Financial Accounting Assignment: Superstore Ltd Solutions

VerifiedAdded on 2023/06/04

|13

|1208

|248

Homework Assignment

AI Summary

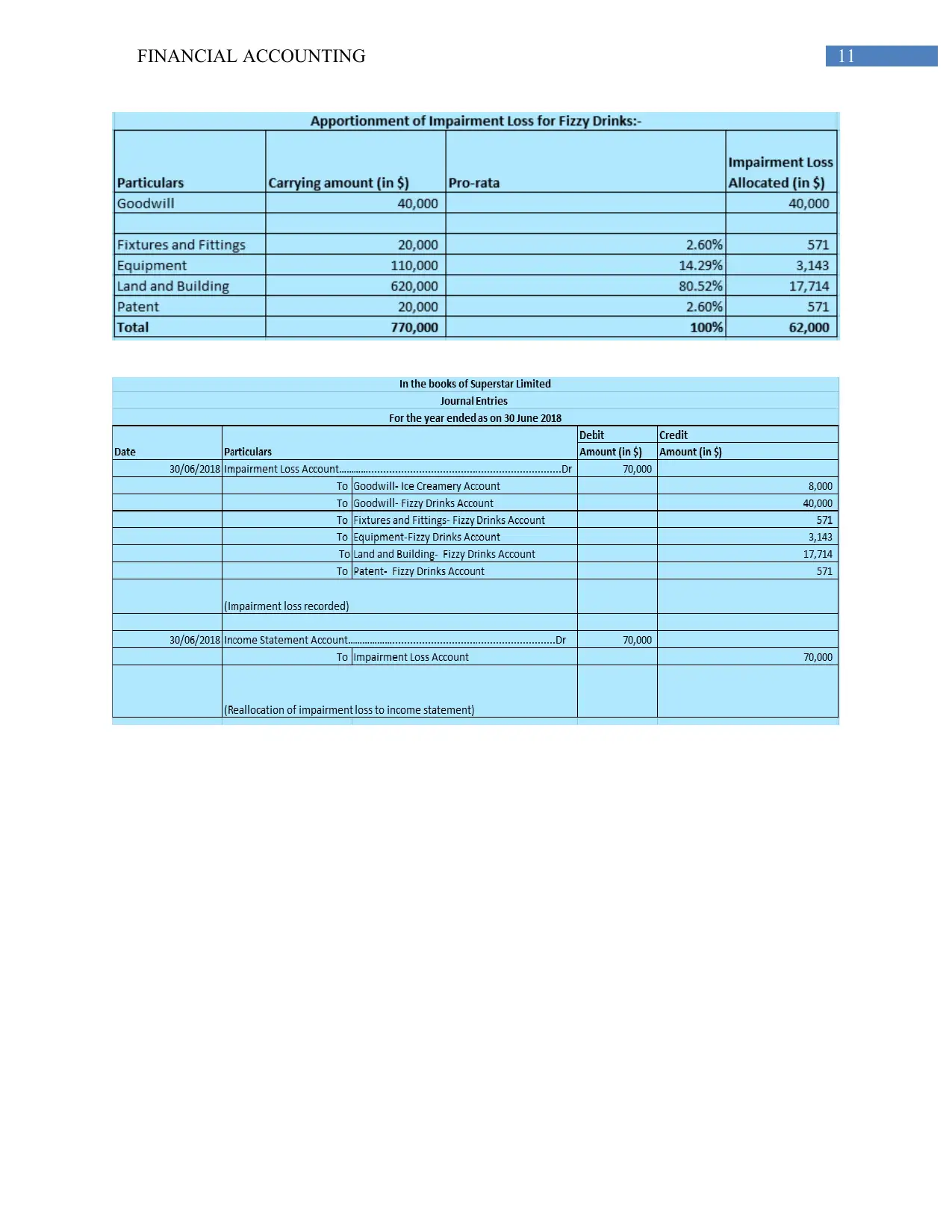

This document presents detailed solutions to a financial accounting assignment involving Superstore Ltd. It addresses various scenarios including changes in asset economic life, accounts payable, investment value declines, and error adjustments, referencing AASB 116 and AASB 110 standards. Journal entries for Rippa Limited's share issuance, allotment, and forfeiture are provided, along with explanations regarding shareholder returns. The document aims to provide comprehensive guidance and solutions for financial accounting problems. Desklib is your go-to resource for more solved assignments and past papers.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.