Financial Accounting and Reporting: LLC, NEXT PLC, and Ratio Analysis

VerifiedAdded on 2020/10/05

|12

|2352

|300

Report

AI Summary

This report delves into financial accounting and reporting, examining the structure of limited liability companies (LLCs) and comparing them to sole proprietorships and partnerships, highlighting their respective merits and demerits. The core of the report involves a detailed analysis and interpretation of the annual reports of NEXT PLC, a UK-based clothing, footwear, and utility products retailer. The analysis employs ratio analysis techniques, evaluating working capital, liquidity, profitability, and investor ratios over a five-year period to assess NEXT PLC's financial position and performance. The report provides insights into trends, such as increasing receivable days and decreasing inventory turnover, and their implications. It also discusses the company's profitability and investor ratios, including earnings per share and dividend per share. Finally, the report forecasts the future of NEXT PLC within the UK clothing retail industry, suggesting potential improvements in profitability and brand image, while also recommending operational adjustments to strengthen its liquidity and working capital position.

Financial Accounting and

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

I. Evaluating limited liability company and its merits & demerits.............................................1

II) Analysis and interpretation of annual reports of NEXT PLC................................................3

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

I. Evaluating limited liability company and its merits & demerits.............................................1

II) Analysis and interpretation of annual reports of NEXT PLC................................................3

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial accounting and reporting is a concept of developing financial accounts in order

to ascertain performance of a business organisation. Main aim of this project report is to build an

understanding about limited liability company and its financial reporting system. Scope of this

project report includes merits and demerits of limited liability company in order to compare it

from sole proprietorship and partnership. In order to better understand this concept annual

reports of NEXT Plc is analysed and interpreted which operates in clothing, footwear and

utility products. Technique of ratio analysis is used to analysis (Adams, 2015).

MAIN BODY

I. Evaluating limited liability company and its merits & demerits

Limited liability company is a corporate structure which allows its members to have a

limited liability to the extend of their share in the company. It is considered that under this

structure members are not personally liable for company's debts. This kind of company is known

as hybrid structure as it involves features of both a company and a sole proprietorship. LLC also

has few taxation features of partnership. There are various advantages and limitations of this

structure which are mentioned below in order to compare LLC with sole proprietorship and

partnership:

Difference between LLC and sole proprietorship:

LLC Sole proprietorship

Merits Members of LLC has limited

liability to the extend of their

share in company's capital.

LLC can enjoy all the

privileges of being a company

and sole proprietorship

(Edwards, 2013).

Owner of sole proprietorship

has unlimited liability and

even their personal assets

can be used to pay off firm's

liability.

This type of corporate

structure only has rights of

sole proprietorship.

Demerits Being a company, LLC has to

pay maintenance fees and high

Sole proprietorship does not

have any liability to get

1

Financial accounting and reporting is a concept of developing financial accounts in order

to ascertain performance of a business organisation. Main aim of this project report is to build an

understanding about limited liability company and its financial reporting system. Scope of this

project report includes merits and demerits of limited liability company in order to compare it

from sole proprietorship and partnership. In order to better understand this concept annual

reports of NEXT Plc is analysed and interpreted which operates in clothing, footwear and

utility products. Technique of ratio analysis is used to analysis (Adams, 2015).

MAIN BODY

I. Evaluating limited liability company and its merits & demerits

Limited liability company is a corporate structure which allows its members to have a

limited liability to the extend of their share in the company. It is considered that under this

structure members are not personally liable for company's debts. This kind of company is known

as hybrid structure as it involves features of both a company and a sole proprietorship. LLC also

has few taxation features of partnership. There are various advantages and limitations of this

structure which are mentioned below in order to compare LLC with sole proprietorship and

partnership:

Difference between LLC and sole proprietorship:

LLC Sole proprietorship

Merits Members of LLC has limited

liability to the extend of their

share in company's capital.

LLC can enjoy all the

privileges of being a company

and sole proprietorship

(Edwards, 2013).

Owner of sole proprietorship

has unlimited liability and

even their personal assets

can be used to pay off firm's

liability.

This type of corporate

structure only has rights of

sole proprietorship.

Demerits Being a company, LLC has to

pay maintenance fees and high

Sole proprietorship does not

have any liability to get

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

registration fee.

There are several regulations

which has to be fulfilled by the

company. This type of

structure is subject to state

laws governing.

registered or pay any fees

regarding maintenance and

registration.

Despite of business laws,

there are no additional

regulations applied on sole

proprietorship.

Difference between LLC and partnership:

LLC Partnership

Merits This type of structure enables

members of LLC to separate

their personal assets from

company's assets. They have a

limited liability to the extend

of their share in company's

capital.

Due to separate entity of

members and the company,

existence of LLC does not

effect with its members. Death

or insolvency of members

does nit influence firm's

existence.

Members of a partnership

firm are referred as partners

which has unlimited liability

for firm's debts and

liabilities.

Partnership firm can dissolve

with death or insolvency of

its partners.

Demerits There are various regulations

which are required to be

fulfilled by the promoter of

limited liability company.

Registration of this type of

company requires a lot of

resources and funds.

Partnership firm can be

formed when two or more

individuals decide to do a

business together. Partners

of this type of structure does

not have to fulfil any legal

requirements (Hoyle,

2

There are several regulations

which has to be fulfilled by the

company. This type of

structure is subject to state

laws governing.

registered or pay any fees

regarding maintenance and

registration.

Despite of business laws,

there are no additional

regulations applied on sole

proprietorship.

Difference between LLC and partnership:

LLC Partnership

Merits This type of structure enables

members of LLC to separate

their personal assets from

company's assets. They have a

limited liability to the extend

of their share in company's

capital.

Due to separate entity of

members and the company,

existence of LLC does not

effect with its members. Death

or insolvency of members

does nit influence firm's

existence.

Members of a partnership

firm are referred as partners

which has unlimited liability

for firm's debts and

liabilities.

Partnership firm can dissolve

with death or insolvency of

its partners.

Demerits There are various regulations

which are required to be

fulfilled by the promoter of

limited liability company.

Registration of this type of

company requires a lot of

resources and funds.

Partnership firm can be

formed when two or more

individuals decide to do a

business together. Partners

of this type of structure does

not have to fulfil any legal

requirements (Hoyle,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Formation and structure of

limited liability company is

more complex.

Schaefer and Doupnik,

2015).

Due to no legal

requirements, formation of

this type of corporate is

easier and cost effective.

By comparing limited liability company with corporate structures of partnership and sole

proprietorship, it has been analysed that structure of LLC is way more effective and beneficial as

a firm can attain benefits of a company without facing any unlimited liability.

II) Analysis and interpretation of annual reports of NEXT PLC

In order to analyse and interpret annual reports of NEXT PLC, ratio analysis technique is

used. Ratio analysis helps an organisation to ascertain their financial position in terms of

liquidity, profitability and efficiency. Information for five years of NEXT PLC is used to

interpret firm's financial position.

Ratio analysis has few limitations also which are mentioned as follows:

Results ascertained from ratios are not 100% reliable and accurate as there are various

non financial managerial factors.

A ratio is relationship between two numbers and sometimes there are few managerial

issues in an organisation due to which ratios can be not relied by management.

Ratios are based on historical data due to which they do not have a direct relevance with

company's performance.

Ratio analysis can not be used for comparison when nature of both businesses is different

(Lima Crisóstomo, 2011).

Computation of various ratios and their understanding is provided below:

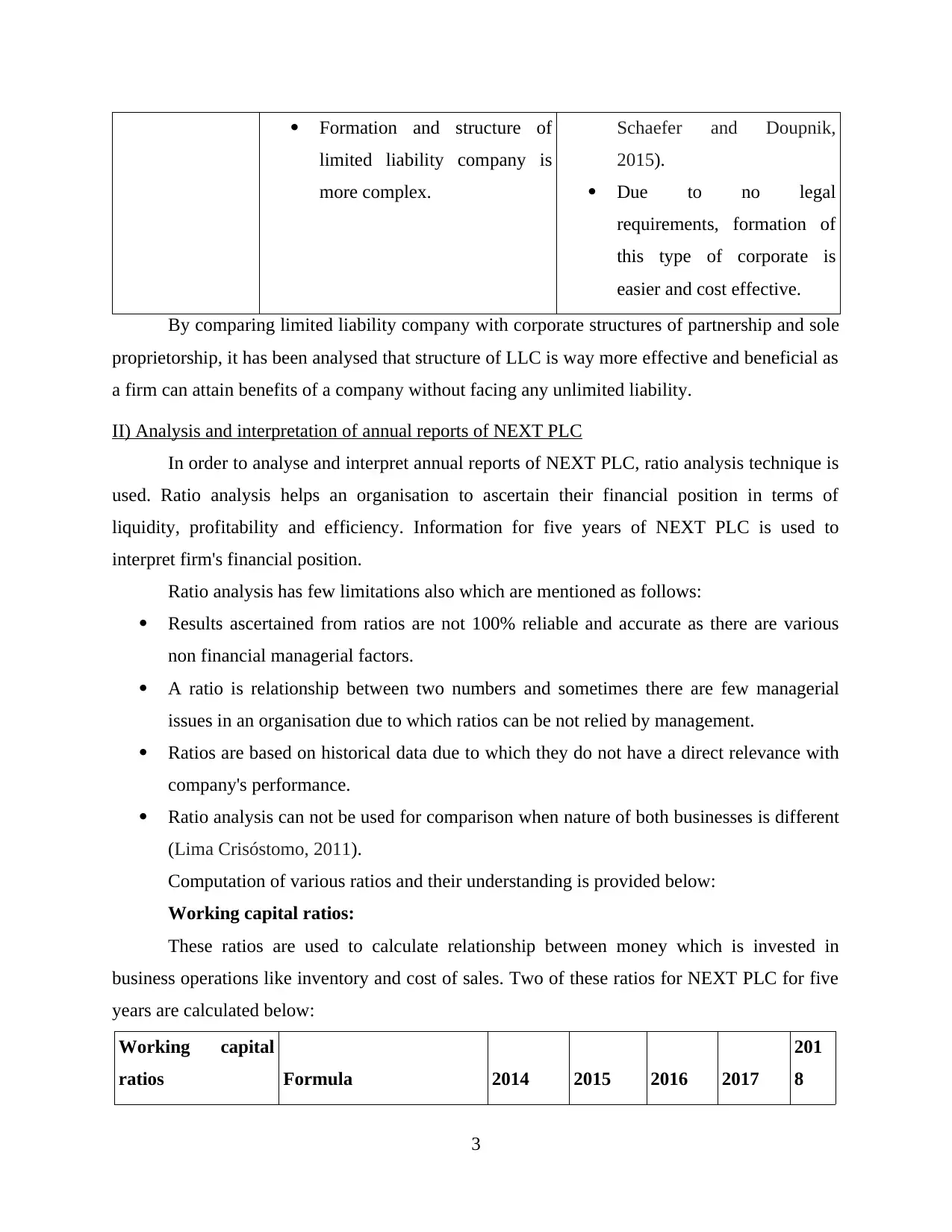

Working capital ratios:

These ratios are used to calculate relationship between money which is invested in

business operations like inventory and cost of sales. Two of these ratios for NEXT PLC for five

years are calculated below:

Working capital

ratios Formula 2014 2015 2016 2017

201

8

3

limited liability company is

more complex.

Schaefer and Doupnik,

2015).

Due to no legal

requirements, formation of

this type of corporate is

easier and cost effective.

By comparing limited liability company with corporate structures of partnership and sole

proprietorship, it has been analysed that structure of LLC is way more effective and beneficial as

a firm can attain benefits of a company without facing any unlimited liability.

II) Analysis and interpretation of annual reports of NEXT PLC

In order to analyse and interpret annual reports of NEXT PLC, ratio analysis technique is

used. Ratio analysis helps an organisation to ascertain their financial position in terms of

liquidity, profitability and efficiency. Information for five years of NEXT PLC is used to

interpret firm's financial position.

Ratio analysis has few limitations also which are mentioned as follows:

Results ascertained from ratios are not 100% reliable and accurate as there are various

non financial managerial factors.

A ratio is relationship between two numbers and sometimes there are few managerial

issues in an organisation due to which ratios can be not relied by management.

Ratios are based on historical data due to which they do not have a direct relevance with

company's performance.

Ratio analysis can not be used for comparison when nature of both businesses is different

(Lima Crisóstomo, 2011).

Computation of various ratios and their understanding is provided below:

Working capital ratios:

These ratios are used to calculate relationship between money which is invested in

business operations like inventory and cost of sales. Two of these ratios for NEXT PLC for five

years are calculated below:

Working capital

ratios Formula 2014 2015 2016 2017

201

8

3

Inventory turnover

Cost of sales / closing

inventory

6.490909

0909

6.38461

53846

5.60493

82716

6.00886

91796

5.50

816

326

53

Receivable days

ratio

Trade receivables / sales *

365

78.85561

49733

77.0342

585646

93.5440

566268

100.225

774957

3

112.

335

388

409

4

Inventory turnover Receivable days ratio

0

20

40

60

80

100

120

6.491

78.856

6.385

77.034

5.605

93.544

6.009

100.226

5.508

112.335

2014

2015

2016

2017

2018

From the ratio analysis of working capital ratios it has been analysed that, receivable days

are increasing every year that is 78.85 in 2014, 93.54 in 2016 and so on. In the case of inventory

turnover, NEXT PLC is having decreasing trend that is 6.49 in 2014, 6.38 in 2015 and so on.

Reason behind increasing trend of receivable days is efficiency in trade receivables. Decreasing

trend inventory turnover is the result low inventories in terms of sales which can further effect

organisation's profitability (Annual reports of NEXT PLC, 2018).

Liquidity ratios:

4

Cost of sales / closing

inventory

6.490909

0909

6.38461

53846

5.60493

82716

6.00886

91796

5.50

816

326

53

Receivable days

ratio

Trade receivables / sales *

365

78.85561

49733

77.0342

585646

93.5440

566268

100.225

774957

3

112.

335

388

409

4

Inventory turnover Receivable days ratio

0

20

40

60

80

100

120

6.491

78.856

6.385

77.034

5.605

93.544

6.009

100.226

5.508

112.335

2014

2015

2016

2017

2018

From the ratio analysis of working capital ratios it has been analysed that, receivable days

are increasing every year that is 78.85 in 2014, 93.54 in 2016 and so on. In the case of inventory

turnover, NEXT PLC is having decreasing trend that is 6.49 in 2014, 6.38 in 2015 and so on.

Reason behind increasing trend of receivable days is efficiency in trade receivables. Decreasing

trend inventory turnover is the result low inventories in terms of sales which can further effect

organisation's profitability (Annual reports of NEXT PLC, 2018).

Liquidity ratios:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

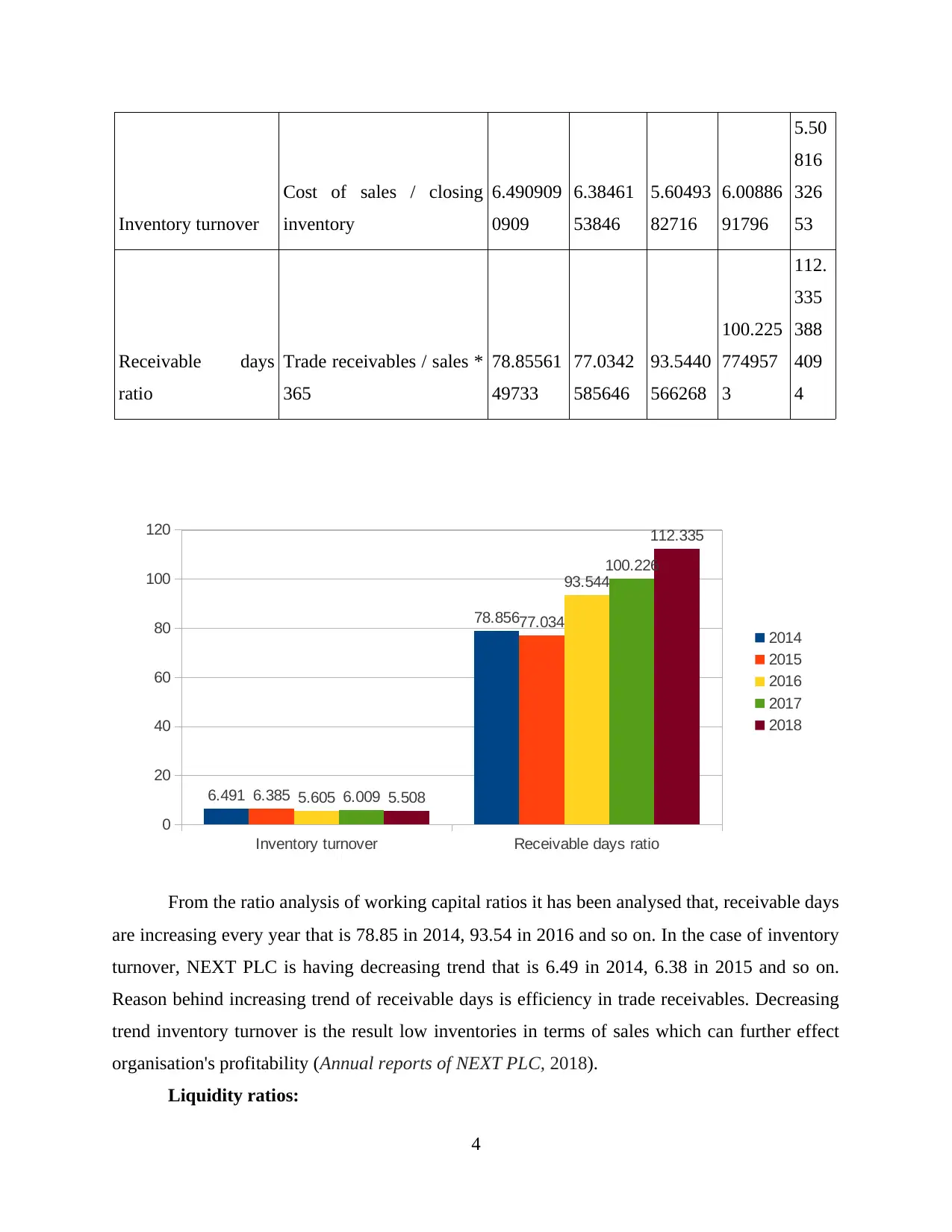

These ratios helps in ascertaining liquidity position of a company so that short term debt

paying ability of a firm can be ascertained. These ratios are used to determine whether a

company is fully utilising their funds in business operations or not, to attain operating benefits

(Lovell and MacKenzie, 2011). Two of these ratios are calculated below:

Liquidity ratios Formula 2014 2015 2016 2017 2018

Current ratio

Current assets / current

liabilities

1.760191

8465

1.49907

23562

1.40683

76068

1.42001

71086

1.96

6083

151

Quick ratio

Current assets –

inventories / current

liabilities

1.298561

1511

1.11317

25417

0.99145

29915

1.03421

72797

1.42

9978

1182

Current ratio Quick ratio

0

0.5

1

1.5

2

2.5

1.760

1.299

1.499

1.113

1.407

0.991

1.420

1.034

1.966

1.430 2014

2015

2016

2017

2018

From the above ascertained ratios and developed graph, it has been ascertained that there

is not suitable trend in both of the ratios. In the case of current ratio, year 2018 results to be

highest and year 2016 results to be lowest. This uneven current ratio of NEXT PLC shows that

this company does not have any uniformity in their current assets and current liabilities due to

5

paying ability of a firm can be ascertained. These ratios are used to determine whether a

company is fully utilising their funds in business operations or not, to attain operating benefits

(Lovell and MacKenzie, 2011). Two of these ratios are calculated below:

Liquidity ratios Formula 2014 2015 2016 2017 2018

Current ratio

Current assets / current

liabilities

1.760191

8465

1.49907

23562

1.40683

76068

1.42001

71086

1.96

6083

151

Quick ratio

Current assets –

inventories / current

liabilities

1.298561

1511

1.11317

25417

0.99145

29915

1.03421

72797

1.42

9978

1182

Current ratio Quick ratio

0

0.5

1

1.5

2

2.5

1.760

1.299

1.499

1.113

1.407

0.991

1.420

1.034

1.966

1.430 2014

2015

2016

2017

2018

From the above ascertained ratios and developed graph, it has been ascertained that there

is not suitable trend in both of the ratios. In the case of current ratio, year 2018 results to be

highest and year 2016 results to be lowest. This uneven current ratio of NEXT PLC shows that

this company does not have any uniformity in their current assets and current liabilities due to

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which they have to suffer excessive short term liability in most of their accounting periods. Ideal

current ratio is considered to be 2:1, but this company has low ratio in all the years.

Under the case of quick ratio, there is a same trend as current ratio, which shows that

there is less fluctuations in inventories. Ideal quick ratio is considered to be 1:1 and in every year

company is having ratio near to 1:1 which shows they are able to maintain their effective cash

position in the market.

Profitability ratios:

These ratios helps an organisation to ascertain whether or not company is earning reliable

and expected profits. Efficiency of earnings is ascertained by these ratios against incurred

expenses. By calculating these ratios, an individual can ascertain profit generating ability of a

company (Nobes, 2014). Two of these ratios are determined below:

Profitability ratios Formula 2014 2015 2016 2017 2018

Gross profit margin

Gross profit / revenue *

100

33.15508

02139

33.5833

95849

0.34770

11494

0.33829

63144

0.33

4401

9729

Net profit ratio Net profit / revenue * 100

0.147860

9626

0.15853

96349

0.15948

27586

0.15499

14572

0.14

5745

9926

6

current ratio is considered to be 2:1, but this company has low ratio in all the years.

Under the case of quick ratio, there is a same trend as current ratio, which shows that

there is less fluctuations in inventories. Ideal quick ratio is considered to be 1:1 and in every year

company is having ratio near to 1:1 which shows they are able to maintain their effective cash

position in the market.

Profitability ratios:

These ratios helps an organisation to ascertain whether or not company is earning reliable

and expected profits. Efficiency of earnings is ascertained by these ratios against incurred

expenses. By calculating these ratios, an individual can ascertain profit generating ability of a

company (Nobes, 2014). Two of these ratios are determined below:

Profitability ratios Formula 2014 2015 2016 2017 2018

Gross profit margin

Gross profit / revenue *

100

33.15508

02139

33.5833

95849

0.34770

11494

0.33829

63144

0.33

4401

9729

Net profit ratio Net profit / revenue * 100

0.147860

9626

0.15853

96349

0.15948

27586

0.15499

14572

0.14

5745

9926

6

Gross profit margin Net profit ratio

0

5

10

15

20

25

30

35

40

33.155

14.786

33.583

15.854

34.770

15.948

33.830

15.499

33.440

14.575

2014

2015

2016

2017

2018

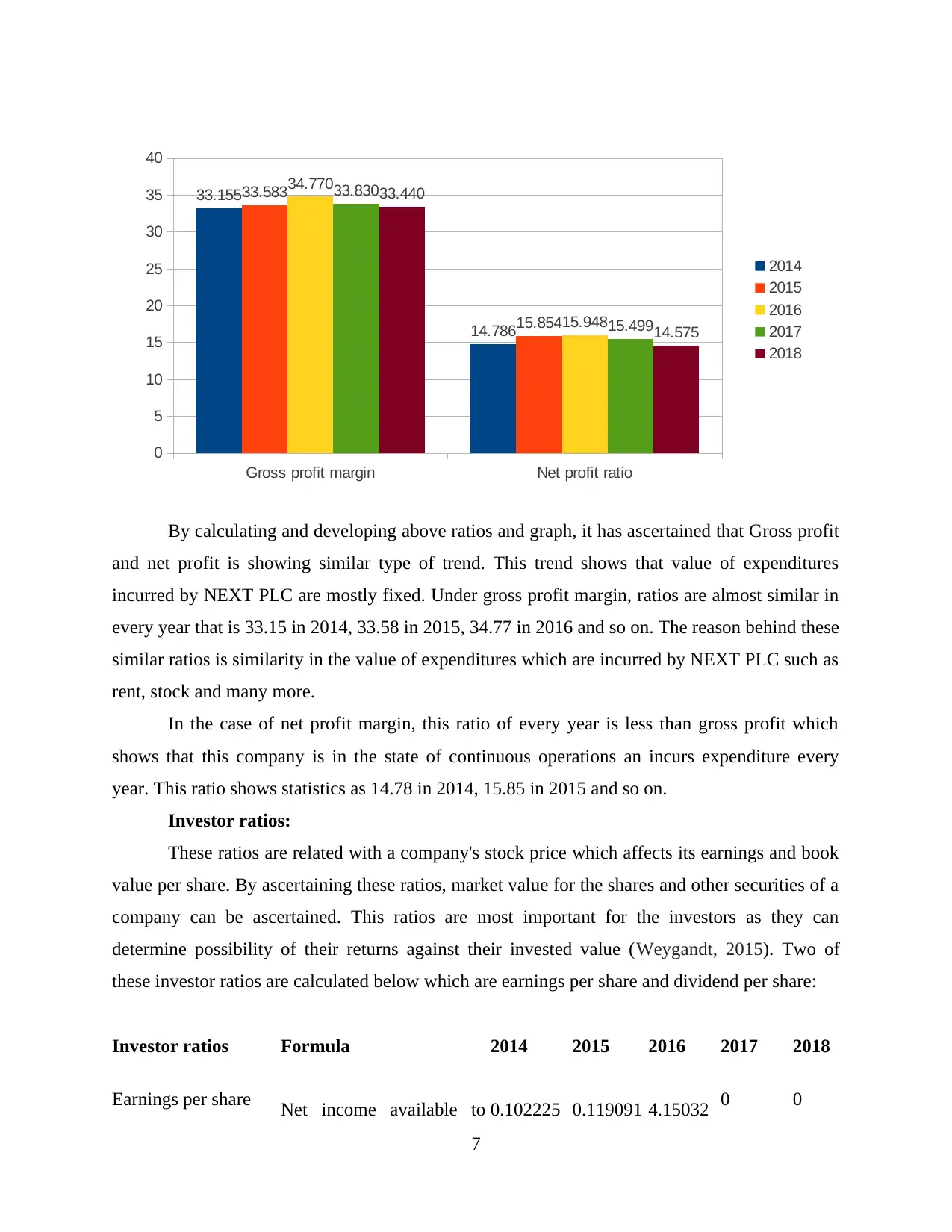

By calculating and developing above ratios and graph, it has ascertained that Gross profit

and net profit is showing similar type of trend. This trend shows that value of expenditures

incurred by NEXT PLC are mostly fixed. Under gross profit margin, ratios are almost similar in

every year that is 33.15 in 2014, 33.58 in 2015, 34.77 in 2016 and so on. The reason behind these

similar ratios is similarity in the value of expenditures which are incurred by NEXT PLC such as

rent, stock and many more.

In the case of net profit margin, this ratio of every year is less than gross profit which

shows that this company is in the state of continuous operations an incurs expenditure every

year. This ratio shows statistics as 14.78 in 2014, 15.85 in 2015 and so on.

Investor ratios:

These ratios are related with a company's stock price which affects its earnings and book

value per share. By ascertaining these ratios, market value for the shares and other securities of a

company can be ascertained. This ratios are most important for the investors as they can

determine possibility of their returns against their invested value (Weygandt, 2015). Two of

these investor ratios are calculated below which are earnings per share and dividend per share:

Investor ratios Formula 2014 2015 2016 2017 2018

Earnings per share Net income available to 0.102225 0.119091 4.15032 0 0

7

0

5

10

15

20

25

30

35

40

33.155

14.786

33.583

15.854

34.770

15.948

33.830

15.499

33.440

14.575

2014

2015

2016

2017

2018

By calculating and developing above ratios and graph, it has ascertained that Gross profit

and net profit is showing similar type of trend. This trend shows that value of expenditures

incurred by NEXT PLC are mostly fixed. Under gross profit margin, ratios are almost similar in

every year that is 33.15 in 2014, 33.58 in 2015, 34.77 in 2016 and so on. The reason behind these

similar ratios is similarity in the value of expenditures which are incurred by NEXT PLC such as

rent, stock and many more.

In the case of net profit margin, this ratio of every year is less than gross profit which

shows that this company is in the state of continuous operations an incurs expenditure every

year. This ratio shows statistics as 14.78 in 2014, 15.85 in 2015 and so on.

Investor ratios:

These ratios are related with a company's stock price which affects its earnings and book

value per share. By ascertaining these ratios, market value for the shares and other securities of a

company can be ascertained. This ratios are most important for the investors as they can

determine possibility of their returns against their invested value (Weygandt, 2015). Two of

these investor ratios are calculated below which are earnings per share and dividend per share:

Investor ratios Formula 2014 2015 2016 2017 2018

Earnings per share Net income available to 0.102225 0.119091 4.15032 0 0

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

common shareholders /

Number of common shares 0887 7516 67974

Dividend per share

Total dividend / number of

common shares

0.069816

1883

0.269230

7692

1.47058

82353

1.51006

71141

3.23

6486

4865

Earnings per share Dividend per share

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0.102 0.0700.119 0.269

4.150

1.471

0.000

1.510

0.000

3.236

2014

2015

2016

2017

2018

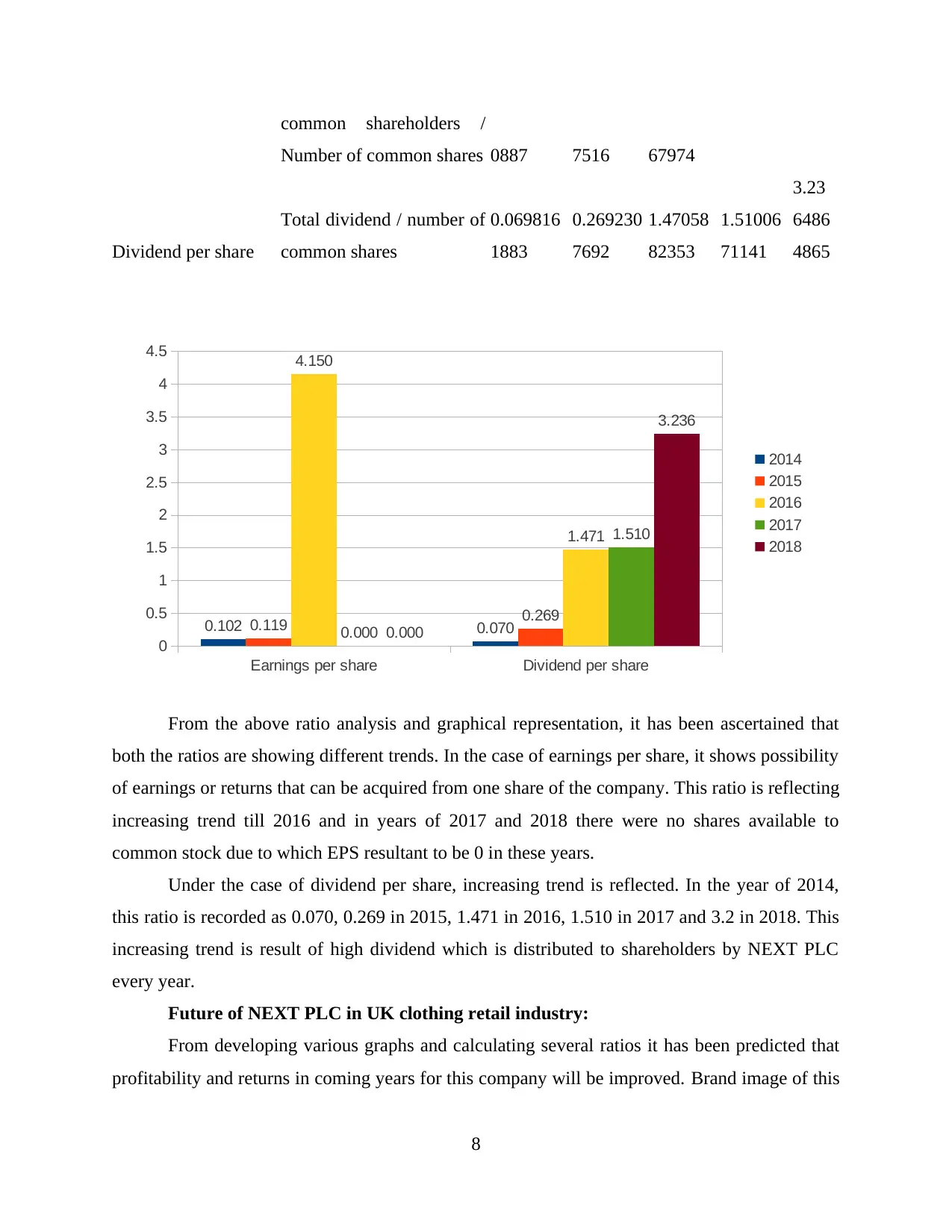

From the above ratio analysis and graphical representation, it has been ascertained that

both the ratios are showing different trends. In the case of earnings per share, it shows possibility

of earnings or returns that can be acquired from one share of the company. This ratio is reflecting

increasing trend till 2016 and in years of 2017 and 2018 there were no shares available to

common stock due to which EPS resultant to be 0 in these years.

Under the case of dividend per share, increasing trend is reflected. In the year of 2014,

this ratio is recorded as 0.070, 0.269 in 2015, 1.471 in 2016, 1.510 in 2017 and 3.2 in 2018. This

increasing trend is result of high dividend which is distributed to shareholders by NEXT PLC

every year.

Future of NEXT PLC in UK clothing retail industry:

From developing various graphs and calculating several ratios it has been predicted that

profitability and returns in coming years for this company will be improved. Brand image of this

8

Number of common shares 0887 7516 67974

Dividend per share

Total dividend / number of

common shares

0.069816

1883

0.269230

7692

1.47058

82353

1.51006

71141

3.23

6486

4865

Earnings per share Dividend per share

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

0.102 0.0700.119 0.269

4.150

1.471

0.000

1.510

0.000

3.236

2014

2015

2016

2017

2018

From the above ratio analysis and graphical representation, it has been ascertained that

both the ratios are showing different trends. In the case of earnings per share, it shows possibility

of earnings or returns that can be acquired from one share of the company. This ratio is reflecting

increasing trend till 2016 and in years of 2017 and 2018 there were no shares available to

common stock due to which EPS resultant to be 0 in these years.

Under the case of dividend per share, increasing trend is reflected. In the year of 2014,

this ratio is recorded as 0.070, 0.269 in 2015, 1.471 in 2016, 1.510 in 2017 and 3.2 in 2018. This

increasing trend is result of high dividend which is distributed to shareholders by NEXT PLC

every year.

Future of NEXT PLC in UK clothing retail industry:

From developing various graphs and calculating several ratios it has been predicted that

profitability and returns in coming years for this company will be improved. Brand image of this

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company is also forecasted to be enhanced because of high shareholder's satisfaction from

regular dividends. NEXT PLC should reconsider their operations to ensure better future for their

liquidity and working capital position.

CONCLUSION

From the above project report, it has been ascertained that limited liability company is a

better structure than partnership or sole proprietorship as it enables a business firm to take

benefits of being a company which any unlimited liability. By developing various graphs and

calculating several ratios, it has been ascertained that this technique can help any individual in

ascertaining financial position of a company but fails to re[present managerial position.

9

regular dividends. NEXT PLC should reconsider their operations to ensure better future for their

liquidity and working capital position.

CONCLUSION

From the above project report, it has been ascertained that limited liability company is a

better structure than partnership or sole proprietorship as it enables a business firm to take

benefits of being a company which any unlimited liability. By developing various graphs and

calculating several ratios, it has been ascertained that this technique can help any individual in

ascertaining financial position of a company but fails to re[present managerial position.

9

REFERENCES

Books and Journals

Adams, C. A., 2015. The international integrated reporting council: a call to action. Critical

Perspectives on Accounting. 27. pp.23-28.

Lima Crisóstomo, J. R., 2011. A History of Financial Accounting (RLE Accounting). Routledge.

Hoyle, J. B., Schaefer and Doupnik T. T., 2015 . Advanced accounting. McGraw Hill.

Lima Crisóstomo, V., de Souza Freire, F. and Cortes de Vasconcellos, F., 2011. Corporate social

responsibility, firm value and financial performance in Brazil. Social Responsibility

Journal. 7(2). pp.295-309.

Lovell H. and MacKenzie,. aD., 2011. Accounting for carbon: the role of accounting

professional organisations in governing climate change. Antipode. 43(3). pp.704-730.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Kimmel, P. D. and Kieso, D. E., . Financial & managerial accounting. John Wiley & Sons.

Online

Annual reports of NEXT PLC. 2018. [Online]. Available through:

<https://www.nextplc.co.uk/~/media/Files/N/Next-PLC-V2/documents/2018/annual-

report-and-accounts-jan-2018.pdf>

10

Books and Journals

Adams, C. A., 2015. The international integrated reporting council: a call to action. Critical

Perspectives on Accounting. 27. pp.23-28.

Lima Crisóstomo, J. R., 2011. A History of Financial Accounting (RLE Accounting). Routledge.

Hoyle, J. B., Schaefer and Doupnik T. T., 2015 . Advanced accounting. McGraw Hill.

Lima Crisóstomo, V., de Souza Freire, F. and Cortes de Vasconcellos, F., 2011. Corporate social

responsibility, firm value and financial performance in Brazil. Social Responsibility

Journal. 7(2). pp.295-309.

Lovell H. and MacKenzie,. aD., 2011. Accounting for carbon: the role of accounting

professional organisations in governing climate change. Antipode. 43(3). pp.704-730.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Kimmel, P. D. and Kieso, D. E., . Financial & managerial accounting. John Wiley & Sons.

Online

Annual reports of NEXT PLC. 2018. [Online]. Available through:

<https://www.nextplc.co.uk/~/media/Files/N/Next-PLC-V2/documents/2018/annual-

report-and-accounts-jan-2018.pdf>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.