Financial Accounting: Concepts and Application

VerifiedAdded on 2023/01/11

|27

|4293

|40

AI Summary

This guide provides an overview of financial accounting, including the concepts and application of the double entry system, trial balance, and allocation of accounts to financial statements. It covers topics such as recording business transactions, analysing financial statements using ratio analysis, and reconciling bank and cash balances.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................2

1.3..............................................................................................................................................11

TASK 2..........................................................................................................................................12

2.1..............................................................................................................................................12

2.2..............................................................................................................................................13

2.3..............................................................................................................................................14

2.4..............................................................................................................................................16

TASK 3..........................................................................................................................................17

3.1..............................................................................................................................................17

3.2..............................................................................................................................................18

3.3..............................................................................................................................................19

3.4..............................................................................................................................................19

TASK 4..........................................................................................................................................21

4.1..............................................................................................................................................21

4.2..............................................................................................................................................21

4.3..............................................................................................................................................22

4.4..............................................................................................................................................23

CONCLUSIONS...........................................................................................................................24

REFERENCES..............................................................................................................................25

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................2

1.3..............................................................................................................................................11

TASK 2..........................................................................................................................................12

2.1..............................................................................................................................................12

2.2..............................................................................................................................................13

2.3..............................................................................................................................................14

2.4..............................................................................................................................................16

TASK 3..........................................................................................................................................17

3.1..............................................................................................................................................17

3.2..............................................................................................................................................18

3.3..............................................................................................................................................19

3.4..............................................................................................................................................19

TASK 4..........................................................................................................................................21

4.1..............................................................................................................................................21

4.2..............................................................................................................................................21

4.3..............................................................................................................................................22

4.4..............................................................................................................................................23

CONCLUSIONS...........................................................................................................................24

REFERENCES..............................................................................................................................25

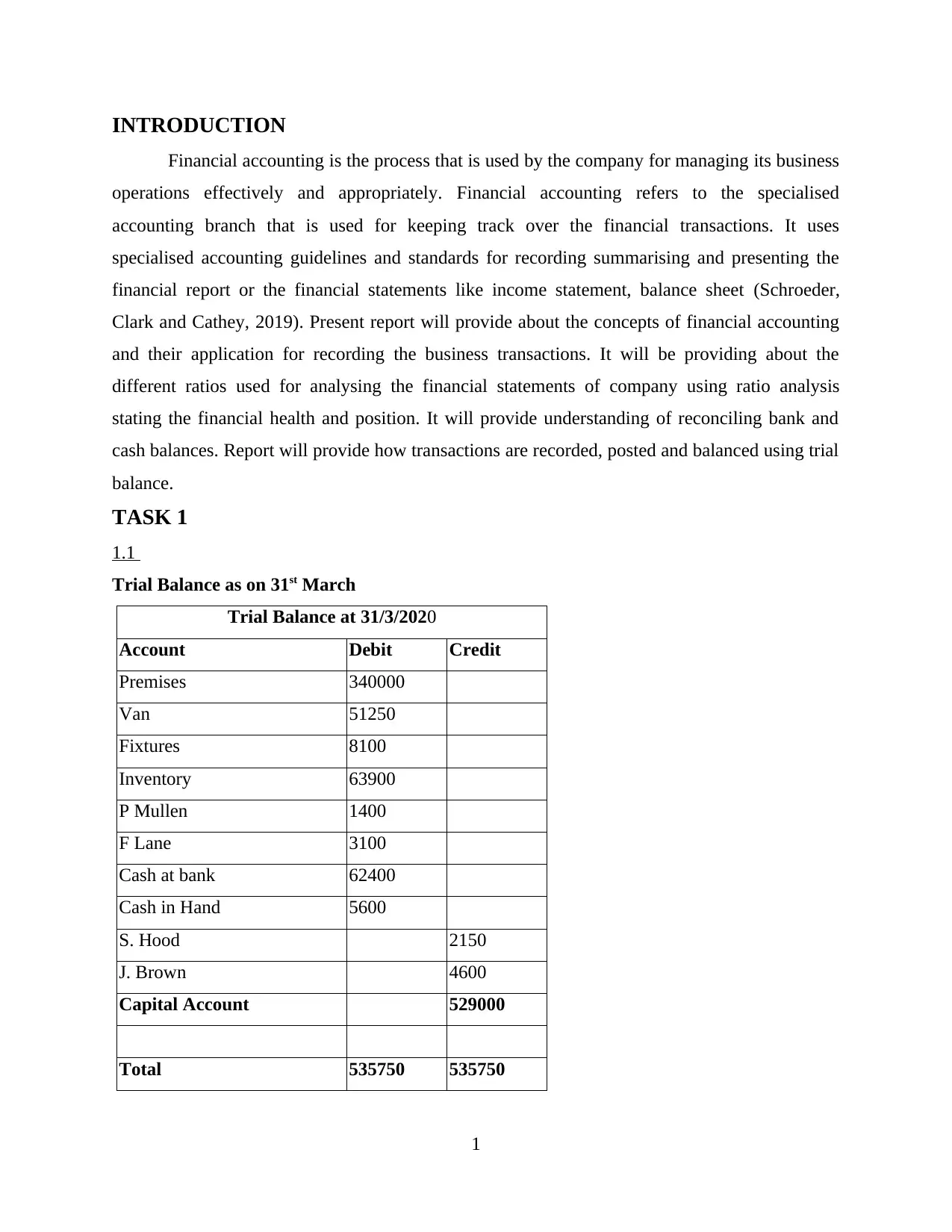

INTRODUCTION

Financial accounting is the process that is used by the company for managing its business

operations effectively and appropriately. Financial accounting refers to the specialised

accounting branch that is used for keeping track over the financial transactions. It uses

specialised accounting guidelines and standards for recording summarising and presenting the

financial report or the financial statements like income statement, balance sheet (Schroeder,

Clark and Cathey, 2019). Present report will provide about the concepts of financial accounting

and their application for recording the business transactions. It will be providing about the

different ratios used for analysing the financial statements of company using ratio analysis

stating the financial health and position. It will provide understanding of reconciling bank and

cash balances. Report will provide how transactions are recorded, posted and balanced using trial

balance.

TASK 1

1.1

Trial Balance as on 31st March

Trial Balance at 31/3/2020

Account Debit Credit

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

P Mullen 1400

F Lane 3100

Cash at bank 62400

Cash in Hand 5600

S. Hood 2150

J. Brown 4600

Capital Account 529000

Total 535750 535750

1

Financial accounting is the process that is used by the company for managing its business

operations effectively and appropriately. Financial accounting refers to the specialised

accounting branch that is used for keeping track over the financial transactions. It uses

specialised accounting guidelines and standards for recording summarising and presenting the

financial report or the financial statements like income statement, balance sheet (Schroeder,

Clark and Cathey, 2019). Present report will provide about the concepts of financial accounting

and their application for recording the business transactions. It will be providing about the

different ratios used for analysing the financial statements of company using ratio analysis

stating the financial health and position. It will provide understanding of reconciling bank and

cash balances. Report will provide how transactions are recorded, posted and balanced using trial

balance.

TASK 1

1.1

Trial Balance as on 31st March

Trial Balance at 31/3/2020

Account Debit Credit

Premises 340000

Van 51250

Fixtures 8100

Inventory 63900

P Mullen 1400

F Lane 3100

Cash at bank 62400

Cash in Hand 5600

S. Hood 2150

J. Brown 4600

Capital Account 529000

Total 535750 535750

1

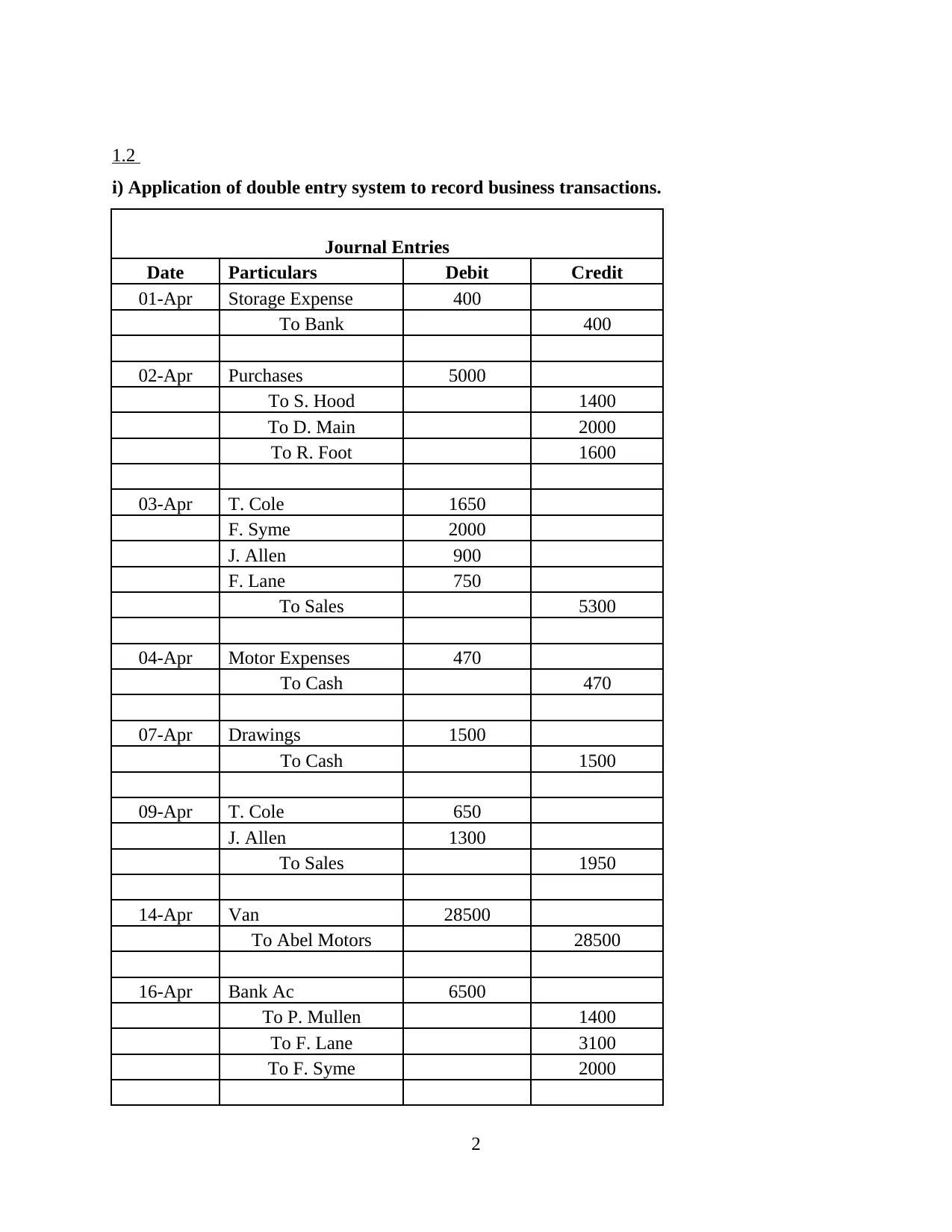

1.2

i) Application of double entry system to record business transactions.

Journal Entries

Date Particulars Debit Credit

01-Apr Storage Expense 400

To Bank 400

02-Apr Purchases 5000

To S. Hood 1400

To D. Main 2000

To R. Foot 1600

03-Apr T. Cole 1650

F. Syme 2000

J. Allen 900

F. Lane 750

To Sales 5300

04-Apr Motor Expenses 470

To Cash 470

07-Apr Drawings 1500

To Cash 1500

09-Apr T. Cole 650

J. Allen 1300

To Sales 1950

14-Apr Van 28500

To Abel Motors 28500

16-Apr Bank Ac 6500

To P. Mullen 1400

To F. Lane 3100

To F. Syme 2000

2

i) Application of double entry system to record business transactions.

Journal Entries

Date Particulars Debit Credit

01-Apr Storage Expense 400

To Bank 400

02-Apr Purchases 5000

To S. Hood 1400

To D. Main 2000

To R. Foot 1600

03-Apr T. Cole 1650

F. Syme 2000

J. Allen 900

F. Lane 750

To Sales 5300

04-Apr Motor Expenses 470

To Cash 470

07-Apr Drawings 1500

To Cash 1500

09-Apr T. Cole 650

J. Allen 1300

To Sales 1950

14-Apr Van 28500

To Abel Motors 28500

16-Apr Bank Ac 6500

To P. Mullen 1400

To F. Lane 3100

To F. Syme 2000

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

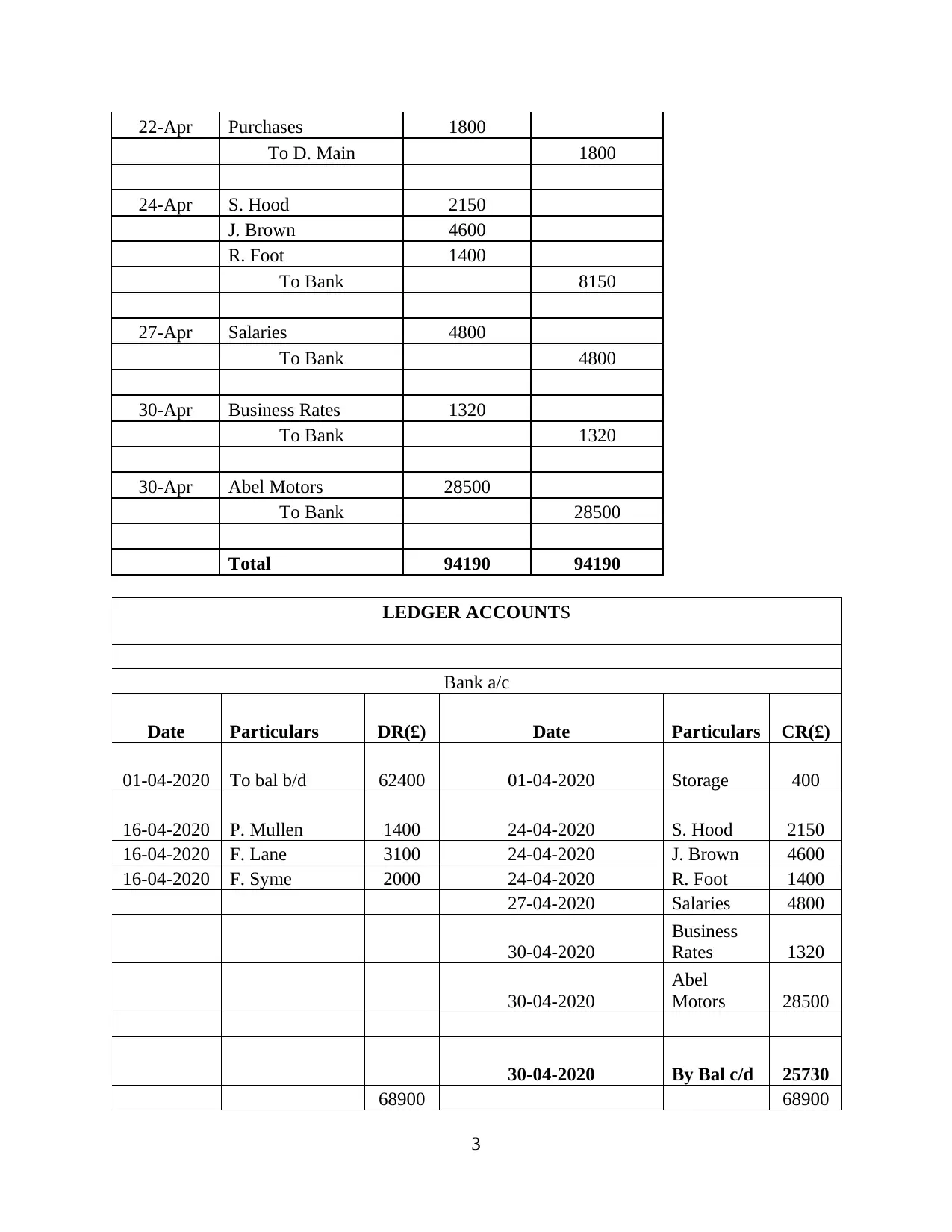

22-Apr Purchases 1800

To D. Main 1800

24-Apr S. Hood 2150

J. Brown 4600

R. Foot 1400

To Bank 8150

27-Apr Salaries 4800

To Bank 4800

30-Apr Business Rates 1320

To Bank 1320

30-Apr Abel Motors 28500

To Bank 28500

Total 94190 94190

LEDGER ACCOUNTS

Bank a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 62400 01-04-2020 Storage 400

16-04-2020 P. Mullen 1400 24-04-2020 S. Hood 2150

16-04-2020 F. Lane 3100 24-04-2020 J. Brown 4600

16-04-2020 F. Syme 2000 24-04-2020 R. Foot 1400

27-04-2020 Salaries 4800

30-04-2020

Business

Rates 1320

30-04-2020

Abel

Motors 28500

30-04-2020 By Bal c/d 25730

68900 68900

3

To D. Main 1800

24-Apr S. Hood 2150

J. Brown 4600

R. Foot 1400

To Bank 8150

27-Apr Salaries 4800

To Bank 4800

30-Apr Business Rates 1320

To Bank 1320

30-Apr Abel Motors 28500

To Bank 28500

Total 94190 94190

LEDGER ACCOUNTS

Bank a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 62400 01-04-2020 Storage 400

16-04-2020 P. Mullen 1400 24-04-2020 S. Hood 2150

16-04-2020 F. Lane 3100 24-04-2020 J. Brown 4600

16-04-2020 F. Syme 2000 24-04-2020 R. Foot 1400

27-04-2020 Salaries 4800

30-04-2020

Business

Rates 1320

30-04-2020

Abel

Motors 28500

30-04-2020 By Bal c/d 25730

68900 68900

3

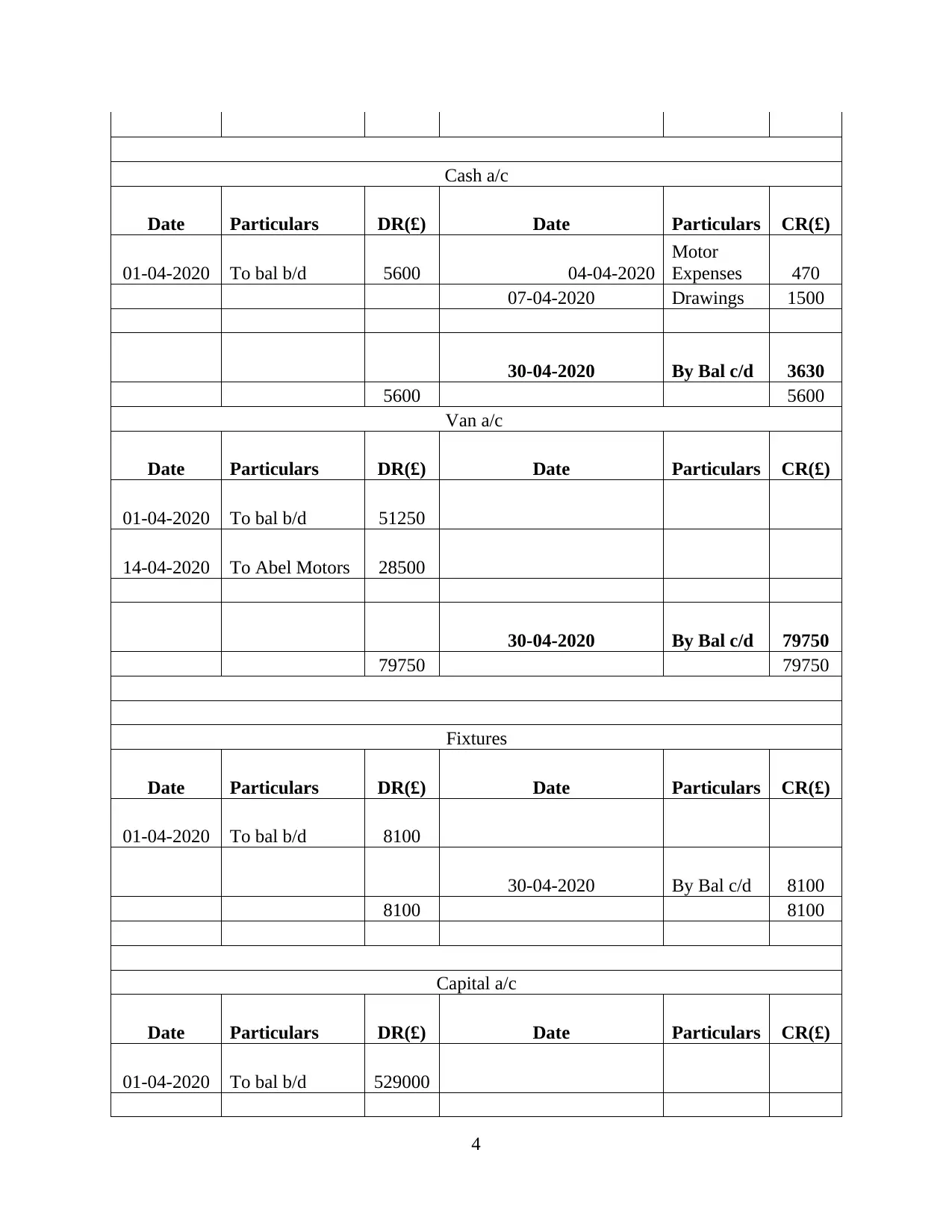

Cash a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 5600 04-04-2020

Motor

Expenses 470

07-04-2020 Drawings 1500

30-04-2020 By Bal c/d 3630

5600 5600

Van a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 51250

14-04-2020 To Abel Motors 28500

30-04-2020 By Bal c/d 79750

79750 79750

Fixtures

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 8100

30-04-2020 By Bal c/d 8100

8100 8100

Capital a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 529000

4

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 5600 04-04-2020

Motor

Expenses 470

07-04-2020 Drawings 1500

30-04-2020 By Bal c/d 3630

5600 5600

Van a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 51250

14-04-2020 To Abel Motors 28500

30-04-2020 By Bal c/d 79750

79750 79750

Fixtures

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 8100

30-04-2020 By Bal c/d 8100

8100 8100

Capital a/c

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 529000

4

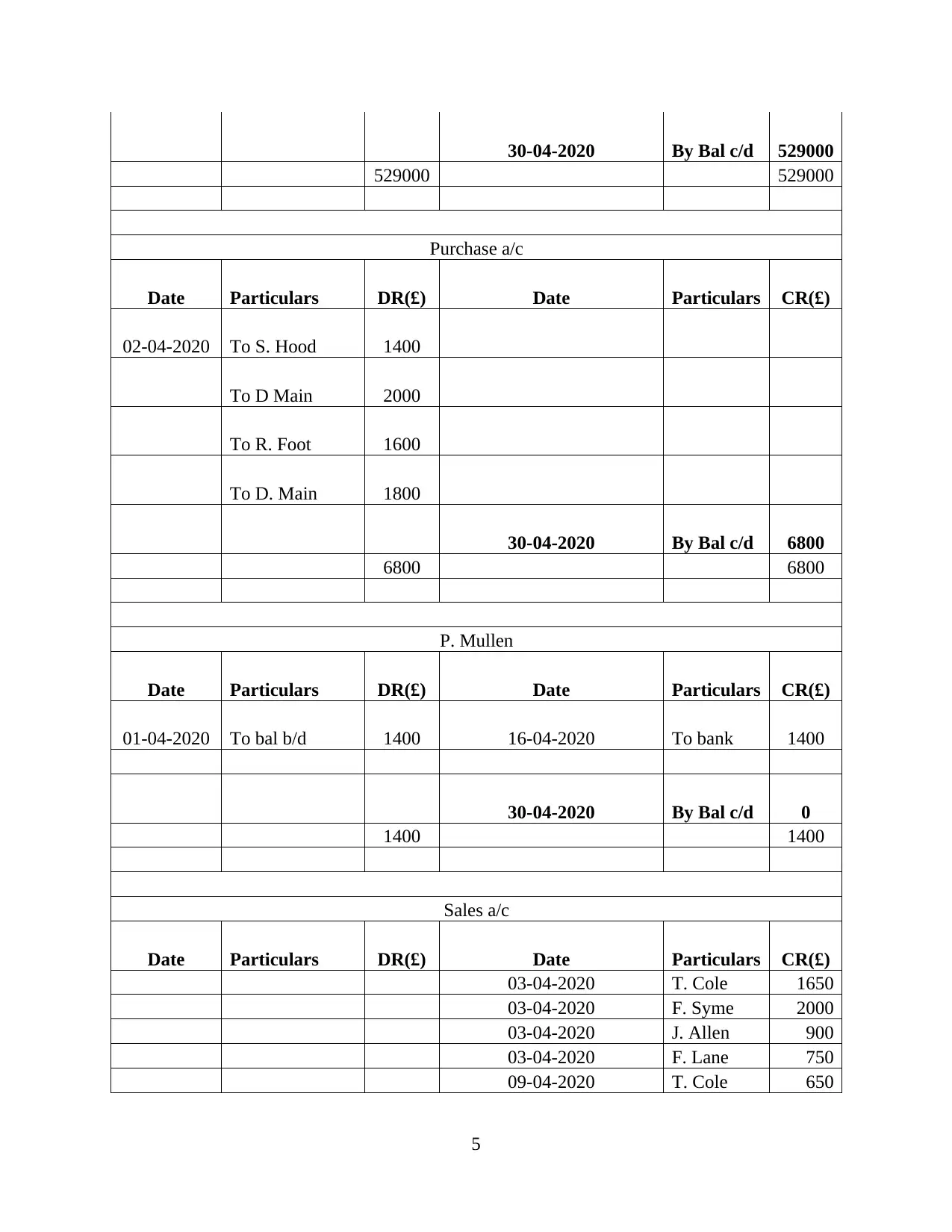

30-04-2020 By Bal c/d 529000

529000 529000

Purchase a/c

Date Particulars DR(£) Date Particulars CR(£)

02-04-2020 To S. Hood 1400

To D Main 2000

To R. Foot 1600

To D. Main 1800

30-04-2020 By Bal c/d 6800

6800 6800

P. Mullen

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 1400 16-04-2020 To bank 1400

30-04-2020 By Bal c/d 0

1400 1400

Sales a/c

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 T. Cole 1650

03-04-2020 F. Syme 2000

03-04-2020 J. Allen 900

03-04-2020 F. Lane 750

09-04-2020 T. Cole 650

5

529000 529000

Purchase a/c

Date Particulars DR(£) Date Particulars CR(£)

02-04-2020 To S. Hood 1400

To D Main 2000

To R. Foot 1600

To D. Main 1800

30-04-2020 By Bal c/d 6800

6800 6800

P. Mullen

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 1400 16-04-2020 To bank 1400

30-04-2020 By Bal c/d 0

1400 1400

Sales a/c

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 T. Cole 1650

03-04-2020 F. Syme 2000

03-04-2020 J. Allen 900

03-04-2020 F. Lane 750

09-04-2020 T. Cole 650

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

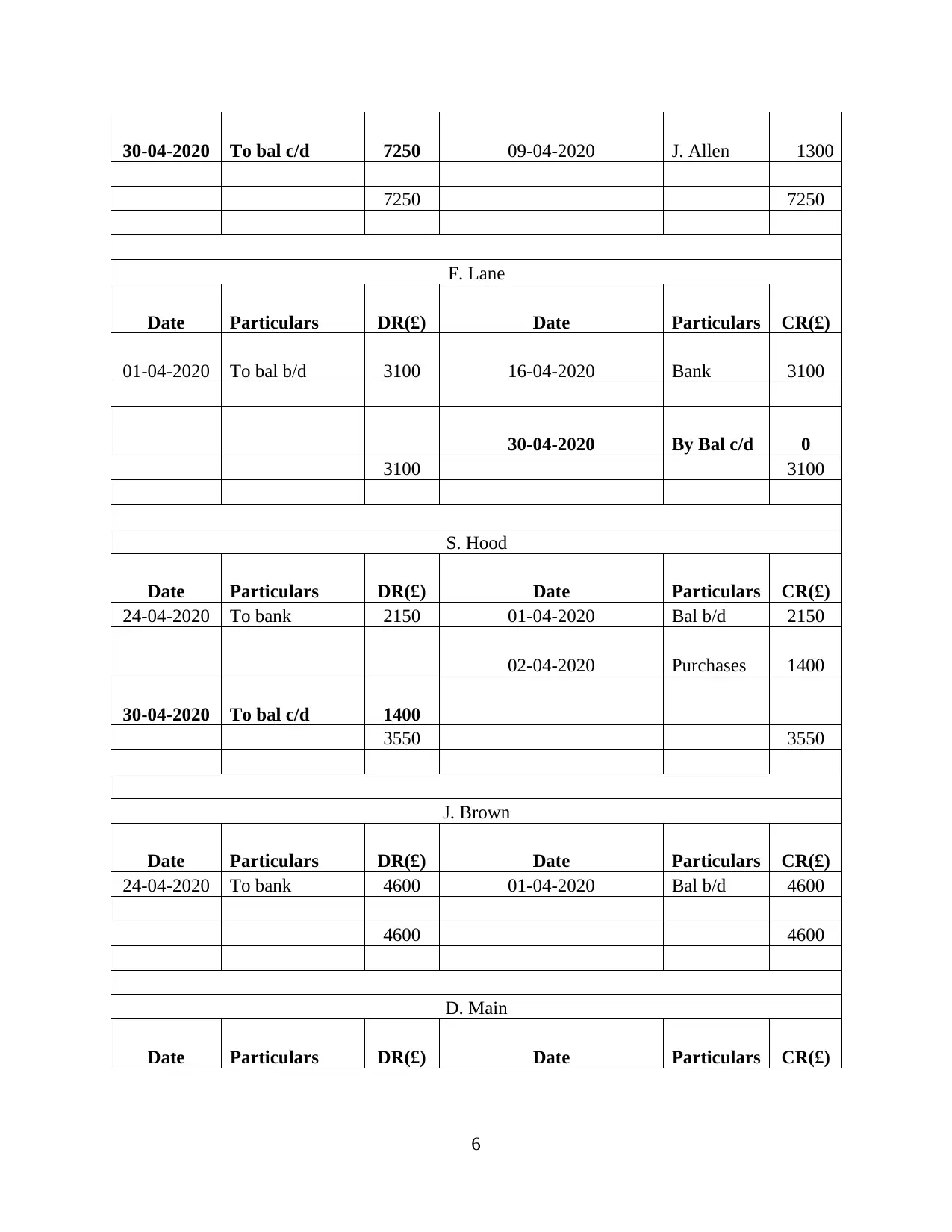

30-04-2020 To bal c/d 7250 09-04-2020 J. Allen 1300

7250 7250

F. Lane

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 3100 16-04-2020 Bank 3100

30-04-2020 By Bal c/d 0

3100 3100

S. Hood

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To bank 2150 01-04-2020 Bal b/d 2150

02-04-2020 Purchases 1400

30-04-2020 To bal c/d 1400

3550 3550

J. Brown

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To bank 4600 01-04-2020 Bal b/d 4600

4600 4600

D. Main

Date Particulars DR(£) Date Particulars CR(£)

6

7250 7250

F. Lane

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bal b/d 3100 16-04-2020 Bank 3100

30-04-2020 By Bal c/d 0

3100 3100

S. Hood

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To bank 2150 01-04-2020 Bal b/d 2150

02-04-2020 Purchases 1400

30-04-2020 To bal c/d 1400

3550 3550

J. Brown

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To bank 4600 01-04-2020 Bal b/d 4600

4600 4600

D. Main

Date Particulars DR(£) Date Particulars CR(£)

6

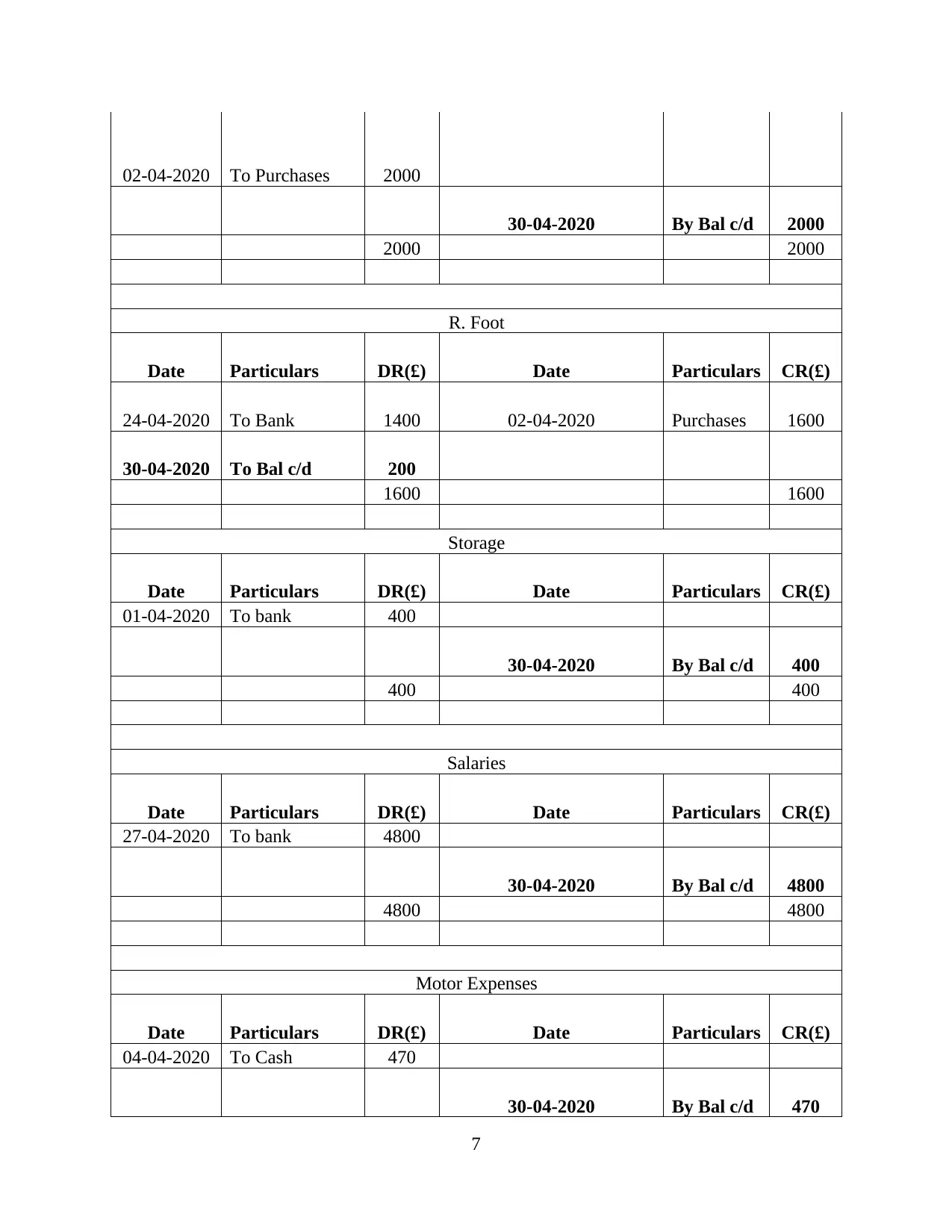

02-04-2020 To Purchases 2000

30-04-2020 By Bal c/d 2000

2000 2000

R. Foot

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To Bank 1400 02-04-2020 Purchases 1600

30-04-2020 To Bal c/d 200

1600 1600

Storage

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bank 400

30-04-2020 By Bal c/d 400

400 400

Salaries

Date Particulars DR(£) Date Particulars CR(£)

27-04-2020 To bank 4800

30-04-2020 By Bal c/d 4800

4800 4800

Motor Expenses

Date Particulars DR(£) Date Particulars CR(£)

04-04-2020 To Cash 470

30-04-2020 By Bal c/d 470

7

30-04-2020 By Bal c/d 2000

2000 2000

R. Foot

Date Particulars DR(£) Date Particulars CR(£)

24-04-2020 To Bank 1400 02-04-2020 Purchases 1600

30-04-2020 To Bal c/d 200

1600 1600

Storage

Date Particulars DR(£) Date Particulars CR(£)

01-04-2020 To bank 400

30-04-2020 By Bal c/d 400

400 400

Salaries

Date Particulars DR(£) Date Particulars CR(£)

27-04-2020 To bank 4800

30-04-2020 By Bal c/d 4800

4800 4800

Motor Expenses

Date Particulars DR(£) Date Particulars CR(£)

04-04-2020 To Cash 470

30-04-2020 By Bal c/d 470

7

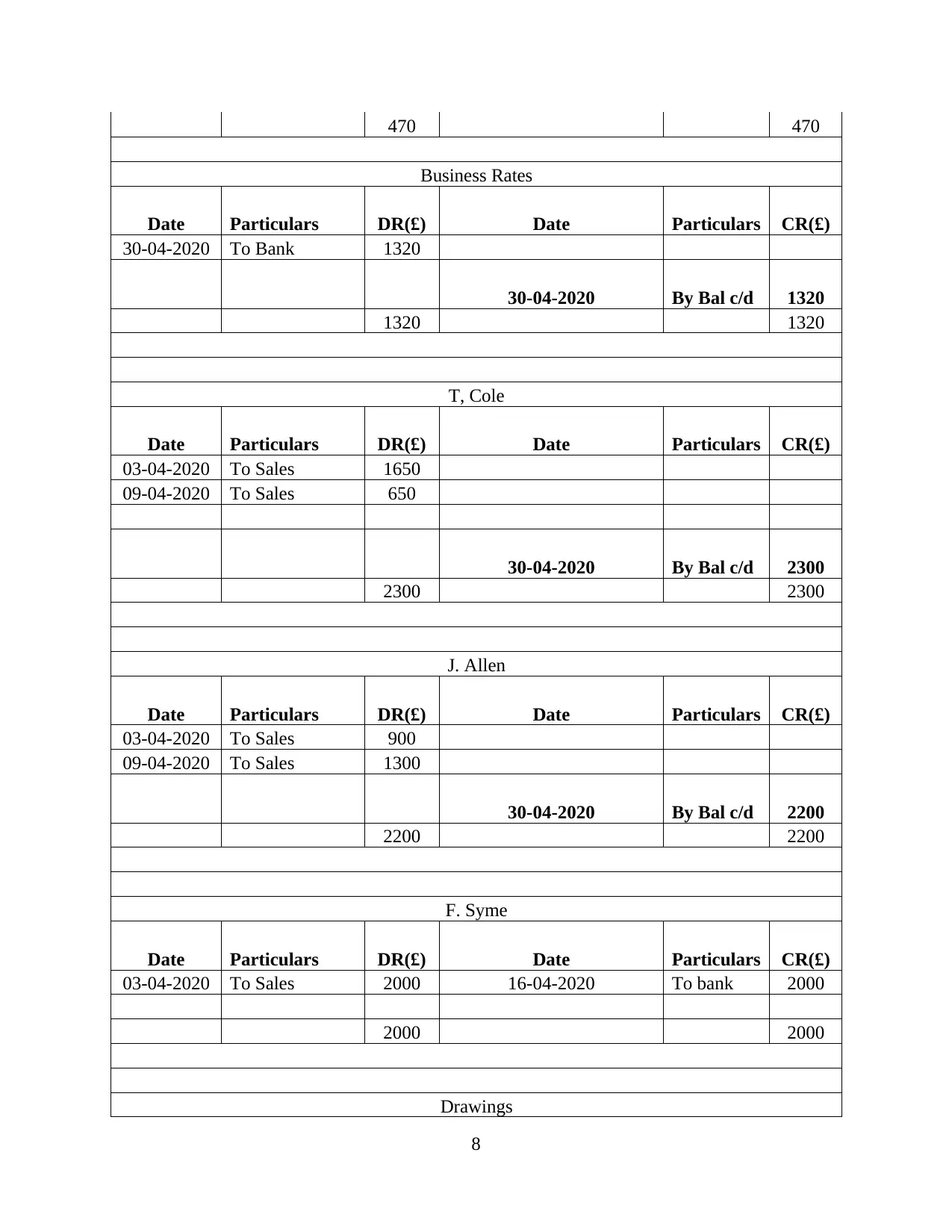

470 470

Business Rates

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To Bank 1320

30-04-2020 By Bal c/d 1320

1320 1320

T, Cole

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 1650

09-04-2020 To Sales 650

30-04-2020 By Bal c/d 2300

2300 2300

J. Allen

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 900

09-04-2020 To Sales 1300

30-04-2020 By Bal c/d 2200

2200 2200

F. Syme

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 2000 16-04-2020 To bank 2000

2000 2000

Drawings

8

Business Rates

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To Bank 1320

30-04-2020 By Bal c/d 1320

1320 1320

T, Cole

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 1650

09-04-2020 To Sales 650

30-04-2020 By Bal c/d 2300

2300 2300

J. Allen

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 900

09-04-2020 To Sales 1300

30-04-2020 By Bal c/d 2200

2200 2200

F. Syme

Date Particulars DR(£) Date Particulars CR(£)

03-04-2020 To Sales 2000 16-04-2020 To bank 2000

2000 2000

Drawings

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

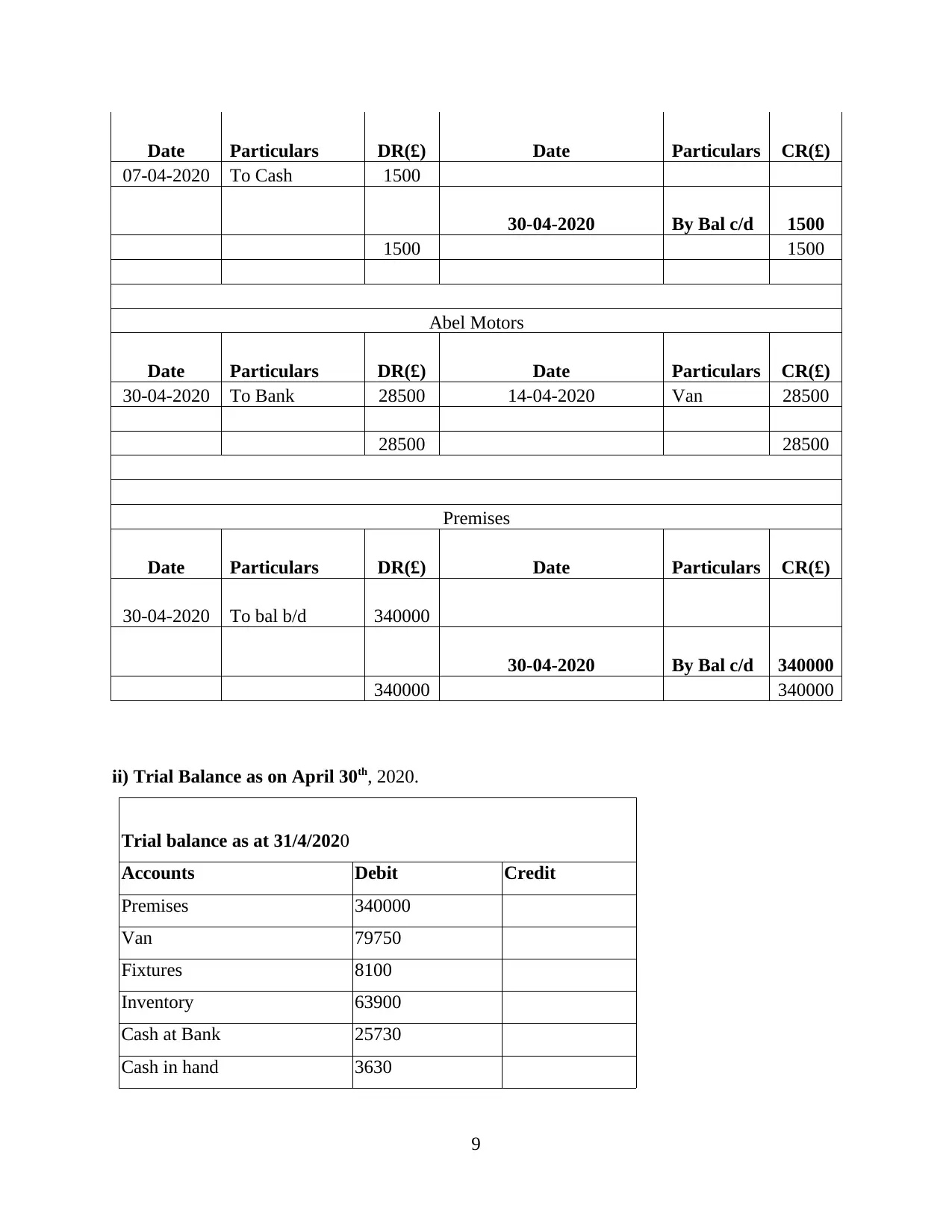

Date Particulars DR(£) Date Particulars CR(£)

07-04-2020 To Cash 1500

30-04-2020 By Bal c/d 1500

1500 1500

Abel Motors

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To Bank 28500 14-04-2020 Van 28500

28500 28500

Premises

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To bal b/d 340000

30-04-2020 By Bal c/d 340000

340000 340000

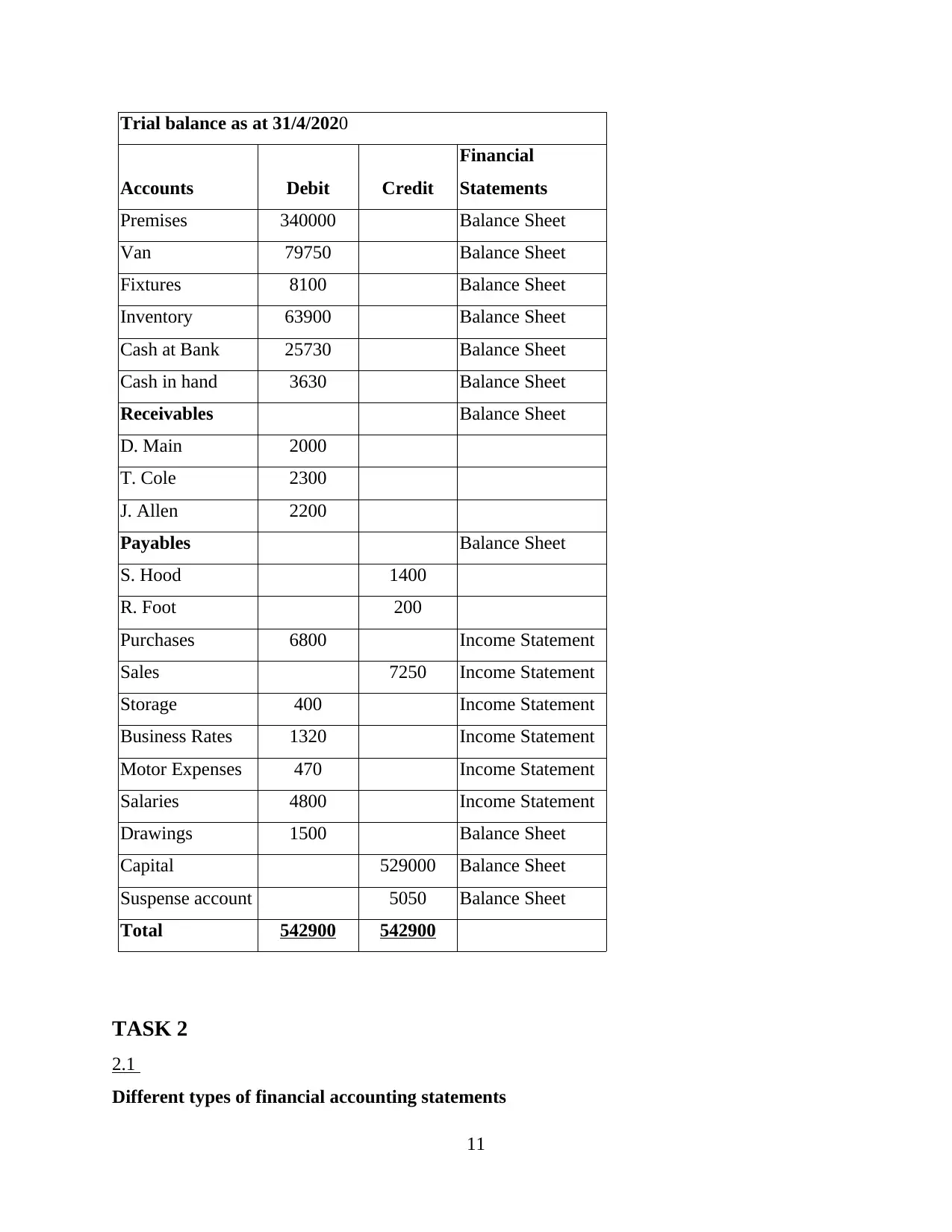

ii) Trial Balance as on April 30th, 2020.

Trial balance as at 31/4/2020

Accounts Debit Credit

Premises 340000

Van 79750

Fixtures 8100

Inventory 63900

Cash at Bank 25730

Cash in hand 3630

9

07-04-2020 To Cash 1500

30-04-2020 By Bal c/d 1500

1500 1500

Abel Motors

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To Bank 28500 14-04-2020 Van 28500

28500 28500

Premises

Date Particulars DR(£) Date Particulars CR(£)

30-04-2020 To bal b/d 340000

30-04-2020 By Bal c/d 340000

340000 340000

ii) Trial Balance as on April 30th, 2020.

Trial balance as at 31/4/2020

Accounts Debit Credit

Premises 340000

Van 79750

Fixtures 8100

Inventory 63900

Cash at Bank 25730

Cash in hand 3630

9

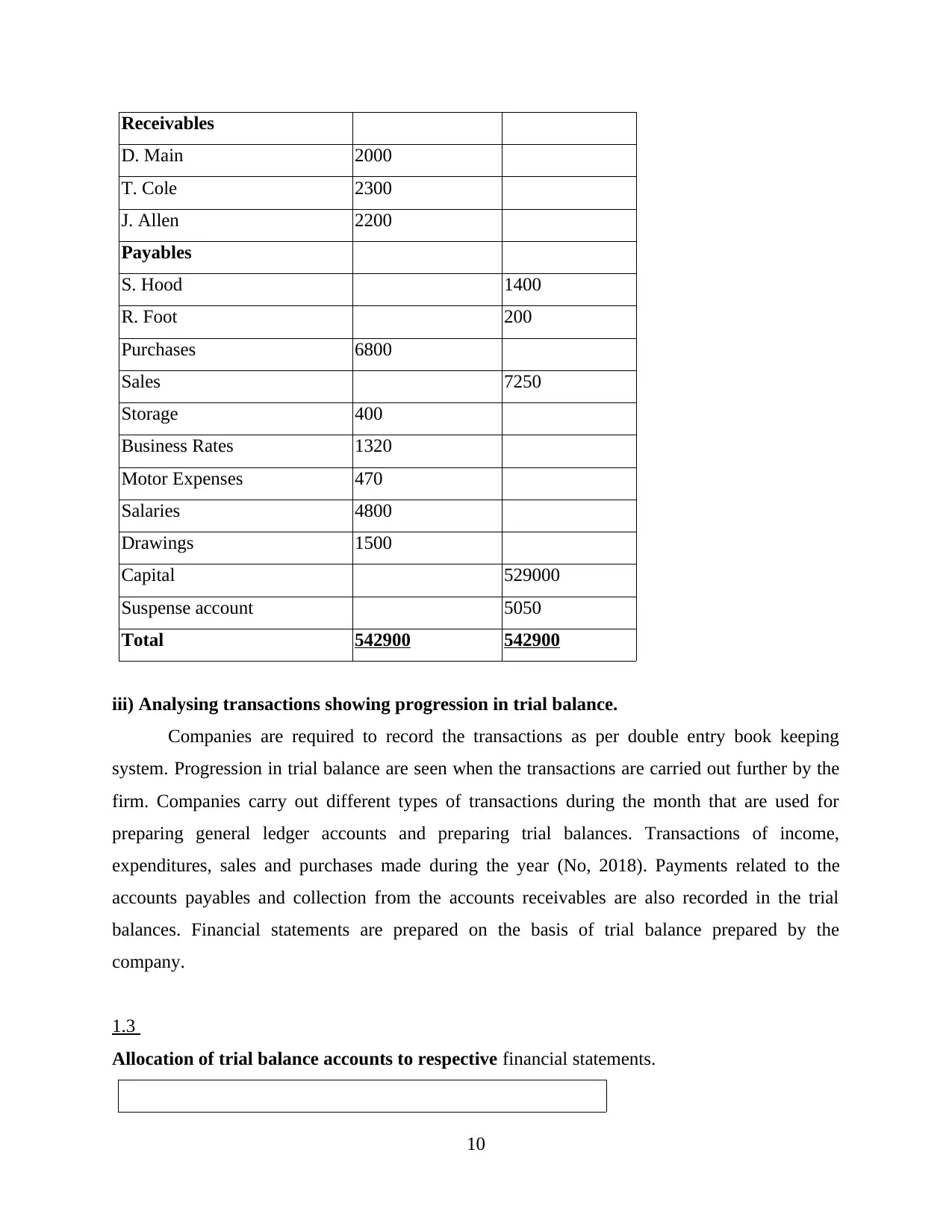

Receivables

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables

S. Hood 1400

R. Foot 200

Purchases 6800

Sales 7250

Storage 400

Business Rates 1320

Motor Expenses 470

Salaries 4800

Drawings 1500

Capital 529000

Suspense account 5050

Total 542900 542900

iii) Analysing transactions showing progression in trial balance.

Companies are required to record the transactions as per double entry book keeping

system. Progression in trial balance are seen when the transactions are carried out further by the

firm. Companies carry out different types of transactions during the month that are used for

preparing general ledger accounts and preparing trial balances. Transactions of income,

expenditures, sales and purchases made during the year (No, 2018). Payments related to the

accounts payables and collection from the accounts receivables are also recorded in the trial

balances. Financial statements are prepared on the basis of trial balance prepared by the

company.

1.3

Allocation of trial balance accounts to respective financial statements.

10

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables

S. Hood 1400

R. Foot 200

Purchases 6800

Sales 7250

Storage 400

Business Rates 1320

Motor Expenses 470

Salaries 4800

Drawings 1500

Capital 529000

Suspense account 5050

Total 542900 542900

iii) Analysing transactions showing progression in trial balance.

Companies are required to record the transactions as per double entry book keeping

system. Progression in trial balance are seen when the transactions are carried out further by the

firm. Companies carry out different types of transactions during the month that are used for

preparing general ledger accounts and preparing trial balances. Transactions of income,

expenditures, sales and purchases made during the year (No, 2018). Payments related to the

accounts payables and collection from the accounts receivables are also recorded in the trial

balances. Financial statements are prepared on the basis of trial balance prepared by the

company.

1.3

Allocation of trial balance accounts to respective financial statements.

10

Trial balance as at 31/4/2020

Accounts Debit Credit

Financial

Statements

Premises 340000 Balance Sheet

Van 79750 Balance Sheet

Fixtures 8100 Balance Sheet

Inventory 63900 Balance Sheet

Cash at Bank 25730 Balance Sheet

Cash in hand 3630 Balance Sheet

Receivables Balance Sheet

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables Balance Sheet

S. Hood 1400

R. Foot 200

Purchases 6800 Income Statement

Sales 7250 Income Statement

Storage 400 Income Statement

Business Rates 1320 Income Statement

Motor Expenses 470 Income Statement

Salaries 4800 Income Statement

Drawings 1500 Balance Sheet

Capital 529000 Balance Sheet

Suspense account 5050 Balance Sheet

Total 542900 542900

TASK 2

2.1

Different types of financial accounting statements

11

Accounts Debit Credit

Financial

Statements

Premises 340000 Balance Sheet

Van 79750 Balance Sheet

Fixtures 8100 Balance Sheet

Inventory 63900 Balance Sheet

Cash at Bank 25730 Balance Sheet

Cash in hand 3630 Balance Sheet

Receivables Balance Sheet

D. Main 2000

T. Cole 2300

J. Allen 2200

Payables Balance Sheet

S. Hood 1400

R. Foot 200

Purchases 6800 Income Statement

Sales 7250 Income Statement

Storage 400 Income Statement

Business Rates 1320 Income Statement

Motor Expenses 470 Income Statement

Salaries 4800 Income Statement

Drawings 1500 Balance Sheet

Capital 529000 Balance Sheet

Suspense account 5050 Balance Sheet

Total 542900 542900

TASK 2

2.1

Different types of financial accounting statements

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

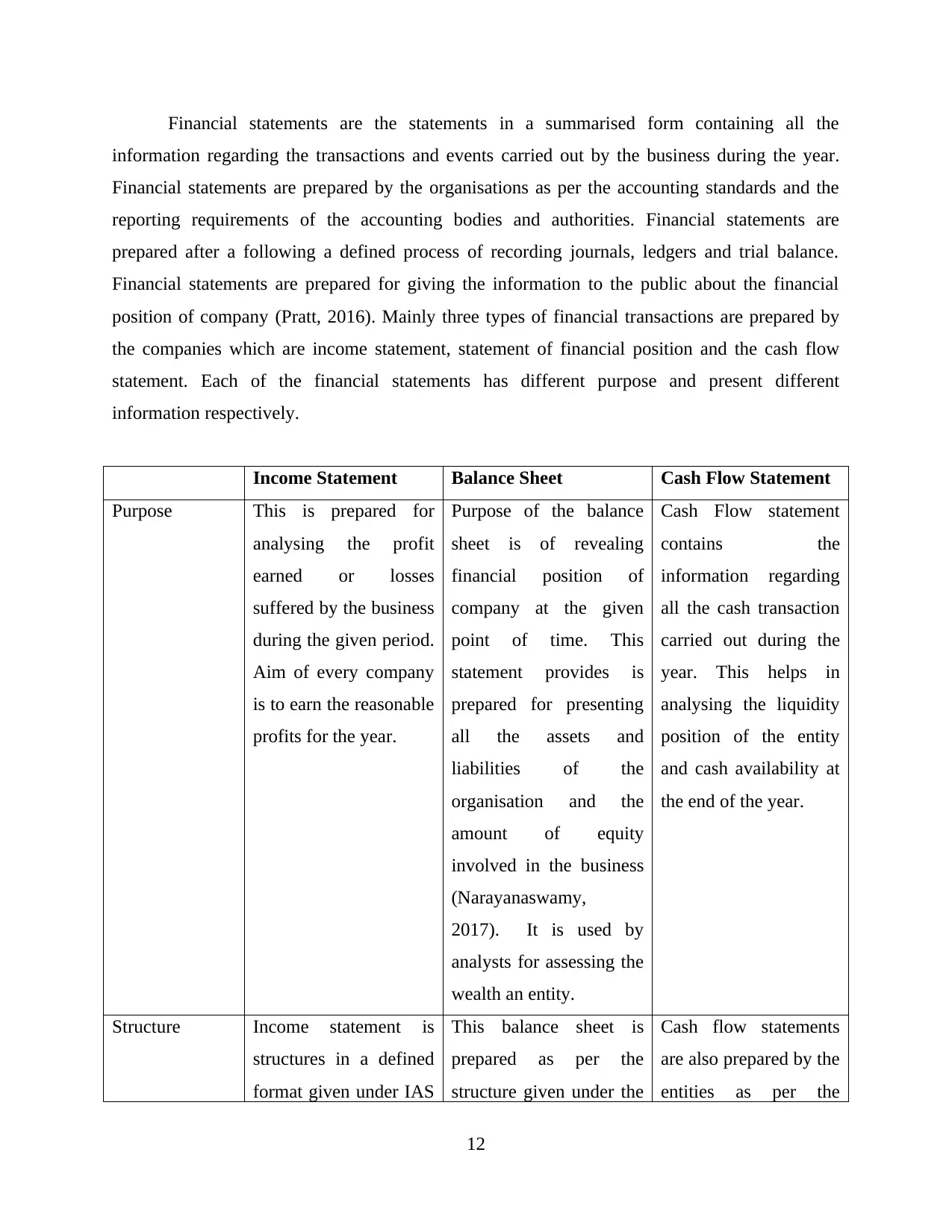

Financial statements are the statements in a summarised form containing all the

information regarding the transactions and events carried out by the business during the year.

Financial statements are prepared by the organisations as per the accounting standards and the

reporting requirements of the accounting bodies and authorities. Financial statements are

prepared after a following a defined process of recording journals, ledgers and trial balance.

Financial statements are prepared for giving the information to the public about the financial

position of company (Pratt, 2016). Mainly three types of financial transactions are prepared by

the companies which are income statement, statement of financial position and the cash flow

statement. Each of the financial statements has different purpose and present different

information respectively.

Income Statement Balance Sheet Cash Flow Statement

Purpose This is prepared for

analysing the profit

earned or losses

suffered by the business

during the given period.

Aim of every company

is to earn the reasonable

profits for the year.

Purpose of the balance

sheet is of revealing

financial position of

company at the given

point of time. This

statement provides is

prepared for presenting

all the assets and

liabilities of the

organisation and the

amount of equity

involved in the business

(Narayanaswamy,

2017). It is used by

analysts for assessing the

wealth an entity.

Cash Flow statement

contains the

information regarding

all the cash transaction

carried out during the

year. This helps in

analysing the liquidity

position of the entity

and cash availability at

the end of the year.

Structure Income statement is

structures in a defined

format given under IAS

This balance sheet is

prepared as per the

structure given under the

Cash flow statements

are also prepared by the

entities as per the

12

information regarding the transactions and events carried out by the business during the year.

Financial statements are prepared by the organisations as per the accounting standards and the

reporting requirements of the accounting bodies and authorities. Financial statements are

prepared after a following a defined process of recording journals, ledgers and trial balance.

Financial statements are prepared for giving the information to the public about the financial

position of company (Pratt, 2016). Mainly three types of financial transactions are prepared by

the companies which are income statement, statement of financial position and the cash flow

statement. Each of the financial statements has different purpose and present different

information respectively.

Income Statement Balance Sheet Cash Flow Statement

Purpose This is prepared for

analysing the profit

earned or losses

suffered by the business

during the given period.

Aim of every company

is to earn the reasonable

profits for the year.

Purpose of the balance

sheet is of revealing

financial position of

company at the given

point of time. This

statement provides is

prepared for presenting

all the assets and

liabilities of the

organisation and the

amount of equity

involved in the business

(Narayanaswamy,

2017). It is used by

analysts for assessing the

wealth an entity.

Cash Flow statement

contains the

information regarding

all the cash transaction

carried out during the

year. This helps in

analysing the liquidity

position of the entity

and cash availability at

the end of the year.

Structure Income statement is

structures in a defined

format given under IAS

This balance sheet is

prepared as per the

structure given under the

Cash flow statements

are also prepared by the

entities as per the

12

Presentation of

Financial Statement.

prescribed schedule of

IAS.

reporting requirements

of the accounting

boards (Warren and

Jones, 2018).

Content Income statement

contains the details

regarding all the

incomes earned and the

expenditures incurred

during the year. This

states all the

transactions that are

carried out during the

year (Cascino And

et.al., 2019). It contains

all the cash and non

cash expenses of the

company during the

year.

Balance sheet contains

assets that are sub

divided in current and

noncurrent assets.

Liabilities stating the

obligations of company

divided into current and

noncurrent liabilities.

Equity that contains the

equity capital and

retained earnings of the

company.

Cash flow statement

contains all the cash

inflows and outflows of

the entity for the given

time period. It provides

the cash flows from

operating activities,

investing and financing

activities. It contains

detailed information

about the cash flows of

the company.

2.2

Profit or Loss

statement in

accordance with IAS

for Italian Wines as on

March 31, 2020

13

Income Statement on the March 2020

Particulars Amount Amount

Continuing Operations

Revenue from operations 198000

Cost of good sold 100000

Gross Profits 98000

Distribution Cost 14000

Administrative Cost 24500

Salaries and Wages (2000+5500) 7500

Impairment

Property 6000

Motor Vehicle 1000 53000

Operating Profit 45000

Finance Cost 1500

Share of Net profits of joint ventures &

associates 0 1500

Profit Before Income Tax 43500

Income Tax Expense 9000

Net Income for Year 34500

Earnings per share 0.345

Financial Statement.

prescribed schedule of

IAS.

reporting requirements

of the accounting

boards (Warren and

Jones, 2018).

Content Income statement

contains the details

regarding all the

incomes earned and the

expenditures incurred

during the year. This

states all the

transactions that are

carried out during the

year (Cascino And

et.al., 2019). It contains

all the cash and non

cash expenses of the

company during the

year.

Balance sheet contains

assets that are sub

divided in current and

noncurrent assets.

Liabilities stating the

obligations of company

divided into current and

noncurrent liabilities.

Equity that contains the

equity capital and

retained earnings of the

company.

Cash flow statement

contains all the cash

inflows and outflows of

the entity for the given

time period. It provides

the cash flows from

operating activities,

investing and financing

activities. It contains

detailed information

about the cash flows of

the company.

2.2

Profit or Loss

statement in

accordance with IAS

for Italian Wines as on

March 31, 2020

13

Income Statement on the March 2020

Particulars Amount Amount

Continuing Operations

Revenue from operations 198000

Cost of good sold 100000

Gross Profits 98000

Distribution Cost 14000

Administrative Cost 24500

Salaries and Wages (2000+5500) 7500

Impairment

Property 6000

Motor Vehicle 1000 53000

Operating Profit 45000

Finance Cost 1500

Share of Net profits of joint ventures &

associates 0 1500

Profit Before Income Tax 43500

Income Tax Expense 9000

Net Income for Year 34500

Earnings per share 0.345

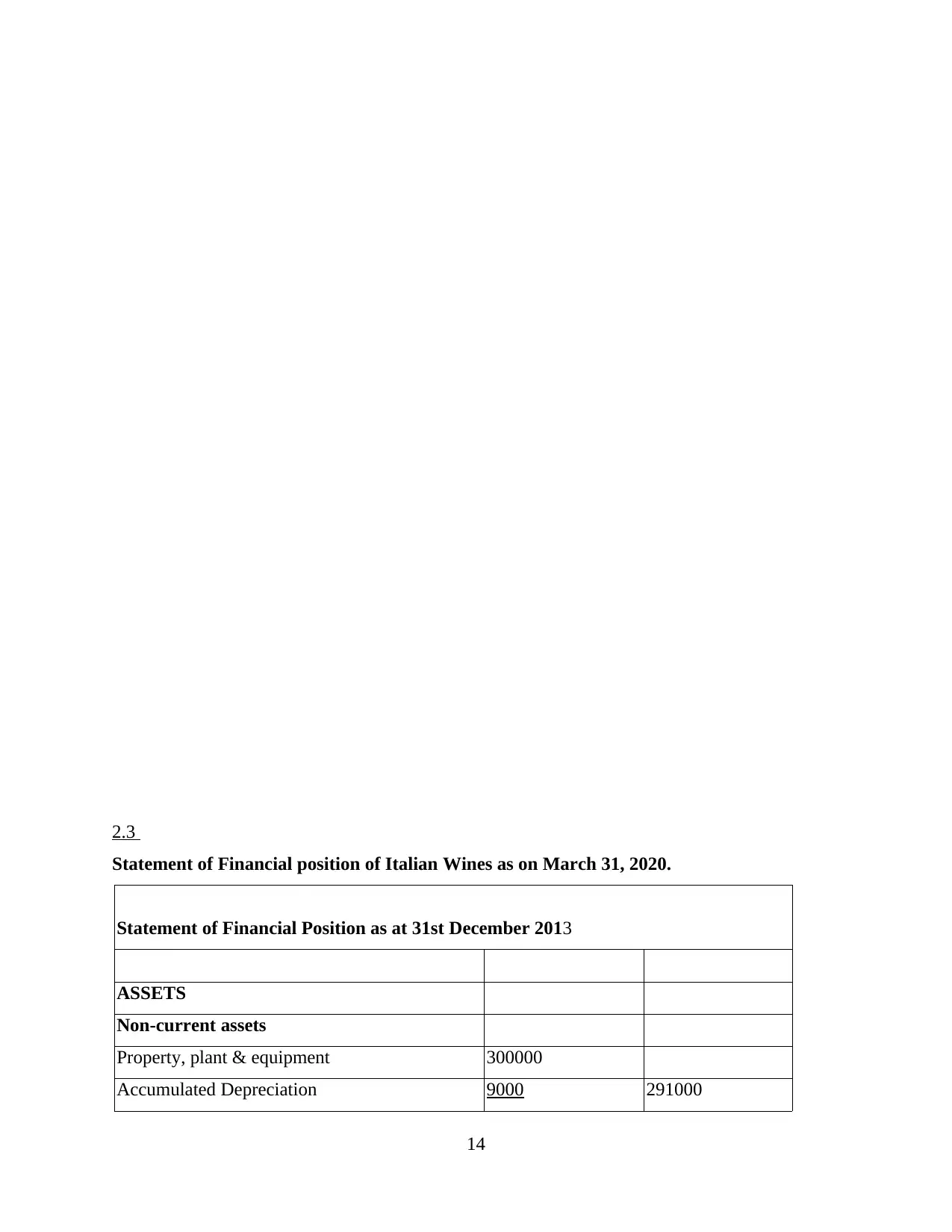

2.3

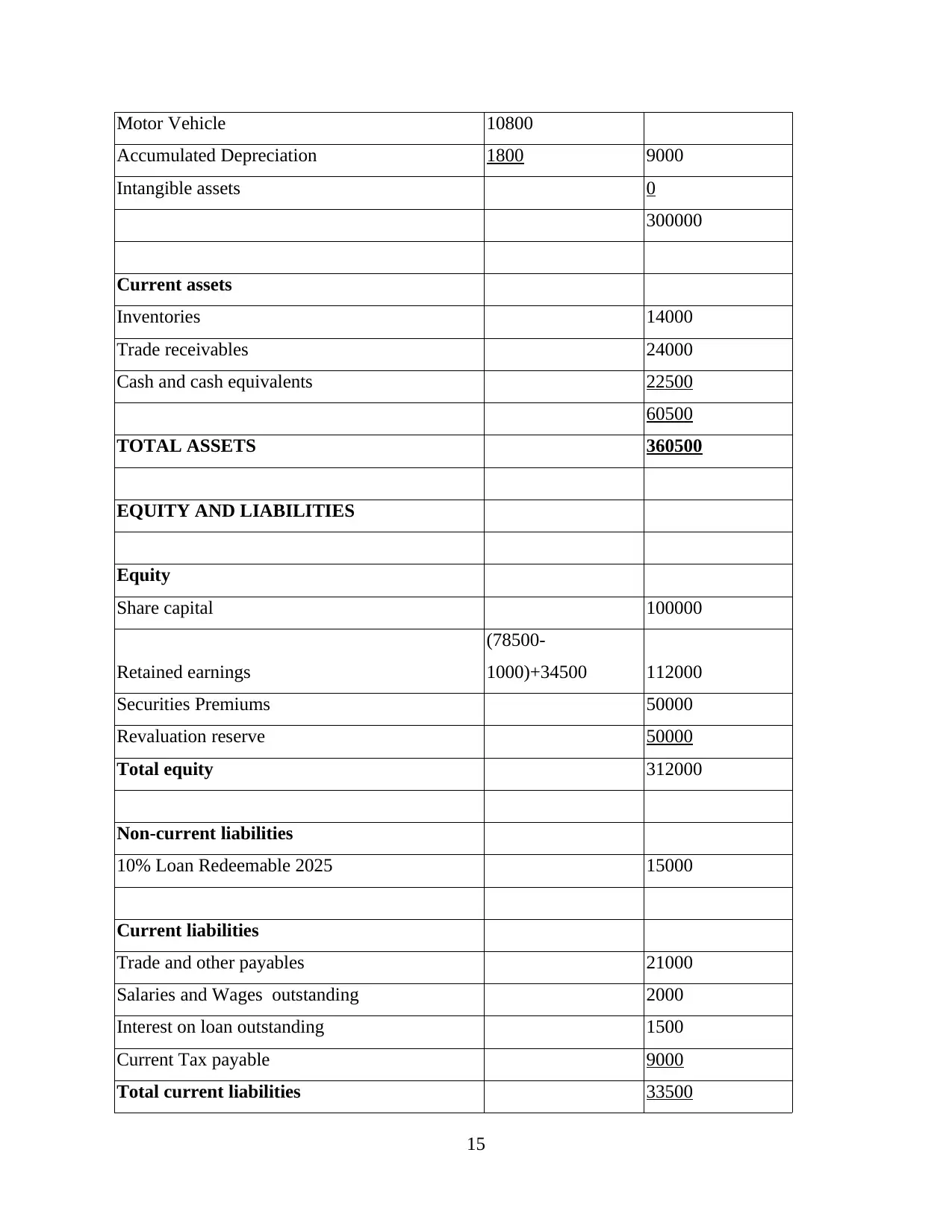

Statement of Financial position of Italian Wines as on March 31, 2020.

Statement of Financial Position as at 31st December 2013

ASSETS

Non-current assets

Property, plant & equipment 300000

Accumulated Depreciation 9000 291000

14

Statement of Financial position of Italian Wines as on March 31, 2020.

Statement of Financial Position as at 31st December 2013

ASSETS

Non-current assets

Property, plant & equipment 300000

Accumulated Depreciation 9000 291000

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Motor Vehicle 10800

Accumulated Depreciation 1800 9000

Intangible assets 0

300000

Current assets

Inventories 14000

Trade receivables 24000

Cash and cash equivalents 22500

60500

TOTAL ASSETS 360500

EQUITY AND LIABILITIES

Equity

Share capital 100000

Retained earnings

(78500-

1000)+34500 112000

Securities Premiums 50000

Revaluation reserve 50000

Total equity 312000

Non-current liabilities

10% Loan Redeemable 2025 15000

Current liabilities

Trade and other payables 21000

Salaries and Wages outstanding 2000

Interest on loan outstanding 1500

Current Tax payable 9000

Total current liabilities 33500

15

Accumulated Depreciation 1800 9000

Intangible assets 0

300000

Current assets

Inventories 14000

Trade receivables 24000

Cash and cash equivalents 22500

60500

TOTAL ASSETS 360500

EQUITY AND LIABILITIES

Equity

Share capital 100000

Retained earnings

(78500-

1000)+34500 112000

Securities Premiums 50000

Revaluation reserve 50000

Total equity 312000

Non-current liabilities

10% Loan Redeemable 2025 15000

Current liabilities

Trade and other payables 21000

Salaries and Wages outstanding 2000

Interest on loan outstanding 1500

Current Tax payable 9000

Total current liabilities 33500

15

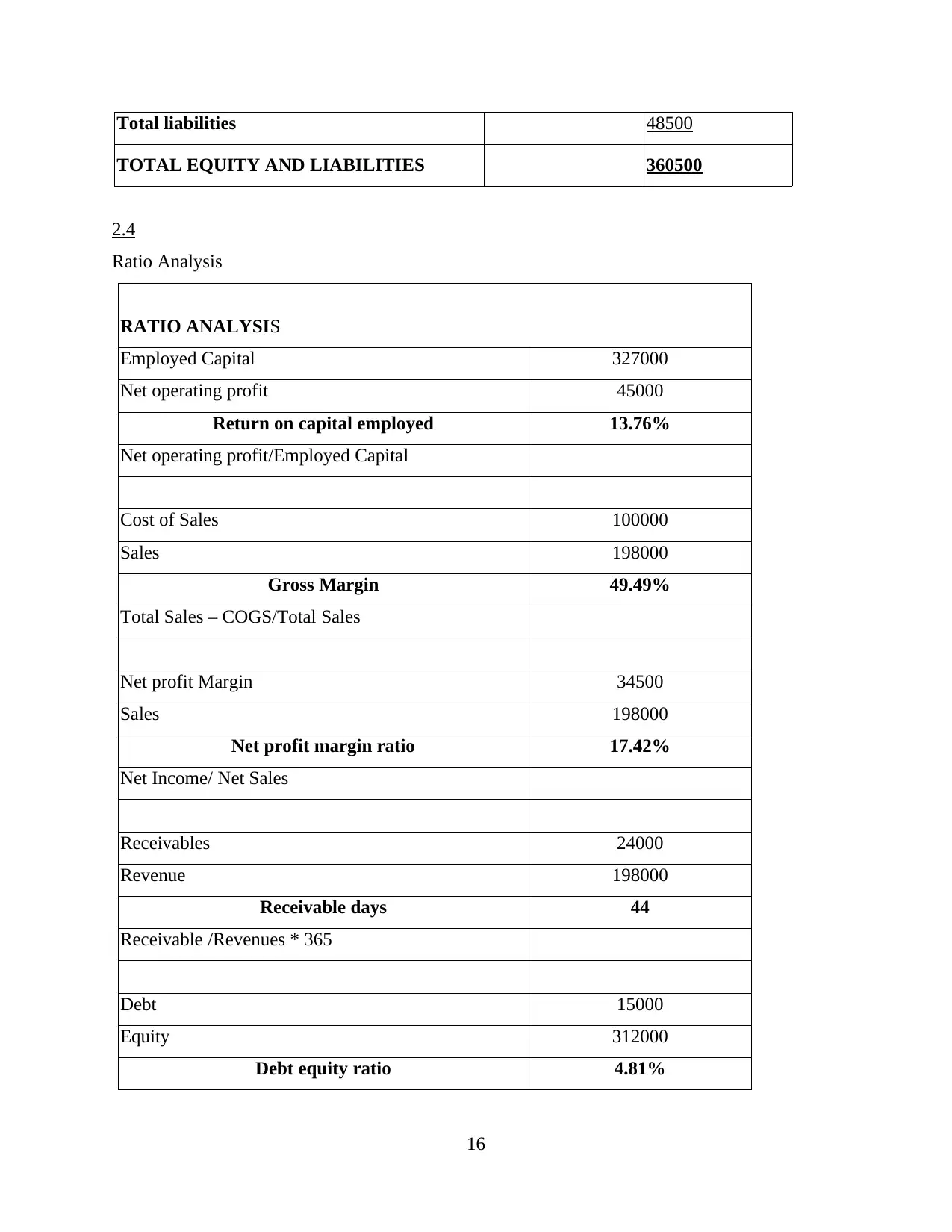

Total liabilities 48500

TOTAL EQUITY AND LIABILITIES 360500

2.4

Ratio Analysis

RATIO ANALYSIS

Employed Capital 327000

Net operating profit 45000

Return on capital employed 13.76%

Net operating profit/Employed Capital

Cost of Sales 100000

Sales 198000

Gross Margin 49.49%

Total Sales – COGS/Total Sales

Net profit Margin 34500

Sales 198000

Net profit margin ratio 17.42%

Net Income/ Net Sales

Receivables 24000

Revenue 198000

Receivable days 44

Receivable /Revenues * 365

Debt 15000

Equity 312000

Debt equity ratio 4.81%

16

TOTAL EQUITY AND LIABILITIES 360500

2.4

Ratio Analysis

RATIO ANALYSIS

Employed Capital 327000

Net operating profit 45000

Return on capital employed 13.76%

Net operating profit/Employed Capital

Cost of Sales 100000

Sales 198000

Gross Margin 49.49%

Total Sales – COGS/Total Sales

Net profit Margin 34500

Sales 198000

Net profit margin ratio 17.42%

Net Income/ Net Sales

Receivables 24000

Revenue 198000

Receivable days 44

Receivable /Revenues * 365

Debt 15000

Equity 312000

Debt equity ratio 4.81%

16

Debt/ Equity

TASK 3

3.1

Bank Reconciliation Statement

Purpose of Bank Reconciliation Statement

Bank Reconciliation statements refers to the summary of the banking as well as business

activity which reconciles the bank account of the entity with financial records. Reconciliation

statements outline withdrawals, deposits and other transaction affecting the bank account for the

specific period. Reconciliation statement is an internal control also used by the management in

indentifying frauds or errors carried out in the business regarding handling of cash. It is used by

business for correcting the mistakes of cash books by reconciling them with bank pass book. It

ensures that all the cash of the business is deposited on a timely manner in the banks and

payments made directly through banks are recorded in the book maintained by company (Biddle,

Ma. and Song, 2019). It helps the business to match the balances of company with that of bank

pass book. All fees that are charged by bank should be recorded in the cash book.

How this is achieved ?

This is achieved by preparing the reconciliation statement at respective intervals.

Management ensures that all the payments are processed at time and cash collection are also

deposited at time with the bank. The balances of the debit side of cash book are reconciled with

credit side of the pass book. The balance not appearing on the credit side of the pas book are

deducted back from the cash book. Similarly the credit side of the cash book is reconciled with

the debit side of cash book. Balances that are not appearing in the debit side are added back to

the cash book. Making adjustments for interest and bank charges not recorded in the cash books

of company. at the end of the reconciliation balance as per cash book should be same as per that

of the bank pass book.

Parties interested in the bank reconciliation statements.

Bank reconciliation is prepared for matching the balances as per bank pas book and cash

book so that the effect of every transaction is not left unrecorded or is having double effect.

Reconciliation provides evidence to the accuracy of financial figures to be stated in the financial

17

TASK 3

3.1

Bank Reconciliation Statement

Purpose of Bank Reconciliation Statement

Bank Reconciliation statements refers to the summary of the banking as well as business

activity which reconciles the bank account of the entity with financial records. Reconciliation

statements outline withdrawals, deposits and other transaction affecting the bank account for the

specific period. Reconciliation statement is an internal control also used by the management in

indentifying frauds or errors carried out in the business regarding handling of cash. It is used by

business for correcting the mistakes of cash books by reconciling them with bank pass book. It

ensures that all the cash of the business is deposited on a timely manner in the banks and

payments made directly through banks are recorded in the book maintained by company (Biddle,

Ma. and Song, 2019). It helps the business to match the balances of company with that of bank

pass book. All fees that are charged by bank should be recorded in the cash book.

How this is achieved ?

This is achieved by preparing the reconciliation statement at respective intervals.

Management ensures that all the payments are processed at time and cash collection are also

deposited at time with the bank. The balances of the debit side of cash book are reconciled with

credit side of the pass book. The balance not appearing on the credit side of the pas book are

deducted back from the cash book. Similarly the credit side of the cash book is reconciled with

the debit side of cash book. Balances that are not appearing in the debit side are added back to

the cash book. Making adjustments for interest and bank charges not recorded in the cash books

of company. at the end of the reconciliation balance as per cash book should be same as per that

of the bank pass book.

Parties interested in the bank reconciliation statements.

Bank reconciliation is prepared for matching the balances as per bank pas book and cash

book so that the effect of every transaction is not left unrecorded or is having double effect.

Reconciliation provides evidence to the accuracy of financial figures to be stated in the financial

17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements (Mullinova, 2016). Reconciliation of bank statements is required by the accounting

professional and management. Accounting professional are interested that the balance of both the

accounting is matching after making adjustments for all the unrecorded transactions.

Managements is interested in reconciliation statement for ensuring that the cash is deposited

timely in bank and no fraud is committed in handling the cash of entity.

3.2

Cash book showing correct balances.

CASH BOOK

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 5000

02/04/20 Green 5500 02/04/20 Rent – Miller 5000

05/04/20 Spencer Ltd 2500 08/04/20

Interest on

Debenture 2500

09/04/20 Cash 1500 15/04/20 PC World 6000

14/04/20 Capital – Jack 5000 20/04/20 Electricity 1800

20/04/20

Insurance

Claim 15000 21/04/20

Loan

Repayment 9200

25/04/20 Cash 8000 23/04/20 Legal Fees 4100

28/04/20 North Wings 5000 29/04/20 Salary :

30/04/20 Legal Fees 100 Amber 2000

Oshun 2500

Baker 2800

30/04/20 Bank Charges 100

30/04/20

Green (Cheque

Dishonoured ) 5500

30/04/20 Bal c/d 6100

47600 47600

18

professional and management. Accounting professional are interested that the balance of both the

accounting is matching after making adjustments for all the unrecorded transactions.

Managements is interested in reconciliation statement for ensuring that the cash is deposited

timely in bank and no fraud is committed in handling the cash of entity.

3.2

Cash book showing correct balances.

CASH BOOK

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 To bal b/d 5000

02/04/20 Green 5500 02/04/20 Rent – Miller 5000

05/04/20 Spencer Ltd 2500 08/04/20

Interest on

Debenture 2500

09/04/20 Cash 1500 15/04/20 PC World 6000

14/04/20 Capital – Jack 5000 20/04/20 Electricity 1800

20/04/20

Insurance

Claim 15000 21/04/20

Loan

Repayment 9200

25/04/20 Cash 8000 23/04/20 Legal Fees 4100

28/04/20 North Wings 5000 29/04/20 Salary :

30/04/20 Legal Fees 100 Amber 2000

Oshun 2500

Baker 2800

30/04/20 Bank Charges 100

30/04/20

Green (Cheque

Dishonoured ) 5500

30/04/20 Bal c/d 6100

47600 47600

18

3.3

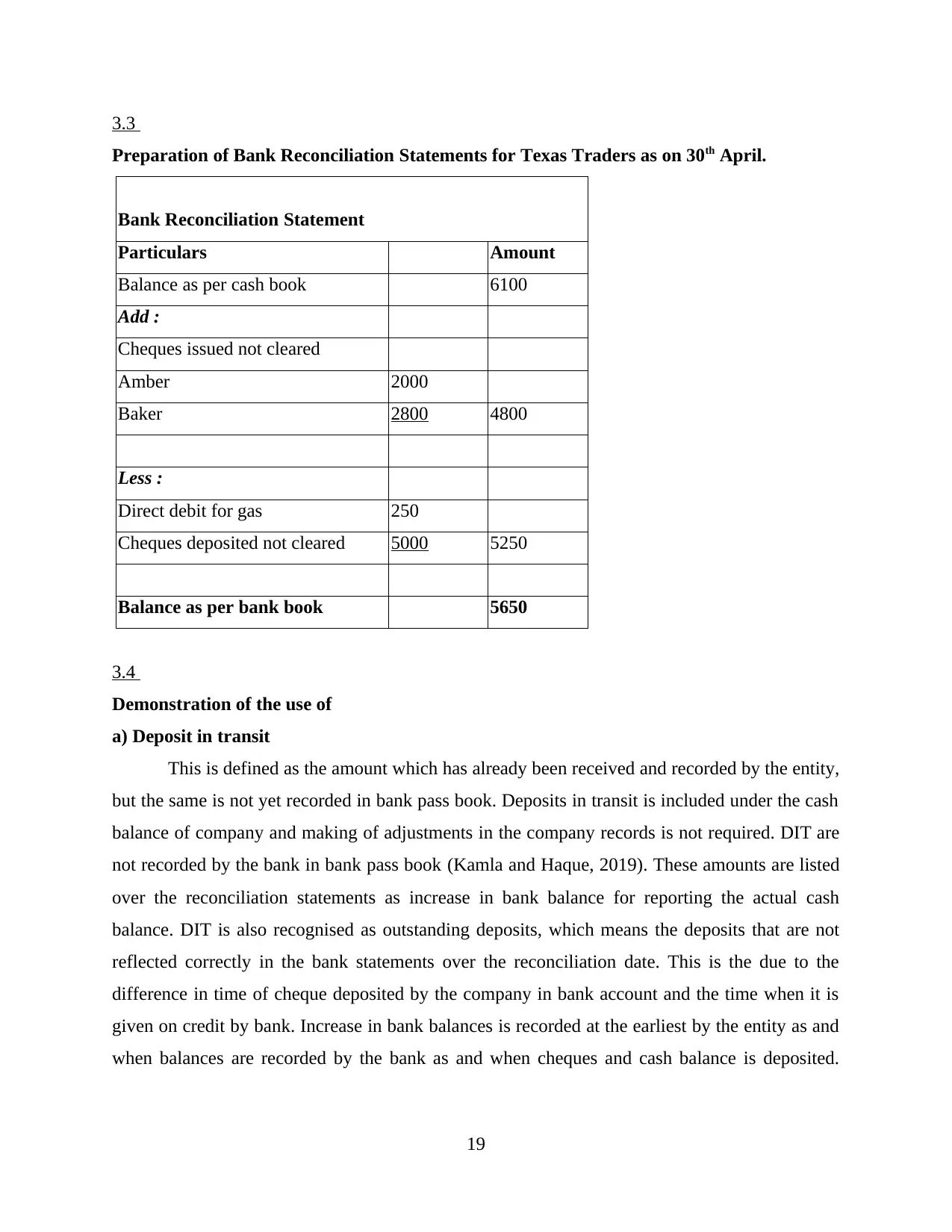

Preparation of Bank Reconciliation Statements for Texas Traders as on 30th April.

Bank Reconciliation Statement

Particulars Amount

Balance as per cash book 6100

Add :

Cheques issued not cleared

Amber 2000

Baker 2800 4800

Less :

Direct debit for gas 250

Cheques deposited not cleared 5000 5250

Balance as per bank book 5650

3.4

Demonstration of the use of

a) Deposit in transit

This is defined as the amount which has already been received and recorded by the entity,

but the same is not yet recorded in bank pass book. Deposits in transit is included under the cash

balance of company and making of adjustments in the company records is not required. DIT are

not recorded by the bank in bank pass book (Kamla and Haque, 2019). These amounts are listed

over the reconciliation statements as increase in bank balance for reporting the actual cash

balance. DIT is also recognised as outstanding deposits, which means the deposits that are not

reflected correctly in the bank statements over the reconciliation date. This is the due to the

difference in time of cheque deposited by the company in bank account and the time when it is

given on credit by bank. Increase in bank balances is recorded at the earliest by the entity as and

when balances are recorded by the bank as and when cheques and cash balance is deposited.

19

Preparation of Bank Reconciliation Statements for Texas Traders as on 30th April.

Bank Reconciliation Statement

Particulars Amount

Balance as per cash book 6100

Add :

Cheques issued not cleared

Amber 2000

Baker 2800 4800

Less :

Direct debit for gas 250

Cheques deposited not cleared 5000 5250

Balance as per bank book 5650

3.4

Demonstration of the use of

a) Deposit in transit

This is defined as the amount which has already been received and recorded by the entity,

but the same is not yet recorded in bank pass book. Deposits in transit is included under the cash

balance of company and making of adjustments in the company records is not required. DIT are

not recorded by the bank in bank pass book (Kamla and Haque, 2019). These amounts are listed

over the reconciliation statements as increase in bank balance for reporting the actual cash

balance. DIT is also recognised as outstanding deposits, which means the deposits that are not

reflected correctly in the bank statements over the reconciliation date. This is the due to the

difference in time of cheque deposited by the company in bank account and the time when it is

given on credit by bank. Increase in bank balances is recorded at the earliest by the entity as and

when balances are recorded by the bank as and when cheques and cash balance is deposited.

19

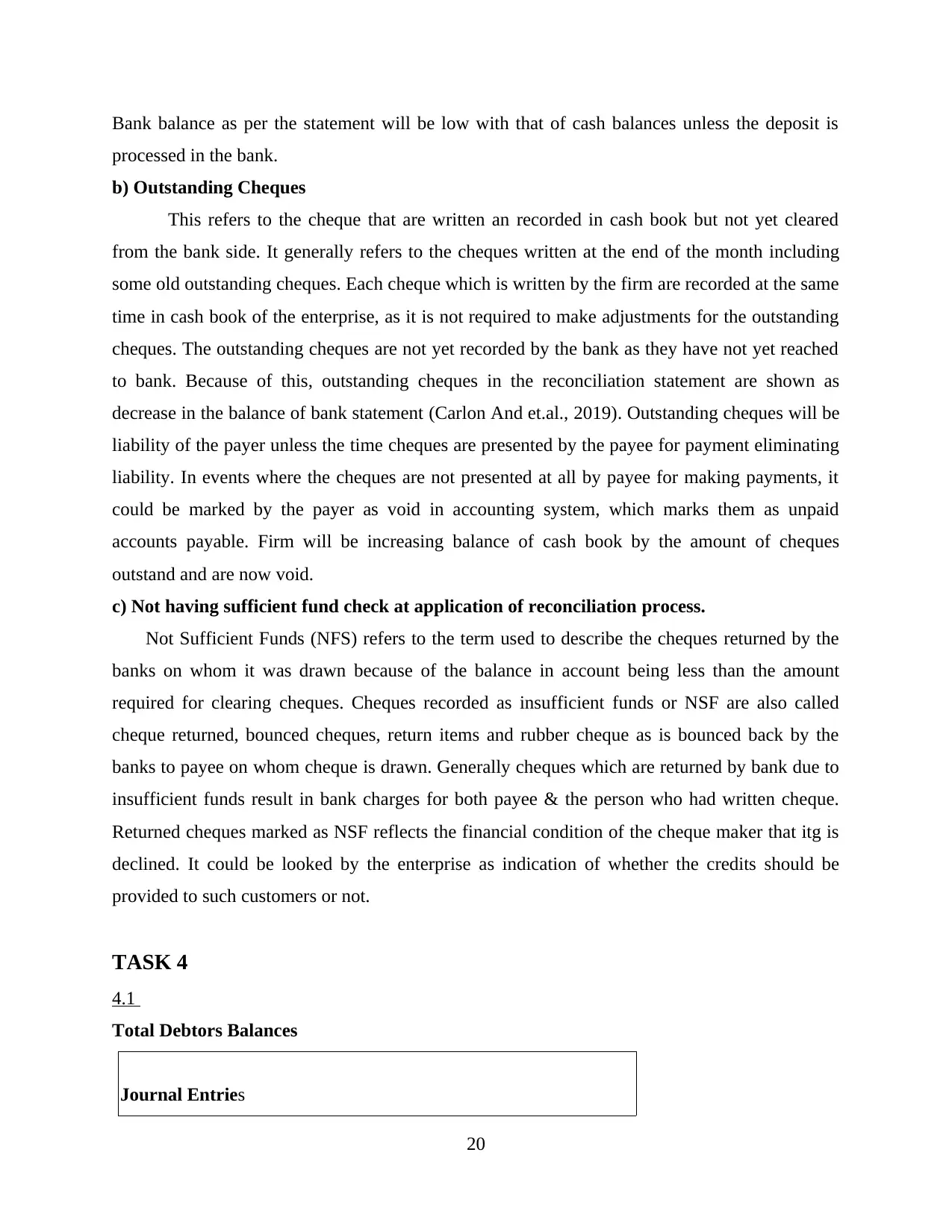

Bank balance as per the statement will be low with that of cash balances unless the deposit is

processed in the bank.

b) Outstanding Cheques

This refers to the cheque that are written an recorded in cash book but not yet cleared

from the bank side. It generally refers to the cheques written at the end of the month including

some old outstanding cheques. Each cheque which is written by the firm are recorded at the same

time in cash book of the enterprise, as it is not required to make adjustments for the outstanding

cheques. The outstanding cheques are not yet recorded by the bank as they have not yet reached

to bank. Because of this, outstanding cheques in the reconciliation statement are shown as

decrease in the balance of bank statement (Carlon And et.al., 2019). Outstanding cheques will be

liability of the payer unless the time cheques are presented by the payee for payment eliminating

liability. In events where the cheques are not presented at all by payee for making payments, it

could be marked by the payer as void in accounting system, which marks them as unpaid

accounts payable. Firm will be increasing balance of cash book by the amount of cheques

outstand and are now void.

c) Not having sufficient fund check at application of reconciliation process.

Not Sufficient Funds (NFS) refers to the term used to describe the cheques returned by the

banks on whom it was drawn because of the balance in account being less than the amount

required for clearing cheques. Cheques recorded as insufficient funds or NSF are also called

cheque returned, bounced cheques, return items and rubber cheque as is bounced back by the

banks to payee on whom cheque is drawn. Generally cheques which are returned by bank due to

insufficient funds result in bank charges for both payee & the person who had written cheque.

Returned cheques marked as NSF reflects the financial condition of the cheque maker that itg is

declined. It could be looked by the enterprise as indication of whether the credits should be

provided to such customers or not.

TASK 4

4.1

Total Debtors Balances

Journal Entries

20

processed in the bank.

b) Outstanding Cheques

This refers to the cheque that are written an recorded in cash book but not yet cleared

from the bank side. It generally refers to the cheques written at the end of the month including

some old outstanding cheques. Each cheque which is written by the firm are recorded at the same

time in cash book of the enterprise, as it is not required to make adjustments for the outstanding

cheques. The outstanding cheques are not yet recorded by the bank as they have not yet reached

to bank. Because of this, outstanding cheques in the reconciliation statement are shown as

decrease in the balance of bank statement (Carlon And et.al., 2019). Outstanding cheques will be

liability of the payer unless the time cheques are presented by the payee for payment eliminating

liability. In events where the cheques are not presented at all by payee for making payments, it

could be marked by the payer as void in accounting system, which marks them as unpaid

accounts payable. Firm will be increasing balance of cash book by the amount of cheques

outstand and are now void.

c) Not having sufficient fund check at application of reconciliation process.

Not Sufficient Funds (NFS) refers to the term used to describe the cheques returned by the

banks on whom it was drawn because of the balance in account being less than the amount

required for clearing cheques. Cheques recorded as insufficient funds or NSF are also called

cheque returned, bounced cheques, return items and rubber cheque as is bounced back by the

banks to payee on whom cheque is drawn. Generally cheques which are returned by bank due to

insufficient funds result in bank charges for both payee & the person who had written cheque.

Returned cheques marked as NSF reflects the financial condition of the cheque maker that itg is

declined. It could be looked by the enterprise as indication of whether the credits should be

provided to such customers or not.

TASK 4

4.1

Total Debtors Balances

Journal Entries

20

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Suspense account 9000

To Customer 9000

Customer 250

To Delivery payment 250

Sales Day Book 1600

To Suspense 1600

Debtor Control Account 6800

To Suspense 6800

Sales ledger control account 8200

To Purchases ledger control

account 8200

4.2

Statements of Reconciliation of Sales with the balances in the Debtors Control Account.

Debtors Control account

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 Balance b/d 276800

30/04/20

Debtors

(SDB) 9000

Bank 6800 Sales 1600

30/04/20

By balance

b/d 273000

283600 283600

21

To Customer 9000

Customer 250

To Delivery payment 250

Sales Day Book 1600

To Suspense 1600

Debtor Control Account 6800

To Suspense 6800

Sales ledger control account 8200

To Purchases ledger control

account 8200

4.2

Statements of Reconciliation of Sales with the balances in the Debtors Control Account.

Debtors Control account

Date Particulars DR(£) Date Particulars CR(£)

01/04/20 Balance b/d 276800

30/04/20

Debtors

(SDB) 9000

Bank 6800 Sales 1600

30/04/20

By balance

b/d 273000

283600 283600

21

Reconciliation statement.

Reconciliation of Sales Ledger with Debtor Control Account

Balances of sales 176800

Adjustment of errors 3800

Revised Total agreeing with control account 173000

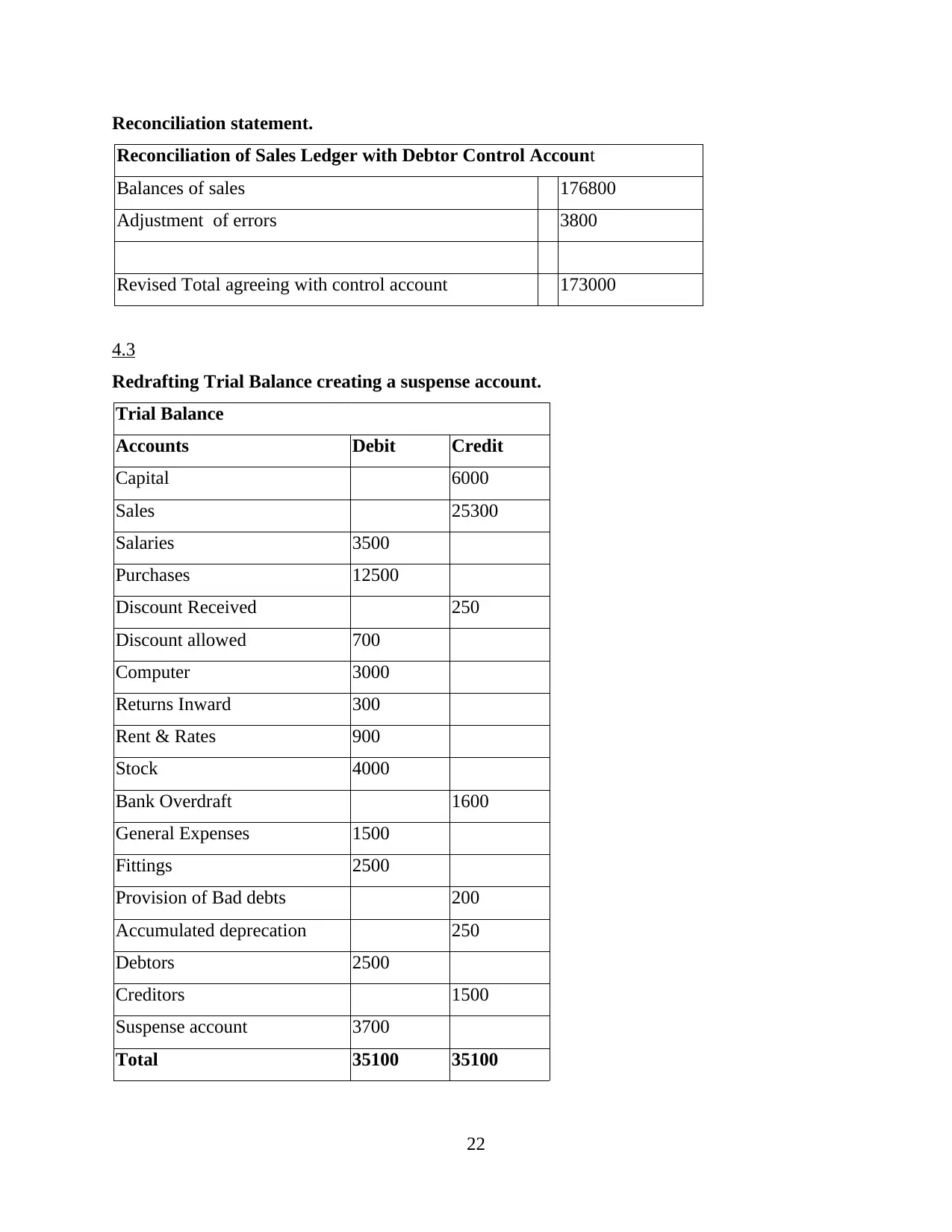

4.3

Redrafting Trial Balance creating a suspense account.

Trial Balance

Accounts Debit Credit

Capital 6000

Sales 25300

Salaries 3500

Purchases 12500

Discount Received 250

Discount allowed 700

Computer 3000

Returns Inward 300

Rent & Rates 900

Stock 4000

Bank Overdraft 1600

General Expenses 1500

Fittings 2500

Provision of Bad debts 200

Accumulated deprecation 250

Debtors 2500

Creditors 1500

Suspense account 3700

Total 35100 35100

22

Reconciliation of Sales Ledger with Debtor Control Account

Balances of sales 176800

Adjustment of errors 3800

Revised Total agreeing with control account 173000

4.3

Redrafting Trial Balance creating a suspense account.

Trial Balance

Accounts Debit Credit

Capital 6000

Sales 25300

Salaries 3500

Purchases 12500

Discount Received 250

Discount allowed 700

Computer 3000

Returns Inward 300

Rent & Rates 900

Stock 4000

Bank Overdraft 1600

General Expenses 1500

Fittings 2500

Provision of Bad debts 200

Accumulated deprecation 250

Debtors 2500

Creditors 1500

Suspense account 3700

Total 35100 35100

22

4.4

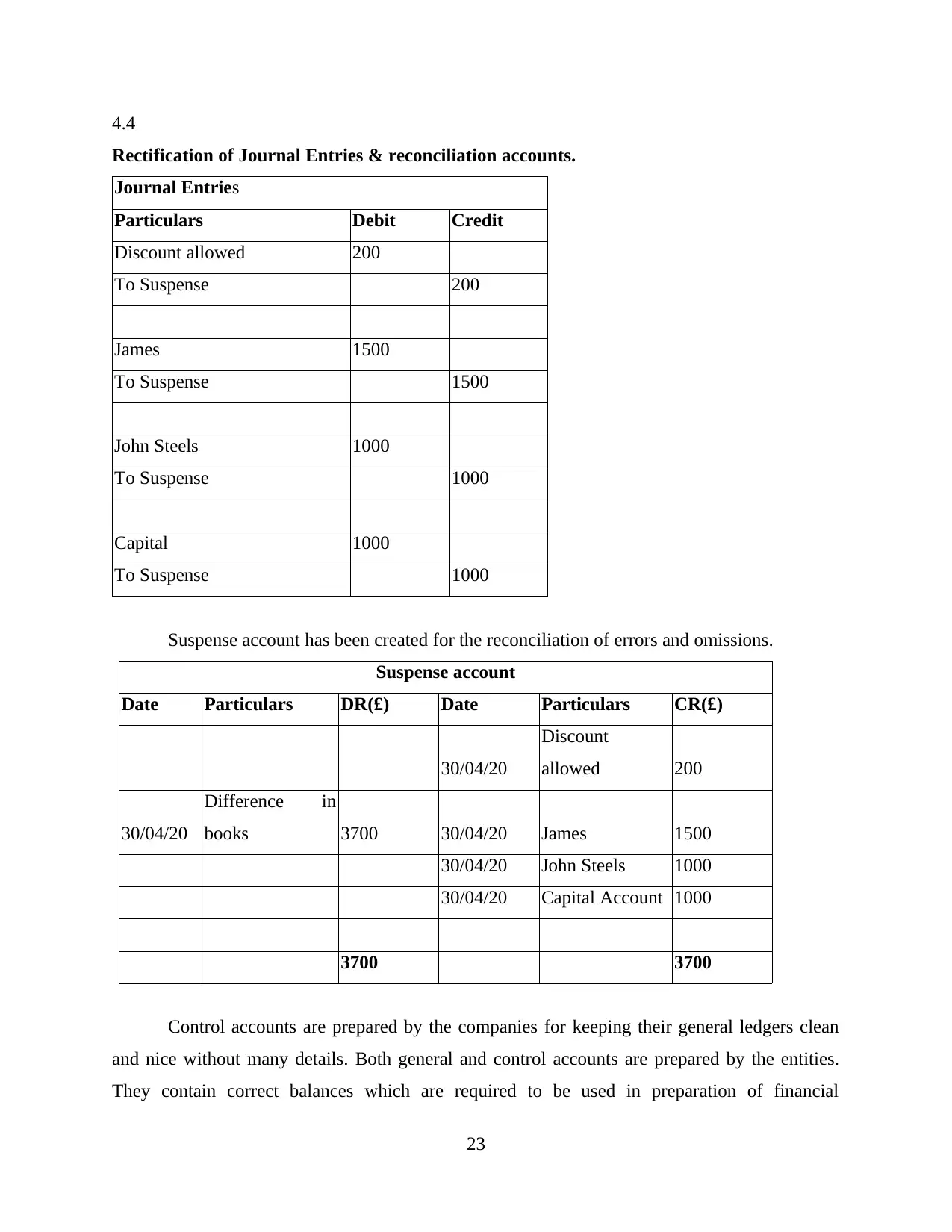

Rectification of Journal Entries & reconciliation accounts.

Journal Entries

Particulars Debit Credit

Discount allowed 200

To Suspense 200

James 1500

To Suspense 1500

John Steels 1000

To Suspense 1000

Capital 1000

To Suspense 1000

Suspense account has been created for the reconciliation of errors and omissions.

Suspense account

Date Particulars DR(£) Date Particulars CR(£)

30/04/20

Discount

allowed 200

30/04/20

Difference in

books 3700 30/04/20 James 1500

30/04/20 John Steels 1000

30/04/20 Capital Account 1000

3700 3700

Control accounts are prepared by the companies for keeping their general ledgers clean

and nice without many details. Both general and control accounts are prepared by the entities.

They contain correct balances which are required to be used in preparation of financial

23

Rectification of Journal Entries & reconciliation accounts.

Journal Entries

Particulars Debit Credit

Discount allowed 200

To Suspense 200

James 1500

To Suspense 1500

John Steels 1000

To Suspense 1000

Capital 1000

To Suspense 1000

Suspense account has been created for the reconciliation of errors and omissions.

Suspense account

Date Particulars DR(£) Date Particulars CR(£)

30/04/20

Discount

allowed 200

30/04/20

Difference in

books 3700 30/04/20 James 1500

30/04/20 John Steels 1000

30/04/20 Capital Account 1000

3700 3700

Control accounts are prepared by the companies for keeping their general ledgers clean

and nice without many details. Both general and control accounts are prepared by the entities.

They contain correct balances which are required to be used in preparation of financial

23

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statements. Control accounts are prepared for more accuracy of the financial transactions carried

out by the business enterprise. It helps the accountants in finding out errors and mistakes in the

balances and accounts by making comparison with purchase or sales ledger on periodic basis. It

is also used for keeping internal check over the transactions of entities. Using control accounts

debtors and creditor balance could be more easily identified for preparation of trial balances and

balance sheet (Warren, Jonick and Schneider, 2020). Control accounts enable the accountants in

preparing the accounts required under double entry system. Companies using these accounts are

more accurately making adjustments in the different records and accounts. Under the control

accounts different types of accounts are prepared such as purchase ledger, sales ledger, debtor

control account and many more.

CONCLUSIONS

It could be concluded from the above report that financial accounting refers to the core

branch of accounting giving base to the enterprise and its accounting transactions. Financial

accounting helps the business enterprise in recording all the business transactions accurately and

as per required accounting standard and reporting frameworks. Transactions are recorded under

the financial accounting as per the double entry system of book keeping. It ensures the company

to follow universally acceptable accounting principles. This gives the procedure of recording

business transaction from journal entries to the preparation of financial statements. It has also

provided the understanding about the preparation of bank reconciliation statements and different

control accounts.

24

out by the business enterprise. It helps the accountants in finding out errors and mistakes in the

balances and accounts by making comparison with purchase or sales ledger on periodic basis. It

is also used for keeping internal check over the transactions of entities. Using control accounts

debtors and creditor balance could be more easily identified for preparation of trial balances and

balance sheet (Warren, Jonick and Schneider, 2020). Control accounts enable the accountants in

preparing the accounts required under double entry system. Companies using these accounts are

more accurately making adjustments in the different records and accounts. Under the control

accounts different types of accounts are prepared such as purchase ledger, sales ledger, debtor

control account and many more.

CONCLUSIONS

It could be concluded from the above report that financial accounting refers to the core

branch of accounting giving base to the enterprise and its accounting transactions. Financial

accounting helps the business enterprise in recording all the business transactions accurately and

as per required accounting standard and reporting frameworks. Transactions are recorded under

the financial accounting as per the double entry system of book keeping. It ensures the company

to follow universally acceptable accounting principles. This gives the procedure of recording

business transaction from journal entries to the preparation of financial statements. It has also

provided the understanding about the preparation of bank reconciliation statements and different

control accounts.

24

REFERENCES

Books and Journals

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

No, A.S., 2018. Conceptual framework for financial reporting. Norwalk, CT: FASB.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Cascino, S. And et.al., 2019. The usefulness of financial accounting information: Evidence from

the field. Available at SSRN 3008083.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2018. Financial accounting: tools for business

decision making. John Wiley & Sons.

Biddle, G.C., Ma, M.L. and Song, F.M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-

64.

Kamla, R. and Haque, F., 2019. Islamic accounting, neo-imperialism and identity staging: The

Accounting and Auditing Organization for Islamic Financial Institutions. Critical

Perspectives on Accounting. 63.p.102000.

Carlon, S. And et.al., 2019. Financial accounting: Reporting, analysis and decision making.

John Wiley and Sons Australia.

Warren, C., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

25

Books and Journals

Schroeder, R.G., Clark, M.W. and Cathey, J.M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

No, A.S., 2018. Conceptual framework for financial reporting. Norwalk, CT: FASB.

Pratt, J., 2016. Financial accounting in an economic context. John Wiley & Sons.

Narayanaswamy, R., 2017. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Warren, C. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Cascino, S. And et.al., 2019. The usefulness of financial accounting information: Evidence from

the field. Available at SSRN 3008083.

Kimmel, P.D., Weygandt, J.J. and Kieso, D.E., 2018. Financial accounting: tools for business

decision making. John Wiley & Sons.

Biddle, G.C., Ma, M.L. and Song, F.M., 2019. Accounting conservatism and bankruptcy

risk. Available at SSRN 1621272.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments: recognition

and assessment" for bank financial accounting. Modern European Researches, (1), pp.60-

64.

Kamla, R. and Haque, F., 2019. Islamic accounting, neo-imperialism and identity staging: The

Accounting and Auditing Organization for Islamic Financial Institutions. Critical

Perspectives on Accounting. 63.p.102000.

Carlon, S. And et.al., 2019. Financial accounting: Reporting, analysis and decision making.

John Wiley and Sons Australia.

Warren, C., Jonick, C. and Schneider, J., 2020. Financial accounting. Cengage Learning.

25

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.