Financial Accounting: A Comprehensive Guide to Principles and Techniques

VerifiedAdded on 2024/06/04

|14

|970

|71

AI Summary

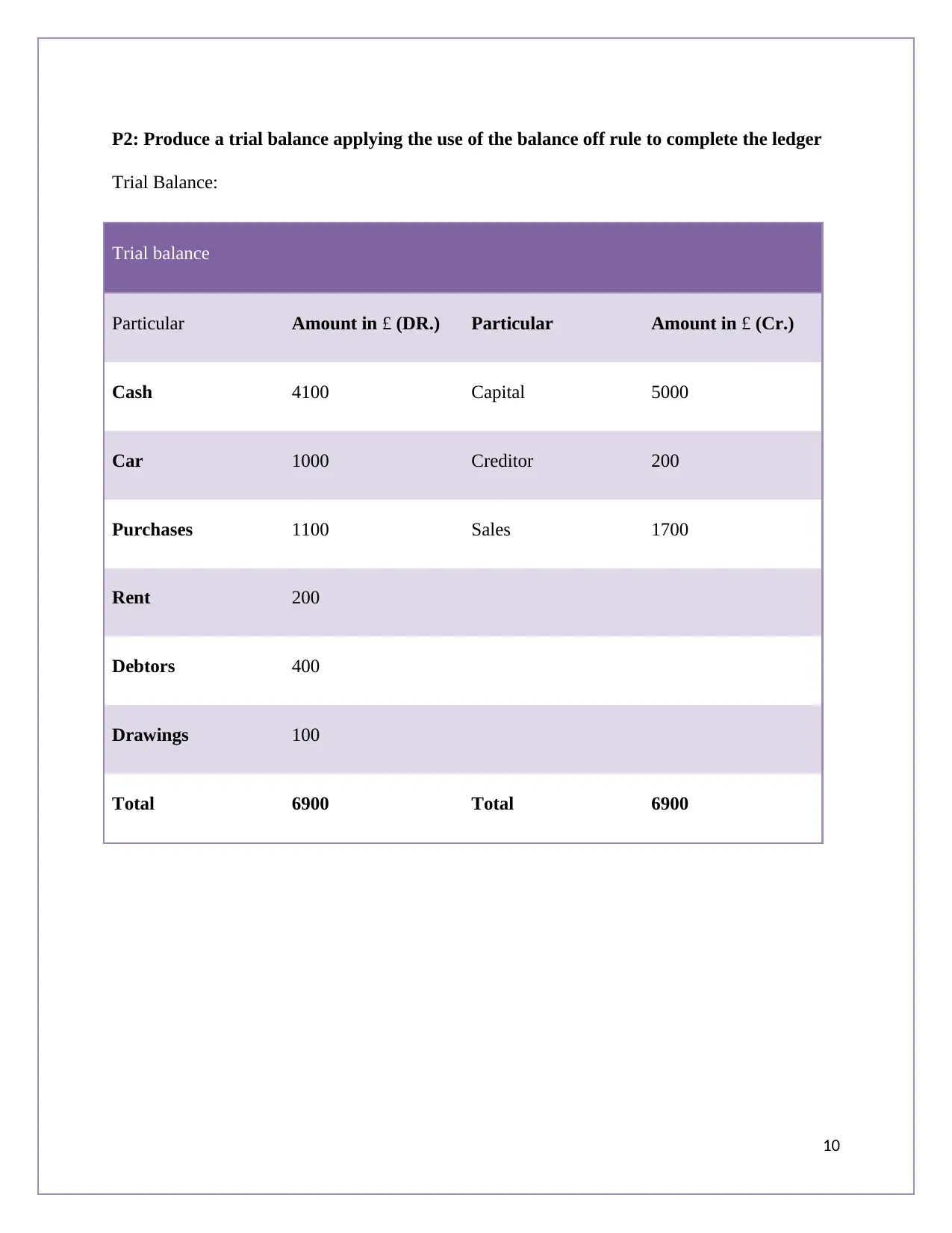

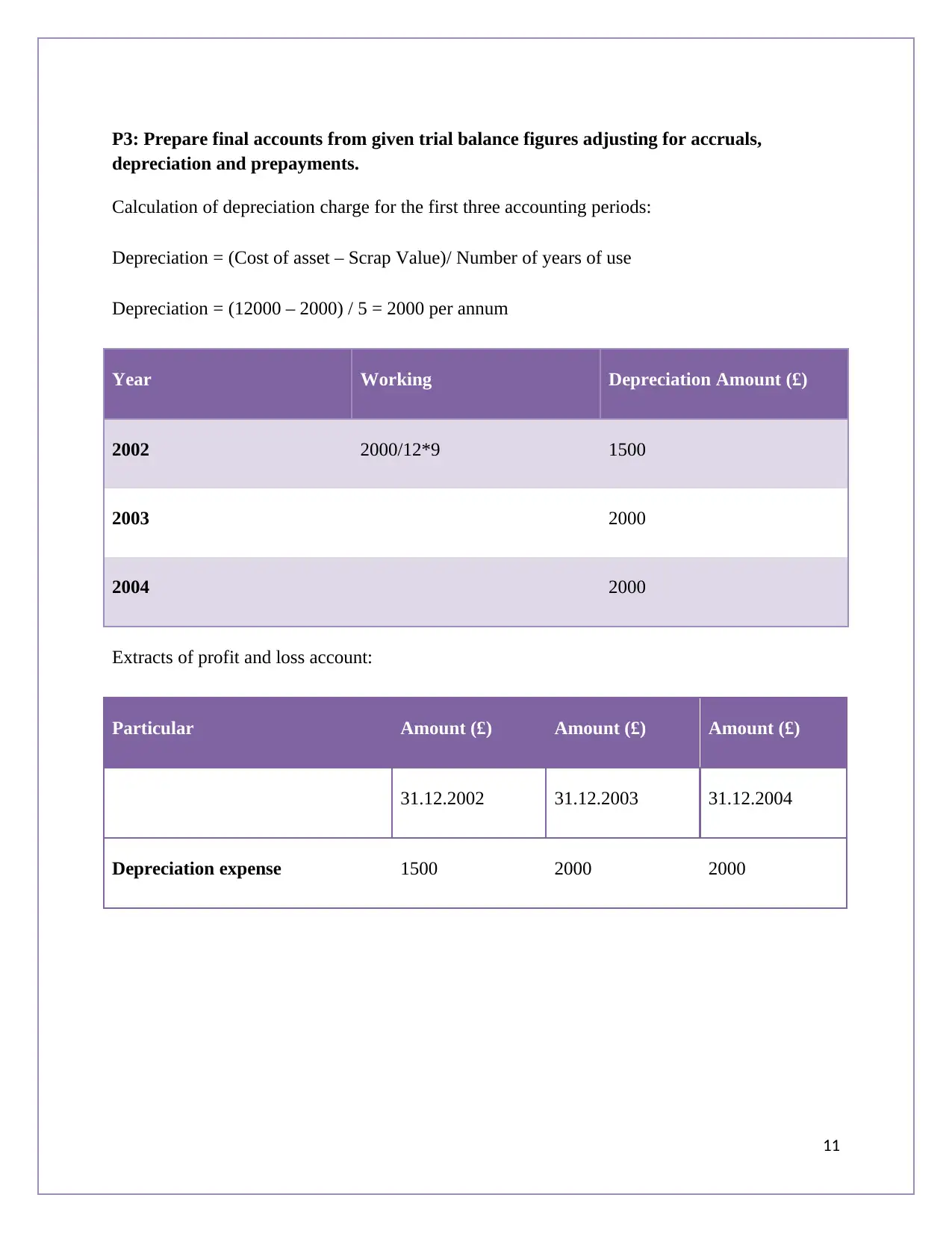

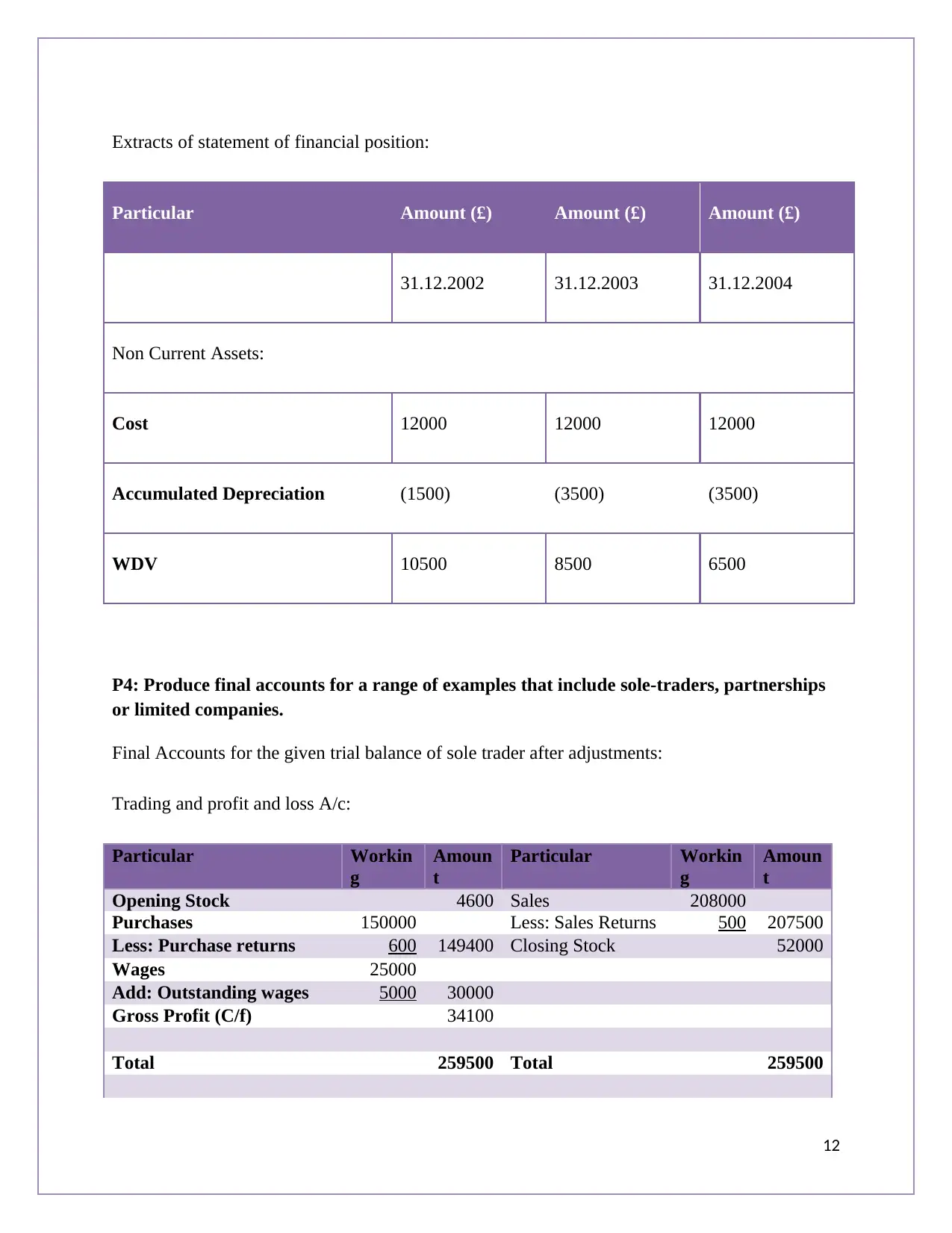

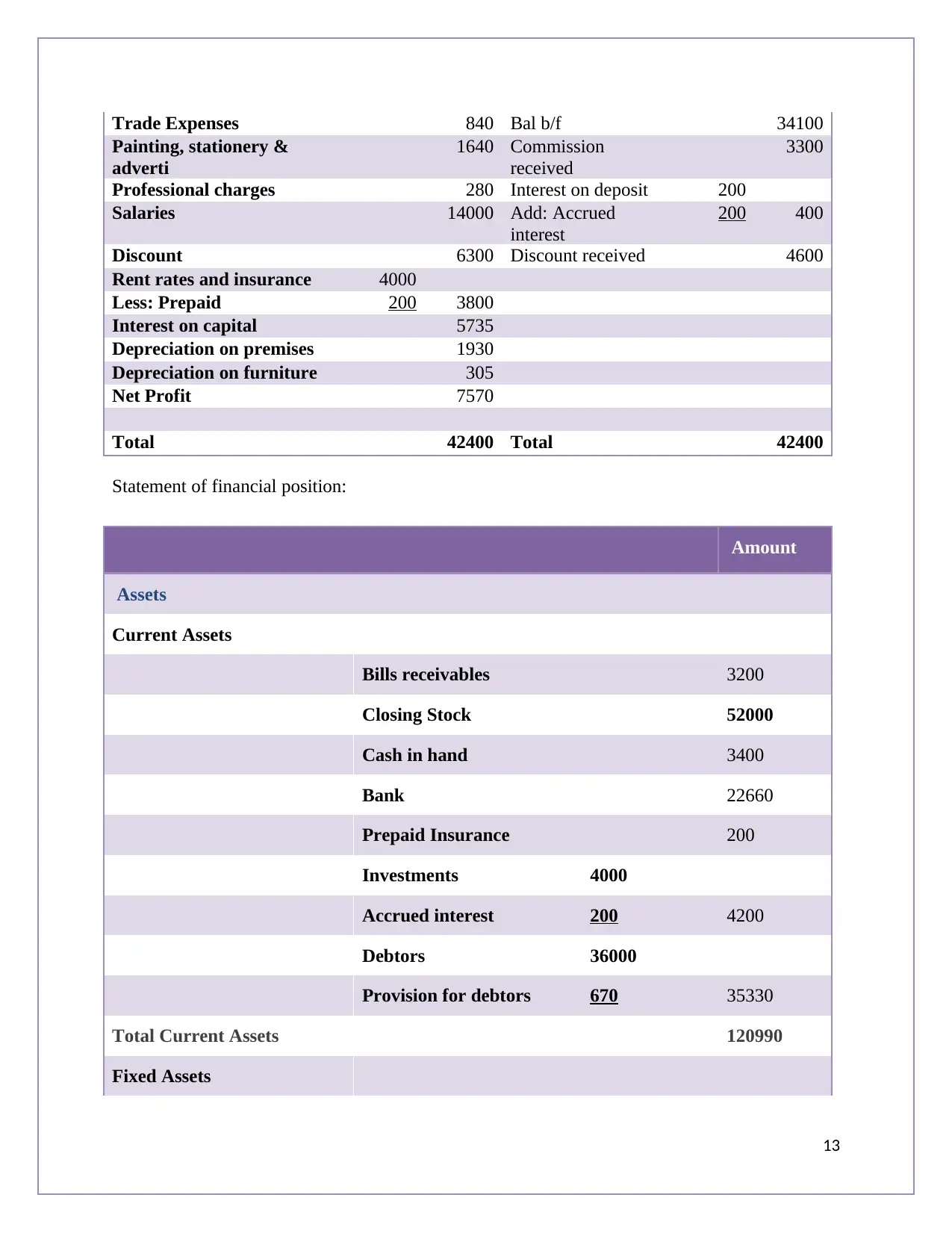

This report delves into the fundamental principles and techniques of financial accounting, providing a comprehensive understanding of the subject. It covers key aspects such as double-entry bookkeeping, trial balance preparation, final account generation for various business entities, bank reconciliation, and the use of suspense accounts. The report utilizes practical examples and real-world scenarios to illustrate the application of these concepts, making it an invaluable resource for students and professionals alike.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.