Financial Accounting Assessment 2

VerifiedAdded on 2023/06/11

|23

|4971

|466

AI Summary

This assessment includes tasks related to petty cash system, batching of transactions, and cash summary calculation sheet. It is for FNSACC301 Process financial transactions and extract interim reports and BSBFIA401 Prepare financial reports units of FNS40615 Certificate IV in Accounting. The due date is in Week 8 and the assessment weighting is 35%.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

T-1.8.1

Details of Assessment

Term and Year T2 2018 Time allowed 6 weeks

Assessment No 2 Assessment Weighting 35%

Assessment Type Project

Due Date Week 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code and Title FNSACC301 Process financial transactions and extract interim reports

BSBFIA401 Prepare financial reports

Details of Student

Student Name

Student ID College

Student Declaration: I declare that the work submitted

is my own, and has not been copied or plagiarised from

any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim

Assessment Outcome

Results Competent Not yet competent Marks / 35

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

__________________________________________

Financial Accounting, Assessment 2, v1.0 Page 1

Details of Assessment

Term and Year T2 2018 Time allowed 6 weeks

Assessment No 2 Assessment Weighting 35%

Assessment Type Project

Due Date Week 8 Room 609

Details of Subject

Qualification FNS40615 Certificate IV in Accounting

Subject Name Financial Accounting

Details of Unit(s) of competency

Unit Code and Title FNSACC301 Process financial transactions and extract interim reports

BSBFIA401 Prepare financial reports

Details of Student

Student Name

Student ID College

Student Declaration: I declare that the work submitted

is my own, and has not been copied or plagiarised from

any person or source.

Signature: ___________________________

Date: _______/________/_______________

Details of Assessor

Assessor’s Name Kaneez Selim

Assessment Outcome

Results Competent Not yet competent Marks / 35

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

_______________________________________________________________________________________

__________________________________________

Financial Accounting, Assessment 2, v1.0 Page 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/__2018_

Purpose of the Assessment FNSACC301

The purpose of this assessment is to assess the student in the following learning elements

and performance criteria of the unit:

Assessment task

1: portfolio of

activities (Task

numbers)

Competent (C) Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents Task 1, 4

Element 2: Prepare and process banking and petty cash documents

2.1 Enter accurately and balance deposits and withdrawals according to

organisational procedures

Task 3

2.3 Reconcile banking documentation with organisation’s financial records Task 3

2.4 Check, process and record petty cash claims and vouchers, and balance petty

cash book according to organisational procedures

Task 1

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

Task 4

4.2 Match batch items precisely to initial receipt records Task 2

4.3 Ensure journals are authorised by appropriate person and process in accordance

with organisational policy and procedures

Task 4

Element 5: Post journals to ledger Task 5

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Task 5

Element 6: Enter data into system Task 1

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

Task 1

6.2 Update related systems to maintain integrity of relationships between financial

systems

Task 4

Element 7: Prepare deposit facility and lodge flows Task 3

7.1 Select deposit facility appropriate to banking method to be used Task 3

Financial Accounting, Assessment 2, v1.0 Page 2

Student Declaration: I declare that I have been assessed

in this unit, and I have been advised of my result. I also

am aware of my appeal rights and reassessment

procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have conducted a

fair, valid, reliable and flexible assessment with this

student, and I have provided appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/__2018_

Purpose of the Assessment FNSACC301

The purpose of this assessment is to assess the student in the following learning elements

and performance criteria of the unit:

Assessment task

1: portfolio of

activities (Task

numbers)

Competent (C) Not yet

competent

(NYC)

Element 1: Check and verify supporting documentation

1.1 Identify, check and record information from documents Task 1, 4

Element 2: Prepare and process banking and petty cash documents

2.1 Enter accurately and balance deposits and withdrawals according to

organisational procedures

Task 3

2.3 Reconcile banking documentation with organisation’s financial records Task 3

2.4 Check, process and record petty cash claims and vouchers, and balance petty

cash book according to organisational procedures

Task 1

Element 4: Prepare and post journals and batch monetary items

4.1 Prepare journals accurately and completely, and batch items within

organisational timelines

Task 4

4.2 Match batch items precisely to initial receipt records Task 2

4.3 Ensure journals are authorised by appropriate person and process in accordance

with organisational policy and procedures

Task 4

Element 5: Post journals to ledger Task 5

5.1 Post journals accurately to ledger in accordance with organisational input

standards, with transactions correctly allocated to system and accounts

Task 5

Element 6: Enter data into system Task 1

6.1 Enter data accurately into system in accordance with organisational input

standards and correctly allocate transactions to system and accounts

Task 1

6.2 Update related systems to maintain integrity of relationships between financial

systems

Task 4

Element 7: Prepare deposit facility and lodge flows Task 3

7.1 Select deposit facility appropriate to banking method to be used Task 3

Financial Accounting, Assessment 2, v1.0 Page 2

T-1.8.1

7.2 Balance batch with deposit facility without error Task 3

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

Task 3

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable Task 3

Element 8: Extract a trial balance and interim reports

8.2 Complete cash and credit journals and post to general ledger Task 4, 5

8.3 Extract and check trial balance and prepare other required reports Task 6

Purpose of the Assessment

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment

from fixed asset transactions in accordance with

organisational policy and procedures

Task 7, 8

1.2 Determine method of calculating depreciation in

accordance with organisational requirements

Task 7, 8

Element 2: [Record general journal entries for balance day adjustments]

2.1 Record depreciation of non-current assets and

disposal of fixed assets in accordance with organisational

policy, procedures and accounting requirements

Task 7, 8, 9

2.2Adjust expense accounts and revenue accounts for

prepayments and accruals

Task 9

2.3. Record bad and doubtful debts in accordance

with organizational policy, procedures and accounting

requirements

2.4. Adjust ledger accounts for inventories, if

required, and transfer to final accounts

Task 7, 8, 9, 10

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day

adjustments in general ledger system in accordance with

organisational policy, procedures and accounting

requirements

Task 9

3.2 Post revenue and expense account balances to final

general ledger accounts system

Task 9, 10

3.3Prepare final general ledger accounts to reflect gross

and net profits for reporting period

Task 9, 10

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with

organisational requirements to reflect operating profit

Task 10

Financial Accounting, Assessment 2, v1.0 Page 3

The purpose of this assessment is to assess the student

in the following learning elements and performance

criteria of the unit :

Assessment task 2:

Assignment (Task

numbers)

Satisfactory

(S)

Not Yet

Satisfactory

(NYC)

7.2 Balance batch with deposit facility without error Task 3

7.3 Take security and safety precautions appropriate to method of banking, in

accordance with organisational policy and industry and legislative requirements

Task 3

7.4 Obtain and file proof of lodgement so that it is easily accessible and traceable Task 3

Element 8: Extract a trial balance and interim reports

8.2 Complete cash and credit journals and post to general ledger Task 4, 5

8.3 Extract and check trial balance and prepare other required reports Task 6

Purpose of the Assessment

Element 1: [Maintain asset register]

1.1 Prepare a register of property, plant and equipment

from fixed asset transactions in accordance with

organisational policy and procedures

Task 7, 8

1.2 Determine method of calculating depreciation in

accordance with organisational requirements

Task 7, 8

Element 2: [Record general journal entries for balance day adjustments]

2.1 Record depreciation of non-current assets and

disposal of fixed assets in accordance with organisational

policy, procedures and accounting requirements

Task 7, 8, 9

2.2Adjust expense accounts and revenue accounts for

prepayments and accruals

Task 9

2.3. Record bad and doubtful debts in accordance

with organizational policy, procedures and accounting

requirements

2.4. Adjust ledger accounts for inventories, if

required, and transfer to final accounts

Task 7, 8, 9, 10

Element 3: [Prepare final general ledger accounts]

3.1 Make general journal entries for balance day

adjustments in general ledger system in accordance with

organisational policy, procedures and accounting

requirements

Task 9

3.2 Post revenue and expense account balances to final

general ledger accounts system

Task 9, 10

3.3Prepare final general ledger accounts to reflect gross

and net profits for reporting period

Task 9, 10

Element 4: [Prepare end of period financial reports]

4.1 Prepare revenue statement in accordance with

organisational requirements to reflect operating profit

Task 10

Financial Accounting, Assessment 2, v1.0 Page 3

The purpose of this assessment is to assess the student

in the following learning elements and performance

criteria of the unit :

Assessment task 2:

Assignment (Task

numbers)

Satisfactory

(S)

Not Yet

Satisfactory

(NYC)

T-1.8.1

for reporting period

4.3 Identify and correct, or refer errors for resolution in

accordance with organisational policy and procedures

Task 8

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

Financial Accounting, Assessment 2, v1.0 Page 4

for reporting period

4.3 Identify and correct, or refer errors for resolution in

accordance with organisational policy and procedures

Task 8

Assessment/evidence gathering conditions

Each assessment component is recorded as either Satisfactory (S) or Not Satisfactory (NS). A student can only achieve

competence when all assessment components listed under Purpose of the assessment section are Satisfactory. Your

trainer will give you feedback after the completion of each assessment. A student who is assessed as NS (Not

Satisfactory) is eligible for re-assessment.

Resources required for this Assessment

Upon completion, submit the assessment copy to your trainer along with assessment coversheet.

Refer to the notes on eLearning to answer the tasks

Any additional material will be provided by Trainer, if needed

Instructions for Students

Please read the following instructions carefully

This assessment has to be completed In class At home

The assessment is to be completed according to the instructions given by your assessor.

Feedback on each task will be provided to enable you to determine how your work could be improved. You will

be provided with feedback on your work within two weeks of the assessment due date. All other feedback will be

provided by the end of the term.

Should you not answer the questions correctly, you will be given feedback on the results and your gaps in

knowledge. You will be given another opportunity to demonstrate your knowledge and skills to be deemed

competent for this unit of competency.

If you are not sure about any aspect of this assessment, please ask for clarification from your assessor.

Please refer to the College re-assessment for more information (Student handbook).

Financial Accounting, Assessment 2, v1.0 Page 4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

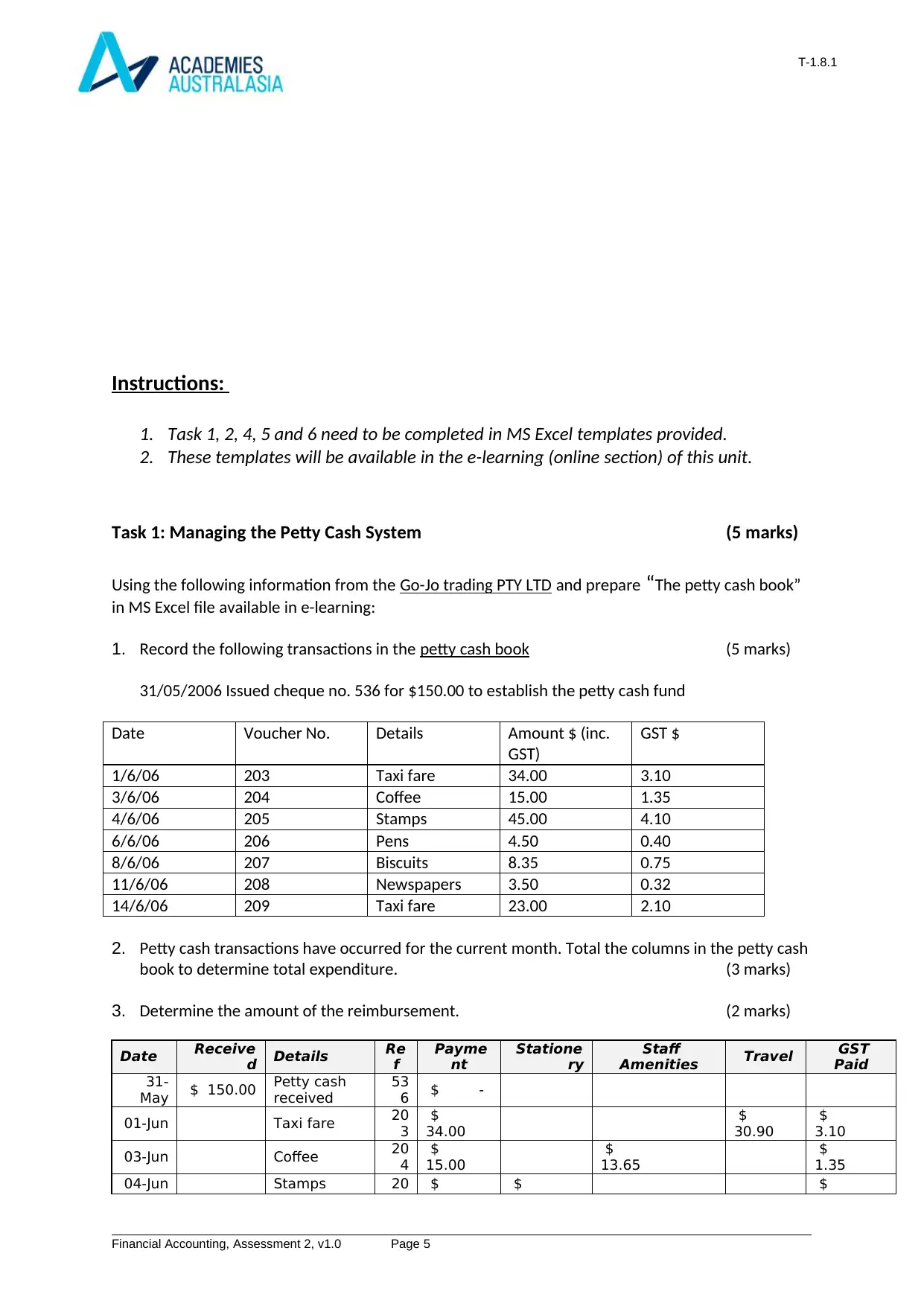

Instructions:

1. Task 1, 2, 4, 5 and 6 need to be completed in MS Excel templates provided.

2. These templates will be available in the e-learning (online section) of this unit.

Task 1: Managing the Petty Cash System (5 marks)

Using the following information from the Go-Jo trading PTY LTD and prepare “The petty cash book”

in MS Excel file available in e-learning:

1. Record the following transactions in the petty cash book (5 marks)

31/05/2006 Issued cheque no. 536 for $150.00 to establish the petty cash fund

Date Voucher No. Details Amount $ (inc.

GST)

GST $

1/6/06 203 Taxi fare 34.00 3.10

3/6/06 204 Coffee 15.00 1.35

4/6/06 205 Stamps 45.00 4.10

6/6/06 206 Pens 4.50 0.40

8/6/06 207 Biscuits 8.35 0.75

11/6/06 208 Newspapers 3.50 0.32

14/6/06 209 Taxi fare 23.00 2.10

2. Petty cash transactions have occurred for the current month. Total the columns in the petty cash

book to determine total expenditure. (3 marks)

3. Determine the amount of the reimbursement. (2 marks)

Date Receive

d Details Re

f

Payme

nt

Statione

ry

Staff

Amenities Travel GST

Paid

31-

May $ 150.00 Petty cash

received

53

6 $ -

01-Jun Taxi fare 20

3

$

34.00

$

30.90

$

3.10

03-Jun Coffee 20

4

$

15.00

$

13.65

$

1.35

04-Jun Stamps 20 $ $ $

Financial Accounting, Assessment 2, v1.0 Page 5

Instructions:

1. Task 1, 2, 4, 5 and 6 need to be completed in MS Excel templates provided.

2. These templates will be available in the e-learning (online section) of this unit.

Task 1: Managing the Petty Cash System (5 marks)

Using the following information from the Go-Jo trading PTY LTD and prepare “The petty cash book”

in MS Excel file available in e-learning:

1. Record the following transactions in the petty cash book (5 marks)

31/05/2006 Issued cheque no. 536 for $150.00 to establish the petty cash fund

Date Voucher No. Details Amount $ (inc.

GST)

GST $

1/6/06 203 Taxi fare 34.00 3.10

3/6/06 204 Coffee 15.00 1.35

4/6/06 205 Stamps 45.00 4.10

6/6/06 206 Pens 4.50 0.40

8/6/06 207 Biscuits 8.35 0.75

11/6/06 208 Newspapers 3.50 0.32

14/6/06 209 Taxi fare 23.00 2.10

2. Petty cash transactions have occurred for the current month. Total the columns in the petty cash

book to determine total expenditure. (3 marks)

3. Determine the amount of the reimbursement. (2 marks)

Date Receive

d Details Re

f

Payme

nt

Statione

ry

Staff

Amenities Travel GST

Paid

31-

May $ 150.00 Petty cash

received

53

6 $ -

01-Jun Taxi fare 20

3

$

34.00

$

30.90

$

3.10

03-Jun Coffee 20

4

$

15.00

$

13.65

$

1.35

04-Jun Stamps 20 $ $ $

Financial Accounting, Assessment 2, v1.0 Page 5

T-1.8.1

5 45.00 40.90 4.10

06-Jun Pens 20

6

$

4.50

$

4.10

$

0.40

08-Jun Biscuits 20

7

$

8.35

$

7.60

$

0.75

11-Jun Newspapers 20

8

$

3.50

$

3.18

$

0.32

14-Jun Taxi fare 20

9

$

23.00

$

20.90

$

2.10

$

133.35

$

45.00

$

24.43

$

51.80

$

12.12

Balance c/d $

16.65

$

150.00 Total $

150.00

30-Jun $ 16.65 Balance b/d

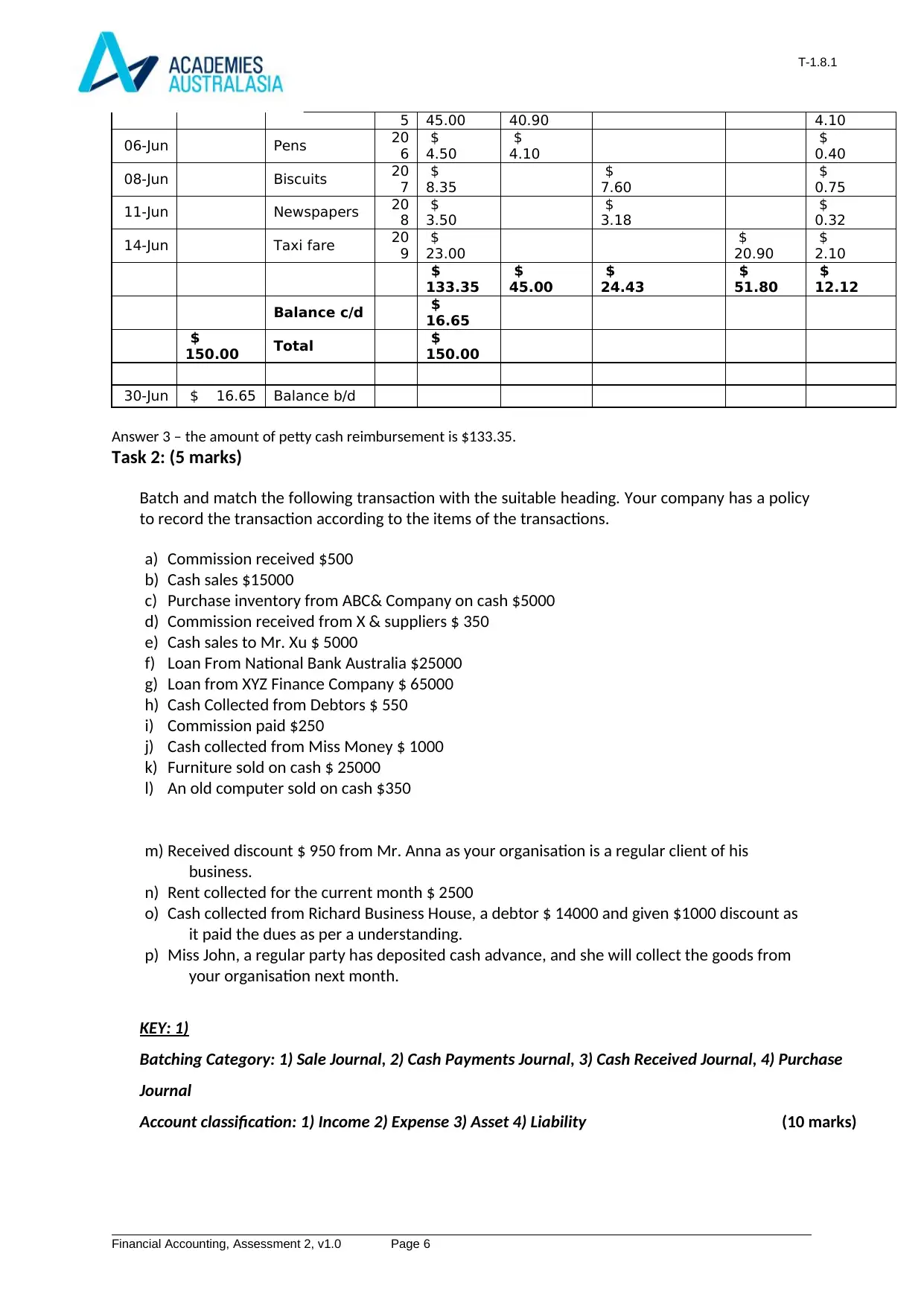

Answer 3 – the amount of petty cash reimbursement is $133.35.

Task 2: (5 marks)

Batch and match the following transaction with the suitable heading. Your company has a policy

to record the transaction according to the items of the transactions.

a) Commission received $500

b) Cash sales $15000

c) Purchase inventory from ABC& Company on cash $5000

d) Commission received from X & suppliers $ 350

e) Cash sales to Mr. Xu $ 5000

f) Loan From National Bank Australia $25000

g) Loan from XYZ Finance Company $ 65000

h) Cash Collected from Debtors $ 550

i) Commission paid $250

j) Cash collected from Miss Money $ 1000

k) Furniture sold on cash $ 25000

l) An old computer sold on cash $350

m) Received discount $ 950 from Mr. Anna as your organisation is a regular client of his

business.

n) Rent collected for the current month $ 2500

o) Cash collected from Richard Business House, a debtor $ 14000 and given $1000 discount as

it paid the dues as per a understanding.

p) Miss John, a regular party has deposited cash advance, and she will collect the goods from

your organisation next month.

KEY: 1)

Batching Category: 1) Sale Journal, 2) Cash Payments Journal, 3) Cash Received Journal, 4) Purchase

Journal

Account classification: 1) Income 2) Expense 3) Asset 4) Liability (10 marks)

Financial Accounting, Assessment 2, v1.0 Page 6

5 45.00 40.90 4.10

06-Jun Pens 20

6

$

4.50

$

4.10

$

0.40

08-Jun Biscuits 20

7

$

8.35

$

7.60

$

0.75

11-Jun Newspapers 20

8

$

3.50

$

3.18

$

0.32

14-Jun Taxi fare 20

9

$

23.00

$

20.90

$

2.10

$

133.35

$

45.00

$

24.43

$

51.80

$

12.12

Balance c/d $

16.65

$

150.00 Total $

150.00

30-Jun $ 16.65 Balance b/d

Answer 3 – the amount of petty cash reimbursement is $133.35.

Task 2: (5 marks)

Batch and match the following transaction with the suitable heading. Your company has a policy

to record the transaction according to the items of the transactions.

a) Commission received $500

b) Cash sales $15000

c) Purchase inventory from ABC& Company on cash $5000

d) Commission received from X & suppliers $ 350

e) Cash sales to Mr. Xu $ 5000

f) Loan From National Bank Australia $25000

g) Loan from XYZ Finance Company $ 65000

h) Cash Collected from Debtors $ 550

i) Commission paid $250

j) Cash collected from Miss Money $ 1000

k) Furniture sold on cash $ 25000

l) An old computer sold on cash $350

m) Received discount $ 950 from Mr. Anna as your organisation is a regular client of his

business.

n) Rent collected for the current month $ 2500

o) Cash collected from Richard Business House, a debtor $ 14000 and given $1000 discount as

it paid the dues as per a understanding.

p) Miss John, a regular party has deposited cash advance, and she will collect the goods from

your organisation next month.

KEY: 1)

Batching Category: 1) Sale Journal, 2) Cash Payments Journal, 3) Cash Received Journal, 4) Purchase

Journal

Account classification: 1) Income 2) Expense 3) Asset 4) Liability (10 marks)

Financial Accounting, Assessment 2, v1.0 Page 6

T-1.8.1

Account classification Batching Category

a) Income Cash received Journal

b) Income Sales Journal

c) Assets Purchase Journal

d) Income Cash received Journal

e) Income Sales Journal

f) Liabilities Cash received Journal

g) Liabilities Cash received Journal

h) Assets Cash received Journal

i) Expense Cash payment Journal

j) Assets Cash received Journal

k) Assets Cash received Journal

l) Assets Cash received Journal

m) Income Purchase Journal

n) Income Cash received Journal

o) Assets Cash received Journal

p) Liabilities Cash received Journal

Task 3: (5 marks)

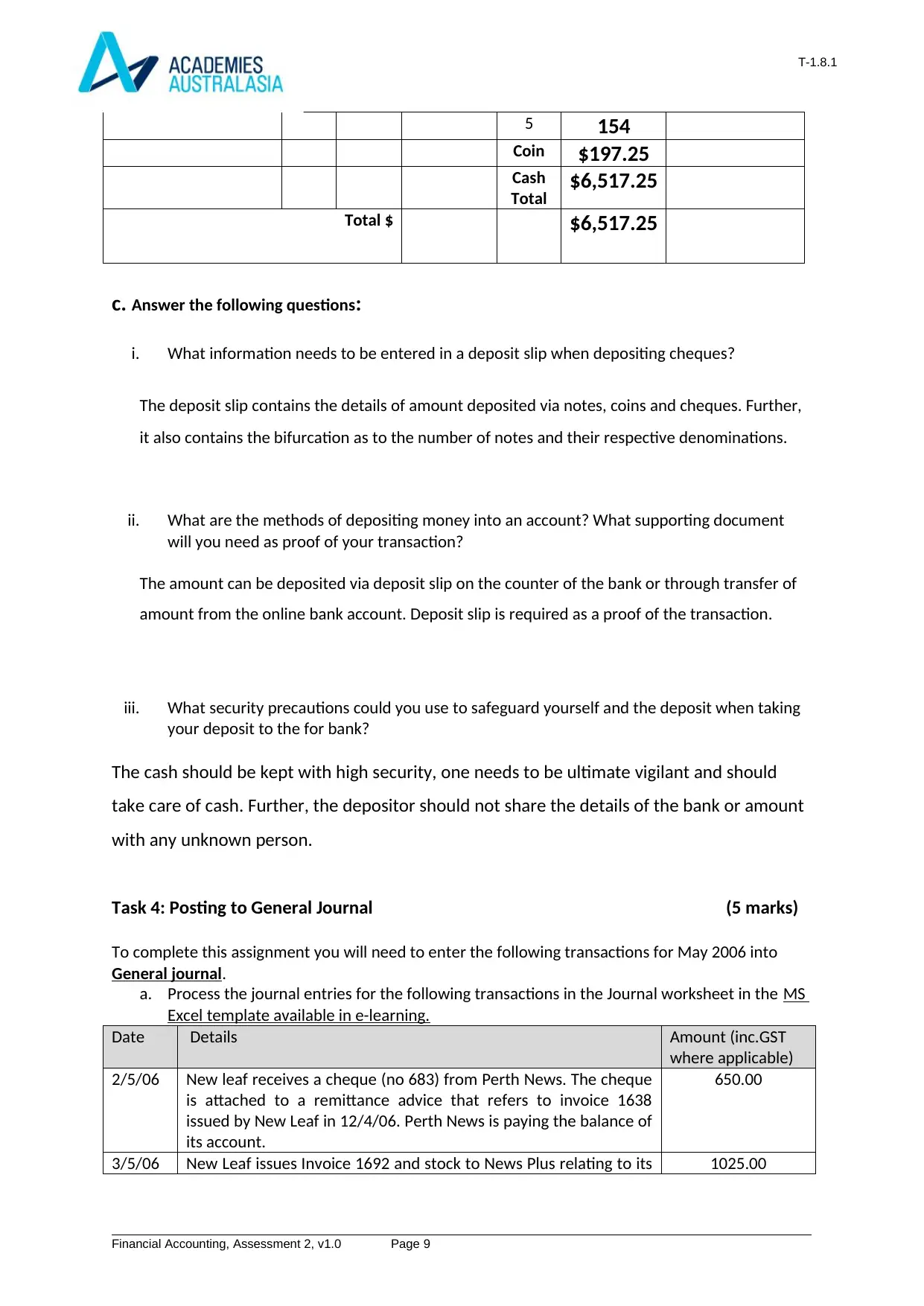

a) Complete the cash Summary calculation sheet of notes, coins and cheques for the daily cash

taking of 22nd of March 2012 (3 marks)

Cash Summary Slip March 22, 2012

Notes Number Value

$100 11 $1,100.00

50 25 $1,250.00

20 112 $2,240.00

10 96 $960.00

5 154 $770.00

Total $6,320.00

Coins

2 32 $64.00

1 52 $52.00

0.50 44 $22.00

0.20 152 $30.40

0.10 256 $25.60

0.05 65 $3.25

Financial Accounting, Assessment 2, v1.0 Page 7

Account classification Batching Category

a) Income Cash received Journal

b) Income Sales Journal

c) Assets Purchase Journal

d) Income Cash received Journal

e) Income Sales Journal

f) Liabilities Cash received Journal

g) Liabilities Cash received Journal

h) Assets Cash received Journal

i) Expense Cash payment Journal

j) Assets Cash received Journal

k) Assets Cash received Journal

l) Assets Cash received Journal

m) Income Purchase Journal

n) Income Cash received Journal

o) Assets Cash received Journal

p) Liabilities Cash received Journal

Task 3: (5 marks)

a) Complete the cash Summary calculation sheet of notes, coins and cheques for the daily cash

taking of 22nd of March 2012 (3 marks)

Cash Summary Slip March 22, 2012

Notes Number Value

$100 11 $1,100.00

50 25 $1,250.00

20 112 $2,240.00

10 96 $960.00

5 154 $770.00

Total $6,320.00

Coins

2 32 $64.00

1 52 $52.00

0.50 44 $22.00

0.20 152 $30.40

0.10 256 $25.60

0.05 65 $3.25

Financial Accounting, Assessment 2, v1.0 Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

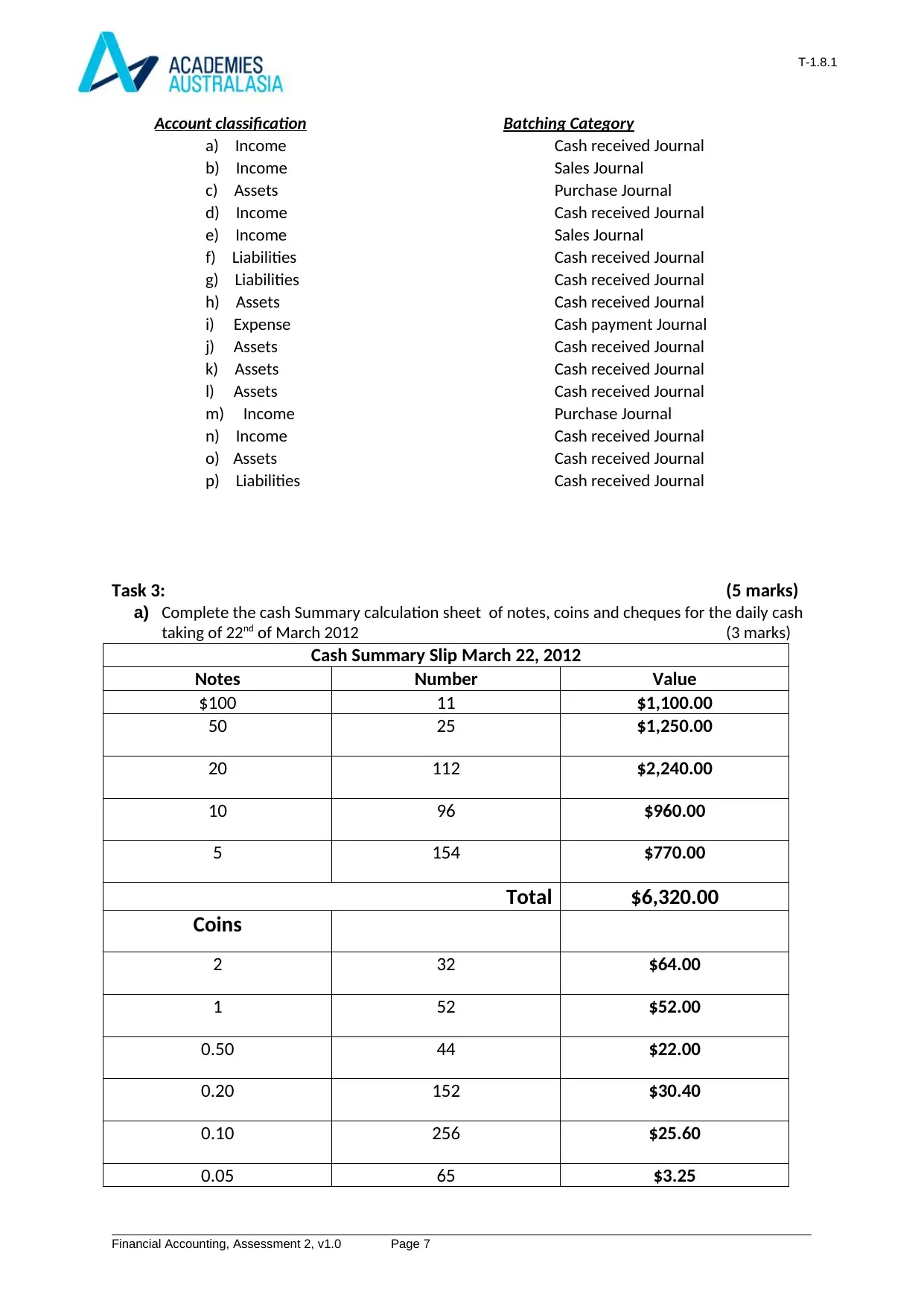

Total $197.25

Total Cash $6,517.25

Cheques received 0

Total 0

Total deposit cash & Cheques $6,517.25

b) Complete both sides of the deposit slip as at 22nd of March 2012 by using the above

information. (3 marks)

Deposit Slip (Front side)

Bank of XYZ Bank of XYZDEPOSIT DATE: 22/03/2012

ABN 78 344 123 456 Branch Name

Date: Broadmeadows

Deposited for credit of For credit of Cash $ 6,517.25

Cash $ 6,517.25 ABC Pty Ltd Cheques 0

Cheques 0 Bankcard/

MasterCard/

Visa/other

0

Bankcard/

MasterCard/

Visa/other

0 Paid by (Signature) Total $ $

6,517.25

Total $ 6,517.25

Teller

Deposit Slip (reverse side)

Bank use only

Third party cheques explanation

Drawer (account name

on cheque)

Bank Branch Amount Bank use only

100 11 Detail of

cheques

50 25

20 112

10 96

Financial Accounting, Assessment 2, v1.0 Page 8

0523 256 78 3456

Total $197.25

Total Cash $6,517.25

Cheques received 0

Total 0

Total deposit cash & Cheques $6,517.25

b) Complete both sides of the deposit slip as at 22nd of March 2012 by using the above

information. (3 marks)

Deposit Slip (Front side)

Bank of XYZ Bank of XYZDEPOSIT DATE: 22/03/2012

ABN 78 344 123 456 Branch Name

Date: Broadmeadows

Deposited for credit of For credit of Cash $ 6,517.25

Cash $ 6,517.25 ABC Pty Ltd Cheques 0

Cheques 0 Bankcard/

MasterCard/

Visa/other

0

Bankcard/

MasterCard/

Visa/other

0 Paid by (Signature) Total $ $

6,517.25

Total $ 6,517.25

Teller

Deposit Slip (reverse side)

Bank use only

Third party cheques explanation

Drawer (account name

on cheque)

Bank Branch Amount Bank use only

100 11 Detail of

cheques

50 25

20 112

10 96

Financial Accounting, Assessment 2, v1.0 Page 8

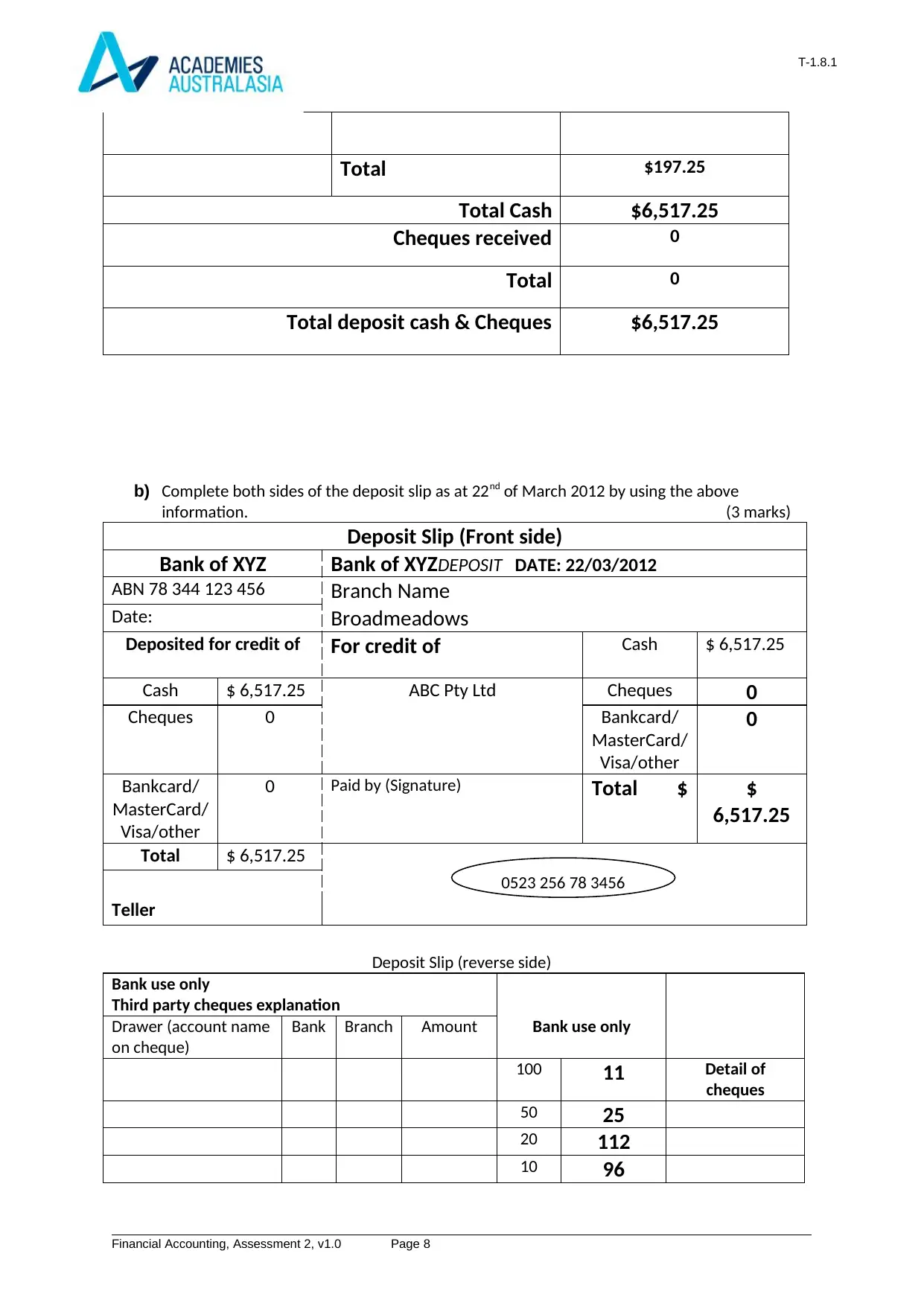

0523 256 78 3456

T-1.8.1

5 154

Coin $197.25

Cash

Total $6,517.25

Total $ $6,517.25

c. Answer the following questions:

i. What information needs to be entered in a deposit slip when depositing cheques?

The deposit slip contains the details of amount deposited via notes, coins and cheques. Further,

it also contains the bifurcation as to the number of notes and their respective denominations.

ii. What are the methods of depositing money into an account? What supporting document

will you need as proof of your transaction?

The amount can be deposited via deposit slip on the counter of the bank or through transfer of

amount from the online bank account. Deposit slip is required as a proof of the transaction.

iii. What security precautions could you use to safeguard yourself and the deposit when taking

your deposit to the for bank?

The cash should be kept with high security, one needs to be ultimate vigilant and should

take care of cash. Further, the depositor should not share the details of the bank or amount

with any unknown person.

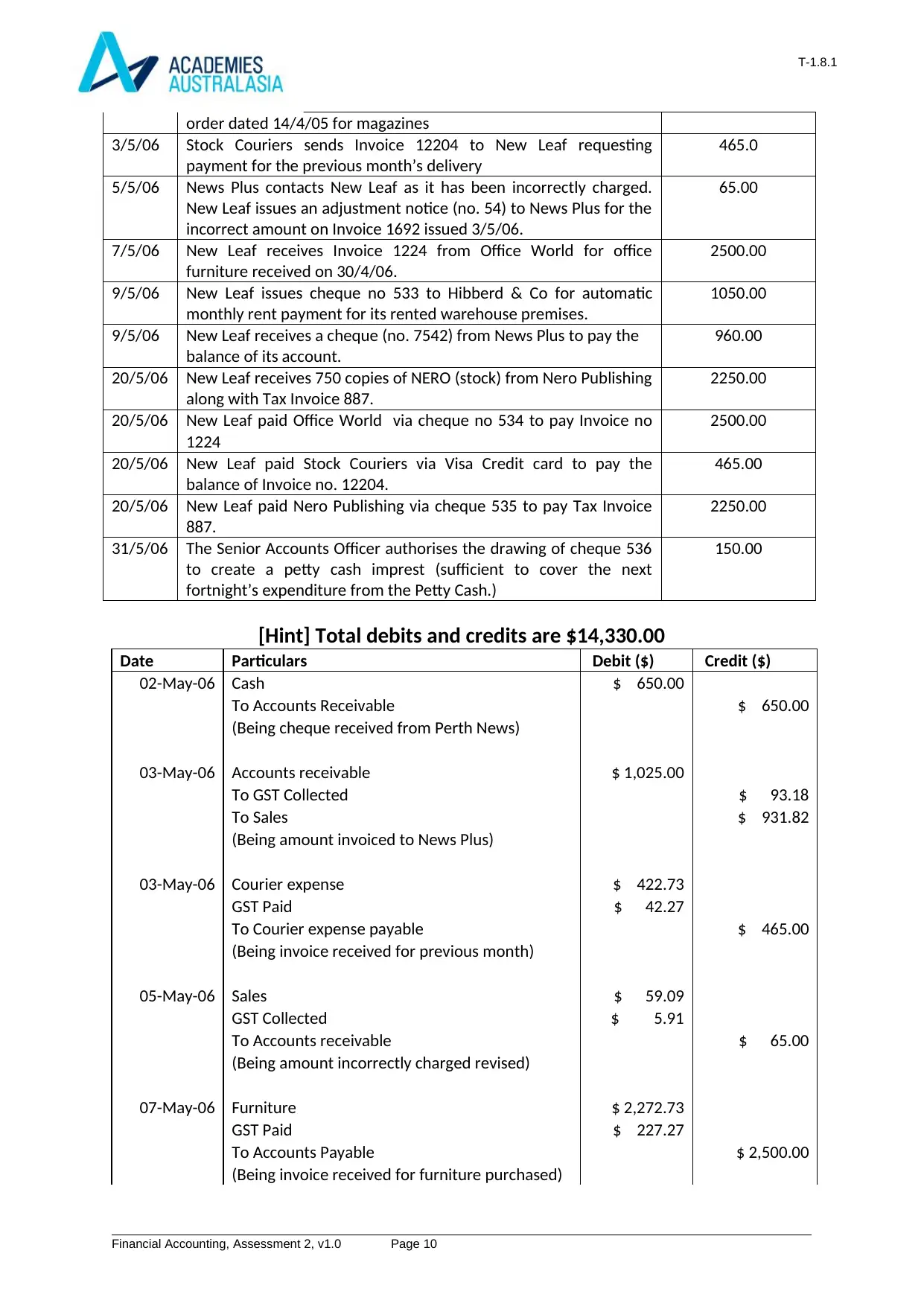

Task 4: Posting to General Journal (5 marks)

To complete this assignment you will need to enter the following transactions for May 2006 into

General journal.

a. Process the journal entries for the following transactions in the Journal worksheet in the MS

Excel template available in e-learning.

Date Details Amount (inc.GST

where applicable)

2/5/06 New leaf receives a cheque (no 683) from Perth News. The cheque

is attached to a remittance advice that refers to invoice 1638

issued by New Leaf in 12/4/06. Perth News is paying the balance of

its account.

650.00

3/5/06 New Leaf issues Invoice 1692 and stock to News Plus relating to its 1025.00

Financial Accounting, Assessment 2, v1.0 Page 9

5 154

Coin $197.25

Cash

Total $6,517.25

Total $ $6,517.25

c. Answer the following questions:

i. What information needs to be entered in a deposit slip when depositing cheques?

The deposit slip contains the details of amount deposited via notes, coins and cheques. Further,

it also contains the bifurcation as to the number of notes and their respective denominations.

ii. What are the methods of depositing money into an account? What supporting document

will you need as proof of your transaction?

The amount can be deposited via deposit slip on the counter of the bank or through transfer of

amount from the online bank account. Deposit slip is required as a proof of the transaction.

iii. What security precautions could you use to safeguard yourself and the deposit when taking

your deposit to the for bank?

The cash should be kept with high security, one needs to be ultimate vigilant and should

take care of cash. Further, the depositor should not share the details of the bank or amount

with any unknown person.

Task 4: Posting to General Journal (5 marks)

To complete this assignment you will need to enter the following transactions for May 2006 into

General journal.

a. Process the journal entries for the following transactions in the Journal worksheet in the MS

Excel template available in e-learning.

Date Details Amount (inc.GST

where applicable)

2/5/06 New leaf receives a cheque (no 683) from Perth News. The cheque

is attached to a remittance advice that refers to invoice 1638

issued by New Leaf in 12/4/06. Perth News is paying the balance of

its account.

650.00

3/5/06 New Leaf issues Invoice 1692 and stock to News Plus relating to its 1025.00

Financial Accounting, Assessment 2, v1.0 Page 9

T-1.8.1

order dated 14/4/05 for magazines

3/5/06 Stock Couriers sends Invoice 12204 to New Leaf requesting

payment for the previous month’s delivery

465.0

5/5/06 News Plus contacts New Leaf as it has been incorrectly charged.

New Leaf issues an adjustment notice (no. 54) to News Plus for the

incorrect amount on Invoice 1692 issued 3/5/06.

65.00

7/5/06 New Leaf receives Invoice 1224 from Office World for office

furniture received on 30/4/06.

2500.00

9/5/06 New Leaf issues cheque no 533 to Hibberd & Co for automatic

monthly rent payment for its rented warehouse premises.

1050.00

9/5/06 New Leaf receives a cheque (no. 7542) from News Plus to pay the

balance of its account.

960.00

20/5/06 New Leaf receives 750 copies of NERO (stock) from Nero Publishing

along with Tax Invoice 887.

2250.00

20/5/06 New Leaf paid Office World via cheque no 534 to pay Invoice no

1224

2500.00

20/5/06 New Leaf paid Stock Couriers via Visa Credit card to pay the

balance of Invoice no. 12204.

465.00

20/5/06 New Leaf paid Nero Publishing via cheque 535 to pay Tax Invoice

887.

2250.00

31/5/06 The Senior Accounts Officer authorises the drawing of cheque 536

to create a petty cash imprest (sufficient to cover the next

fortnight’s expenditure from the Petty Cash.)

150.00

[Hint] Total debits and credits are $14,330.00

Date Particulars Debit ($) Credit ($)

02-May-06 Cash $ 650.00

To Accounts Receivable $ 650.00

(Being cheque received from Perth News)

03-May-06 Accounts receivable $ 1,025.00

To GST Collected $ 93.18

To Sales $ 931.82

(Being amount invoiced to News Plus)

03-May-06 Courier expense $ 422.73

GST Paid $ 42.27

To Courier expense payable $ 465.00

(Being invoice received for previous month)

05-May-06 Sales $ 59.09

GST Collected $ 5.91

To Accounts receivable $ 65.00

(Being amount incorrectly charged revised)

07-May-06 Furniture $ 2,272.73

GST Paid $ 227.27

To Accounts Payable $ 2,500.00

(Being invoice received for furniture purchased)

Financial Accounting, Assessment 2, v1.0 Page 10

order dated 14/4/05 for magazines

3/5/06 Stock Couriers sends Invoice 12204 to New Leaf requesting

payment for the previous month’s delivery

465.0

5/5/06 News Plus contacts New Leaf as it has been incorrectly charged.

New Leaf issues an adjustment notice (no. 54) to News Plus for the

incorrect amount on Invoice 1692 issued 3/5/06.

65.00

7/5/06 New Leaf receives Invoice 1224 from Office World for office

furniture received on 30/4/06.

2500.00

9/5/06 New Leaf issues cheque no 533 to Hibberd & Co for automatic

monthly rent payment for its rented warehouse premises.

1050.00

9/5/06 New Leaf receives a cheque (no. 7542) from News Plus to pay the

balance of its account.

960.00

20/5/06 New Leaf receives 750 copies of NERO (stock) from Nero Publishing

along with Tax Invoice 887.

2250.00

20/5/06 New Leaf paid Office World via cheque no 534 to pay Invoice no

1224

2500.00

20/5/06 New Leaf paid Stock Couriers via Visa Credit card to pay the

balance of Invoice no. 12204.

465.00

20/5/06 New Leaf paid Nero Publishing via cheque 535 to pay Tax Invoice

887.

2250.00

31/5/06 The Senior Accounts Officer authorises the drawing of cheque 536

to create a petty cash imprest (sufficient to cover the next

fortnight’s expenditure from the Petty Cash.)

150.00

[Hint] Total debits and credits are $14,330.00

Date Particulars Debit ($) Credit ($)

02-May-06 Cash $ 650.00

To Accounts Receivable $ 650.00

(Being cheque received from Perth News)

03-May-06 Accounts receivable $ 1,025.00

To GST Collected $ 93.18

To Sales $ 931.82

(Being amount invoiced to News Plus)

03-May-06 Courier expense $ 422.73

GST Paid $ 42.27

To Courier expense payable $ 465.00

(Being invoice received for previous month)

05-May-06 Sales $ 59.09

GST Collected $ 5.91

To Accounts receivable $ 65.00

(Being amount incorrectly charged revised)

07-May-06 Furniture $ 2,272.73

GST Paid $ 227.27

To Accounts Payable $ 2,500.00

(Being invoice received for furniture purchased)

Financial Accounting, Assessment 2, v1.0 Page 10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

09-May-06 Accounts receivable $ 1,050.00

To GST Collected $ 95.45

To Rent Income $ 954.55

(Being invoice raised for warehouse rent

payment)

09-May-06 Cash $ 960.00

To Accounts receivable $ 960.00

(Being amount received from News Plus)

20-May-06 Inventory $ 2,045.45

GST Paid $ 204.55

To Accounts Payable $ 2,250.00

(Being stock purchased on credit)

20-May-06 Accounts Payable $ 2,500.00

To Cash $ 2,500.00

(Being amount paid for office furniture)

20-May-06 Courier expense payable $ 465.00

To Cash $ 465.00

(Being amount paid for courier services)

20-May-06 Accounts Payable $ 2,250.00

To Cash $ 2,250.00

(Being amount paid for stock)

31-May-06 Petty Cash $ 150.00

To Cash $ 150.00

(Being petty cash reimbursed)

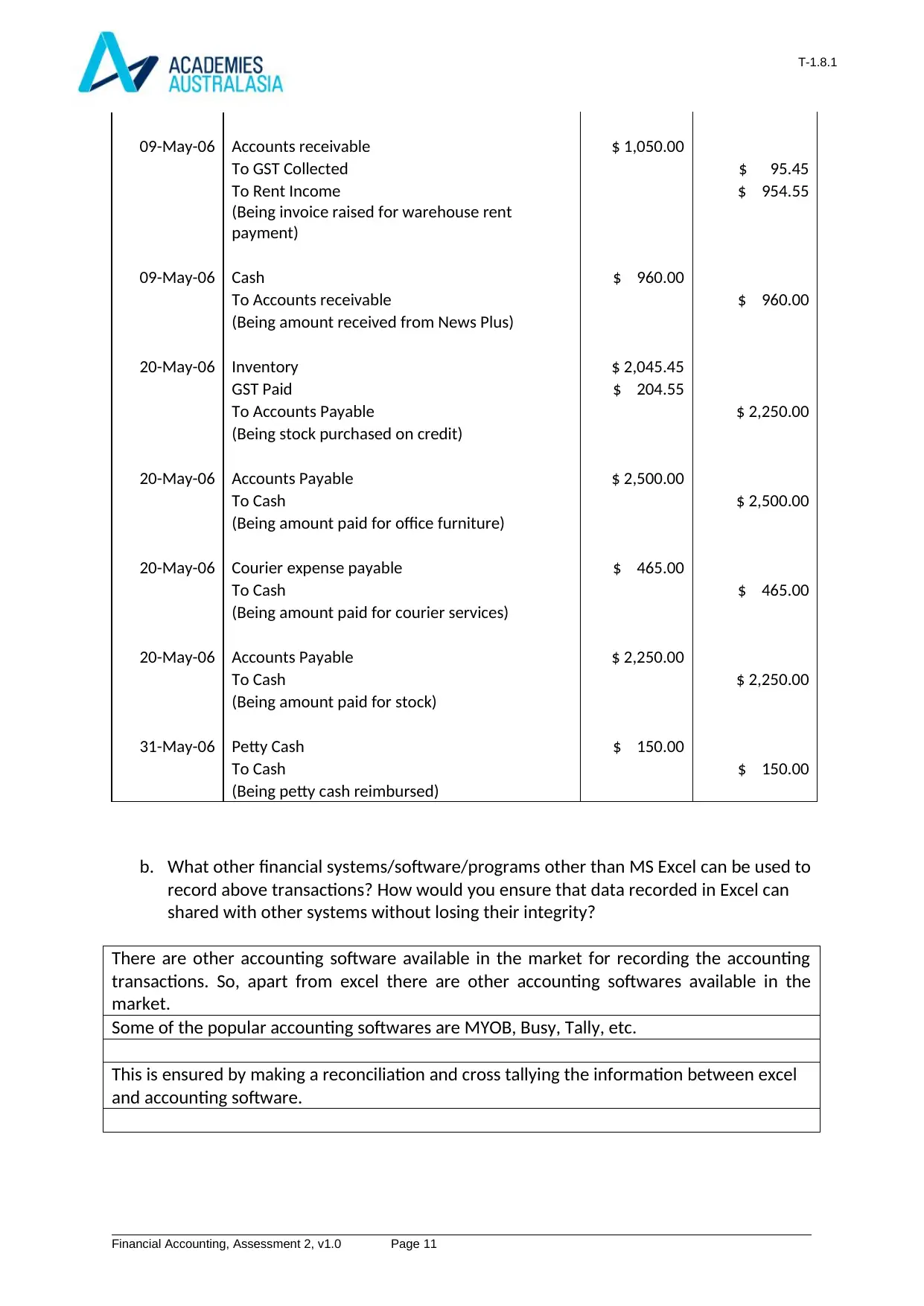

b. What other financial systems/software/programs other than MS Excel can be used to

record above transactions? How would you ensure that data recorded in Excel can

shared with other systems without losing their integrity?

There are other accounting software available in the market for recording the accounting

transactions. So, apart from excel there are other accounting softwares available in the

market.

Some of the popular accounting softwares are MYOB, Busy, Tally, etc.

This is ensured by making a reconciliation and cross tallying the information between excel

and accounting software.

Financial Accounting, Assessment 2, v1.0 Page 11

09-May-06 Accounts receivable $ 1,050.00

To GST Collected $ 95.45

To Rent Income $ 954.55

(Being invoice raised for warehouse rent

payment)

09-May-06 Cash $ 960.00

To Accounts receivable $ 960.00

(Being amount received from News Plus)

20-May-06 Inventory $ 2,045.45

GST Paid $ 204.55

To Accounts Payable $ 2,250.00

(Being stock purchased on credit)

20-May-06 Accounts Payable $ 2,500.00

To Cash $ 2,500.00

(Being amount paid for office furniture)

20-May-06 Courier expense payable $ 465.00

To Cash $ 465.00

(Being amount paid for courier services)

20-May-06 Accounts Payable $ 2,250.00

To Cash $ 2,250.00

(Being amount paid for stock)

31-May-06 Petty Cash $ 150.00

To Cash $ 150.00

(Being petty cash reimbursed)

b. What other financial systems/software/programs other than MS Excel can be used to

record above transactions? How would you ensure that data recorded in Excel can

shared with other systems without losing their integrity?

There are other accounting software available in the market for recording the accounting

transactions. So, apart from excel there are other accounting softwares available in the

market.

Some of the popular accounting softwares are MYOB, Busy, Tally, etc.

This is ensured by making a reconciliation and cross tallying the information between excel

and accounting software.

Financial Accounting, Assessment 2, v1.0 Page 11

T-1.8.1

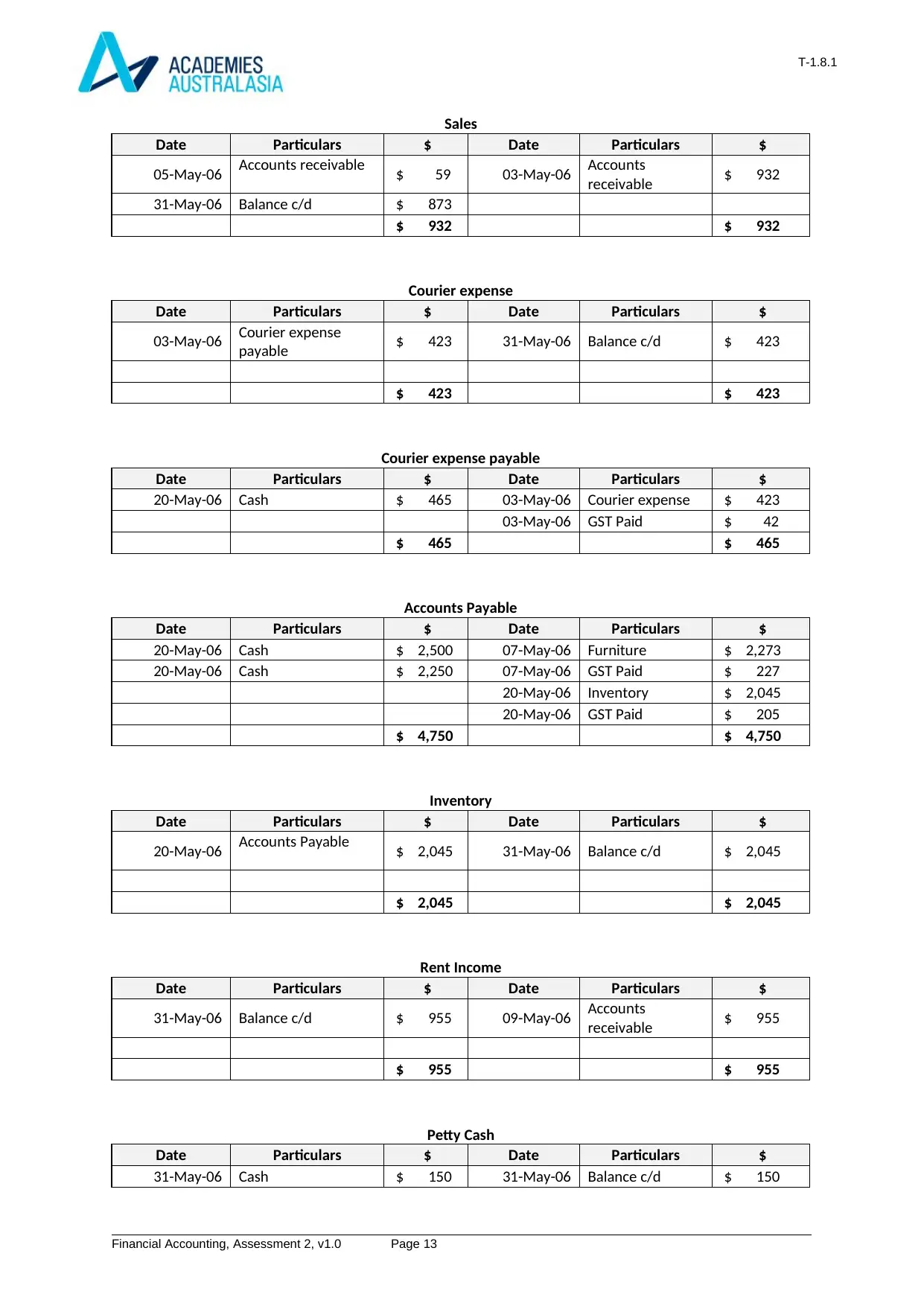

Task 5 Posting to the General Ledger

(5 marks)

At the end of each month, you are required to post the journal entries to the general ledger.

Complete the following tasks:

1. Post the journal entries to the general ledger accounts in the Ledger worksheet @ 31/05/06.

2. Total each of the account balances in the General ledger?

Cash

Date Particulars $ Date Particulars $

02-May-06 Accounts Receivable $ 650 20-May-06 Accounts Payable $ 2,500

09-May-06 Accounts Receivable $ 960 20-May-06 Courier expense

payable $ 465

31-May-06 Balance c/d $ 3,755 20-May-06 Accounts Payable $ 2,250

31-May-06 Petty Cash $ 150

$ 5,365 $ 5,365

Accounts Receivable

Date Particulars $ Date Particulars $

03-May-06 GST Collected $ 93 02-May-06 Cash $ 650

03-May-06 Sales $ 932 05-May-06 Sales $ 59

09-May-06 GST Collected $ 95 05-May-06 GST Collected $ 6

09-May-06 Rent Income $ 955 09-May-06 Cash $ 960

31-May-06 Balance c/d $ 400

$ 2,075 $ 2,075

GST Collected

Date Particulars $ Date Particulars $

05-May-06 Accounts receivable $ 6 03-May-06 Accounts

receivable $ 93

31-May-06 Balance c/d $ 183 09-May-06 Accounts

receivable $ 95

$ 189 $ 189

GST Paid

Date Particulars $ Date Particulars $

03-May-06 Courier expense

payable $ 42 31-May-06 Balance c/d $ 474

07-May-06 Accounts payable $ 227

20-May-06 Accounts payable $ 205

$ 474 $ 474

Financial Accounting, Assessment 2, v1.0 Page 12

Task 5 Posting to the General Ledger

(5 marks)

At the end of each month, you are required to post the journal entries to the general ledger.

Complete the following tasks:

1. Post the journal entries to the general ledger accounts in the Ledger worksheet @ 31/05/06.

2. Total each of the account balances in the General ledger?

Cash

Date Particulars $ Date Particulars $

02-May-06 Accounts Receivable $ 650 20-May-06 Accounts Payable $ 2,500

09-May-06 Accounts Receivable $ 960 20-May-06 Courier expense

payable $ 465

31-May-06 Balance c/d $ 3,755 20-May-06 Accounts Payable $ 2,250

31-May-06 Petty Cash $ 150

$ 5,365 $ 5,365

Accounts Receivable

Date Particulars $ Date Particulars $

03-May-06 GST Collected $ 93 02-May-06 Cash $ 650

03-May-06 Sales $ 932 05-May-06 Sales $ 59

09-May-06 GST Collected $ 95 05-May-06 GST Collected $ 6

09-May-06 Rent Income $ 955 09-May-06 Cash $ 960

31-May-06 Balance c/d $ 400

$ 2,075 $ 2,075

GST Collected

Date Particulars $ Date Particulars $

05-May-06 Accounts receivable $ 6 03-May-06 Accounts

receivable $ 93

31-May-06 Balance c/d $ 183 09-May-06 Accounts

receivable $ 95

$ 189 $ 189

GST Paid

Date Particulars $ Date Particulars $

03-May-06 Courier expense

payable $ 42 31-May-06 Balance c/d $ 474

07-May-06 Accounts payable $ 227

20-May-06 Accounts payable $ 205

$ 474 $ 474

Financial Accounting, Assessment 2, v1.0 Page 12

T-1.8.1

Sales

Date Particulars $ Date Particulars $

05-May-06 Accounts receivable $ 59 03-May-06 Accounts

receivable $ 932

31-May-06 Balance c/d $ 873

$ 932 $ 932

Courier expense

Date Particulars $ Date Particulars $

03-May-06 Courier expense

payable $ 423 31-May-06 Balance c/d $ 423

$ 423 $ 423

Courier expense payable

Date Particulars $ Date Particulars $

20-May-06 Cash $ 465 03-May-06 Courier expense $ 423

03-May-06 GST Paid $ 42

$ 465 $ 465

Accounts Payable

Date Particulars $ Date Particulars $

20-May-06 Cash $ 2,500 07-May-06 Furniture $ 2,273

20-May-06 Cash $ 2,250 07-May-06 GST Paid $ 227

20-May-06 Inventory $ 2,045

20-May-06 GST Paid $ 205

$ 4,750 $ 4,750

Inventory

Date Particulars $ Date Particulars $

20-May-06 Accounts Payable $ 2,045 31-May-06 Balance c/d $ 2,045

$ 2,045 $ 2,045

Rent Income

Date Particulars $ Date Particulars $

31-May-06 Balance c/d $ 955 09-May-06 Accounts

receivable $ 955

$ 955 $ 955

Petty Cash

Date Particulars $ Date Particulars $

31-May-06 Cash $ 150 31-May-06 Balance c/d $ 150

Financial Accounting, Assessment 2, v1.0 Page 13

Sales

Date Particulars $ Date Particulars $

05-May-06 Accounts receivable $ 59 03-May-06 Accounts

receivable $ 932

31-May-06 Balance c/d $ 873

$ 932 $ 932

Courier expense

Date Particulars $ Date Particulars $

03-May-06 Courier expense

payable $ 423 31-May-06 Balance c/d $ 423

$ 423 $ 423

Courier expense payable

Date Particulars $ Date Particulars $

20-May-06 Cash $ 465 03-May-06 Courier expense $ 423

03-May-06 GST Paid $ 42

$ 465 $ 465

Accounts Payable

Date Particulars $ Date Particulars $

20-May-06 Cash $ 2,500 07-May-06 Furniture $ 2,273

20-May-06 Cash $ 2,250 07-May-06 GST Paid $ 227

20-May-06 Inventory $ 2,045

20-May-06 GST Paid $ 205

$ 4,750 $ 4,750

Inventory

Date Particulars $ Date Particulars $

20-May-06 Accounts Payable $ 2,045 31-May-06 Balance c/d $ 2,045

$ 2,045 $ 2,045

Rent Income

Date Particulars $ Date Particulars $

31-May-06 Balance c/d $ 955 09-May-06 Accounts

receivable $ 955

$ 955 $ 955

Petty Cash

Date Particulars $ Date Particulars $

31-May-06 Cash $ 150 31-May-06 Balance c/d $ 150

Financial Accounting, Assessment 2, v1.0 Page 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

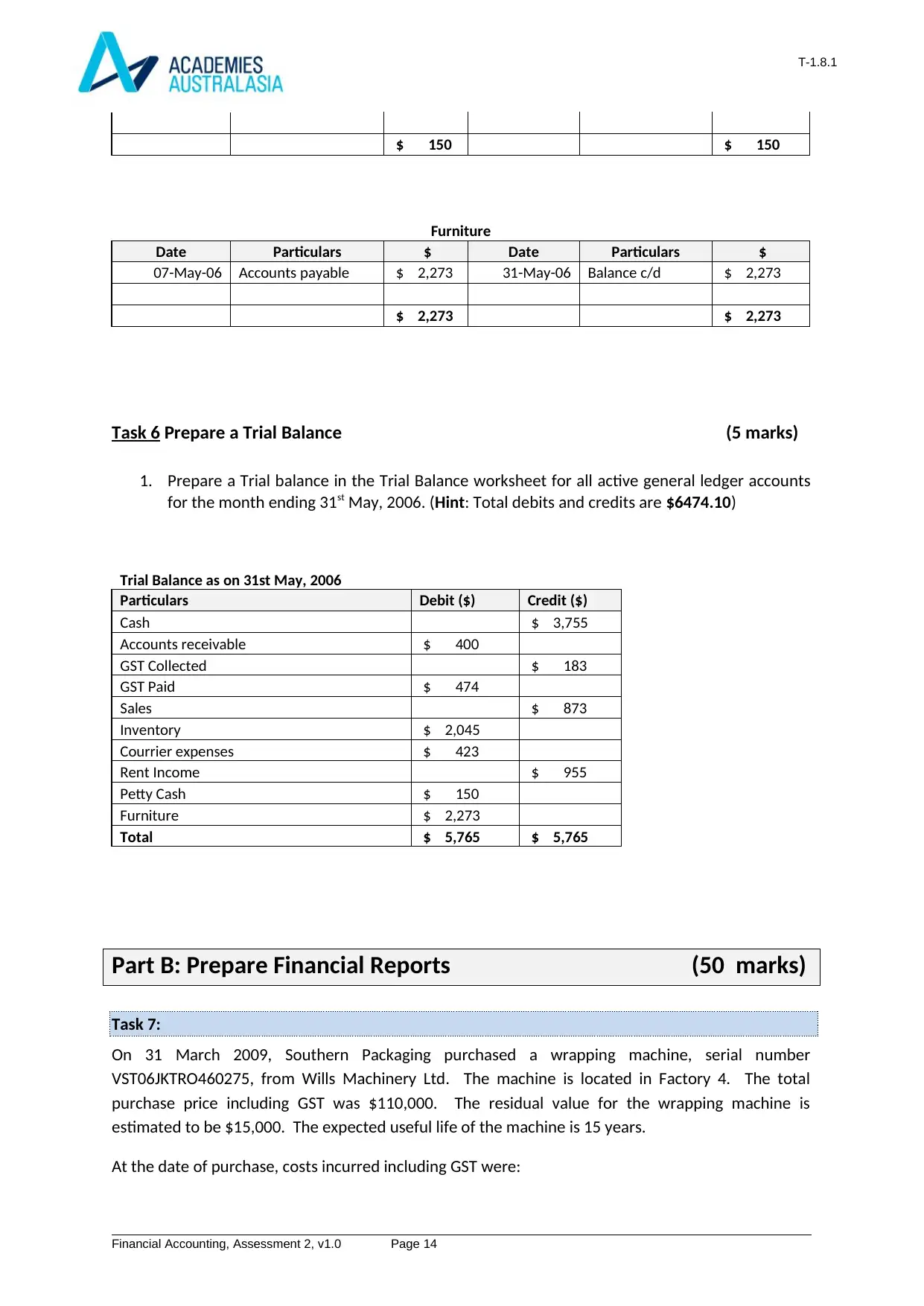

$ 150 $ 150

Furniture

Date Particulars $ Date Particulars $

07-May-06 Accounts payable $ 2,273 31-May-06 Balance c/d $ 2,273

$ 2,273 $ 2,273

Task 6 Prepare a Trial Balance (5 marks)

1. Prepare a Trial balance in the Trial Balance worksheet for all active general ledger accounts

for the month ending 31st May, 2006. (Hint: Total debits and credits are $6474.10)

Trial Balance as on 31st May, 2006

Particulars Debit ($) Credit ($)

Cash $ 3,755

Accounts receivable $ 400

GST Collected $ 183

GST Paid $ 474

Sales $ 873

Inventory $ 2,045

Courrier expenses $ 423

Rent Income $ 955

Petty Cash $ 150

Furniture $ 2,273

Total $ 5,765 $ 5,765

Part B: Prepare Financial Reports (50 marks)

Task 7:

On 31 March 2009, Southern Packaging purchased a wrapping machine, serial number

VST06JKTRO460275, from Wills Machinery Ltd. The machine is located in Factory 4. The total

purchase price including GST was $110,000. The residual value for the wrapping machine is

estimated to be $15,000. The expected useful life of the machine is 15 years.

At the date of purchase, costs incurred including GST were:

Financial Accounting, Assessment 2, v1.0 Page 14

$ 150 $ 150

Furniture

Date Particulars $ Date Particulars $

07-May-06 Accounts payable $ 2,273 31-May-06 Balance c/d $ 2,273

$ 2,273 $ 2,273

Task 6 Prepare a Trial Balance (5 marks)

1. Prepare a Trial balance in the Trial Balance worksheet for all active general ledger accounts

for the month ending 31st May, 2006. (Hint: Total debits and credits are $6474.10)

Trial Balance as on 31st May, 2006

Particulars Debit ($) Credit ($)

Cash $ 3,755

Accounts receivable $ 400

GST Collected $ 183

GST Paid $ 474

Sales $ 873

Inventory $ 2,045

Courrier expenses $ 423

Rent Income $ 955

Petty Cash $ 150

Furniture $ 2,273

Total $ 5,765 $ 5,765

Part B: Prepare Financial Reports (50 marks)

Task 7:

On 31 March 2009, Southern Packaging purchased a wrapping machine, serial number

VST06JKTRO460275, from Wills Machinery Ltd. The machine is located in Factory 4. The total

purchase price including GST was $110,000. The residual value for the wrapping machine is

estimated to be $15,000. The expected useful life of the machine is 15 years.

At the date of purchase, costs incurred including GST were:

Financial Accounting, Assessment 2, v1.0 Page 14

T-1.8.1

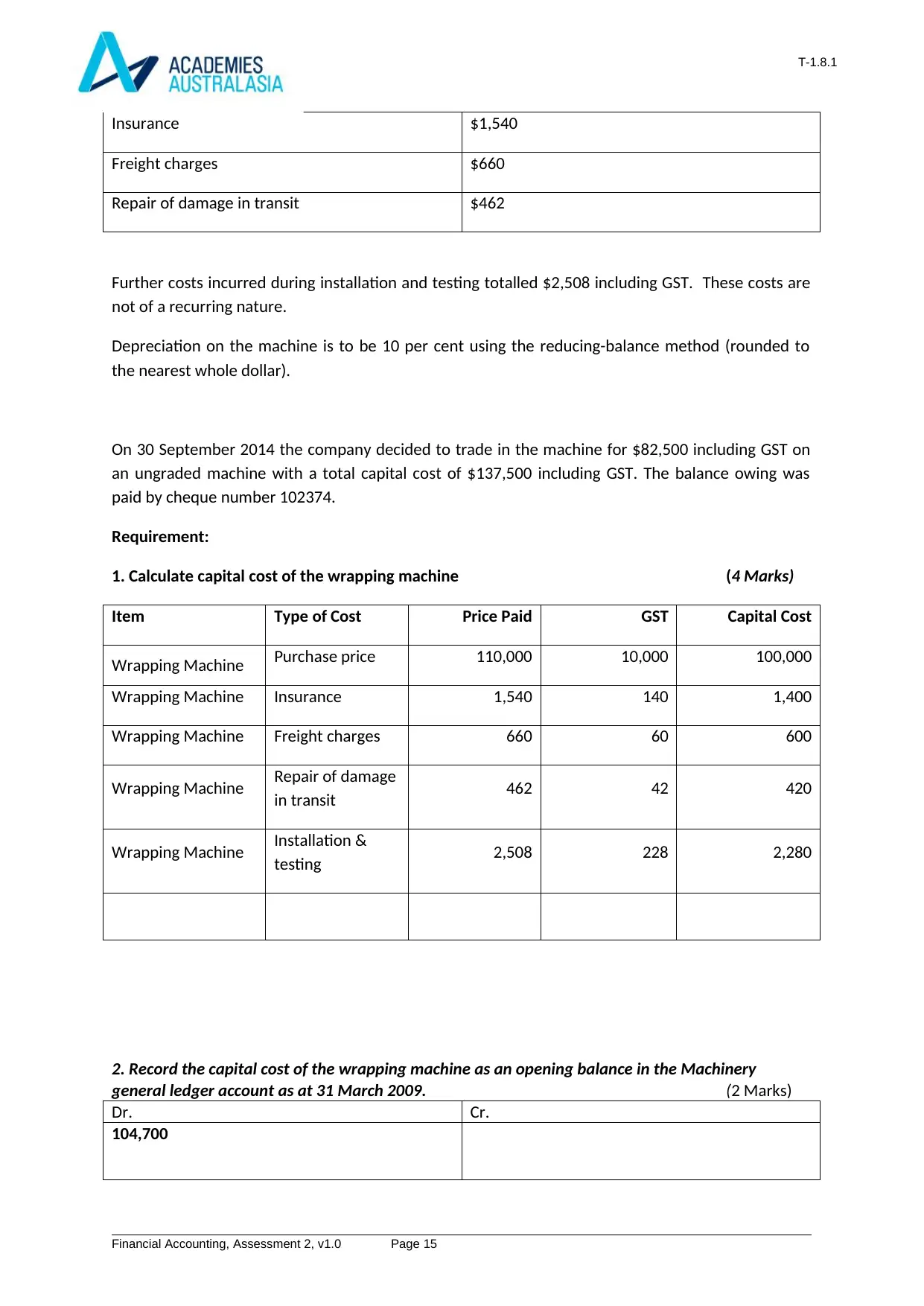

Insurance $1,540

Freight charges $660

Repair of damage in transit $462

Further costs incurred during installation and testing totalled $2,508 including GST. These costs are

not of a recurring nature.

Depreciation on the machine is to be 10 per cent using the reducing-balance method (rounded to

the nearest whole dollar).

On 30 September 2014 the company decided to trade in the machine for $82,500 including GST on

an ungraded machine with a total capital cost of $137,500 including GST. The balance owing was

paid by cheque number 102374.

Requirement:

1. Calculate capital cost of the wrapping machine (4 Marks)

Item Type of Cost Price Paid GST Capital Cost

Wrapping Machine Purchase price 110,000 10,000 100,000

Wrapping Machine Insurance 1,540 140 1,400

Wrapping Machine Freight charges 660 60 600

Wrapping Machine Repair of damage

in transit 462 42 420

Wrapping Machine Installation &

testing 2,508 228 2,280

2. Record the capital cost of the wrapping machine as an opening balance in the Machinery

general ledger account as at 31 March 2009. (2 Marks)

Dr. Cr.

104,700

Financial Accounting, Assessment 2, v1.0 Page 15

Insurance $1,540

Freight charges $660

Repair of damage in transit $462

Further costs incurred during installation and testing totalled $2,508 including GST. These costs are

not of a recurring nature.

Depreciation on the machine is to be 10 per cent using the reducing-balance method (rounded to

the nearest whole dollar).

On 30 September 2014 the company decided to trade in the machine for $82,500 including GST on

an ungraded machine with a total capital cost of $137,500 including GST. The balance owing was

paid by cheque number 102374.

Requirement:

1. Calculate capital cost of the wrapping machine (4 Marks)

Item Type of Cost Price Paid GST Capital Cost

Wrapping Machine Purchase price 110,000 10,000 100,000

Wrapping Machine Insurance 1,540 140 1,400

Wrapping Machine Freight charges 660 60 600

Wrapping Machine Repair of damage

in transit 462 42 420

Wrapping Machine Installation &

testing 2,508 228 2,280

2. Record the capital cost of the wrapping machine as an opening balance in the Machinery

general ledger account as at 31 March 2009. (2 Marks)

Dr. Cr.

104,700

Financial Accounting, Assessment 2, v1.0 Page 15

T-1.8.1

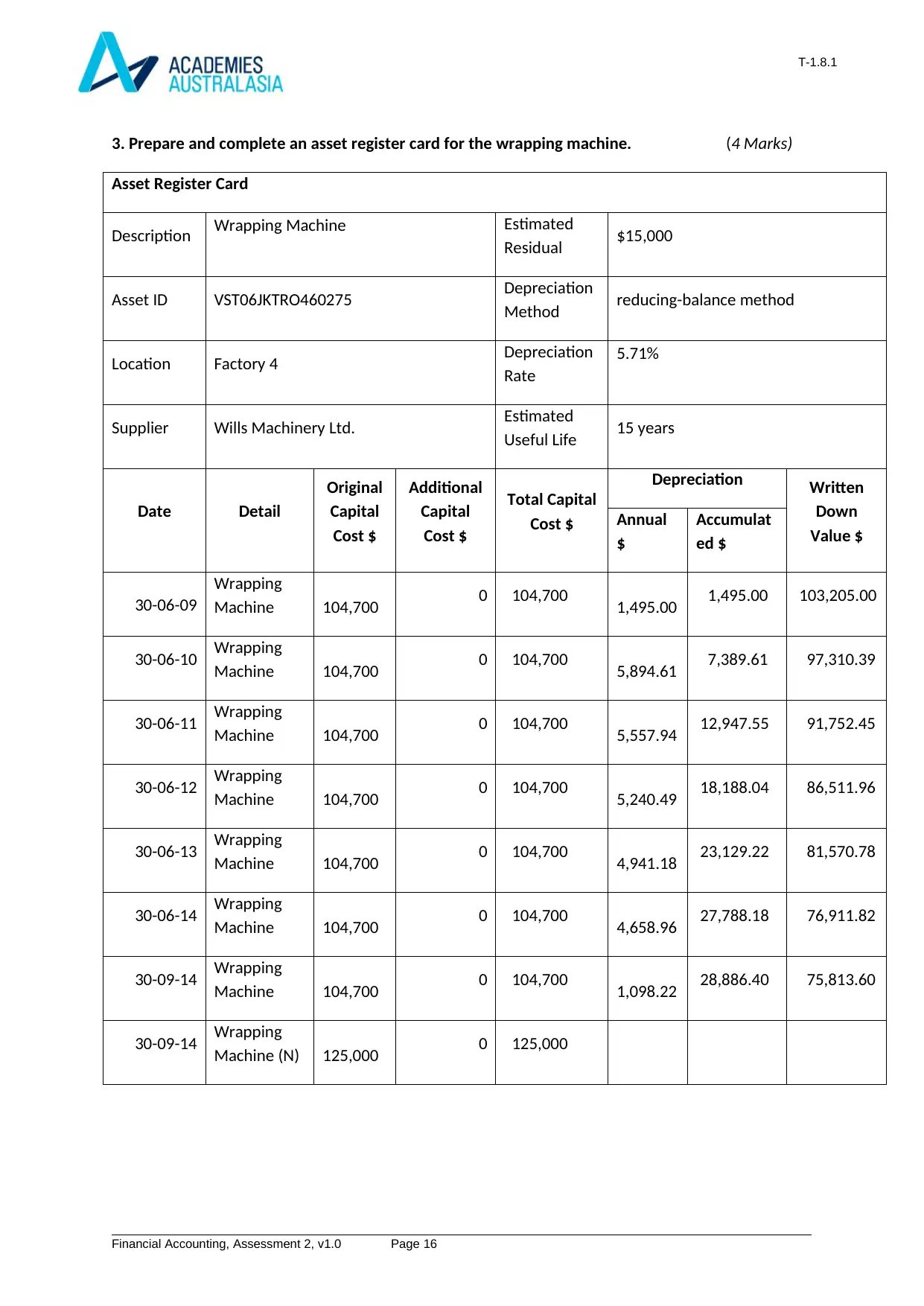

3. Prepare and complete an asset register card for the wrapping machine. (4 Marks)

Asset Register Card

Description Wrapping Machine Estimated

Residual $15,000

Asset ID VST06JKTRO460275 Depreciation

Method reducing-balance method

Location Factory 4 Depreciation

Rate

5.71%

Supplier Wills Machinery Ltd. Estimated

Useful Life 15 years

Date Detail

Original

Capital

Cost $

Additional

Capital

Cost $

Total Capital

Cost $

Depreciation Written

Down

Value $

Annual

$

Accumulat

ed $

30-06-09

Wrapping

Machine 104,700 0 104,700 1,495.00 1,495.00 103,205.00

30-06-10 Wrapping

Machine 104,700 0 104,700 5,894.61 7,389.61 97,310.39

30-06-11 Wrapping

Machine 104,700 0 104,700 5,557.94 12,947.55 91,752.45

30-06-12 Wrapping

Machine 104,700 0 104,700 5,240.49 18,188.04 86,511.96

30-06-13 Wrapping

Machine 104,700 0 104,700 4,941.18 23,129.22 81,570.78

30-06-14 Wrapping

Machine 104,700 0 104,700 4,658.96 27,788.18 76,911.82

30-09-14 Wrapping

Machine 104,700 0 104,700 1,098.22 28,886.40 75,813.60

30-09-14 Wrapping

Machine (N) 125,000 0 125,000

Financial Accounting, Assessment 2, v1.0 Page 16

3. Prepare and complete an asset register card for the wrapping machine. (4 Marks)

Asset Register Card

Description Wrapping Machine Estimated

Residual $15,000

Asset ID VST06JKTRO460275 Depreciation

Method reducing-balance method

Location Factory 4 Depreciation

Rate

5.71%

Supplier Wills Machinery Ltd. Estimated

Useful Life 15 years

Date Detail

Original

Capital

Cost $

Additional

Capital

Cost $

Total Capital

Cost $

Depreciation Written

Down

Value $

Annual

$

Accumulat

ed $

30-06-09

Wrapping

Machine 104,700 0 104,700 1,495.00 1,495.00 103,205.00

30-06-10 Wrapping

Machine 104,700 0 104,700 5,894.61 7,389.61 97,310.39

30-06-11 Wrapping

Machine 104,700 0 104,700 5,557.94 12,947.55 91,752.45

30-06-12 Wrapping

Machine 104,700 0 104,700 5,240.49 18,188.04 86,511.96

30-06-13 Wrapping

Machine 104,700 0 104,700 4,941.18 23,129.22 81,570.78

30-06-14 Wrapping

Machine 104,700 0 104,700 4,658.96 27,788.18 76,911.82

30-09-14 Wrapping

Machine 104,700 0 104,700 1,098.22 28,886.40 75,813.60

30-09-14 Wrapping

Machine (N) 125,000 0 125,000

Financial Accounting, Assessment 2, v1.0 Page 16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

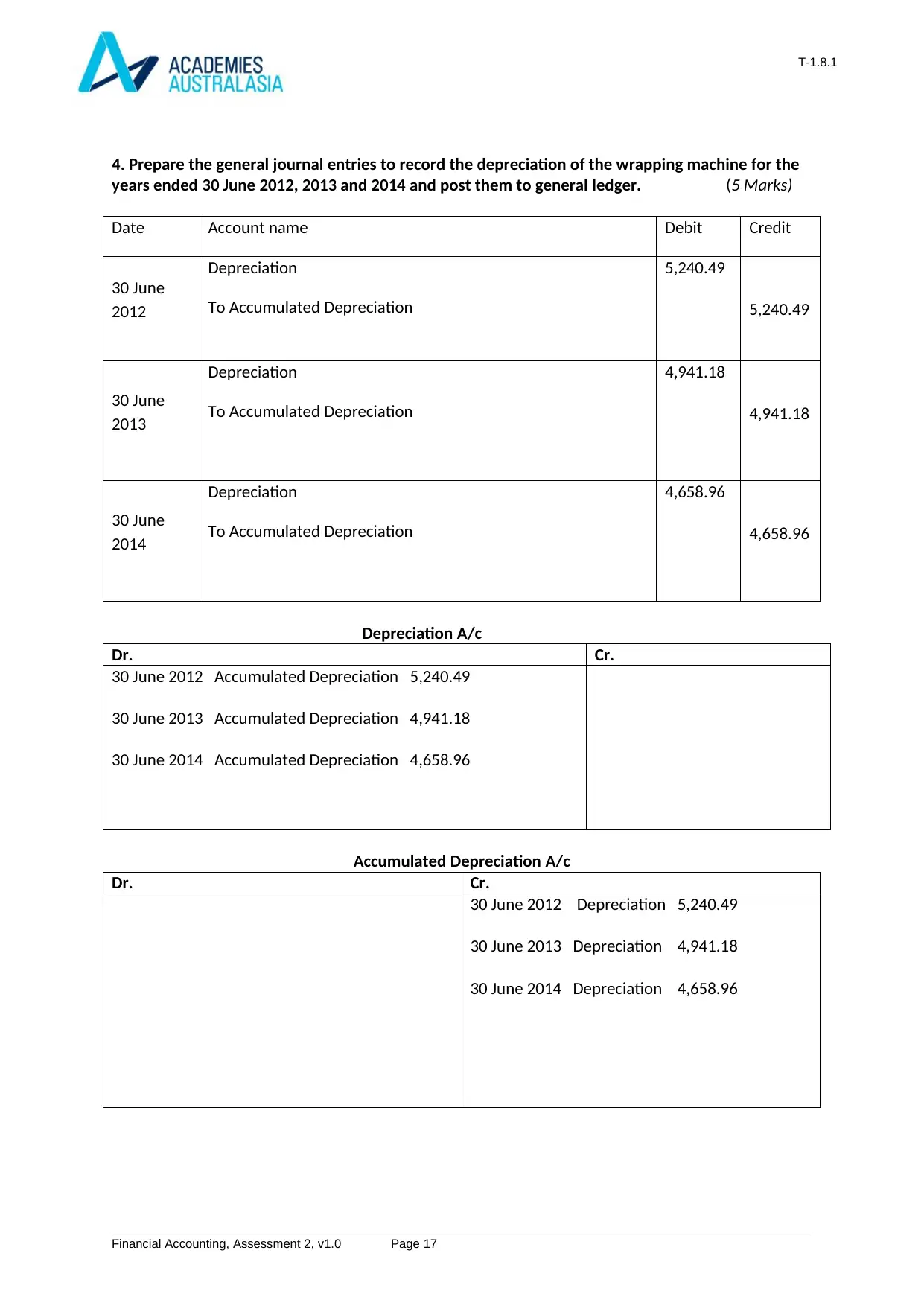

4. Prepare the general journal entries to record the depreciation of the wrapping machine for the

years ended 30 June 2012, 2013 and 2014 and post them to general ledger. (5 Marks)

Date Account name Debit Credit

30 June

2012

Depreciation

To Accumulated Depreciation

5,240.49

5,240.49

30 June

2013

Depreciation

To Accumulated Depreciation

4,941.18

4,941.18

30 June

2014

Depreciation

To Accumulated Depreciation

4,658.96

4,658.96

Depreciation A/c

Dr. Cr.

30 June 2012 Accumulated Depreciation 5,240.49

30 June 2013 Accumulated Depreciation 4,941.18

30 June 2014 Accumulated Depreciation 4,658.96

Accumulated Depreciation A/c

Dr. Cr.

30 June 2012 Depreciation 5,240.49

30 June 2013 Depreciation 4,941.18

30 June 2014 Depreciation 4,658.96

Financial Accounting, Assessment 2, v1.0 Page 17

4. Prepare the general journal entries to record the depreciation of the wrapping machine for the

years ended 30 June 2012, 2013 and 2014 and post them to general ledger. (5 Marks)

Date Account name Debit Credit

30 June

2012

Depreciation

To Accumulated Depreciation

5,240.49

5,240.49

30 June

2013

Depreciation

To Accumulated Depreciation

4,941.18

4,941.18

30 June

2014

Depreciation

To Accumulated Depreciation

4,658.96

4,658.96

Depreciation A/c

Dr. Cr.

30 June 2012 Accumulated Depreciation 5,240.49

30 June 2013 Accumulated Depreciation 4,941.18

30 June 2014 Accumulated Depreciation 4,658.96

Accumulated Depreciation A/c

Dr. Cr.

30 June 2012 Depreciation 5,240.49

30 June 2013 Depreciation 4,941.18

30 June 2014 Depreciation 4,658.96

Financial Accounting, Assessment 2, v1.0 Page 17

T-1.8.1

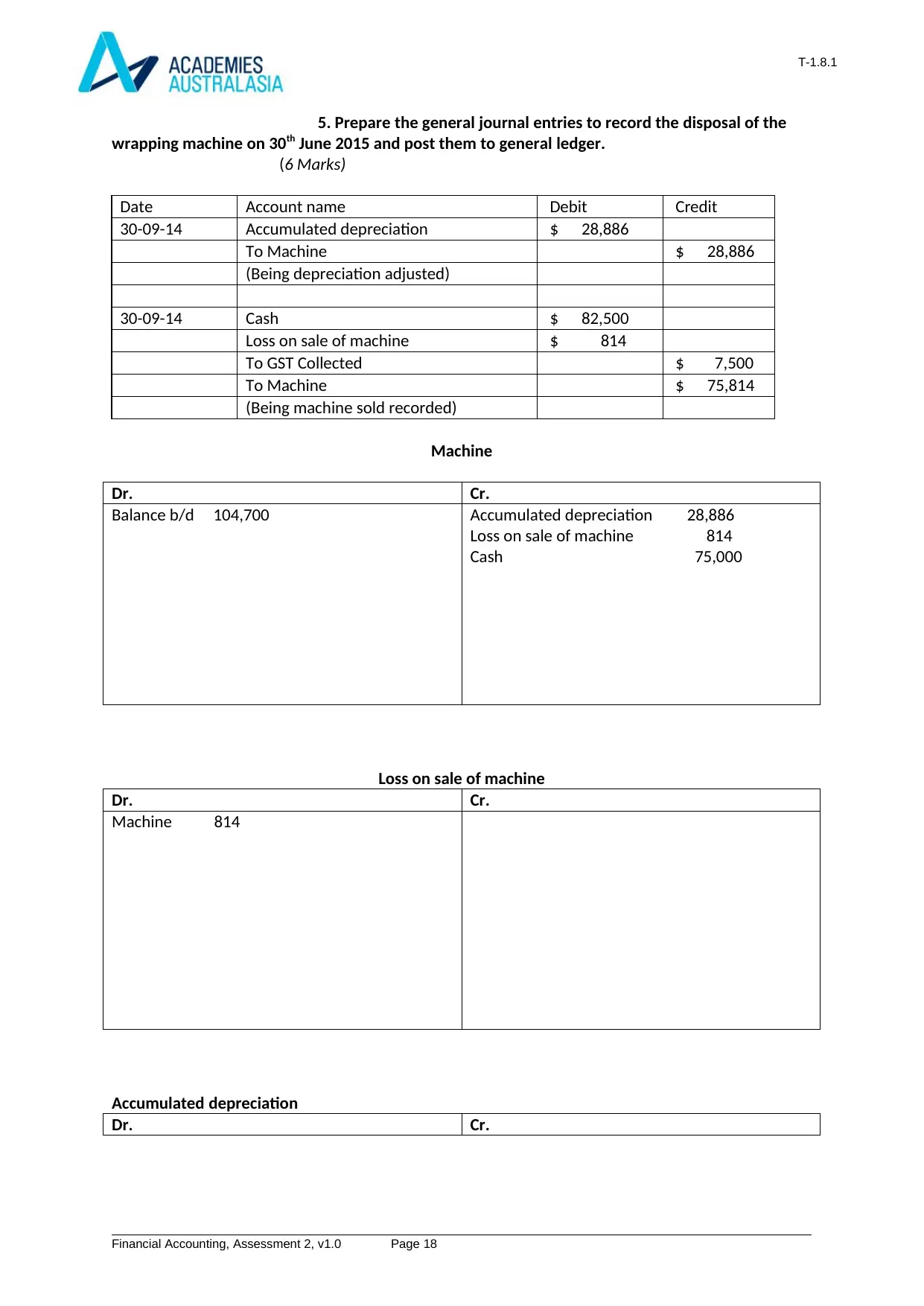

5. Prepare the general journal entries to record the disposal of the

wrapping machine on 30th June 2015 and post them to general ledger.

(6 Marks)

Date Account name Debit Credit

30-09-14 Accumulated depreciation $ 28,886

To Machine $ 28,886

(Being depreciation adjusted)

30-09-14 Cash $ 82,500

Loss on sale of machine $ 814

To GST Collected $ 7,500

To Machine $ 75,814

(Being machine sold recorded)

Machine

Dr. Cr.

Balance b/d 104,700 Accumulated depreciation 28,886

Loss on sale of machine 814

Cash 75,000

Loss on sale of machine

Dr. Cr.

Machine 814

Accumulated depreciation

Dr. Cr.

Financial Accounting, Assessment 2, v1.0 Page 18

5. Prepare the general journal entries to record the disposal of the

wrapping machine on 30th June 2015 and post them to general ledger.

(6 Marks)

Date Account name Debit Credit

30-09-14 Accumulated depreciation $ 28,886

To Machine $ 28,886

(Being depreciation adjusted)

30-09-14 Cash $ 82,500

Loss on sale of machine $ 814

To GST Collected $ 7,500

To Machine $ 75,814

(Being machine sold recorded)

Machine

Dr. Cr.

Balance b/d 104,700 Accumulated depreciation 28,886

Loss on sale of machine 814

Cash 75,000

Loss on sale of machine

Dr. Cr.

Machine 814

Accumulated depreciation

Dr. Cr.

Financial Accounting, Assessment 2, v1.0 Page 18

T-1.8.1

Machine 28,886

Financial Accounting, Assessment 2, v1.0 Page 19

Machine 28,886

Financial Accounting, Assessment 2, v1.0 Page 19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

T-1.8.1

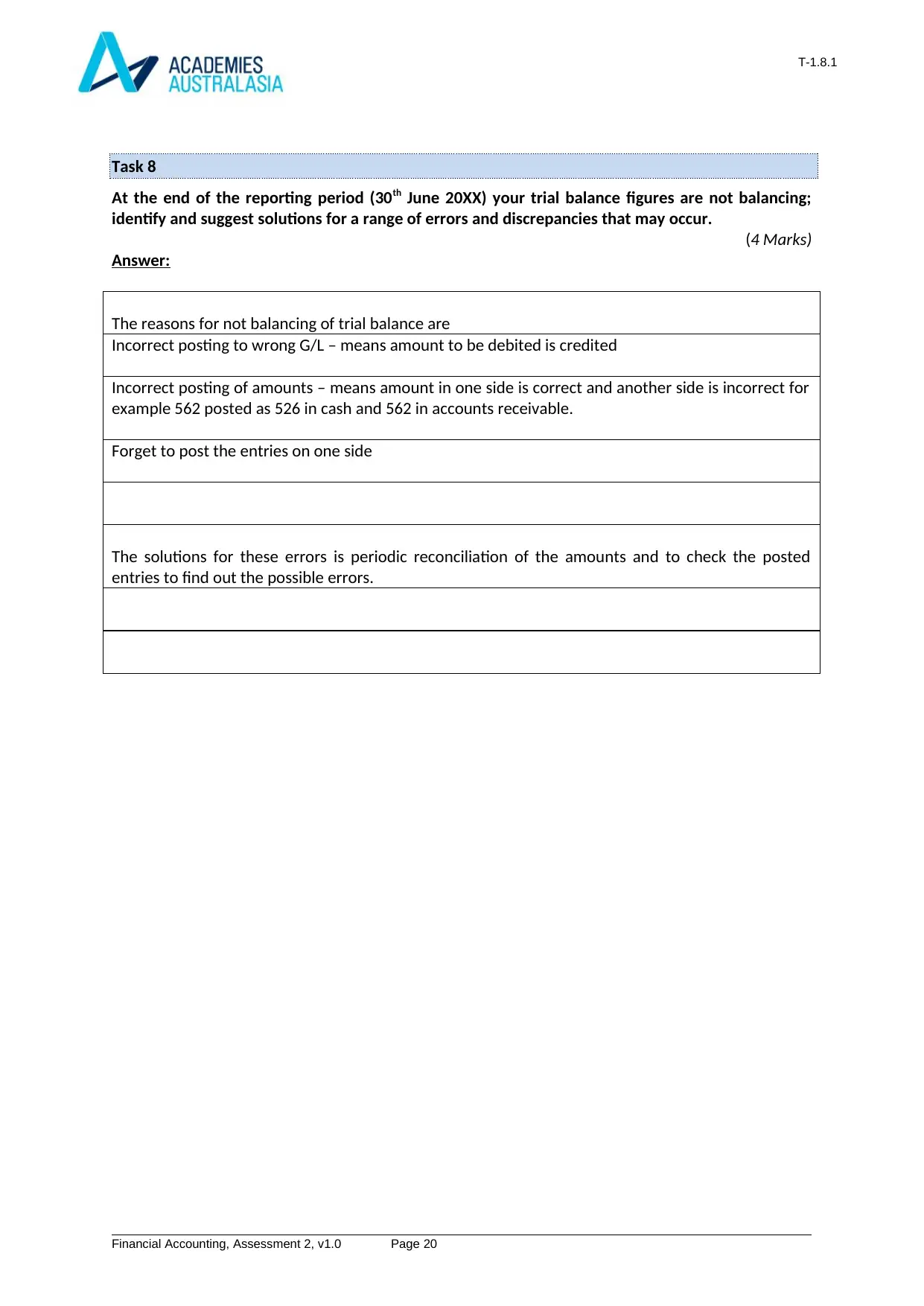

Task 8

At the end of the reporting period (30th June 20XX) your trial balance figures are not balancing;

identify and suggest solutions for a range of errors and discrepancies that may occur.

(4 Marks)

Answer:

The reasons for not balancing of trial balance are

Incorrect posting to wrong G/L – means amount to be debited is credited

Incorrect posting of amounts – means amount in one side is correct and another side is incorrect for

example 562 posted as 526 in cash and 562 in accounts receivable.

Forget to post the entries on one side

The solutions for these errors is periodic reconciliation of the amounts and to check the posted

entries to find out the possible errors.

Financial Accounting, Assessment 2, v1.0 Page 20

Task 8

At the end of the reporting period (30th June 20XX) your trial balance figures are not balancing;

identify and suggest solutions for a range of errors and discrepancies that may occur.

(4 Marks)

Answer:

The reasons for not balancing of trial balance are

Incorrect posting to wrong G/L – means amount to be debited is credited

Incorrect posting of amounts – means amount in one side is correct and another side is incorrect for

example 562 posted as 526 in cash and 562 in accounts receivable.

Forget to post the entries on one side

The solutions for these errors is periodic reconciliation of the amounts and to check the posted

entries to find out the possible errors.

Financial Accounting, Assessment 2, v1.0 Page 20

T-1.8.1

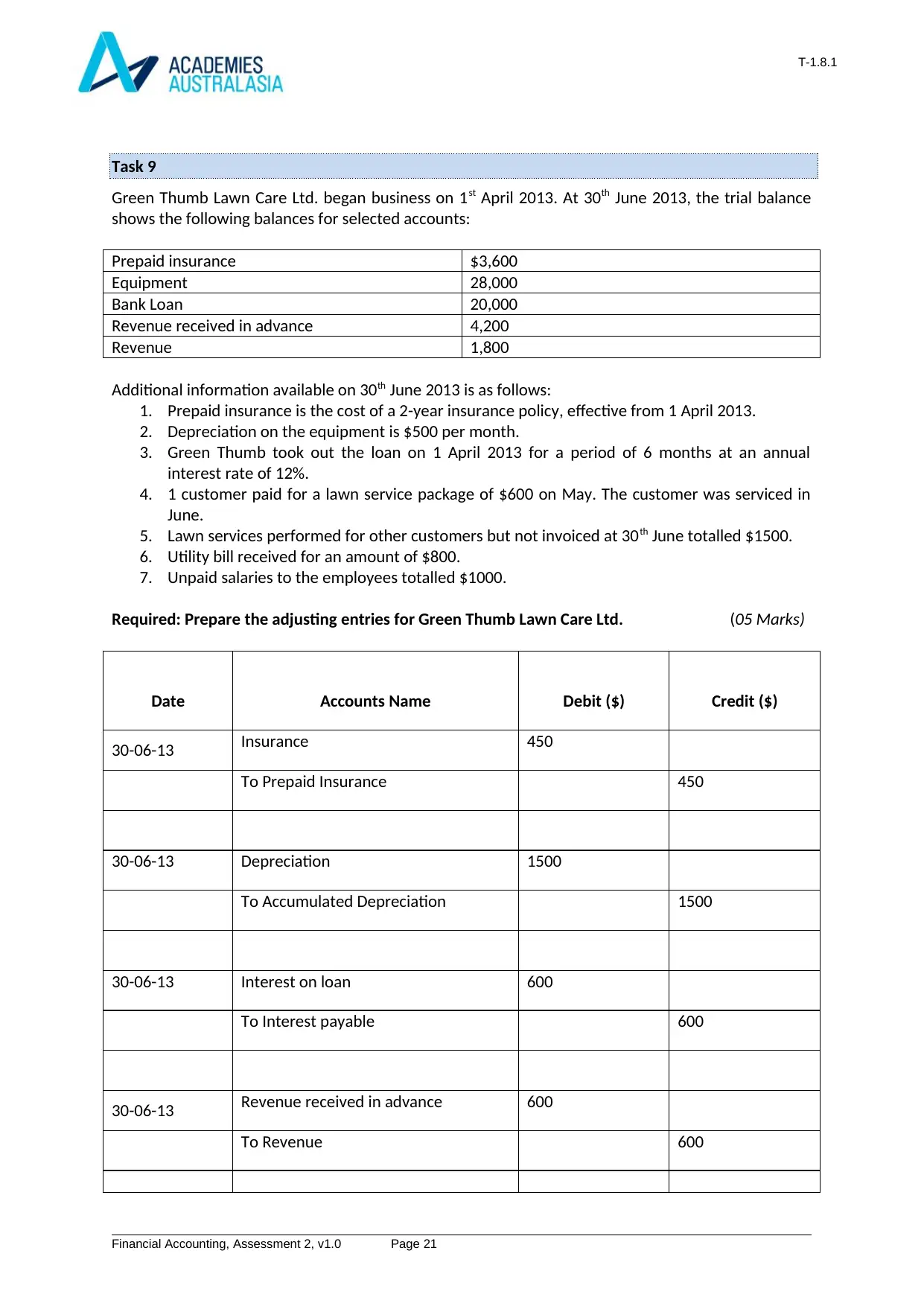

Task 9

Green Thumb Lawn Care Ltd. began business on 1st April 2013. At 30th June 2013, the trial balance

shows the following balances for selected accounts:

Prepaid insurance $3,600

Equipment 28,000

Bank Loan 20,000

Revenue received in advance 4,200

Revenue 1,800

Additional information available on 30th June 2013 is as follows:

1. Prepaid insurance is the cost of a 2-year insurance policy, effective from 1 April 2013.

2. Depreciation on the equipment is $500 per month.

3. Green Thumb took out the loan on 1 April 2013 for a period of 6 months at an annual

interest rate of 12%.

4. 1 customer paid for a lawn service package of $600 on May. The customer was serviced in

June.

5. Lawn services performed for other customers but not invoiced at 30th June totalled $1500.

6. Utility bill received for an amount of $800.

7. Unpaid salaries to the employees totalled $1000.

Required: Prepare the adjusting entries for Green Thumb Lawn Care Ltd. (05 Marks)

Date Accounts Name Debit ($) Credit ($)

30-06-13 Insurance 450

To Prepaid Insurance 450

30-06-13 Depreciation 1500

To Accumulated Depreciation 1500

30-06-13 Interest on loan 600

To Interest payable 600

30-06-13 Revenue received in advance 600

To Revenue 600

Financial Accounting, Assessment 2, v1.0 Page 21

Task 9

Green Thumb Lawn Care Ltd. began business on 1st April 2013. At 30th June 2013, the trial balance

shows the following balances for selected accounts:

Prepaid insurance $3,600

Equipment 28,000

Bank Loan 20,000

Revenue received in advance 4,200

Revenue 1,800

Additional information available on 30th June 2013 is as follows:

1. Prepaid insurance is the cost of a 2-year insurance policy, effective from 1 April 2013.

2. Depreciation on the equipment is $500 per month.

3. Green Thumb took out the loan on 1 April 2013 for a period of 6 months at an annual

interest rate of 12%.

4. 1 customer paid for a lawn service package of $600 on May. The customer was serviced in

June.

5. Lawn services performed for other customers but not invoiced at 30th June totalled $1500.

6. Utility bill received for an amount of $800.

7. Unpaid salaries to the employees totalled $1000.

Required: Prepare the adjusting entries for Green Thumb Lawn Care Ltd. (05 Marks)

Date Accounts Name Debit ($) Credit ($)

30-06-13 Insurance 450

To Prepaid Insurance 450

30-06-13 Depreciation 1500

To Accumulated Depreciation 1500

30-06-13 Interest on loan 600

To Interest payable 600

30-06-13 Revenue received in advance 600

To Revenue 600

Financial Accounting, Assessment 2, v1.0 Page 21

T-1.8.1

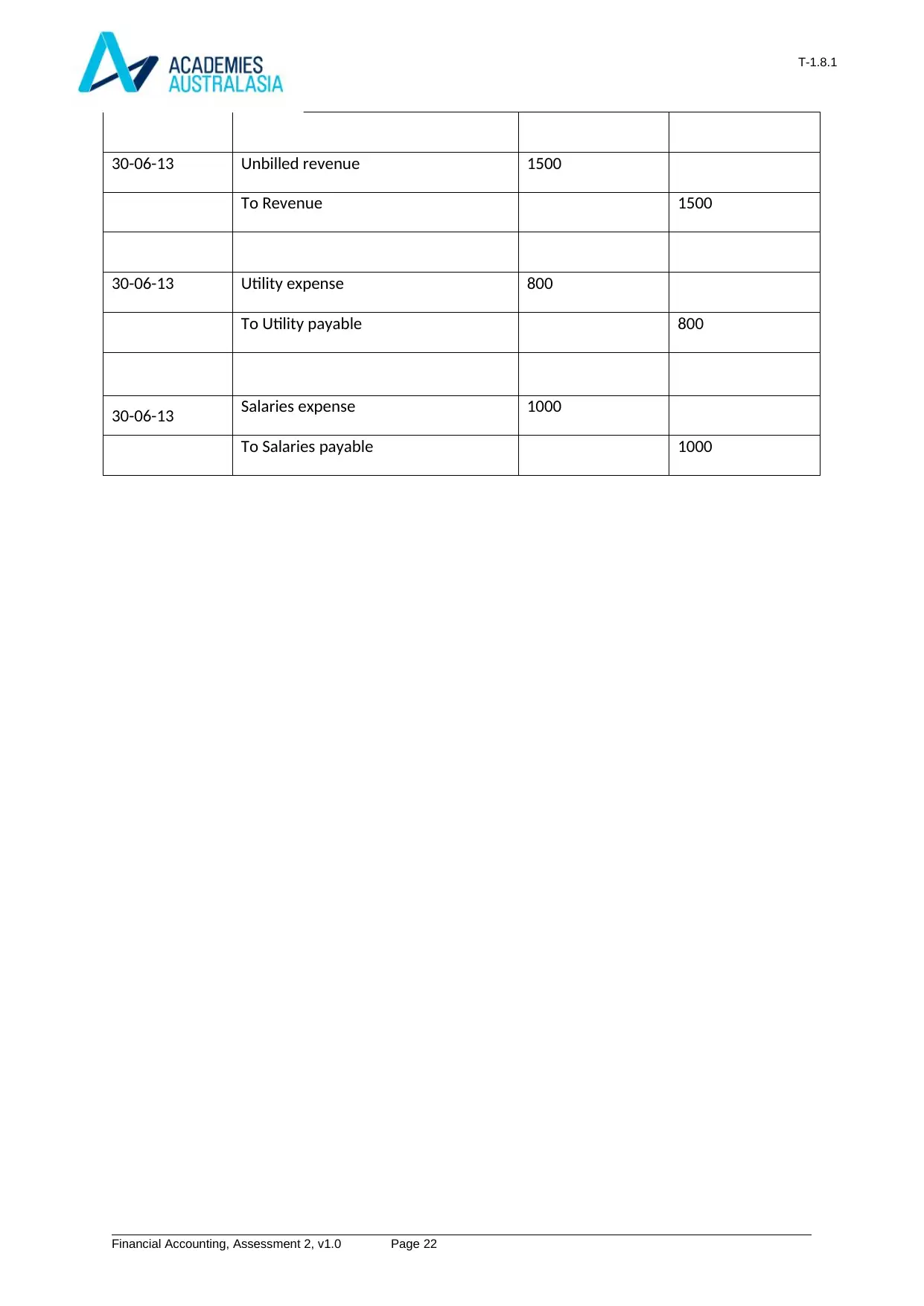

30-06-13 Unbilled revenue 1500

To Revenue 1500

30-06-13 Utility expense 800

To Utility payable 800

30-06-13 Salaries expense 1000

To Salaries payable 1000

Financial Accounting, Assessment 2, v1.0 Page 22

30-06-13 Unbilled revenue 1500

To Revenue 1500

30-06-13 Utility expense 800

To Utility payable 800

30-06-13 Salaries expense 1000

To Salaries payable 1000

Financial Accounting, Assessment 2, v1.0 Page 22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

T-1.8.1

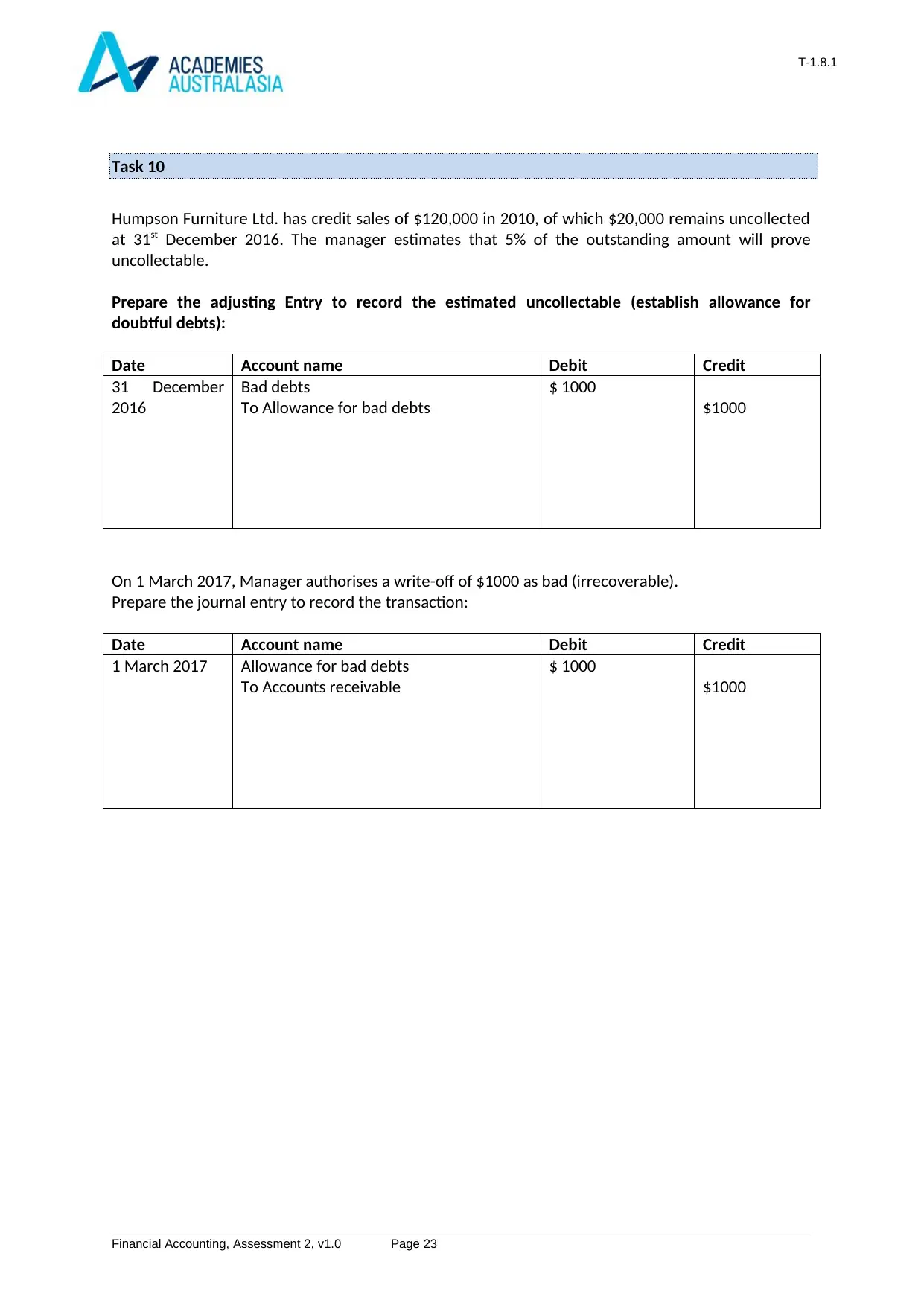

Task 10

Humpson Furniture Ltd. has credit sales of $120,000 in 2010, of which $20,000 remains uncollected

at 31st December 2016. The manager estimates that 5% of the outstanding amount will prove

uncollectable.

Prepare the adjusting Entry to record the estimated uncollectable (establish allowance for

doubtful debts):

Date Account name Debit Credit

31 December

2016

Bad debts

To Allowance for bad debts

$ 1000

$1000

On 1 March 2017, Manager authorises a write-off of $1000 as bad (irrecoverable).

Prepare the journal entry to record the transaction:

Date Account name Debit Credit

1 March 2017 Allowance for bad debts

To Accounts receivable

$ 1000

$1000

Financial Accounting, Assessment 2, v1.0 Page 23

Task 10

Humpson Furniture Ltd. has credit sales of $120,000 in 2010, of which $20,000 remains uncollected

at 31st December 2016. The manager estimates that 5% of the outstanding amount will prove

uncollectable.

Prepare the adjusting Entry to record the estimated uncollectable (establish allowance for

doubtful debts):

Date Account name Debit Credit

31 December

2016

Bad debts

To Allowance for bad debts

$ 1000

$1000

On 1 March 2017, Manager authorises a write-off of $1000 as bad (irrecoverable).

Prepare the journal entry to record the transaction:

Date Account name Debit Credit

1 March 2017 Allowance for bad debts

To Accounts receivable

$ 1000

$1000

Financial Accounting, Assessment 2, v1.0 Page 23

1 out of 23

Related Documents

![[FULL ACCESS] Preparing Trial Balance for OMG Ltd](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fgd%2F67a5b66c94624beab9c6278552dc283a.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.