Financial Accounting: Double Entry, Final Accounts and Reconciliation

VerifiedAdded on 2024/06/03

|19

|3448

|463

Report

AI Summary

This assignment solution delves into the core concepts of financial accounting, starting with the application of the double-entry book-keeping system, including recording sales and purchases in a general ledger and producing a trial balance. It then progresses to preparing final accounts from given trial balance figures, adjusting for accruals, depreciation, and prepayments, with examples covering sole-traders, partnerships, and limited companies. The assignment further explores the bank reconciliation process and explains the reconciliation of control accounts, along with clearing suspense accounts using practical examples. This comprehensive overview provides a solid foundation in essential financial accounting principles and practices.

Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1:.............................................................................................................................................3

P1: Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger...................................................................................3

P2: Produce a trial balance applying the use of the balance of rule to complete the ledger........6

Task 2:.............................................................................................................................................7

P3: Prepare final accounts from given trial balance figures adjusting for accruals, depreciation

and prepayments..........................................................................................................................7

P4 Produce final accounts for a range of example that include sole-traders, partnerships or

limited companies......................................................................................................................10

Task 3:...........................................................................................................................................14

P5: Apply the bank reconciliation process to prepare a number of bank reconciliations..........14

Task 4.............................................................................................................................................16

P6 Explain the process taken to reconcile control accounts and clear suspense account using

account examples.......................................................................................................................16

References:....................................................................................................................................18

2

Task 1:.............................................................................................................................................3

P1: Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger...................................................................................3

P2: Produce a trial balance applying the use of the balance of rule to complete the ledger........6

Task 2:.............................................................................................................................................7

P3: Prepare final accounts from given trial balance figures adjusting for accruals, depreciation

and prepayments..........................................................................................................................7

P4 Produce final accounts for a range of example that include sole-traders, partnerships or

limited companies......................................................................................................................10

Task 3:...........................................................................................................................................14

P5: Apply the bank reconciliation process to prepare a number of bank reconciliations..........14

Task 4.............................................................................................................................................16

P6 Explain the process taken to reconcile control accounts and clear suspense account using

account examples.......................................................................................................................16

References:....................................................................................................................................18

2

Task 1:

P1: Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger

Business transaction: Any transactions in the business which is related to the accounting terms

such as income, expense, assets and capital. An event or an activity which is measured in

monetary terms and performs the functions and operates the business entity is known as a

business transaction. The business transaction shows the financial position of the company.

Types of a business transaction

Each transaction of a company is recorded in a journal entry by a source document.

Sales transaction: The transactions related to sales can be based on the cash, credit and advance

payment sale. It is an agreement between the two party’s buyer and seller, where the buyer

receives the goods and services on the security of a price. The sales transaction is credited in the

business while the cash is debited.

Purchase transaction: Purchase transactions are those transactions in which the cash is paid for

taking an acquisition of the asset. Purchase transactions include both cash and credit purchases.

Purchase transactions are debited in the business while the cash is credited.

Receipts transaction: This transaction is recorded in the business when the items are received

from the suppliers against our purchase order. The accounting of cash receipts is done as by

debiting the cash or the asset which is increasing.

Payment transaction: In this type of transaction the payment is made to customers, clients and

consumer in monetary terms. In payment account, the cash is credited. A payment is a

transaction in which the consumer pays the bills or deposits the money.

Regulations apply to financial accounting

The GAAP is followed for the accounting rules and regulation for financial reporting. GAAP is

used by the organisation to record the accounting information. It summarises the accounting

records into the financial statement. GAAP also helps in business by comparing the different

financial records such as assets, liabilities, equity, revenues, expenses, etc. Different accounting

standards have been adopted by the company for the proper recording of the financial records.

IFRS is also an accounting standard which helps the companies in disclosing the financial

statements.

Double entry and book keeping:

3

P1: Apply the double entry book-keeping system of debits and credits. Record sales and

purchases transactions in a general ledger

Business transaction: Any transactions in the business which is related to the accounting terms

such as income, expense, assets and capital. An event or an activity which is measured in

monetary terms and performs the functions and operates the business entity is known as a

business transaction. The business transaction shows the financial position of the company.

Types of a business transaction

Each transaction of a company is recorded in a journal entry by a source document.

Sales transaction: The transactions related to sales can be based on the cash, credit and advance

payment sale. It is an agreement between the two party’s buyer and seller, where the buyer

receives the goods and services on the security of a price. The sales transaction is credited in the

business while the cash is debited.

Purchase transaction: Purchase transactions are those transactions in which the cash is paid for

taking an acquisition of the asset. Purchase transactions include both cash and credit purchases.

Purchase transactions are debited in the business while the cash is credited.

Receipts transaction: This transaction is recorded in the business when the items are received

from the suppliers against our purchase order. The accounting of cash receipts is done as by

debiting the cash or the asset which is increasing.

Payment transaction: In this type of transaction the payment is made to customers, clients and

consumer in monetary terms. In payment account, the cash is credited. A payment is a

transaction in which the consumer pays the bills or deposits the money.

Regulations apply to financial accounting

The GAAP is followed for the accounting rules and regulation for financial reporting. GAAP is

used by the organisation to record the accounting information. It summarises the accounting

records into the financial statement. GAAP also helps in business by comparing the different

financial records such as assets, liabilities, equity, revenues, expenses, etc. Different accounting

standards have been adopted by the company for the proper recording of the financial records.

IFRS is also an accounting standard which helps the companies in disclosing the financial

statements.

Double entry and book keeping:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Double entry or book keeping is the transaction which involves two accounts. It generally means

the transaction is recorded two of its general ledger accounts. Debit side of the general leger

account should be equal to the credit side in double entry system.

Double entry recording in purchase: The transaction of purchase in double entry system affects

both buyer and seller. The cash balance of the buyer would decrease and the cash balance of

seller would increase.

Double entry recording in sales: Every transaction affects the two accounts and the financial

statement. Sales transaction also affects the two systems of buyer and seller. Firstly the company

will record the data in sales account and then enter in the customer’s account if the sales are done

on credit basis.

Double entry recording in cash disbursement: It records all the transactions which are related to

the cash payment and cash outflows. These transactions are recorded in the cash payment journal

and update the subsidiary ledgers also.

Double entry recording in cash receipts: Cash is coming in the business from customers so it will

also affect the two transactions. The one account will affect the cash account and other will

affect the accounts receivable.

Manual and electronic systems:

The manual accounting system is a system in which the company records the data manually by

hand or paper work. The electronic system is a system in which all the transactions of the

company are recorded by the computer in software. Manual recording is less expensive as a

comparison to electronic accounting. Electronic accounting records all the transactions in detail

such as expenses, payment, assets, etc. Electronic accounting has more security for the data and

also requires less storage. Less calculation is incurred as compare to manual accounting. There

are the chances of error in manual accounting but in the electronic system, the chances of fraud

and error are less (Amahalu, et.al, 2017).

Books of Accounts of Kristine

Capital Account

To Balance b/d 5000 By cash 5000

5000 5000

Car Account

To Cash 1000 By Balance b/d 1000

1000 1000

4

the transaction is recorded two of its general ledger accounts. Debit side of the general leger

account should be equal to the credit side in double entry system.

Double entry recording in purchase: The transaction of purchase in double entry system affects

both buyer and seller. The cash balance of the buyer would decrease and the cash balance of

seller would increase.

Double entry recording in sales: Every transaction affects the two accounts and the financial

statement. Sales transaction also affects the two systems of buyer and seller. Firstly the company

will record the data in sales account and then enter in the customer’s account if the sales are done

on credit basis.

Double entry recording in cash disbursement: It records all the transactions which are related to

the cash payment and cash outflows. These transactions are recorded in the cash payment journal

and update the subsidiary ledgers also.

Double entry recording in cash receipts: Cash is coming in the business from customers so it will

also affect the two transactions. The one account will affect the cash account and other will

affect the accounts receivable.

Manual and electronic systems:

The manual accounting system is a system in which the company records the data manually by

hand or paper work. The electronic system is a system in which all the transactions of the

company are recorded by the computer in software. Manual recording is less expensive as a

comparison to electronic accounting. Electronic accounting records all the transactions in detail

such as expenses, payment, assets, etc. Electronic accounting has more security for the data and

also requires less storage. Less calculation is incurred as compare to manual accounting. There

are the chances of error in manual accounting but in the electronic system, the chances of fraud

and error are less (Amahalu, et.al, 2017).

Books of Accounts of Kristine

Capital Account

To Balance b/d 5000 By cash 5000

5000 5000

Car Account

To Cash 1000 By Balance b/d 1000

1000 1000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

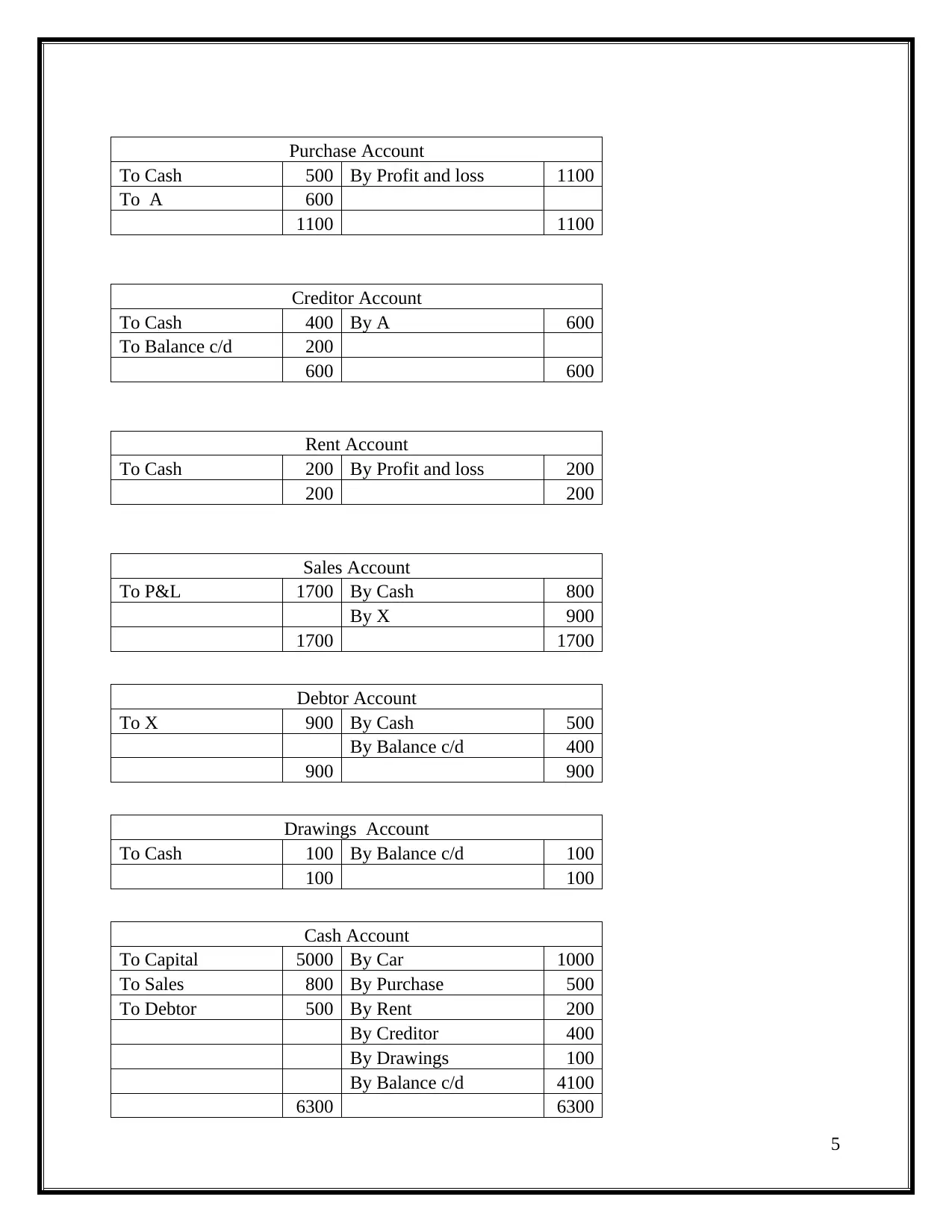

Purchase Account

To Cash 500 By Profit and loss 1100

To A 600

1100 1100

Creditor Account

To Cash 400 By A 600

To Balance c/d 200

600 600

Rent Account

To Cash 200 By Profit and loss 200

200 200

Sales Account

To P&L 1700 By Cash 800

By X 900

1700 1700

Debtor Account

To X 900 By Cash 500

By Balance c/d 400

900 900

Drawings Account

To Cash 100 By Balance c/d 100

100 100

Cash Account

To Capital 5000 By Car 1000

To Sales 800 By Purchase 500

To Debtor 500 By Rent 200

By Creditor 400

By Drawings 100

By Balance c/d 4100

6300 6300

5

To Cash 500 By Profit and loss 1100

To A 600

1100 1100

Creditor Account

To Cash 400 By A 600

To Balance c/d 200

600 600

Rent Account

To Cash 200 By Profit and loss 200

200 200

Sales Account

To P&L 1700 By Cash 800

By X 900

1700 1700

Debtor Account

To X 900 By Cash 500

By Balance c/d 400

900 900

Drawings Account

To Cash 100 By Balance c/d 100

100 100

Cash Account

To Capital 5000 By Car 1000

To Sales 800 By Purchase 500

To Debtor 500 By Rent 200

By Creditor 400

By Drawings 100

By Balance c/d 4100

6300 6300

5

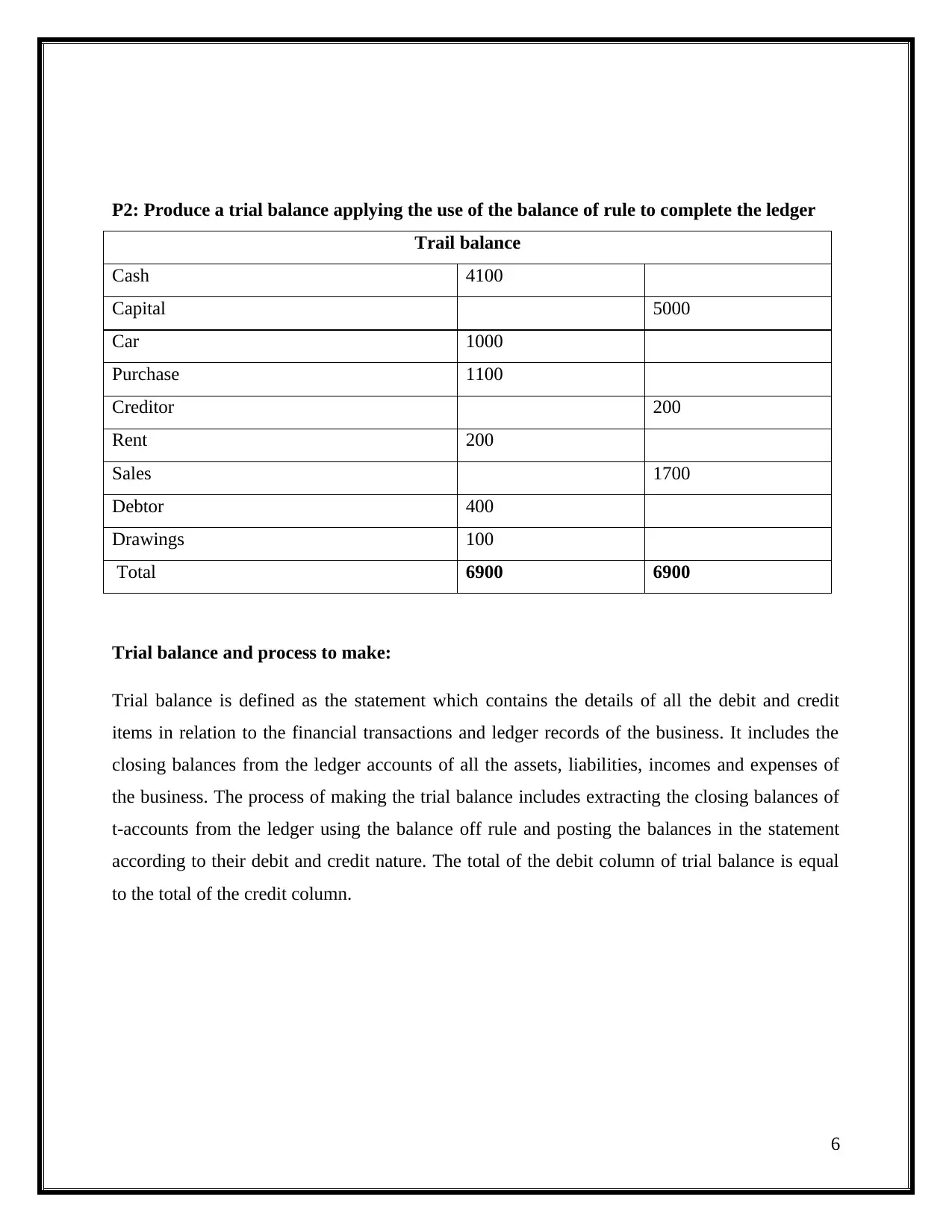

P2: Produce a trial balance applying the use of the balance of rule to complete the ledger

Trail balance

Cash 4100

Capital 5000

Car 1000

Purchase 1100

Creditor 200

Rent 200

Sales 1700

Debtor 400

Drawings 100

Total 6900 6900

Trial balance and process to make:

Trial balance is defined as the statement which contains the details of all the debit and credit

items in relation to the financial transactions and ledger records of the business. It includes the

closing balances from the ledger accounts of all the assets, liabilities, incomes and expenses of

the business. The process of making the trial balance includes extracting the closing balances of

t-accounts from the ledger using the balance off rule and posting the balances in the statement

according to their debit and credit nature. The total of the debit column of trial balance is equal

to the total of the credit column.

6

Trail balance

Cash 4100

Capital 5000

Car 1000

Purchase 1100

Creditor 200

Rent 200

Sales 1700

Debtor 400

Drawings 100

Total 6900 6900

Trial balance and process to make:

Trial balance is defined as the statement which contains the details of all the debit and credit

items in relation to the financial transactions and ledger records of the business. It includes the

closing balances from the ledger accounts of all the assets, liabilities, incomes and expenses of

the business. The process of making the trial balance includes extracting the closing balances of

t-accounts from the ledger using the balance off rule and posting the balances in the statement

according to their debit and credit nature. The total of the debit column of trial balance is equal

to the total of the credit column.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2:

P3: Prepare final accounts from given trial balance figures adjusting for accruals,

depreciation and prepayments

Financial statements are the statements which include the details of accounting and business

transactions of the business presented in an organised form and manner. On the other hand

financial reports are the reports which provide information about the financial performance and

its analysis. The financial statements form part of financial reports and are included in the

financial reports of company. The following are the differences in financial statements and

financial reports of a business:

The financial statements are prepared in accordance with the applicable accounting and

financial legislations such as GAAP, IFRS, etc. and principles whereas the financial reports

are prepared in accordance with the business and company policies and reporting

requirements.

The publishing and disclosure of financial reports is not necessary whereas it is mandatory to

publish their financial statements to stakeholders and public.

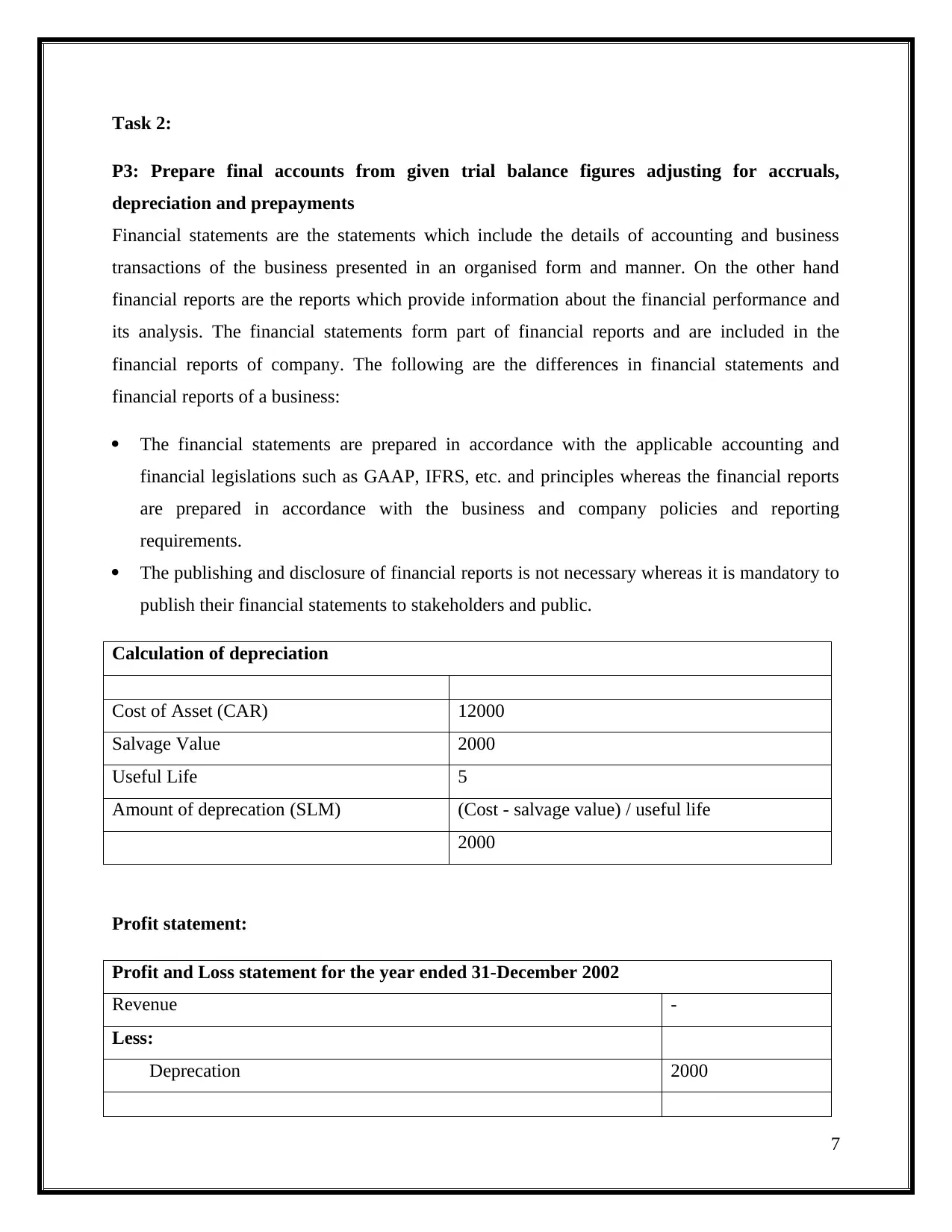

Calculation of depreciation

Cost of Asset (CAR) 12000

Salvage Value 2000

Useful Life 5

Amount of deprecation (SLM) (Cost - salvage value) / useful life

2000

Profit statement:

Profit and Loss statement for the year ended 31-December 2002

Revenue -

Less:

Deprecation 2000

7

P3: Prepare final accounts from given trial balance figures adjusting for accruals,

depreciation and prepayments

Financial statements are the statements which include the details of accounting and business

transactions of the business presented in an organised form and manner. On the other hand

financial reports are the reports which provide information about the financial performance and

its analysis. The financial statements form part of financial reports and are included in the

financial reports of company. The following are the differences in financial statements and

financial reports of a business:

The financial statements are prepared in accordance with the applicable accounting and

financial legislations such as GAAP, IFRS, etc. and principles whereas the financial reports

are prepared in accordance with the business and company policies and reporting

requirements.

The publishing and disclosure of financial reports is not necessary whereas it is mandatory to

publish their financial statements to stakeholders and public.

Calculation of depreciation

Cost of Asset (CAR) 12000

Salvage Value 2000

Useful Life 5

Amount of deprecation (SLM) (Cost - salvage value) / useful life

2000

Profit statement:

Profit and Loss statement for the year ended 31-December 2002

Revenue -

Less:

Deprecation 2000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

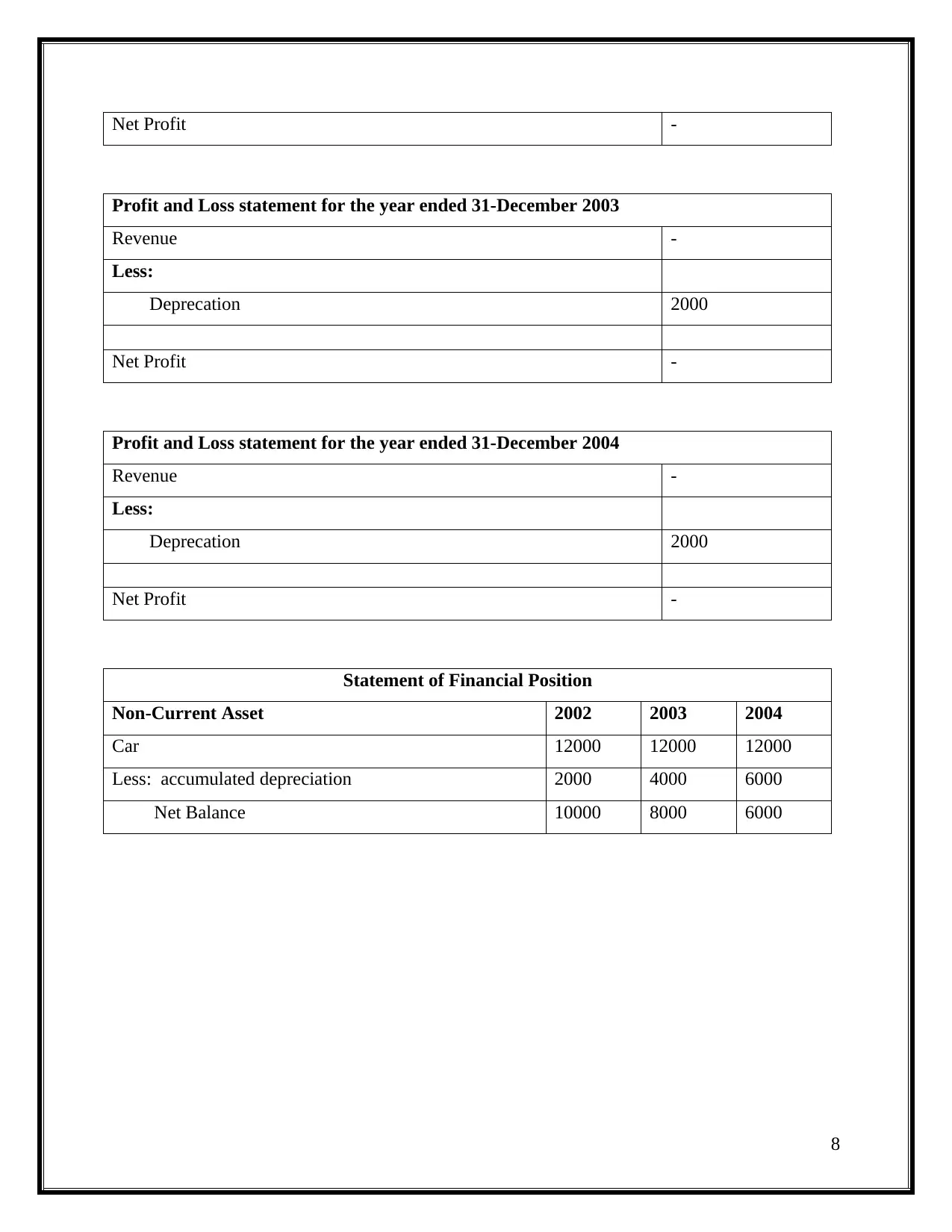

Net Profit -

Profit and Loss statement for the year ended 31-December 2003

Revenue -

Less:

Deprecation 2000

Net Profit -

Profit and Loss statement for the year ended 31-December 2004

Revenue -

Less:

Deprecation 2000

Net Profit -

Statement of Financial Position

Non-Current Asset 2002 2003 2004

Car 12000 12000 12000

Less: accumulated depreciation 2000 4000 6000

Net Balance 10000 8000 6000

8

Profit and Loss statement for the year ended 31-December 2003

Revenue -

Less:

Deprecation 2000

Net Profit -

Profit and Loss statement for the year ended 31-December 2004

Revenue -

Less:

Deprecation 2000

Net Profit -

Statement of Financial Position

Non-Current Asset 2002 2003 2004

Car 12000 12000 12000

Less: accumulated depreciation 2000 4000 6000

Net Balance 10000 8000 6000

8

Different types of financial statements

There are three types of financial statements which include statement of financial position,

statement of profit and loss and cash flow statement. These types of financial statements are

explained as follows:

Statement of profit and loss – The statement of profit and loss includes the details of

income and expenses and calculation of profits. The financial performance of the business

over the period is presented in this financial statement.

Statement of financial position – This is the balance sheet of the business which contains

the details of assets and liabilities of the business and presents the financial position of the

business at the end of the period.

Cash Flow Statement – This financial statement include the details of cash inflows and cash

outflows of the business. This includes the cash transaction in relation to operating, financing

and investment activities of the business segregated on the basis of nature of cash transaction.

Adjustments for prepaid, accruals and bad debts:

In a business there are various periodical expenses which relate to a specific period such as rent,

electricity, etc. According to the accrual system of accounting the expenses which relate to a

specific period are recorded in the profit and loss statement of that period and income and

expense that relate to other period are recorded as prepaid or accruals. Prepaid expenses or

prepayments are referred to as the amount of business expenses which are paid in advance. The

accruals are the expenses which relate to the current period but are not paid in the current period.

Depreciation is the amount which relates to the decline in the value of fixed assets of the

business. The adjustment of depreciation is made by deducting the value of fixed assets in each

accounting period till the completion of the life of the asset (Unegbu, 2014).

9

There are three types of financial statements which include statement of financial position,

statement of profit and loss and cash flow statement. These types of financial statements are

explained as follows:

Statement of profit and loss – The statement of profit and loss includes the details of

income and expenses and calculation of profits. The financial performance of the business

over the period is presented in this financial statement.

Statement of financial position – This is the balance sheet of the business which contains

the details of assets and liabilities of the business and presents the financial position of the

business at the end of the period.

Cash Flow Statement – This financial statement include the details of cash inflows and cash

outflows of the business. This includes the cash transaction in relation to operating, financing

and investment activities of the business segregated on the basis of nature of cash transaction.

Adjustments for prepaid, accruals and bad debts:

In a business there are various periodical expenses which relate to a specific period such as rent,

electricity, etc. According to the accrual system of accounting the expenses which relate to a

specific period are recorded in the profit and loss statement of that period and income and

expense that relate to other period are recorded as prepaid or accruals. Prepaid expenses or

prepayments are referred to as the amount of business expenses which are paid in advance. The

accruals are the expenses which relate to the current period but are not paid in the current period.

Depreciation is the amount which relates to the decline in the value of fixed assets of the

business. The adjustment of depreciation is made by deducting the value of fixed assets in each

accounting period till the completion of the life of the asset (Unegbu, 2014).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

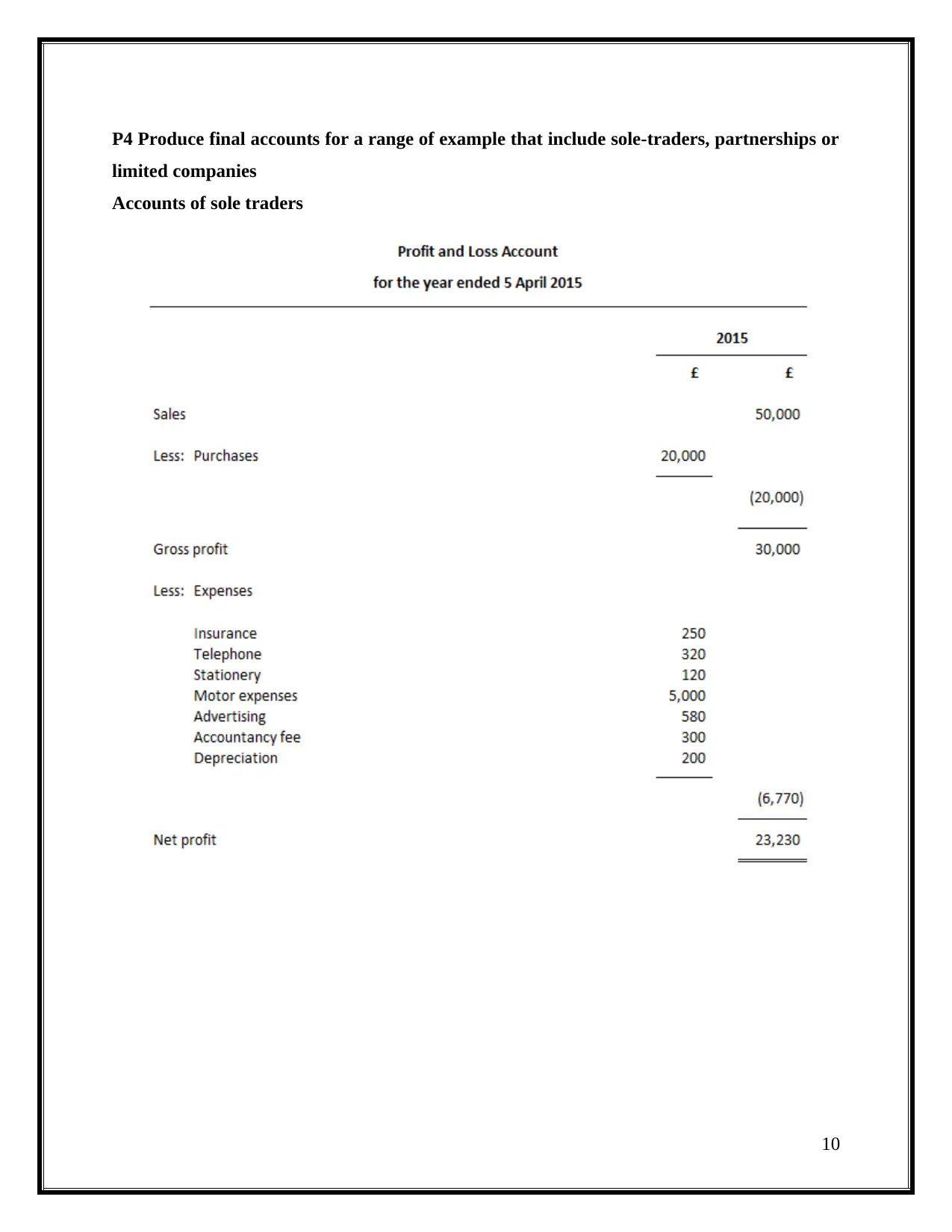

P4 Produce final accounts for a range of example that include sole-traders, partnerships or

limited companies

Accounts of sole traders

10

limited companies

Accounts of sole traders

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

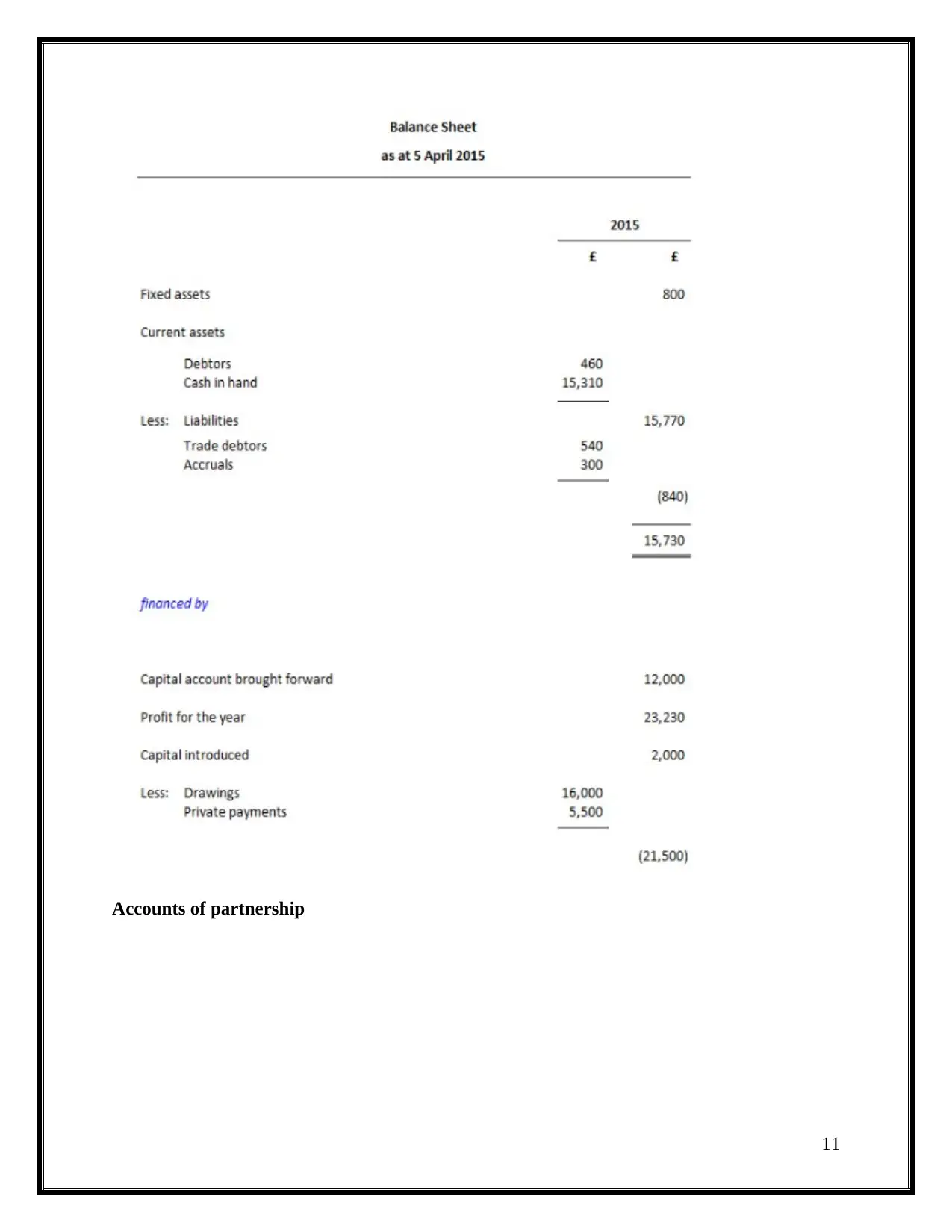

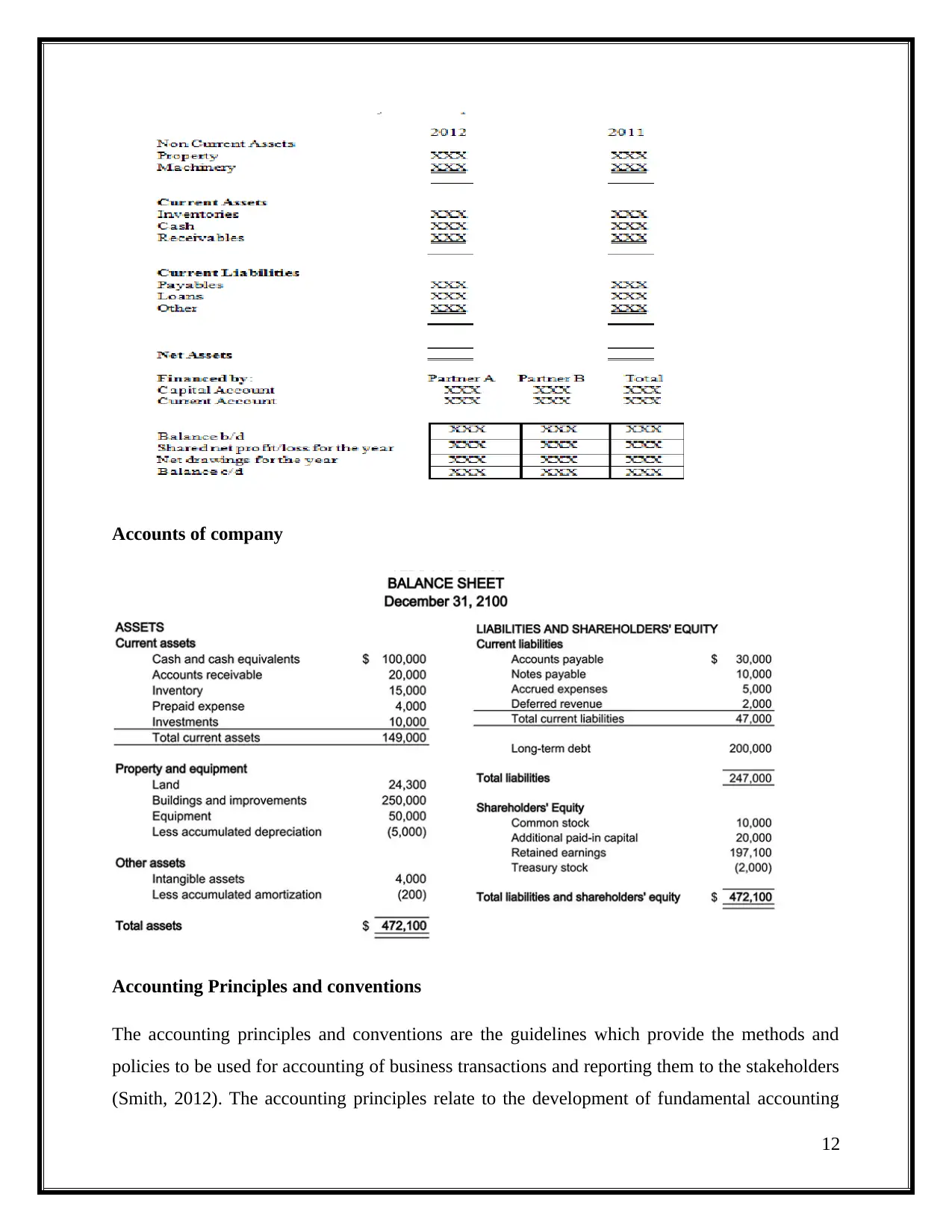

Accounts of partnership

11

11

Accounts of company

Accounting Principles and conventions

The accounting principles and conventions are the guidelines which provide the methods and

policies to be used for accounting of business transactions and reporting them to the stakeholders

(Smith, 2012). The accounting principles relate to the development of fundamental accounting

12

Accounting Principles and conventions

The accounting principles and conventions are the guidelines which provide the methods and

policies to be used for accounting of business transactions and reporting them to the stakeholders

(Smith, 2012). The accounting principles relate to the development of fundamental accounting

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.