Recent Changes in Financial Reporting Environment

VerifiedAdded on 2023/01/18

|10

|1172

|25

AI Summary

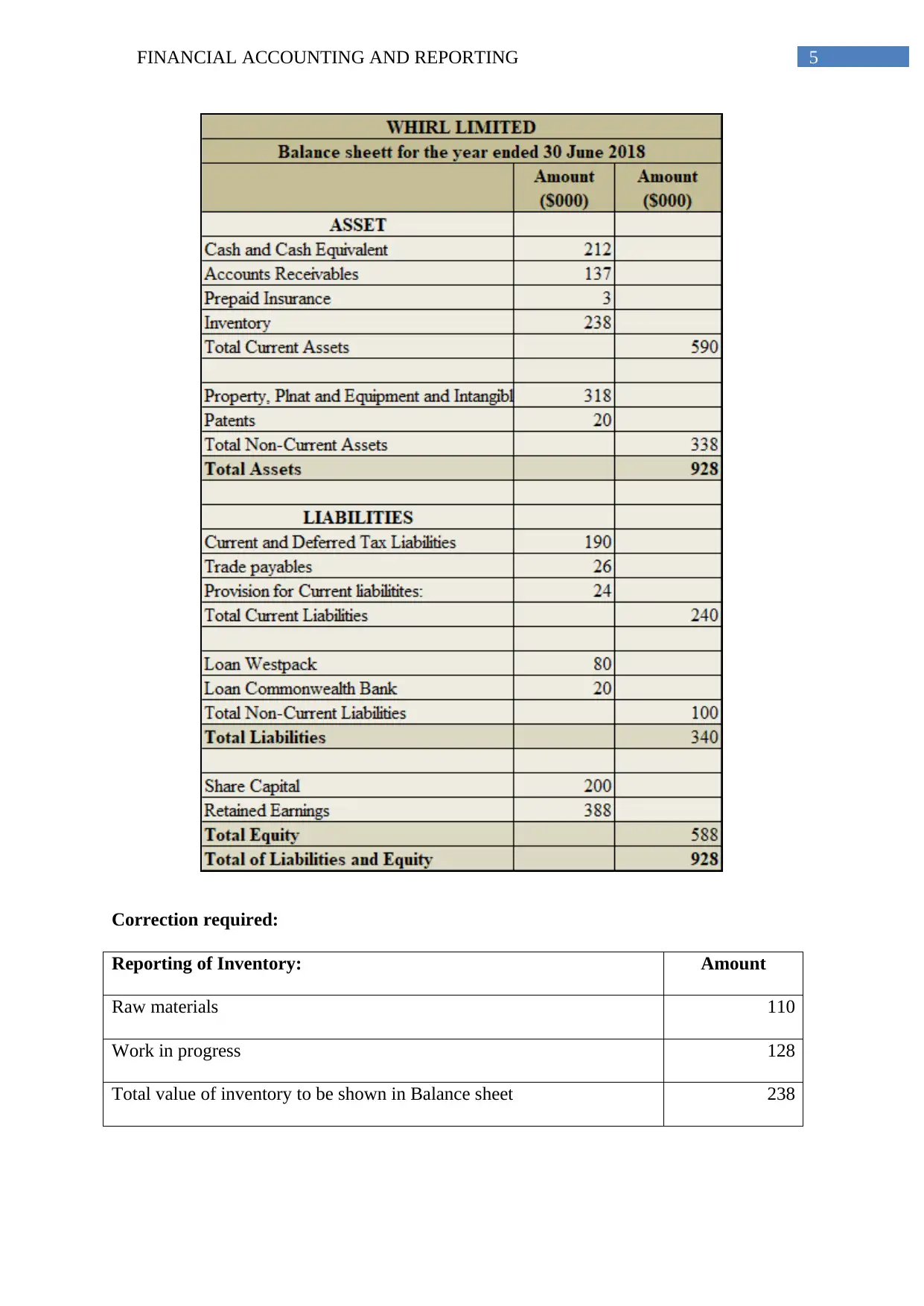

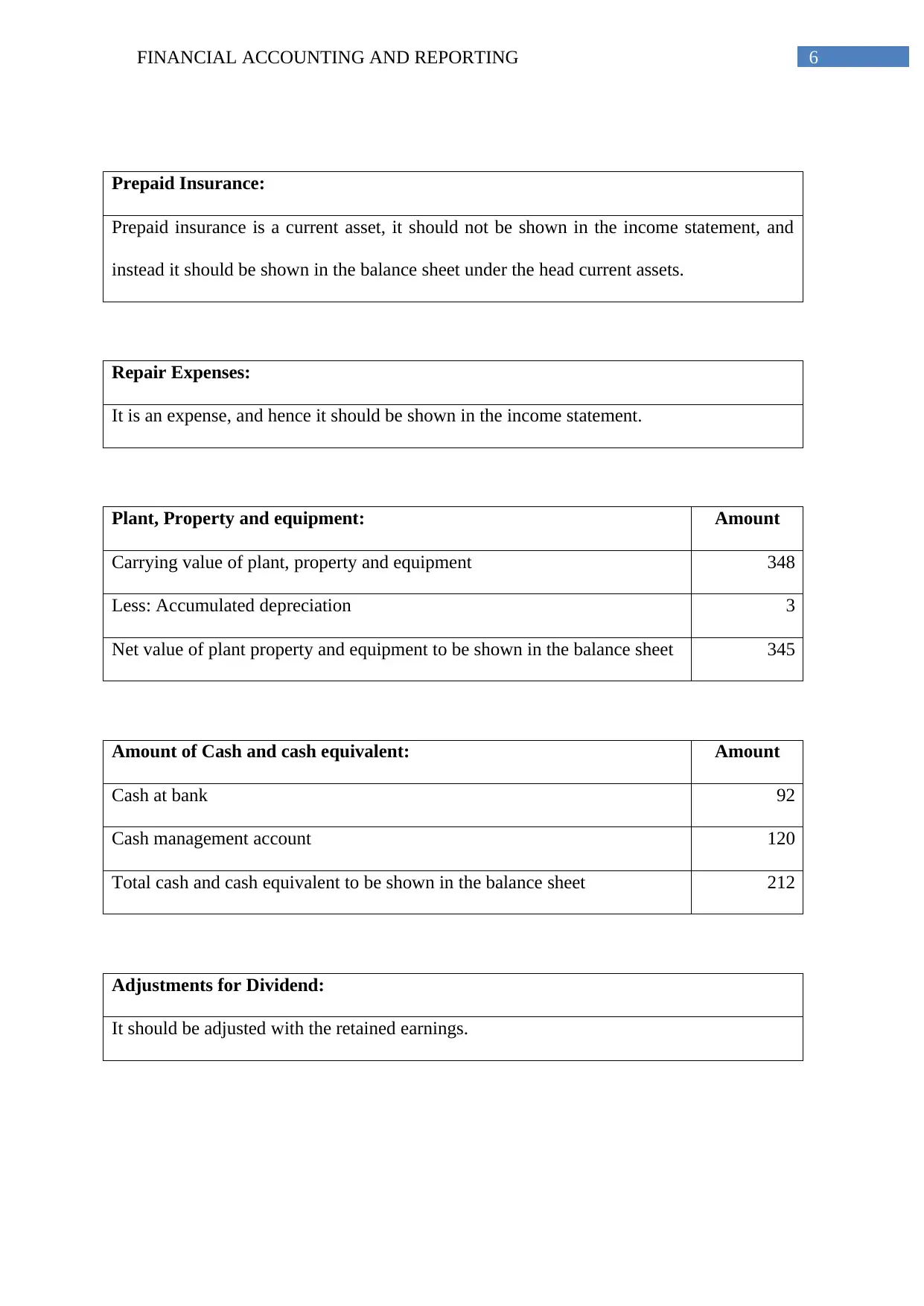

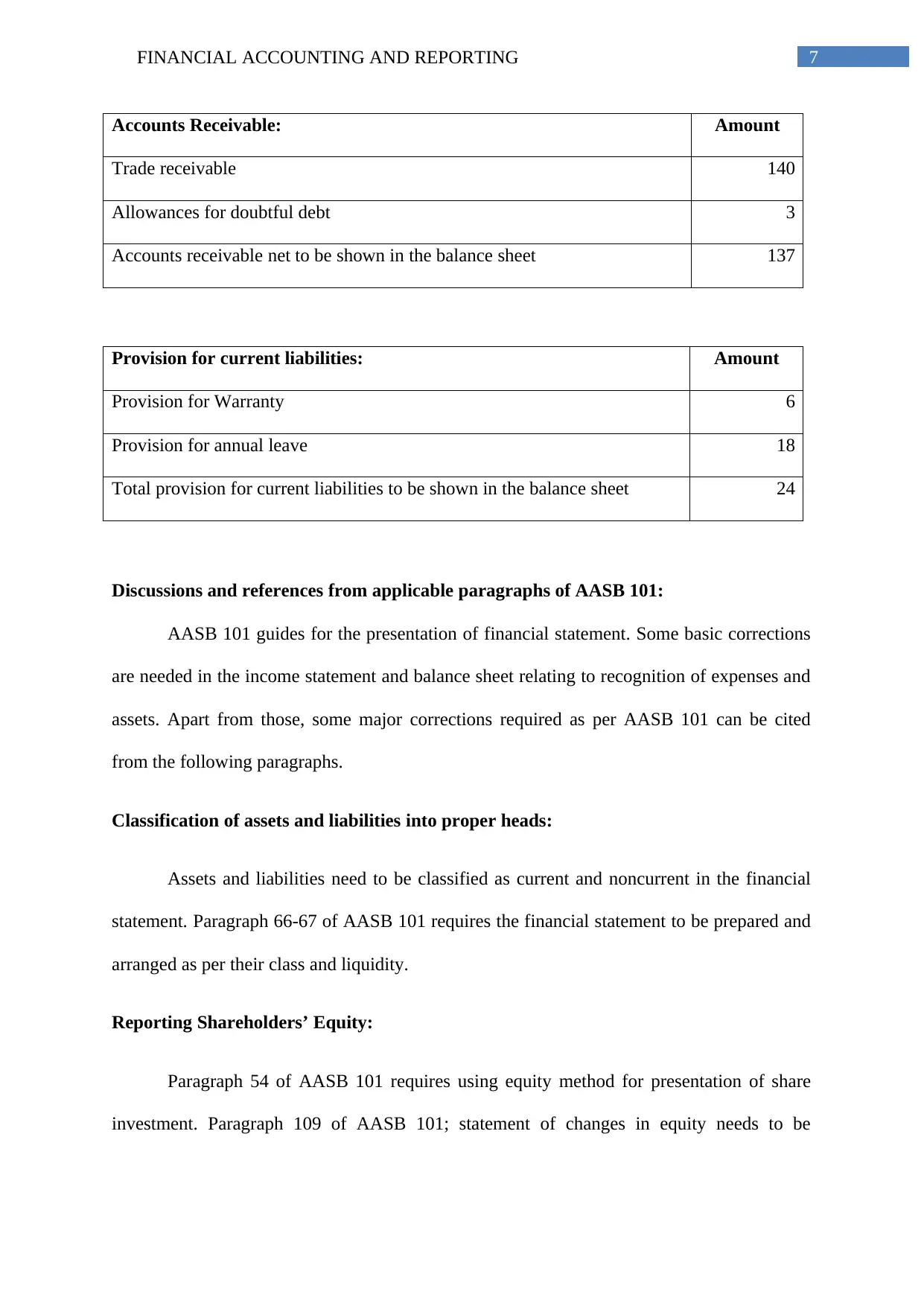

This document discusses the recent changes and developments in the financial reporting environment, including newly amended accounting standards and mandatory compliances. It provides information on the applicability of these changes and their impact on financial reporting. The document also includes corrections required in the reporting of inventory and other financial items.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.