ACC2102 Financial Accounting: In-depth Analysis of BHP Group Ltd

VerifiedAdded on 2023/06/18

|14

|3994

|129

Report

AI Summary

This report presents a comprehensive financial analysis of BHP Group Ltd, focusing on its accounting equation, revenue sources, profitability, and cash flow. It examines the company's financial performance in 2020, including profit margins, operating expenses, and significant expense items like depr...

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

REFERENCES..............................................................................................................................12

Books & Journals.................................................................................................................12

REFERENCES..............................................................................................................................12

Books & Journals.................................................................................................................12

Task - (I)

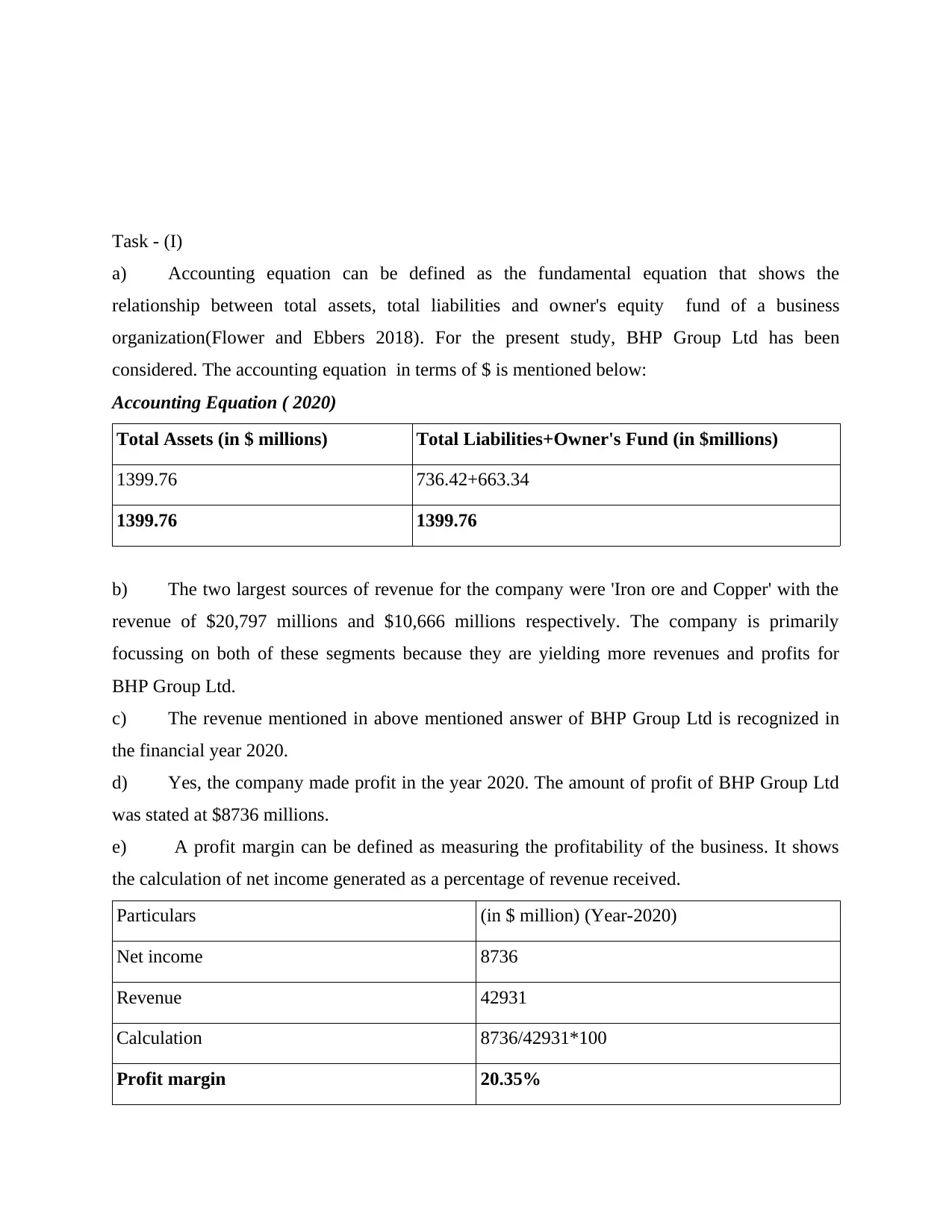

a) Accounting equation can be defined as the fundamental equation that shows the

relationship between total assets, total liabilities and owner's equity fund of a business

organization(Flower and Ebbers 2018). For the present study, BHP Group Ltd has been

considered. The accounting equation in terms of $ is mentioned below:

Accounting Equation ( 2020)

Total Assets (in $ millions) Total Liabilities+Owner's Fund (in $millions)

1399.76 736.42+663.34

1399.76 1399.76

b) The two largest sources of revenue for the company were 'Iron ore and Copper' with the

revenue of $20,797 millions and $10,666 millions respectively. The company is primarily

focussing on both of these segments because they are yielding more revenues and profits for

BHP Group Ltd.

c) The revenue mentioned in above mentioned answer of BHP Group Ltd is recognized in

the financial year 2020.

d) Yes, the company made profit in the year 2020. The amount of profit of BHP Group Ltd

was stated at $8736 millions.

e) A profit margin can be defined as measuring the profitability of the business. It shows

the calculation of net income generated as a percentage of revenue received.

Particulars (in $ million) (Year-2020)

Net income 8736

Revenue 42931

Calculation 8736/42931*100

Profit margin 20.35%

a) Accounting equation can be defined as the fundamental equation that shows the

relationship between total assets, total liabilities and owner's equity fund of a business

organization(Flower and Ebbers 2018). For the present study, BHP Group Ltd has been

considered. The accounting equation in terms of $ is mentioned below:

Accounting Equation ( 2020)

Total Assets (in $ millions) Total Liabilities+Owner's Fund (in $millions)

1399.76 736.42+663.34

1399.76 1399.76

b) The two largest sources of revenue for the company were 'Iron ore and Copper' with the

revenue of $20,797 millions and $10,666 millions respectively. The company is primarily

focussing on both of these segments because they are yielding more revenues and profits for

BHP Group Ltd.

c) The revenue mentioned in above mentioned answer of BHP Group Ltd is recognized in

the financial year 2020.

d) Yes, the company made profit in the year 2020. The amount of profit of BHP Group Ltd

was stated at $8736 millions.

e) A profit margin can be defined as measuring the profitability of the business. It shows

the calculation of net income generated as a percentage of revenue received.

Particulars (in $ million) (Year-2020)

Net income 8736

Revenue 42931

Calculation 8736/42931*100

Profit margin 20.35%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The profit margin of BHP Group Ltd in the year 2020 was 20.35%.

f) In the income statement of the year 2020, it is clearly visible in income statement that

there is a increase in operating expenses from 2019 to 2020. BHP Group Ltd faced lower

volumes at few operated assets as well as major shutdowns at different unit

locations(Saeidmoghadam, Javid and HEMATFAR,2018). This directly increased the

attributable costs including all the expenses incurred to maintain provisions for health and

hygiene along with social distancing. Therefore, all these reasons resulted into reducing the

operations revenue for the year 2020(Liu, 2019). The implications for the business in the year

2021 can be taken as opportunity to resolve the issues of previous year and increase the

operational revenue for the financial year 2021.

g) The two biggest single expense items of BHP Group Ltd are 'Depreciation and

amortisation expense' and 'Raw materials and consumables used'. Both of these items were

biggest single expense for the company. The respective amounts of both the expenses are

mentioned below:

Expense Amount (in $ millions)

Depreciation and amortisation expense 6112

Raw materials and consumables used 5509

h) In the financial statements of BHP Group Ltd, the largest expense in the percentage of

sales revenue is 'Raw materials and consumables used' with an amount stated as $ 5,509 millions

in the year 2020. in comparison to the year 2019, the amount was $ 4591 millions. This shows

that there was a considerable hike in the total amount of raw materials and consumables used.

The reason behind that is because of the global pandemic coronavirus. The company bought the

raw material and consumables items but it remained difficult for it to improve the sales resulting

into bearing higher costs of raw material(Harper and Dunn, 2018). Yes, the cost is considerably

high and in accordance with that effective measures can be taken in order to manage this cost to

prevent upcoming losses. The company should procure less raw materials and consumables in

the upcoming year 2021 by using the existing ones. This will help BHP Group Ltd to save huge

costs. Also, in order to avoid the obsolescence costs, the company can sell them in the market at

f) In the income statement of the year 2020, it is clearly visible in income statement that

there is a increase in operating expenses from 2019 to 2020. BHP Group Ltd faced lower

volumes at few operated assets as well as major shutdowns at different unit

locations(Saeidmoghadam, Javid and HEMATFAR,2018). This directly increased the

attributable costs including all the expenses incurred to maintain provisions for health and

hygiene along with social distancing. Therefore, all these reasons resulted into reducing the

operations revenue for the year 2020(Liu, 2019). The implications for the business in the year

2021 can be taken as opportunity to resolve the issues of previous year and increase the

operational revenue for the financial year 2021.

g) The two biggest single expense items of BHP Group Ltd are 'Depreciation and

amortisation expense' and 'Raw materials and consumables used'. Both of these items were

biggest single expense for the company. The respective amounts of both the expenses are

mentioned below:

Expense Amount (in $ millions)

Depreciation and amortisation expense 6112

Raw materials and consumables used 5509

h) In the financial statements of BHP Group Ltd, the largest expense in the percentage of

sales revenue is 'Raw materials and consumables used' with an amount stated as $ 5,509 millions

in the year 2020. in comparison to the year 2019, the amount was $ 4591 millions. This shows

that there was a considerable hike in the total amount of raw materials and consumables used.

The reason behind that is because of the global pandemic coronavirus. The company bought the

raw material and consumables items but it remained difficult for it to improve the sales resulting

into bearing higher costs of raw material(Harper and Dunn, 2018). Yes, the cost is considerably

high and in accordance with that effective measures can be taken in order to manage this cost to

prevent upcoming losses. The company should procure less raw materials and consumables in

the upcoming year 2021 by using the existing ones. This will help BHP Group Ltd to save huge

costs. Also, in order to avoid the obsolescence costs, the company can sell them in the market at

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

trending prices and get back some amount which the company may loose in coming future if the

stock become obsolete.

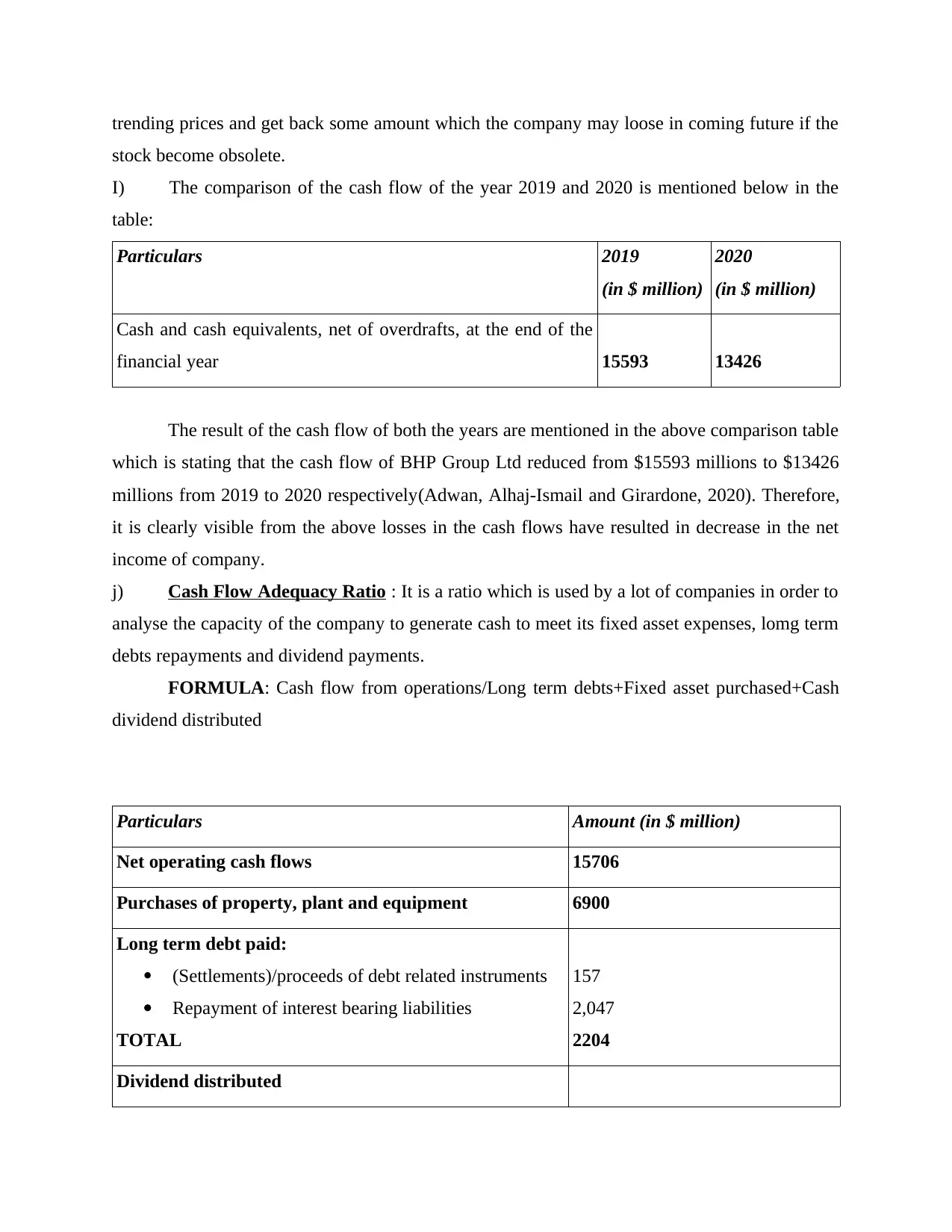

I) The comparison of the cash flow of the year 2019 and 2020 is mentioned below in the

table:

Particulars 2019

(in $ million)

2020

(in $ million)

Cash and cash equivalents, net of overdrafts, at the end of the

financial year 15593 13426

The result of the cash flow of both the years are mentioned in the above comparison table

which is stating that the cash flow of BHP Group Ltd reduced from $15593 millions to $13426

millions from 2019 to 2020 respectively(Adwan, Alhaj-Ismail and Girardone, 2020). Therefore,

it is clearly visible from the above losses in the cash flows have resulted in decrease in the net

income of company.

j) Cash Flow Adequacy Ratio : It is a ratio which is used by a lot of companies in order to

analyse the capacity of the company to generate cash to meet its fixed asset expenses, lomg term

debts repayments and dividend payments.

FORMULA: Cash flow from operations/Long term debts+Fixed asset purchased+Cash

dividend distributed

Particulars Amount (in $ million)

Net operating cash flows 15706

Purchases of property, plant and equipment 6900

Long term debt paid:

(Settlements)/proceeds of debt related instruments

Repayment of interest bearing liabilities

TOTAL

157

2,047

2204

Dividend distributed

stock become obsolete.

I) The comparison of the cash flow of the year 2019 and 2020 is mentioned below in the

table:

Particulars 2019

(in $ million)

2020

(in $ million)

Cash and cash equivalents, net of overdrafts, at the end of the

financial year 15593 13426

The result of the cash flow of both the years are mentioned in the above comparison table

which is stating that the cash flow of BHP Group Ltd reduced from $15593 millions to $13426

millions from 2019 to 2020 respectively(Adwan, Alhaj-Ismail and Girardone, 2020). Therefore,

it is clearly visible from the above losses in the cash flows have resulted in decrease in the net

income of company.

j) Cash Flow Adequacy Ratio : It is a ratio which is used by a lot of companies in order to

analyse the capacity of the company to generate cash to meet its fixed asset expenses, lomg term

debts repayments and dividend payments.

FORMULA: Cash flow from operations/Long term debts+Fixed asset purchased+Cash

dividend distributed

Particulars Amount (in $ million)

Net operating cash flows 15706

Purchases of property, plant and equipment 6900

Long term debt paid:

(Settlements)/proceeds of debt related instruments

Repayment of interest bearing liabilities

TOTAL

157

2,047

2204

Dividend distributed

Dividends paid

Dividends paid to non-controlling interests

TOTAL

6876

1,043

7919

Calculation: 15706/6900+2204+7919= 0.9226:1

Interpretation: The ideal value of 'cash flow adequacy ratio' is 1 or more. The ratio obtained is

0.9226 showing that the sum of long term debts, dividends paid and fixed asset purchased are

higher than the cash flow from operations. The company must increase its cash flow from

operations in order to improve the ratio and reach to a desired level of achieving organizational

goals.

Cash Flow to Revenue Ratio: It is a type of ratio revealing that whether the company

has the ability to generate cash flows in relation to its sales volume.

FORMULA: Operating cash flows/Net Sales

Particulars Amount (in $ million)

Net operating cash flows 15706

Net Sales 42931

Calculation: 15706/42931= 0.365:1

Interpretation: The ideal ratio of this ratio is 1 or more but the ratio obtained is 0.365 showing

weak position by not generating enough cash flow from its sales. Also, it has not even able to

reach the break even point which brings an element of inefficiency.

k) The largest non-current asset of BHP Group Ltd is 'property, plant and equipment'. The

opening and closing balance is given below:

Non-Current Asset Opening balance

(2019)

Closing balance

(2020)

Property, plant and equipment 68041 72362

Dividends paid to non-controlling interests

TOTAL

6876

1,043

7919

Calculation: 15706/6900+2204+7919= 0.9226:1

Interpretation: The ideal value of 'cash flow adequacy ratio' is 1 or more. The ratio obtained is

0.9226 showing that the sum of long term debts, dividends paid and fixed asset purchased are

higher than the cash flow from operations. The company must increase its cash flow from

operations in order to improve the ratio and reach to a desired level of achieving organizational

goals.

Cash Flow to Revenue Ratio: It is a type of ratio revealing that whether the company

has the ability to generate cash flows in relation to its sales volume.

FORMULA: Operating cash flows/Net Sales

Particulars Amount (in $ million)

Net operating cash flows 15706

Net Sales 42931

Calculation: 15706/42931= 0.365:1

Interpretation: The ideal ratio of this ratio is 1 or more but the ratio obtained is 0.365 showing

weak position by not generating enough cash flow from its sales. Also, it has not even able to

reach the break even point which brings an element of inefficiency.

k) The largest non-current asset of BHP Group Ltd is 'property, plant and equipment'. The

opening and closing balance is given below:

Non-Current Asset Opening balance

(2019)

Closing balance

(2020)

Property, plant and equipment 68041 72362

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

l) The method of depreciation used to write off the property, plant and equipment is

'Straight line depreciation methodology'. In this methodology of depreciation the value of

fixed or long term asset such as property, plant and equipment is reduced over its useful life.

m) Yes, BHP Group Ltd is having intangible assets in its 'Statement of Balance Sheet'. One

of the example of intangible asset is 'goodwill' and its stated value in the financial year 2021 is $

247 millions. Goodwill is considered as one of the most important intangible asset for any

company as it portrays an effective image in the minds of related stakeholder and different

parties related to the organization(Mulenga and Bhatia, 2018).

n) The two current assets and two current liabilities are mentioned below with the values in

the following table:

Current Liabilities Amount (in $

millions)

Current Assets Amount (in $

millions)

Trade and other payables 5767 Cash and cash equivalents 13426

Interest bearing liabilities 5012 Trade and other receivables 3364

o) Current ratio can be defined as one the most important and vital tool in order to calculate

and measure the liquidity position of the company. It basically uses two elements namely current

assets and current liabilities (Sanoran, 2018). Current Assets are those items which are

considered as cash or items that can be converted into cash in a short term. While pn the other

sides current liabilities are those items which are considered as a financial responsibility that the

company has to pay back within a year.

FORMULA: Current Assets/Current Liabilities

Current Liabilities Amount (in $

millions)

Current Assets Amount (in $

millions)

Trade and other payables 5767 Cash and cash equivalents 13426

Interest bearing liabilities 5012 Trade and other receivables 3364

Other financial liabilities 225 Other financial assets 84

Current tax payable 913 Inventories 4101

'Straight line depreciation methodology'. In this methodology of depreciation the value of

fixed or long term asset such as property, plant and equipment is reduced over its useful life.

m) Yes, BHP Group Ltd is having intangible assets in its 'Statement of Balance Sheet'. One

of the example of intangible asset is 'goodwill' and its stated value in the financial year 2021 is $

247 millions. Goodwill is considered as one of the most important intangible asset for any

company as it portrays an effective image in the minds of related stakeholder and different

parties related to the organization(Mulenga and Bhatia, 2018).

n) The two current assets and two current liabilities are mentioned below with the values in

the following table:

Current Liabilities Amount (in $

millions)

Current Assets Amount (in $

millions)

Trade and other payables 5767 Cash and cash equivalents 13426

Interest bearing liabilities 5012 Trade and other receivables 3364

o) Current ratio can be defined as one the most important and vital tool in order to calculate

and measure the liquidity position of the company. It basically uses two elements namely current

assets and current liabilities (Sanoran, 2018). Current Assets are those items which are

considered as cash or items that can be converted into cash in a short term. While pn the other

sides current liabilities are those items which are considered as a financial responsibility that the

company has to pay back within a year.

FORMULA: Current Assets/Current Liabilities

Current Liabilities Amount (in $

millions)

Current Assets Amount (in $

millions)

Trade and other payables 5767 Cash and cash equivalents 13426

Interest bearing liabilities 5012 Trade and other receivables 3364

Other financial liabilities 225 Other financial assets 84

Current tax payable 913 Inventories 4101

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Provisions 2810 Current tax assets 366

Deferred income 97 Other 130

TOTAL 14824 TOTAL 21471

FORMULA: Current Assets/Current Liabilities

Calculation: 21471/14824= 1.4483:1

Interpretation: The current ratio of BHP Group Ltd is calculated as 1.4483. the ratio obtained

states that the company has enough more current assets than liabilities in order to cover its debts.

Therefore, the ratio is considered as satisfactory showing that the company has enough capacity

to meet its short term liabilities with a scope of development in the near future.

p) The long-term debt that BHP Group Ltd is carrying are the 'Interest bearing liabilities'

with the stated amount of $22,036 millions. These are those liabilities or debts that the cost

money to hold. For this type of liability the company is obliged to pay back the interest amount

that has been agreed by the concerned parties (Saeidi Goraghani and Asadi Dobani, 2018). All

the interest bearing liabilities are mentioned below in the table with their specific amounts in the

table:

Interest Bearing Liabilities Amount (in $ millions)

Bank loans 1755

Notes and debentures 17691

Lease liabilities 2590

TOTAL 22036

q) Debt ratio can be defined as the determination of the relative proportion of debt to total

assets. This ratio is usually used by the top level management as well as the investors for the

purpose of making decisions regarding important investment and financial decisions. If the ratio

is higher then it shows that the company is levered portraying that the company has higher level

of financial risks.

FORMULA: Total Liabilities/Total Equity

Particulars Amount (in $ millions)

Deferred income 97 Other 130

TOTAL 14824 TOTAL 21471

FORMULA: Current Assets/Current Liabilities

Calculation: 21471/14824= 1.4483:1

Interpretation: The current ratio of BHP Group Ltd is calculated as 1.4483. the ratio obtained

states that the company has enough more current assets than liabilities in order to cover its debts.

Therefore, the ratio is considered as satisfactory showing that the company has enough capacity

to meet its short term liabilities with a scope of development in the near future.

p) The long-term debt that BHP Group Ltd is carrying are the 'Interest bearing liabilities'

with the stated amount of $22,036 millions. These are those liabilities or debts that the cost

money to hold. For this type of liability the company is obliged to pay back the interest amount

that has been agreed by the concerned parties (Saeidi Goraghani and Asadi Dobani, 2018). All

the interest bearing liabilities are mentioned below in the table with their specific amounts in the

table:

Interest Bearing Liabilities Amount (in $ millions)

Bank loans 1755

Notes and debentures 17691

Lease liabilities 2590

TOTAL 22036

q) Debt ratio can be defined as the determination of the relative proportion of debt to total

assets. This ratio is usually used by the top level management as well as the investors for the

purpose of making decisions regarding important investment and financial decisions. If the ratio

is higher then it shows that the company is levered portraying that the company has higher level

of financial risks.

FORMULA: Total Liabilities/Total Equity

Particulars Amount (in $ millions)

Total Liabilities 52537

Total Equity 52246

Calculation: 52537/52246= 1.0055

Interpretation: The debt ratio of BHP Group Ltd is obtained as 1.0055 which is indicates that

for ever $1 of assets, the company is having $1 of liabilities with a fact that the investors as well

as creditors are having equal stake in the business assets. It is always recommended to every

business in order to have a lower ratio in case of debt to equity ratio to avoid the possible risks.

BHP Group Ltd is having a ratio which is showing that the company is highly levered along with

the financial risk.

r) The financial report of BHP Group Ltd in regards with the environmental matters

disclosed that the company is highly concerned towards the environment and its issues which

may arise due to its operational activities(Baxter and et. al., 2019). The company has adopted

'sustainability' as its key essence in their working showing that they want to develop their

business keeping in mind that they are not harming the environment in any case. They have

disclosed the fact that they have a responsibility for the purpose of minimising the unpleasant

and adverse environmental impacts by contributing to the resilience towards the natural

environment. BHP Group Ltd have taken significant initiative for the purpose of managing the

environment risks associated and have considered the suggestions and opinions of all the

stakeholders in the decision making process.

For the purpose of minimising and mitigating the environmental risks, BHP Group Ltd

has developed different policies as well as processes in order to manage those risks and achieve

the environmental objectives(Elaine Gioiosa, and Kinkela, 2019). The company have also

implemented different practices in order to ensure that the environmental risks can be managed

with the help of business planning as well as project evaluation cycles. BHP Group Ltd has taken

considerable actions in order to tackle such risks by way of applying mitigating hierarchies,

commitments to avoid after effects, air emissions management, waste management.

Total Equity 52246

Calculation: 52537/52246= 1.0055

Interpretation: The debt ratio of BHP Group Ltd is obtained as 1.0055 which is indicates that

for ever $1 of assets, the company is having $1 of liabilities with a fact that the investors as well

as creditors are having equal stake in the business assets. It is always recommended to every

business in order to have a lower ratio in case of debt to equity ratio to avoid the possible risks.

BHP Group Ltd is having a ratio which is showing that the company is highly levered along with

the financial risk.

r) The financial report of BHP Group Ltd in regards with the environmental matters

disclosed that the company is highly concerned towards the environment and its issues which

may arise due to its operational activities(Baxter and et. al., 2019). The company has adopted

'sustainability' as its key essence in their working showing that they want to develop their

business keeping in mind that they are not harming the environment in any case. They have

disclosed the fact that they have a responsibility for the purpose of minimising the unpleasant

and adverse environmental impacts by contributing to the resilience towards the natural

environment. BHP Group Ltd have taken significant initiative for the purpose of managing the

environment risks associated and have considered the suggestions and opinions of all the

stakeholders in the decision making process.

For the purpose of minimising and mitigating the environmental risks, BHP Group Ltd

has developed different policies as well as processes in order to manage those risks and achieve

the environmental objectives(Elaine Gioiosa, and Kinkela, 2019). The company have also

implemented different practices in order to ensure that the environmental risks can be managed

with the help of business planning as well as project evaluation cycles. BHP Group Ltd has taken

considerable actions in order to tackle such risks by way of applying mitigating hierarchies,

commitments to avoid after effects, air emissions management, waste management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

s) The financial statements of BHP Group Ltd have been audited by two auditing firms

named as EY Australia and EY UK with Australian Auditing Standards and International

Standards on Auditing (UK) (ISAs (UK)) and applicable law.

The auditors namely EY Australia and EY UK issued different opinions on various

matters after auditing the financial reports of BHP Group Ltd. They issued opinions on several

matters which are mentioned below:

In context to Samarco dam failure, they reported that the provisions presented were

reasonable as well as the contingent liabilities disclosures were appropriate.

They reported that they are satisfies with the company's management in managing the

impact of climate change while assessing the value of the long lived assets.

They concluded that the amount which was to be recovered of Carrejon was appropriate

and there was no impairment charged in that case.

They also reported that the fluctuations in the global oil prices and the benchmarking of

forecasted prices in comparison to the market data was highly reasonable of the group's

assessment in order to calculate the long term price assumptions.

They also mentioned that they are highly satisfied the estimated provided in accordance

to the climate change along with the climate change disclosure in the company's financial

statements.

At last, they concluded by issuing a statement that BHP Group Ltd is complying with all

the procedures of enquiries, internal audits and all the legal processes required(Hariyati,

Tjahjadi, and Soewarno, 2019). They also authenticated all the enquiries through the issued

board minutes to the Sustainable Committee as well as the Risk & Audit committee that there

was no contradictory evidence.

t) In the annual financial report of BHP Group Ltd, the chief executive reports disclosed a

summary of working of whole year including the achievements as well as the failures. The CEO

also mentioned the scope of works in which the company can excel in the near future. The

management is highly concerned with issues recovering from the drastic phase of covid-19. The

company will taking forward the issues of environmental sustainability high on priority. They are

also considering the issue of high unemployment and rising debts because of covid-19. Along

with this, the company is going to have regular check on the climate change issues so that they

can have prioritize the sustainability to higher levels(Mukhlisin, 2020). Therefore, BHP Group

named as EY Australia and EY UK with Australian Auditing Standards and International

Standards on Auditing (UK) (ISAs (UK)) and applicable law.

The auditors namely EY Australia and EY UK issued different opinions on various

matters after auditing the financial reports of BHP Group Ltd. They issued opinions on several

matters which are mentioned below:

In context to Samarco dam failure, they reported that the provisions presented were

reasonable as well as the contingent liabilities disclosures were appropriate.

They reported that they are satisfies with the company's management in managing the

impact of climate change while assessing the value of the long lived assets.

They concluded that the amount which was to be recovered of Carrejon was appropriate

and there was no impairment charged in that case.

They also reported that the fluctuations in the global oil prices and the benchmarking of

forecasted prices in comparison to the market data was highly reasonable of the group's

assessment in order to calculate the long term price assumptions.

They also mentioned that they are highly satisfied the estimated provided in accordance

to the climate change along with the climate change disclosure in the company's financial

statements.

At last, they concluded by issuing a statement that BHP Group Ltd is complying with all

the procedures of enquiries, internal audits and all the legal processes required(Hariyati,

Tjahjadi, and Soewarno, 2019). They also authenticated all the enquiries through the issued

board minutes to the Sustainable Committee as well as the Risk & Audit committee that there

was no contradictory evidence.

t) In the annual financial report of BHP Group Ltd, the chief executive reports disclosed a

summary of working of whole year including the achievements as well as the failures. The CEO

also mentioned the scope of works in which the company can excel in the near future. The

management is highly concerned with issues recovering from the drastic phase of covid-19. The

company will taking forward the issues of environmental sustainability high on priority. They are

also considering the issue of high unemployment and rising debts because of covid-19. Along

with this, the company is going to have regular check on the climate change issues so that they

can have prioritize the sustainability to higher levels(Mukhlisin, 2020). Therefore, BHP Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ltd is going to carry forward all this issue with a motive to resolve from its root and d3evelop

the organization with high level effectiveness as well as efficiency. The CEO of the company

also indicated that the company and its workforce along with all the stakeholders are all set to

deal with any uncertainty coming on the way in the near future with a focus on growing values

and returns for the shareholders as well as the society.

u) What factors would you as a prospective investor consider? Would you buy shares in the

company and why?

If any individual wants to invest amount in the BHP billion so for this require considering

various factors from investor perspective that are mentioned below:

Investment is in the pockets of big business by placing money into expanding enterprises.

Although every owner makes a living, the difficult aspect is figuring out how to woo each

professional buyer in a manner that tickles their curiosity. Understand that, at the conclusion of

each day, traders are just individuals, and each one will have their own set of sticking points and

intangible elements for investment decision making.

Stability: One of the most important aspects to examine before investing in stocks is the

firm's sustainability. In most cases, a company's value will lose value over a period of time. It's a

regular occurrence, particularly throughout downturns and sometimes even market turmoil.

Time Horizon: One of the most important differences between buying and selling stocks

is that the latter often has a larger scope. The individual's income requirements and preferred

perceived risk are determined by the equity portfolio, which aids in the selection of the right

investment scheme. Concentrate on the company's current stability in relation to its financial

situations rather than on its tough moment. If they see a lot of volatility, it might be a warning

sign. However, when they notice the firm experiencing problems with others at a time when the

marketplace is suffering, it could be a good option to think investing in its shares.

Risk Vs reward: Any type of investment has a certain amount of risk. It matters is that

you take reasonable risks and keep to a risk/reward ratio that is appropriate for your appetite for

risk. The projected profits of a transaction are comparison to the number of risk incurred to

invest in that asset in a risk/reward proportion. This ratio is derived by dividing the sum an

owner risks losing (the risk) if such market reaches in an unanticipated manner by the

profitability whenever the investment is carried up.

the organization with high level effectiveness as well as efficiency. The CEO of the company

also indicated that the company and its workforce along with all the stakeholders are all set to

deal with any uncertainty coming on the way in the near future with a focus on growing values

and returns for the shareholders as well as the society.

u) What factors would you as a prospective investor consider? Would you buy shares in the

company and why?

If any individual wants to invest amount in the BHP billion so for this require considering

various factors from investor perspective that are mentioned below:

Investment is in the pockets of big business by placing money into expanding enterprises.

Although every owner makes a living, the difficult aspect is figuring out how to woo each

professional buyer in a manner that tickles their curiosity. Understand that, at the conclusion of

each day, traders are just individuals, and each one will have their own set of sticking points and

intangible elements for investment decision making.

Stability: One of the most important aspects to examine before investing in stocks is the

firm's sustainability. In most cases, a company's value will lose value over a period of time. It's a

regular occurrence, particularly throughout downturns and sometimes even market turmoil.

Time Horizon: One of the most important differences between buying and selling stocks

is that the latter often has a larger scope. The individual's income requirements and preferred

perceived risk are determined by the equity portfolio, which aids in the selection of the right

investment scheme. Concentrate on the company's current stability in relation to its financial

situations rather than on its tough moment. If they see a lot of volatility, it might be a warning

sign. However, when they notice the firm experiencing problems with others at a time when the

marketplace is suffering, it could be a good option to think investing in its shares.

Risk Vs reward: Any type of investment has a certain amount of risk. It matters is that

you take reasonable risks and keep to a risk/reward ratio that is appropriate for your appetite for

risk. The projected profits of a transaction are comparison to the number of risk incurred to

invest in that asset in a risk/reward proportion. This ratio is derived by dividing the sum an

owner risks losing (the risk) if such market reaches in an unanticipated manner by the

profitability whenever the investment is carried up.

It revealed that earnings from operations increased by 80% year on year to US$25.9 billion, with

underlying EBITDA (EBITDA explained) up 69 percent to $37.4 billion. The actual profit was

up 88 percent to US$17 billion, while the declared profit was up 42 percent to US$11.3 billion.

The reduced declared profit was mostly due to losses, which totalled $5.8 billion. The company's

net operational cash increased by 73 percent to US$27.2 billion. Nevertheless, in the initial

reaction to the results and other steps by the company, BHP's stock dropped approximately 7%

yesterday. From the overall analysis it is saying that BHP Billiton shares is good for long term

investment.

v) BHP Group Ltd was affected by the global pandemic Coronavaus (Covid- 19). There

were major impacts of covid-19 which had significantly impacted their group of suppliers. As

suppliers are the most important for a business to carry its operations therefore, the company was

highly concerned with the safety and health of its suppliers community. They considered that it

is important for them to remember the important role that they are going to play in context to

employees, partners and suppliers as well. During the hard and tough times of Covid–19, BHP

Group Ltd made it sure that they have implemented certain specific measures and protocols in

underlying EBITDA (EBITDA explained) up 69 percent to $37.4 billion. The actual profit was

up 88 percent to US$17 billion, while the declared profit was up 42 percent to US$11.3 billion.

The reduced declared profit was mostly due to losses, which totalled $5.8 billion. The company's

net operational cash increased by 73 percent to US$27.2 billion. Nevertheless, in the initial

reaction to the results and other steps by the company, BHP's stock dropped approximately 7%

yesterday. From the overall analysis it is saying that BHP Billiton shares is good for long term

investment.

v) BHP Group Ltd was affected by the global pandemic Coronavaus (Covid- 19). There

were major impacts of covid-19 which had significantly impacted their group of suppliers. As

suppliers are the most important for a business to carry its operations therefore, the company was

highly concerned with the safety and health of its suppliers community. They considered that it

is important for them to remember the important role that they are going to play in context to

employees, partners and suppliers as well. During the hard and tough times of Covid–19, BHP

Group Ltd made it sure that they have implemented certain specific measures and protocols in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

order to support their community of suppliers(Magnan and Parbonetti, 2018). With he entry of

Covid-19, the impact directly came on the transportation of the goods as well which made it

difficult for the company to carry on its regular business operations efficiently. The global -

pandemic tapped almost all the sections of the society. In response to the pandemic, BHP Group

Ltd made its first priority to consider the health and safety of all the related groups who are a

directly or indirectly a part of there organization(Imoniana, Soares and Domingos, 2018). As per

the financial statements of BHP Group Ltd, there is no disclosure of any kind of job keeper

received from the end of government for the company to retain its employees. Infact, the

company raised huge amount through different internal as well as external sources in order to

help several communities to handle the crisis which happened because of the global pandemic

coronavirus.

REFERENCES

Books & Journals

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Saeidmoghadam, M., Javid, D. and HEMATFAR, M., 2018. Detecting automotive and parts

manufacturing industry earnings management by combining Bayesian networks and C5.

0 decision tree.

Liu, B., 2019, September. Consideration and Practice of Flipped Classroom Teaching Mode

Based on “Rain Classroom”—Taking “Intermediate Financial Accounting” as an

Example. In 2019 3rd International Conference on Education, Management Science and

Economics (ICEMSE 2019) (pp. 309-312). Atlantis Press.

Harper, C. and Dunn, C., 2018. Building better accounting curricula. Strategic Finance, 100(2),

pp.46-54.

Adwan, S., Alhaj-Ismail, A. and Girardone, C., 2020. Fair value accounting and value relevance

of equity book value and net income for European financial firms during the

crisis. Journal of International Accounting, Auditing and Taxation, 39, p.100320.

Covid-19, the impact directly came on the transportation of the goods as well which made it

difficult for the company to carry on its regular business operations efficiently. The global -

pandemic tapped almost all the sections of the society. In response to the pandemic, BHP Group

Ltd made its first priority to consider the health and safety of all the related groups who are a

directly or indirectly a part of there organization(Imoniana, Soares and Domingos, 2018). As per

the financial statements of BHP Group Ltd, there is no disclosure of any kind of job keeper

received from the end of government for the company to retain its employees. Infact, the

company raised huge amount through different internal as well as external sources in order to

help several communities to handle the crisis which happened because of the global pandemic

coronavirus.

REFERENCES

Books & Journals

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Saeidmoghadam, M., Javid, D. and HEMATFAR, M., 2018. Detecting automotive and parts

manufacturing industry earnings management by combining Bayesian networks and C5.

0 decision tree.

Liu, B., 2019, September. Consideration and Practice of Flipped Classroom Teaching Mode

Based on “Rain Classroom”—Taking “Intermediate Financial Accounting” as an

Example. In 2019 3rd International Conference on Education, Management Science and

Economics (ICEMSE 2019) (pp. 309-312). Atlantis Press.

Harper, C. and Dunn, C., 2018. Building better accounting curricula. Strategic Finance, 100(2),

pp.46-54.

Adwan, S., Alhaj-Ismail, A. and Girardone, C., 2020. Fair value accounting and value relevance

of equity book value and net income for European financial firms during the

crisis. Journal of International Accounting, Auditing and Taxation, 39, p.100320.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mulenga, M. J. and Bhatia, M., 2018. Review of Accounting Variables Affecting Stock Price

Movements. Amity Business Review, 19(1).

Sanoran, K. L., 2018. Auditors’ going concern reporting accuracy during and after the global

financial crisis. Journal of Contemporary Accounting & Economics, 14(2). pp.164-178.

Saeidi Goraghani, M. and Asadi Dobani, N., 2018. The effect of revaluation of assets on audit

fees. Journal of Knowledge Accounting, 8(4). pp.141-159.

Baxter, J., and et. al., 2019. Accounting and passionate interests: the case of a Swedish football

club. Accounting, Organizations and Society, 74. pp.21-40.

Elaine Gioiosa, M. and Kinkela, K., 2019. Active learning in accounting classes with technology

and communication skills: A two-semester study of student perceptions. Journal of

Education for Business, 94(8). pp.561-568.

Hariyati, H., Tjahjadi, B. and Soewarno, N., 2019. The mediating effect of intellectual capital,

management accounting information systems, internal process performance, and

customer performance. International journal of productivity and performance

management.

Mukhlisin, M., 2020. Level of Maqāsid ul-Shari’āh’s in financial reporting standards for Islamic

financial institutions. Journal of Islamic Accounting and Business Research.

Imoniana, J.O., Soares, R.R. and Domingos, L.C., 2018. A review of sustainability accounting

for emission reduction credit and compliance with emission rules in Brazil: A discourse

analysis. Journal of cleaner production, 172, pp.2045-2057.

Magnan, M. and Parbonetti, A., 2018. Fair value accounting: A standard-Setting perspective.

In The Routledge Companion to Fair Value in Accounting (pp. 41-55). Routledge.

Movements. Amity Business Review, 19(1).

Sanoran, K. L., 2018. Auditors’ going concern reporting accuracy during and after the global

financial crisis. Journal of Contemporary Accounting & Economics, 14(2). pp.164-178.

Saeidi Goraghani, M. and Asadi Dobani, N., 2018. The effect of revaluation of assets on audit

fees. Journal of Knowledge Accounting, 8(4). pp.141-159.

Baxter, J., and et. al., 2019. Accounting and passionate interests: the case of a Swedish football

club. Accounting, Organizations and Society, 74. pp.21-40.

Elaine Gioiosa, M. and Kinkela, K., 2019. Active learning in accounting classes with technology

and communication skills: A two-semester study of student perceptions. Journal of

Education for Business, 94(8). pp.561-568.

Hariyati, H., Tjahjadi, B. and Soewarno, N., 2019. The mediating effect of intellectual capital,

management accounting information systems, internal process performance, and

customer performance. International journal of productivity and performance

management.

Mukhlisin, M., 2020. Level of Maqāsid ul-Shari’āh’s in financial reporting standards for Islamic

financial institutions. Journal of Islamic Accounting and Business Research.

Imoniana, J.O., Soares, R.R. and Domingos, L.C., 2018. A review of sustainability accounting

for emission reduction credit and compliance with emission rules in Brazil: A discourse

analysis. Journal of cleaner production, 172, pp.2045-2057.

Magnan, M. and Parbonetti, A., 2018. Fair value accounting: A standard-Setting perspective.

In The Routledge Companion to Fair Value in Accounting (pp. 41-55). Routledge.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.