Analysis of Financial Accounting for Intangible Assets: AASB 138

VerifiedAdded on 2022/08/28

|8

|2555

|17

Report

AI Summary

This report provides a comprehensive analysis of financial accounting for intangible assets, with a specific focus on the guidelines outlined in AASB 138. It distinguishes between internally generated and acquired goodwill, outlining the recognition and measurement criteria for each. The report explores the importance of accurate cost measurement and future benefit assessment for intangible assets, including the treatment of research and development phases. It provides practical examples of acquired goodwill calculations and journal entries, while also addressing the disclosure requirements necessary for transparent financial reporting. The report emphasizes the importance of adhering to AASB 138 to ensure accurate presentation of a company's financial position, offering valuable insights into the complexities of accounting for intangible assets.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL ACCOUNTING

Executive Summary

The assessment would be focusing on proper reporting process for intangible asset of a business

considering relevant accounting standard. The analysis would be showing difference which

exists between internally generated goodwill and purchased goodwill for the business so that the

same can be reported appropriately in the financial statements. The provisions which are stated

in AASB 138 effectively provides the guidelines for making the classification and how the

different types of intangible assets are to be disclosed in the annual reports for a business. The

analysis would also be providing numerical examples relating to the treatment of acquired

goodwill and journal entry associated with the same are also portrayed in the assessment.

FINANCIAL ACCOUNTING

Executive Summary

The assessment would be focusing on proper reporting process for intangible asset of a business

considering relevant accounting standard. The analysis would be showing difference which

exists between internally generated goodwill and purchased goodwill for the business so that the

same can be reported appropriately in the financial statements. The provisions which are stated

in AASB 138 effectively provides the guidelines for making the classification and how the

different types of intangible assets are to be disclosed in the annual reports for a business. The

analysis would also be providing numerical examples relating to the treatment of acquired

goodwill and journal entry associated with the same are also portrayed in the assessment.

2

FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Recognition and Measurement of Intangible Assets...................................................................3

Distinction Between Internally Generated Intangible Assets and Acquired Intangible Assets...4

Disclosure Requirements.............................................................................................................5

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................6

FINANCIAL ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Recognition and Measurement of Intangible Assets...................................................................3

Distinction Between Internally Generated Intangible Assets and Acquired Intangible Assets...4

Disclosure Requirements.............................................................................................................5

Conclusion.......................................................................................................................................6

Reference.........................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL ACCOUNTING

Introduction

The focus of the assessment is to conduct an analysis on the reporting framework which

is related to accounting for intangible assets. The reporting for intangibles assets would be

considered for both internally generated goodwill and purchased goodwill for an entity. The case

of US firms is being analyzed who are following different accounting practices for recording

intangible assets such as brands, information technology and other assets. The analysis further

would be showing the main difference which exists between reporting for internally generated

intangible assets and purchased intangible assets. In order to provide appropriate justification in

this regard, the provisions of AASB 138 “Intangible Assets” would be considered. The analysis

would also be recommending the company as to what action need to be taken by companies for

the purpose of reporting intangible assets (Ifrs.org. 2020). The discussion would be including

provisions and examples which would show treatment for intangible assets both in the case of

internally generated intangible assets and acquired intangible assets. The assessment would be

including numerical examples for the purpose of better presentation of treatments from the

perspective of accounting.

Discussion

Recognition and Measurement of Intangible Assets

The intangible assets for a business are portrayed in the annual statements and the same

covers both internally generated intangibles assets and acquired intangible assets. As per the

provisions of AASB 138 “Intangible Assets”, an intangible asset shall be recognized only on the

basis of two conditions:

The asset would be bearing future benefits which is directly attributable to the asset and

would be flowing directly to the asset.

The costs which is associated with the intangible asset can be measured accurately.

The companies are required to adhere to the above principles of AASB 138 so that the

intangible assets of the business are measured in an appropriate manner. The above points

effectively show that future benefits which is associated with the intangible assets should be

accurately measured. In the case of Intangible assets which are internally generated, the reporting

process is similar and the same should adhere to recognition criteria which is cited in AASB 138

“Intangible Assets”. As per para 24 of AASB 138 “Intangible Assets”, an intangible asset shall

be measured initially at costs and would be portrayed in the annual report of the business

(Aasb.gov.au. 2020).

In certain circumstances internally-generated intangible assets are sometimes reported in the

books of accounts and the same qualifies for recognition. The qualifying criteria which is being

considered is related is the presence of assets and another criterion which needs to be met is the

accurate measurement of costs which is related to the asset. The internally generated intangible

assets need to be classified into two sections for generation of asset which are research phase and

development phase. On the basis of the classification of the activities for the generation of

internally generated intangible assets, reporting process which is to be followed by the business

is decided. As per the provisions of para 54 of AASB 138 “Intangible Assets”, any intangible

asset which is generated from research activities should not be recognized as intangible asset for

the business (Wallstreet Mojo. 2018). The expenditure which is related to the research phase of

FINANCIAL ACCOUNTING

Introduction

The focus of the assessment is to conduct an analysis on the reporting framework which

is related to accounting for intangible assets. The reporting for intangibles assets would be

considered for both internally generated goodwill and purchased goodwill for an entity. The case

of US firms is being analyzed who are following different accounting practices for recording

intangible assets such as brands, information technology and other assets. The analysis further

would be showing the main difference which exists between reporting for internally generated

intangible assets and purchased intangible assets. In order to provide appropriate justification in

this regard, the provisions of AASB 138 “Intangible Assets” would be considered. The analysis

would also be recommending the company as to what action need to be taken by companies for

the purpose of reporting intangible assets (Ifrs.org. 2020). The discussion would be including

provisions and examples which would show treatment for intangible assets both in the case of

internally generated intangible assets and acquired intangible assets. The assessment would be

including numerical examples for the purpose of better presentation of treatments from the

perspective of accounting.

Discussion

Recognition and Measurement of Intangible Assets

The intangible assets for a business are portrayed in the annual statements and the same

covers both internally generated intangibles assets and acquired intangible assets. As per the

provisions of AASB 138 “Intangible Assets”, an intangible asset shall be recognized only on the

basis of two conditions:

The asset would be bearing future benefits which is directly attributable to the asset and

would be flowing directly to the asset.

The costs which is associated with the intangible asset can be measured accurately.

The companies are required to adhere to the above principles of AASB 138 so that the

intangible assets of the business are measured in an appropriate manner. The above points

effectively show that future benefits which is associated with the intangible assets should be

accurately measured. In the case of Intangible assets which are internally generated, the reporting

process is similar and the same should adhere to recognition criteria which is cited in AASB 138

“Intangible Assets”. As per para 24 of AASB 138 “Intangible Assets”, an intangible asset shall

be measured initially at costs and would be portrayed in the annual report of the business

(Aasb.gov.au. 2020).

In certain circumstances internally-generated intangible assets are sometimes reported in the

books of accounts and the same qualifies for recognition. The qualifying criteria which is being

considered is related is the presence of assets and another criterion which needs to be met is the

accurate measurement of costs which is related to the asset. The internally generated intangible

assets need to be classified into two sections for generation of asset which are research phase and

development phase. On the basis of the classification of the activities for the generation of

internally generated intangible assets, reporting process which is to be followed by the business

is decided. As per the provisions of para 54 of AASB 138 “Intangible Assets”, any intangible

asset which is generated from research activities should not be recognized as intangible asset for

the business (Wallstreet Mojo. 2018). The expenditure which is related to the research phase of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL ACCOUNTING

the intangible asset should be recognized by the management of the company as research

expenses and the same needs to be recognized according in the income statement of the business.

Some of the research activities which can be recognized are activities of obtaining new

knowledge, requirements of materials which will be used for the purpose of conducting the

research.

Another phase which is considered for the purpose of recognition of intangible asset is

development phase where the asset would be recognized as intangible assets on meeting of the

following criteria (Su and Wells 2015). The conditions which needs to be met are effectively

listed below in details:

The technical feasibility which is associated with the research considering that the same

would be available for sale.

The intention of the business to use or sell the intangible assets so that it can provide

value to the business and thereby the same can be reported.

The ability of the business to fully use or sell the intangible assets to third party.

The ability of the business to appropriately measure the future benefits of the intangible

assets and the same can be measured in an appropriate manner in the financial terms by

the management of the company.

The developmental phase expenses are considered to be qualified for intangible assets if the

above criteria are appropriately met and intangible assets are developed in an appropriate

manner. Some of the example of developmental research expenses are design, construction and

pre-testing of products, the design of tools, jigs and other instruments which cab effectively save

the costs which is associated with the business (Carvalho, Rodrigues and Ferreira 2016). The

above analysis effectively shows that intangible assets which are internally generated are

frequently recognized in the financial statements depending on the fulfillment of the conditions

which are specified in the accounting standard of AASB 138. However, it is to be noted that

internally generated intangible assets also have certain exception which are stated in AASB 138

“Intangible Assets”. As per the provisions of para 63 of AASB 138 “Intangible Assets”,

internally generated brands, , titles of publishing houses, lists from customers and similar

substances items should not be recognized in the financial statements as intangible assets (Chang

and Tsai 2013). In case such items are recognized in the financial statements then the same

would be treated as violation of this accounting standard and would be giving an inappropriate

presentation of the financial position of the business.

Distinction Between Internally Generated Intangible Assets and Acquired Intangible

Assets

The provisions which are stated in AASB 138 “Intangible Assets” states different

regarding the treatment of the two different types of intangible assets for a business. The

recognition criteria for both the types of goodwill are quite similar considering the criteria which

is present for measuring the intangible assets of the business. Th criteria for recognition remains

the same which is accurate estimation of the future benefits associated with the intangible assets

and effective estimation of costs of the business. It is to be noted that intangible assets which is

acquired needs to be portrayed in the financial accounts on an immediate basis. The costs of such

acquired intangible assets needs to be incorporated along with the purchase price of the

intangible assets. The purchase price of intangible assets means the purchase consideration

which the business needs to pay for acquiring the intangible asset (Mohr and Batsakis 2014). In

FINANCIAL ACCOUNTING

the intangible asset should be recognized by the management of the company as research

expenses and the same needs to be recognized according in the income statement of the business.

Some of the research activities which can be recognized are activities of obtaining new

knowledge, requirements of materials which will be used for the purpose of conducting the

research.

Another phase which is considered for the purpose of recognition of intangible asset is

development phase where the asset would be recognized as intangible assets on meeting of the

following criteria (Su and Wells 2015). The conditions which needs to be met are effectively

listed below in details:

The technical feasibility which is associated with the research considering that the same

would be available for sale.

The intention of the business to use or sell the intangible assets so that it can provide

value to the business and thereby the same can be reported.

The ability of the business to fully use or sell the intangible assets to third party.

The ability of the business to appropriately measure the future benefits of the intangible

assets and the same can be measured in an appropriate manner in the financial terms by

the management of the company.

The developmental phase expenses are considered to be qualified for intangible assets if the

above criteria are appropriately met and intangible assets are developed in an appropriate

manner. Some of the example of developmental research expenses are design, construction and

pre-testing of products, the design of tools, jigs and other instruments which cab effectively save

the costs which is associated with the business (Carvalho, Rodrigues and Ferreira 2016). The

above analysis effectively shows that intangible assets which are internally generated are

frequently recognized in the financial statements depending on the fulfillment of the conditions

which are specified in the accounting standard of AASB 138. However, it is to be noted that

internally generated intangible assets also have certain exception which are stated in AASB 138

“Intangible Assets”. As per the provisions of para 63 of AASB 138 “Intangible Assets”,

internally generated brands, , titles of publishing houses, lists from customers and similar

substances items should not be recognized in the financial statements as intangible assets (Chang

and Tsai 2013). In case such items are recognized in the financial statements then the same

would be treated as violation of this accounting standard and would be giving an inappropriate

presentation of the financial position of the business.

Distinction Between Internally Generated Intangible Assets and Acquired Intangible

Assets

The provisions which are stated in AASB 138 “Intangible Assets” states different

regarding the treatment of the two different types of intangible assets for a business. The

recognition criteria for both the types of goodwill are quite similar considering the criteria which

is present for measuring the intangible assets of the business. Th criteria for recognition remains

the same which is accurate estimation of the future benefits associated with the intangible assets

and effective estimation of costs of the business. It is to be noted that intangible assets which is

acquired needs to be portrayed in the financial accounts on an immediate basis. The costs of such

acquired intangible assets needs to be incorporated along with the purchase price of the

intangible assets. The purchase price of intangible assets means the purchase consideration

which the business needs to pay for acquiring the intangible asset (Mohr and Batsakis 2014). In

5

FINANCIAL ACCOUNTING

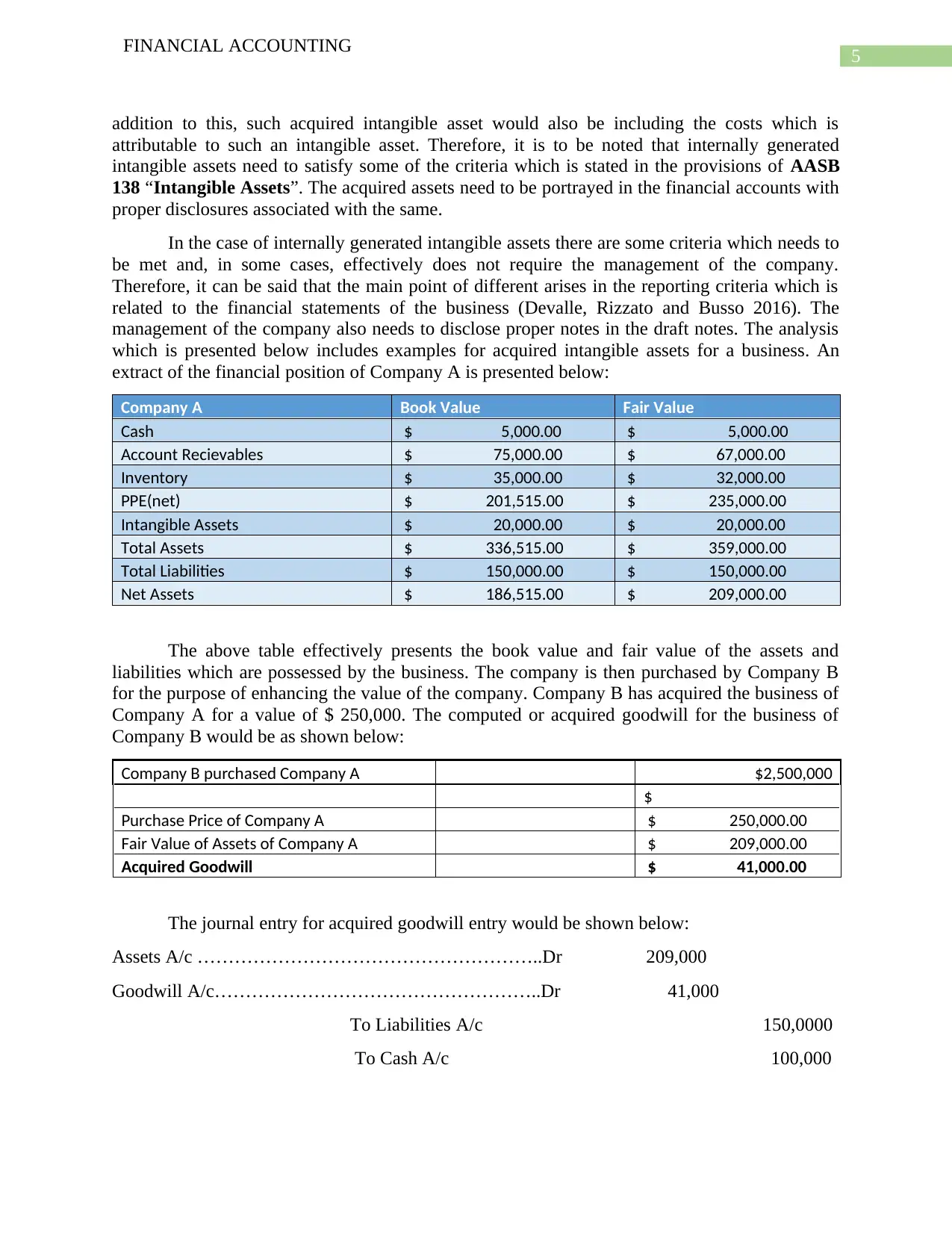

addition to this, such acquired intangible asset would also be including the costs which is

attributable to such an intangible asset. Therefore, it is to be noted that internally generated

intangible assets need to satisfy some of the criteria which is stated in the provisions of AASB

138 “Intangible Assets”. The acquired assets need to be portrayed in the financial accounts with

proper disclosures associated with the same.

In the case of internally generated intangible assets there are some criteria which needs to

be met and, in some cases, effectively does not require the management of the company.

Therefore, it can be said that the main point of different arises in the reporting criteria which is

related to the financial statements of the business (Devalle, Rizzato and Busso 2016). The

management of the company also needs to disclose proper notes in the draft notes. The analysis

which is presented below includes examples for acquired intangible assets for a business. An

extract of the financial position of Company A is presented below:

Company A Book Value Fair Value

Cash $ 5,000.00 $ 5,000.00

Account Recievables $ 75,000.00 $ 67,000.00

Inventory $ 35,000.00 $ 32,000.00

PPE(net) $ 201,515.00 $ 235,000.00

Intangible Assets $ 20,000.00 $ 20,000.00

Total Assets $ 336,515.00 $ 359,000.00

Total Liabilities $ 150,000.00 $ 150,000.00

Net Assets $ 186,515.00 $ 209,000.00

The above table effectively presents the book value and fair value of the assets and

liabilities which are possessed by the business. The company is then purchased by Company B

for the purpose of enhancing the value of the company. Company B has acquired the business of

Company A for a value of $ 250,000. The computed or acquired goodwill for the business of

Company B would be as shown below:

Company B purchased Company A $2,500,000

$

Purchase Price of Company A $ 250,000.00

Fair Value of Assets of Company A $ 209,000.00

Acquired Goodwill $ 41,000.00

The journal entry for acquired goodwill entry would be shown below:

Assets A/c ………………………………………………..Dr 209,000

Goodwill A/c……………………………………………..Dr 41,000

To Liabilities A/c 150,0000

To Cash A/c 100,000

FINANCIAL ACCOUNTING

addition to this, such acquired intangible asset would also be including the costs which is

attributable to such an intangible asset. Therefore, it is to be noted that internally generated

intangible assets need to satisfy some of the criteria which is stated in the provisions of AASB

138 “Intangible Assets”. The acquired assets need to be portrayed in the financial accounts with

proper disclosures associated with the same.

In the case of internally generated intangible assets there are some criteria which needs to

be met and, in some cases, effectively does not require the management of the company.

Therefore, it can be said that the main point of different arises in the reporting criteria which is

related to the financial statements of the business (Devalle, Rizzato and Busso 2016). The

management of the company also needs to disclose proper notes in the draft notes. The analysis

which is presented below includes examples for acquired intangible assets for a business. An

extract of the financial position of Company A is presented below:

Company A Book Value Fair Value

Cash $ 5,000.00 $ 5,000.00

Account Recievables $ 75,000.00 $ 67,000.00

Inventory $ 35,000.00 $ 32,000.00

PPE(net) $ 201,515.00 $ 235,000.00

Intangible Assets $ 20,000.00 $ 20,000.00

Total Assets $ 336,515.00 $ 359,000.00

Total Liabilities $ 150,000.00 $ 150,000.00

Net Assets $ 186,515.00 $ 209,000.00

The above table effectively presents the book value and fair value of the assets and

liabilities which are possessed by the business. The company is then purchased by Company B

for the purpose of enhancing the value of the company. Company B has acquired the business of

Company A for a value of $ 250,000. The computed or acquired goodwill for the business of

Company B would be as shown below:

Company B purchased Company A $2,500,000

$

Purchase Price of Company A $ 250,000.00

Fair Value of Assets of Company A $ 209,000.00

Acquired Goodwill $ 41,000.00

The journal entry for acquired goodwill entry would be shown below:

Assets A/c ………………………………………………..Dr 209,000

Goodwill A/c……………………………………………..Dr 41,000

To Liabilities A/c 150,0000

To Cash A/c 100,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL ACCOUNTING

The internally generated goodwill for a business can be generated by technological

advancements but the same needs to be measured in an appropriate manner. The internally

generated goodwill or intangible assets are directly shown in the annual reports of the business if

the same satisfies the criteria which is stated in the AASB 138.

Disclosure Requirements

The management of a company which is recognizing the intangible assets of a business

needs to appropriately consider the model which is to be followed for the purpose of measuring

the intangible assets. The provisions of AASB 138 effectively shows that there are two models

which the business can follow which are revaluation model and cost model for the purpose of

effectively reporting the intangible assets of the business (Arrighetti, Landini and Lasagni 2014).

The management of the company needs to appropriate provide proper disclosures in the notes to

accounting statements so that information is available to the users regarding the type of

intangible asset which is used by the business. The disclosure requirements which is required to

be portrayed is shown below:

whether the intangible assets have definite or indefinite lives considering their useful lifes

the amortization methods used for intangible asset

the gross carrying amount and any accumulated amortization

a reconciliation of the carrying amount at the beginning and end of the period

impairment losses reversed in profit or loss during the period in accordance with AASB

136

The disclosure requirements for the business needs to be appropriate and the same effectively

provides better clarity of the financial position of the business (Peters and Taylor 2017). The

financial situation of the business appropriately presents the intangible assets if the same is

disclosed using the provisions which are provided in AASB 138.

Conclusion

The above discussion effectively shows the reporting process which is followed for

reporting of intangible assets of a business. The analysis which is presented in the above

discussion shows that there are two types of intangible assets which involves acquired goodwill

and internally generated goodwill for a business. The assessment also shows differences which

exists between reporting process of both the types of goodwill. The analysis also shows reporting

criteria separately for both the types of intangible assets and also cites provisions which are

stated in ASSB 138. In addition to this, the analysis also includes examples which is of a

hypothetical company and journal entries are also portrayed along with the same. The numerical

example makes it clear regarding the treatments which needs to be shown in the notes to

accounts section. Further proper notes and disclosures are also required as presented in the above

discussion. Therefore, it can be concluded that reporting framework for both types of goodwill is

different considering the nature of disclosures as well.

FINANCIAL ACCOUNTING

The internally generated goodwill for a business can be generated by technological

advancements but the same needs to be measured in an appropriate manner. The internally

generated goodwill or intangible assets are directly shown in the annual reports of the business if

the same satisfies the criteria which is stated in the AASB 138.

Disclosure Requirements

The management of a company which is recognizing the intangible assets of a business

needs to appropriately consider the model which is to be followed for the purpose of measuring

the intangible assets. The provisions of AASB 138 effectively shows that there are two models

which the business can follow which are revaluation model and cost model for the purpose of

effectively reporting the intangible assets of the business (Arrighetti, Landini and Lasagni 2014).

The management of the company needs to appropriate provide proper disclosures in the notes to

accounting statements so that information is available to the users regarding the type of

intangible asset which is used by the business. The disclosure requirements which is required to

be portrayed is shown below:

whether the intangible assets have definite or indefinite lives considering their useful lifes

the amortization methods used for intangible asset

the gross carrying amount and any accumulated amortization

a reconciliation of the carrying amount at the beginning and end of the period

impairment losses reversed in profit or loss during the period in accordance with AASB

136

The disclosure requirements for the business needs to be appropriate and the same effectively

provides better clarity of the financial position of the business (Peters and Taylor 2017). The

financial situation of the business appropriately presents the intangible assets if the same is

disclosed using the provisions which are provided in AASB 138.

Conclusion

The above discussion effectively shows the reporting process which is followed for

reporting of intangible assets of a business. The analysis which is presented in the above

discussion shows that there are two types of intangible assets which involves acquired goodwill

and internally generated goodwill for a business. The assessment also shows differences which

exists between reporting process of both the types of goodwill. The analysis also shows reporting

criteria separately for both the types of intangible assets and also cites provisions which are

stated in ASSB 138. In addition to this, the analysis also includes examples which is of a

hypothetical company and journal entries are also portrayed along with the same. The numerical

example makes it clear regarding the treatments which needs to be shown in the notes to

accounts section. Further proper notes and disclosures are also required as presented in the above

discussion. Therefore, it can be concluded that reporting framework for both types of goodwill is

different considering the nature of disclosures as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL ACCOUNTING

Reference

Aasb.gov.au. (2020). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-14.pdf

[Accessed 14 Jan. 2020].

Arrighetti, A., Landini, F. and Lasagni, A., 2014. Intangible assets and firm heterogeneity:

Evidence from Italy. Research Policy, 43(1), pp.202-213.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–The Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Chang, S.C. and Tsai, M.T., 2013. The effect of prior alliance experience on acquisition

performance. Applied Economics, 45(6), pp.765-773.

Devalle, A., Rizzato, F. and Busso, D., 2016. Disclosure indexes and compliance with mandatory

disclosure—The case of intangible assets in the Italian market. Advances in accounting, 35, pp.8-

25.

Ifrs.org. (2020). IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-38-intangible-assets/ [Accessed 14 Jan. 2020].

Mohr, A. and Batsakis, G., 2014. Intangible assets, international experience and the

internationalisation speed of retailers. International Marketing Review, 31(6), pp.601-620.

Peters, R.H. and Taylor, L.A., 2017. Intangible capital and the investment-q relation. Journal of

Financial Economics, 123(2), pp.251-272.

Su, W.H. and Wells, P., 2015. The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), pp.1171-1199.

Wallstreet Mojo. (2018). Goodwill (Example, Accounting) | How to Calculate Goodwill in

M&A?. [online] Available at: https://www.wallstreetmojo.com/goodwill/ [Accessed 14 Jan.

2020].

FINANCIAL ACCOUNTING

Reference

Aasb.gov.au. (2020). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB138_07-04_COMPjun14_07-14.pdf

[Accessed 14 Jan. 2020].

Arrighetti, A., Landini, F. and Lasagni, A., 2014. Intangible assets and firm heterogeneity:

Evidence from Italy. Research Policy, 43(1), pp.202-213.

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The recognition of goodwill and other

intangible assets in business combinations–The Portuguese case. Australian Accounting

Review, 26(1), pp.4-20.

Chang, S.C. and Tsai, M.T., 2013. The effect of prior alliance experience on acquisition

performance. Applied Economics, 45(6), pp.765-773.

Devalle, A., Rizzato, F. and Busso, D., 2016. Disclosure indexes and compliance with mandatory

disclosure—The case of intangible assets in the Italian market. Advances in accounting, 35, pp.8-

25.

Ifrs.org. (2020). IFRS . [online] Available at: https://www.ifrs.org/issued-standards/list-of-

standards/ias-38-intangible-assets/ [Accessed 14 Jan. 2020].

Mohr, A. and Batsakis, G., 2014. Intangible assets, international experience and the

internationalisation speed of retailers. International Marketing Review, 31(6), pp.601-620.

Peters, R.H. and Taylor, L.A., 2017. Intangible capital and the investment-q relation. Journal of

Financial Economics, 123(2), pp.251-272.

Su, W.H. and Wells, P., 2015. The association of identifiable intangible assets acquired and

recognised in business acquisitions with postacquisition firm performance. Accounting &

Finance, 55(4), pp.1171-1199.

Wallstreet Mojo. (2018). Goodwill (Example, Accounting) | How to Calculate Goodwill in

M&A?. [online] Available at: https://www.wallstreetmojo.com/goodwill/ [Accessed 14 Jan.

2020].

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.