Financial Accounting and Audit Report: Analysis and Recommendations

VerifiedAdded on 2023/01/11

|8

|1722

|100

Report

AI Summary

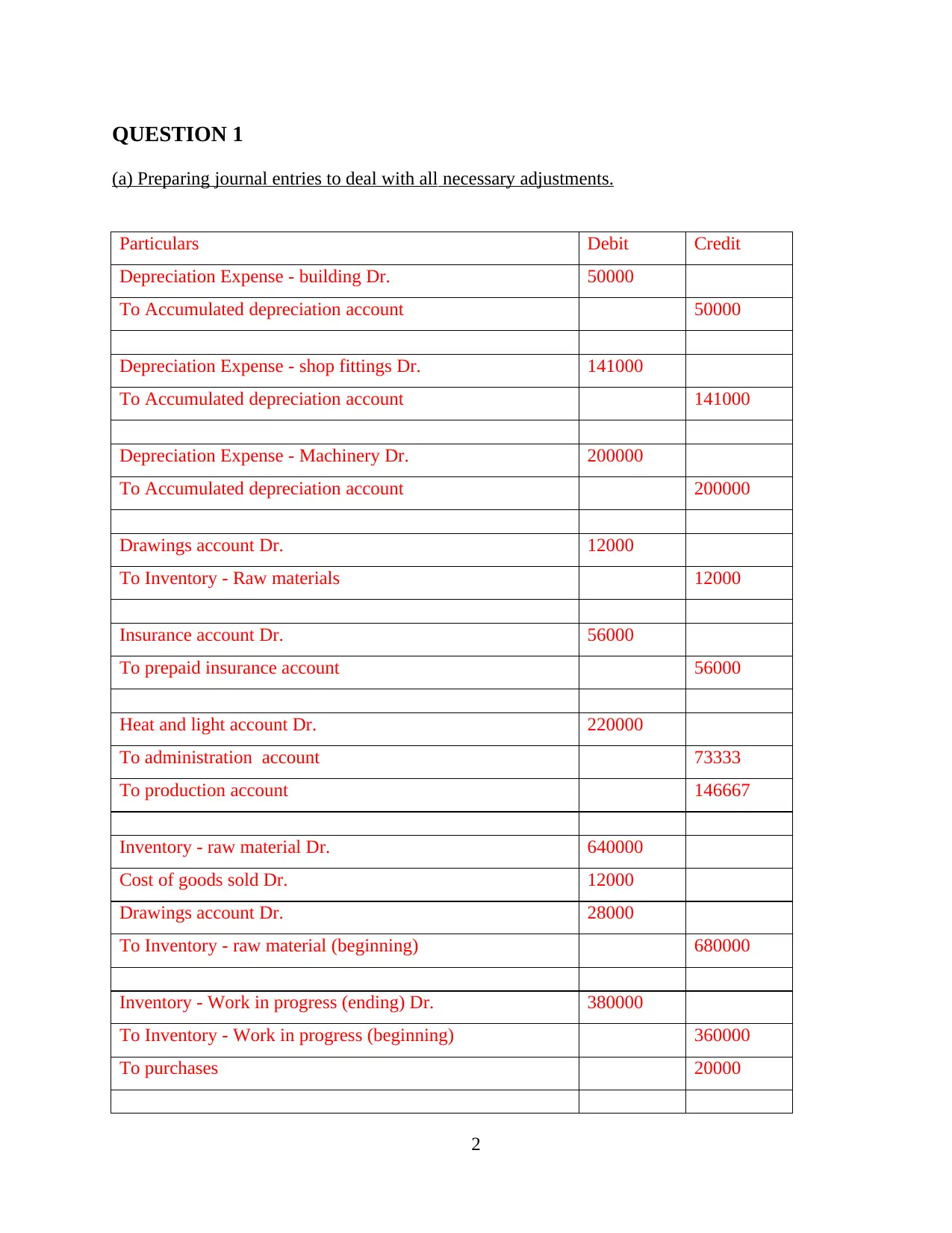

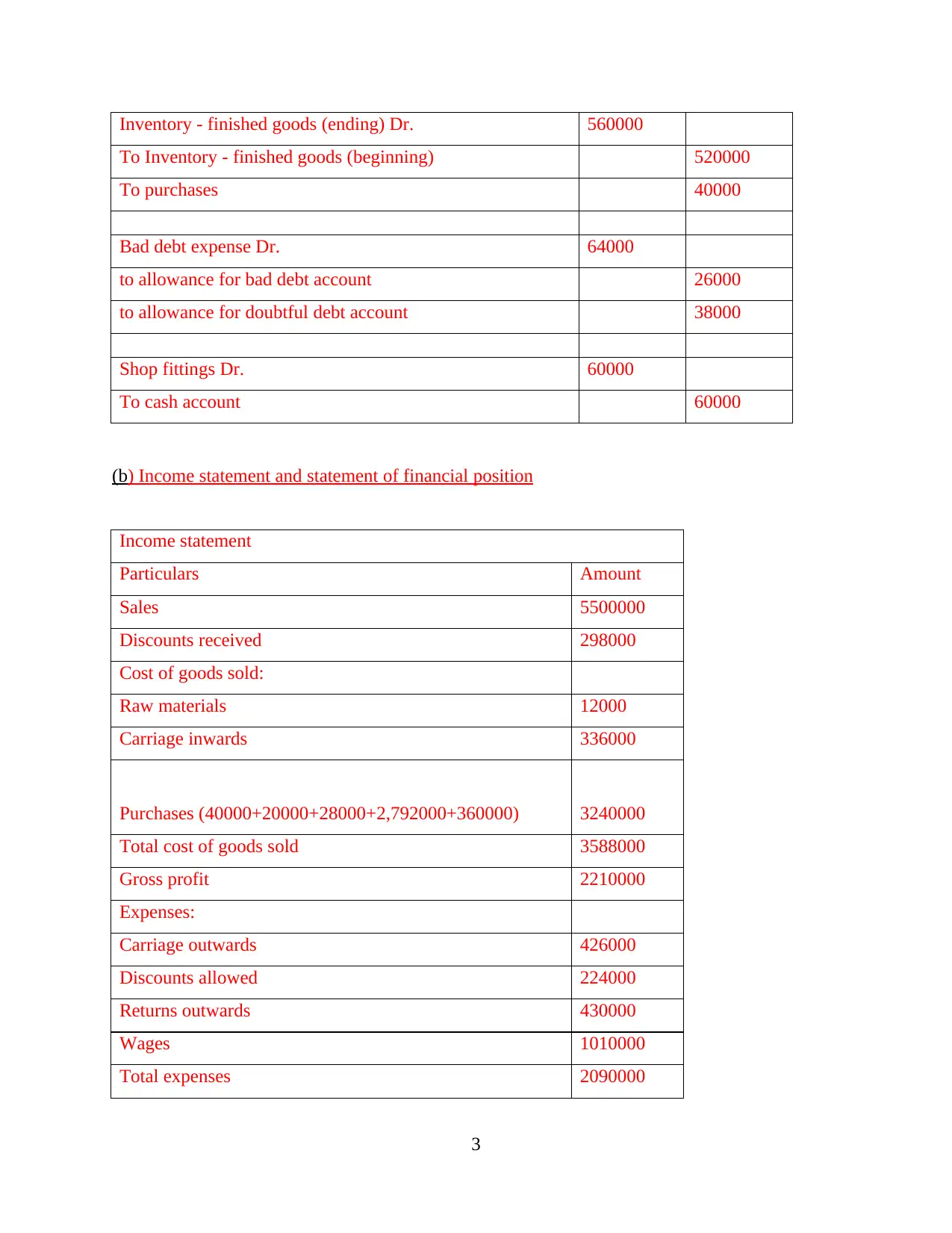

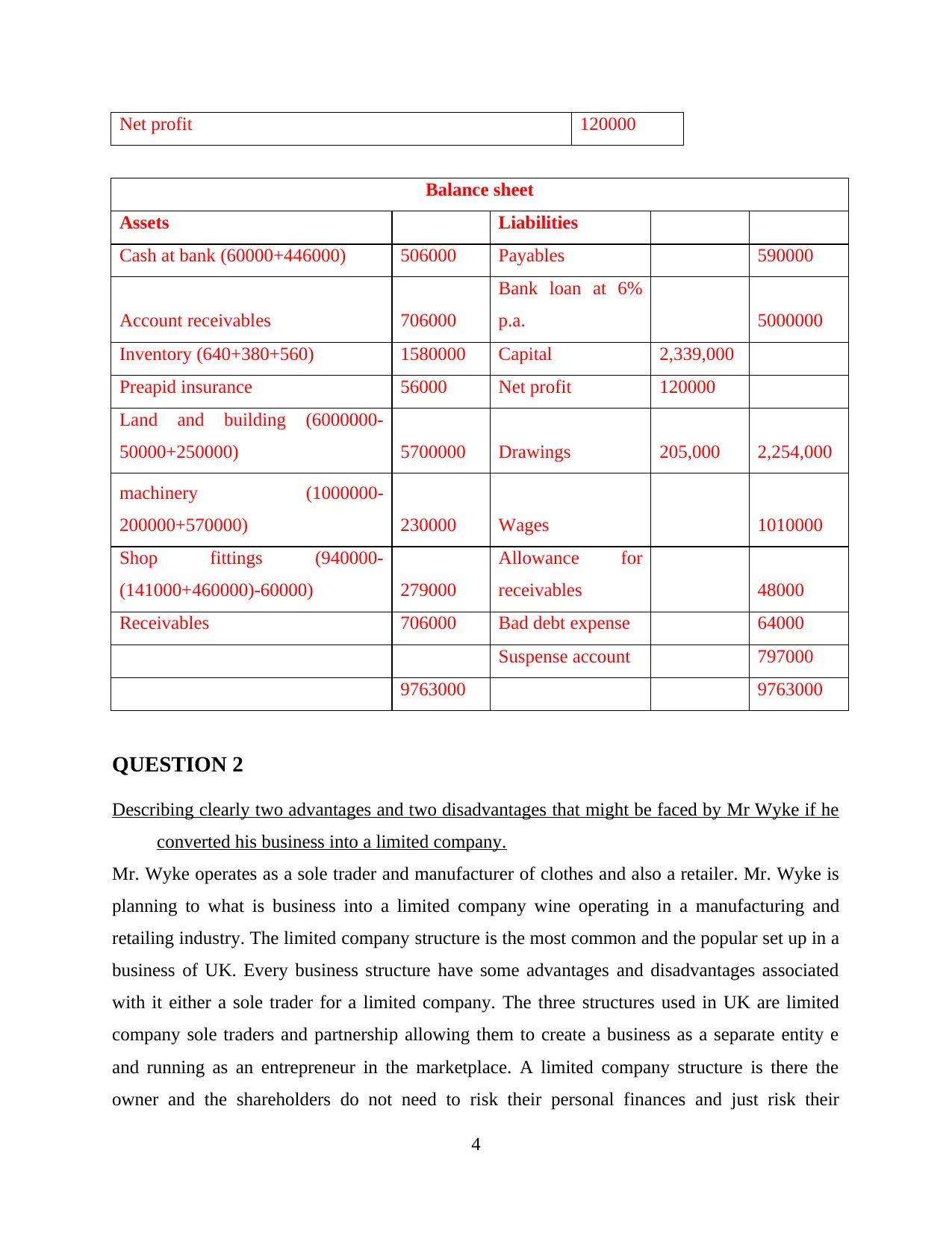

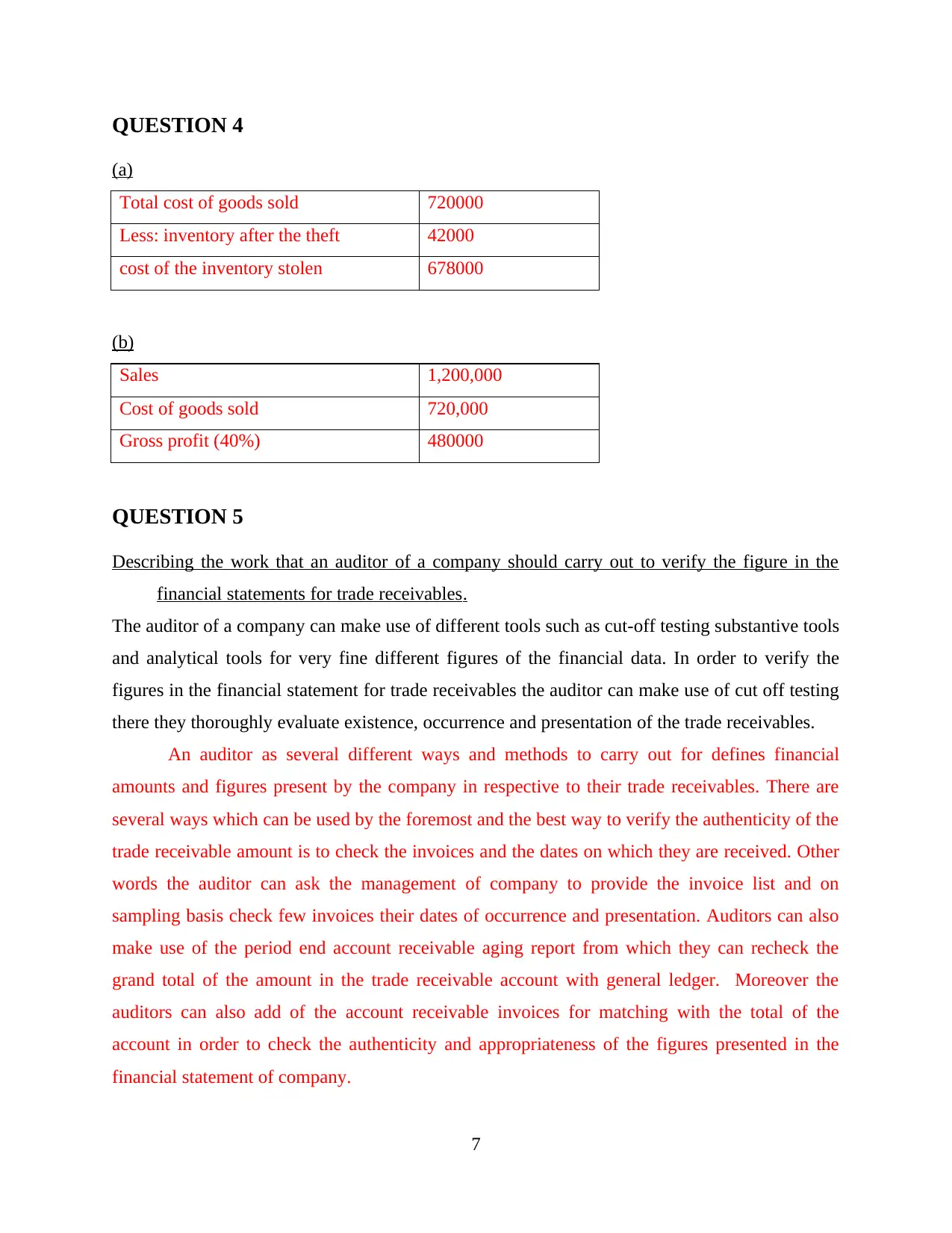

This assignment provides a comprehensive analysis of financial accounting and auditing principles, focusing on a case study involving a sole trader, Mr. Wyke, who is considering converting his business into a limited company. The report begins with the preparation of journal entries to address necessary adjustments, followed by the creation of an income statement and a statement of financial position. It then explores the advantages and disadvantages of converting a business into a limited company. The assignment also examines how financial statements of a listed company can be used for investment decisions, including additional sources of information. Furthermore, the report details the work an auditor should perform to verify trade receivables figures. The report encompasses critical accounting concepts, including depreciation, inventory valuation, bad debt expense, and financial statement analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.