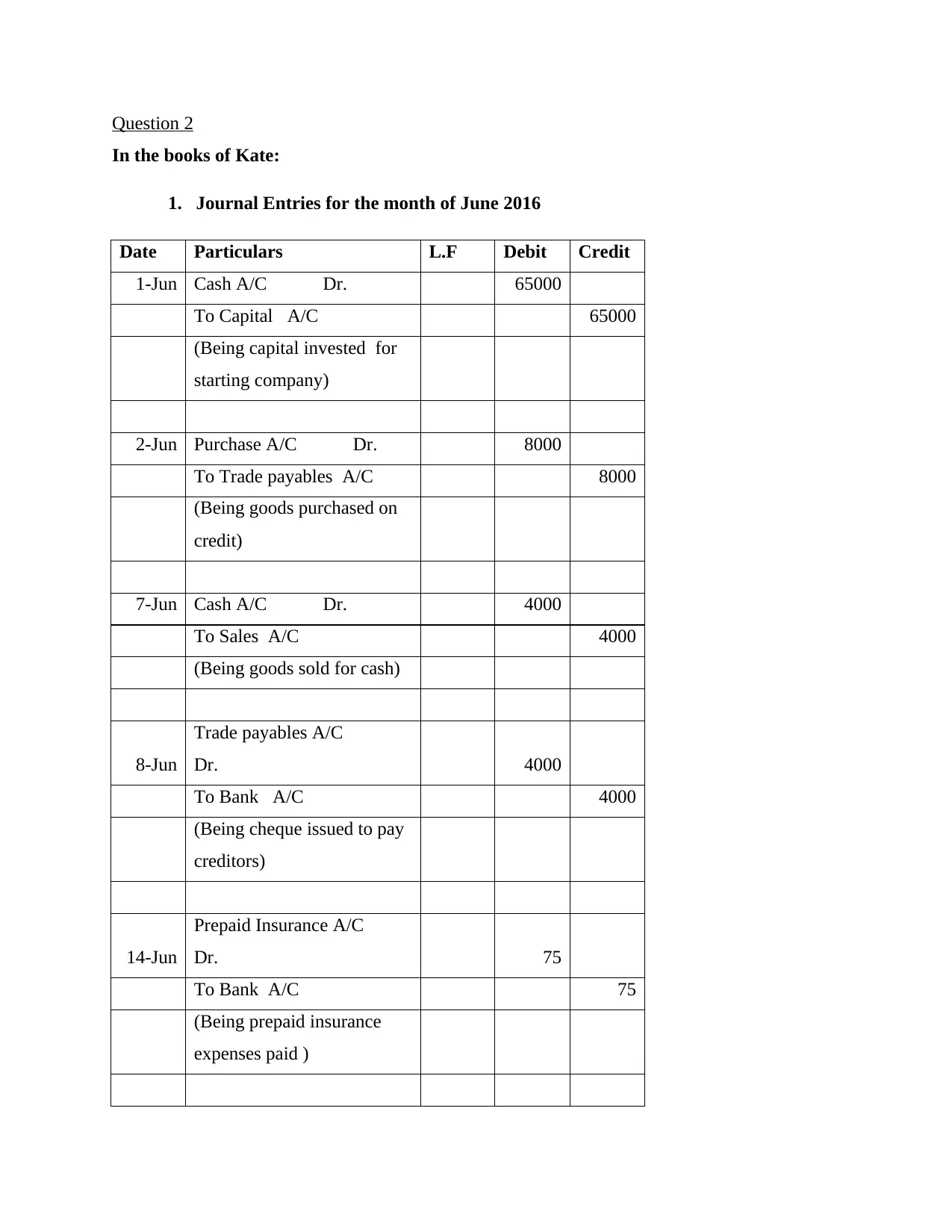

In the books of Kate:

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

In the books of Kate:

1. Journal Entries for the month of June 2016

Date Particulars L.F Debit Credit

1-Jun Cash A/C Dr. 65000

To Capital A/C 65000

(Being capital invested for

starting company)

2-Jun Purchase A/C Dr. 8000

To Trade payables A/C 8000

(Being goods purchased on

credit)

7-Jun Cash A/C Dr. 4000

To Sales A/C 4000

(Being goods sold for cash)

8-Jun

Trade payables A/C

Dr. 4000

To Bank A/C 4000

(Being cheque issued to pay

creditors)

14-Jun

Prepaid Insurance A/C

Dr. 75

To Bank A/C 75

(Being prepaid insurance

expenses paid )

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

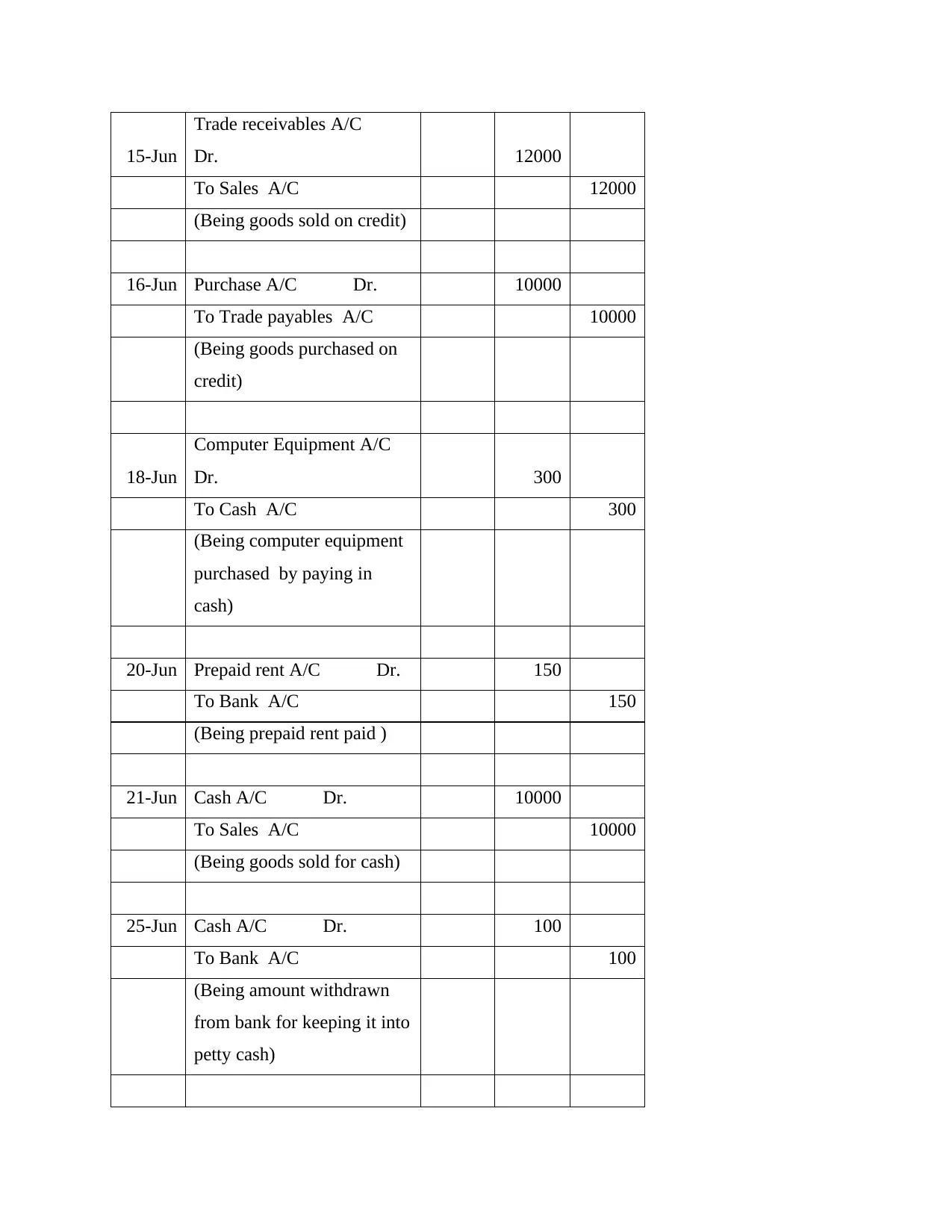

15-Jun

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

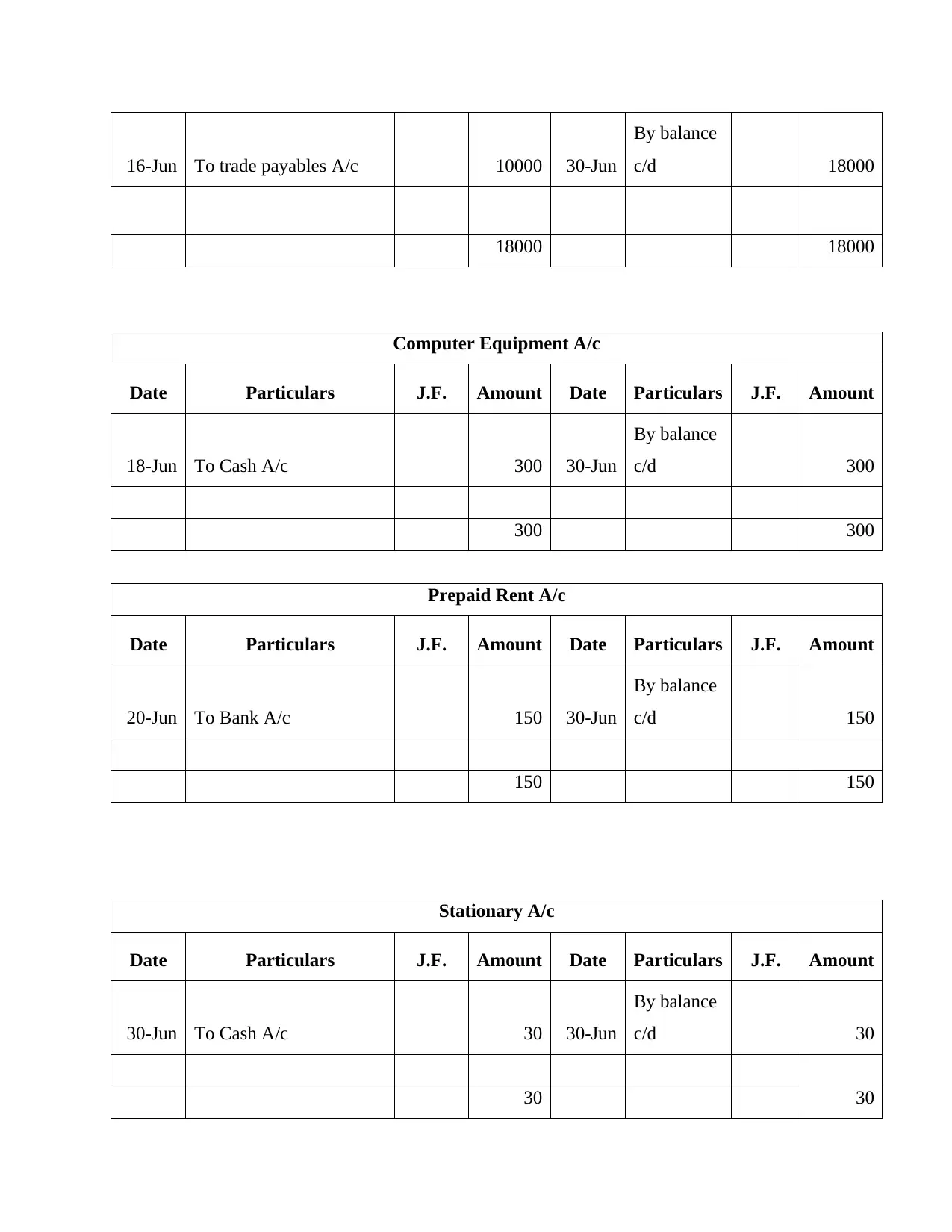

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

Trade receivables A/C

Dr. 12000

To Sales A/C 12000

(Being goods sold on credit)

16-Jun Purchase A/C Dr. 10000

To Trade payables A/C 10000

(Being goods purchased on

credit)

18-Jun

Computer Equipment A/C

Dr. 300

To Cash A/C 300

(Being computer equipment

purchased by paying in

cash)

20-Jun Prepaid rent A/C Dr. 150

To Bank A/C 150

(Being prepaid rent paid )

21-Jun Cash A/C Dr. 10000

To Sales A/C 10000

(Being goods sold for cash)

25-Jun Cash A/C Dr. 100

To Bank A/C 100

(Being amount withdrawn

from bank for keeping it into

petty cash)

30-Jun Stationary A/C Dr. 30

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

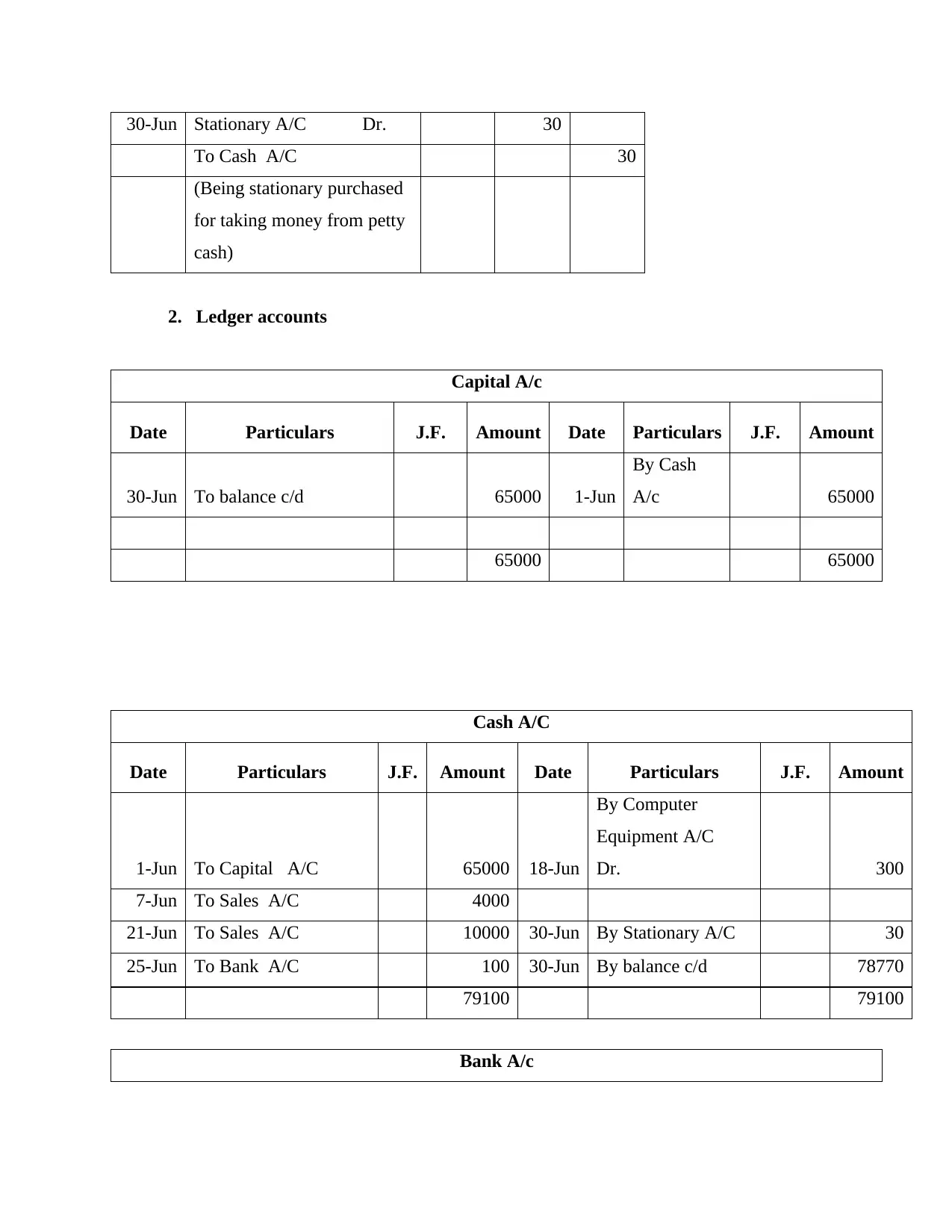

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Bank A/c

To Cash A/C 30

(Being stationary purchased

for taking money from petty

cash)

2. Ledger accounts

Capital A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To balance c/d 65000 1-Jun

By Cash

A/c 65000

65000 65000

Cash A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

1-Jun To Capital A/C 65000 18-Jun

By Computer

Equipment A/C

Dr. 300

7-Jun To Sales A/C 4000

21-Jun To Sales A/C 10000 30-Jun By Stationary A/C 30

25-Jun To Bank A/C 100 30-Jun By balance c/d 78770

79100 79100

Bank A/c

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

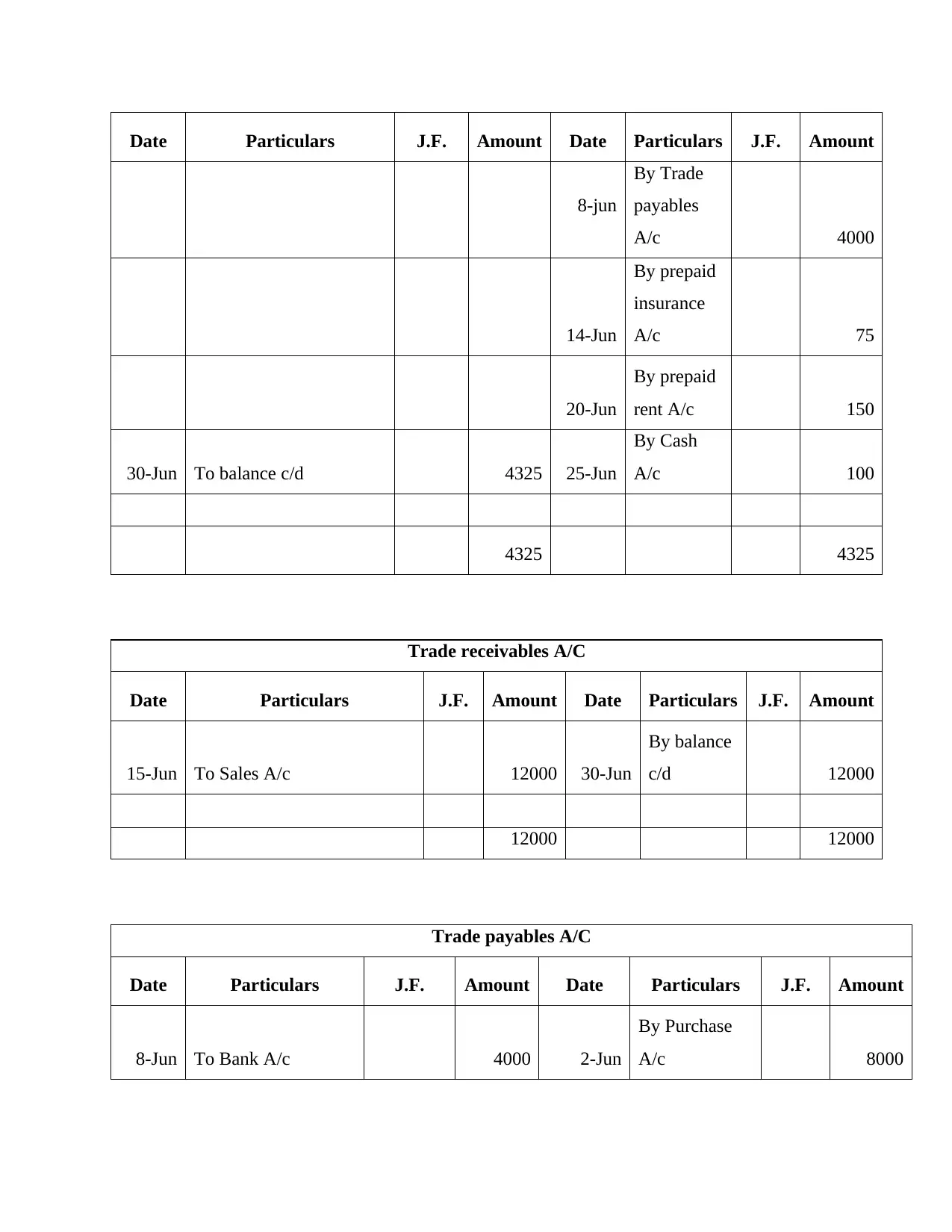

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

8-jun

By Trade

payables

A/c 4000

14-Jun

By prepaid

insurance

A/c 75

20-Jun

By prepaid

rent A/c 150

30-Jun To balance c/d 4325 25-Jun

By Cash

A/c 100

4325 4325

Trade receivables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

15-Jun To Sales A/c 12000 30-Jun

By balance

c/d 12000

12000 12000

Trade payables A/C

Date Particulars J.F. Amount Date Particulars J.F. Amount

8-Jun To Bank A/c 4000 2-Jun

By Purchase

A/c 8000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

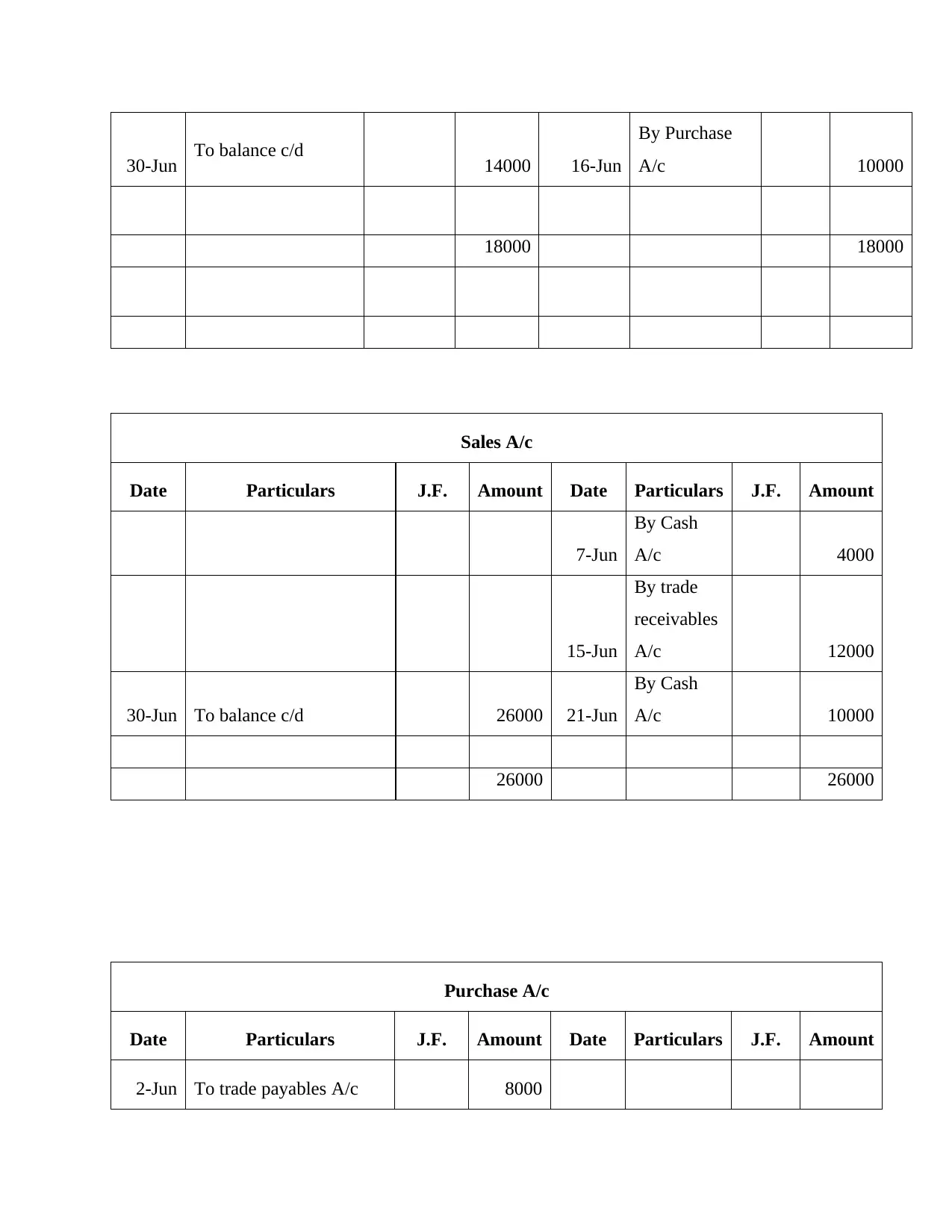

30-Jun To balance c/d 14000 16-Jun

By Purchase

A/c 10000

18000 18000

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

By Purchase

A/c 10000

18000 18000

Sales A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

7-Jun

By Cash

A/c 4000

15-Jun

By trade

receivables

A/c 12000

30-Jun To balance c/d 26000 21-Jun

By Cash

A/c 10000

26000 26000

Purchase A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

2-Jun To trade payables A/c 8000

16-Jun To trade payables A/c 10000 30-Jun

By balance

c/d 18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

By balance

c/d 18000

18000 18000

Computer Equipment A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

18-Jun To Cash A/c 300 30-Jun

By balance

c/d 300

300 300

Prepaid Rent A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

20-Jun To Bank A/c 150 30-Jun

By balance

c/d 150

150 150

Stationary A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

30-Jun To Cash A/c 30 30-Jun

By balance

c/d 30

30 30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

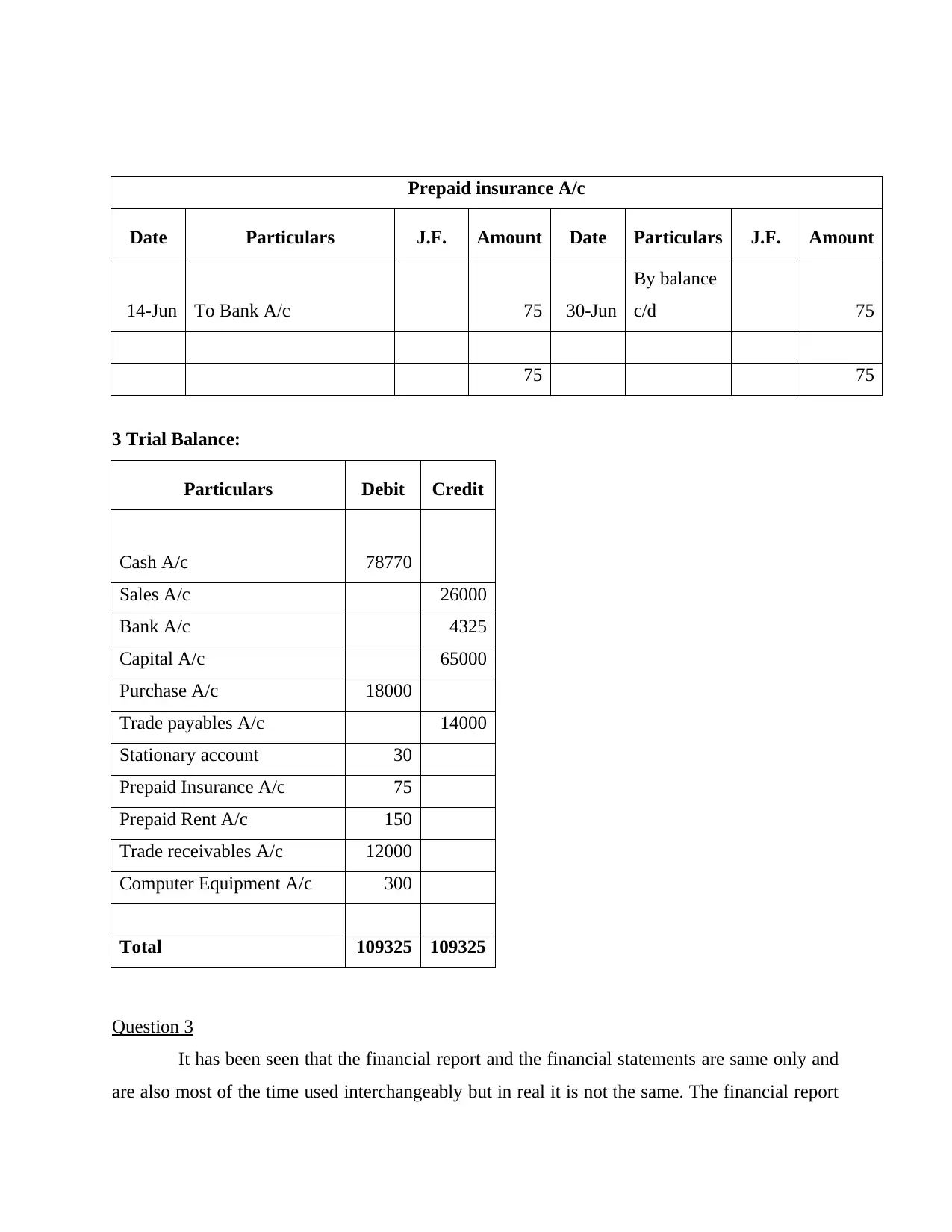

Prepaid insurance A/c

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

It has been seen that the financial report and the financial statements are same only and

are also most of the time used interchangeably but in real it is not the same. The financial report

Date Particulars J.F. Amount Date Particulars J.F. Amount

14-Jun To Bank A/c 75 30-Jun

By balance

c/d 75

75 75

3 Trial Balance:

Particulars Debit Credit

Cash A/c 78770

Sales A/c 26000

Bank A/c 4325

Capital A/c 65000

Purchase A/c 18000

Trade payables A/c 14000

Stationary account 30

Prepaid Insurance A/c 75

Prepaid Rent A/c 150

Trade receivables A/c 12000

Computer Equipment A/c 300

Total 109325 109325

Question 3

It has been seen that the financial report and the financial statements are same only and

are also most of the time used interchangeably but in real it is not the same. The financial report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounts for the term which incorporates various types of reports while the financial statements

are considered as one of the reports which falls under the roof of financial report. In simple

terms, the financial statements are basically the financial reports but it is important to understand

that all financial reports are not financial statements. The financial reports collect the relevant

financial information for the purpose of distributing it in public while the financial statements

offer information pertaining to the financial position and the outcomes of the operations

(Difference Between Financial Reporting and Financial Statements. 2017). There is a need of

financial report which provides information on the working or the operations of the business as it

involves reports like the income statement, balance sheet, cash flow statement, equity report, and

other reports as per the business requirement. These reports are essential as it helps in

determining the financial position and performance of the company. Based upon this, various

business-related decisions are being undertaken which helps in bringing benefits to the business.

There are number of users of financial statements which are bifurcated into internal and

external users. The management team uses the financial statements in order understand the

profitability and liquidity position of the company so that they can undertake operational and

financial decisions. The competitors also use such statements in order to gain competitive insight

about its rival so that it can formulate better and effective competitive strategies. Government is

also interested in looking at the financial statements of the company with the objective of

identifying whether the organization has paid the right amount of tax or not. Investors are also

interested into the financial statements as it helps in determining whether the company is

performing well or not and the trend pertaining to the return it is generating. This helps in taking

decision whether the investor should make an investment or not (Users of financial statements.

2021). The suppliers of the company will also require it as it assists in determining the extend to

which the credit can be provided to the firm. this is very important for the suppliers in order to

avoid the chances of bad debts from supplier’s perspective. Banks and the other financial

institutions are also interested as they in-depth analyse the financial statements which helps in

knowing the credibility and the capability of the company in terms of making repayment of the

loan amount along with the interest. Investment analyst is also interested in knowing the

performance and the position of the firm as they provide recommendation in regard to the

financial securities in which the company should make an investment into. Therefore, these are

are considered as one of the reports which falls under the roof of financial report. In simple

terms, the financial statements are basically the financial reports but it is important to understand

that all financial reports are not financial statements. The financial reports collect the relevant

financial information for the purpose of distributing it in public while the financial statements

offer information pertaining to the financial position and the outcomes of the operations

(Difference Between Financial Reporting and Financial Statements. 2017). There is a need of

financial report which provides information on the working or the operations of the business as it

involves reports like the income statement, balance sheet, cash flow statement, equity report, and

other reports as per the business requirement. These reports are essential as it helps in

determining the financial position and performance of the company. Based upon this, various

business-related decisions are being undertaken which helps in bringing benefits to the business.

There are number of users of financial statements which are bifurcated into internal and

external users. The management team uses the financial statements in order understand the

profitability and liquidity position of the company so that they can undertake operational and

financial decisions. The competitors also use such statements in order to gain competitive insight

about its rival so that it can formulate better and effective competitive strategies. Government is

also interested in looking at the financial statements of the company with the objective of

identifying whether the organization has paid the right amount of tax or not. Investors are also

interested into the financial statements as it helps in determining whether the company is

performing well or not and the trend pertaining to the return it is generating. This helps in taking

decision whether the investor should make an investment or not (Users of financial statements.

2021). The suppliers of the company will also require it as it assists in determining the extend to

which the credit can be provided to the firm. this is very important for the suppliers in order to

avoid the chances of bad debts from supplier’s perspective. Banks and the other financial

institutions are also interested as they in-depth analyse the financial statements which helps in

knowing the credibility and the capability of the company in terms of making repayment of the

loan amount along with the interest. Investment analyst is also interested in knowing the

performance and the position of the firm as they provide recommendation in regard to the

financial securities in which the company should make an investment into. Therefore, these are

the key users of the financial statements of the company and plays an important role in the

growth and the progress of the company.

Question 4

Fundamental principles of accounting are crucial and universally applicable which

provides road map to business organization in order to move towards success. These are

mentioned as following

Matching principle -

This allows to achieve aim to match expenses with association revenue for te particular

span of time. It states that firm's earning statement present not only revenue for that duration but

also cost associated with it (McCallig, Robb and Rohde, 2019). This is core of accrual basis of

accounting for adjusting entries.

Accrual principle

It is concerned with recording transactions in effective manner in time when it has

actually occur. With respect to this, it is one of the important principle which play crucial role in

recording & analyzing business transaction in fair manner to determine business actual financial

health.

Going concern

It is related with assumption that entity will continue for longer duration in future . it

helps company to prepare its financial planning in effective manner with keeping in mind

regarding its sustainability so that accomplishment of business objectives can become possible.

This is mostly concerned with having ability to have liquidity in order to avoid insolvency

situations. It allows firm to utilize organizational assets in wise manner so that longer stability in

industry can be attained.

Full disclosure principle

Important information in relevant and fair pattern should be provided by company

through accurate formed financial statements. It is essential for financial analysis and modeling

as these requires fair data in order to make proper decisions, In addition to this, without full

disclosing company any be indulged into legal obligations therefore it becomes essential for

growth and the progress of the company.

Question 4

Fundamental principles of accounting are crucial and universally applicable which

provides road map to business organization in order to move towards success. These are

mentioned as following

Matching principle -

This allows to achieve aim to match expenses with association revenue for te particular

span of time. It states that firm's earning statement present not only revenue for that duration but

also cost associated with it (McCallig, Robb and Rohde, 2019). This is core of accrual basis of

accounting for adjusting entries.

Accrual principle

It is concerned with recording transactions in effective manner in time when it has

actually occur. With respect to this, it is one of the important principle which play crucial role in

recording & analyzing business transaction in fair manner to determine business actual financial

health.

Going concern

It is related with assumption that entity will continue for longer duration in future . it

helps company to prepare its financial planning in effective manner with keeping in mind

regarding its sustainability so that accomplishment of business objectives can become possible.

This is mostly concerned with having ability to have liquidity in order to avoid insolvency

situations. It allows firm to utilize organizational assets in wise manner so that longer stability in

industry can be attained.

Full disclosure principle

Important information in relevant and fair pattern should be provided by company

through accurate formed financial statements. It is essential for financial analysis and modeling

as these requires fair data in order to make proper decisions, In addition to this, without full

disclosing company any be indulged into legal obligations therefore it becomes essential for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.