Financial Accounting and Reporting: A Comprehensive Analysis of Brambles Limited

VerifiedAdded on 2024/06/04

|12

|2923

|63

AI Summary

This report delves into the financial accounting and reporting practices of Brambles Limited, a leading industrial products company. It examines the nature of general purpose financial reports (GPFR) in the context of AASB's SAC 1, explores the recognition criteria for property, plant and equipment (PPE), and analyzes the requirements of AASB 116. The report also discusses depreciation expense, useful life, residual value, and fair value, providing insights into the ethical considerations involved in financial statement preparation. Through a comprehensive analysis of Brambles Limited's financial statements, the report aims to provide a clear understanding of key accounting concepts and their practical application in a real-world business context.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Accounting and Reporting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary:

The accounting and reporting work performed in an enterprise have become increasingly

important and relevant for the success and growth of an enterprise. The financial reports as

presented by the organisation represent the way in which the enterprise informs their investors

regarding the financial position and performance of an enterprise. The report will thus help in

evaluating the financial statement preparation of an enterprise in context of various accounting

standards provided in AASB. The function of high quality reporting is considered crucial for

analysing the operational efficiently of an enterprise and the same assists in effective reporting.

The report will include the financial analysis of an enterprise which is listed in the Australian

Stock Exchange and the interpretations will thus be used to recommend the solution for the

relevant problems associated.

2

The accounting and reporting work performed in an enterprise have become increasingly

important and relevant for the success and growth of an enterprise. The financial reports as

presented by the organisation represent the way in which the enterprise informs their investors

regarding the financial position and performance of an enterprise. The report will thus help in

evaluating the financial statement preparation of an enterprise in context of various accounting

standards provided in AASB. The function of high quality reporting is considered crucial for

analysing the operational efficiently of an enterprise and the same assists in effective reporting.

The report will include the financial analysis of an enterprise which is listed in the Australian

Stock Exchange and the interpretations will thus be used to recommend the solution for the

relevant problems associated.

2

Contents

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................4

1. Explain the nature of general purpose financial reports (GPFR) in the context of the

AASB’s current SAC 1 Definition of the Reporting Entity.........................................................5

2. Describe what assets constitute property, plant and equipment (PPE), and what the

recognition criteria are for PPE....................................................................................................5

3. Outline and explain the requirements of AASB 116 in relation to:.........................................6

4. What is meant by depreciation expense, and explain whether all assets are subject to

depreciation?................................................................................................................................7

5. How is useful life determined, and what is meant by residual value of an asset?...................8

6. What is fair value? Discuss whether AASB 116 set fair value as the ceiling for the carrying

amount of assets and the impact of AASB 112 tax effect accounting on assets carried at fair

value.............................................................................................................................................9

7. Discuss whether CEO’s argument is ethical when preparing the company’s financial

statements in accordance with AASB101..................................................................................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

3

Executive Summary:........................................................................................................................2

Introduction:....................................................................................................................................4

1. Explain the nature of general purpose financial reports (GPFR) in the context of the

AASB’s current SAC 1 Definition of the Reporting Entity.........................................................5

2. Describe what assets constitute property, plant and equipment (PPE), and what the

recognition criteria are for PPE....................................................................................................5

3. Outline and explain the requirements of AASB 116 in relation to:.........................................6

4. What is meant by depreciation expense, and explain whether all assets are subject to

depreciation?................................................................................................................................7

5. How is useful life determined, and what is meant by residual value of an asset?...................8

6. What is fair value? Discuss whether AASB 116 set fair value as the ceiling for the carrying

amount of assets and the impact of AASB 112 tax effect accounting on assets carried at fair

value.............................................................................................................................................9

7. Discuss whether CEO’s argument is ethical when preparing the company’s financial

statements in accordance with AASB101..................................................................................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

3

Introduction:

The main purpose of the report is to conduct a financial analysis of an enterprise in order to make

decisions. In order to serve this purpose a company will has been chosen whose name Brambles

Limited is dealing in industrial products. The report will contain the matter related with general

purpose associate with prepari8ng the financial statement of an enterprise. The description about

various assets recognized in property, plant and equipment will be identified and the

measurement and recognition criteria will be evaluated in context of an organization. The

information about depreciation treatment in an enterprise will be explained and the residual value

will be explained appropriately. The fair value assessment regarding the different assets of an

enterprise will be recognized and recommendation will be made for the same.

4

The main purpose of the report is to conduct a financial analysis of an enterprise in order to make

decisions. In order to serve this purpose a company will has been chosen whose name Brambles

Limited is dealing in industrial products. The report will contain the matter related with general

purpose associate with prepari8ng the financial statement of an enterprise. The description about

various assets recognized in property, plant and equipment will be identified and the

measurement and recognition criteria will be evaluated in context of an organization. The

information about depreciation treatment in an enterprise will be explained and the residual value

will be explained appropriately. The fair value assessment regarding the different assets of an

enterprise will be recognized and recommendation will be made for the same.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1. Explain the nature of general purpose financial reports (GPFR) in the context of the

AASB’s current SAC 1 Definition of the Reporting Entity.

As per SAC 1, Definition of Reporting Entity The objective and nature of general purpose

financial reporting is to provide the users with sufficient and adequate information about the

reporting entity so that the users can make the informed and appropriate decision after making

evaluations about the various aspects of entity (Barth, 2015). The objective also means the way

in which the management and governing bodies of the organisation discharge their

accountabilities and responsibilities regarding users. The general purpose financial reports needs

to be prepared for the users who are required to make decisions about the allocation of various

resources and make a correct investment decision. The concept requires the identification of an

entity in reference to the existence of users who are highly dependent on the general purpose

financial statement for their decision making purpose. In case of Brambles Limited it can be

established that the nature of general purpose of financial statement is associated with

recognizing the information needs of the users who are willing to make investment in company

and discharging the accountability towards various stakeholders of company.

2. Describe what assets constitute property, plant and equipment (PPE), and what the

recognition criteria are for PPE.

The property, plant and equipments are recognized and reported at liabilities side of balance

sheet as noncurrent assets and these includes the items such as land, buildings, office

equipments, machinery, furniture and fixtures and vehicles which are used in a business. The

[property, plant and equipments also includes the accumulated depreciation concerned with these

items (Beatty & Liao, 2014). Thus the property, plant and equipment consist of the tangible and

long lived assets of the company which are held for long purpose.

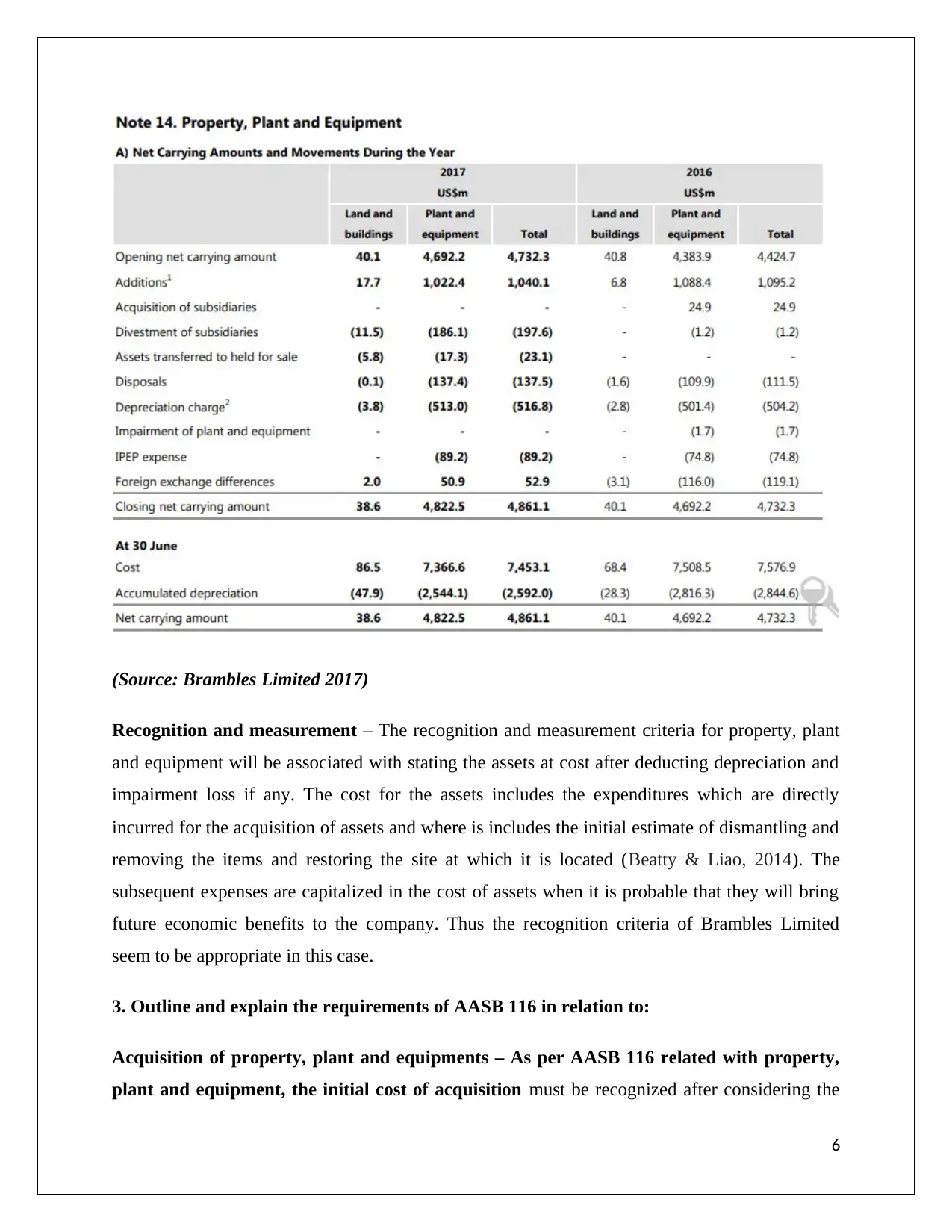

The property, plant and equipment section for Brambles Limited includes the assets such as land

and buildings and plant and equipment necessary for carrying out the operational functions of

company. The schedule for property, plant and equipment is presented below:

5

AASB’s current SAC 1 Definition of the Reporting Entity.

As per SAC 1, Definition of Reporting Entity The objective and nature of general purpose

financial reporting is to provide the users with sufficient and adequate information about the

reporting entity so that the users can make the informed and appropriate decision after making

evaluations about the various aspects of entity (Barth, 2015). The objective also means the way

in which the management and governing bodies of the organisation discharge their

accountabilities and responsibilities regarding users. The general purpose financial reports needs

to be prepared for the users who are required to make decisions about the allocation of various

resources and make a correct investment decision. The concept requires the identification of an

entity in reference to the existence of users who are highly dependent on the general purpose

financial statement for their decision making purpose. In case of Brambles Limited it can be

established that the nature of general purpose of financial statement is associated with

recognizing the information needs of the users who are willing to make investment in company

and discharging the accountability towards various stakeholders of company.

2. Describe what assets constitute property, plant and equipment (PPE), and what the

recognition criteria are for PPE.

The property, plant and equipments are recognized and reported at liabilities side of balance

sheet as noncurrent assets and these includes the items such as land, buildings, office

equipments, machinery, furniture and fixtures and vehicles which are used in a business. The

[property, plant and equipments also includes the accumulated depreciation concerned with these

items (Beatty & Liao, 2014). Thus the property, plant and equipment consist of the tangible and

long lived assets of the company which are held for long purpose.

The property, plant and equipment section for Brambles Limited includes the assets such as land

and buildings and plant and equipment necessary for carrying out the operational functions of

company. The schedule for property, plant and equipment is presented below:

5

(Source: Brambles Limited 2017)

Recognition and measurement – The recognition and measurement criteria for property, plant

and equipment will be associated with stating the assets at cost after deducting depreciation and

impairment loss if any. The cost for the assets includes the expenditures which are directly

incurred for the acquisition of assets and where is includes the initial estimate of dismantling and

removing the items and restoring the site at which it is located (Beatty & Liao, 2014). The

subsequent expenses are capitalized in the cost of assets when it is probable that they will bring

future economic benefits to the company. Thus the recognition criteria of Brambles Limited

seem to be appropriate in this case.

3. Outline and explain the requirements of AASB 116 in relation to:

Acquisition of property, plant and equipments – As per AASB 116 related with property,

plant and equipment, the initial cost of acquisition must be recognized after considering the

6

Recognition and measurement – The recognition and measurement criteria for property, plant

and equipment will be associated with stating the assets at cost after deducting depreciation and

impairment loss if any. The cost for the assets includes the expenditures which are directly

incurred for the acquisition of assets and where is includes the initial estimate of dismantling and

removing the items and restoring the site at which it is located (Beatty & Liao, 2014). The

subsequent expenses are capitalized in the cost of assets when it is probable that they will bring

future economic benefits to the company. Thus the recognition criteria of Brambles Limited

seem to be appropriate in this case.

3. Outline and explain the requirements of AASB 116 in relation to:

Acquisition of property, plant and equipments – As per AASB 116 related with property,

plant and equipment, the initial cost of acquisition must be recognized after considering the

6

nature and purpose for which the cost has been incurred for an enterprise. Te cost of acquisition

for a property, plant and equipments refers to eth cash price equivalent at the recognition date

(Waegenaere, et. al., 2015). If the payments are deferred over the normal credit period of

company then the difference between the cash price and the payments will be recognized as

interest over the period of credit unless these are capitalized to the cost of acquisition. Also the

cost of acquisition system includes the basic elements described below:

The purchase price of the asset including the import duties and non refundable taxes

which is obtained after deducting the rebates and discounts allowed by the supplier.

Any type of costs which are directly attributable for bringing the asset to the location and

the condition necessary for carrying out operations associated.

The initial cost of removing and dismantling the item and restoring the same at the place

of operations.

The measurement of property, plant and equipments subsequent to acquisition – The

measurement of subsequent cost associated with cost of asset is related with identifying the cost

that has been incurred in relation to replacement of asset. The cost must be measured after

considering the amounts expended for the replacement(Beatty & Liao, 2014). Thus the

subsequent cost of improvement will be capitalized in the value of asst if it is probable that it will

bring future economic benefits to the company and the entity will be able to use the asset for a

longer period of time.

4. What is meant by depreciation expense, and explain whether all assets are subject to

depreciation?

The depreciation associated with the assets in a business can be defined as the expense of an

asset involved in producing various types of revenues for the company during its useful life

(Robson, et. al., 2017). In context of accounting it is defined as the allocation of cost of assets to

the periods in which the asset is used by the company The calculation of depreciation expense

affects the value of business as the accumulated depreciation as disclosed in the financial

statement will reduce the book value of asset and it also affects the net income derived by the

company during the year.

7

for a property, plant and equipments refers to eth cash price equivalent at the recognition date

(Waegenaere, et. al., 2015). If the payments are deferred over the normal credit period of

company then the difference between the cash price and the payments will be recognized as

interest over the period of credit unless these are capitalized to the cost of acquisition. Also the

cost of acquisition system includes the basic elements described below:

The purchase price of the asset including the import duties and non refundable taxes

which is obtained after deducting the rebates and discounts allowed by the supplier.

Any type of costs which are directly attributable for bringing the asset to the location and

the condition necessary for carrying out operations associated.

The initial cost of removing and dismantling the item and restoring the same at the place

of operations.

The measurement of property, plant and equipments subsequent to acquisition – The

measurement of subsequent cost associated with cost of asset is related with identifying the cost

that has been incurred in relation to replacement of asset. The cost must be measured after

considering the amounts expended for the replacement(Beatty & Liao, 2014). Thus the

subsequent cost of improvement will be capitalized in the value of asst if it is probable that it will

bring future economic benefits to the company and the entity will be able to use the asset for a

longer period of time.

4. What is meant by depreciation expense, and explain whether all assets are subject to

depreciation?

The depreciation associated with the assets in a business can be defined as the expense of an

asset involved in producing various types of revenues for the company during its useful life

(Robson, et. al., 2017). In context of accounting it is defined as the allocation of cost of assets to

the periods in which the asset is used by the company The calculation of depreciation expense

affects the value of business as the accumulated depreciation as disclosed in the financial

statement will reduce the book value of asset and it also affects the net income derived by the

company during the year.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The tangible assets of the company are subjected to depreciation but there are some kinds of

assets on which no depreciation is charged and they are as follows:

Land – Although it is a long term tangible asset of the company still it is not changed to

depreciations.

Financial assets – The financial assets of the company including the various types of

current assets are not depreciated by the management. These types of assets include

accounts receivables, derivatives and other assets (Scott, 2015). These assts does not lose

their value due to time and hence are not depreciated.

For Brambles Limited, the depreciation expense for the year has amounted to $500.0 million in

the year 2017 which is related to property, plant and equipments of company.

5. How is useful life determined, and what is meant by residual value of an asset?

The useful life associated with the asset of company is the estimation of the length of time in

which the asset can be reasonable used by the company and will bring benefits to the company. It

does not really means the time the asset will last for the company (Warren & Jones, 2018). The

useful life of the asset will vary according to user and to is also dependent on the asset age, the

frequency with which it is used, the condition of the environment of business in which it is used

and the asset repairmen policy of company. The other factors which impact the determination of

depreciation includes the anticipated technological improvements, changes in economic factors

and the associated changes in laws.

The useful life in case of Brambles Limited has been estimated after making careful assumptions

and considering the economic conditions of the business and industry in which the company is

operating. The operating life of asset which is estimated for different assets in property, plant and

equipments are shown as under:

Buildings – 50 Years

Pooling equipments – 5 – 10 years

Other plant and equipments – 3 – 20 years.

8

assets on which no depreciation is charged and they are as follows:

Land – Although it is a long term tangible asset of the company still it is not changed to

depreciations.

Financial assets – The financial assets of the company including the various types of

current assets are not depreciated by the management. These types of assets include

accounts receivables, derivatives and other assets (Scott, 2015). These assts does not lose

their value due to time and hence are not depreciated.

For Brambles Limited, the depreciation expense for the year has amounted to $500.0 million in

the year 2017 which is related to property, plant and equipments of company.

5. How is useful life determined, and what is meant by residual value of an asset?

The useful life associated with the asset of company is the estimation of the length of time in

which the asset can be reasonable used by the company and will bring benefits to the company. It

does not really means the time the asset will last for the company (Warren & Jones, 2018). The

useful life of the asset will vary according to user and to is also dependent on the asset age, the

frequency with which it is used, the condition of the environment of business in which it is used

and the asset repairmen policy of company. The other factors which impact the determination of

depreciation includes the anticipated technological improvements, changes in economic factors

and the associated changes in laws.

The useful life in case of Brambles Limited has been estimated after making careful assumptions

and considering the economic conditions of the business and industry in which the company is

operating. The operating life of asset which is estimated for different assets in property, plant and

equipments are shown as under:

Buildings – 50 Years

Pooling equipments – 5 – 10 years

Other plant and equipments – 3 – 20 years.

8

Residual value of an asset – The residual value associated with an asset refers to the estimated

amount that a company can realize on the disposal of asset at the end of its useful life. The

determination of residual value of an asset is a subject matter of deducting the estimated cost of

disposing the asset.

6. What is fair value? Discuss whether AASB 116 set fair value as the ceiling for the

carrying amount of assets and the impact of AASB 112 tax effect accounting on assets

carried at fair value.

Fair value of an asset represents the current value or price of the asset in market. In other words

it can be represented as the value of the asset which it can fetch in the outside market when it is

sold. The fair value can be measured as the monetary amount which a buyer is willing to pay to

the seller of the asset considering the current economic conditions and circumstances of the asset

(Scott, 2015). The market approach of valuing the asset is easier in order to recognize the fair

value of the asset as the ready to sae price is available in the market for an asset. The

determination of fair value of an asset is significant for the company in determining the financial

statements and this will help the company in estimating the total; worth of company in the

market.

The fair value of an asset can be recognized maximum to its recoverable value less costs incurred

to sell the asset. As per AASB 116, the cost of an asset recognized in the property, plant and

equipment can be carried maximum to its fair value and if there is any reduction in the fair value

of an asset then it is impaired accordingly (Waegenaere, et. al., 2015). The carrying amount of an

asset thus can be recognized at fair value which can be recognized by the company in its normal

course of business at the end of life of asset.

The Australian Accounting Standard allows the use of fair value for the prose of carrying the

asset in its financial statement but the same results in some of the temporary differences as and

when in some jurisdictions the revaluation of other restatement affects the taxable profit of the

company for the current period and in some other jurisdictions the taxable profits are not affected

by those adjustments or revaluations. In such cases the tax base of the company needs to be

adjusted according to the taxable portion of company.

9

amount that a company can realize on the disposal of asset at the end of its useful life. The

determination of residual value of an asset is a subject matter of deducting the estimated cost of

disposing the asset.

6. What is fair value? Discuss whether AASB 116 set fair value as the ceiling for the

carrying amount of assets and the impact of AASB 112 tax effect accounting on assets

carried at fair value.

Fair value of an asset represents the current value or price of the asset in market. In other words

it can be represented as the value of the asset which it can fetch in the outside market when it is

sold. The fair value can be measured as the monetary amount which a buyer is willing to pay to

the seller of the asset considering the current economic conditions and circumstances of the asset

(Scott, 2015). The market approach of valuing the asset is easier in order to recognize the fair

value of the asset as the ready to sae price is available in the market for an asset. The

determination of fair value of an asset is significant for the company in determining the financial

statements and this will help the company in estimating the total; worth of company in the

market.

The fair value of an asset can be recognized maximum to its recoverable value less costs incurred

to sell the asset. As per AASB 116, the cost of an asset recognized in the property, plant and

equipment can be carried maximum to its fair value and if there is any reduction in the fair value

of an asset then it is impaired accordingly (Waegenaere, et. al., 2015). The carrying amount of an

asset thus can be recognized at fair value which can be recognized by the company in its normal

course of business at the end of life of asset.

The Australian Accounting Standard allows the use of fair value for the prose of carrying the

asset in its financial statement but the same results in some of the temporary differences as and

when in some jurisdictions the revaluation of other restatement affects the taxable profit of the

company for the current period and in some other jurisdictions the taxable profits are not affected

by those adjustments or revaluations. In such cases the tax base of the company needs to be

adjusted according to the taxable portion of company.

9

7. Discuss whether CEO’s argument is ethical when preparing the company’s financial

statements in accordance with AASB101.

No the CEO argument regarding the depreciation is not ethical and the reason for the same is

described below:

The purpose of charging depreciation is to match the cost of productive asset with the revenues

obtained by the company while using the asset. However it is hard to track a direct link with the

revenues and therefore the cost of asset is allocated to the years of using the asset. Thus the

allocation of depreciation helps in ensuring that the matching principle of accounting is followed

while preparing the financial statement of company. Also the determination of depreciation

expense helps in estimating the real profits of the company which are concerned with

establishing the financial performance during the year. The use of depreciation allows the

business to claim tax benefits by showing the depreciation expense as the allowable deduction

for taxation purposes (Warren & Jones, 2018).

Thus the depreciation should be recognized even if there is no diminution in the value f the asset

in order to ensure eth accuracy of matching principle.

10

statements in accordance with AASB101.

No the CEO argument regarding the depreciation is not ethical and the reason for the same is

described below:

The purpose of charging depreciation is to match the cost of productive asset with the revenues

obtained by the company while using the asset. However it is hard to track a direct link with the

revenues and therefore the cost of asset is allocated to the years of using the asset. Thus the

allocation of depreciation helps in ensuring that the matching principle of accounting is followed

while preparing the financial statement of company. Also the determination of depreciation

expense helps in estimating the real profits of the company which are concerned with

establishing the financial performance during the year. The use of depreciation allows the

business to claim tax benefits by showing the depreciation expense as the allowable deduction

for taxation purposes (Warren & Jones, 2018).

Thus the depreciation should be recognized even if there is no diminution in the value f the asset

in order to ensure eth accuracy of matching principle.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Conclusion:

The above report concludes that financial accounting and reporting can be recognized as a

crucial element of financial decision making in a company and the management needs to prepare

the accounting reports as per eth accountings standards prescribed for the company. By analysing

the current situation of financial statements of company it can be established that the financial

reports have been prepared after considering all the standards appropriately and the CEO of the

company should take into consideration the depreciation expense while preparing the financial

reports. This will help in ensuring that adequate correct financial reports have been provided to

various users and they can make appropriate decision regarding the investment to be made.

11

The above report concludes that financial accounting and reporting can be recognized as a

crucial element of financial decision making in a company and the management needs to prepare

the accounting reports as per eth accountings standards prescribed for the company. By analysing

the current situation of financial statements of company it can be established that the financial

reports have been prepared after considering all the standards appropriately and the CEO of the

company should take into consideration the depreciation expense while preparing the financial

reports. This will help in ensuring that adequate correct financial reports have been provided to

various users and they can make appropriate decision regarding the investment to be made.

11

References:

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of

the empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Dutta, S., & Patatoukas, P. N. (2016). Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), 191-216.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Reid, W., & Myddelton, D. R. (2017). The meaning of company accounts. Routledge.

Robson, K., Young, J., & Power, M. (2017). Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, 35-37.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Waegenaere, A., Sansing, R., & Wielhouwer, J. L. (2015). Financial accounting effects of

tax aggressiveness: Contracting and measurement. Contemporary Accounting

Research, 32(1), 223-242.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

12

Barth, M. E. (2015). Financial accounting research, practice, and financial

accountability. Abacus, 51(4), 499-510.

Beatty, A., & Liao, S. (2014). Financial accounting in the banking industry: A review of

the empirical literature. Journal of Accounting and Economics, 58(2-3), 339-383.

Dutta, S., & Patatoukas, P. N. (2016). Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), 191-216.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Reid, W., & Myddelton, D. R. (2017). The meaning of company accounts. Routledge.

Robson, K., Young, J., & Power, M. (2017). Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, 35-37.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Waegenaere, A., Sansing, R., & Wielhouwer, J. L. (2015). Financial accounting effects of

tax aggressiveness: Contracting and measurement. Contemporary Accounting

Research, 32(1), 223-242.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

12

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.