Financial Accounting Research Paper

VerifiedAdded on 2020/01/07

|40

|5589

|141

Essay

AI Summary

This assignment involves a critical review of scholarly articles related to financial accounting. Students are expected to analyze diverse perspectives on the topic, covering areas like the history of financial accounting, its role in different industries (government, nonprofit, manufacturing), and emerging trends such as the influence of carbon markets and environmental regulations. The assignment emphasizes research skills, analytical thinking, and the ability to synthesize information from various sources.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION

The criteria and department of the accounting under which all kinds of the financial and

monetary transactions are to be recorded as well as analysed is identified as the financial

accounting. When the business entity going to assess that company and business entity

performing in which manner such as declining or upward then the financial accounting is the

most helpful criteria for this condition. An entrepreneur when want to check that whether the

financial and profitability position of the company growing or not in the industry then use such

mentioned branch. Apart from this, by considering the financial accounting process the

management able to make the different types of the financial reports and accounts like as income

statement, balance sheet, cash flow etc. In addition to this, all the disclosures and theories,

standards etc. of the accounting are to be analysed and while making the accounts of the

financial (Weil, Schipper and Francis, 2013). The current project is based on the different

number of the accounts from initial or start to end of the financial statements. On the basis of the

present report the reader able to know formate and process to prepare journal entries, trial

balance, ledger account, profit and loss accounts, statement of financial position etc. by

considering such all the statements the management of business organisation able to make the

strategies for the further and next financial periods to make the company healthier in for of the

profitability. In addition to this, about the two types of depreciation techniques, suspense and

clearing account etc. also explained in the current case study. Apart from this, the report shows

about the BRS which states for the bank reconciliation statement used by the companies for

assessing various financial data and conditions in the segment where it existed and operating.

Financial accountancy is the record of accountancy preoccupied with the compact and analysis

and reporting of financial transaction concern to a enterprise.

When make financial statement ,they necessary follows points:-

Relevance:- Financial accounting which is mind particular.it is very important for

preparation of financial accounting statement of the organization for information to

determiner decisions. Unless this evidence is present ,there is no point in disorderliness

statement.

Materiality :- materiality is important for reparation of fiscal statement in the

organization because information is materiality if its mistake or statement could

1

The criteria and department of the accounting under which all kinds of the financial and

monetary transactions are to be recorded as well as analysed is identified as the financial

accounting. When the business entity going to assess that company and business entity

performing in which manner such as declining or upward then the financial accounting is the

most helpful criteria for this condition. An entrepreneur when want to check that whether the

financial and profitability position of the company growing or not in the industry then use such

mentioned branch. Apart from this, by considering the financial accounting process the

management able to make the different types of the financial reports and accounts like as income

statement, balance sheet, cash flow etc. In addition to this, all the disclosures and theories,

standards etc. of the accounting are to be analysed and while making the accounts of the

financial (Weil, Schipper and Francis, 2013). The current project is based on the different

number of the accounts from initial or start to end of the financial statements. On the basis of the

present report the reader able to know formate and process to prepare journal entries, trial

balance, ledger account, profit and loss accounts, statement of financial position etc. by

considering such all the statements the management of business organisation able to make the

strategies for the further and next financial periods to make the company healthier in for of the

profitability. In addition to this, about the two types of depreciation techniques, suspense and

clearing account etc. also explained in the current case study. Apart from this, the report shows

about the BRS which states for the bank reconciliation statement used by the companies for

assessing various financial data and conditions in the segment where it existed and operating.

Financial accountancy is the record of accountancy preoccupied with the compact and analysis

and reporting of financial transaction concern to a enterprise.

When make financial statement ,they necessary follows points:-

Relevance:- Financial accounting which is mind particular.it is very important for

preparation of financial accounting statement of the organization for information to

determiner decisions. Unless this evidence is present ,there is no point in disorderliness

statement.

Materiality :- materiality is important for reparation of fiscal statement in the

organization because information is materiality if its mistake or statement could

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

determiner the economical decisions of exploiter confiscate on the basis of the financial

statement.

Reliability:- accounting essential be self-governing from important mistake or bias. It

should be easy relied upon by managers. Often message that is extremely applicable.

Understand-ability:- financial accounting written report should be ununderstood by

those to whom the content.

Comparability :-- financial reports from different time period should be compare with

one some other in command to conclude meaningful assumption about the tendency in an

entity fiscal presentation and perspective over time.

this point are very important for preparation of correct and valuable financial statement for the

organization.

2

statement.

Reliability:- accounting essential be self-governing from important mistake or bias. It

should be easy relied upon by managers. Often message that is extremely applicable.

Understand-ability:- financial accounting written report should be ununderstood by

those to whom the content.

Comparability :-- financial reports from different time period should be compare with

one some other in command to conclude meaningful assumption about the tendency in an

entity fiscal presentation and perspective over time.

this point are very important for preparation of correct and valuable financial statement for the

organization.

2

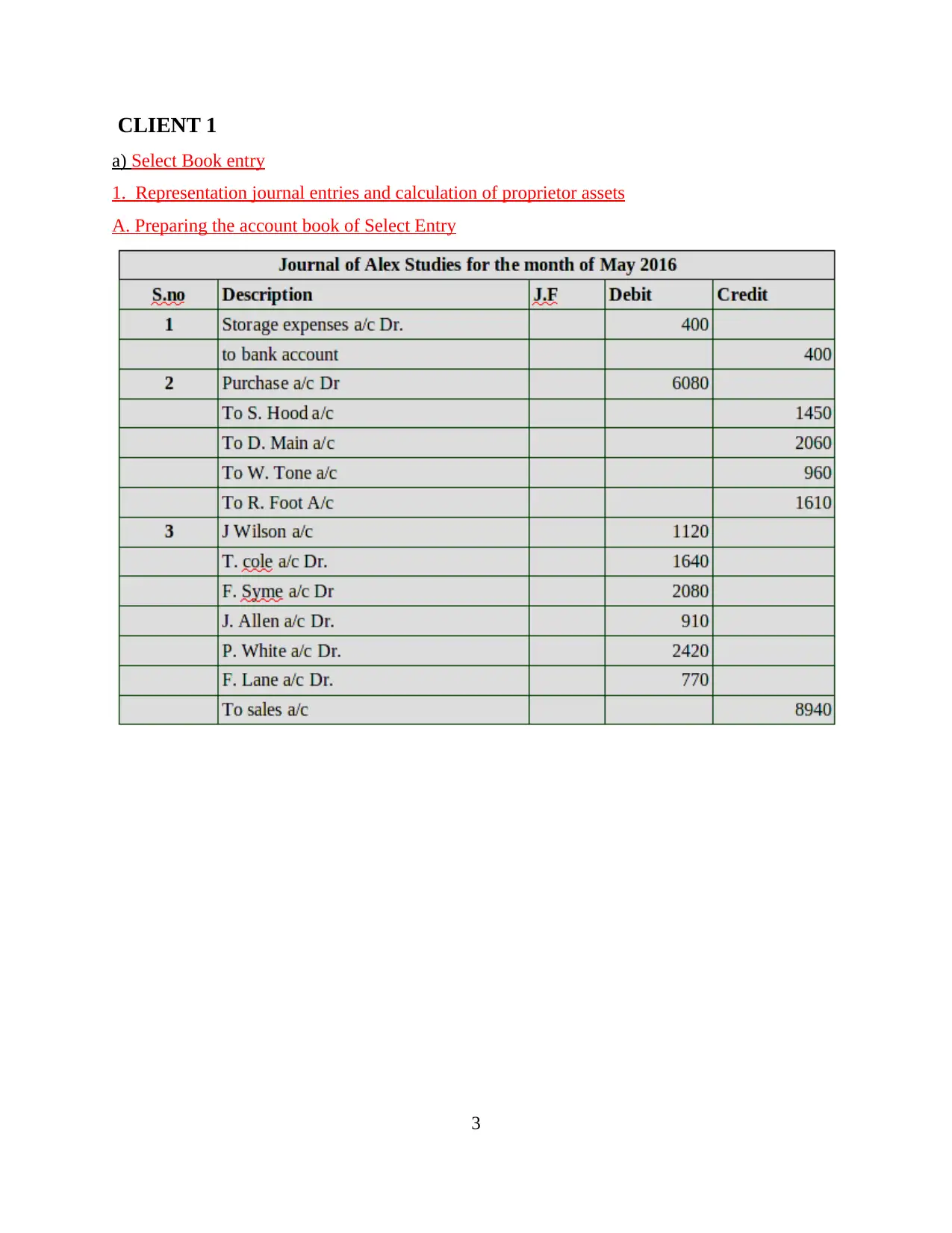

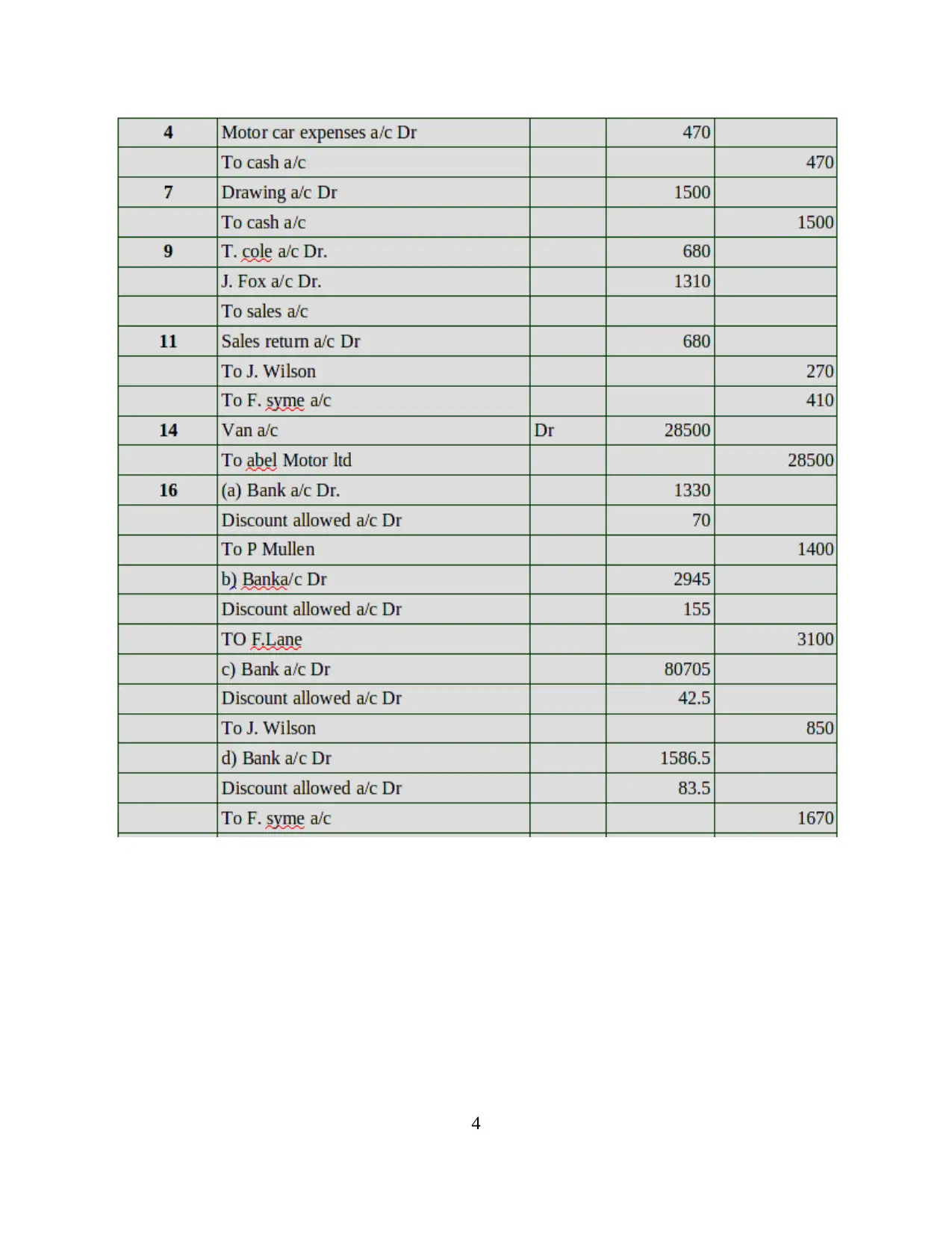

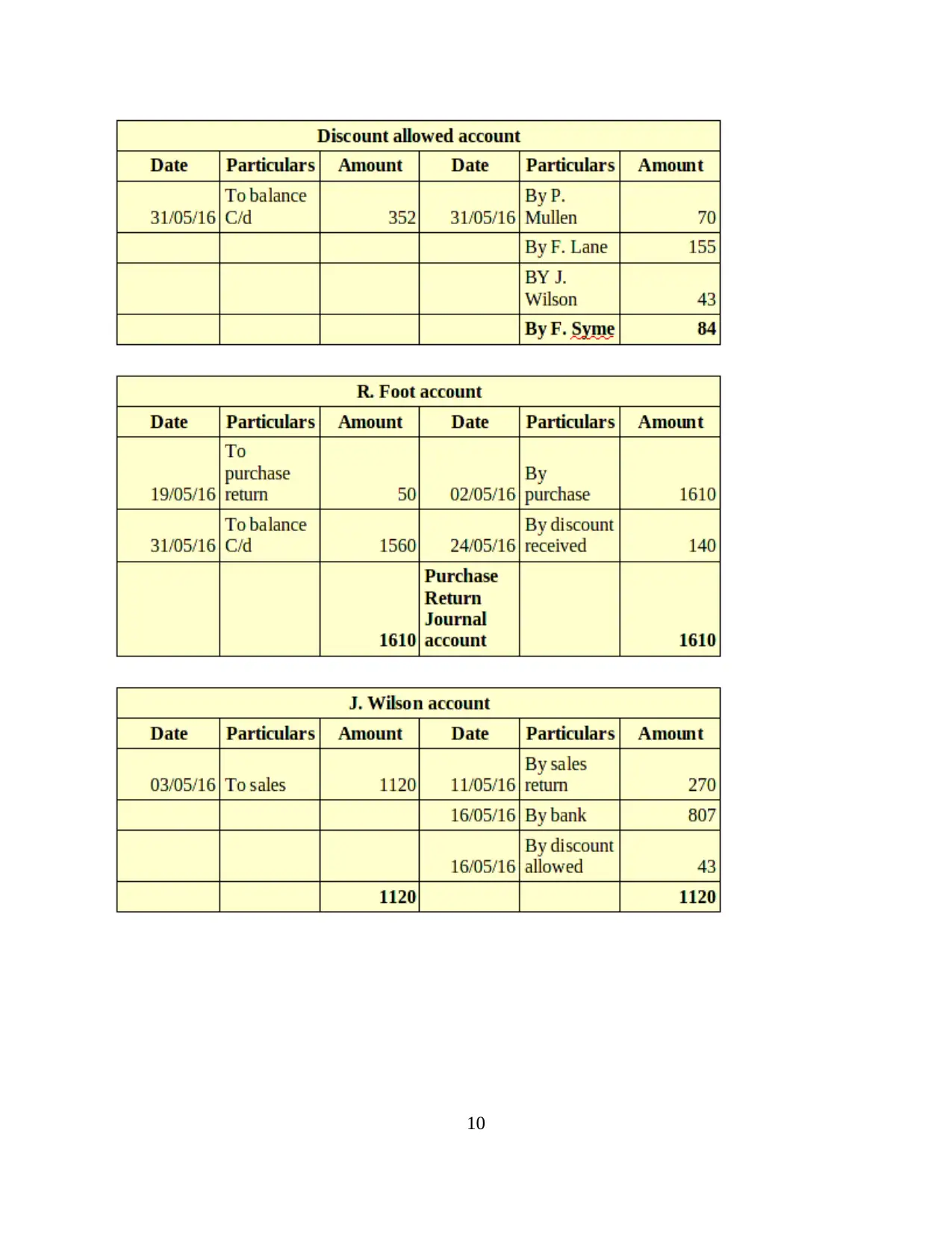

CLIENT 1

a) Select Book entry

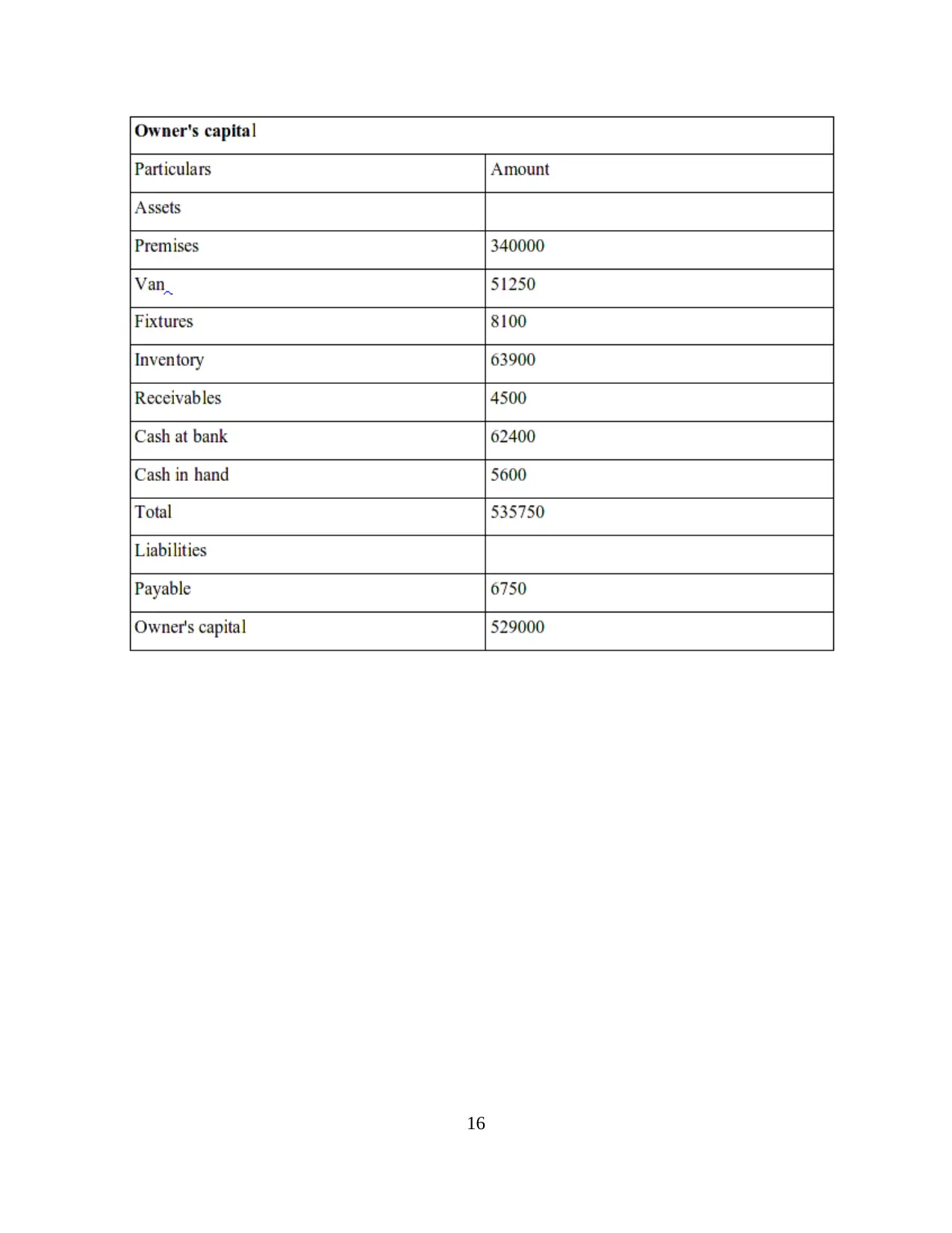

1. Representation journal entries and calculation of proprietor assets

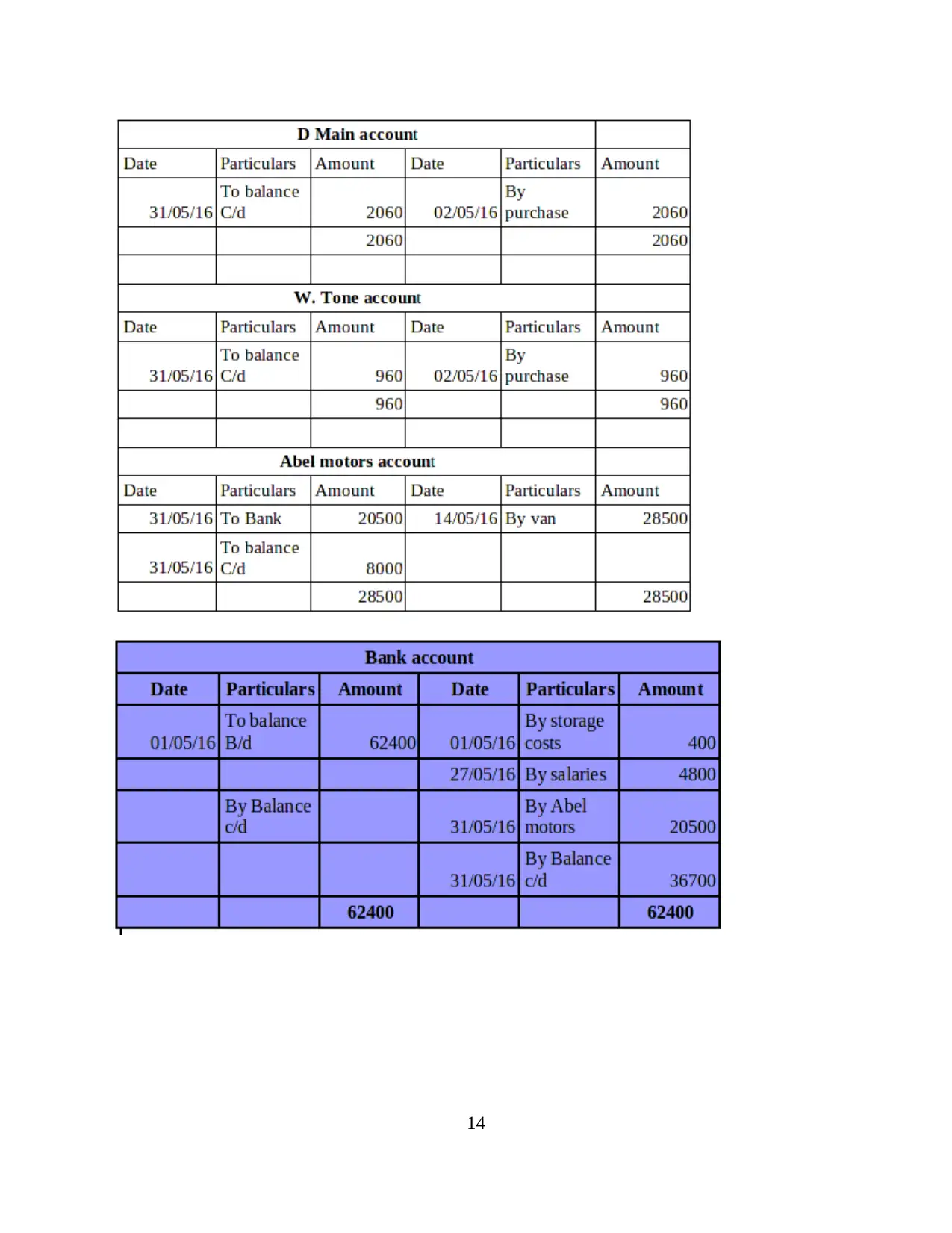

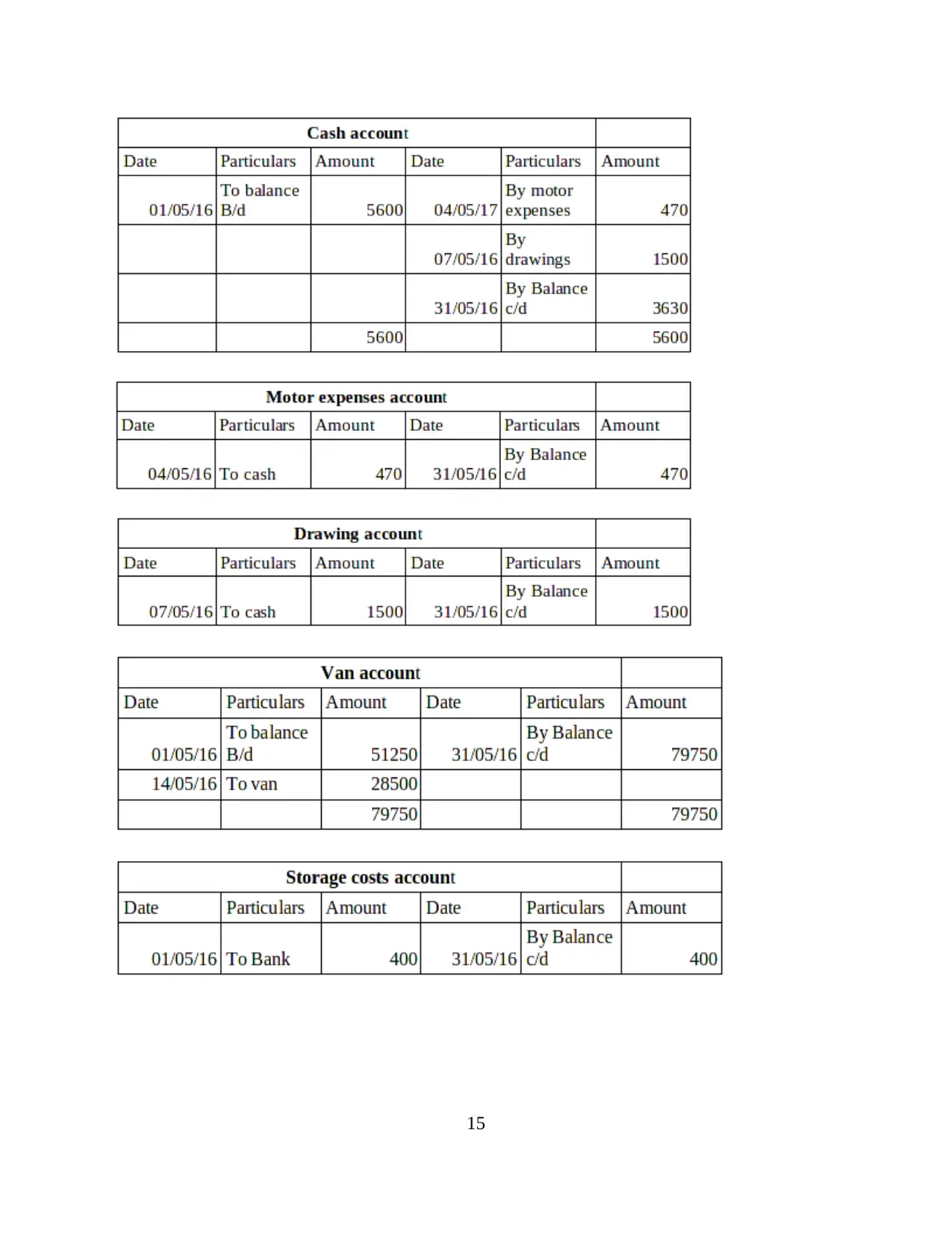

A. Preparing the account book of Select Entry

3

a) Select Book entry

1. Representation journal entries and calculation of proprietor assets

A. Preparing the account book of Select Entry

3

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

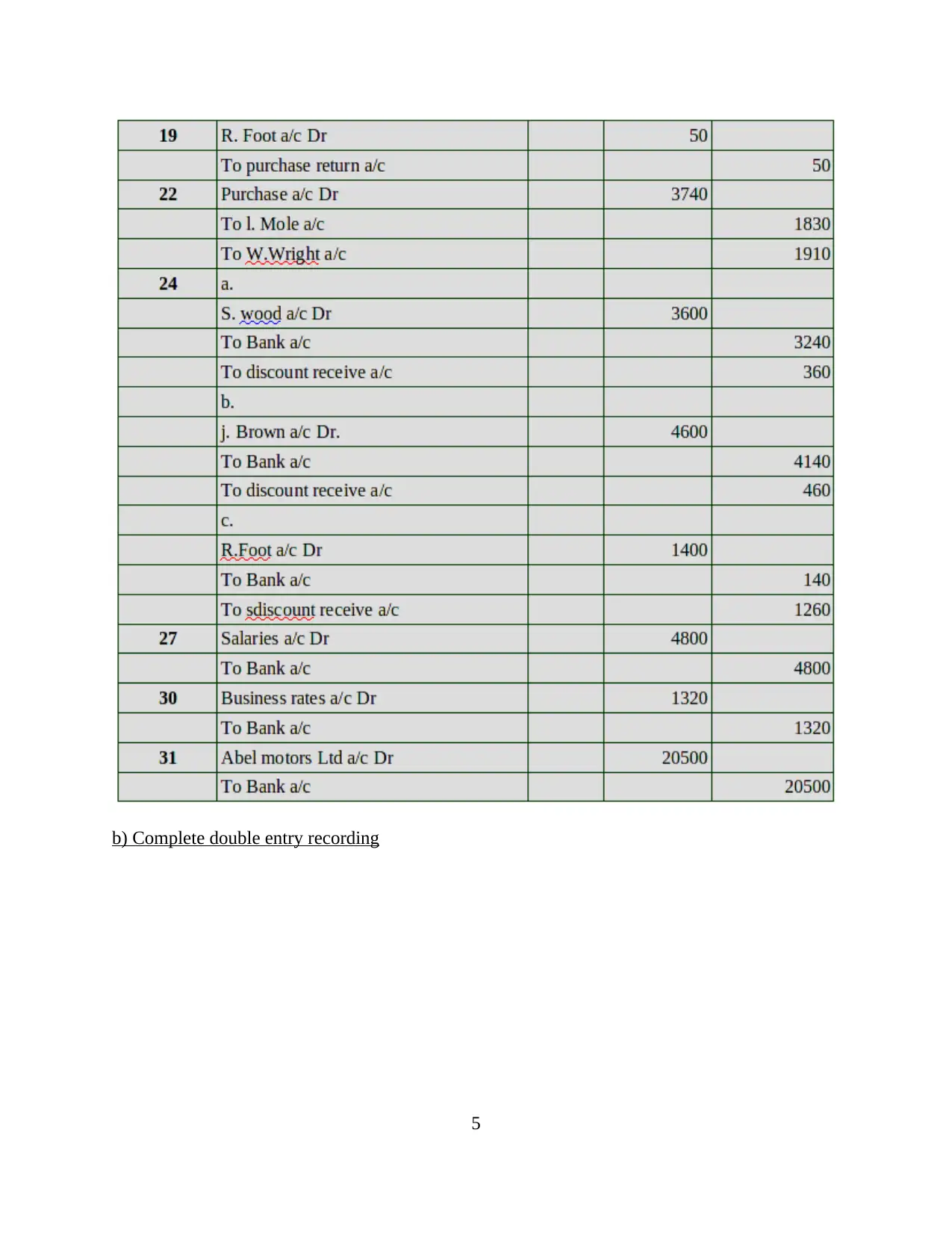

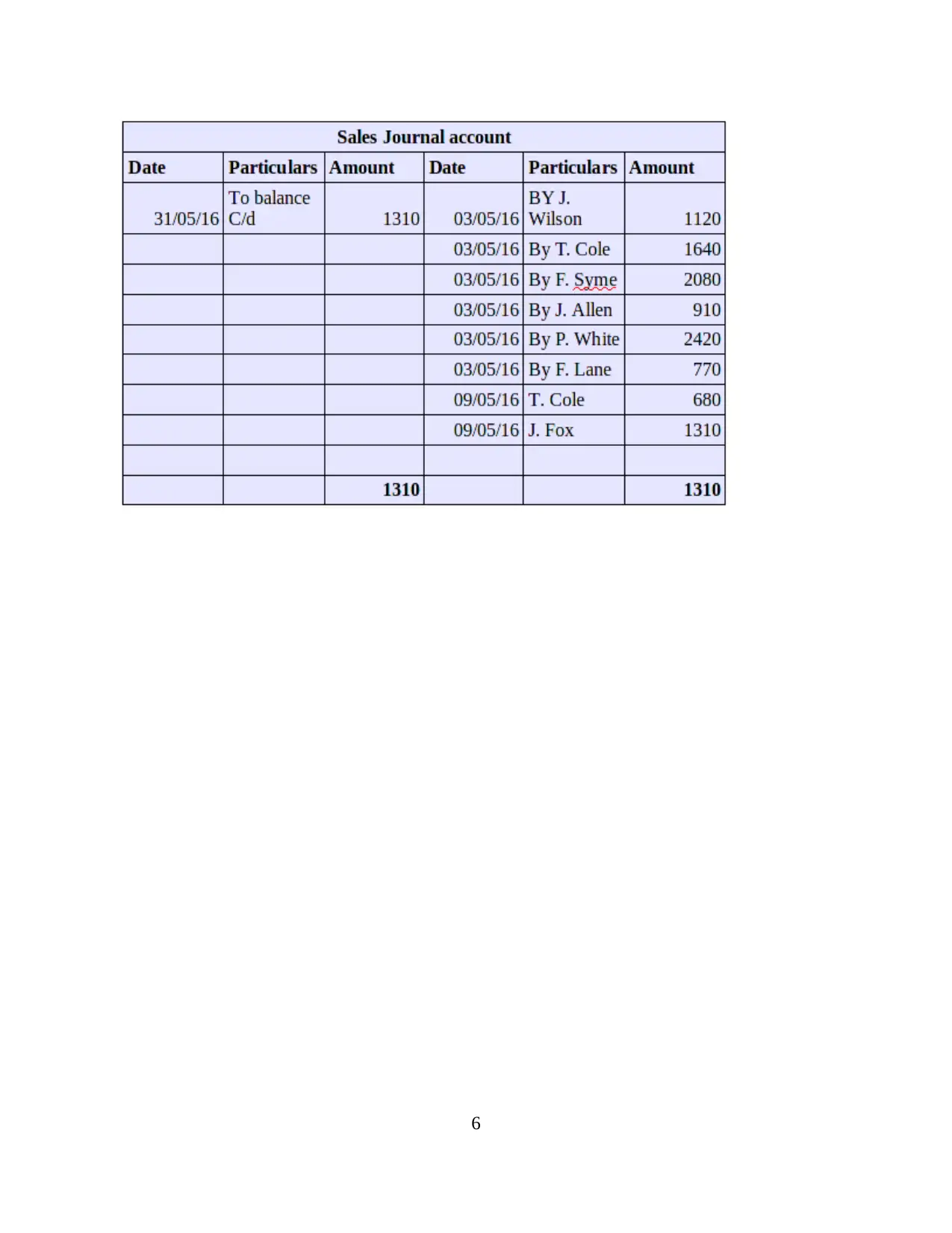

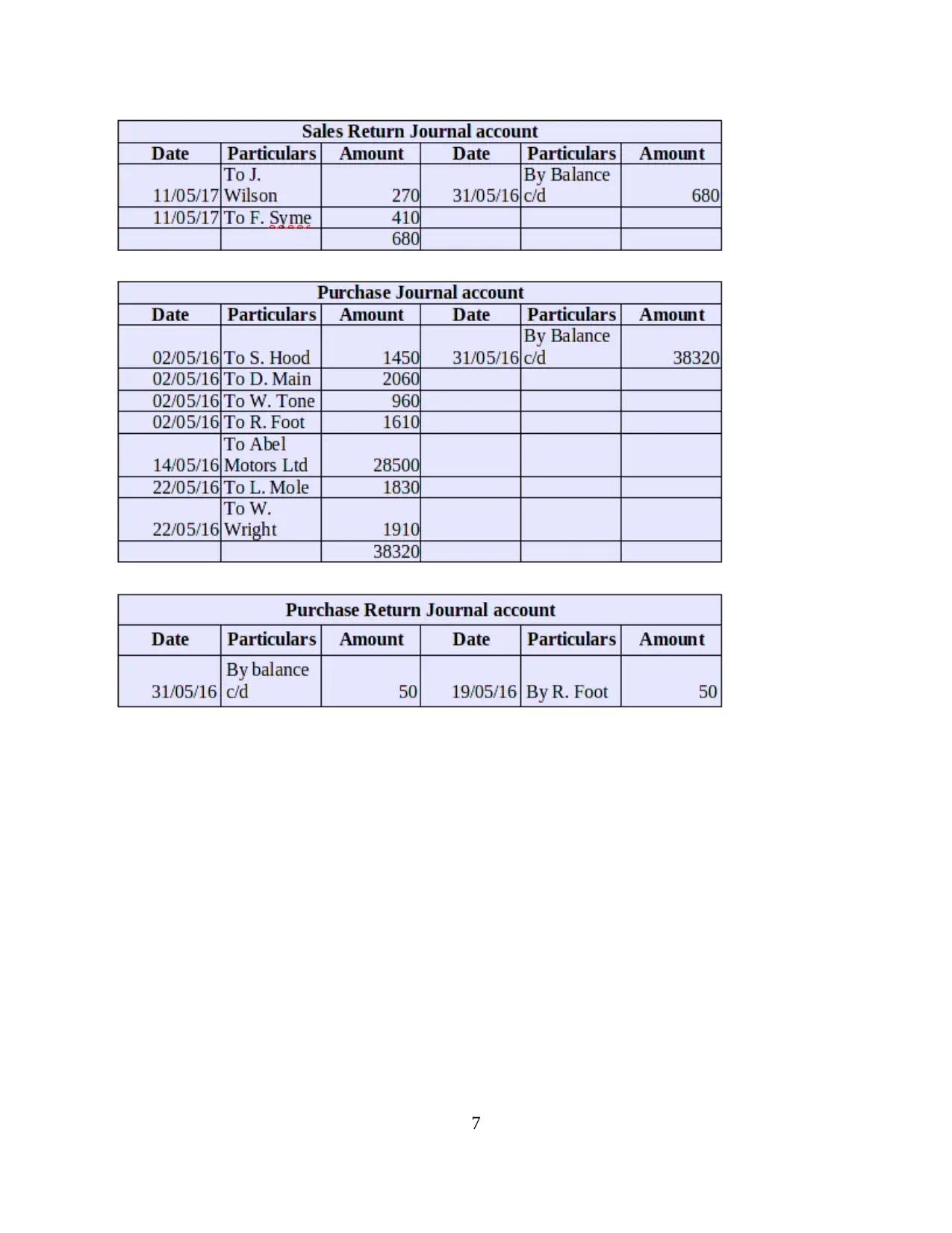

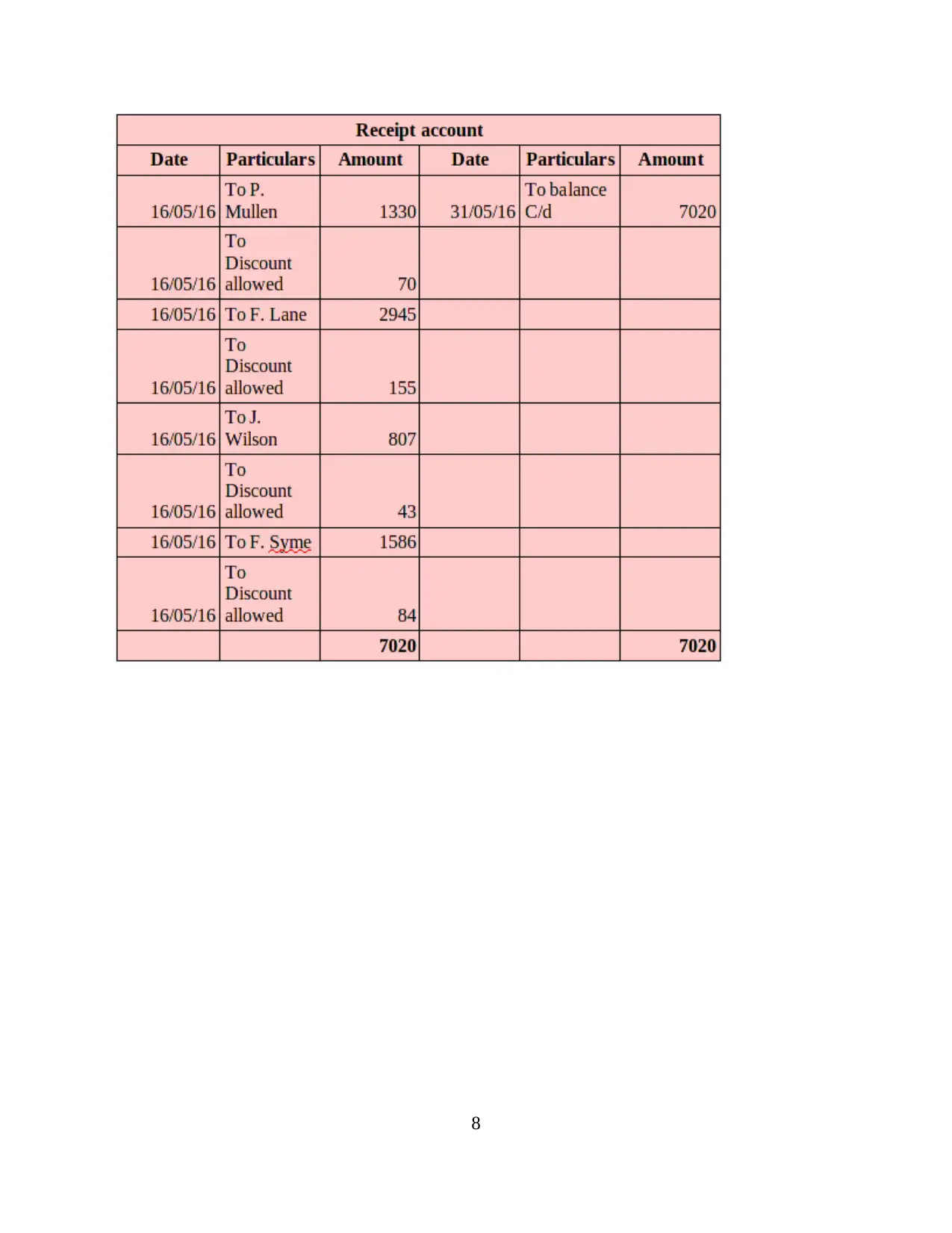

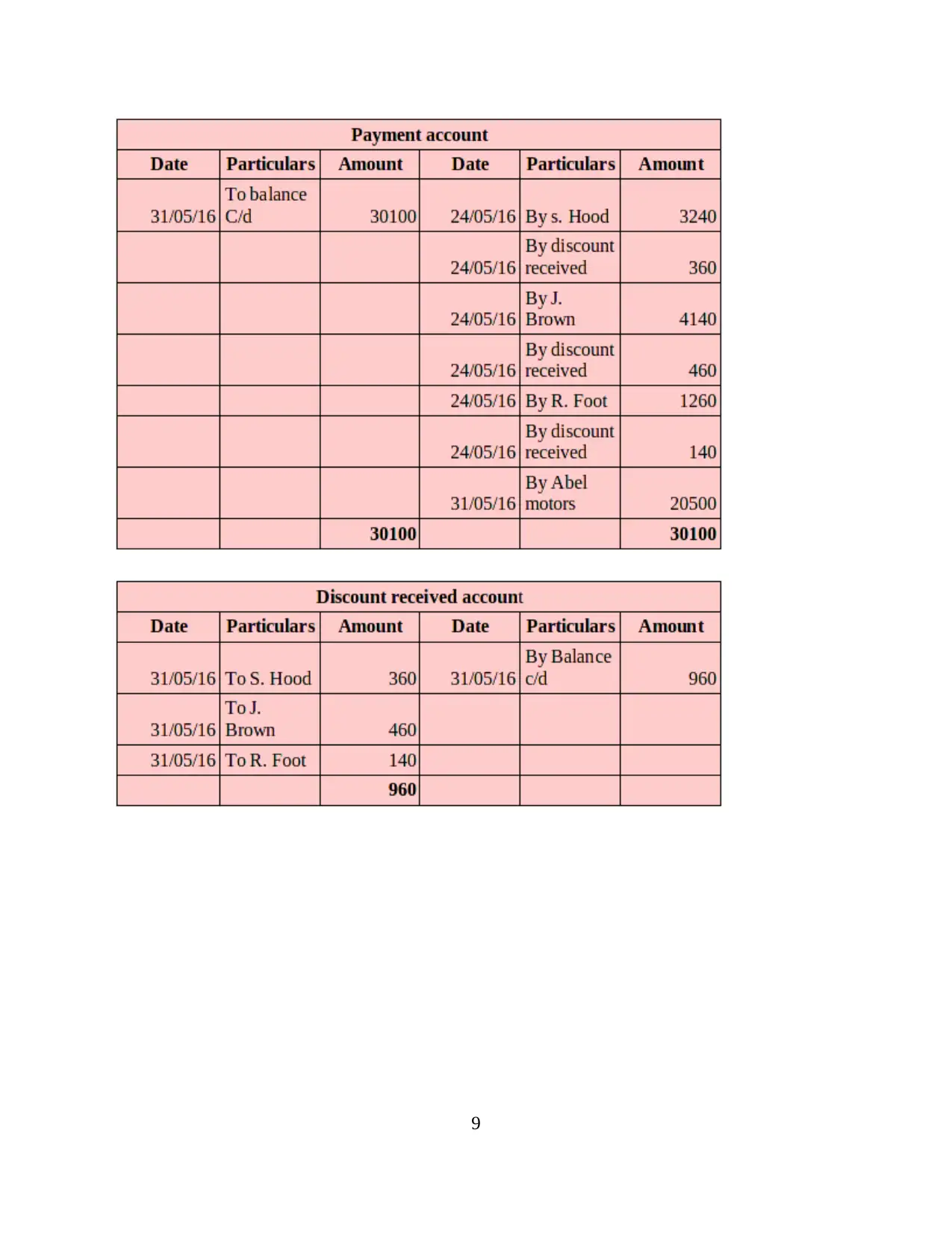

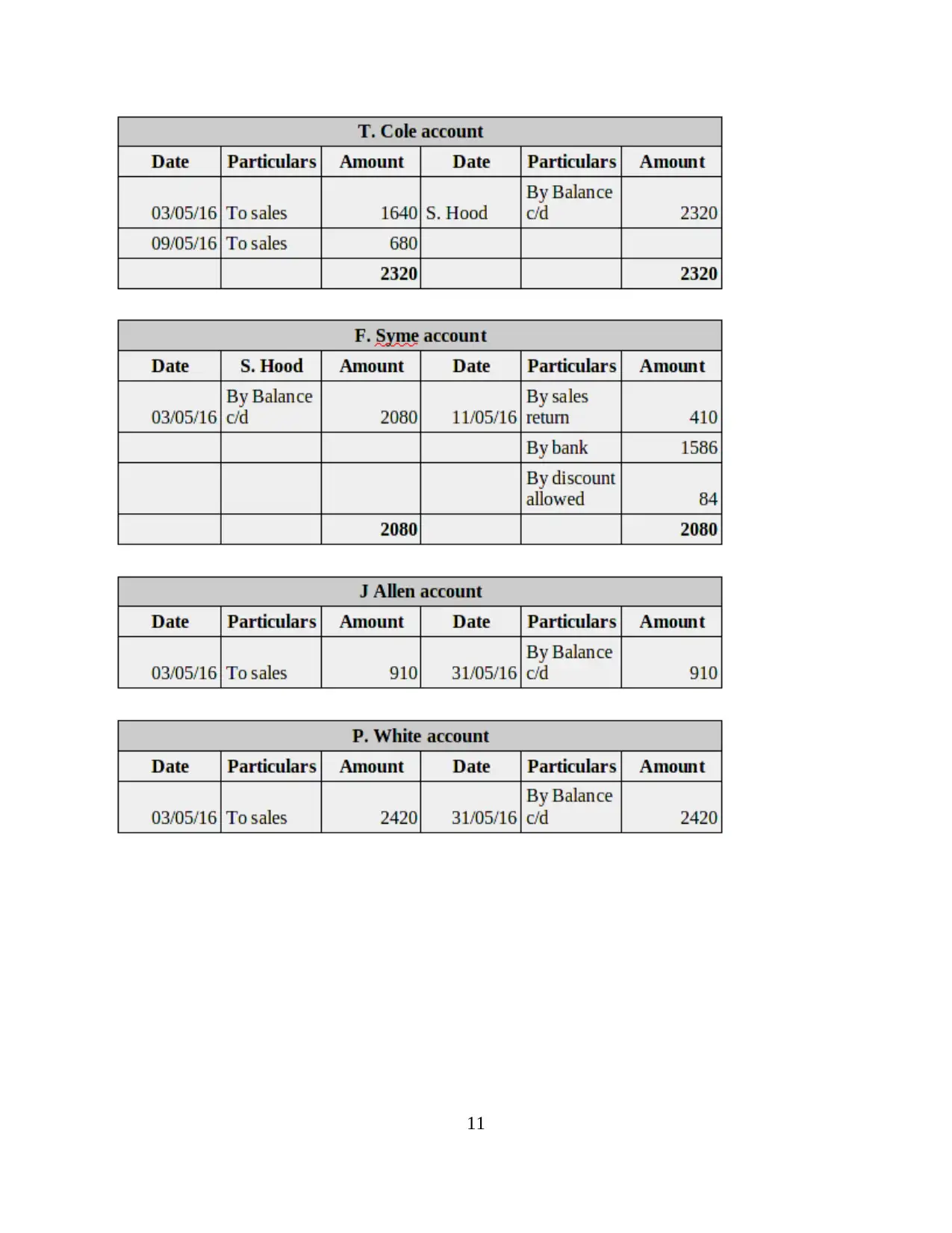

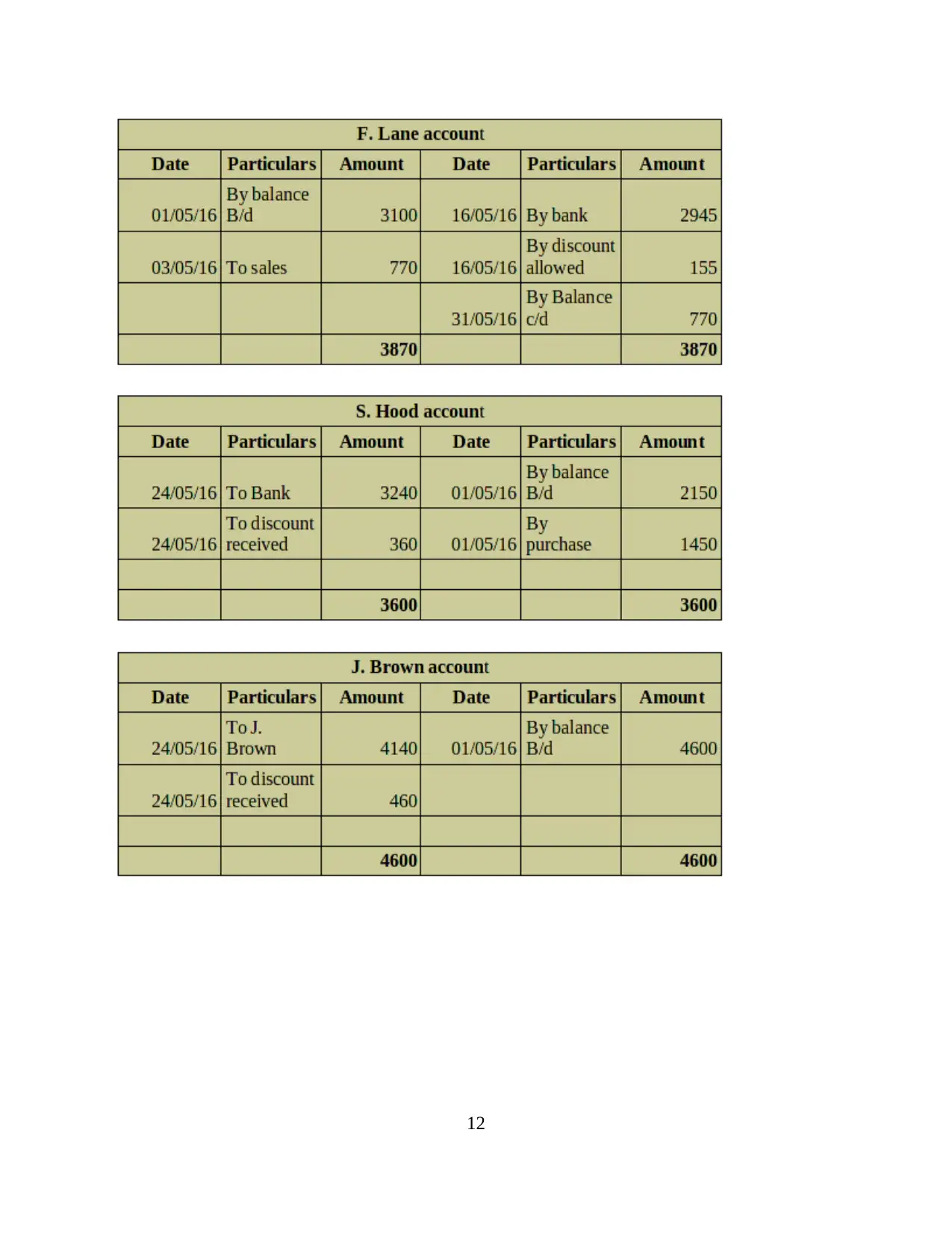

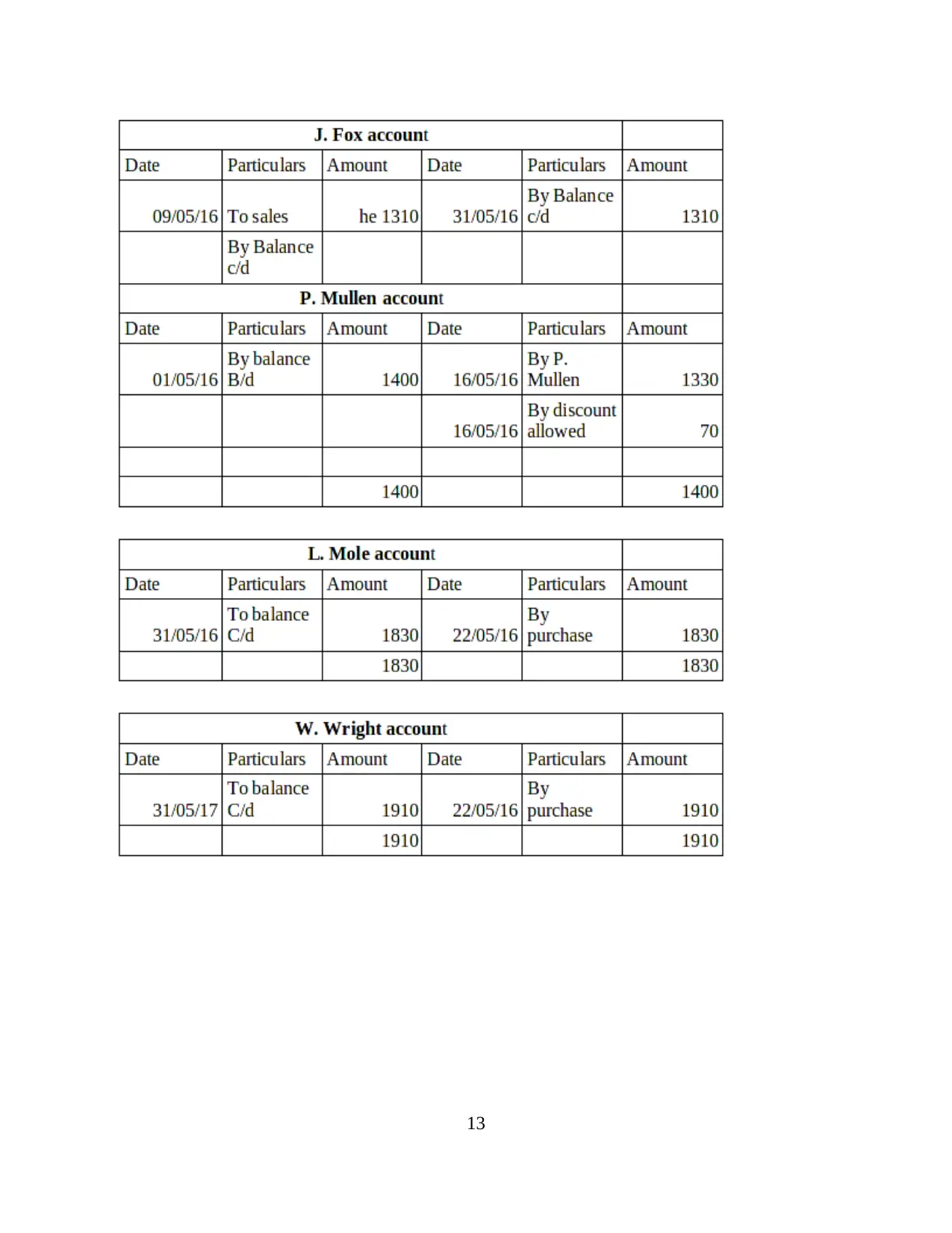

b) Complete double entry recording

5

5

6

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

8

9

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

14

15

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

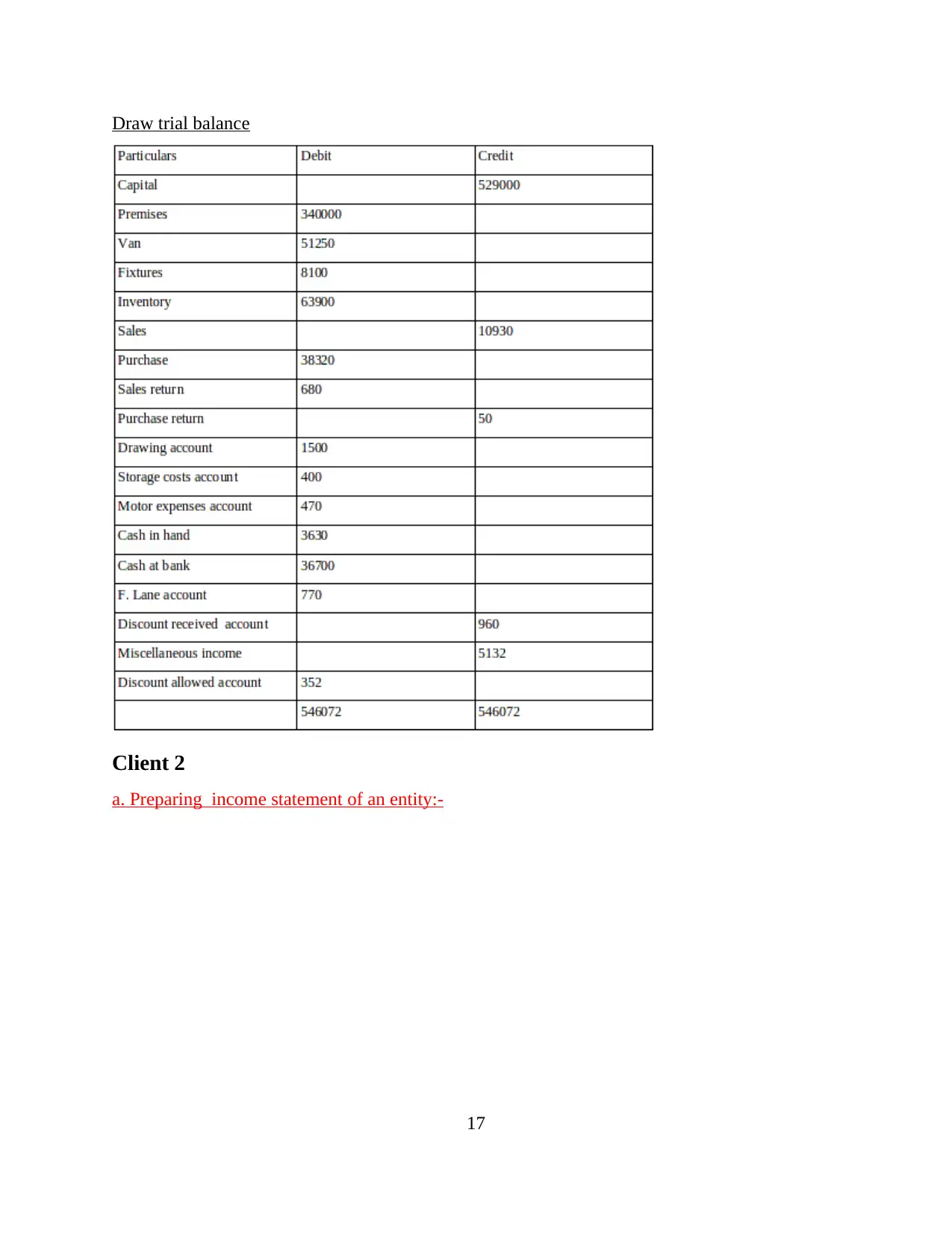

Draw trial balance

Client 2

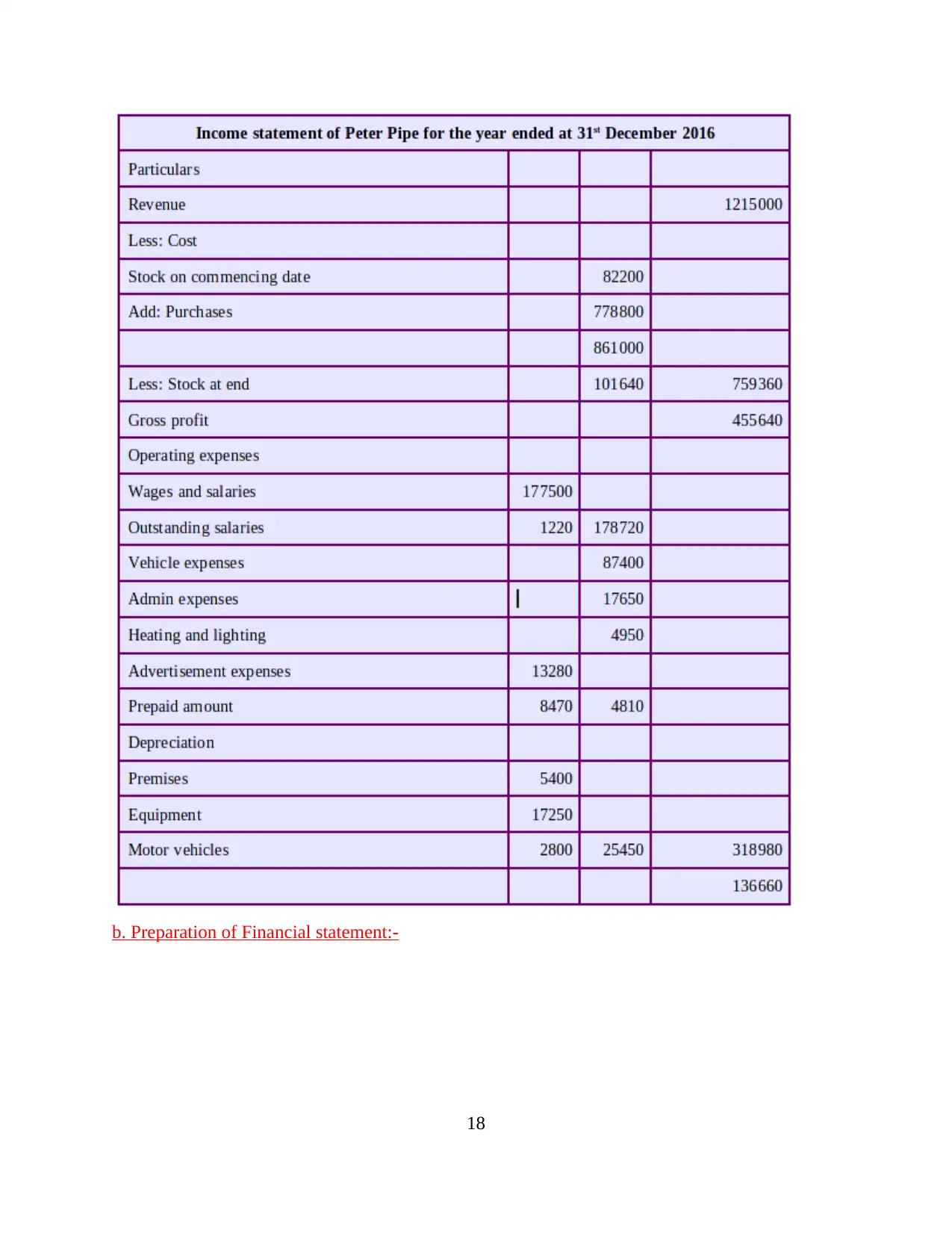

a. Preparing income statement of an entity:-

17

Client 2

a. Preparing income statement of an entity:-

17

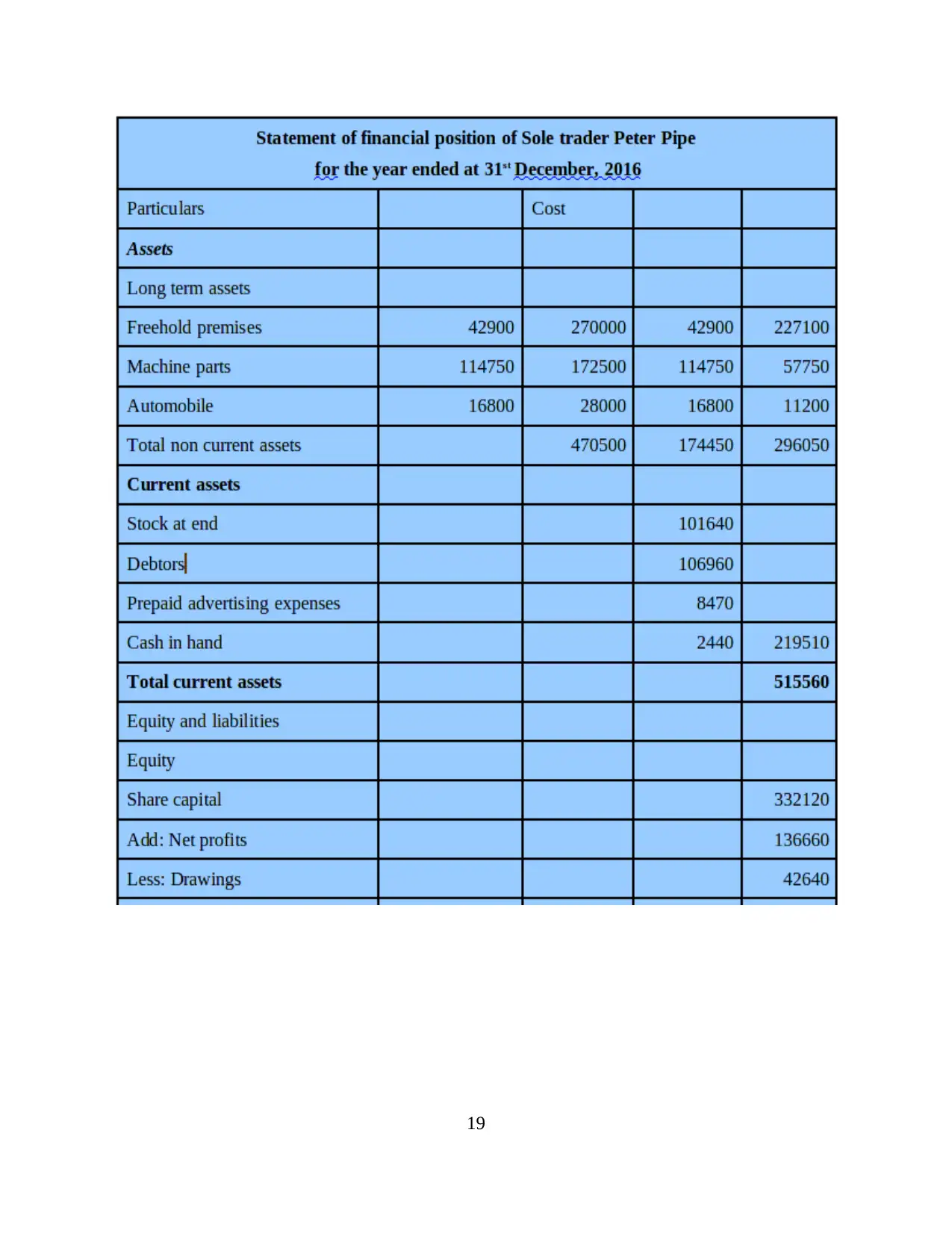

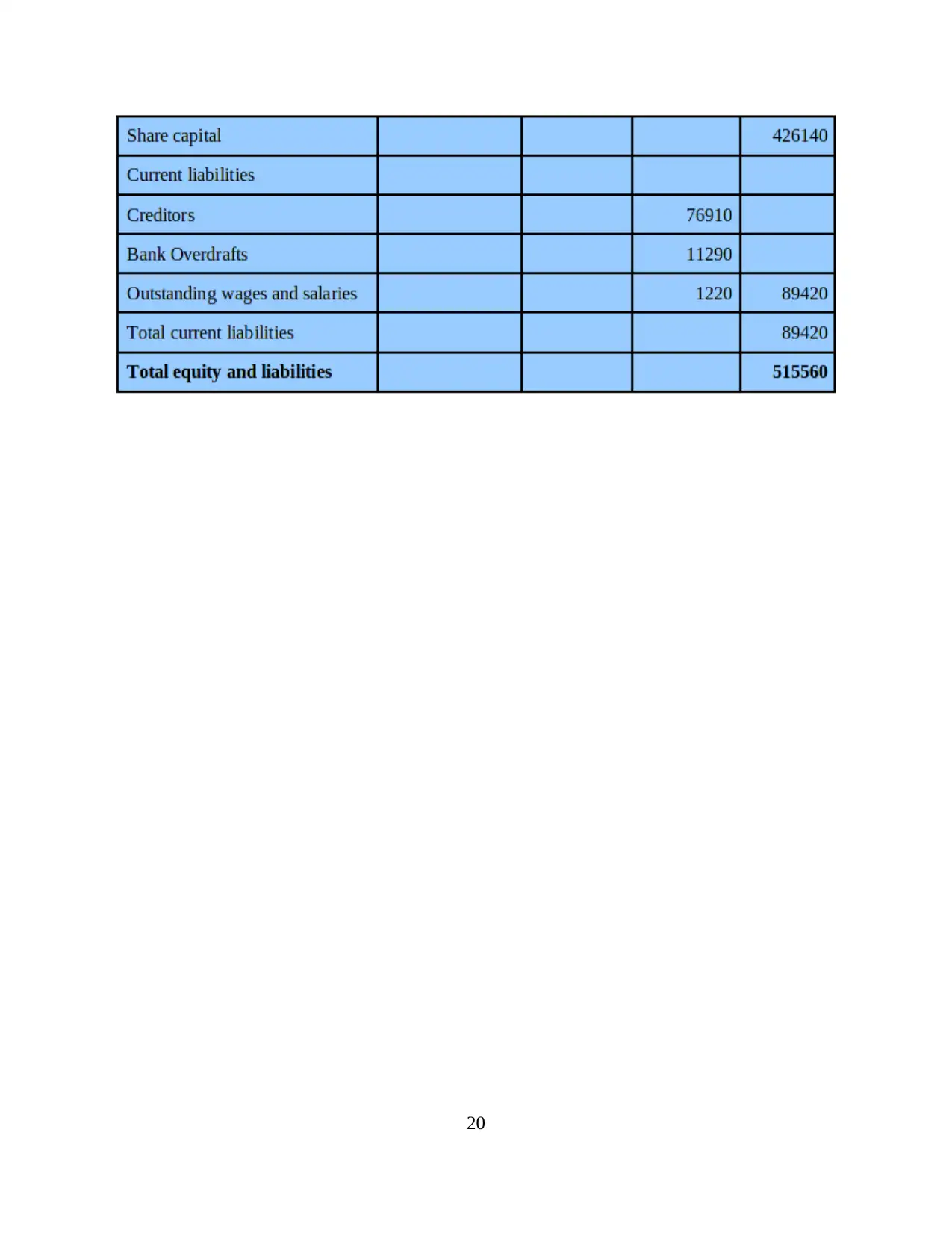

b. Preparation of Financial statement:-

18

18

19

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

20

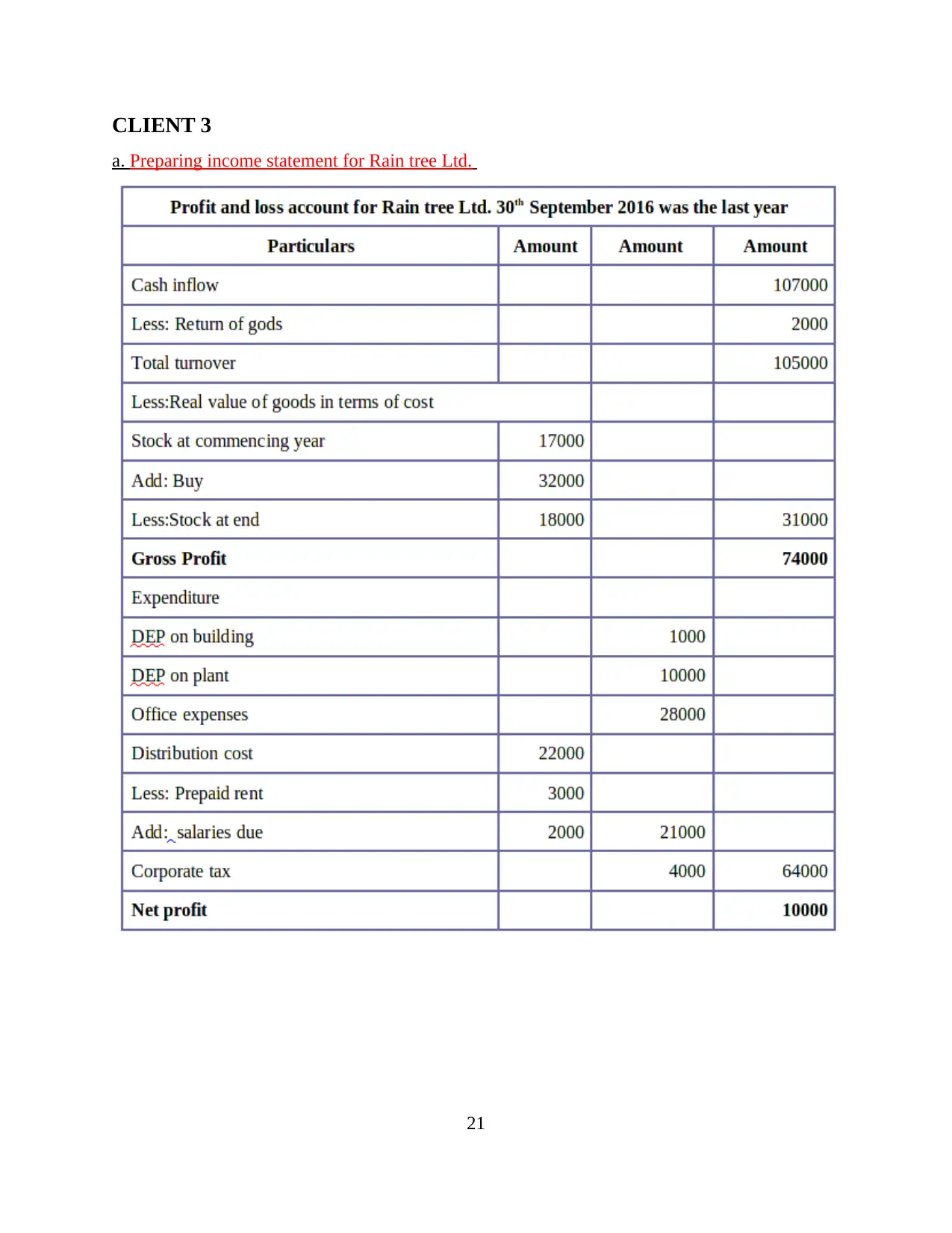

CLIENT 3

a. Preparing income statement for Rain tree Ltd.

21

a. Preparing income statement for Rain tree Ltd.

21

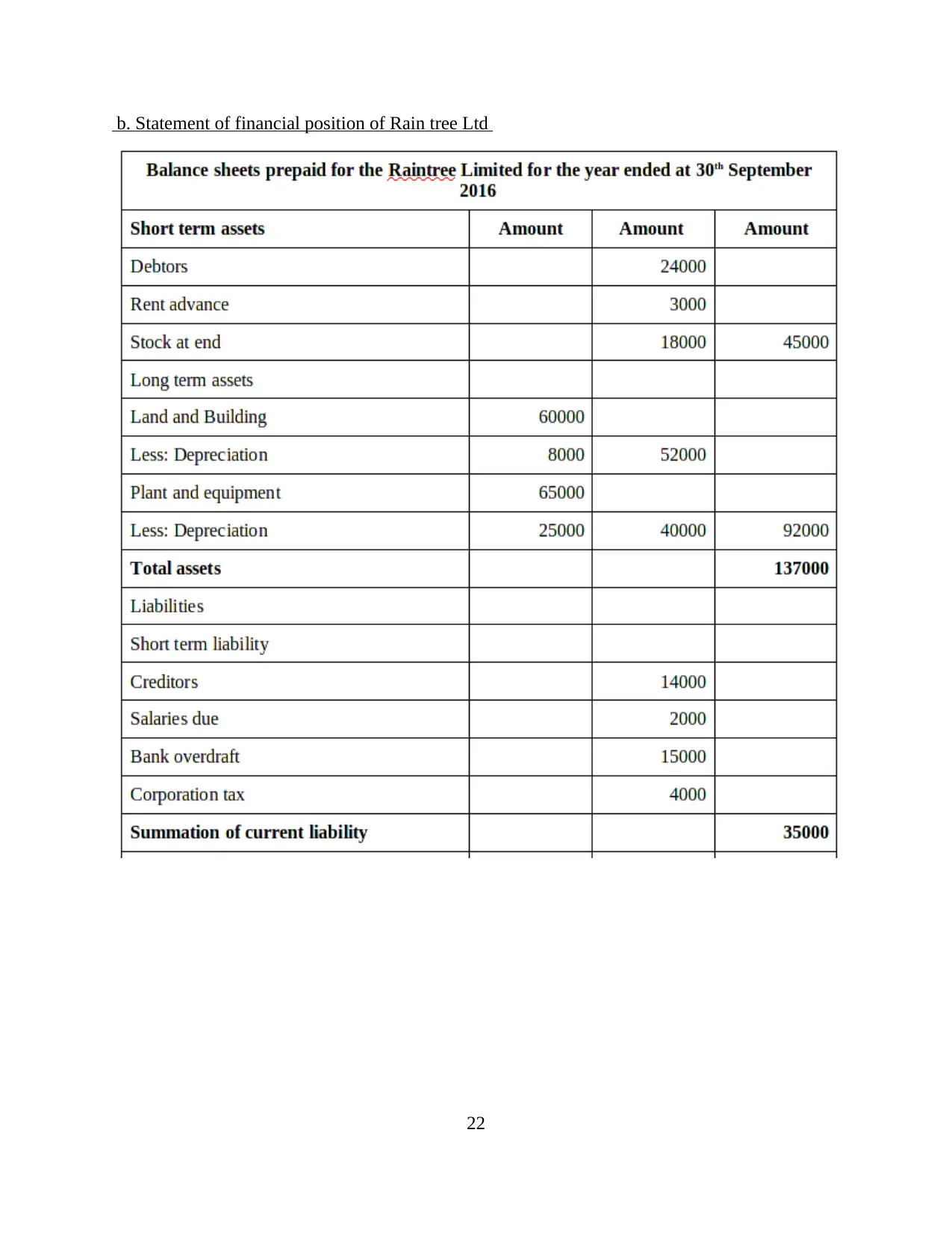

b. Statement of financial position of Rain tree Ltd

22

22

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

C. Justify two concepts of accounting such as consistency and prudence

In the accounting and financials aspect there are several number of the concepts comes

under which are followed by the companies in order to fill books of accounts and make the

financial statements. When the company not able to follow different kinds of the concepts and

aspects of the accounting then in the proper and appropriate manner cannot prepare the financial

statements and determine all kinds of the data and performance (Edwards, 2013). In the

accounting there are mainly two types of the principles or concepts are to be used which are like

as consistency and prudence. Furthermore, both the concepts which rely under the accounting

process are such as follows:

Consistency Concept

Consistency means adopts a one principle for rules in the organization for long time of

period and follow the system by all company's employee on the regular basis. Only modification

an accounting principle or method if the new technology or version than the company adopts

new version for improvement in financial results. Then the organization adopts new technology

for profit maximization or success of company in this competitive market environment. In other

Consistency means to use a particular and specific kind of the aspect and principle on the

continuous basis in the one kind of the criteria. On the basis of this concept the company needs

to used one method and technique for the continuously in the company and there are cannot

make changes in the systems. Once the business and accounting manager adopt and follow one

kind of the accounting principle as well as treatment method then for the further and all the fiscal

periods he must apply and adopt respective type of the system in the entity. There are not any

chance and option for him to use and follow other type of the accounting principle until and

23

In the accounting and financials aspect there are several number of the concepts comes

under which are followed by the companies in order to fill books of accounts and make the

financial statements. When the company not able to follow different kinds of the concepts and

aspects of the accounting then in the proper and appropriate manner cannot prepare the financial

statements and determine all kinds of the data and performance (Edwards, 2013). In the

accounting there are mainly two types of the principles or concepts are to be used which are like

as consistency and prudence. Furthermore, both the concepts which rely under the accounting

process are such as follows:

Consistency Concept

Consistency means adopts a one principle for rules in the organization for long time of

period and follow the system by all company's employee on the regular basis. Only modification

an accounting principle or method if the new technology or version than the company adopts

new version for improvement in financial results. Then the organization adopts new technology

for profit maximization or success of company in this competitive market environment. In other

Consistency means to use a particular and specific kind of the aspect and principle on the

continuous basis in the one kind of the criteria. On the basis of this concept the company needs

to used one method and technique for the continuously in the company and there are cannot

make changes in the systems. Once the business and accounting manager adopt and follow one

kind of the accounting principle as well as treatment method then for the further and all the fiscal

periods he must apply and adopt respective type of the system in the entity. There are not any

chance and option for him to use and follow other type of the accounting principle until and

23

unless feature and aspects of the principle become changes. Apart from adopt only one method

on the continuously basis, in case there are the principle become changes and occurs any kind of

modification then has to make changes in the accounting treatments for preparing the financial

statements (Consistency Concept, 2013). The consistency concept and principle of the

accounting is very important and significant for the business entity because of making the

comparison between previous as well as current. On the basis of such aspect the analysers and

stakeholders like as employees, stockholders, customers etc. also capable to assess the position

and compare from the previous financial performance. Consistency concepts is very important

concept for company because every organization more concern for customers stakeholders or

employee through this accounting concepts because the consistency concept helpful for

organization it is regular method than every user have knowledge about this concept and they are

working on this concepts. Ultimately decision making capacity improves up to the better and

effectual manner of all the stakeholders.

For instance: A business organization using the particular method for assessing

valuation of the stock and inventory available in the firm is such as last in first out method

(LIFO) and adopt the consistency concept for preparing the accounts of stock. Due to using such

concept it must follow same method of stock valuation over the each and every accounting

period to analyses the final value of the stock. Apart from this, in the every year the stock which

produce has to sale in the market at initially and the go for selling old inventory and products to

the customers. Last in first out method is good and beneficial method for every organization

because company have knowledge about stock inventory and company covers last stock

inventory in first because of reduce the problems of dad stock and it is beneficial for the

company.

Prudence Concept

Apart from the consistency concept, there are prudence concept is also one of the widely

used by the companies in order to make reserve in the company which lead to meet the criteria

occurs suddenly. In short, it can be said that prudence concept is helps to the company for

meeting the contingency situation as well as make the appropriate solutions at the time of

problems arises in at the sudden time at the workplace. Moreover, by making the accounting

treatments for resolving the contingency situation the management become more efficient which

24

on the continuously basis, in case there are the principle become changes and occurs any kind of

modification then has to make changes in the accounting treatments for preparing the financial

statements (Consistency Concept, 2013). The consistency concept and principle of the

accounting is very important and significant for the business entity because of making the

comparison between previous as well as current. On the basis of such aspect the analysers and

stakeholders like as employees, stockholders, customers etc. also capable to assess the position

and compare from the previous financial performance. Consistency concepts is very important

concept for company because every organization more concern for customers stakeholders or

employee through this accounting concepts because the consistency concept helpful for

organization it is regular method than every user have knowledge about this concept and they are

working on this concepts. Ultimately decision making capacity improves up to the better and

effectual manner of all the stakeholders.

For instance: A business organization using the particular method for assessing

valuation of the stock and inventory available in the firm is such as last in first out method

(LIFO) and adopt the consistency concept for preparing the accounts of stock. Due to using such

concept it must follow same method of stock valuation over the each and every accounting

period to analyses the final value of the stock. Apart from this, in the every year the stock which

produce has to sale in the market at initially and the go for selling old inventory and products to

the customers. Last in first out method is good and beneficial method for every organization

because company have knowledge about stock inventory and company covers last stock

inventory in first because of reduce the problems of dad stock and it is beneficial for the

company.

Prudence Concept

Apart from the consistency concept, there are prudence concept is also one of the widely

used by the companies in order to make reserve in the company which lead to meet the criteria

occurs suddenly. In short, it can be said that prudence concept is helps to the company for

meeting the contingency situation as well as make the appropriate solutions at the time of

problems arises in at the sudden time at the workplace. Moreover, by making the accounting

treatments for resolving the contingency situation the management become more efficient which

24

because of eliminating the problem which can be comes into consideration at the working

environment on the suddenly (Horngren and et.al., 2012). In addition to this, for keeping the

records of reserve amount to control and resolve the sudden situation there are prudence concept

of accounting is to adopted while preparing the financial statements. Adoption of this concept

than company remove all business trade barrier for running successful business in this

competitive working Environment and for gaining good profit from market or use for customers

retention and new customers attraction for organization.

For example: In the company there are bad debts are often occurs because some clients

or customers purchase the products and services but not able to pay the proper amount of the

product bought. In this case, for create the specific kind of the account such as contra account is

to be made in which the accounts receivables are to be recorded. For this kind of the accounting

treatment there are prudence is to be used which can be on the consistent basis or as per the

understanding of the manager.

D) Explaining two ways of deprecation in the accounting

Deprecation is the concept which shows the value of scrape over the each and every

financial assets which comes under the long term and fixed assets like as plant, machinery,

property, equipment etc. Higher the cost of the assets lead to incur more amount of the

deprecation on the specific kind of the assets which is available within the workplace of the

company. The amount of deprecation is to be incur as well as deduct from the initial cost of the

assets because of the taxation and different accounting purposes. There are mainly two methods

adopted by the businesses for calculate amount of the depreciation which are like as straight line

method (SLM), as well as the written down method (WDM) (Freeman and et.al., 2014). Apart

from this, to determine value of the depreciation on the non current assets there are specific

formula is to be used in the general which is given as below:

Depreciation = Cost of asset – scrape value of asset / estimated life of asset or equipment

Both the methods like as WDM and SLM are explained and described as below:

Straight Line Method-

In the SLM method of the depreciation of assets there are depreciate amount is to be used

and deducted in the books of account same over the each and every financial year. Every

25

environment on the suddenly (Horngren and et.al., 2012). In addition to this, for keeping the

records of reserve amount to control and resolve the sudden situation there are prudence concept

of accounting is to adopted while preparing the financial statements. Adoption of this concept

than company remove all business trade barrier for running successful business in this

competitive working Environment and for gaining good profit from market or use for customers

retention and new customers attraction for organization.

For example: In the company there are bad debts are often occurs because some clients

or customers purchase the products and services but not able to pay the proper amount of the

product bought. In this case, for create the specific kind of the account such as contra account is

to be made in which the accounts receivables are to be recorded. For this kind of the accounting

treatment there are prudence is to be used which can be on the consistent basis or as per the

understanding of the manager.

D) Explaining two ways of deprecation in the accounting

Deprecation is the concept which shows the value of scrape over the each and every

financial assets which comes under the long term and fixed assets like as plant, machinery,

property, equipment etc. Higher the cost of the assets lead to incur more amount of the

deprecation on the specific kind of the assets which is available within the workplace of the

company. The amount of deprecation is to be incur as well as deduct from the initial cost of the

assets because of the taxation and different accounting purposes. There are mainly two methods

adopted by the businesses for calculate amount of the depreciation which are like as straight line

method (SLM), as well as the written down method (WDM) (Freeman and et.al., 2014). Apart

from this, to determine value of the depreciation on the non current assets there are specific

formula is to be used in the general which is given as below:

Depreciation = Cost of asset – scrape value of asset / estimated life of asset or equipment

Both the methods like as WDM and SLM are explained and described as below:

Straight Line Method-

In the SLM method of the depreciation of assets there are depreciate amount is to be used

and deducted in the books of account same over the each and every financial year. Every

25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

company which operates in the industry use the amount of depreciation on the fixed assets which

helps to determine that at the end of year there are how much costing remains with the firm.

Moreover, it able to take decisions that whether the fixed assets needs to sale after some year or

replace it or make expense for maintaining it. Here the amount which assessed in form of the

depreciation is shown in the same amount in the financial accounts of profit and loss which is

one kind of indirect expense for an entity. The current method of depreciation is very easy as

well as simple for calculate within the accounting process and due to such factor the accounting

manager adopt SLM method (Lovell and et.al., 2013). Apart from such things, sometimes there

are more amount and value of the depreciation incur while using the method of SLM in the firm.

In other words with the help of this method company's save more money form deprecation of

assets in future management analyses the actual value of machinery or other assets at present

time for future .With the help of such method the management not need to put more effort

because of simple and easy calcualtion. Further, formula of SLM is such as follows:

Depreciation: SLM = Amount of the depreciable on assets / Useful life of the assets

Depreciable value = cost – salvage value

For example: 250000 – 50000 / 8 years = 25000 GBP

At the cost of 250000 GBP value of the scrape of equipment is 50000 GBP in which

expected life of the machine is 8 years. On the basis of the SLM method depreciation amount is

worth of 25000 GBP which will be carried forward same in the books of account up to the 8

financial years.

Written Down Method-

Another method of the depreciation is such as the written down under which amount of

the decipherable changes over the period of each and every financial years and shows different

amount in the books of profit and loss account. In this the sum of money of the depreciation

which is one of kind of indirect expense for the firm is reduces over the years of fiscal. In this

method,company reduce the all indirect expense for the financial year covers the other

expenditure from the cost of asset or equipment there are percentage of the depreciation are to be

deducted. The amount which remains after deducting depreciation from cost in the first year that

will be consider for the next year (Narayanaswamy, 2014). For example: if the company follow

26

helps to determine that at the end of year there are how much costing remains with the firm.

Moreover, it able to take decisions that whether the fixed assets needs to sale after some year or

replace it or make expense for maintaining it. Here the amount which assessed in form of the

depreciation is shown in the same amount in the financial accounts of profit and loss which is

one kind of indirect expense for an entity. The current method of depreciation is very easy as

well as simple for calculate within the accounting process and due to such factor the accounting

manager adopt SLM method (Lovell and et.al., 2013). Apart from such things, sometimes there

are more amount and value of the depreciation incur while using the method of SLM in the firm.

In other words with the help of this method company's save more money form deprecation of

assets in future management analyses the actual value of machinery or other assets at present

time for future .With the help of such method the management not need to put more effort

because of simple and easy calcualtion. Further, formula of SLM is such as follows:

Depreciation: SLM = Amount of the depreciable on assets / Useful life of the assets

Depreciable value = cost – salvage value

For example: 250000 – 50000 / 8 years = 25000 GBP

At the cost of 250000 GBP value of the scrape of equipment is 50000 GBP in which

expected life of the machine is 8 years. On the basis of the SLM method depreciation amount is

worth of 25000 GBP which will be carried forward same in the books of account up to the 8

financial years.

Written Down Method-

Another method of the depreciation is such as the written down under which amount of

the decipherable changes over the period of each and every financial years and shows different

amount in the books of profit and loss account. In this the sum of money of the depreciation

which is one of kind of indirect expense for the firm is reduces over the years of fiscal. In this

method,company reduce the all indirect expense for the financial year covers the other

expenditure from the cost of asset or equipment there are percentage of the depreciation are to be

deducted. The amount which remains after deducting depreciation from cost in the first year that

will be consider for the next year (Narayanaswamy, 2014). For example: if the company follow

26

WDM where percentage of the depreciation is such as 20% and cost of the machine is like as

300000 GBP. In this case, for the first and more years depreciation amount will be such as

follows:

First year = 300000 * 20% = 60000 GBP

For second year cost of machine will 300000 – 60000 = 240000 and depreciation will be

such as below:

Second year = 240000 * 20% = 48000 GBP

Cost of third year will be 240000 – 48000 = 192000 GBP and amount of depreciation is:

Third year = 192000 * 20% = 38400 GBP.

Up to the expected life of the machine same criteria will be consider by the company.

CLIENT 4

a. Describing doubt account along with its chief characteristic:-

Suspense account that part of an organization printing where it records its uncategorised debits

and credit. This account temporarily acquisitive these unclassified transaction while the

Organization makes judgement about their collection.

Doubtful account is created by an entity owner which is regard as one of the centre thought in the

accounting that helps to correct fault or exclude that takes places in the business activity. It can

be said that this kind of account is come into existence for the temporary purpose in order to

handle all kinds of competitors faced by an entity in its business. Future complexities will be

determined by an individual in the initial phase as this is attentiveness as one of the essential

formulation to be considered aside an entity individual in order of magnitude to improve its

existing business nature. Accounting errors will be ascertained by an entity proprietor that will

improves the existing

Need of doubt account is raised with the increase in complexness of the business

activities that in turn affects the complete business firm's display in a particular time . Main goal

of the enterprise is to accomplish all its desired goal and the subjective by identifying all the

errors or frauds at the initial stage as improving its performance initially will be helpful for an

entity in order to improve the quality of transactions to be recorded in the financial statement's

27

300000 GBP. In this case, for the first and more years depreciation amount will be such as

follows:

First year = 300000 * 20% = 60000 GBP

For second year cost of machine will 300000 – 60000 = 240000 and depreciation will be

such as below:

Second year = 240000 * 20% = 48000 GBP

Cost of third year will be 240000 – 48000 = 192000 GBP and amount of depreciation is:

Third year = 192000 * 20% = 38400 GBP.

Up to the expected life of the machine same criteria will be consider by the company.

CLIENT 4

a. Describing doubt account along with its chief characteristic:-

Suspense account that part of an organization printing where it records its uncategorised debits

and credit. This account temporarily acquisitive these unclassified transaction while the

Organization makes judgement about their collection.

Doubtful account is created by an entity owner which is regard as one of the centre thought in the

accounting that helps to correct fault or exclude that takes places in the business activity. It can

be said that this kind of account is come into existence for the temporary purpose in order to

handle all kinds of competitors faced by an entity in its business. Future complexities will be

determined by an individual in the initial phase as this is attentiveness as one of the essential

formulation to be considered aside an entity individual in order of magnitude to improve its

existing business nature. Accounting errors will be ascertained by an entity proprietor that will

improves the existing

Need of doubt account is raised with the increase in complexness of the business

activities that in turn affects the complete business firm's display in a particular time . Main goal

of the enterprise is to accomplish all its desired goal and the subjective by identifying all the

errors or frauds at the initial stage as improving its performance initially will be helpful for an

entity in order to improve the quality of transactions to be recorded in the financial statement's

27

(Lovell, 2014). True formation is essential to e included in the financial statement as this will

reflect true image of the business concern in front of the external market users. Suspense account

terminology is used in accounting refers to recording all debit and credit transactions in the

existing accounting records to influence the actual fiscal perspective of an entity. This charitable

of account is make by an entity in their business for transitory purpose element this suspenseful

account unt is just created in state to meet the external difficulties imposed on an entity for

limited span of time. The suspense account is used in the accounting records generally in the

general ledger in the books of accounts to improve the overall efficiency of all the transactions

recorded in the existing books of accounts as its desired aim is to capture higher market share by

reflect true image of an entity. Value of suspense report affects the functioning and success of an

organisation and also the firm is not able to fulfil its aims. It is helpful for analysis of financial

point of the organization on different areas and covers all the debts burden and credit transaction

of an organisation. Determine the financial position of the organization or other external source

covers through the Doubt account for compete with other market leaders for running the business

and reduce all internal or external expenditure of the organization and with the help of doubt

account company reduce the trade barriers at te of international.

From the perspective business the meaning of this suspense account gets changes as

external market changes will be take into consideration by an entity in order to present its true

image in front of external market users. Suspense account will be helpful for an entity in order to

considered all kinds of accounting errors takes paces in an entity (Cuckston, 2013). There are

different kinds of errors incurred in the business such as error of omission in which the

intentional mistake of accountant a particular transaction omitted to be recorded in the books of

accounts. The accounting process has a connected link with the existing performance of an entity

as this will help in ascertaining the financial performance of the business concern. Function of an

entity acquire flexure with the transition of time as in this particular case quality of all the

business transactions in which each and every transactions to be considered by an entity owner.

Temporary nature of this particular account alert the top management in ensuring its overall

business performance. Quality of all accounting transactions will get improved as the desired aim

of the business enterprise is to gain higher competitive advantage in the external business

environment. This particular method is attentiveness as one of the of the essence formulation that

will be exploited by the business concern in order of magnitude to consider each and every

28

reflect true image of the business concern in front of the external market users. Suspense account

terminology is used in accounting refers to recording all debit and credit transactions in the

existing accounting records to influence the actual fiscal perspective of an entity. This charitable

of account is make by an entity in their business for transitory purpose element this suspenseful

account unt is just created in state to meet the external difficulties imposed on an entity for

limited span of time. The suspense account is used in the accounting records generally in the

general ledger in the books of accounts to improve the overall efficiency of all the transactions

recorded in the existing books of accounts as its desired aim is to capture higher market share by

reflect true image of an entity. Value of suspense report affects the functioning and success of an

organisation and also the firm is not able to fulfil its aims. It is helpful for analysis of financial

point of the organization on different areas and covers all the debts burden and credit transaction

of an organisation. Determine the financial position of the organization or other external source

covers through the Doubt account for compete with other market leaders for running the business

and reduce all internal or external expenditure of the organization and with the help of doubt

account company reduce the trade barriers at te of international.

From the perspective business the meaning of this suspense account gets changes as

external market changes will be take into consideration by an entity in order to present its true

image in front of external market users. Suspense account will be helpful for an entity in order to

considered all kinds of accounting errors takes paces in an entity (Cuckston, 2013). There are

different kinds of errors incurred in the business such as error of omission in which the

intentional mistake of accountant a particular transaction omitted to be recorded in the books of

accounts. The accounting process has a connected link with the existing performance of an entity

as this will help in ascertaining the financial performance of the business concern. Function of an

entity acquire flexure with the transition of time as in this particular case quality of all the

business transactions in which each and every transactions to be considered by an entity owner.

Temporary nature of this particular account alert the top management in ensuring its overall

business performance. Quality of all accounting transactions will get improved as the desired aim

of the business enterprise is to gain higher competitive advantage in the external business

environment. This particular method is attentiveness as one of the of the essence formulation that

will be exploited by the business concern in order of magnitude to consider each and every

28

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

factors lies in the external business environment to represent its true image in front of the

stakeholders as investors will rely upon the annular financial statement's of an entity in a

particular financial year. The doubt account can be comparison with the rectification of errors

that is attentiveness as the of the essence conception in the accounting concept (Watrin, Pott and

Ullmann, 2012). In this particulate approach, all actual treatment in the accounting records are

compared with the wrong treatment made by an entity in order to ascertain all the errors found

by the investigator in the books of accounts of the business entity. Business efficiency will be

ascertained with the help of this particular approach that enhances the overall quality of an entity

in order to target higher users of the external business environment.

CLIENT 5

a. Explaining bank reconciliation statement

Nowadays frauds ad errors has become on of the important business issue that needs to

be ascertained by an individual in the initial stage in order to protect its overall brand image.

Bank reconciliation statement is regarded as the monitoring tool in which existing

performance of the firm will e compared with the bank statement in order to know the different

lies between actual cash book and bank pass to now the material misstatements. This kind of

statements are prepared in every entity as it reveals the shortfalls lies in the actual business

enterprise n order to improve the existing performance of the corporation in both manner such as

qualitative as well as quantitative performance of the business entity. This is act like a

comparison tool in which actual business performance will be compared with the bank balance

of an entity (Biondi and et.al., 2012). It is regarded as the process that shows the difference

between cash balance of bank and organization which will assistance an entity in state to focus

on desired goal and mark of the business concern entity to be completed within a given span of

time. All kinds of deposits whether cash or any other kinds of deposits in the business will be

analyses properly in relation to the external market aims and targets to be accomplished in a

given time period.

It contains all kinds of transactions incurred in an entity that involves all types of cheques

written by an entity owner for the purpose of dealing various operations of a business are

checked in accordance with the dates mentioned on the cheque. Series wise cheque is record is

mentioned in the books of accounts in dictation to determine the actual financial presentation of

29

stakeholders as investors will rely upon the annular financial statement's of an entity in a

particular financial year. The doubt account can be comparison with the rectification of errors

that is attentiveness as the of the essence conception in the accounting concept (Watrin, Pott and

Ullmann, 2012). In this particulate approach, all actual treatment in the accounting records are

compared with the wrong treatment made by an entity in order to ascertain all the errors found

by the investigator in the books of accounts of the business entity. Business efficiency will be

ascertained with the help of this particular approach that enhances the overall quality of an entity

in order to target higher users of the external business environment.

CLIENT 5

a. Explaining bank reconciliation statement

Nowadays frauds ad errors has become on of the important business issue that needs to

be ascertained by an individual in the initial stage in order to protect its overall brand image.

Bank reconciliation statement is regarded as the monitoring tool in which existing

performance of the firm will e compared with the bank statement in order to know the different

lies between actual cash book and bank pass to now the material misstatements. This kind of

statements are prepared in every entity as it reveals the shortfalls lies in the actual business

enterprise n order to improve the existing performance of the corporation in both manner such as

qualitative as well as quantitative performance of the business entity. This is act like a

comparison tool in which actual business performance will be compared with the bank balance

of an entity (Biondi and et.al., 2012). It is regarded as the process that shows the difference

between cash balance of bank and organization which will assistance an entity in state to focus

on desired goal and mark of the business concern entity to be completed within a given span of

time. All kinds of deposits whether cash or any other kinds of deposits in the business will be

analyses properly in relation to the external market aims and targets to be accomplished in a

given time period.

It contains all kinds of transactions incurred in an entity that involves all types of cheques

written by an entity owner for the purpose of dealing various operations of a business are

checked in accordance with the dates mentioned on the cheque. Series wise cheque is record is

mentioned in the books of accounts in dictation to determine the actual financial presentation of

29

an entity with the transition of time in order to get actual business performance within a given

span of time. All the transactions incurred in an entity are properly checked with the similar

vouchers of all the transactions incurred in the business enterprise. The true meaning of bank

reconciliation statement is that bank balance will be matched with the cash balance by knowing

all the transaction's efficiency incurred in an entity. Various review procedures are used aside an

entity businessman in order to analyze all the transactions incurred in the organization enterprise

(Carvalho and Salotti, 2012). This kind of message prepared by an entity will be helpful for an

enterprise owner in order to collect relevant information by analyzing the bank reconciliation

statement's as this will generate all actual transactions incurred in the business to be rectified by

considering all the transactions to e included in the business transactions incurred in the business.

Consistency will be maintained by an entity owner y using this particular method as this will

ascertain the existing efficiency of an entity in order to eliminate all kinds of frauds or errors

incurred in the business. Errors are identified initial will help an entity proprietor in command to

accomplishing the desirable market purpose and mark in order to achieve all targets and

objectives in less period. Role of an entity gets increases by providing wide number of

opportunities by taken into consideration all the facts and figures which are essential for the

business in minimizing its deficiencies and enhancing its overall quality. Now a days bank facing

many issues of fraud and errors but bank have more concern on document verification of the

organization or client and after verification they provide transaction permission for organization

or client because of just improvement of performance working for organization achieve te gaol

and target of production.

b. Measure the reasons due to which bank records conform from cash book:-

Changes may be incurred in the bank reconciliation statement's due to several reasons

that created lost of changes due to different balance show in the cash book and bank pass book of

an entity which needs to be checked properly. The differences arise in both the statements is due

to cheque deposited in the bank but its balance does not credit by the bank. This particular

change incurred in the business will differentiates the overall balance of both bank pass book and

cash balance of cash book of an entity. The cash book balance shows higher than compared to

the balance of bank needs to be adjust properly in order to reconcile both the figure appropriately

in order to enhance the existing performance of an entity (Prabowo and Tambotoh, 2012).

Another differences created in both the book is due to hidden transactions charged by the bank

30

span of time. All the transactions incurred in an entity are properly checked with the similar

vouchers of all the transactions incurred in the business enterprise. The true meaning of bank

reconciliation statement is that bank balance will be matched with the cash balance by knowing

all the transaction's efficiency incurred in an entity. Various review procedures are used aside an

entity businessman in order to analyze all the transactions incurred in the organization enterprise

(Carvalho and Salotti, 2012). This kind of message prepared by an entity will be helpful for an

enterprise owner in order to collect relevant information by analyzing the bank reconciliation

statement's as this will generate all actual transactions incurred in the business to be rectified by

considering all the transactions to e included in the business transactions incurred in the business.

Consistency will be maintained by an entity owner y using this particular method as this will

ascertain the existing efficiency of an entity in order to eliminate all kinds of frauds or errors

incurred in the business. Errors are identified initial will help an entity proprietor in command to

accomplishing the desirable market purpose and mark in order to achieve all targets and

objectives in less period. Role of an entity gets increases by providing wide number of

opportunities by taken into consideration all the facts and figures which are essential for the

business in minimizing its deficiencies and enhancing its overall quality. Now a days bank facing

many issues of fraud and errors but bank have more concern on document verification of the

organization or client and after verification they provide transaction permission for organization

or client because of just improvement of performance working for organization achieve te gaol

and target of production.

b. Measure the reasons due to which bank records conform from cash book:-

Changes may be incurred in the bank reconciliation statement's due to several reasons

that created lost of changes due to different balance show in the cash book and bank pass book of

an entity which needs to be checked properly. The differences arise in both the statements is due

to cheque deposited in the bank but its balance does not credit by the bank. This particular

change incurred in the business will differentiates the overall balance of both bank pass book and

cash balance of cash book of an entity. The cash book balance shows higher than compared to

the balance of bank needs to be adjust properly in order to reconcile both the figure appropriately

in order to enhance the existing performance of an entity (Prabowo and Tambotoh, 2012).

Another differences created in both the book is due to hidden transactions charged by the bank

30

such as interest or charge of commissions are not recorded in the cash book of an entity as

business owner are not ware about the expenditures charged by the bank intentionally on their

own. The correct treatment will be made by an entity by believe the true facts and illustration by

comparing both of the statement in order to present the true figures in the business.

Changes may be incurred in the bank verification Statement's due to many reasons tht create loss

of modification due to difference balance shows in the payment book and pass book of entity

which needs to be patterned properly.

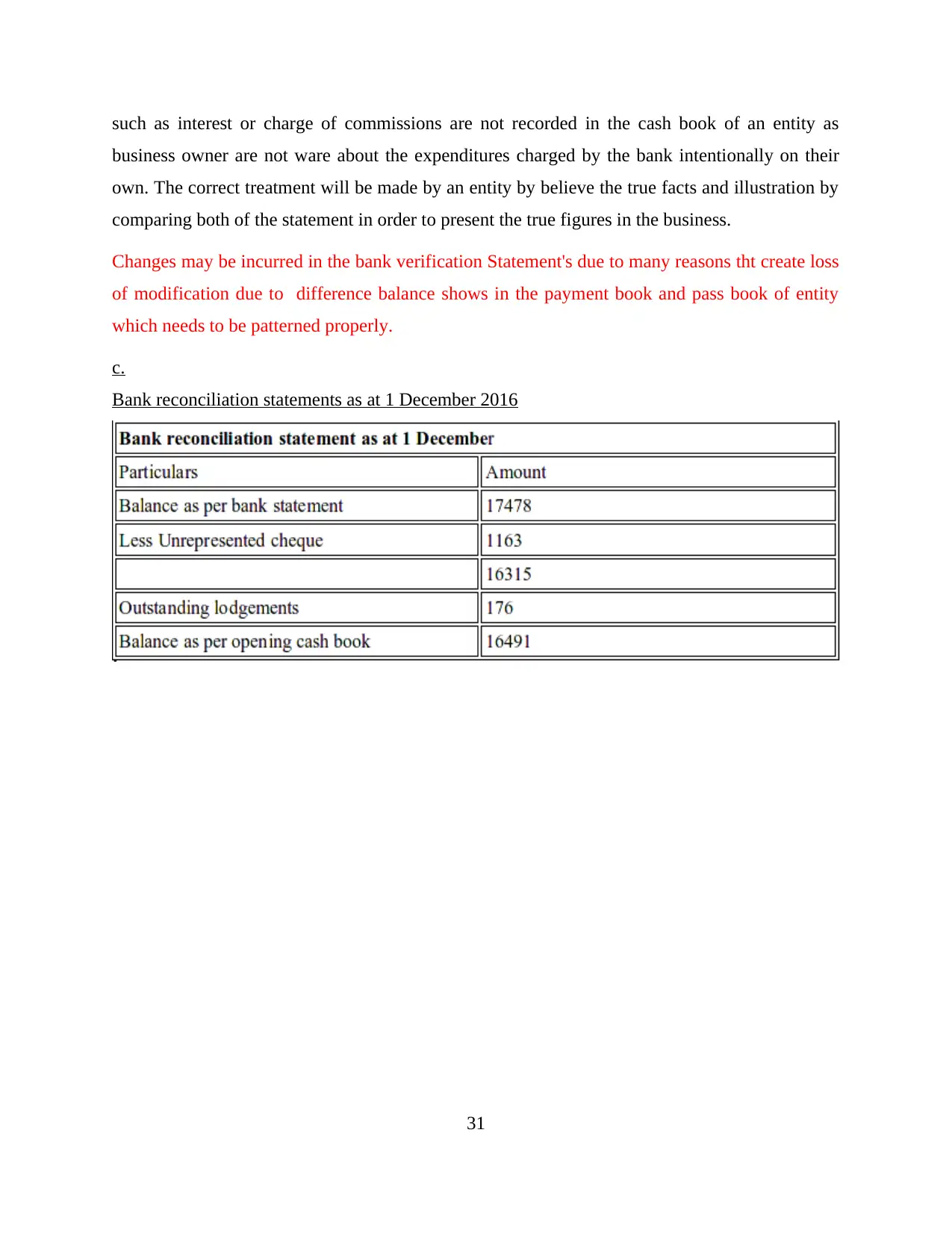

c.

Bank reconciliation statements as at 1 December 2016

31

business owner are not ware about the expenditures charged by the bank intentionally on their

own. The correct treatment will be made by an entity by believe the true facts and illustration by

comparing both of the statement in order to present the true figures in the business.

Changes may be incurred in the bank verification Statement's due to many reasons tht create loss

of modification due to difference balance shows in the payment book and pass book of entity

which needs to be patterned properly.

c.

Bank reconciliation statements as at 1 December 2016

31

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

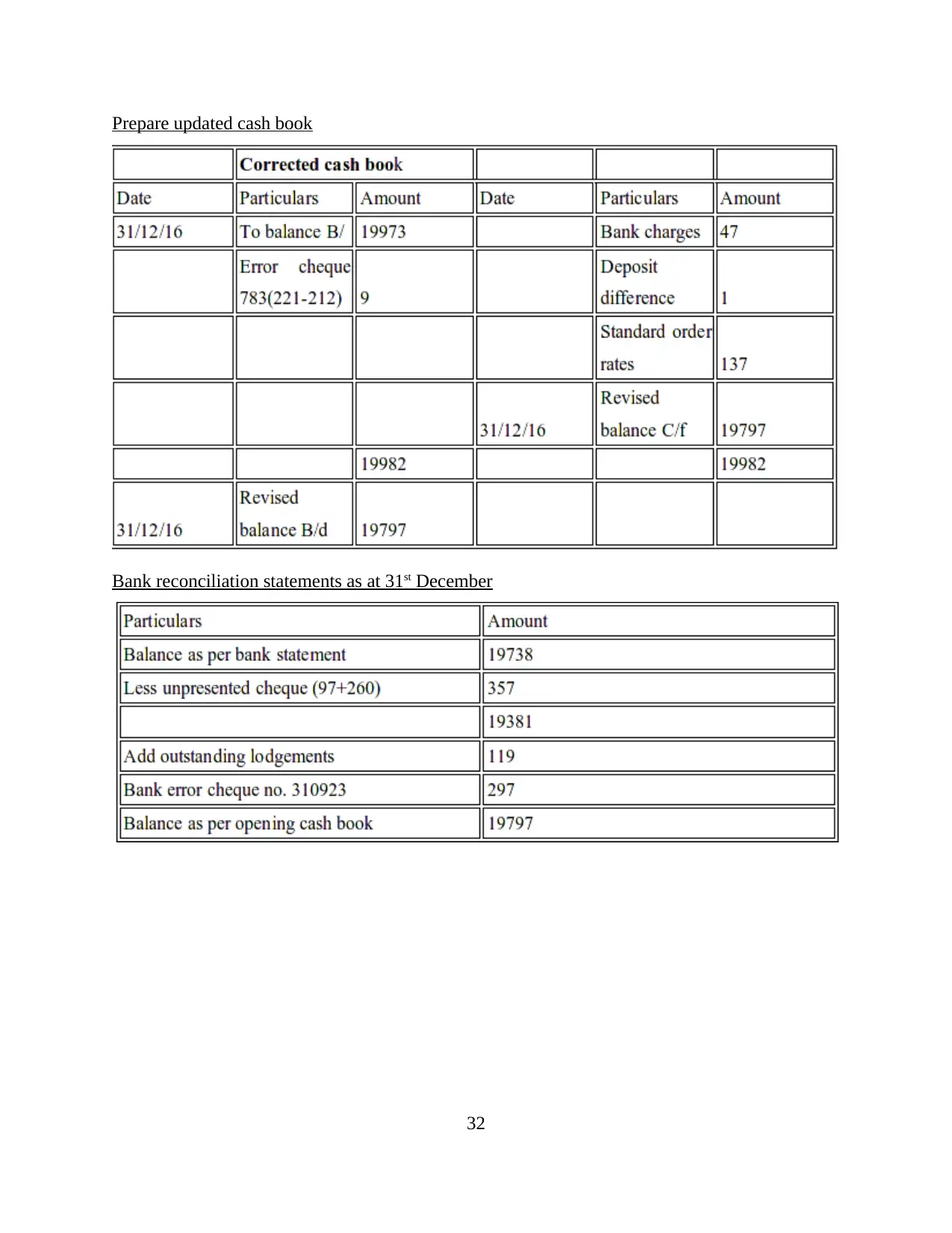

Prepare updated cash book

Bank reconciliation statements as at 31st December

32

Bank reconciliation statements as at 31st December

32

CLIENT 6

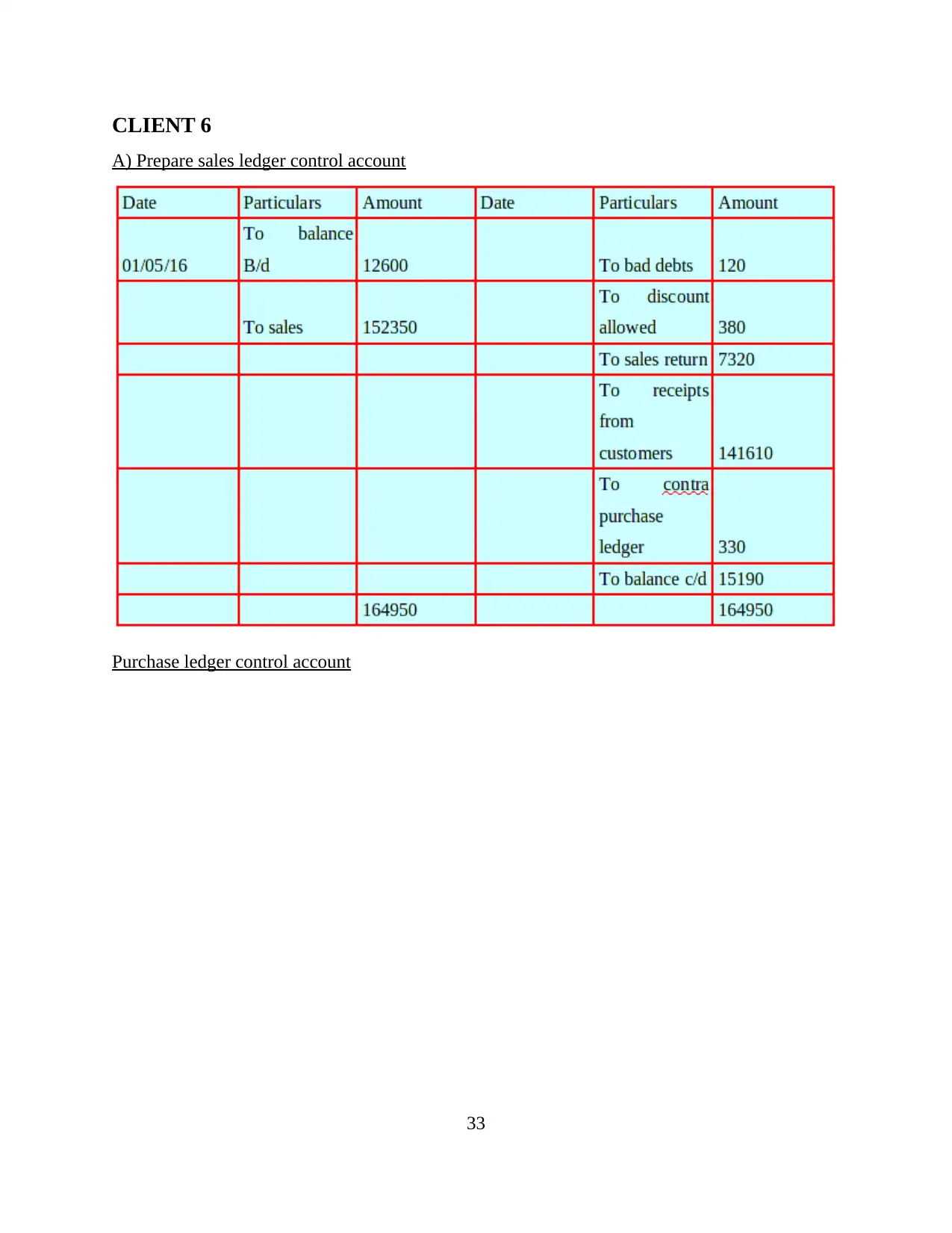

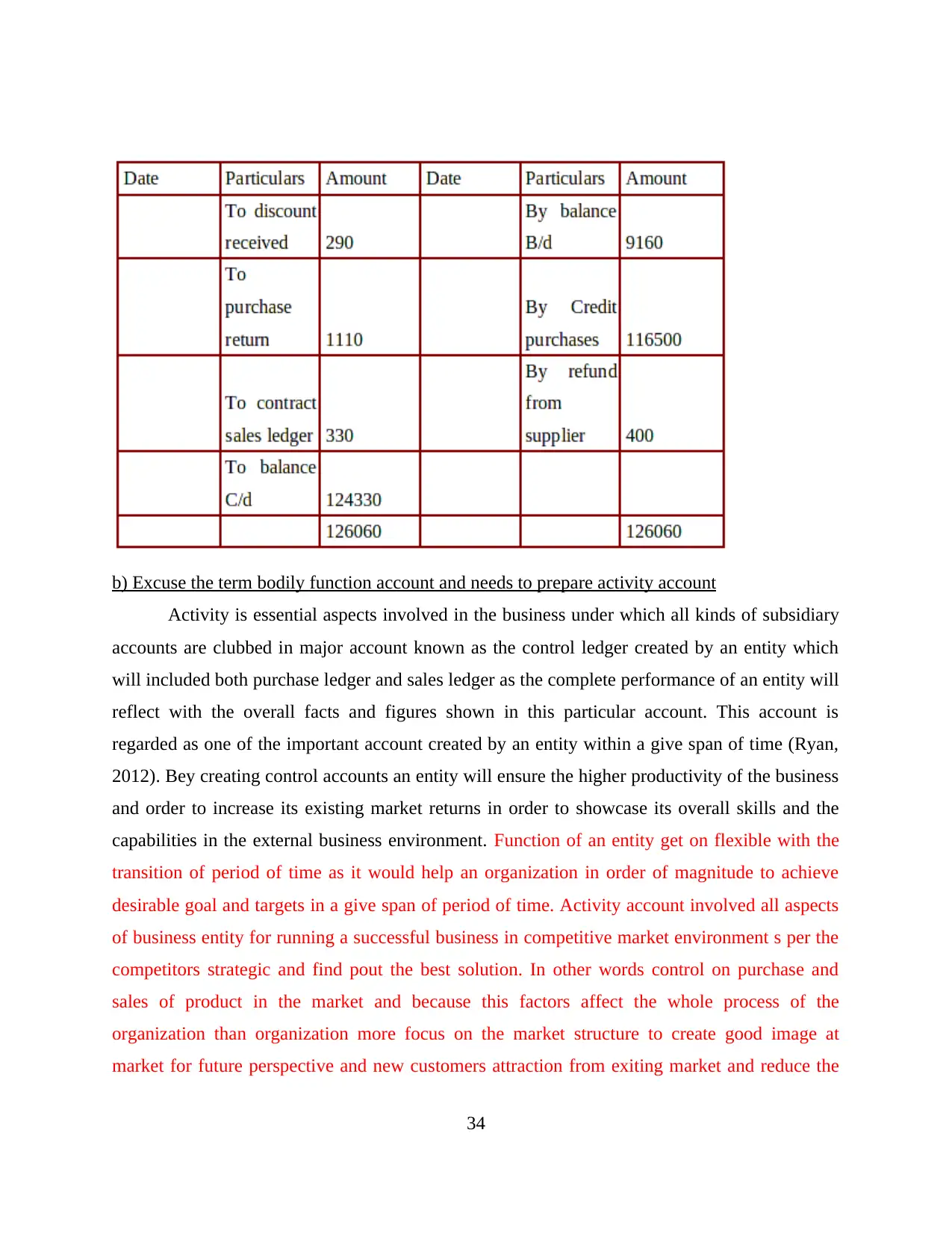

A) Prepare sales ledger control account

Purchase ledger control account

33

A) Prepare sales ledger control account

Purchase ledger control account

33

b) Excuse the term bodily function account and needs to prepare activity account

Activity is essential aspects involved in the business under which all kinds of subsidiary

accounts are clubbed in major account known as the control ledger created by an entity which

will included both purchase ledger and sales ledger as the complete performance of an entity will

reflect with the overall facts and figures shown in this particular account. This account is

regarded as one of the important account created by an entity within a give span of time (Ryan,

2012). Bey creating control accounts an entity will ensure the higher productivity of the business

and order to increase its existing market returns in order to showcase its overall skills and the

capabilities in the external business environment. Function of an entity get on flexible with the

transition of period of time as it would help an organization in order of magnitude to achieve

desirable goal and targets in a give span of period of time. Activity account involved all aspects

of business entity for running a successful business in competitive market environment s per the

competitors strategic and find pout the best solution. In other words control on purchase and

sales of product in the market and because this factors affect the whole process of the

organization than organization more focus on the market structure to create good image at

market for future perspective and new customers attraction from exiting market and reduce the

34

Activity is essential aspects involved in the business under which all kinds of subsidiary

accounts are clubbed in major account known as the control ledger created by an entity which

will included both purchase ledger and sales ledger as the complete performance of an entity will

reflect with the overall facts and figures shown in this particular account. This account is

regarded as one of the important account created by an entity within a give span of time (Ryan,

2012). Bey creating control accounts an entity will ensure the higher productivity of the business

and order to increase its existing market returns in order to showcase its overall skills and the

capabilities in the external business environment. Function of an entity get on flexible with the

transition of period of time as it would help an organization in order of magnitude to achieve

desirable goal and targets in a give span of period of time. Activity account involved all aspects

of business entity for running a successful business in competitive market environment s per the

competitors strategic and find pout the best solution. In other words control on purchase and

sales of product in the market and because this factors affect the whole process of the

organization than organization more focus on the market structure to create good image at

market for future perspective and new customers attraction from exiting market and reduce the

34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

cost of many expenditure on wastes in the organization. It would helpful for the company In

terms of achieving goal and target in short period of time.

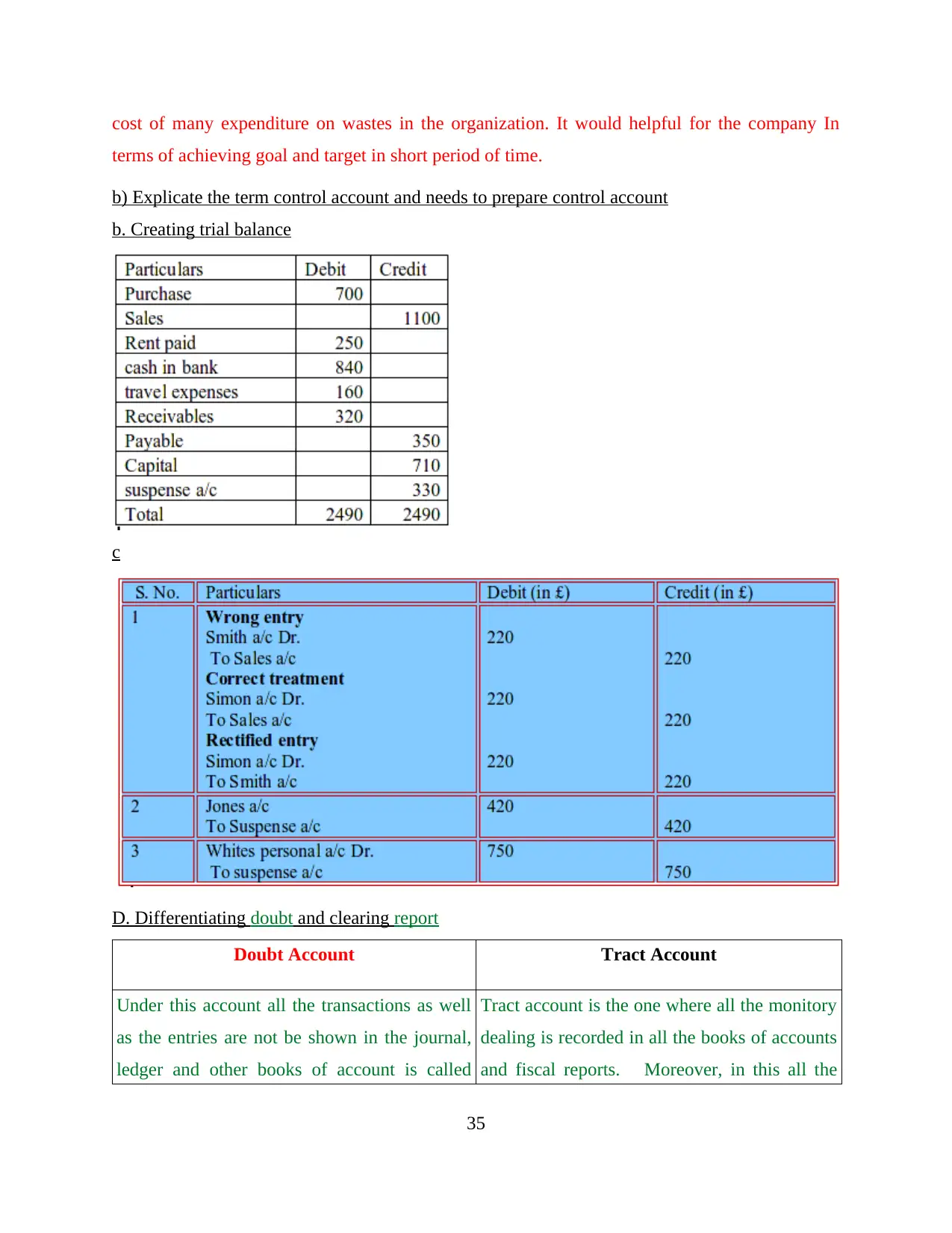

b) Explicate the term control account and needs to prepare control account

b. Creating trial balance

c

D. Differentiating doubt and clearing report

Doubt Account Tract Account

Under this account all the transactions as well

as the entries are not be shown in the journal,

ledger and other books of account is called

Tract account is the one where all the monitory

dealing is recorded in all the books of accounts

and fiscal reports. Moreover, in this all the

35

terms of achieving goal and target in short period of time.

b) Explicate the term control account and needs to prepare control account

b. Creating trial balance

c

D. Differentiating doubt and clearing report

Doubt Account Tract Account

Under this account all the transactions as well

as the entries are not be shown in the journal,

ledger and other books of account is called

Tract account is the one where all the monitory

dealing is recorded in all the books of accounts

and fiscal reports. Moreover, in this all the

35

doubt account in the accounting construct

(Bryer, 2013).

written record and belief and taped decently

and guarantee that whether these are the right

and broad or not.

A doubt account is not distinct by the account

director if there some kind of minutes are not

shown and made in the financial statements.

When speaking about the tract account then

until and unless all the transactions like as

report receivables and payables are not distinct

and made then it not prepares.

It not reasoned as the extremely crucial and

important type of the report at the time period

of making all the final accounts and reports.

On the other side, clearing report is regarded as

one of the highly significant report for the

company (Choi, 2013).

CONCLUSION

It can be summarized from the above assignment that accounting is regarded as one f the

important tool that enhances the existing performance of an entity within a give span of time.

This report emphasizes on recording of all kinds of transactions using journal entry till the

preparation of trial balance that will determines all the errors of frauds traced by an individual

while recording all kinds of business transactions in its business enterprise. This report

emphasizes on rectification of errors found by an entity in the given project report. Balance sheet

or income statement will be prepared in dictation to reflect the financial presentation of an entity

in state to target all potential stakeholders who are interested in knowing the actual market status

of the business in order of magnitude to grab high market reward in the outside business

environment.

36

(Bryer, 2013).

written record and belief and taped decently

and guarantee that whether these are the right

and broad or not.

A doubt account is not distinct by the account

director if there some kind of minutes are not

shown and made in the financial statements.

When speaking about the tract account then

until and unless all the transactions like as

report receivables and payables are not distinct

and made then it not prepares.

It not reasoned as the extremely crucial and

important type of the report at the time period

of making all the final accounts and reports.

On the other side, clearing report is regarded as

one of the highly significant report for the

company (Choi, 2013).

CONCLUSION

It can be summarized from the above assignment that accounting is regarded as one f the

important tool that enhances the existing performance of an entity within a give span of time.

This report emphasizes on recording of all kinds of transactions using journal entry till the

preparation of trial balance that will determines all the errors of frauds traced by an individual

while recording all kinds of business transactions in its business enterprise. This report

emphasizes on rectification of errors found by an entity in the given project report. Balance sheet

or income statement will be prepared in dictation to reflect the financial presentation of an entity

in state to target all potential stakeholders who are interested in knowing the actual market status

of the business in order of magnitude to grab high market reward in the outside business

environment.

36

REFERENCES

Books and Journals

Biondi, Y. and et.al., 2012. Some Conceptual Tensions in Financial Reporting: American

Accounting Association's Financial Accounting Standards Committee (FASC). Accounting

Horizons. 26(1). pp. 125-133.

Bryer, R., 2013. Americanism and financial accounting theory–Part 3: Adam Smith, the rise and

fall of socialism, and Irving Fisher's theory of accounting. Critical Perspectives on

Accounting. 24(7). pp. 572-615.

Carvalho, L. N. and Salotti, B. M., 2012. Adoption of IFRS in Brazil and the consequences to

accounting education. Issues in Accounting Education. 28(2). pp. 235-242.

Choi, S., 2013. The Linkage Strategies Between Productivity Metrics and Financial Accounting

Metrics in TPM and PAC Activities. Journal of the Korea Safety Management and

Science. 15(3). pp.151-161.

Cuckston, T., 2013. Bringing tropical forest biodiversity conservation into financial accounting

calculation. Accounting, Auditing & Accountability Journal. 26(5). pp. 688-714.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Freeman, R. J. and et.al., 2014. Governmental and nonprofit accounting: Theory and practice.

JPAEJOURNAL OF PUBLIC AFFAIRS EDUCATION VOLUME 20 NUMBER. 3. p. 441.

Horngren, C. and et.al., 2012. Financial accounting. Pearson Higher Education AU.

Lovell, H. and et.al., 2013. Putting carbon markets into practice: a case study of financial

accounting in Europe. Environment and Planning C: Government and Policy. 31(4). pp.

741-757.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting.

Economy and Society. 43(2). pp. 260-284.

Narayanaswamy, R., 2014. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Prabowo, R. and Tambotoh, J. J. C., 2012. INTERNET FINANCIAL REPORTING AS A

VOLUNTARY DISCLOSURE PRACTICE: AN EMPIRICAL ANALYSIS OF

INDONESIAN MANUFACTURING FIRMS USING ORDER LOGIT REGRESSION.

Journal of Accounting and Business. 5(2).

37

Books and Journals

Biondi, Y. and et.al., 2012. Some Conceptual Tensions in Financial Reporting: American

Accounting Association's Financial Accounting Standards Committee (FASC). Accounting

Horizons. 26(1). pp. 125-133.

Bryer, R., 2013. Americanism and financial accounting theory–Part 3: Adam Smith, the rise and

fall of socialism, and Irving Fisher's theory of accounting. Critical Perspectives on

Accounting. 24(7). pp. 572-615.

Carvalho, L. N. and Salotti, B. M., 2012. Adoption of IFRS in Brazil and the consequences to

accounting education. Issues in Accounting Education. 28(2). pp. 235-242.

Choi, S., 2013. The Linkage Strategies Between Productivity Metrics and Financial Accounting

Metrics in TPM and PAC Activities. Journal of the Korea Safety Management and

Science. 15(3). pp.151-161.

Cuckston, T., 2013. Bringing tropical forest biodiversity conservation into financial accounting

calculation. Accounting, Auditing & Accountability Journal. 26(5). pp. 688-714.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Freeman, R. J. and et.al., 2014. Governmental and nonprofit accounting: Theory and practice.

JPAEJOURNAL OF PUBLIC AFFAIRS EDUCATION VOLUME 20 NUMBER. 3. p. 441.

Horngren, C. and et.al., 2012. Financial accounting. Pearson Higher Education AU.

Lovell, H. and et.al., 2013. Putting carbon markets into practice: a case study of financial

accounting in Europe. Environment and Planning C: Government and Policy. 31(4). pp.

741-757.

Lovell, H., 2014. Climate change, markets and standards: the case of financial accounting.

Economy and Society. 43(2). pp. 260-284.

Narayanaswamy, R., 2014. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd..

Prabowo, R. and Tambotoh, J. J. C., 2012. INTERNET FINANCIAL REPORTING AS A

VOLUNTARY DISCLOSURE PRACTICE: AN EMPIRICAL ANALYSIS OF

INDONESIAN MANUFACTURING FIRMS USING ORDER LOGIT REGRESSION.

Journal of Accounting and Business. 5(2).

37

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.