Financial Accounting: Provisions, Contingent Liabilities, and Contingent Assets

VerifiedAdded on 2023/01/04

|11

|1388

|41

AI Summary

This document discusses the appropriate accounting treatment for provisions, contingent liabilities, and contingent assets in financial accounting. It also provides examples of note disclosures and journal entries for financial statements. The document covers topics such as Australian Accounting Standard 137, provisions, contingent liabilities, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Question 1........................................................................................................................................3

i) Appropriate Accounting treatment...........................................................................................3

ii) Note Disclosures and Journal Entries for the financial statement ended on 2018 in each

situation........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................7

Question 5........................................................................................................................................9

References......................................................................................................................................11

Question 1........................................................................................................................................3

i) Appropriate Accounting treatment...........................................................................................3

ii) Note Disclosures and Journal Entries for the financial statement ended on 2018 in each

situation........................................................................................................................................3

Question 2........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................7

Question 5........................................................................................................................................9

References......................................................................................................................................11

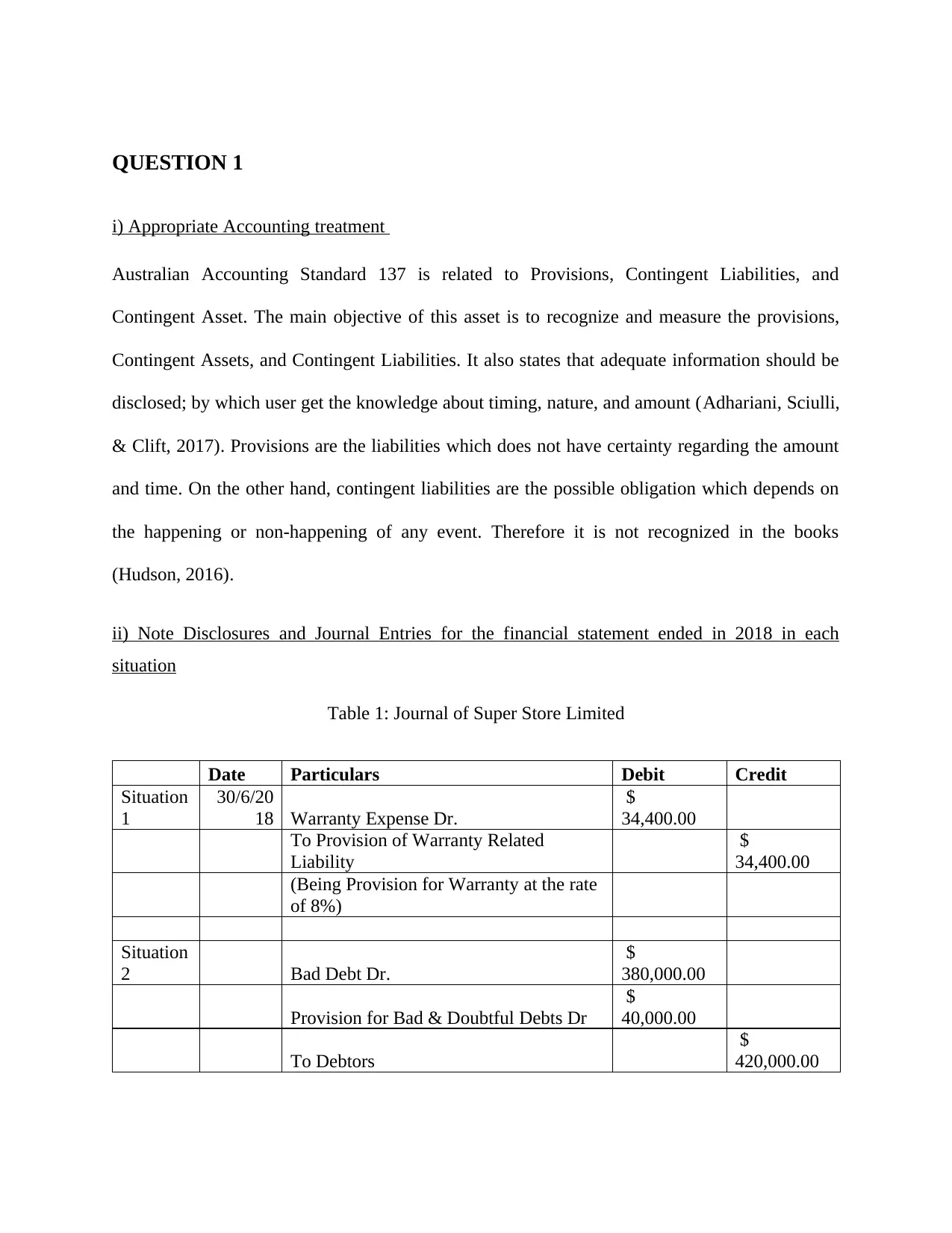

QUESTION 1

i) Appropriate Accounting treatment

Australian Accounting Standard 137 is related to Provisions, Contingent Liabilities, and

Contingent Asset. The main objective of this asset is to recognize and measure the provisions,

Contingent Assets, and Contingent Liabilities. It also states that adequate information should be

disclosed; by which user get the knowledge about timing, nature, and amount (Adhariani, Sciulli,

& Clift, 2017). Provisions are the liabilities which does not have certainty regarding the amount

and time. On the other hand, contingent liabilities are the possible obligation which depends on

the happening or non-happening of any event. Therefore it is not recognized in the books

(Hudson, 2016).

ii) Note Disclosures and Journal Entries for the financial statement ended in 2018 in each

situation

Table 1: Journal of Super Store Limited

Date Particulars Debit Credit

Situation

1

30/6/20

18 Warranty Expense Dr.

$

34,400.00

To Provision of Warranty Related

Liability

$

34,400.00

(Being Provision for Warranty at the rate

of 8%)

Situation

2 Bad Debt Dr.

$

380,000.00

Provision for Bad & Doubtful Debts Dr

$

40,000.00

To Debtors

$

420,000.00

i) Appropriate Accounting treatment

Australian Accounting Standard 137 is related to Provisions, Contingent Liabilities, and

Contingent Asset. The main objective of this asset is to recognize and measure the provisions,

Contingent Assets, and Contingent Liabilities. It also states that adequate information should be

disclosed; by which user get the knowledge about timing, nature, and amount (Adhariani, Sciulli,

& Clift, 2017). Provisions are the liabilities which does not have certainty regarding the amount

and time. On the other hand, contingent liabilities are the possible obligation which depends on

the happening or non-happening of any event. Therefore it is not recognized in the books

(Hudson, 2016).

ii) Note Disclosures and Journal Entries for the financial statement ended in 2018 in each

situation

Table 1: Journal of Super Store Limited

Date Particulars Debit Credit

Situation

1

30/6/20

18 Warranty Expense Dr.

$

34,400.00

To Provision of Warranty Related

Liability

$

34,400.00

(Being Provision for Warranty at the rate

of 8%)

Situation

2 Bad Debt Dr.

$

380,000.00

Provision for Bad & Doubtful Debts Dr

$

40,000.00

To Debtors

$

420,000.00

(Being Amount recognized as Bad Debt

for the Debtors bankrupted)

Situation

3

No entry is required to be passed in this

case.

Situation

4 Repairs Dr.

$

21,000.00

To Trailer (Equipment)

$

21,000.00

$

475,400.00

$

454,400.00

The company should disclose, for every class of provision the following amount –

The carrying amount of provision at the starting of the year (Jeyaretnam, 2017).

Any enhancement in current provision and any additional provision made during the

year.

Any amount charged against the provision (Tran, 2015).

QUESTION 2

Table 2 Journal of Funland Limited

Date Particulars Debit Credit

3/31/2019 Bank Dr. $ 10,400,000.00

To Preference Share Application $ 1,600,000.00

To Equity Share Application $ 8,800,000.00

(being amount received on 800000

Preference Shares at the rate of

2/Share)

4/15/2019 Preference Share Application Dr. $ 1,600,000.00

To Preference Share Paid-up Capital $ 1,600,000.00

(being Preference Share Capital

raised of $1600000)

for the Debtors bankrupted)

Situation

3

No entry is required to be passed in this

case.

Situation

4 Repairs Dr.

$

21,000.00

To Trailer (Equipment)

$

21,000.00

$

475,400.00

$

454,400.00

The company should disclose, for every class of provision the following amount –

The carrying amount of provision at the starting of the year (Jeyaretnam, 2017).

Any enhancement in current provision and any additional provision made during the

year.

Any amount charged against the provision (Tran, 2015).

QUESTION 2

Table 2 Journal of Funland Limited

Date Particulars Debit Credit

3/31/2019 Bank Dr. $ 10,400,000.00

To Preference Share Application $ 1,600,000.00

To Equity Share Application $ 8,800,000.00

(being amount received on 800000

Preference Shares at the rate of

2/Share)

4/15/2019 Preference Share Application Dr. $ 1,600,000.00

To Preference Share Paid-up Capital $ 1,600,000.00

(being Preference Share Capital

raised of $1600000)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

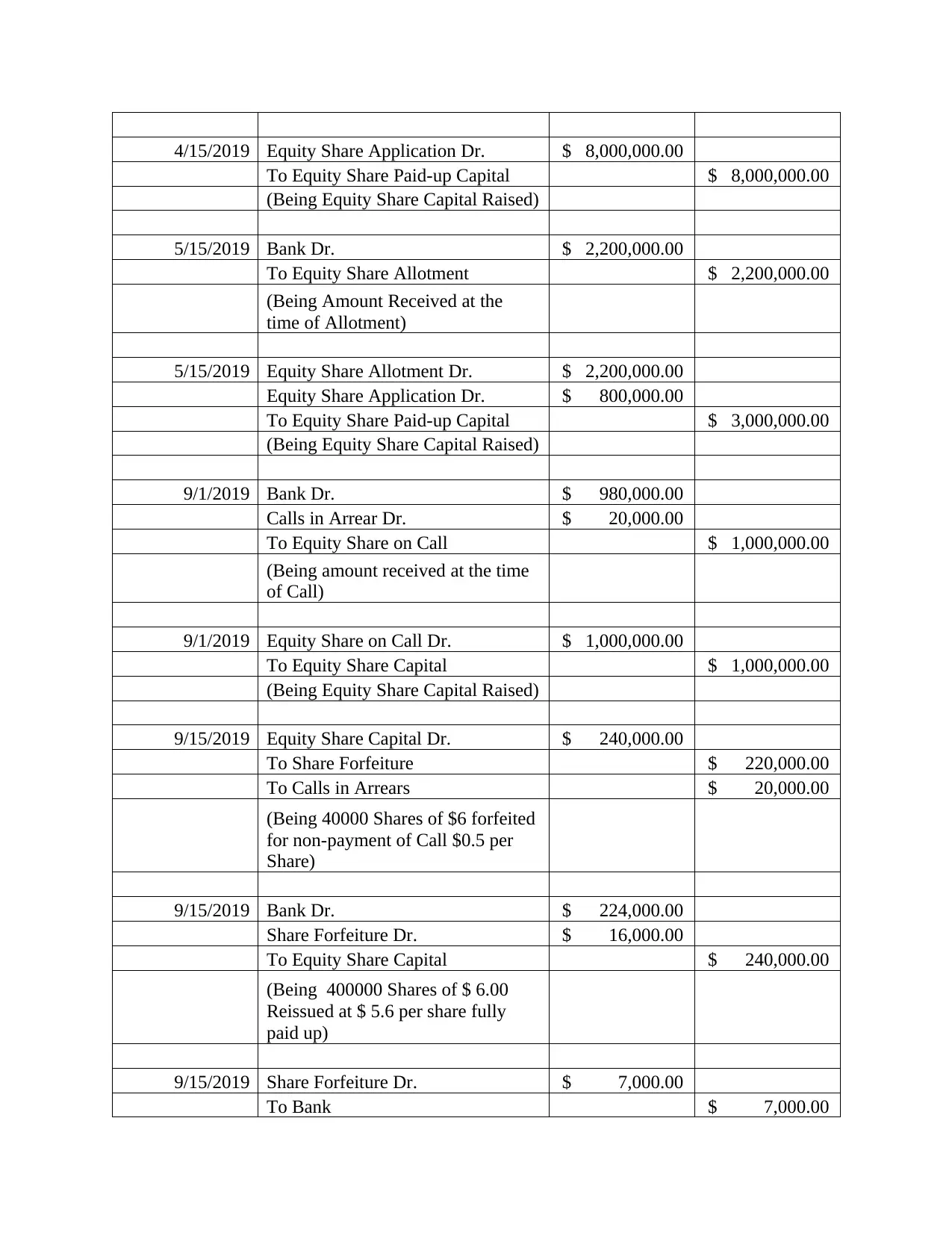

4/15/2019 Equity Share Application Dr. $ 8,000,000.00

To Equity Share Paid-up Capital $ 8,000,000.00

(Being Equity Share Capital Raised)

5/15/2019 Bank Dr. $ 2,200,000.00

To Equity Share Allotment $ 2,200,000.00

(Being Amount Received at the

time of Allotment)

5/15/2019 Equity Share Allotment Dr. $ 2,200,000.00

Equity Share Application Dr. $ 800,000.00

To Equity Share Paid-up Capital $ 3,000,000.00

(Being Equity Share Capital Raised)

9/1/2019 Bank Dr. $ 980,000.00

Calls in Arrear Dr. $ 20,000.00

To Equity Share on Call $ 1,000,000.00

(Being amount received at the time

of Call)

9/1/2019 Equity Share on Call Dr. $ 1,000,000.00

To Equity Share Capital $ 1,000,000.00

(Being Equity Share Capital Raised)

9/15/2019 Equity Share Capital Dr. $ 240,000.00

To Share Forfeiture $ 220,000.00

To Calls in Arrears $ 20,000.00

(Being 40000 Shares of $6 forfeited

for non-payment of Call $0.5 per

Share)

9/15/2019 Bank Dr. $ 224,000.00

Share Forfeiture Dr. $ 16,000.00

To Equity Share Capital $ 240,000.00

(Being 400000 Shares of $ 6.00

Reissued at $ 5.6 per share fully

paid up)

9/15/2019 Share Forfeiture Dr. $ 7,000.00

To Bank $ 7,000.00

To Equity Share Paid-up Capital $ 8,000,000.00

(Being Equity Share Capital Raised)

5/15/2019 Bank Dr. $ 2,200,000.00

To Equity Share Allotment $ 2,200,000.00

(Being Amount Received at the

time of Allotment)

5/15/2019 Equity Share Allotment Dr. $ 2,200,000.00

Equity Share Application Dr. $ 800,000.00

To Equity Share Paid-up Capital $ 3,000,000.00

(Being Equity Share Capital Raised)

9/1/2019 Bank Dr. $ 980,000.00

Calls in Arrear Dr. $ 20,000.00

To Equity Share on Call $ 1,000,000.00

(Being amount received at the time

of Call)

9/1/2019 Equity Share on Call Dr. $ 1,000,000.00

To Equity Share Capital $ 1,000,000.00

(Being Equity Share Capital Raised)

9/15/2019 Equity Share Capital Dr. $ 240,000.00

To Share Forfeiture $ 220,000.00

To Calls in Arrears $ 20,000.00

(Being 40000 Shares of $6 forfeited

for non-payment of Call $0.5 per

Share)

9/15/2019 Bank Dr. $ 224,000.00

Share Forfeiture Dr. $ 16,000.00

To Equity Share Capital $ 240,000.00

(Being 400000 Shares of $ 6.00

Reissued at $ 5.6 per share fully

paid up)

9/15/2019 Share Forfeiture Dr. $ 7,000.00

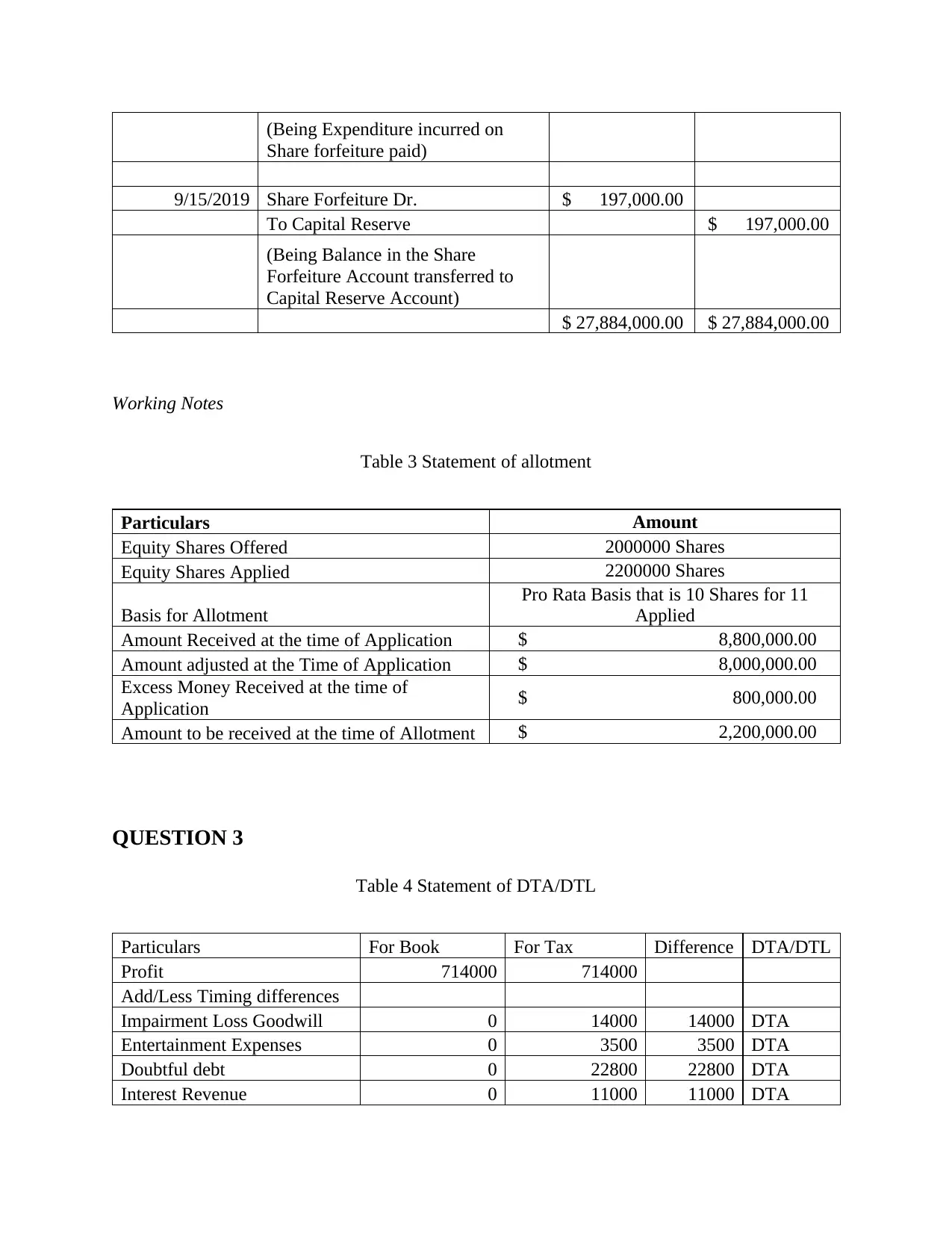

To Bank $ 7,000.00

(Being Expenditure incurred on

Share forfeiture paid)

9/15/2019 Share Forfeiture Dr. $ 197,000.00

To Capital Reserve $ 197,000.00

(Being Balance in the Share

Forfeiture Account transferred to

Capital Reserve Account)

$ 27,884,000.00 $ 27,884,000.00

Working Notes

Table 3 Statement of allotment

Particulars Amount

Equity Shares Offered 2000000 Shares

Equity Shares Applied 2200000 Shares

Basis for Allotment

Pro Rata Basis that is 10 Shares for 11

Applied

Amount Received at the time of Application $ 8,800,000.00

Amount adjusted at the Time of Application $ 8,000,000.00

Excess Money Received at the time of

Application $ 800,000.00

Amount to be received at the time of Allotment $ 2,200,000.00

QUESTION 3

Table 4 Statement of DTA/DTL

Particulars For Book For Tax Difference DTA/DTL

Profit 714000 714000

Add/Less Timing differences

Impairment Loss Goodwill 0 14000 14000 DTA

Entertainment Expenses 0 3500 3500 DTA

Doubtful debt 0 22800 22800 DTA

Interest Revenue 0 11000 11000 DTA

Share forfeiture paid)

9/15/2019 Share Forfeiture Dr. $ 197,000.00

To Capital Reserve $ 197,000.00

(Being Balance in the Share

Forfeiture Account transferred to

Capital Reserve Account)

$ 27,884,000.00 $ 27,884,000.00

Working Notes

Table 3 Statement of allotment

Particulars Amount

Equity Shares Offered 2000000 Shares

Equity Shares Applied 2200000 Shares

Basis for Allotment

Pro Rata Basis that is 10 Shares for 11

Applied

Amount Received at the time of Application $ 8,800,000.00

Amount adjusted at the Time of Application $ 8,000,000.00

Excess Money Received at the time of

Application $ 800,000.00

Amount to be received at the time of Allotment $ 2,200,000.00

QUESTION 3

Table 4 Statement of DTA/DTL

Particulars For Book For Tax Difference DTA/DTL

Profit 714000 714000

Add/Less Timing differences

Impairment Loss Goodwill 0 14000 14000 DTA

Entertainment Expenses 0 3500 3500 DTA

Doubtful debt 0 22800 22800 DTA

Interest Revenue 0 11000 11000 DTA

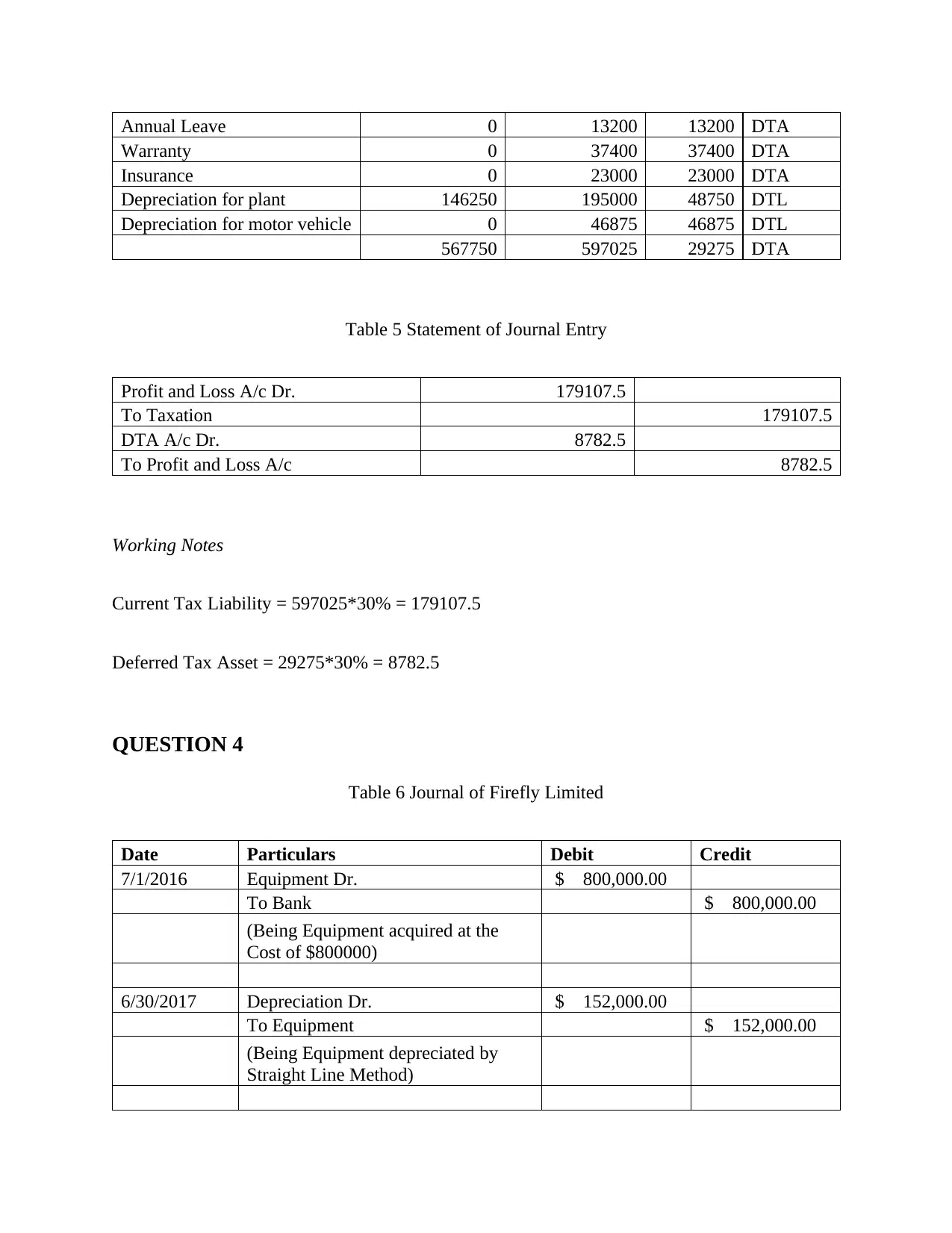

Annual Leave 0 13200 13200 DTA

Warranty 0 37400 37400 DTA

Insurance 0 23000 23000 DTA

Depreciation for plant 146250 195000 48750 DTL

Depreciation for motor vehicle 0 46875 46875 DTL

567750 597025 29275 DTA

Table 5 Statement of Journal Entry

Profit and Loss A/c Dr. 179107.5

To Taxation 179107.5

DTA A/c Dr. 8782.5

To Profit and Loss A/c 8782.5

Working Notes

Current Tax Liability = 597025*30% = 179107.5

Deferred Tax Asset = 29275*30% = 8782.5

QUESTION 4

Table 6 Journal of Firefly Limited

Date Particulars Debit Credit

7/1/2016 Equipment Dr. $ 800,000.00

To Bank $ 800,000.00

(Being Equipment acquired at the

Cost of $800000)

6/30/2017 Depreciation Dr. $ 152,000.00

To Equipment $ 152,000.00

(Being Equipment depreciated by

Straight Line Method)

Warranty 0 37400 37400 DTA

Insurance 0 23000 23000 DTA

Depreciation for plant 146250 195000 48750 DTL

Depreciation for motor vehicle 0 46875 46875 DTL

567750 597025 29275 DTA

Table 5 Statement of Journal Entry

Profit and Loss A/c Dr. 179107.5

To Taxation 179107.5

DTA A/c Dr. 8782.5

To Profit and Loss A/c 8782.5

Working Notes

Current Tax Liability = 597025*30% = 179107.5

Deferred Tax Asset = 29275*30% = 8782.5

QUESTION 4

Table 6 Journal of Firefly Limited

Date Particulars Debit Credit

7/1/2016 Equipment Dr. $ 800,000.00

To Bank $ 800,000.00

(Being Equipment acquired at the

Cost of $800000)

6/30/2017 Depreciation Dr. $ 152,000.00

To Equipment $ 152,000.00

(Being Equipment depreciated by

Straight Line Method)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

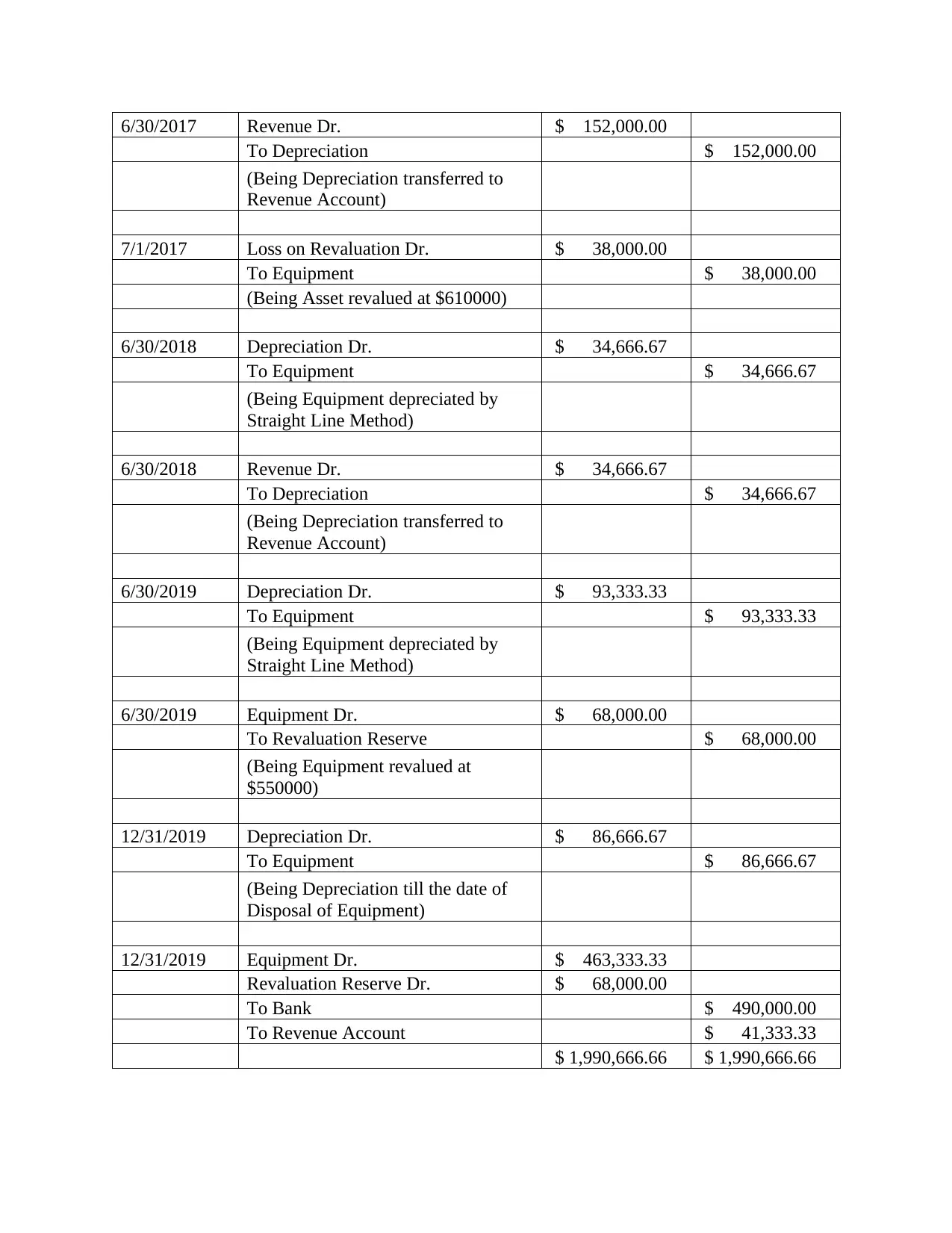

6/30/2017 Revenue Dr. $ 152,000.00

To Depreciation $ 152,000.00

(Being Depreciation transferred to

Revenue Account)

7/1/2017 Loss on Revaluation Dr. $ 38,000.00

To Equipment $ 38,000.00

(Being Asset revalued at $610000)

6/30/2018 Depreciation Dr. $ 34,666.67

To Equipment $ 34,666.67

(Being Equipment depreciated by

Straight Line Method)

6/30/2018 Revenue Dr. $ 34,666.67

To Depreciation $ 34,666.67

(Being Depreciation transferred to

Revenue Account)

6/30/2019 Depreciation Dr. $ 93,333.33

To Equipment $ 93,333.33

(Being Equipment depreciated by

Straight Line Method)

6/30/2019 Equipment Dr. $ 68,000.00

To Revaluation Reserve $ 68,000.00

(Being Equipment revalued at

$550000)

12/31/2019 Depreciation Dr. $ 86,666.67

To Equipment $ 86,666.67

(Being Depreciation till the date of

Disposal of Equipment)

12/31/2019 Equipment Dr. $ 463,333.33

Revaluation Reserve Dr. $ 68,000.00

To Bank $ 490,000.00

To Revenue Account $ 41,333.33

$ 1,990,666.66 $ 1,990,666.66

To Depreciation $ 152,000.00

(Being Depreciation transferred to

Revenue Account)

7/1/2017 Loss on Revaluation Dr. $ 38,000.00

To Equipment $ 38,000.00

(Being Asset revalued at $610000)

6/30/2018 Depreciation Dr. $ 34,666.67

To Equipment $ 34,666.67

(Being Equipment depreciated by

Straight Line Method)

6/30/2018 Revenue Dr. $ 34,666.67

To Depreciation $ 34,666.67

(Being Depreciation transferred to

Revenue Account)

6/30/2019 Depreciation Dr. $ 93,333.33

To Equipment $ 93,333.33

(Being Equipment depreciated by

Straight Line Method)

6/30/2019 Equipment Dr. $ 68,000.00

To Revaluation Reserve $ 68,000.00

(Being Equipment revalued at

$550000)

12/31/2019 Depreciation Dr. $ 86,666.67

To Equipment $ 86,666.67

(Being Depreciation till the date of

Disposal of Equipment)

12/31/2019 Equipment Dr. $ 463,333.33

Revaluation Reserve Dr. $ 68,000.00

To Bank $ 490,000.00

To Revenue Account $ 41,333.33

$ 1,990,666.66 $ 1,990,666.66

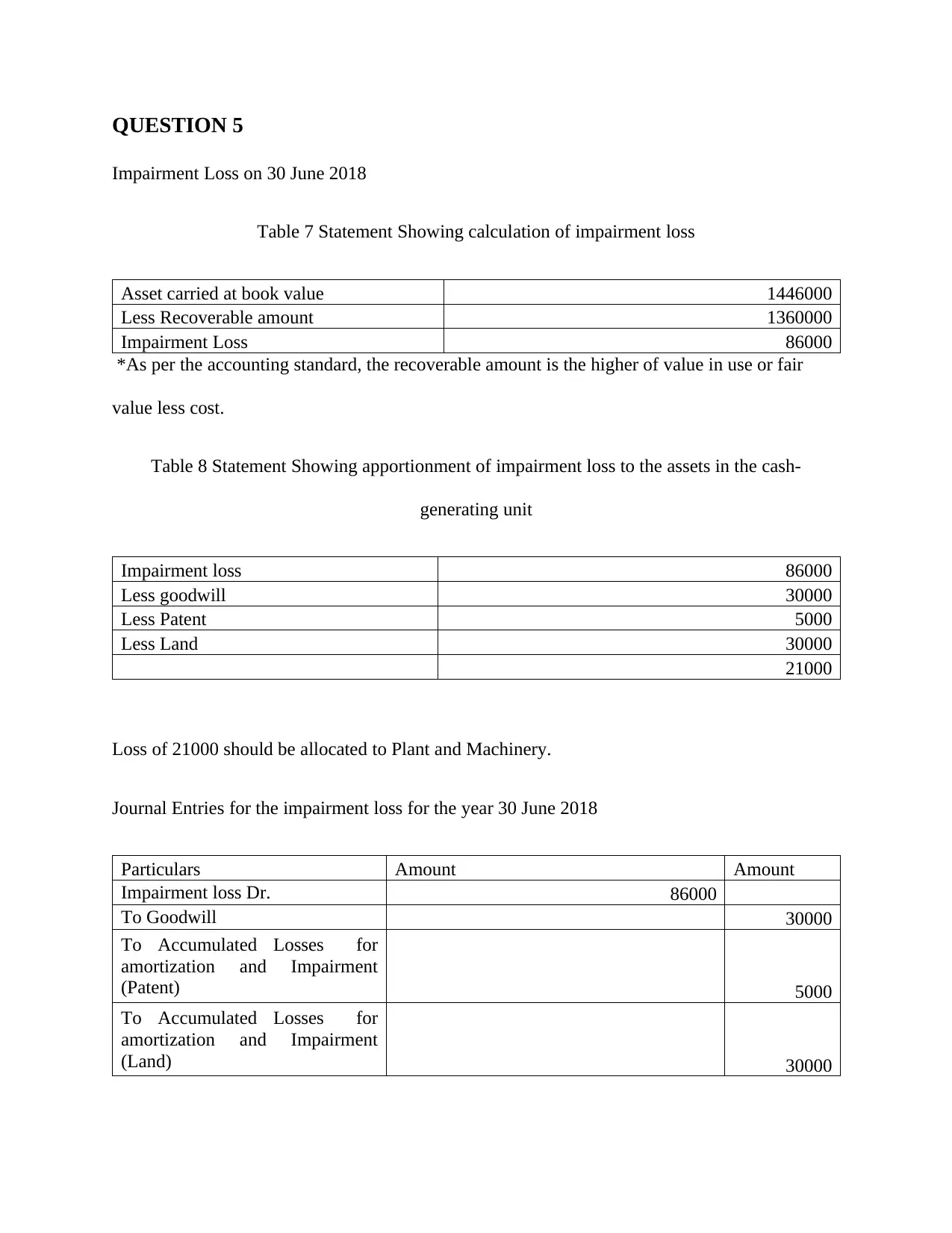

QUESTION 5

Impairment Loss on 30 June 2018

Table 7 Statement Showing calculation of impairment loss

Asset carried at book value 1446000

Less Recoverable amount 1360000

Impairment Loss 86000

*As per the accounting standard, the recoverable amount is the higher of value in use or fair

value less cost.

Table 8 Statement Showing apportionment of impairment loss to the assets in the cash-

generating unit

Impairment loss 86000

Less goodwill 30000

Less Patent 5000

Less Land 30000

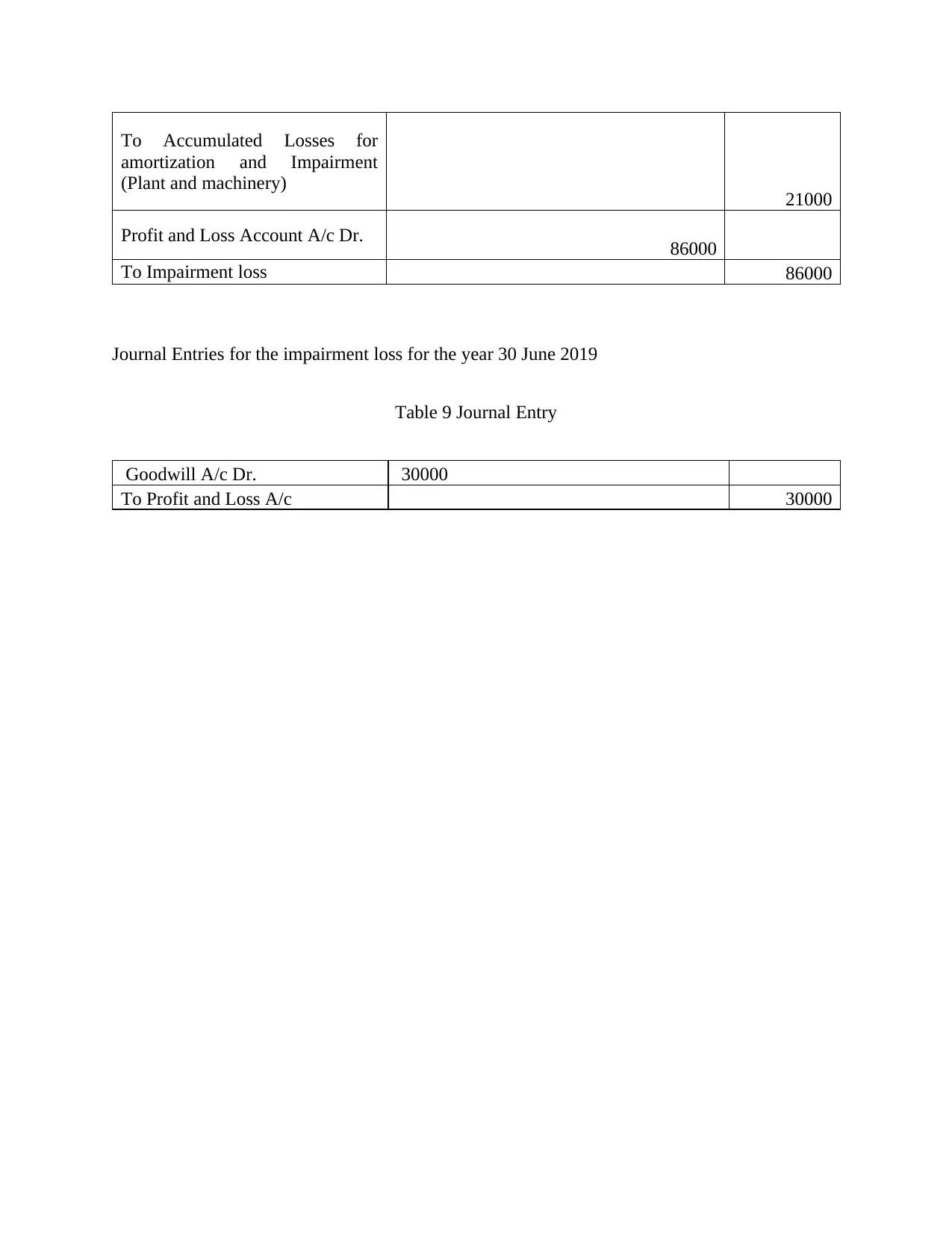

21000

Loss of 21000 should be allocated to Plant and Machinery.

Journal Entries for the impairment loss for the year 30 June 2018

Particulars Amount Amount

Impairment loss Dr. 86000

To Goodwill 30000

To Accumulated Losses for

amortization and Impairment

(Patent) 5000

To Accumulated Losses for

amortization and Impairment

(Land) 30000

Impairment Loss on 30 June 2018

Table 7 Statement Showing calculation of impairment loss

Asset carried at book value 1446000

Less Recoverable amount 1360000

Impairment Loss 86000

*As per the accounting standard, the recoverable amount is the higher of value in use or fair

value less cost.

Table 8 Statement Showing apportionment of impairment loss to the assets in the cash-

generating unit

Impairment loss 86000

Less goodwill 30000

Less Patent 5000

Less Land 30000

21000

Loss of 21000 should be allocated to Plant and Machinery.

Journal Entries for the impairment loss for the year 30 June 2018

Particulars Amount Amount

Impairment loss Dr. 86000

To Goodwill 30000

To Accumulated Losses for

amortization and Impairment

(Patent) 5000

To Accumulated Losses for

amortization and Impairment

(Land) 30000

To Accumulated Losses for

amortization and Impairment

(Plant and machinery) 21000

Profit and Loss Account A/c Dr. 86000

To Impairment loss 86000

Journal Entries for the impairment loss for the year 30 June 2019

Table 9 Journal Entry

Goodwill A/c Dr. 30000

To Profit and Loss A/c 30000

amortization and Impairment

(Plant and machinery) 21000

Profit and Loss Account A/c Dr. 86000

To Impairment loss 86000

Journal Entries for the impairment loss for the year 30 June 2019

Table 9 Journal Entry

Goodwill A/c Dr. 30000

To Profit and Loss A/c 30000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Adhariani, D., Sciulli, N., & Clift, R. (2017). Quantitative Optimisation Model, Results and

Discussion. In Financial Management and Corporate Governance from the Feminist Ethics

of Care Perspective (pp. 209-284). Palgrave Macmillan, Cham.

Hudson, M. (2016). No setting off unfair preferences. Australian Restructuring Insolvency &

Turnaround Association Journal, 28(3), 34.

Jeyaretnam, T. (2017). Emerging risk: Mine closure and rehabilitation. AusIMM Bulletin, (Dec

2017), 24(1). 25-26

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30(1), 569.

Adhariani, D., Sciulli, N., & Clift, R. (2017). Quantitative Optimisation Model, Results and

Discussion. In Financial Management and Corporate Governance from the Feminist Ethics

of Care Perspective (pp. 209-284). Palgrave Macmillan, Cham.

Hudson, M. (2016). No setting off unfair preferences. Australian Restructuring Insolvency &

Turnaround Association Journal, 28(3), 34.

Jeyaretnam, T. (2017). Emerging risk: Mine closure and rehabilitation. AusIMM Bulletin, (Dec

2017), 24(1). 25-26

Tran, A. (2015). Can taxable income be estimated from financial reports of listed companies in

Australia. Austl. Tax F., 30(1), 569.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.