Comprehensive Financial Accounting Assignment: Consolidation Analysis

VerifiedAdded on 2020/05/16

|16

|2765

|140

Homework Assignment

AI Summary

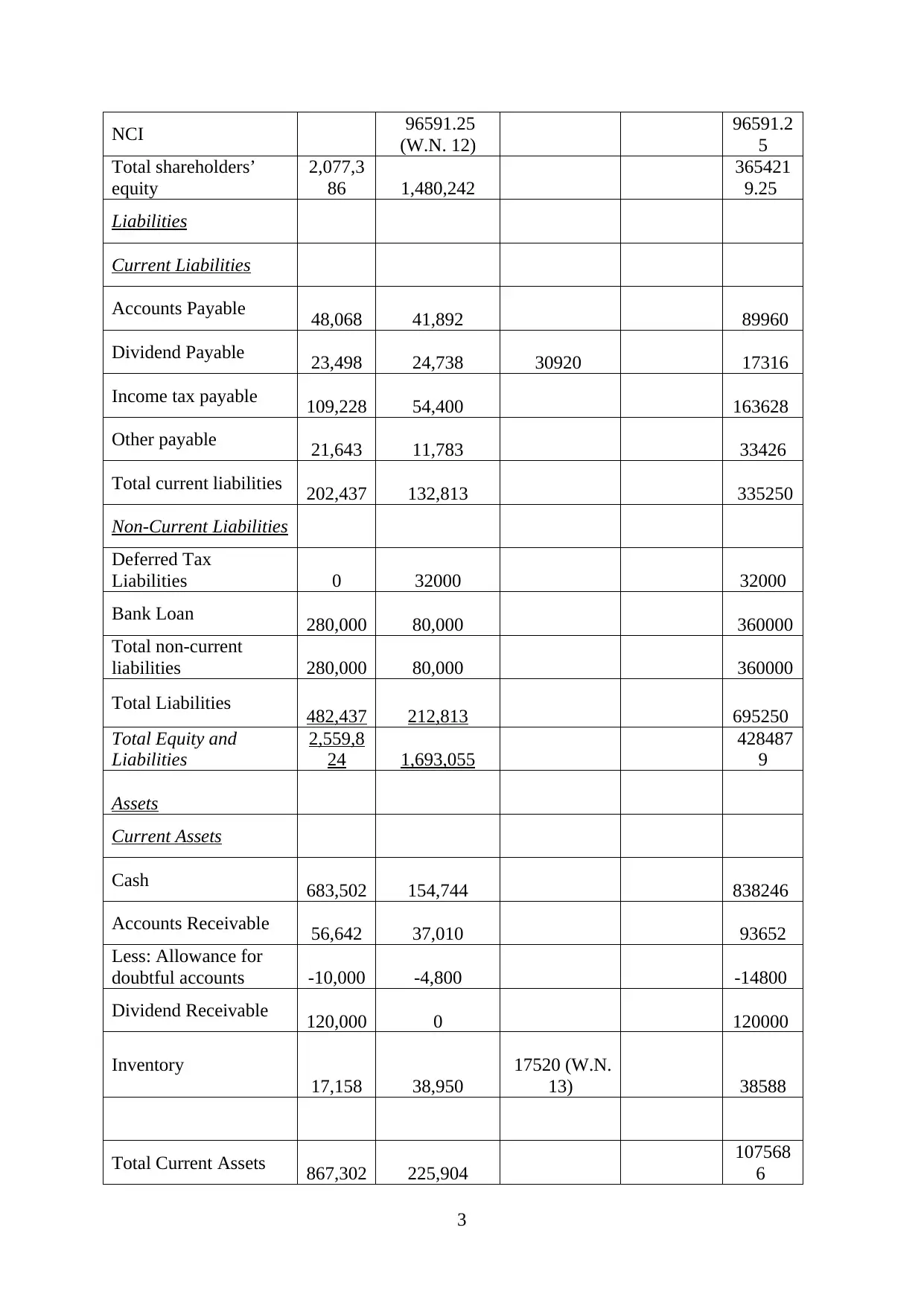

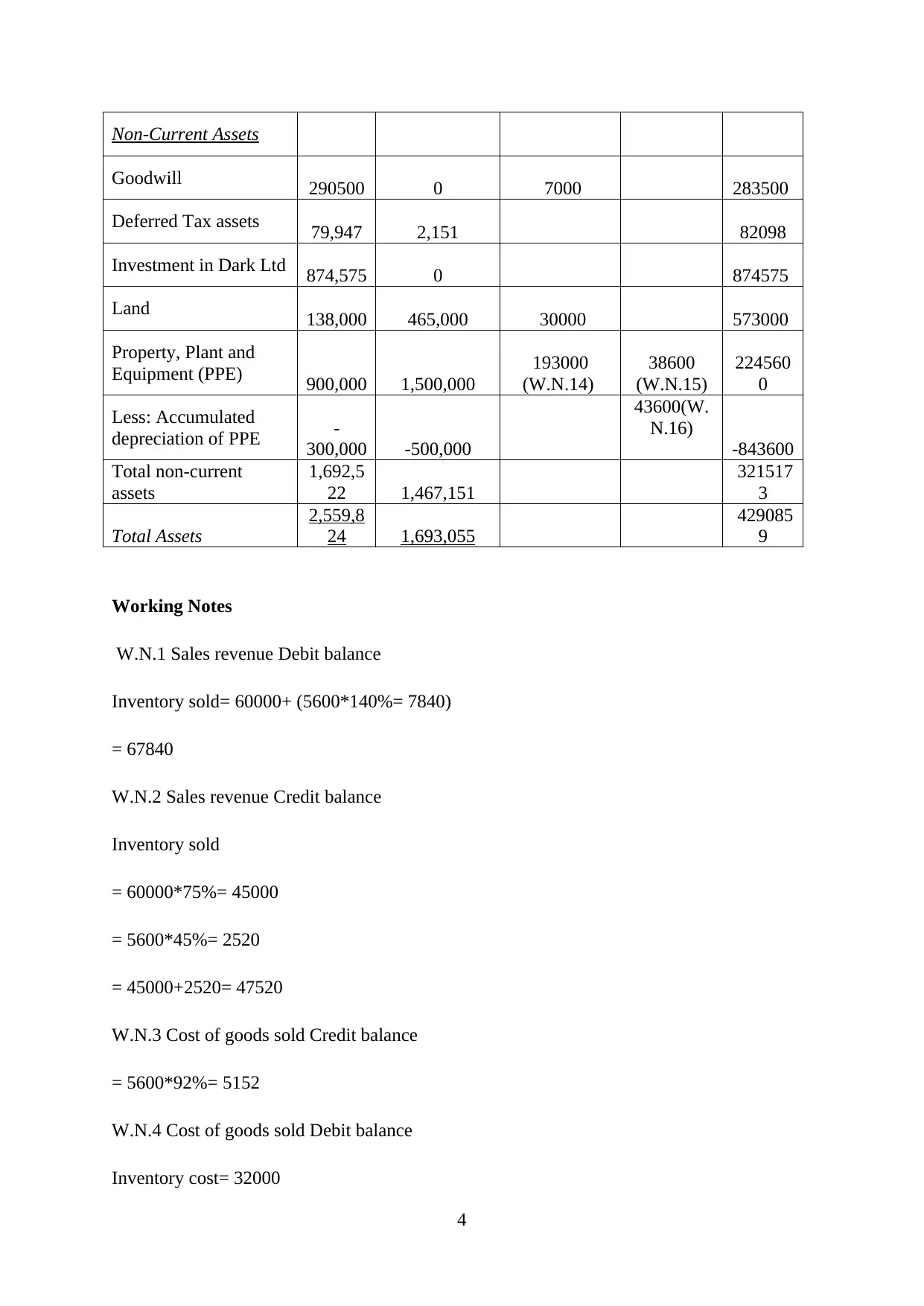

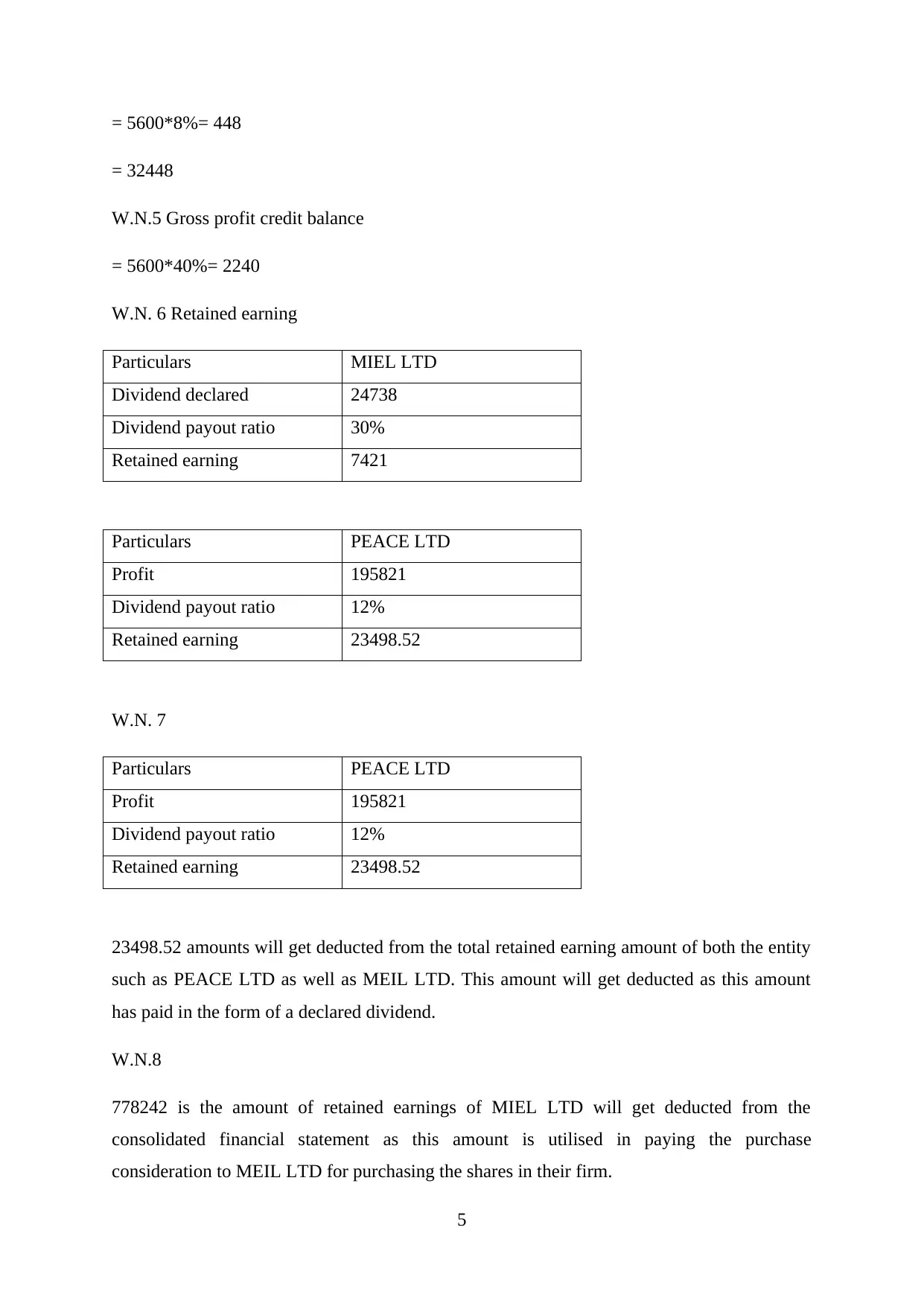

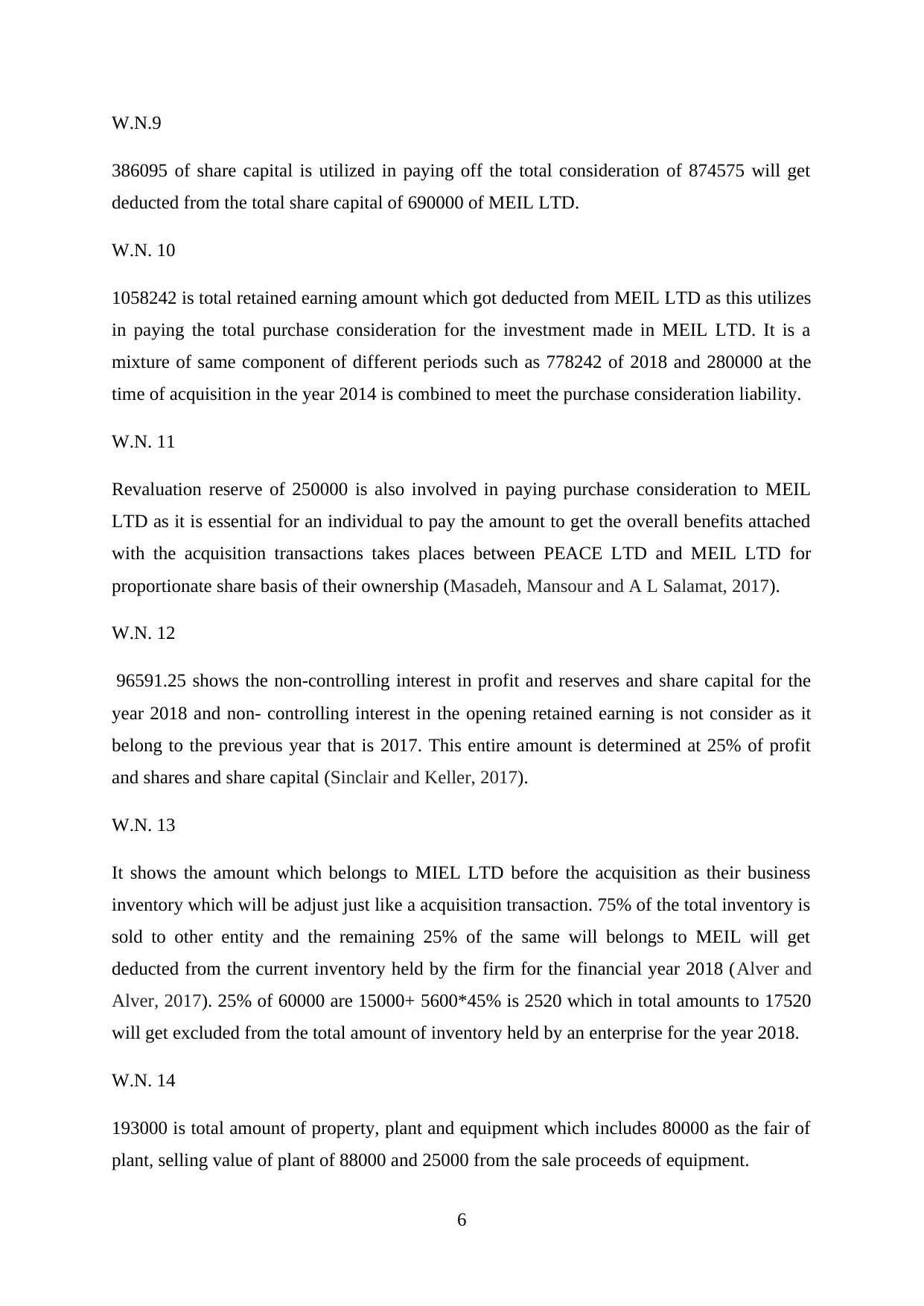

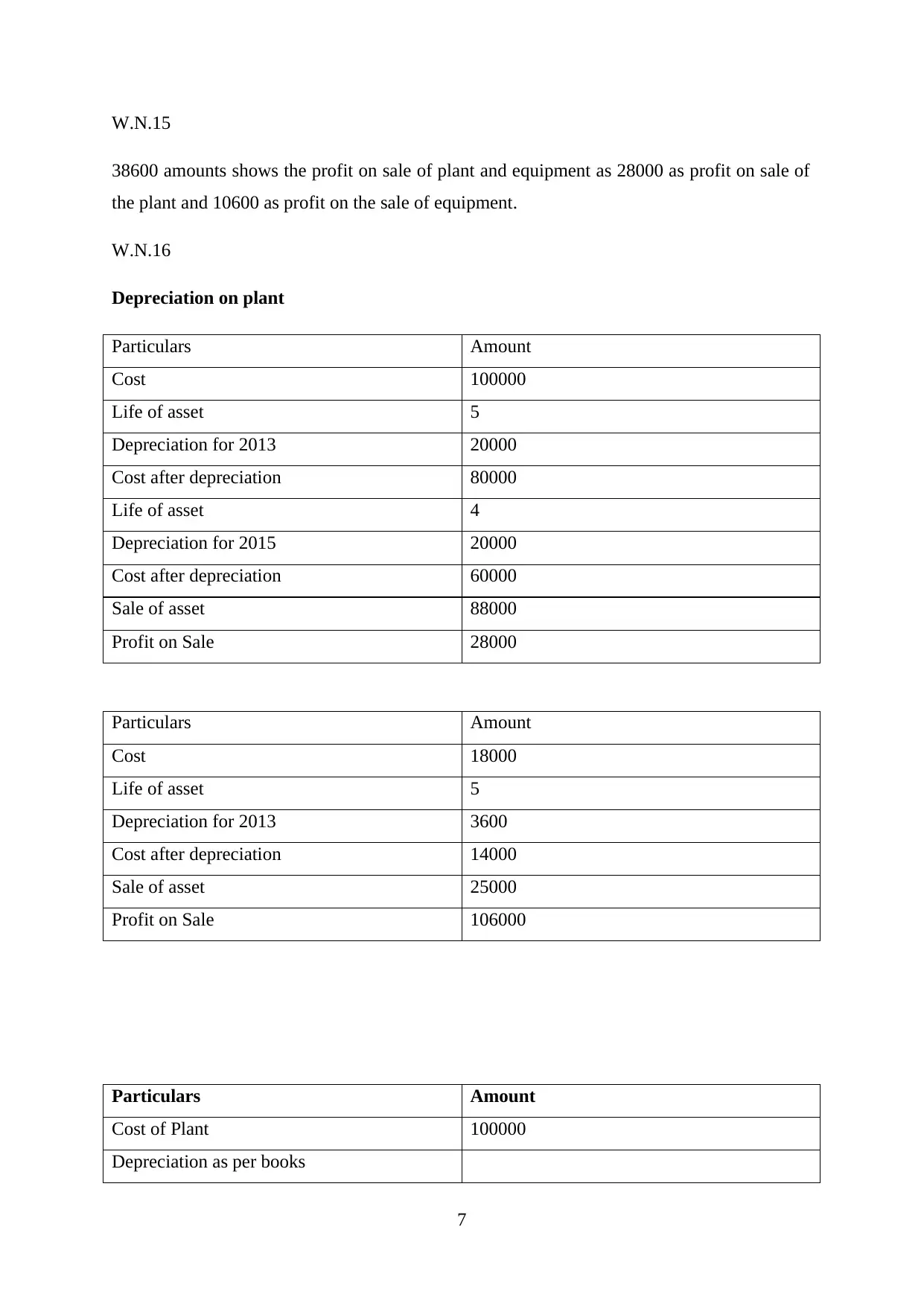

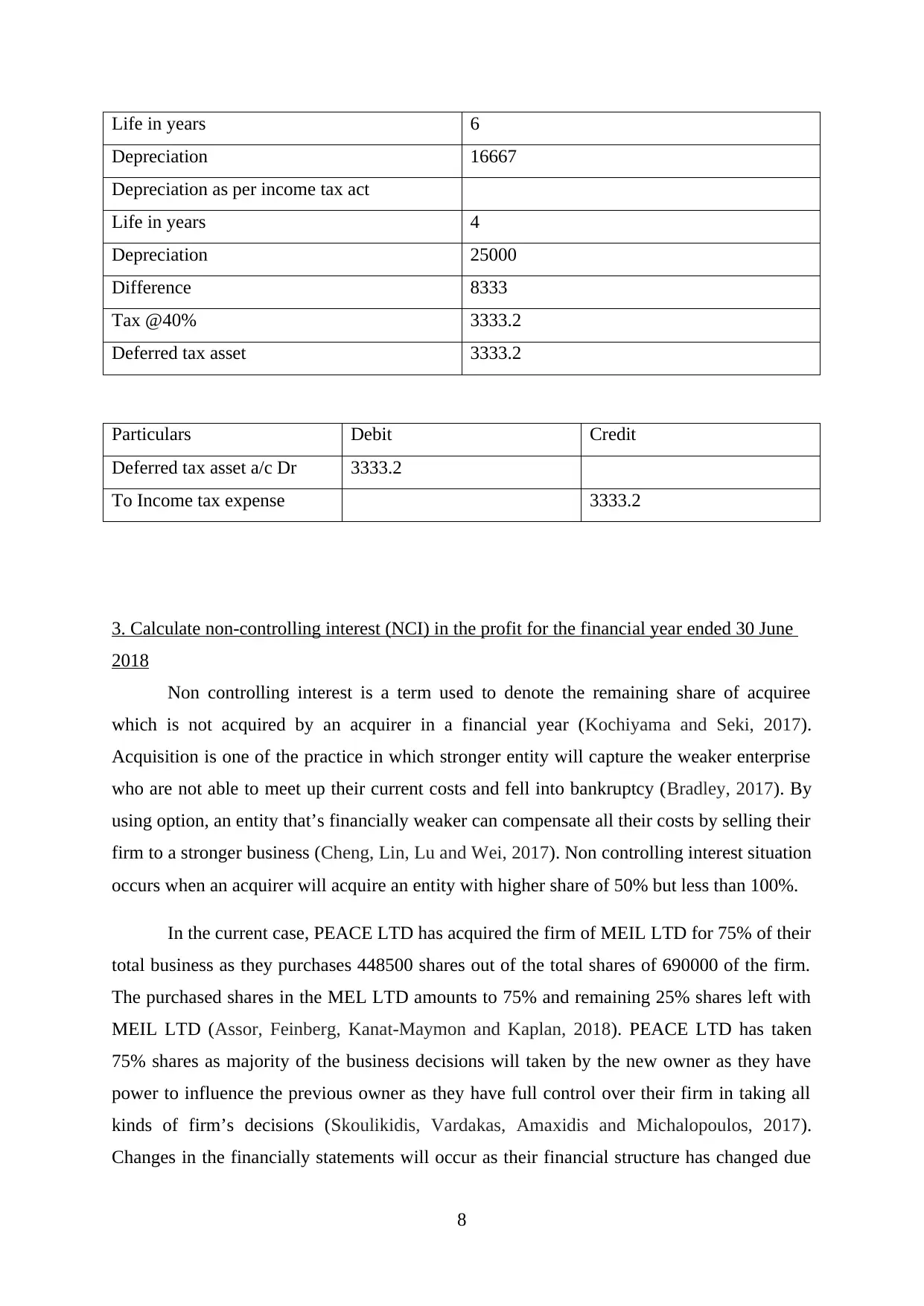

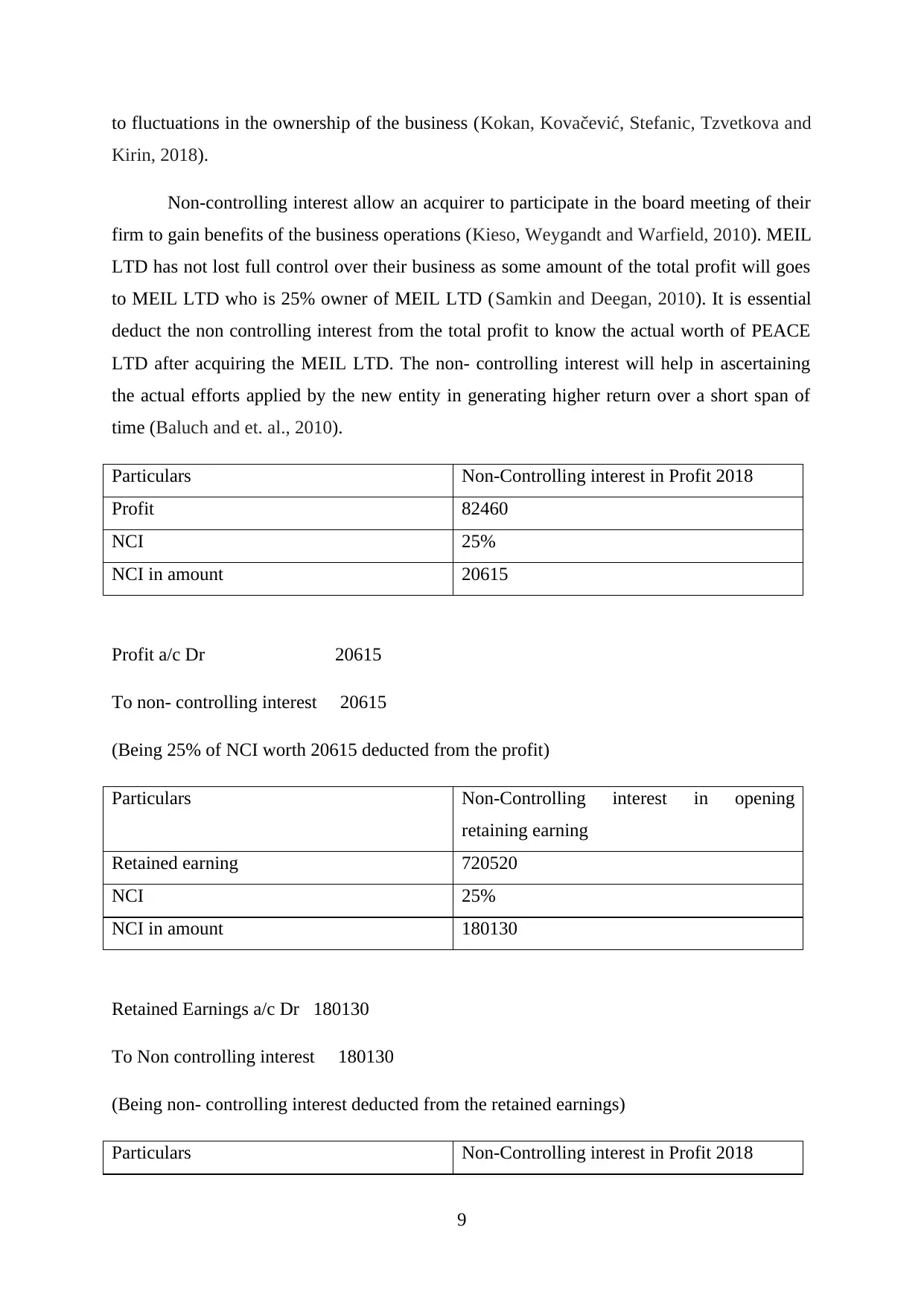

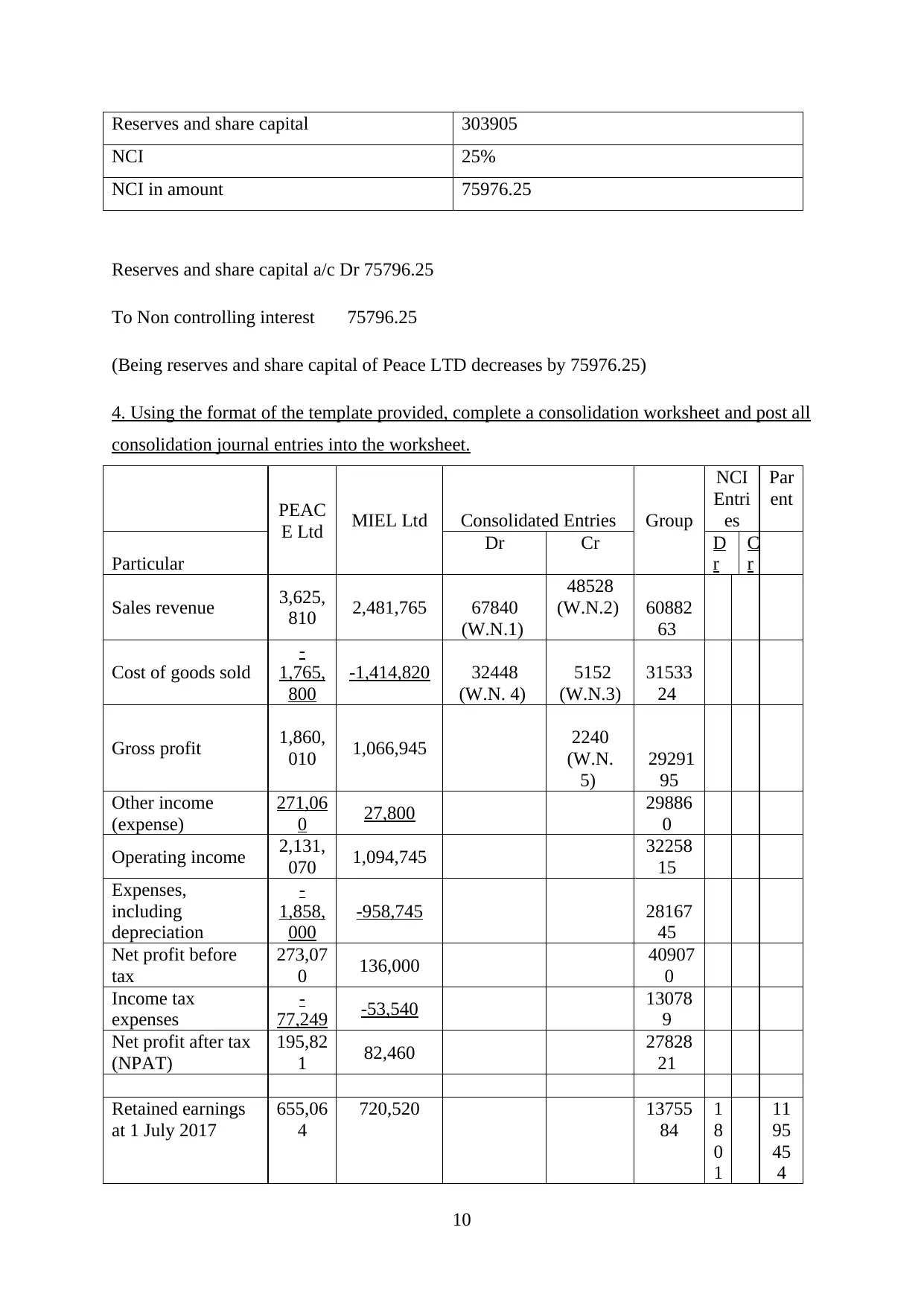

This financial accounting assignment focuses on the consolidation of financial statements. The solution includes the preparation of acquisition analysis, journal entries for the acquisition of equity interest, and consolidated adjustments for PEACE Ltd and its controlled entity. It also involves the calculation of non-controlling interest (NCI) in the profit for the financial year ended, and the completion of a consolidation worksheet with all necessary journal entries. The assignment covers key aspects of consolidation, such as fair value adjustments, deferred tax liabilities, and the treatment of retained earnings, share capital, and revaluation reserves. Additionally, it addresses the impact of intercompany transactions and the allocation of profit to NCI, providing a comprehensive overview of the consolidation process. The document showcases the application of accounting principles to real-world scenarios, demonstrating the student's understanding of financial statement consolidation.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.