Financial Accounting Assignment: Framework, Statements, and Analysis

VerifiedAdded on 2021/02/20

|45

|4552

|44

Homework Assignment

AI Summary

This assignment solution provides a detailed overview of financial accounting principles and practices. It begins with an introduction to financial accounting (FA) and management accounting (MA), explaining their differences and the regulatory and conceptual frameworks that govern financial reporting. The document then explores key accounting concepts, including going concern and accrual concepts, and qualitative characteristics like relevance and reliability. It further elucidates the users of financial information and their respective needs. The solution includes practical examples through the presentation of journal entries, ledgers, trial balances, income statements, balance sheets, and bank reconciliation statements for various clients. The assignment covers topics like depreciation, the imprest system for petty cash, control accounts, and suspense accounts, along with related rectifying entries. Finally, it emphasizes the importance of consistency and prudence in accounting practices and concludes with an analysis of the differences between financial statements of sole traders and limited companies.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Explaining FA and purpose .......................................................................................................1

Differentiating FA and the MA ..................................................................................................1

Explaining regulatory framework and its objectives .................................................................3

Explaining conceptual framework and its usefulness in the accounting community ................3

Explaining the accounting concepts and its principle ................................................................4

Explaining qualitative characteristics and it types .....................................................................4

Explaining users of financial information ..................................................................................5

CLIENT 1........................................................................................................................................6

a. preparing journal and ledger....................................................................................................6

..........................................................................................................................................................8

ii. Ledgers....................................................................................................................................8

iii. Preparation of the trial balance............................................................................................24

........................................................................................................................................................24

CLIENT 2......................................................................................................................................24

a. P&L ACCOUNT...................................................................................................................24

b. preparing balance sheet ........................................................................................................26

c. Stating the consistency & the prudence accounting concept................................................28

d. Explaining purpose of the depreciation and its techniques...................................................29

e. Evaluating the difference in between financial statements of the sole trader and the limited

companies. ................................................................................................................................30

CLIENT 3......................................................................................................................................30

a. Explaining the bank reconciliation statement ......................................................................30

b. Explaining the reasons for the variation in the bank and the cash records...........................31

c. Explaining imprest under the system of petty cash ..............................................................32

d. Preparation BRS....................................................................................................................33

CLIENT 4......................................................................................................................................34

a. Preparing ledger accounts of purchase and sales..................................................................34

INTRODUCTION...........................................................................................................................1

Explaining FA and purpose .......................................................................................................1

Differentiating FA and the MA ..................................................................................................1

Explaining regulatory framework and its objectives .................................................................3

Explaining conceptual framework and its usefulness in the accounting community ................3

Explaining the accounting concepts and its principle ................................................................4

Explaining qualitative characteristics and it types .....................................................................4

Explaining users of financial information ..................................................................................5

CLIENT 1........................................................................................................................................6

a. preparing journal and ledger....................................................................................................6

..........................................................................................................................................................8

ii. Ledgers....................................................................................................................................8

iii. Preparation of the trial balance............................................................................................24

........................................................................................................................................................24

CLIENT 2......................................................................................................................................24

a. P&L ACCOUNT...................................................................................................................24

b. preparing balance sheet ........................................................................................................26

c. Stating the consistency & the prudence accounting concept................................................28

d. Explaining purpose of the depreciation and its techniques...................................................29

e. Evaluating the difference in between financial statements of the sole trader and the limited

companies. ................................................................................................................................30

CLIENT 3......................................................................................................................................30

a. Explaining the bank reconciliation statement ......................................................................30

b. Explaining the reasons for the variation in the bank and the cash records...........................31

c. Explaining imprest under the system of petty cash ..............................................................32

d. Preparation BRS....................................................................................................................33

CLIENT 4......................................................................................................................................34

a. Preparing ledger accounts of purchase and sales..................................................................34

b. Explaining the control account and its need of preparation .................................................36

CLIENT 5......................................................................................................................................36

a. Describing the term called suspense account and its characteristics.....................................36

b. Drafting trial balance.............................................................................................................36

c. Rectifying entries..................................................................................................................38

CONCLUSION..............................................................................................................................38

CLIENT 5......................................................................................................................................36

a. Describing the term called suspense account and its characteristics.....................................36

b. Drafting trial balance.............................................................................................................36

c. Rectifying entries..................................................................................................................38

CONCLUSION..............................................................................................................................38

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

FA means an area of accounting which focuses on facilitating the external and the

internal users with the useful information. Financial accounting is counted as the way in which

the activities of the business are reported and such information is communicated to the people

within and outside the organization. The present study is based on various aspects of FA and

includes the contrast in between the financial and the MA. Furthermore, it includes accounting

principles that is to be followed by firm in respect of preparing its financial statements.

Explaining FA and purpose

FA is considered as the specialized branch that helps in keeping the track of an entity's

financial transactions (Barth, 2015). With the use of the appropriate guidelines, the business

transactions are been entered in the books, presented and is summarized in the financial report

like income statement and the balance sheet. The objective of the FA is facilitating sufficient

information for the users so that they can assess value of the enterprise on their own. Major

purpose of the FA is to accurately formulate final accounts & providing appropriate financial

reporting in relation to performance and position of an enterprise (Libby, 2017). This

information helps the users in reaching the decisions in relation to managing the business,

investment and the other important decisions.

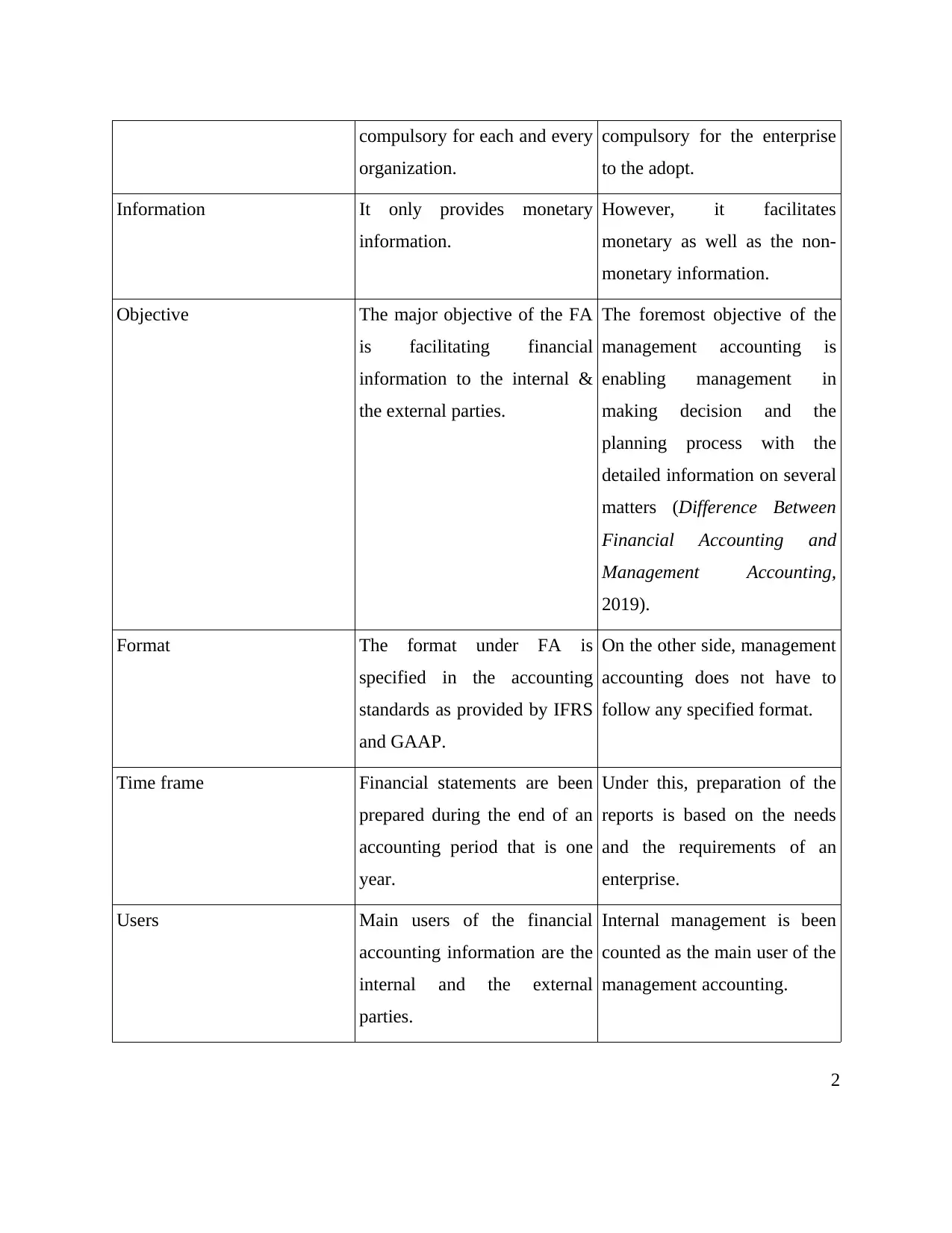

Differentiating FA and the MA

Basis FA MA

Definition This system of accounting

emphasizes on the formulation

of the financial statement in

order to provide financial

information to interested

parties.

Management accounting is an

accounting system that

provides for the relevant

information to managers in

respect of making the policies,

strategies and the plans for

running business effectively

and efficiently.

Compulsion Financial accounting is Management accounting is not

1

FA means an area of accounting which focuses on facilitating the external and the

internal users with the useful information. Financial accounting is counted as the way in which

the activities of the business are reported and such information is communicated to the people

within and outside the organization. The present study is based on various aspects of FA and

includes the contrast in between the financial and the MA. Furthermore, it includes accounting

principles that is to be followed by firm in respect of preparing its financial statements.

Explaining FA and purpose

FA is considered as the specialized branch that helps in keeping the track of an entity's

financial transactions (Barth, 2015). With the use of the appropriate guidelines, the business

transactions are been entered in the books, presented and is summarized in the financial report

like income statement and the balance sheet. The objective of the FA is facilitating sufficient

information for the users so that they can assess value of the enterprise on their own. Major

purpose of the FA is to accurately formulate final accounts & providing appropriate financial

reporting in relation to performance and position of an enterprise (Libby, 2017). This

information helps the users in reaching the decisions in relation to managing the business,

investment and the other important decisions.

Differentiating FA and the MA

Basis FA MA

Definition This system of accounting

emphasizes on the formulation

of the financial statement in

order to provide financial

information to interested

parties.

Management accounting is an

accounting system that

provides for the relevant

information to managers in

respect of making the policies,

strategies and the plans for

running business effectively

and efficiently.

Compulsion Financial accounting is Management accounting is not

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

compulsory for each and every

organization.

compulsory for the enterprise

to the adopt.

Information It only provides monetary

information.

However, it facilitates

monetary as well as the non-

monetary information.

Objective The major objective of the FA

is facilitating financial

information to the internal &

the external parties.

The foremost objective of the

management accounting is

enabling management in

making decision and the

planning process with the

detailed information on several

matters (Difference Between

Financial Accounting and

Management Accounting,

2019).

Format The format under FA is

specified in the accounting

standards as provided by IFRS

and GAAP.

On the other side, management

accounting does not have to

follow any specified format.

Time frame Financial statements are been

prepared during the end of an

accounting period that is one

year.

Under this, preparation of the

reports is based on the needs

and the requirements of an

enterprise.

Users Main users of the financial

accounting information are the

internal and the external

parties.

Internal management is been

counted as the main user of the

management accounting.

2

organization.

compulsory for the enterprise

to the adopt.

Information It only provides monetary

information.

However, it facilitates

monetary as well as the non-

monetary information.

Objective The major objective of the FA

is facilitating financial

information to the internal &

the external parties.

The foremost objective of the

management accounting is

enabling management in

making decision and the

planning process with the

detailed information on several

matters (Difference Between

Financial Accounting and

Management Accounting,

2019).

Format The format under FA is

specified in the accounting

standards as provided by IFRS

and GAAP.

On the other side, management

accounting does not have to

follow any specified format.

Time frame Financial statements are been

prepared during the end of an

accounting period that is one

year.

Under this, preparation of the

reports is based on the needs

and the requirements of an

enterprise.

Users Main users of the financial

accounting information are the

internal and the external

parties.

Internal management is been

counted as the main user of the

management accounting.

2

Reports Financial accounting provides

for the summarized reports

regarding the financial position

of organization.

Management accounting

provides for the complete and

the detailed report in relation

to various information.

Auditing Under this, the financial

statements are required to be

audited by the statutory

auditors.

The reports under the

management accounting need

require any auditing by the

statutory auditors.

Explaining regulatory framework and its objectives

Regulatory framework refers to the regulating authorities that has provisioned the set of

the standards for formulating & presenting financial reports (Balakrishnan, Watts and Zuo,

2016). Such standards and the regulations has been framed by IFRS based on the generally

Accepted Accounting principles (GAAP). The major and the foremost objective in introducing

the regulatory framework is as follows-

In order to ensure that the requirements of users relating to financial statement has been

met with adequate financial information.

For ensuring that each and every information facilitated is within the appropriate

economic arena that is it should be consistent and comparable.

For regulating behaviour of an enterprise & directors towards an investors.

Explaining conceptual framework and its usefulness in the accounting community

Conceptual framework called as the comprehensive set of the concepts that are been

issued by IFRS for the purpose of financial reporting (Christensen, Nikolaev and Wittenberg‐

Moerman, 2016). Conceptual framework helps out the accounting community in following

ways-

This helps the accounting community in setting out the objectives for the financial

reporting.

In knowing the qualitative characteristics relating to the useful accounting information.

Description relating to the reporting entity and boundary

3

for the summarized reports

regarding the financial position

of organization.

Management accounting

provides for the complete and

the detailed report in relation

to various information.

Auditing Under this, the financial

statements are required to be

audited by the statutory

auditors.

The reports under the

management accounting need

require any auditing by the

statutory auditors.

Explaining regulatory framework and its objectives

Regulatory framework refers to the regulating authorities that has provisioned the set of

the standards for formulating & presenting financial reports (Balakrishnan, Watts and Zuo,

2016). Such standards and the regulations has been framed by IFRS based on the generally

Accepted Accounting principles (GAAP). The major and the foremost objective in introducing

the regulatory framework is as follows-

In order to ensure that the requirements of users relating to financial statement has been

met with adequate financial information.

For ensuring that each and every information facilitated is within the appropriate

economic arena that is it should be consistent and comparable.

For regulating behaviour of an enterprise & directors towards an investors.

Explaining conceptual framework and its usefulness in the accounting community

Conceptual framework called as the comprehensive set of the concepts that are been

issued by IFRS for the purpose of financial reporting (Christensen, Nikolaev and Wittenberg‐

Moerman, 2016). Conceptual framework helps out the accounting community in following

ways-

This helps the accounting community in setting out the objectives for the financial

reporting.

In knowing the qualitative characteristics relating to the useful accounting information.

Description relating to the reporting entity and boundary

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Defines the accounts such as asset, income, liability, equity and the expenses.

Provides guidance on the presentation and the disclosure requirements.

Assist all the parties in understanding and interpreting the standards.

Enables the preparers of the financial reports in developing the consistent policies for the

accounting transactions.

Helps the board in developing the IFRS standards on the basis of the consistent concepts

that results in the financial information which is useful for the investors, creditors and the

lenders.

Explaining the accounting concepts and its principle

Recording in the final reports is been made on the basis of accounting principles and

assumptions. These accounting concepts act as the rules that has to considered while preparation

of the accounts and final reports (Azar, Zakaria and Sulaiman, 2019). There are various

accounting concept that are going concern, accrual concept etc.

Going concern concept- This principle states that the firm will be carrying on its

operations for an indefinite period. It means each and every business has the continuity in its life

and does not runs for dissolving in the future. For example- for computing the depreciation,

fixed asset cost will be allocated over useful life of an asset and does not considered as only for

current year.

Accrual concept- This concept of accounting is considered as the fundamental principle

that requires for recording the revenues at times when it has been earned & not at times when

the revenues is received in form of cash and also recording the expenses at time of its occurrence

and at the time of its payment (Andon, Baxter and Chua, 2015). For instance- sales made by

ram on credit amounting to 5000 on 5th July and the amount received on 15th July, the revenue

will be recorded in the books of account on 5th July, the date on which the sales is made and not

on the date when the amount is received.

Explaining qualitative characteristics and it types

Qualitative features of an accounting information involves usefulness of the accounting

information in terms of its relevancy, reliability, materiality and understandability. Mainly there

4

Provides guidance on the presentation and the disclosure requirements.

Assist all the parties in understanding and interpreting the standards.

Enables the preparers of the financial reports in developing the consistent policies for the

accounting transactions.

Helps the board in developing the IFRS standards on the basis of the consistent concepts

that results in the financial information which is useful for the investors, creditors and the

lenders.

Explaining the accounting concepts and its principle

Recording in the final reports is been made on the basis of accounting principles and

assumptions. These accounting concepts act as the rules that has to considered while preparation

of the accounts and final reports (Azar, Zakaria and Sulaiman, 2019). There are various

accounting concept that are going concern, accrual concept etc.

Going concern concept- This principle states that the firm will be carrying on its

operations for an indefinite period. It means each and every business has the continuity in its life

and does not runs for dissolving in the future. For example- for computing the depreciation,

fixed asset cost will be allocated over useful life of an asset and does not considered as only for

current year.

Accrual concept- This concept of accounting is considered as the fundamental principle

that requires for recording the revenues at times when it has been earned & not at times when

the revenues is received in form of cash and also recording the expenses at time of its occurrence

and at the time of its payment (Andon, Baxter and Chua, 2015). For instance- sales made by

ram on credit amounting to 5000 on 5th July and the amount received on 15th July, the revenue

will be recorded in the books of account on 5th July, the date on which the sales is made and not

on the date when the amount is received.

Explaining qualitative characteristics and it types

Qualitative features of an accounting information involves usefulness of the accounting

information in terms of its relevancy, reliability, materiality and understandability. Mainly there

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are two types of the qualitative characteristics that includes fundamental and enhancing

characteristics.

Fundamental qualitative characteristics- It is type of the qualitative characteristics

which sates the relevance and the faithfulness of the information. It includes as follow2s-

Relevance- Financial information is said to be relevant as if it influences the decision of

the users.

Faithful representation- It means that the accounting information provided should be

complete, error free and neutral.

Enhancing qualitative characteristics- There are various kinds of the enhancing

characteristics that includes-

Comparability- Financial results should be such that the entity could be compared with

other entities over the time.

Verifiability- Information must be capable of verification as it facilitates the assurance to

users regarding its credibility and the reliability.

Understandability- An information should be such that it is understandable to the people

who wants to review it. It can be attained through appropriate presentation, classification and the

characterisation.

Timeliness- Financial information provided to the users within the timescale for purpose

of making suitable decisions.

Explaining users of financial information

Internal users- It means the parties that are working within an enterprise that are as follows-

Management- They requires the FI for planning and monitoring in order to make

appropriate business decisions (Cohen and Karatzimas, 2017). Financial information helps the

managers in assessing the performance of the business by applying appropriate performance

indicators such as bench-marking, KPI etc.

Employees- It refers to the internal party who have the keen interest in assessing the

financial state of an entity as it has the implications directly to their job security and the income.

External users- It means the parties present outside the premises of an entity.

5

characteristics.

Fundamental qualitative characteristics- It is type of the qualitative characteristics

which sates the relevance and the faithfulness of the information. It includes as follow2s-

Relevance- Financial information is said to be relevant as if it influences the decision of

the users.

Faithful representation- It means that the accounting information provided should be

complete, error free and neutral.

Enhancing qualitative characteristics- There are various kinds of the enhancing

characteristics that includes-

Comparability- Financial results should be such that the entity could be compared with

other entities over the time.

Verifiability- Information must be capable of verification as it facilitates the assurance to

users regarding its credibility and the reliability.

Understandability- An information should be such that it is understandable to the people

who wants to review it. It can be attained through appropriate presentation, classification and the

characterisation.

Timeliness- Financial information provided to the users within the timescale for purpose

of making suitable decisions.

Explaining users of financial information

Internal users- It means the parties that are working within an enterprise that are as follows-

Management- They requires the FI for planning and monitoring in order to make

appropriate business decisions (Cohen and Karatzimas, 2017). Financial information helps the

managers in assessing the performance of the business by applying appropriate performance

indicators such as bench-marking, KPI etc.

Employees- It refers to the internal party who have the keen interest in assessing the

financial state of an entity as it has the implications directly to their job security and the income.

External users- It means the parties present outside the premises of an entity.

5

Suppliers- Suppliers needs the financial information for assessing credit-worthiness of a

company to which they are offering the goods and the services on credit.

Lenders- They offer the loans and the advances to the organization on analysis of the

financial state of borrowers.

Government- This party act as the reviewing authorities of the accounting information as

regarding all the disclosures are been made or not and the statements prepared are in accordance

with regulations. They monitors such information in order to protect the other stake holder's

interest.

Investors- It is the party that uses the accounting information in assessing that their

investment is going good or not and in making suitable decisions.

Customers- They need financial information for assessing the quality supplies is been

made by the suppliers for the business (Handoko, Sabrina and Hendra, 2017). They also reviews

the performance of the company in order to make comparison with the other competitors.

Public- Other people also has a interest in the financial reporting that includes journalist,

academics and the analysts for the purpose of economic developments.

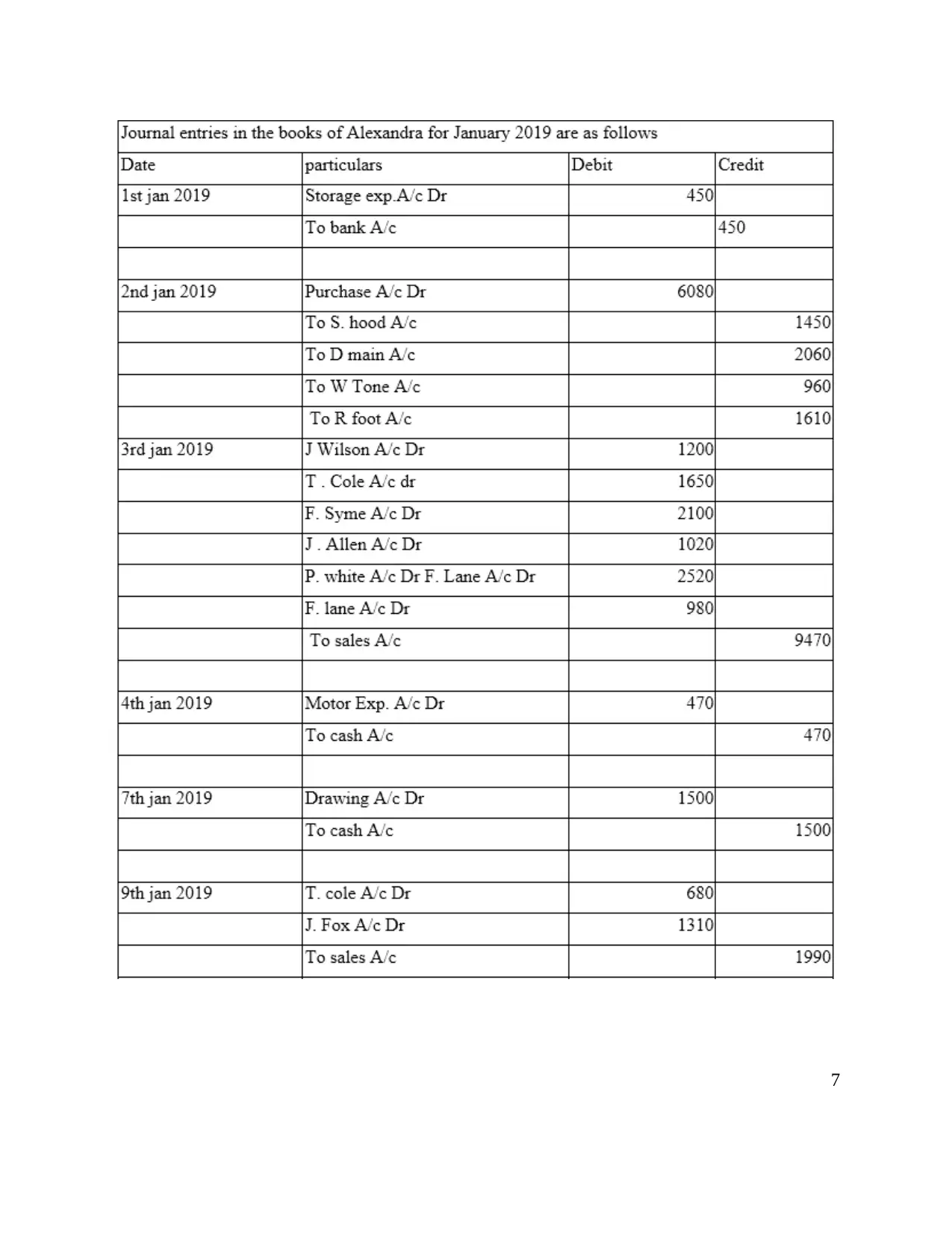

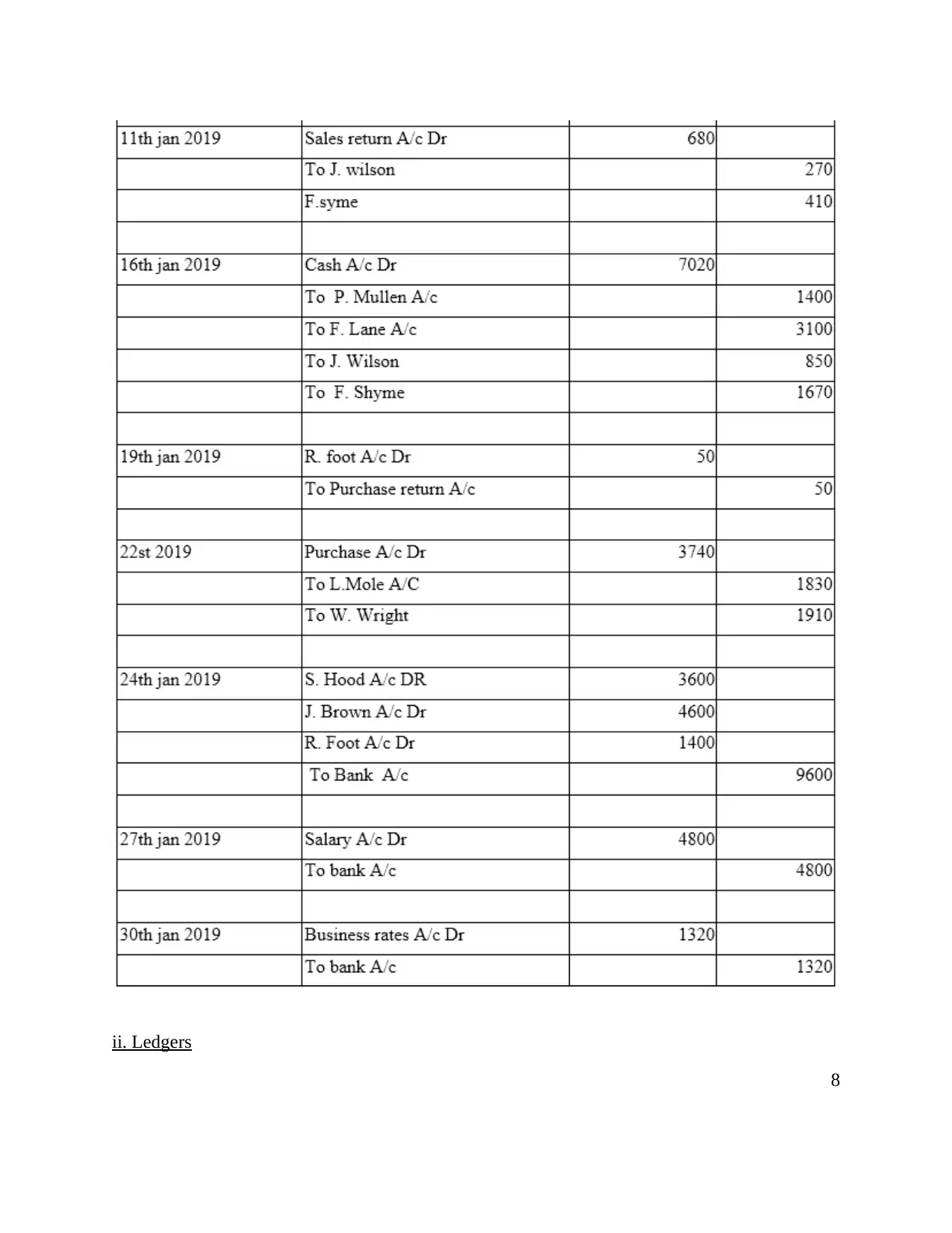

CLIENT 1

a. preparing journal and ledger

6

company to which they are offering the goods and the services on credit.

Lenders- They offer the loans and the advances to the organization on analysis of the

financial state of borrowers.

Government- This party act as the reviewing authorities of the accounting information as

regarding all the disclosures are been made or not and the statements prepared are in accordance

with regulations. They monitors such information in order to protect the other stake holder's

interest.

Investors- It is the party that uses the accounting information in assessing that their

investment is going good or not and in making suitable decisions.

Customers- They need financial information for assessing the quality supplies is been

made by the suppliers for the business (Handoko, Sabrina and Hendra, 2017). They also reviews

the performance of the company in order to make comparison with the other competitors.

Public- Other people also has a interest in the financial reporting that includes journalist,

academics and the analysts for the purpose of economic developments.

CLIENT 1

a. preparing journal and ledger

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

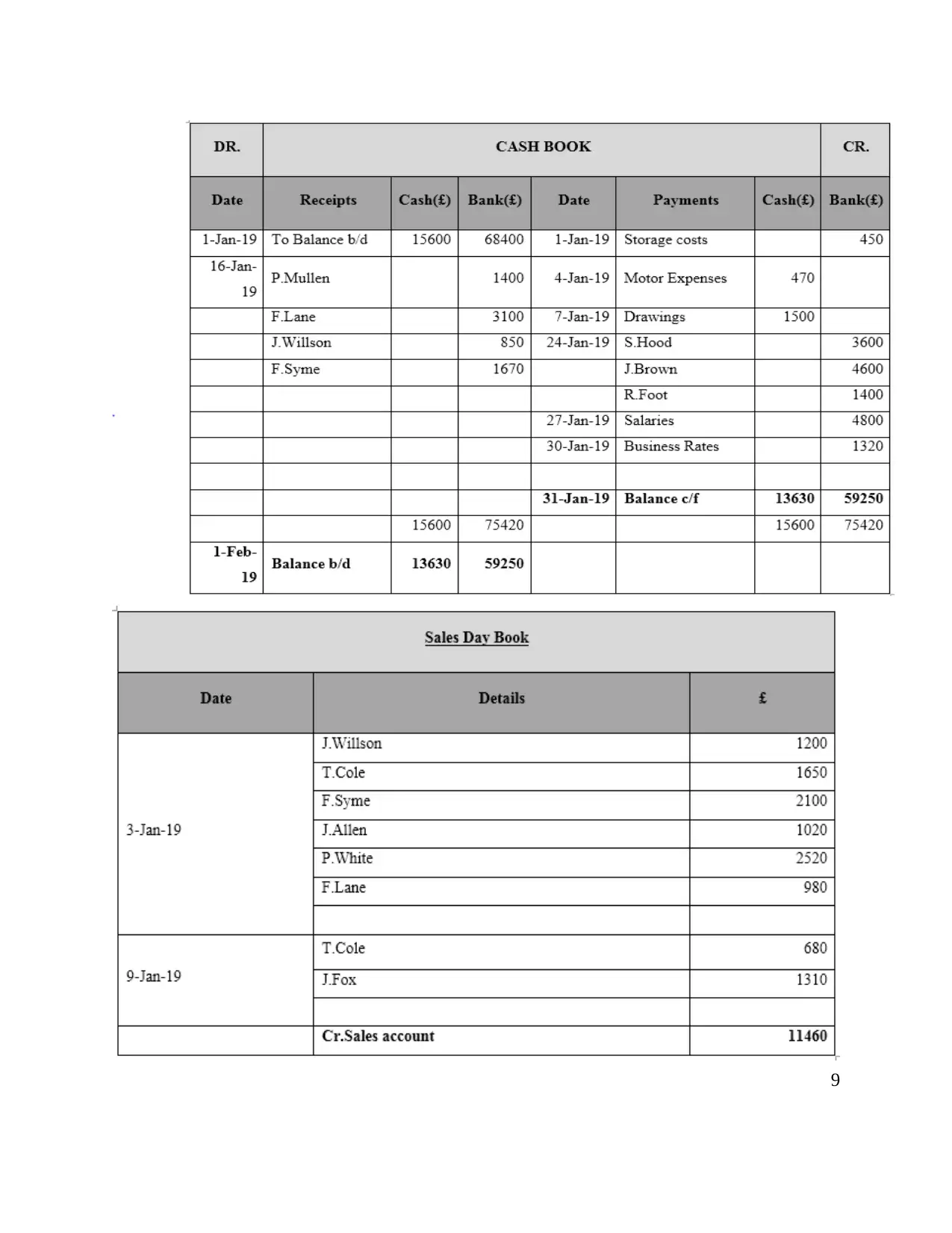

ii. Ledgers

8

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 45