Financial Accounting: Types of Business Transactions, Financial Analysis, Fundamental Principles, Bank Reconciliation

VerifiedAdded on 2023/01/09

|23

|4455

|92

AI Summary

This report provides an analysis of various types of business transactions, financial analysis of Kate's business, fundamental principles of accounting, and the procedure of bank reconciliation. It covers topics such as sales, purchases, payment to suppliers, payment received from customers, borrowing of money, payroll, drawing, single entry and double entry bookkeeping, trial balance, revenue recognition principle, full disclosure principle, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

Question 1: Analyse types of business transaction......................................................................1

Question 2: Financial analysis of Kate’s business.......................................................................3

Question 3: Difference between financial statement and financial report...................................9

Question 4: Fundamental principles of accounting...................................................................10

Question 5: Final accounts of Carol Andrew’s business...........................................................11

SCENARIO 2................................................................................................................................13

Question 1: Bank reconciliation................................................................................................13

Question 2: Control accounts.....................................................................................................14

Question 3: Suspense account...................................................................................................15

Question 4: Bank reconciliation................................................................................................16

Question 5..................................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

Question 1: Analyse types of business transaction......................................................................1

Question 2: Financial analysis of Kate’s business.......................................................................3

Question 3: Difference between financial statement and financial report...................................9

Question 4: Fundamental principles of accounting...................................................................10

Question 5: Final accounts of Carol Andrew’s business...........................................................11

SCENARIO 2................................................................................................................................13

Question 1: Bank reconciliation................................................................................................13

Question 2: Control accounts.....................................................................................................14

Question 3: Suspense account...................................................................................................15

Question 4: Bank reconciliation................................................................................................16

Question 5..................................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

2

INTRODUCTION

Financial accounting is a sub part of the concept accounting which is concerned with the

accounting procedure of the finances of an organisation. This specialised branch of accounting

records each and every transaction of a business organisation and the summarise all those

transactions in the form of financial reports and final accounts (Balakrishnan and Cohen, 2013).

The main aim of this report is to understand the different stages in financial accounting starting

from journal entries to the rectification of bank reconciliation errors. For this aim, the present

report is classified into two sections focusing two difference accounting scenarios.

In the first section or scenario, various types of business transactions are analysed along

with practical application of primary accounts including journal entries, ledger accounts and trial

balance along with final accounts including profit & loss account and balance sheet. In the

second scenario, the concept of bank reconciliation, suspense account and control account along

with their applications.

3

Financial accounting is a sub part of the concept accounting which is concerned with the

accounting procedure of the finances of an organisation. This specialised branch of accounting

records each and every transaction of a business organisation and the summarise all those

transactions in the form of financial reports and final accounts (Balakrishnan and Cohen, 2013).

The main aim of this report is to understand the different stages in financial accounting starting

from journal entries to the rectification of bank reconciliation errors. For this aim, the present

report is classified into two sections focusing two difference accounting scenarios.

In the first section or scenario, various types of business transactions are analysed along

with practical application of primary accounts including journal entries, ledger accounts and trial

balance along with final accounts including profit & loss account and balance sheet. In the

second scenario, the concept of bank reconciliation, suspense account and control account along

with their applications.

3

SCENARIO 1

Question 1: Analyse types of business transaction

Types of business transaction

A business transaction is an exchange of products and services between a business and

other parties. There are various types of business transaction which can be categorised based on

visibility, institutional relationships, exchange of cash, event and objective (Barth, 2015).

Considering these, types of business transactions are analysed based on the events in an

organisation; analysis to these transactions are depicted below:

Sales – In this business transaction, an organisation sells its manufactured or stored goods

to their end customers, wholesalers or retailers. Such transaction can be in cash or in credit.

These transaction builds revenue for the organisation and result in profitability of the

organisation.

Purchase – When a business entity buys goods or services from their suppliers in order to

ensure efficient operations of their organisation, these transactions are known as purchase. These

transactions result in outflow of monetary funds from an organisation and can be done in cash or

credit.

Payment to supplier – This type of business transaction is only preformed in cash and

reduces the cash inventory in an organisation. This transaction involves the payment of money

which organisation promised to pay their supplier against the sourced raw material or services

(Beatty and Liao, 2014).

Payment received from customers – This type of transaction is quite opposite of the

above transaction as in this one money is being received by the company and impact the credit

accounts of the entity. This transaction results to increase the cash position of an entity.

Borrowing of money – In this transaction, a business organisation acquires money from

financial institutions as a form of loan which organisation promises to pay back with appropriate

and pre agreed interest. Such borrowing can be both for short and long term.

Payroll – This type of transaction involves payment of salaries to the employees of the

organisation. This type of transaction is usually done by using a cheque.

Drawing – It is an internal transaction in which owner of the organisation draws money

from the organisation’s fund for personal use. In such transaction, capital is being impacted.

Single entry and double entry book keeping

4

Question 1: Analyse types of business transaction

Types of business transaction

A business transaction is an exchange of products and services between a business and

other parties. There are various types of business transaction which can be categorised based on

visibility, institutional relationships, exchange of cash, event and objective (Barth, 2015).

Considering these, types of business transactions are analysed based on the events in an

organisation; analysis to these transactions are depicted below:

Sales – In this business transaction, an organisation sells its manufactured or stored goods

to their end customers, wholesalers or retailers. Such transaction can be in cash or in credit.

These transaction builds revenue for the organisation and result in profitability of the

organisation.

Purchase – When a business entity buys goods or services from their suppliers in order to

ensure efficient operations of their organisation, these transactions are known as purchase. These

transactions result in outflow of monetary funds from an organisation and can be done in cash or

credit.

Payment to supplier – This type of business transaction is only preformed in cash and

reduces the cash inventory in an organisation. This transaction involves the payment of money

which organisation promised to pay their supplier against the sourced raw material or services

(Beatty and Liao, 2014).

Payment received from customers – This type of transaction is quite opposite of the

above transaction as in this one money is being received by the company and impact the credit

accounts of the entity. This transaction results to increase the cash position of an entity.

Borrowing of money – In this transaction, a business organisation acquires money from

financial institutions as a form of loan which organisation promises to pay back with appropriate

and pre agreed interest. Such borrowing can be both for short and long term.

Payroll – This type of transaction involves payment of salaries to the employees of the

organisation. This type of transaction is usually done by using a cheque.

Drawing – It is an internal transaction in which owner of the organisation draws money

from the organisation’s fund for personal use. In such transaction, capital is being impacted.

Single entry and double entry book keeping

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Single entry book keeping system is a way to maintain business transactions in an

organisation in which every transaction including income and expenses are recorded as one

entry. This system is usually recorded using a two column ledger in which column is for the

transactions and one is for its associated amount. This type of book keeping system is used by

usually small organisations which are not involved in much transactions.

Double entry book keeping system is a procedure according to which every entry is

recorded into two accounts out of each one of debit and one is credit. The basic agenda of double

entry system is to make sure that the balances of both the sides are equal. It is being considered

that every amount of one column impacts the amount of other column (Bushman, 2014). Instead

of two, there are three columns in this system which are transaction, debit amount and credit

amount.

Trial balance and its importance

Trial balance is developed using double entry book keepings system. Trial balance is a

statement which records balances of all ledger accounts and then entire statement is compiled

into two columns of debit and credit. An accurate and duly developed trial balance has balances

of both the sides equal.

Development of trial balance holds various points of importance for a business

transaction. The statement of trial balance is important as it provides the base for development of

income statement and balance sheet (Edwards, 2013). As this statement is developed using

double entry book keeping, it helps in analysing the arithmetical accuracy of the accounts. This

statement of trial balance is also important as it helps in rectifying the errors and helps in making

reliable decisions for the future strategies of the company.

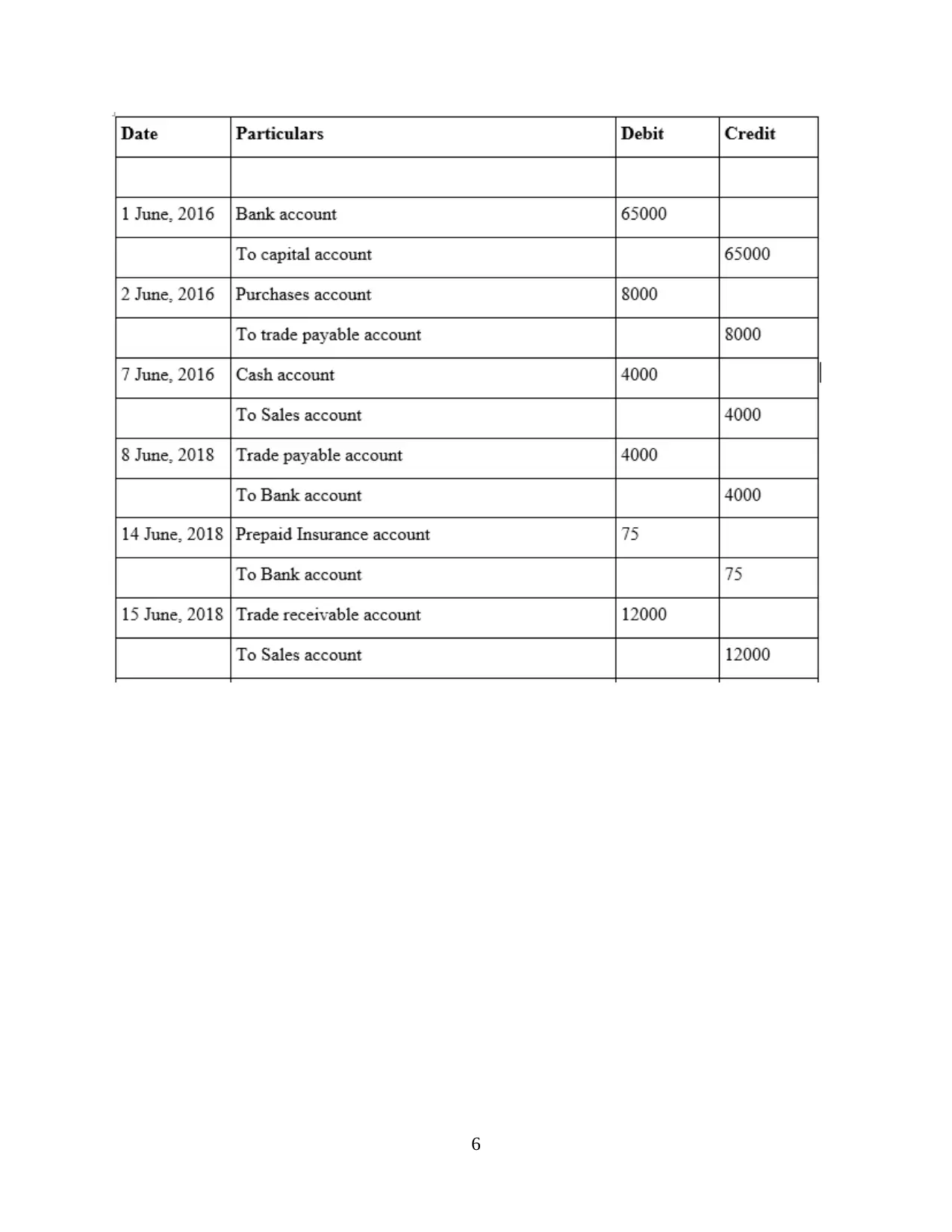

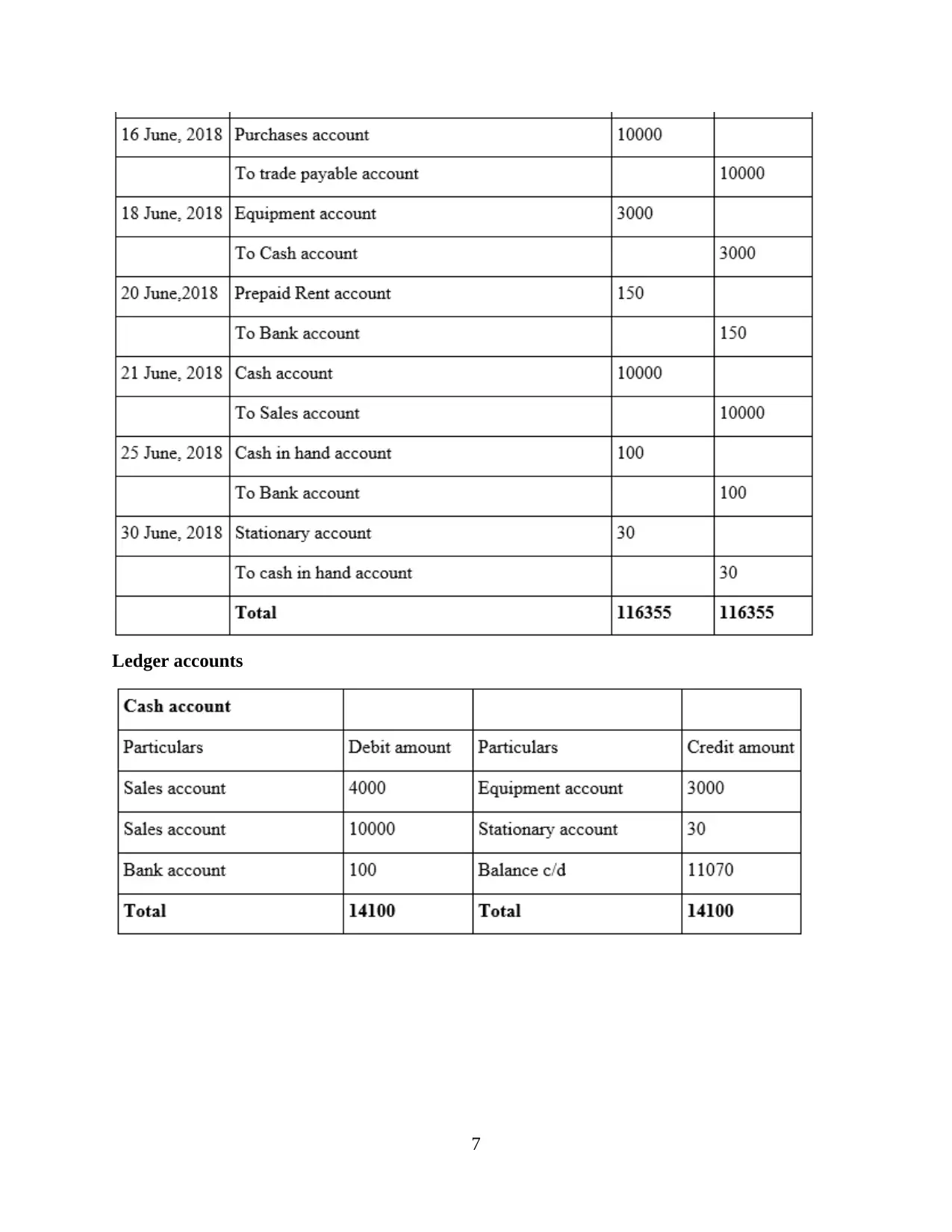

Question 2: Financial analysis of Kate’s business

Journal entries

5

organisation in which every transaction including income and expenses are recorded as one

entry. This system is usually recorded using a two column ledger in which column is for the

transactions and one is for its associated amount. This type of book keeping system is used by

usually small organisations which are not involved in much transactions.

Double entry book keeping system is a procedure according to which every entry is

recorded into two accounts out of each one of debit and one is credit. The basic agenda of double

entry system is to make sure that the balances of both the sides are equal. It is being considered

that every amount of one column impacts the amount of other column (Bushman, 2014). Instead

of two, there are three columns in this system which are transaction, debit amount and credit

amount.

Trial balance and its importance

Trial balance is developed using double entry book keepings system. Trial balance is a

statement which records balances of all ledger accounts and then entire statement is compiled

into two columns of debit and credit. An accurate and duly developed trial balance has balances

of both the sides equal.

Development of trial balance holds various points of importance for a business

transaction. The statement of trial balance is important as it provides the base for development of

income statement and balance sheet (Edwards, 2013). As this statement is developed using

double entry book keeping, it helps in analysing the arithmetical accuracy of the accounts. This

statement of trial balance is also important as it helps in rectifying the errors and helps in making

reliable decisions for the future strategies of the company.

Question 2: Financial analysis of Kate’s business

Journal entries

5

6

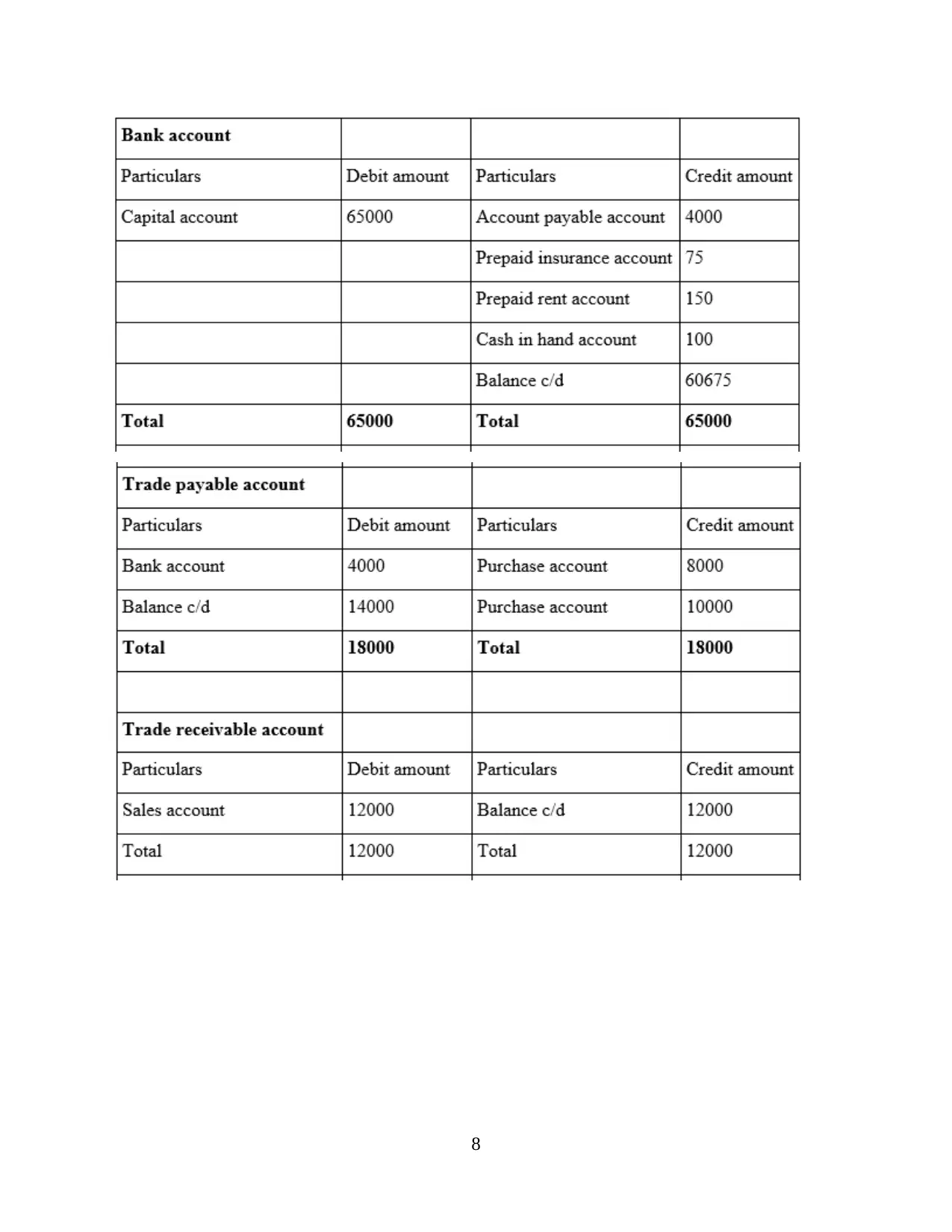

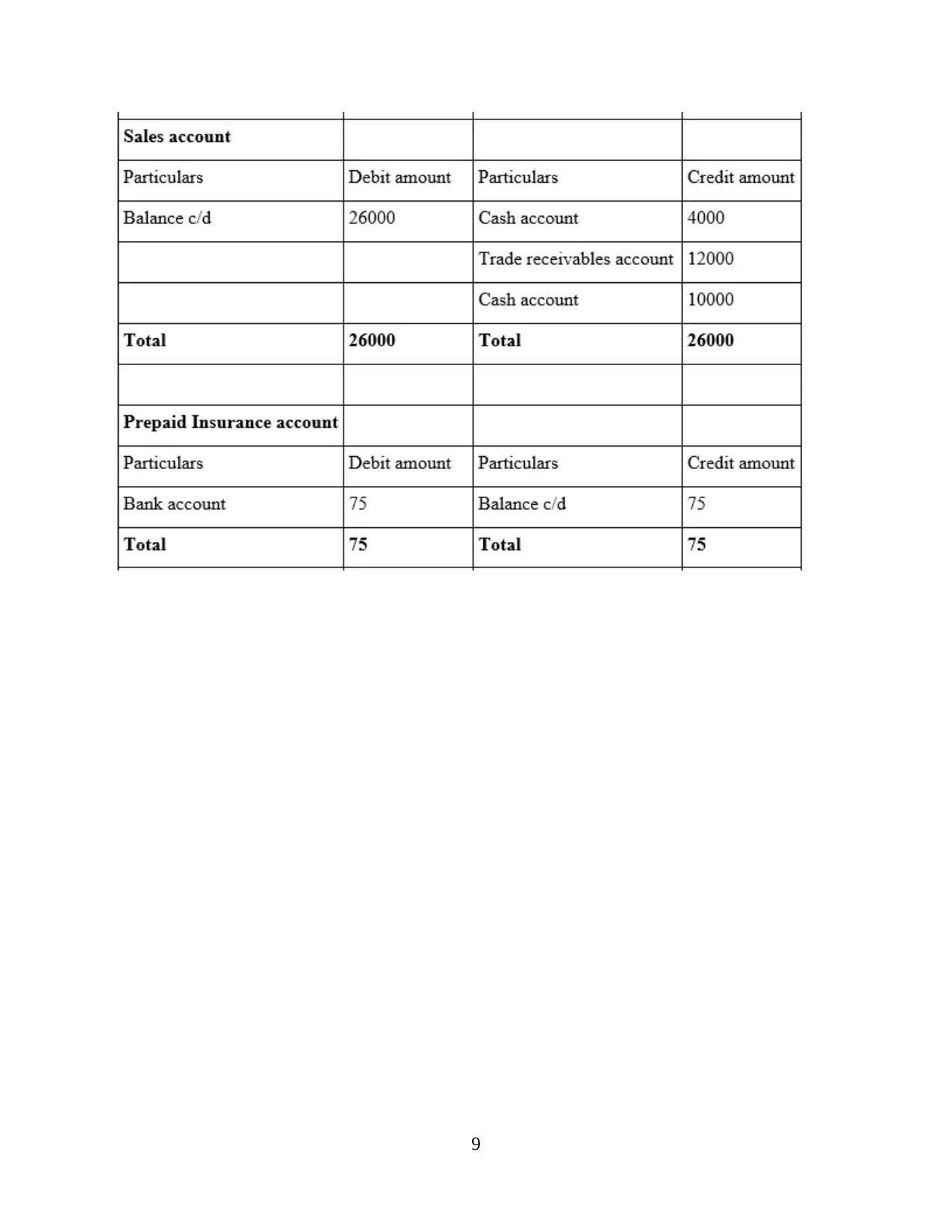

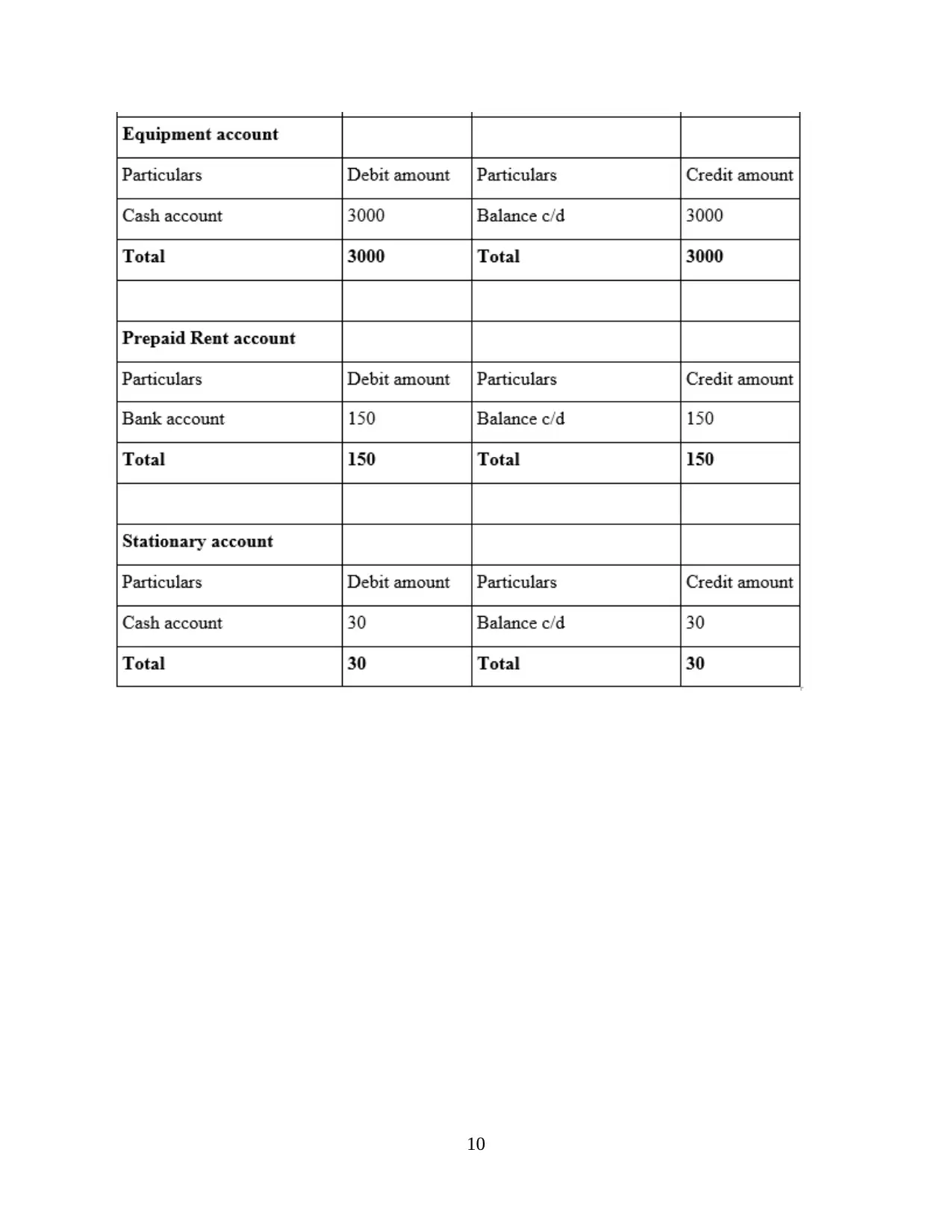

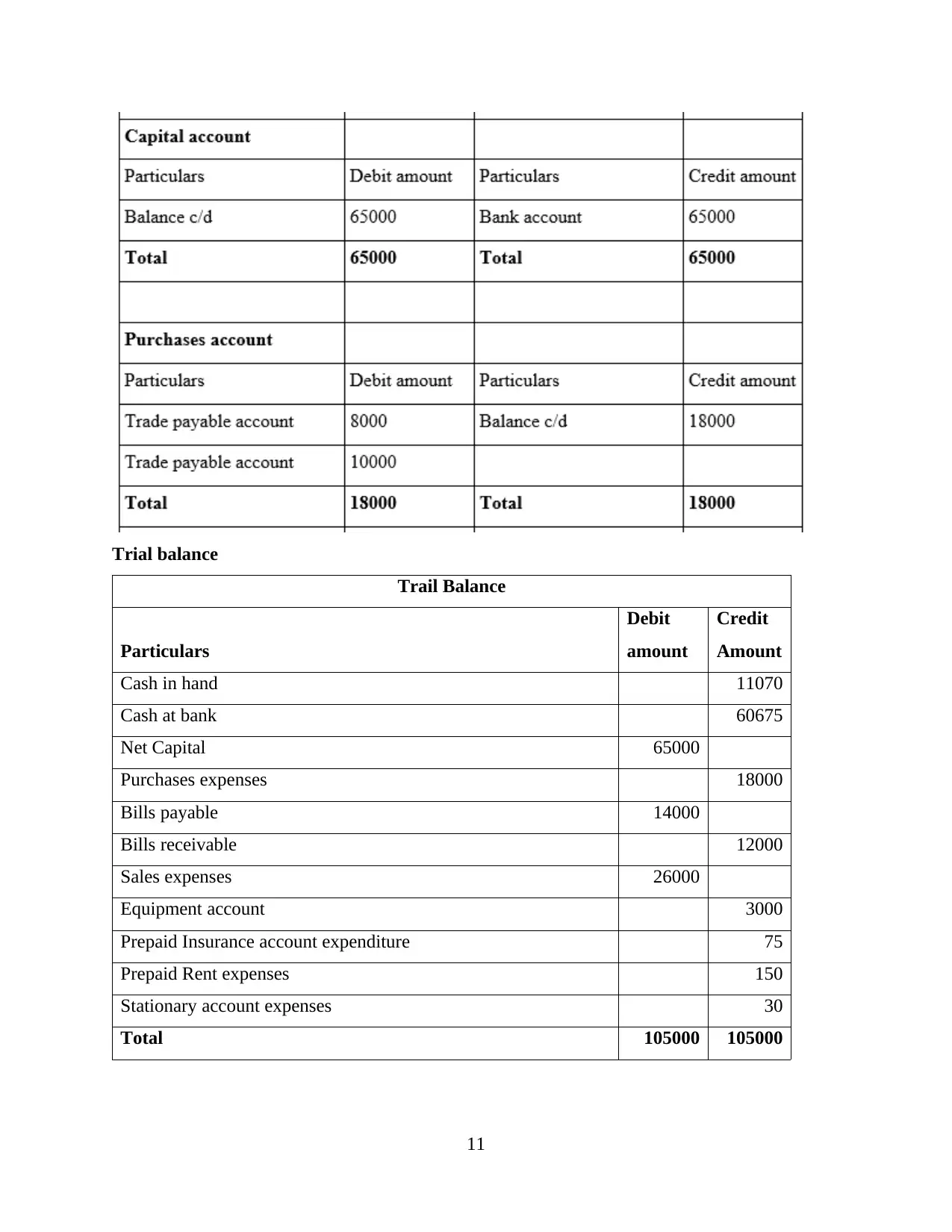

Ledger accounts

7

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Trial balance

Trail Balance

Particulars

Debit

amount

Credit

Amount

Cash in hand 11070

Cash at bank 60675

Net Capital 65000

Purchases expenses 18000

Bills payable 14000

Bills receivable 12000

Sales expenses 26000

Equipment account 3000

Prepaid Insurance account expenditure 75

Prepaid Rent expenses 150

Stationary account expenses 30

Total 105000 105000

11

Trail Balance

Particulars

Debit

amount

Credit

Amount

Cash in hand 11070

Cash at bank 60675

Net Capital 65000

Purchases expenses 18000

Bills payable 14000

Bills receivable 12000

Sales expenses 26000

Equipment account 3000

Prepaid Insurance account expenditure 75

Prepaid Rent expenses 150

Stationary account expenses 30

Total 105000 105000

11

Question 3: Difference between financial statement and financial report

Financial report and financial statements are both the documents of a business organisation

that they develop to summarise their business transactions and to develop a record that can

reflect the true and fair financial position of that organisation (Gassen, 2014). Both of these

documents holds different position in an organisation are have different users and requirements.

The comparative analysis between these documents are analysed below:

Basis of

distinction

Financial statement Financial report

Meaning A financial statement is a document

having monetary information of an

organisation which reflect either the

financial position, performance or cash

fluctuations in the company.

On the other hand, financial reports can

be any report associated with

organisation having monetary matters.

This type of organisational document is

prepared to communicate the internal

financial matters of an organisation to

external stakeholders of the company.

Scope All financial statements are financial

reports due to which scope of such

statements are narrower than financial

reports.

Financial reports have broader scope

than financial statements as these

reports includes financial as well as

managerial information.

Governance Financial statements are required to be

developed in a certain way so that a

uniformity can be maintained. These

certain ways are mentioned in

International Financial Reporting

Standards which levies a compulsion

on every organisation to develop

financial statements in a certain way.

On the other hand, financial reports are

developed using the regulations and

guidelines provided by International

Accounting Standards Board (Haskin

and Burke, 2016).

Needs and

Users

Financial statements have different

uses due to which it is utilised by its

various users:

Employees and managers are

Financial reports also have different

uses for its different users that are

identified below:

Board of directors are the

12

Financial report and financial statements are both the documents of a business organisation

that they develop to summarise their business transactions and to develop a record that can

reflect the true and fair financial position of that organisation (Gassen, 2014). Both of these

documents holds different position in an organisation are have different users and requirements.

The comparative analysis between these documents are analysed below:

Basis of

distinction

Financial statement Financial report

Meaning A financial statement is a document

having monetary information of an

organisation which reflect either the

financial position, performance or cash

fluctuations in the company.

On the other hand, financial reports can

be any report associated with

organisation having monetary matters.

This type of organisational document is

prepared to communicate the internal

financial matters of an organisation to

external stakeholders of the company.

Scope All financial statements are financial

reports due to which scope of such

statements are narrower than financial

reports.

Financial reports have broader scope

than financial statements as these

reports includes financial as well as

managerial information.

Governance Financial statements are required to be

developed in a certain way so that a

uniformity can be maintained. These

certain ways are mentioned in

International Financial Reporting

Standards which levies a compulsion

on every organisation to develop

financial statements in a certain way.

On the other hand, financial reports are

developed using the regulations and

guidelines provided by International

Accounting Standards Board (Haskin

and Burke, 2016).

Needs and

Users

Financial statements have different

uses due to which it is utilised by its

various users:

Employees and managers are

Financial reports also have different

uses for its different users that are

identified below:

Board of directors are the

12

the internal users of financial

statement who use these

documents to analyse the

financial position of the

company in market and the

expenses value so that they can

identify the chances of their

wage rate.

Investors – Investors are the

users who uses the financial

statements to identify the return

rate of the company in order to

decide that whether a company

is worth investing or not.

internal users of financial

reports who uses it to develop

strategies for future

development of the

organisation. BODs analyse the

financial situation of the

company and then make plans

to resolve present issues.

Government – Authorised

parties of the government uses

financial report of an

organisation to identify their

taxable income and analyse the

notes of financial statements

which are recorded in the

financial report (Kaya and

Akbulut, 2018).

Examples There are usually five financial

statements including:

Income statement

Balance sheet

Cash flow statement

Changes in equity statement

Comprehensive income

statement

There are various examples of financial

reports including:

Debtor’s report

Account receivables ageing

report etc.

Question 4: Fundamental principles of accounting

Fundamental principles are the specific rules and standards which are given by authorised

authorities to the business organisations which are mandatory to be followed. The fundamental

accounting principles are the guidelines which helps an organisation to maintain a uniformity in

13

statement who use these

documents to analyse the

financial position of the

company in market and the

expenses value so that they can

identify the chances of their

wage rate.

Investors – Investors are the

users who uses the financial

statements to identify the return

rate of the company in order to

decide that whether a company

is worth investing or not.

internal users of financial

reports who uses it to develop

strategies for future

development of the

organisation. BODs analyse the

financial situation of the

company and then make plans

to resolve present issues.

Government – Authorised

parties of the government uses

financial report of an

organisation to identify their

taxable income and analyse the

notes of financial statements

which are recorded in the

financial report (Kaya and

Akbulut, 2018).

Examples There are usually five financial

statements including:

Income statement

Balance sheet

Cash flow statement

Changes in equity statement

Comprehensive income

statement

There are various examples of financial

reports including:

Debtor’s report

Account receivables ageing

report etc.

Question 4: Fundamental principles of accounting

Fundamental principles are the specific rules and standards which are given by authorised

authorities to the business organisations which are mandatory to be followed. The fundamental

accounting principles are the guidelines which helps an organisation to maintain a uniformity in

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their reports (Phillips, Libby and Libby, 2011). Some of these principles are identified and

analysed below:

Revenue recognition principle – Revenue is the money that has been earned by an

organisation through the way of sales. According to this principle of accounting, an organisation

must only record a transaction resulting in revenue when it has been earned. This principle aims

to recognise revenue only when it has been earned and not when it is being intimated.

Full disclosure principle – Under this fundamental principle, every organisation has to

follow a rule of disclosing each and every information of their organisation. Every company has

a compulsion to disclose their financial statements along with notes of financial statement in

public in order to ensure that their true and fair financial position represented to their

stakeholders.

Principle of prudence – This fundamental accounting principle is based on the conservative

theory under which an organisation must record their expenses and liabilities as soon as they are

intimated but that organisation must only record their revenues and gains when these are earned

and received (Porter and Norton, 2012).

Matching principle – This particular fundamental accounting principle states that every

organisation must develop their financial statements using double entry book keeping system and

the both the sides of their balance sheet must be matched by having a same balance on debit and

credit side. This principle is developed to ensure that assets of an organisation are equal to the

equity and liabilities of that organisation.

Cost principle – It is another essential fundamental accounting principle to understand

under which an organisation records their assets with the amount which is historically paid by

them and as the asset gains or losses its value, the cost of that assets is not modified. This

principle also includes depreciation to depreciate the value of assets as their value cannot be

modified in accounts.

Monetary unit principle – According to this accounting principle, all the monetary values

in a financial statement and report must be recorded using a uniform monetary unit. The currency

value or monetary value cannot be changed in between of the financial statements (Porter, 2019).

All the principles which are discussed above are mandatory for an organisation to be

follow in order to develop effective financial reports.

14

analysed below:

Revenue recognition principle – Revenue is the money that has been earned by an

organisation through the way of sales. According to this principle of accounting, an organisation

must only record a transaction resulting in revenue when it has been earned. This principle aims

to recognise revenue only when it has been earned and not when it is being intimated.

Full disclosure principle – Under this fundamental principle, every organisation has to

follow a rule of disclosing each and every information of their organisation. Every company has

a compulsion to disclose their financial statements along with notes of financial statement in

public in order to ensure that their true and fair financial position represented to their

stakeholders.

Principle of prudence – This fundamental accounting principle is based on the conservative

theory under which an organisation must record their expenses and liabilities as soon as they are

intimated but that organisation must only record their revenues and gains when these are earned

and received (Porter and Norton, 2012).

Matching principle – This particular fundamental accounting principle states that every

organisation must develop their financial statements using double entry book keeping system and

the both the sides of their balance sheet must be matched by having a same balance on debit and

credit side. This principle is developed to ensure that assets of an organisation are equal to the

equity and liabilities of that organisation.

Cost principle – It is another essential fundamental accounting principle to understand

under which an organisation records their assets with the amount which is historically paid by

them and as the asset gains or losses its value, the cost of that assets is not modified. This

principle also includes depreciation to depreciate the value of assets as their value cannot be

modified in accounts.

Monetary unit principle – According to this accounting principle, all the monetary values

in a financial statement and report must be recorded using a uniform monetary unit. The currency

value or monetary value cannot be changed in between of the financial statements (Porter, 2019).

All the principles which are discussed above are mandatory for an organisation to be

follow in order to develop effective financial reports.

14

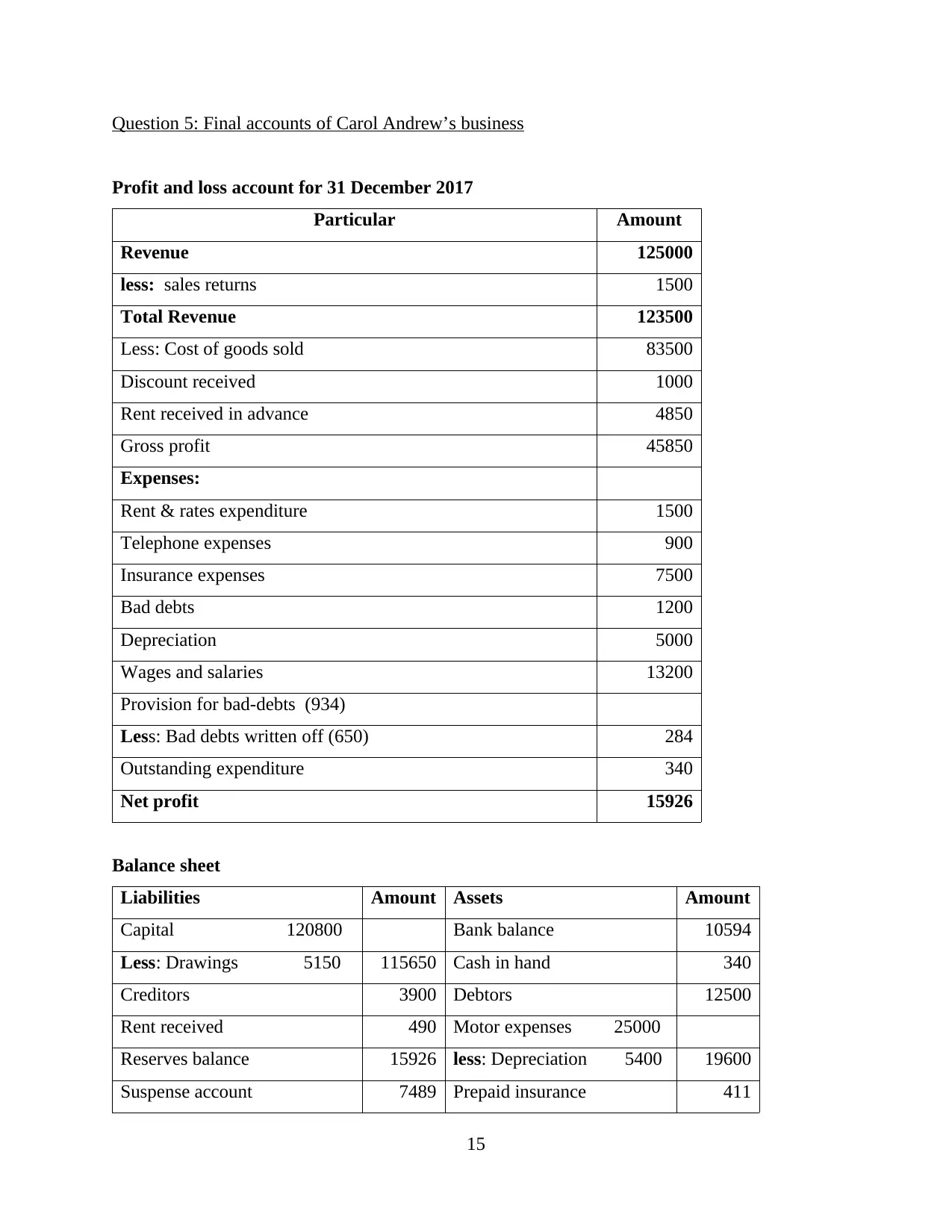

Question 5: Final accounts of Carol Andrew’s business

Profit and loss account for 31 December 2017

Particular Amount

Revenue 125000

less: sales returns 1500

Total Revenue 123500

Less: Cost of goods sold 83500

Discount received 1000

Rent received in advance 4850

Gross profit 45850

Expenses:

Rent & rates expenditure 1500

Telephone expenses 900

Insurance expenses 7500

Bad debts 1200

Depreciation 5000

Wages and salaries 13200

Provision for bad-debts (934)

Less: Bad debts written off (650) 284

Outstanding expenditure 340

Net profit 15926

Balance sheet

Liabilities Amount Assets Amount

Capital 120800 Bank balance 10594

Less: Drawings 5150 115650 Cash in hand 340

Creditors 3900 Debtors 12500

Rent received 490 Motor expenses 25000

Reserves balance 15926 less: Depreciation 5400 19600

Suspense account 7489 Prepaid insurance 411

15

Profit and loss account for 31 December 2017

Particular Amount

Revenue 125000

less: sales returns 1500

Total Revenue 123500

Less: Cost of goods sold 83500

Discount received 1000

Rent received in advance 4850

Gross profit 45850

Expenses:

Rent & rates expenditure 1500

Telephone expenses 900

Insurance expenses 7500

Bad debts 1200

Depreciation 5000

Wages and salaries 13200

Provision for bad-debts (934)

Less: Bad debts written off (650) 284

Outstanding expenditure 340

Net profit 15926

Balance sheet

Liabilities Amount Assets Amount

Capital 120800 Bank balance 10594

Less: Drawings 5150 115650 Cash in hand 340

Creditors 3900 Debtors 12500

Rent received 490 Motor expenses 25000

Reserves balance 15926 less: Depreciation 5400 19600

Suspense account 7489 Prepaid insurance 411

15

Loan provided 100000

143455 143445

SCENARIO 2

Question 1: Bank reconciliation

Meaning of bank reconciliation

Bank reconciliation is a procedure in which closing amount of bank statement developed

by bank and cash statement developed by the organisation is reconciled when the closing balance

of both the statements do not match. There are various reasons due to which balances of these

two statements do not match and this situation is quite usual; this typicality of this situation

triggers the importance of bank reconciliation. An organisation carries the process of bank

reconciliation by developing a bank reconciliation statement.

Requirement of bank reconciliation

There are various requirements due to which the procedure of bank reconciliation is

performed by an organisation; some of these requirements are analysed below:

The procedure of bank reconciliation is required to be performed as it helps in ensuring

that records of the company including cash register and balance sheet are effectively

prepared by comparing them to the bank statement prepared by bank.

This procedure is required as it ensures the arithmetical accuracy of an organisation in

their financial statements that represents the true and fair performance and position of the

company (Schroeder, Clark and Cathey, 2019).

Achievement of bank reconciliation

Bank reconciliation is a state where the balances of cash book and bank statement are

same. In order to achieve this situation, it is important for an organisation to follow a procedure

having following steps:

The first step in the procedure of reconciling the bank and cash books is to compare the

deposits. In this step, an organisation must match the deposits of the bank statement with

the records of business and in case of any deviation, that amount must be added or

deducted in the company records.

16

143455 143445

SCENARIO 2

Question 1: Bank reconciliation

Meaning of bank reconciliation

Bank reconciliation is a procedure in which closing amount of bank statement developed

by bank and cash statement developed by the organisation is reconciled when the closing balance

of both the statements do not match. There are various reasons due to which balances of these

two statements do not match and this situation is quite usual; this typicality of this situation

triggers the importance of bank reconciliation. An organisation carries the process of bank

reconciliation by developing a bank reconciliation statement.

Requirement of bank reconciliation

There are various requirements due to which the procedure of bank reconciliation is

performed by an organisation; some of these requirements are analysed below:

The procedure of bank reconciliation is required to be performed as it helps in ensuring

that records of the company including cash register and balance sheet are effectively

prepared by comparing them to the bank statement prepared by bank.

This procedure is required as it ensures the arithmetical accuracy of an organisation in

their financial statements that represents the true and fair performance and position of the

company (Schroeder, Clark and Cathey, 2019).

Achievement of bank reconciliation

Bank reconciliation is a state where the balances of cash book and bank statement are

same. In order to achieve this situation, it is important for an organisation to follow a procedure

having following steps:

The first step in the procedure of reconciling the bank and cash books is to compare the

deposits. In this step, an organisation must match the deposits of the bank statement with

the records of business and in case of any deviation, that amount must be added or

deducted in the company records.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Another step in this procedure is not adjust the bank statements by adding the amounts of

deposits which are in transit and yet to be transferred. Along with this, amount for

outstanding cheques must be deducted along with the amount wrongly charged due to

bank’s mistake.

Once the bank statement is adjusted, it is time to adjust the cash account of the company.

In this step, the charges charged by bank for bank overdraft or bank fee are added in the

cash account. Along with this, errors in accounting by the organisation’s accounts are

deducted to reconcile the statement.

Lastly, the balances of both the accounts are once again compared to ensure that there is

no deviation between bank statement and cash account is left.

By following the above procedure, the bank reconciliation can be achieved.

Reasons due to which bank reconciliation is necessary

There are various reasons due to which bank statement and cash account do not reconcile

and these are the reasons due to which bank reconciliation is necessary. Some of these reasons

are identified and analysed below:

If an organisation is expecting a payment and they record it in their cash book but as the

payment was in transit, it is not yet recorded in bank statement. This situation results into

non agreement of both the accounts and in order ensure same balance in both the

accounts, the bank reconciliation procedure is necessary (Thornton, 2018).

When a bank charges their service fee without intimating the organisation then the

balance of bank statement reflects lower balance than the cash account. For resolving this

situation, the procedure of bank reconciliation is necessary.

In a situation when an organisation receives a payment from their customer in a form of

cheque they record that received amount in their cash book but due to not having

sufficient funds in the account of customer, bank does not process the payment and this

results in deviation between both the accounts. In order to eliminate and resolve this

deviation, the bank reconciliation is necessary.

Question 2: Control accounts

Meaning of control accounts

Control accounts are a distinctive type of account as even they are developed under

general ledger; it is not related with subsidiary ledger account. The main purpose of developing a

17

deposits which are in transit and yet to be transferred. Along with this, amount for

outstanding cheques must be deducted along with the amount wrongly charged due to

bank’s mistake.

Once the bank statement is adjusted, it is time to adjust the cash account of the company.

In this step, the charges charged by bank for bank overdraft or bank fee are added in the

cash account. Along with this, errors in accounting by the organisation’s accounts are

deducted to reconcile the statement.

Lastly, the balances of both the accounts are once again compared to ensure that there is

no deviation between bank statement and cash account is left.

By following the above procedure, the bank reconciliation can be achieved.

Reasons due to which bank reconciliation is necessary

There are various reasons due to which bank statement and cash account do not reconcile

and these are the reasons due to which bank reconciliation is necessary. Some of these reasons

are identified and analysed below:

If an organisation is expecting a payment and they record it in their cash book but as the

payment was in transit, it is not yet recorded in bank statement. This situation results into

non agreement of both the accounts and in order ensure same balance in both the

accounts, the bank reconciliation procedure is necessary (Thornton, 2018).

When a bank charges their service fee without intimating the organisation then the

balance of bank statement reflects lower balance than the cash account. For resolving this

situation, the procedure of bank reconciliation is necessary.

In a situation when an organisation receives a payment from their customer in a form of

cheque they record that received amount in their cash book but due to not having

sufficient funds in the account of customer, bank does not process the payment and this

results in deviation between both the accounts. In order to eliminate and resolve this

deviation, the bank reconciliation is necessary.

Question 2: Control accounts

Meaning of control accounts

Control accounts are a distinctive type of account as even they are developed under

general ledger; it is not related with subsidiary ledger account. The main purpose of developing a

17

control account is to keep the general ledger free from details so that chaos can be eliminated and

accounts can be accurate.

Explaining the role of control accounts in financial management

Control accounts plays various roles and has significant importance under financial

management which are analysed below:

Control accounts holds a temporary place for cost of different accounts so that they can

managed effectively and can be recorded in financial statements.

It plays a role of the summary account in which balances of the accounts are recorded for

only a temporary point of time.

Question 3: Suspense account

Meaning of suspense account

A suspense account is also a general ledger account like control account which is

developed for a particular time period only but the objectives due to which suspense account is

developed is different than the control accounts. The suspense account is a section of general

ledger where accountant records a transaction for temporary period till the exact position or

source of that amount is not identified. After the source of amount is been identified, the amount

of suspense account is moved to proper account. In a situation where transaction is not

completed but the source of that transaction is yet not clear then instead of recording it in

incorrect account, the transaction is recorded under suspense account until the correct source is

identified.

Reasons for drafting suspense accounts

For an organisation, there are few reasons due to which it is important to draft a suspense

account and these reasons are:

A suspense account under trial balance statement is opened or drafted when the balance

of two sides of trail balance which are debit and credit are not matched. If the balance

amount of debit side of trail balance is higher than the credit side, then a suspense

account is drafted to credit side to match the trail balance. The reason behind drafting the

suspense account is to continue the procedure of developing financial statement as

whenever the source of that suspense account amount will be identified, the trial balance

will be rectified (Zhang, Low and Seow, 2020).

18

accounts can be accurate.

Explaining the role of control accounts in financial management

Control accounts plays various roles and has significant importance under financial

management which are analysed below:

Control accounts holds a temporary place for cost of different accounts so that they can

managed effectively and can be recorded in financial statements.

It plays a role of the summary account in which balances of the accounts are recorded for

only a temporary point of time.

Question 3: Suspense account

Meaning of suspense account

A suspense account is also a general ledger account like control account which is

developed for a particular time period only but the objectives due to which suspense account is

developed is different than the control accounts. The suspense account is a section of general

ledger where accountant records a transaction for temporary period till the exact position or

source of that amount is not identified. After the source of amount is been identified, the amount

of suspense account is moved to proper account. In a situation where transaction is not

completed but the source of that transaction is yet not clear then instead of recording it in

incorrect account, the transaction is recorded under suspense account until the correct source is

identified.

Reasons for drafting suspense accounts

For an organisation, there are few reasons due to which it is important to draft a suspense

account and these reasons are:

A suspense account under trial balance statement is opened or drafted when the balance

of two sides of trail balance which are debit and credit are not matched. If the balance

amount of debit side of trail balance is higher than the credit side, then a suspense

account is drafted to credit side to match the trail balance. The reason behind drafting the

suspense account is to continue the procedure of developing financial statement as

whenever the source of that suspense account amount will be identified, the trial balance

will be rectified (Zhang, Low and Seow, 2020).

18

A suspense account under received payments are drafted when in the chaos of multiple

invoices, accountant is unable to find an invoice for a particular amount. In order to

ensure that the procedure of accounting is not delayed or comprised, a suspense account

is opened and when the invoice is traced the suspense account is then closed.

A suspense account under paid payments is drafted when accountant is unsure that to

which party a particular payment is made and the receipt is unable to traced. In such a

scenario, a suspense account is drafted but only for a temporary period of time. Under

payments account, a suspense account is also drafted when a partial payment is made

against an equipment but the name of the fixed assets will only be known when the

payment is completely done so for the time in between, the suspense account is drafted.

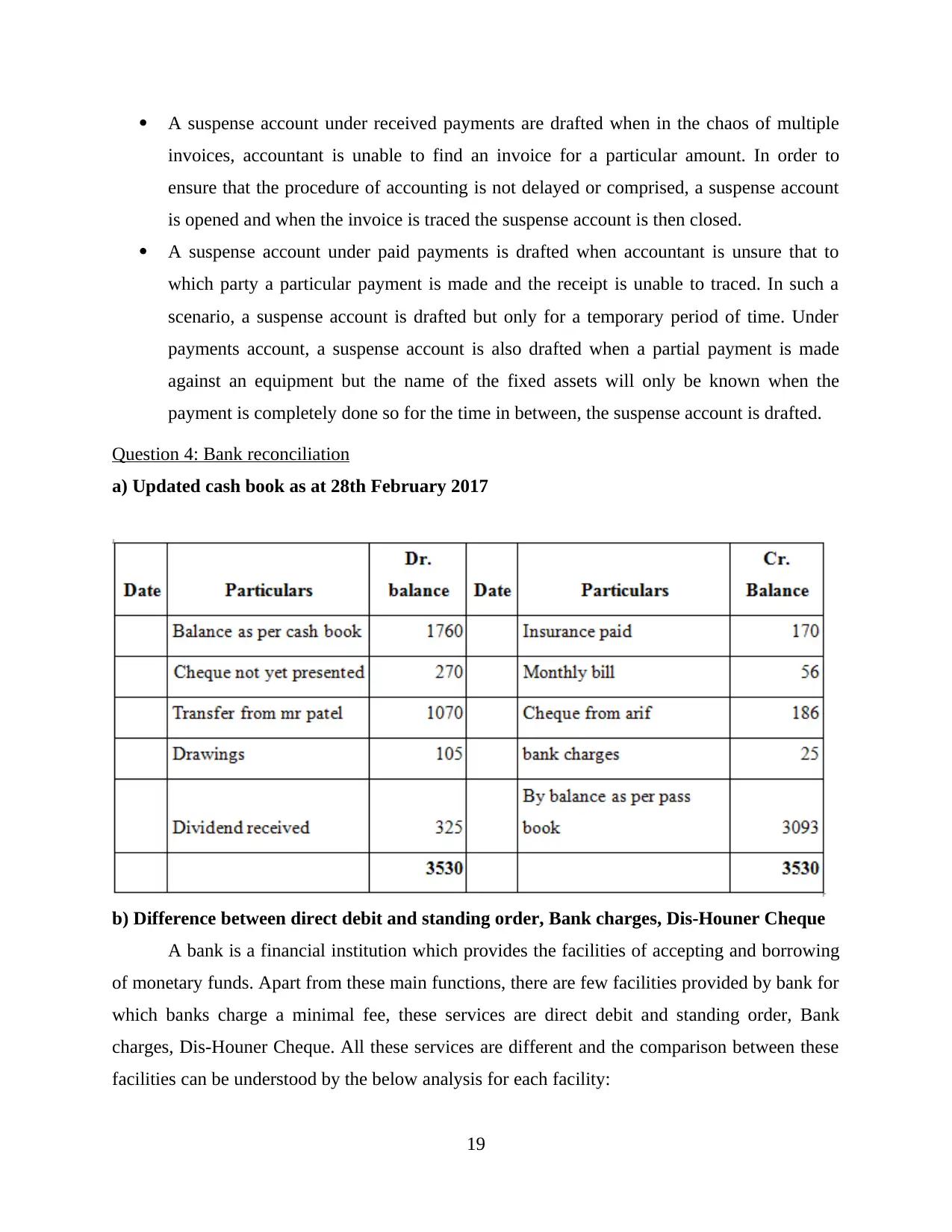

Question 4: Bank reconciliation

a) Updated cash book as at 28th February 2017

b) Difference between direct debit and standing order, Bank charges, Dis-Houner Cheque

A bank is a financial institution which provides the facilities of accepting and borrowing

of monetary funds. Apart from these main functions, there are few facilities provided by bank for

which banks charge a minimal fee, these services are direct debit and standing order, Bank

charges, Dis-Houner Cheque. All these services are different and the comparison between these

facilities can be understood by the below analysis for each facility:

19

invoices, accountant is unable to find an invoice for a particular amount. In order to

ensure that the procedure of accounting is not delayed or comprised, a suspense account

is opened and when the invoice is traced the suspense account is then closed.

A suspense account under paid payments is drafted when accountant is unsure that to

which party a particular payment is made and the receipt is unable to traced. In such a

scenario, a suspense account is drafted but only for a temporary period of time. Under

payments account, a suspense account is also drafted when a partial payment is made

against an equipment but the name of the fixed assets will only be known when the

payment is completely done so for the time in between, the suspense account is drafted.

Question 4: Bank reconciliation

a) Updated cash book as at 28th February 2017

b) Difference between direct debit and standing order, Bank charges, Dis-Houner Cheque

A bank is a financial institution which provides the facilities of accepting and borrowing

of monetary funds. Apart from these main functions, there are few facilities provided by bank for

which banks charge a minimal fee, these services are direct debit and standing order, Bank

charges, Dis-Houner Cheque. All these services are different and the comparison between these

facilities can be understood by the below analysis for each facility:

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct debit

The facility of direct debit is the convenience which provided by the banks to their

clients. Under this facility, client can provide direct order to their bank to access their account

amount and pay to a party at a specific time and date. Bank has the leverage to pay the extend of

the amount which has due at the account of client. The examples of this facility includes

electricity, gas and many more. It is not important that the intervals between these payments is

equal. In direct order, client provides the leverage to their bank to pay a specific utility bill

whenever it becomes due of any amount. Client has to pay a considerable amount of fee against

using this facility.

Standing order

This facility of standing order is similar to the facility of direct debit as in this facility as

well client can order their bank to make a payment on their behalf. The only difference between

standing order and direct debit is that standing order only allows to make a payment at a regular

interval of a specific amount. The examples of this payment includes loan instalments and other

EMIs that client can order to pay to their bank. For this facility as well client has to pay a

negligible amount of fee.

Bank charges

The concept of bank charge is more of a charge than a facility which bank charges from

their client against the services provided. This bank charge is deducted at a certain interval

without any intimation but the deduction from bank account is reflected in the bank statement.

This fee which is charged by bank is charged against the facilities of cheque books, ATM

leverage and more. It is mandatory for every client to pay a bank charge against the services

provided by the bank (Zhang, Low and Seow, 2020).

Dis-Houner Cheque

A dis honour cheque is more of a penalty than a charge or facility levied by a bank. When

a client issues a cheque of self or to a party but at the time of processing of that cheque, there is

no enough funds in the bank account of customer then a penalty of dis honour cheque has to be

paid by the client against the trouble that bank has to go through while processing the cheque. A

cheque can also be dis honoured due to overwriting or incorrect details filled by the client.

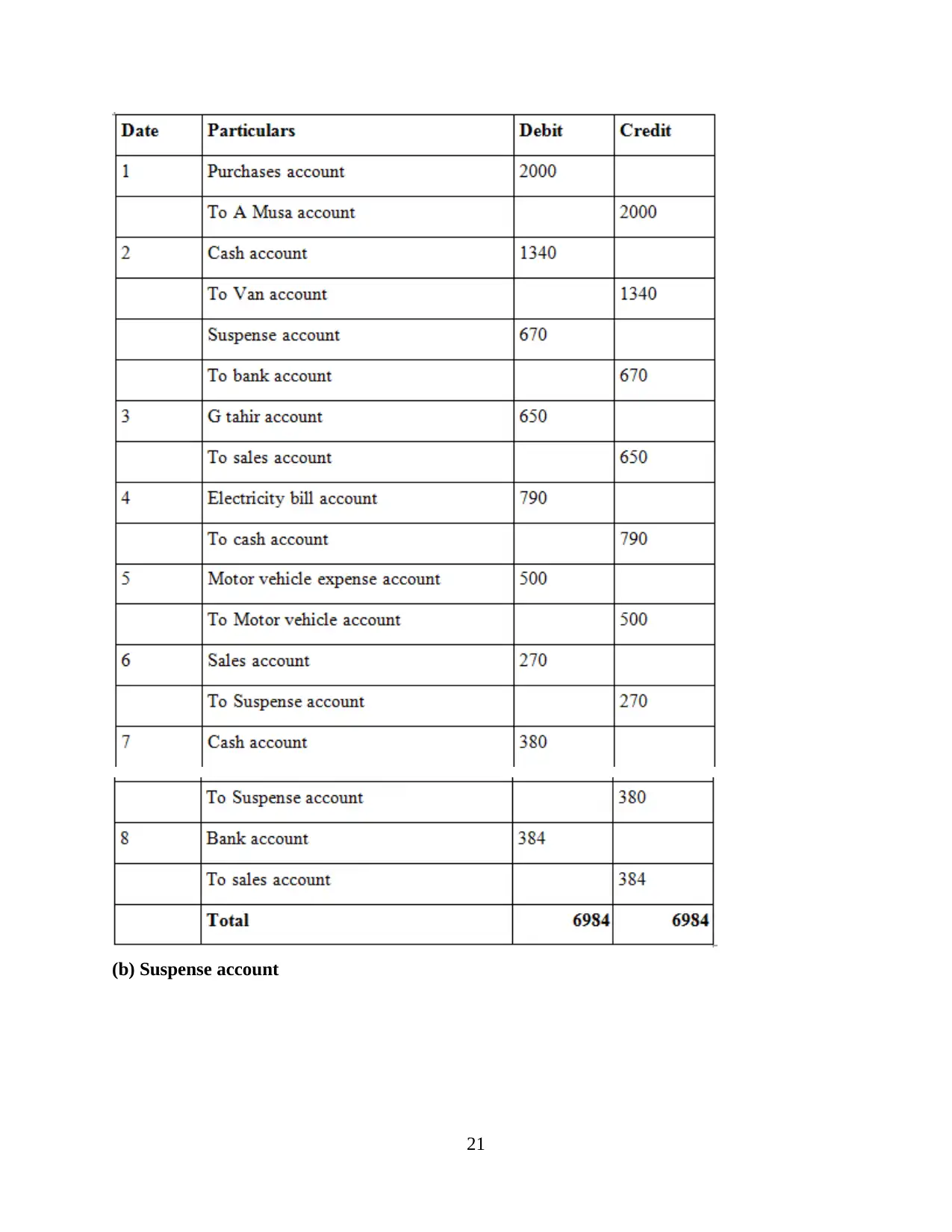

Question 5

(a) Journal entries

20

The facility of direct debit is the convenience which provided by the banks to their

clients. Under this facility, client can provide direct order to their bank to access their account

amount and pay to a party at a specific time and date. Bank has the leverage to pay the extend of

the amount which has due at the account of client. The examples of this facility includes

electricity, gas and many more. It is not important that the intervals between these payments is

equal. In direct order, client provides the leverage to their bank to pay a specific utility bill

whenever it becomes due of any amount. Client has to pay a considerable amount of fee against

using this facility.

Standing order

This facility of standing order is similar to the facility of direct debit as in this facility as

well client can order their bank to make a payment on their behalf. The only difference between

standing order and direct debit is that standing order only allows to make a payment at a regular

interval of a specific amount. The examples of this payment includes loan instalments and other

EMIs that client can order to pay to their bank. For this facility as well client has to pay a

negligible amount of fee.

Bank charges

The concept of bank charge is more of a charge than a facility which bank charges from

their client against the services provided. This bank charge is deducted at a certain interval

without any intimation but the deduction from bank account is reflected in the bank statement.

This fee which is charged by bank is charged against the facilities of cheque books, ATM

leverage and more. It is mandatory for every client to pay a bank charge against the services

provided by the bank (Zhang, Low and Seow, 2020).

Dis-Houner Cheque

A dis honour cheque is more of a penalty than a charge or facility levied by a bank. When

a client issues a cheque of self or to a party but at the time of processing of that cheque, there is

no enough funds in the bank account of customer then a penalty of dis honour cheque has to be

paid by the client against the trouble that bank has to go through while processing the cheque. A

cheque can also be dis honoured due to overwriting or incorrect details filled by the client.

Question 5

(a) Journal entries

20

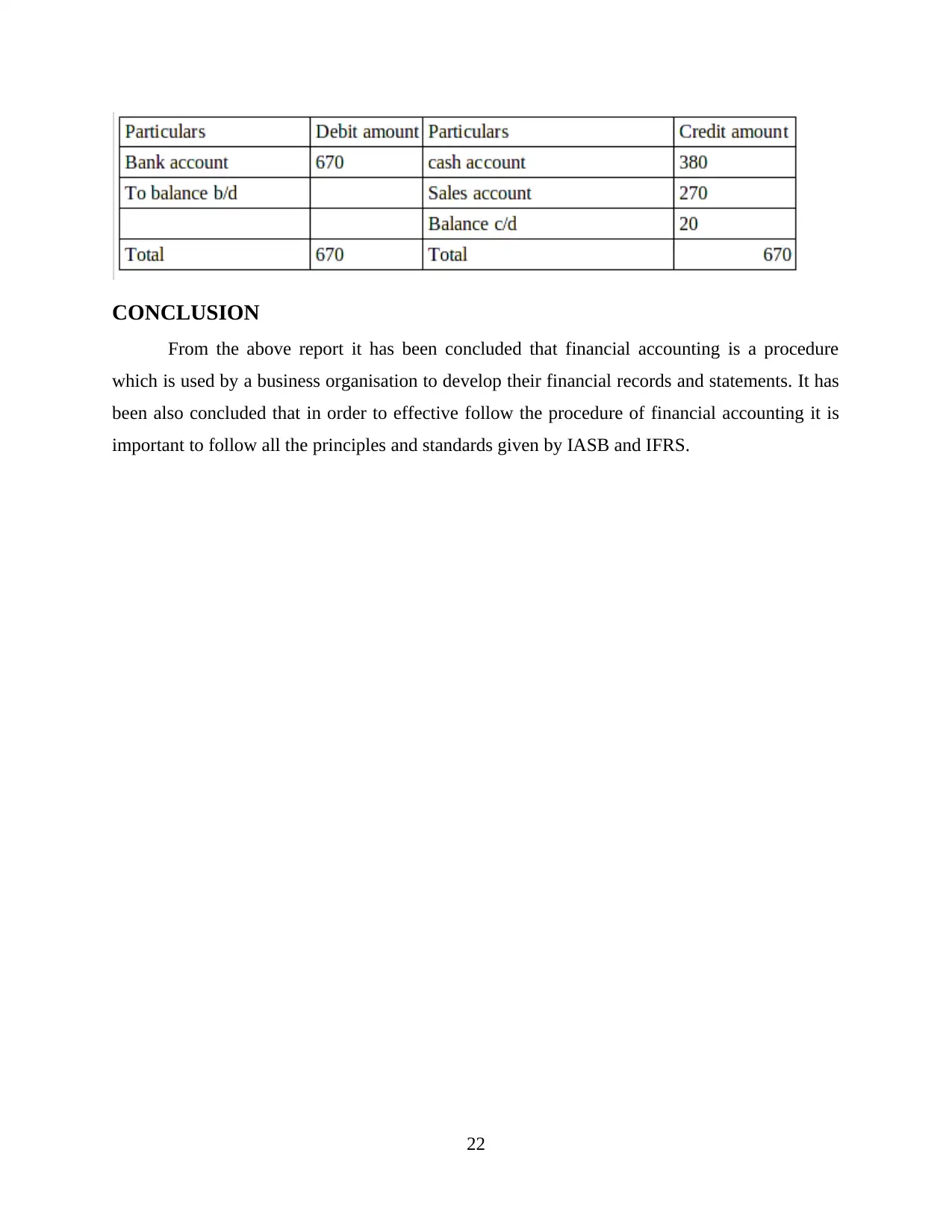

(b) Suspense account

21

21

CONCLUSION

From the above report it has been concluded that financial accounting is a procedure

which is used by a business organisation to develop their financial records and statements. It has

been also concluded that in order to effective follow the procedure of financial accounting it is

important to follow all the principles and standards given by IASB and IFRS.

22

From the above report it has been concluded that financial accounting is a procedure

which is used by a business organisation to develop their financial records and statements. It has

been also concluded that in order to effective follow the procedure of financial accounting it is

important to follow all the principles and standards given by IASB and IFRS.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Balakrishnan, K. and Cohen, D.A., 2013. Competition and financial accounting

misreporting. Available at SSRN 1927427.

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus. 51(4). pp.499-510.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics. 58(2-3). pp.384-395.

Edwards, J.R. ed., 2013. A history of financial accounting (RLE Accounting). Routledge.

Gassen, J., 2014. Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society. 39(7). pp.535-544.

Haskin, D.L. and Burke, M.M., 2016. Incorporating sustainability issues into the financial

accounting curriculum. American Journal of Business Education (AJBE). 9(2). pp.49-56.

Kaya, I. and Akbulut, D.H., 2018. Big data analytics in financial reporting and

accounting. PressAcademia Procedia. 7(1). pp.256-259.

Phillips, F., Libby, R. and Libby, P.A., 2011. Fundamentals of Financial Accounting. New York,

NY: McGraw-Hill Irwin.

Porter, G.A. and Norton, C.L., 2012. Financial accounting: The impact on decision makers.

Cengage Learning.

Porter, J.C., 2019. Beyond debits and credits: Using integrated projects to improve students’

understanding of financial accounting. Journal of Accounting Education. 46. pp.53-71.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Thornton, S.C., 2018. A Collection of Case Studies on Financial Accounting Concepts.

Zhang, T., Low, L.C. and Seow, P.S., 2020. Using online tutorials to teach the accounting

cycle. Journal of Education for Business. 95(4). pp.263-274.

23

Books and Journals

Balakrishnan, K. and Cohen, D.A., 2013. Competition and financial accounting

misreporting. Available at SSRN 1927427.

Barth, M.E., 2015. Financial accounting research, practice, and financial

accountability. Abacus. 51(4). pp.499-510.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics. 58(2-3). pp.339-383.

Bushman, R.M., 2014. Thoughts on financial accounting and the banking industry. Journal of

Accounting and Economics. 58(2-3). pp.384-395.

Edwards, J.R. ed., 2013. A history of financial accounting (RLE Accounting). Routledge.

Gassen, J., 2014. Causal inference in empirical archival financial accounting

research. Accounting, Organizations and Society. 39(7). pp.535-544.

Haskin, D.L. and Burke, M.M., 2016. Incorporating sustainability issues into the financial

accounting curriculum. American Journal of Business Education (AJBE). 9(2). pp.49-56.

Kaya, I. and Akbulut, D.H., 2018. Big data analytics in financial reporting and

accounting. PressAcademia Procedia. 7(1). pp.256-259.

Phillips, F., Libby, R. and Libby, P.A., 2011. Fundamentals of Financial Accounting. New York,

NY: McGraw-Hill Irwin.

Porter, G.A. and Norton, C.L., 2012. Financial accounting: The impact on decision makers.

Cengage Learning.

Porter, J.C., 2019. Beyond debits and credits: Using integrated projects to improve students’

understanding of financial accounting. Journal of Accounting Education. 46. pp.53-71.

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Thornton, S.C., 2018. A Collection of Case Studies on Financial Accounting Concepts.

Zhang, T., Low, L.C. and Seow, P.S., 2020. Using online tutorials to teach the accounting

cycle. Journal of Education for Business. 95(4). pp.263-274.

23

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.