Financial Accounting ACT204 Assignment: Semester 1, 2019, Problems

VerifiedAdded on 2023/03/17

|16

|2213

|98

Homework Assignment

AI Summary

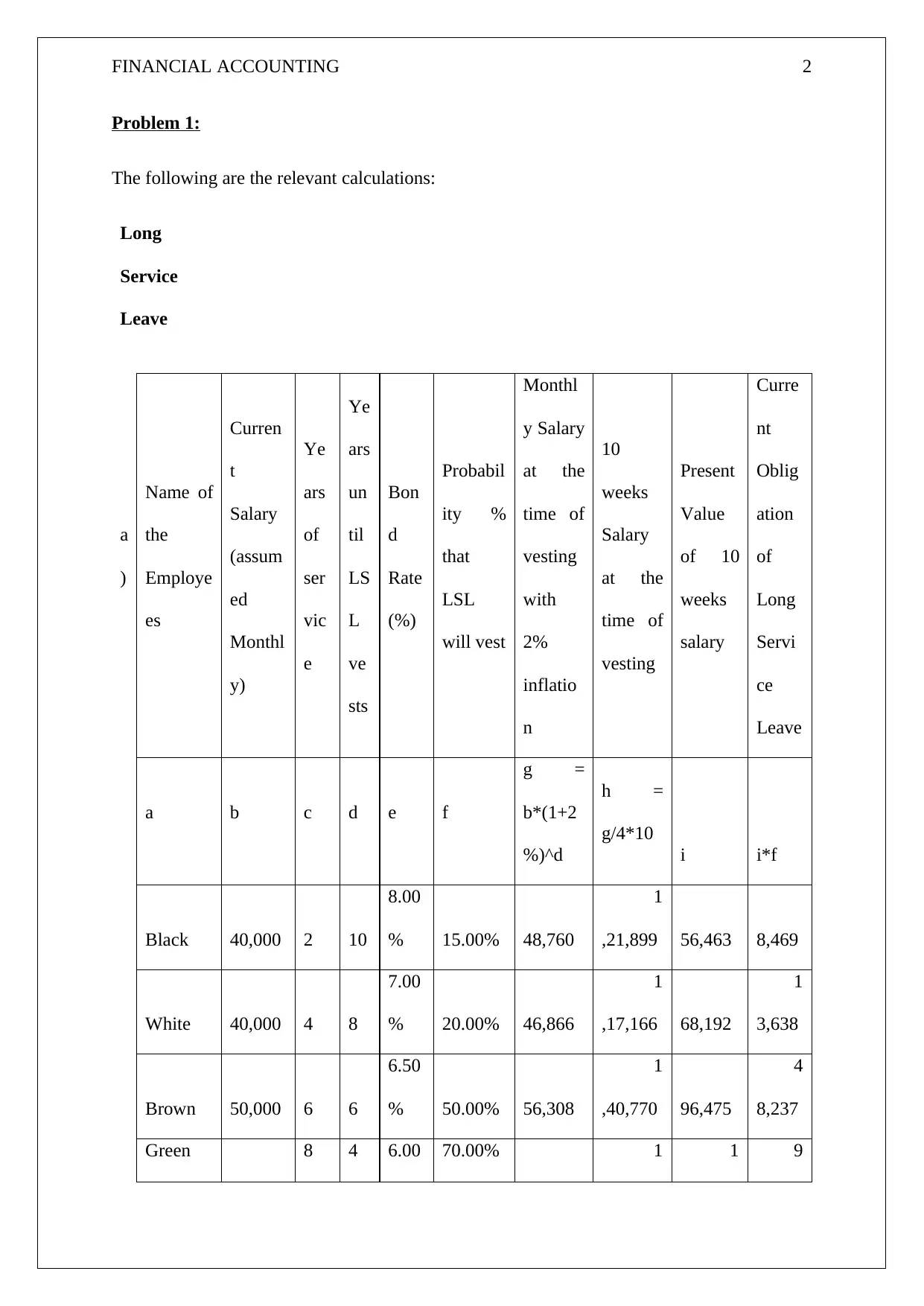

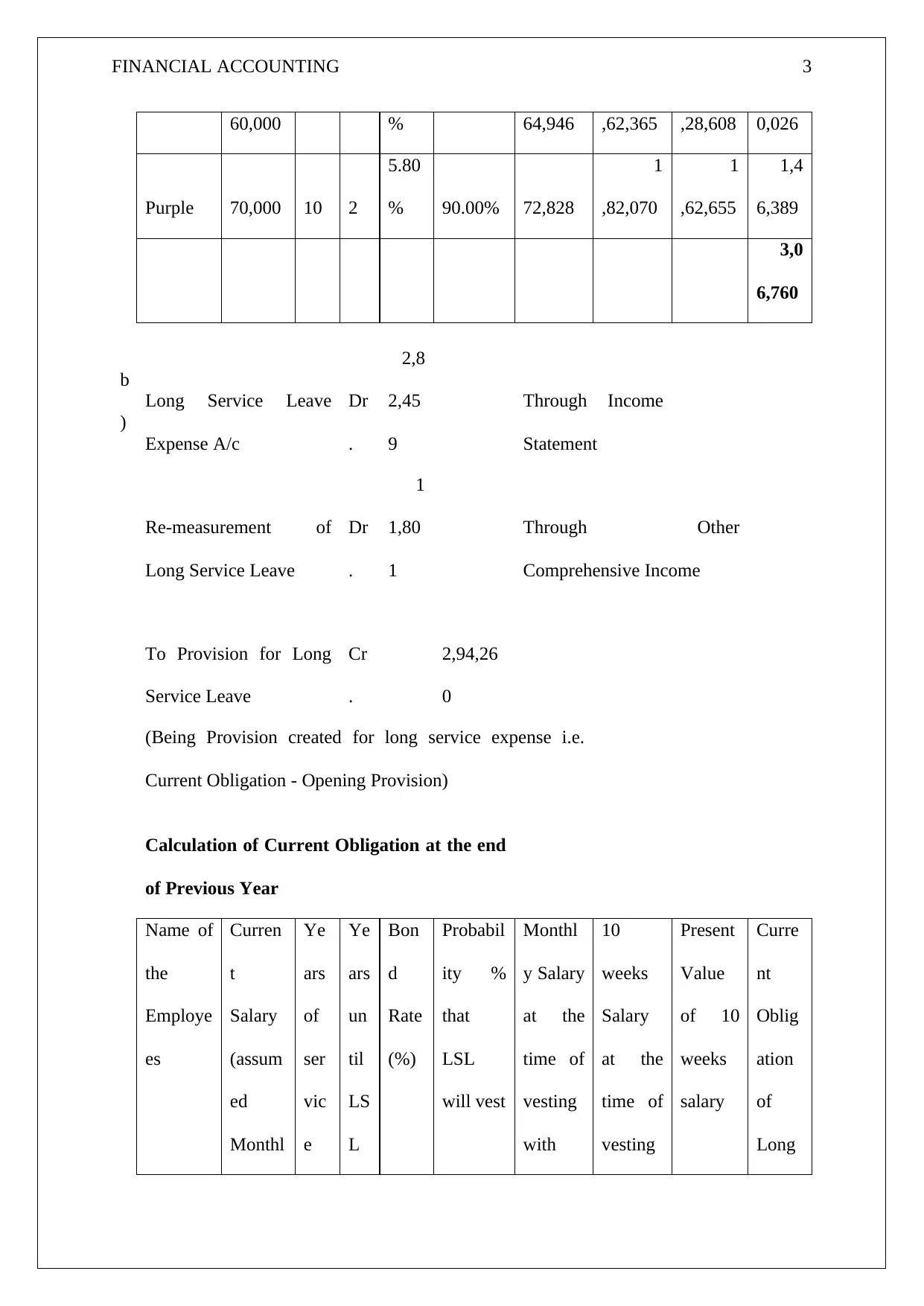

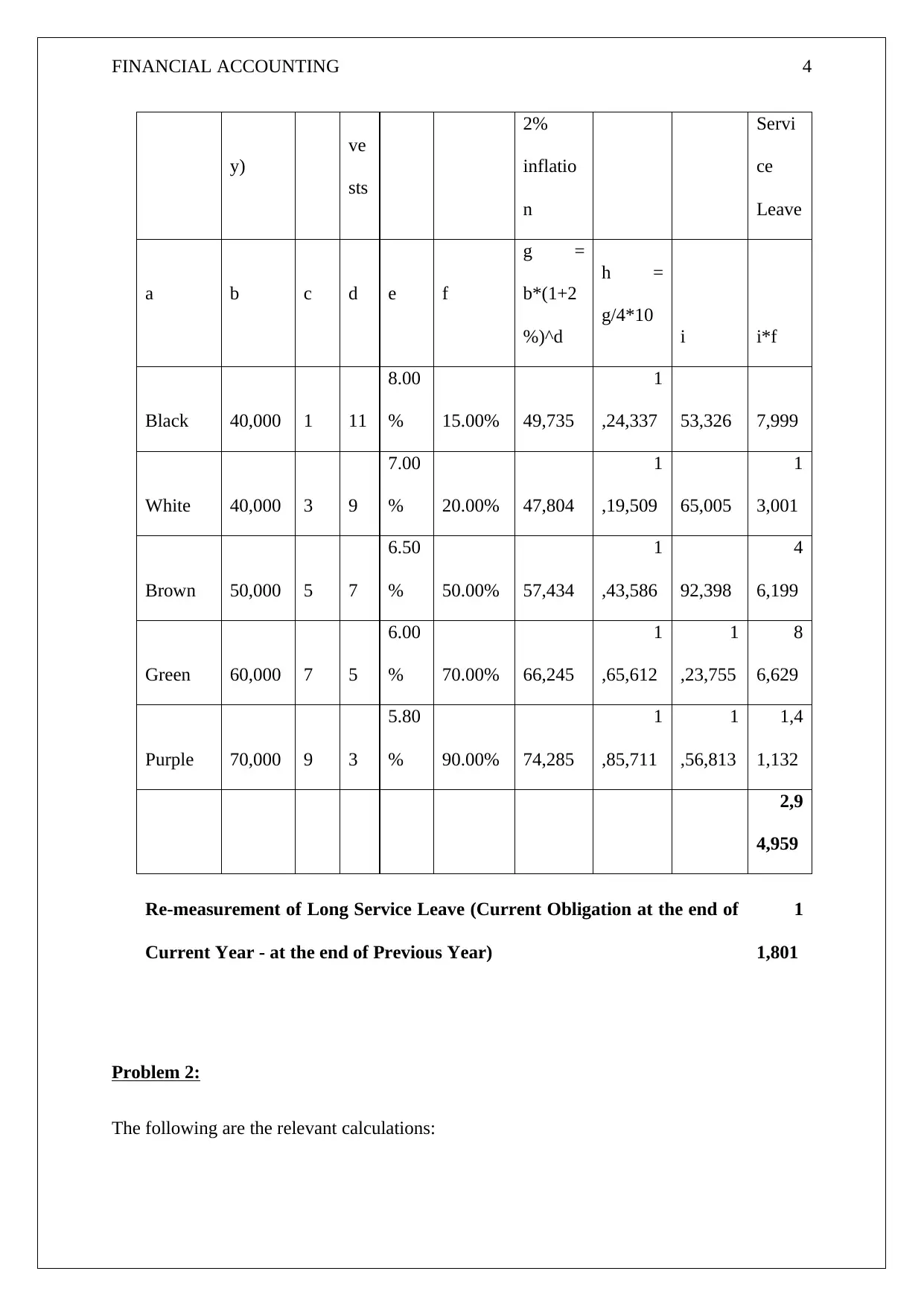

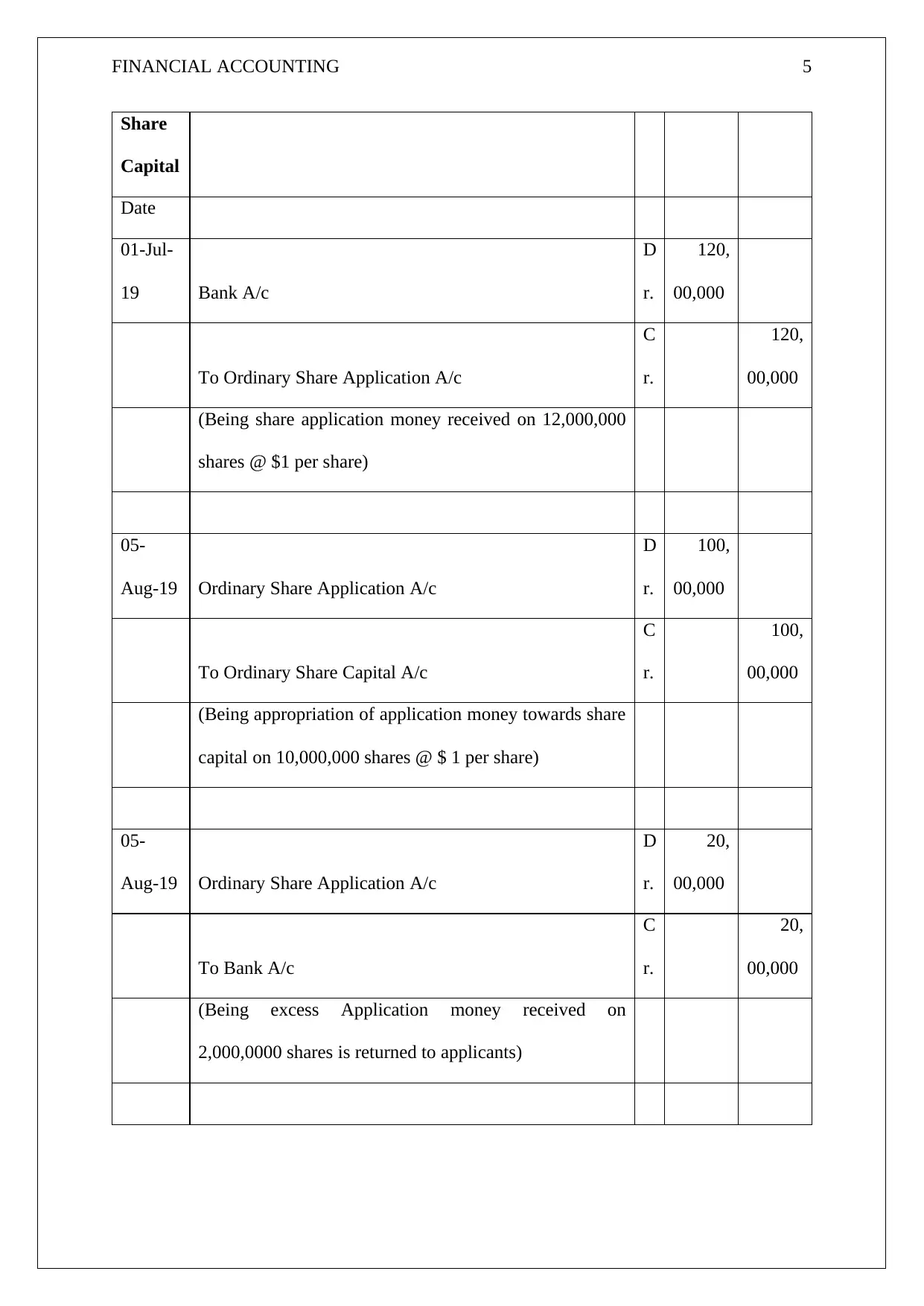

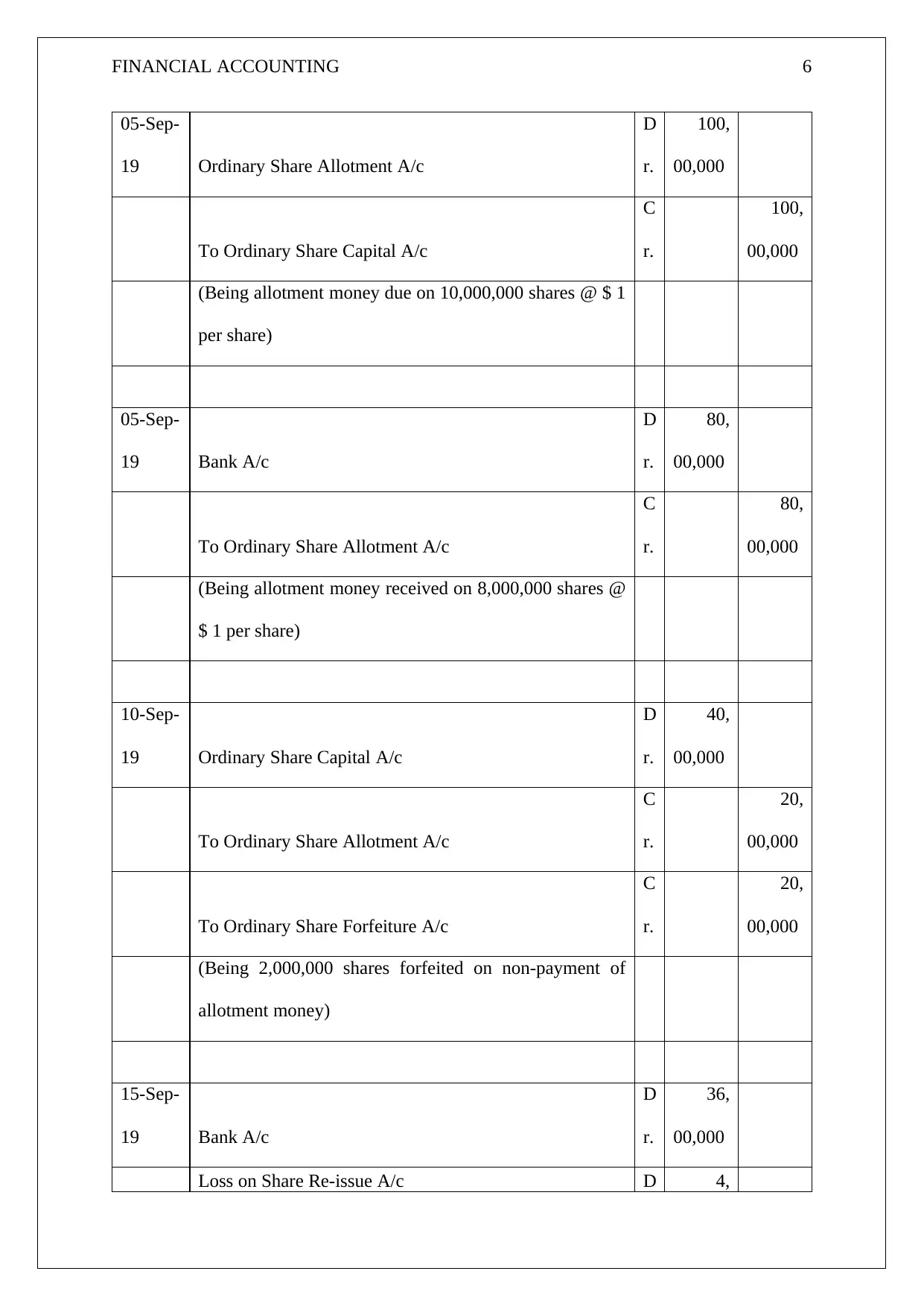

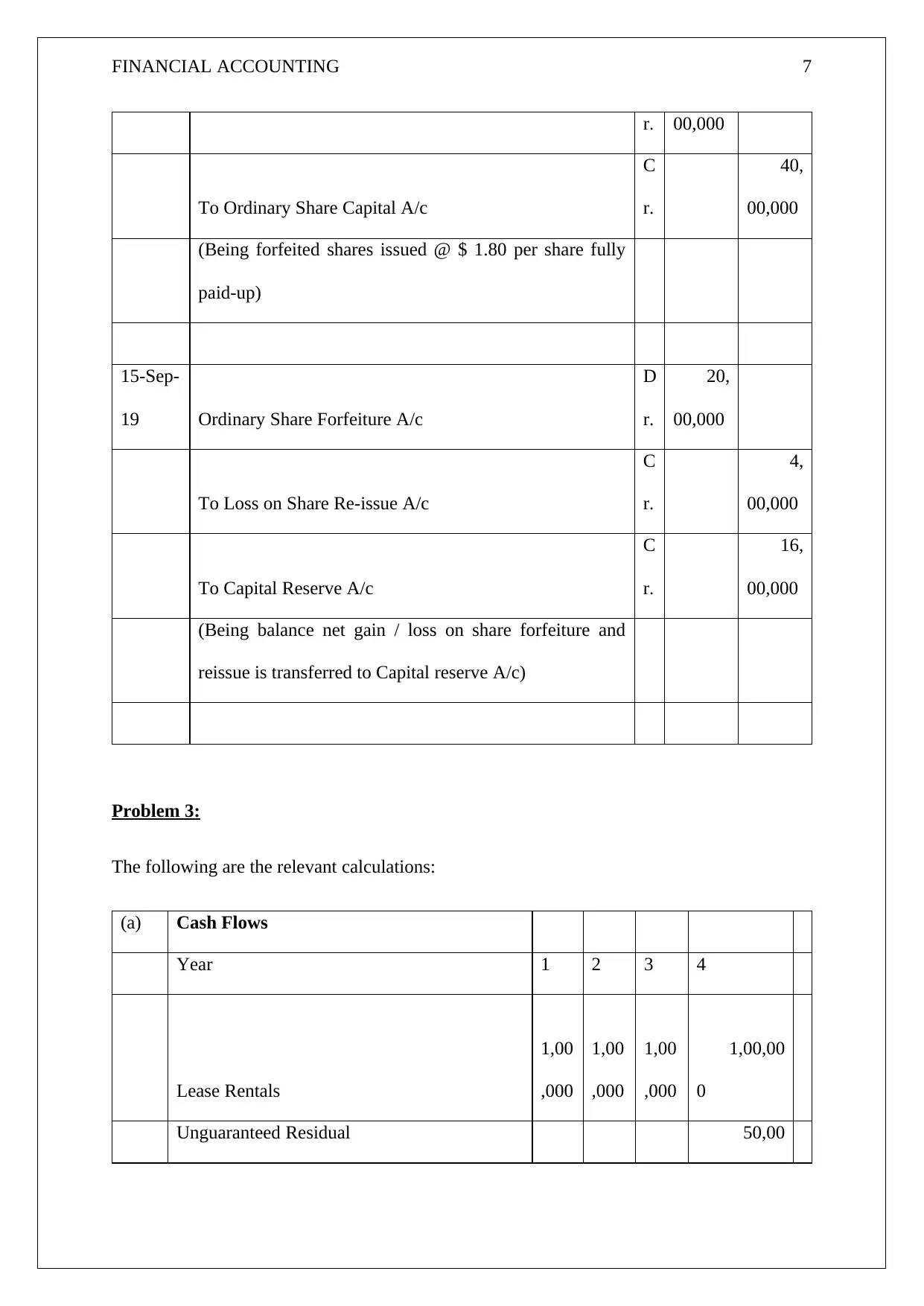

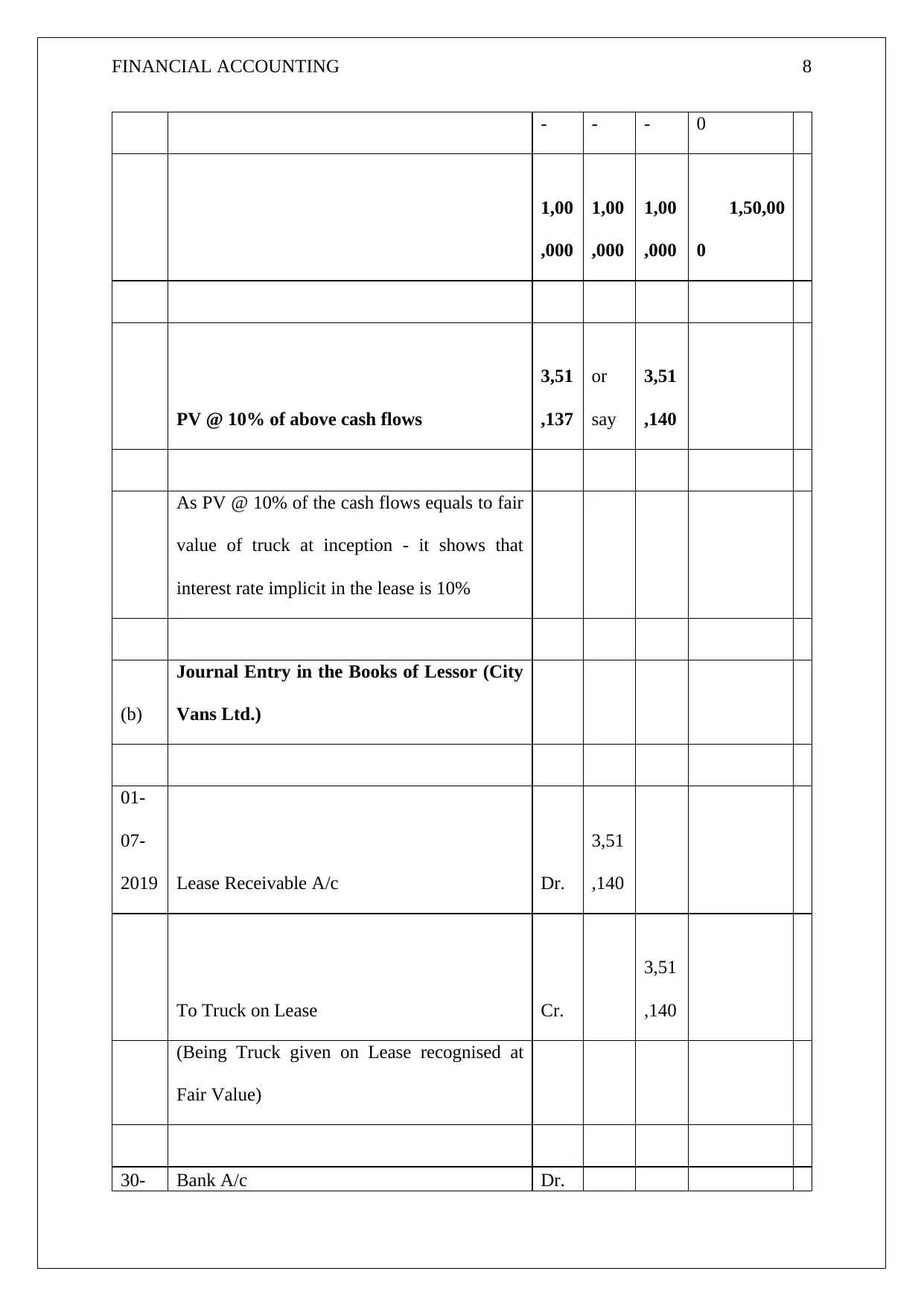

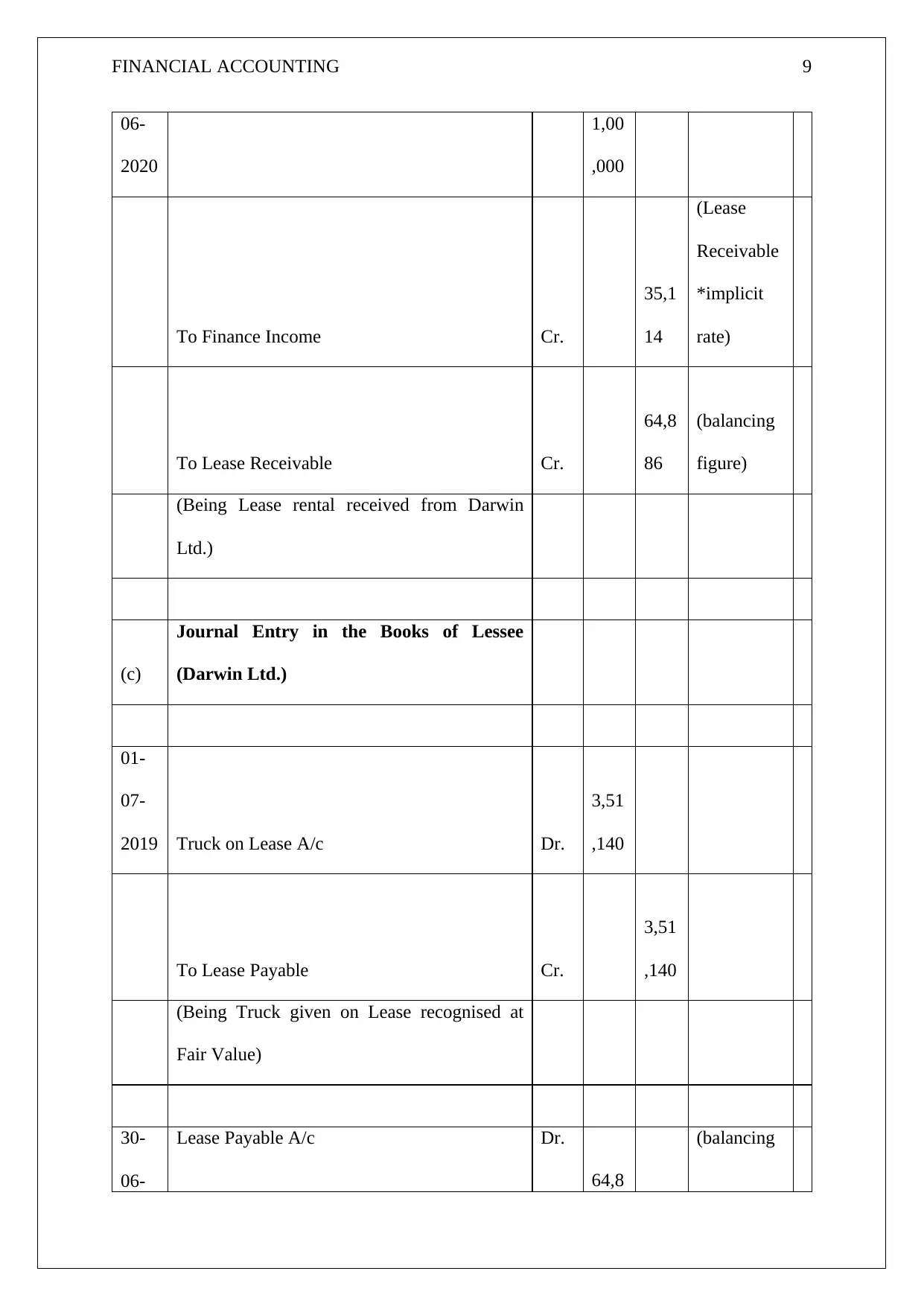

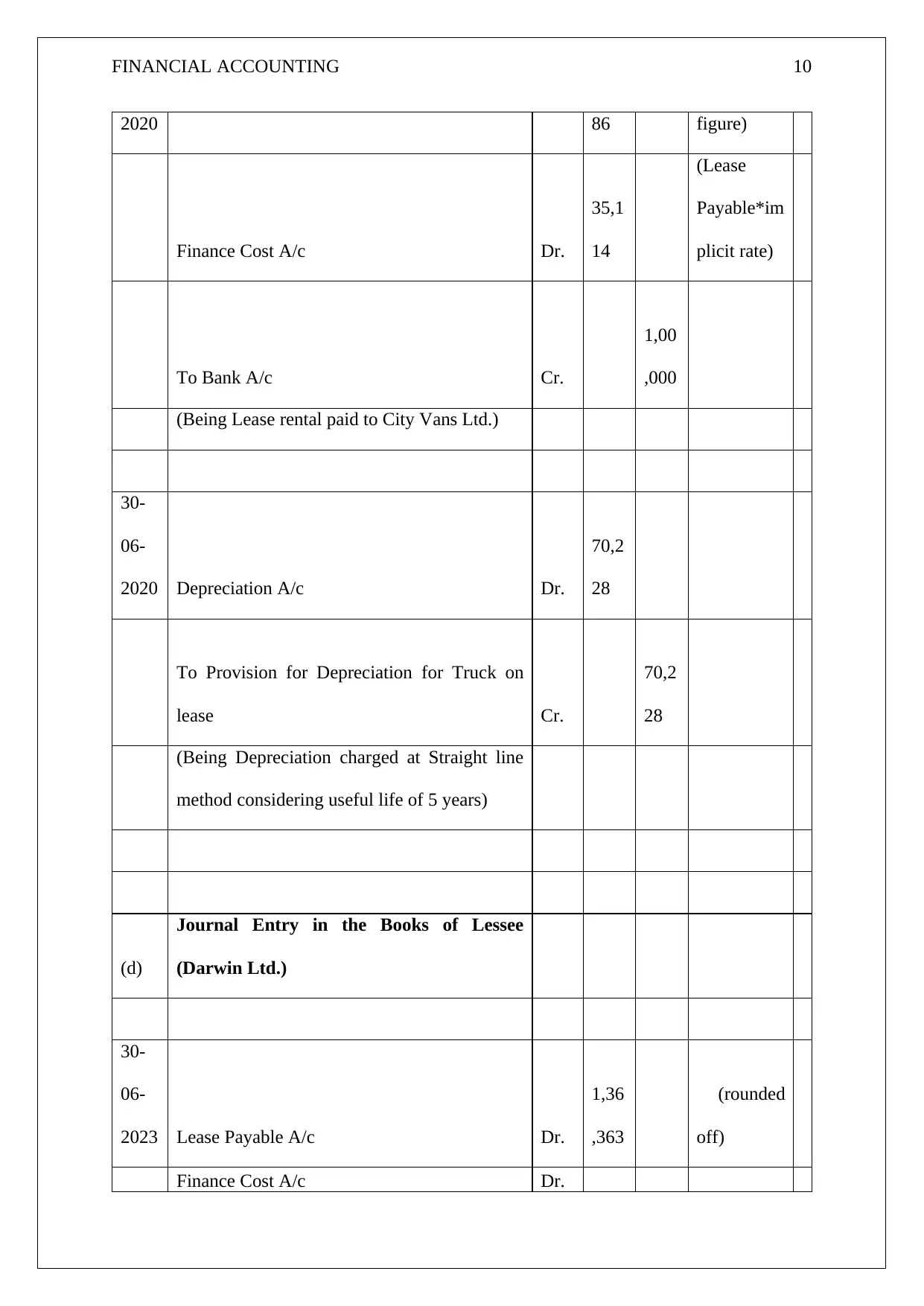

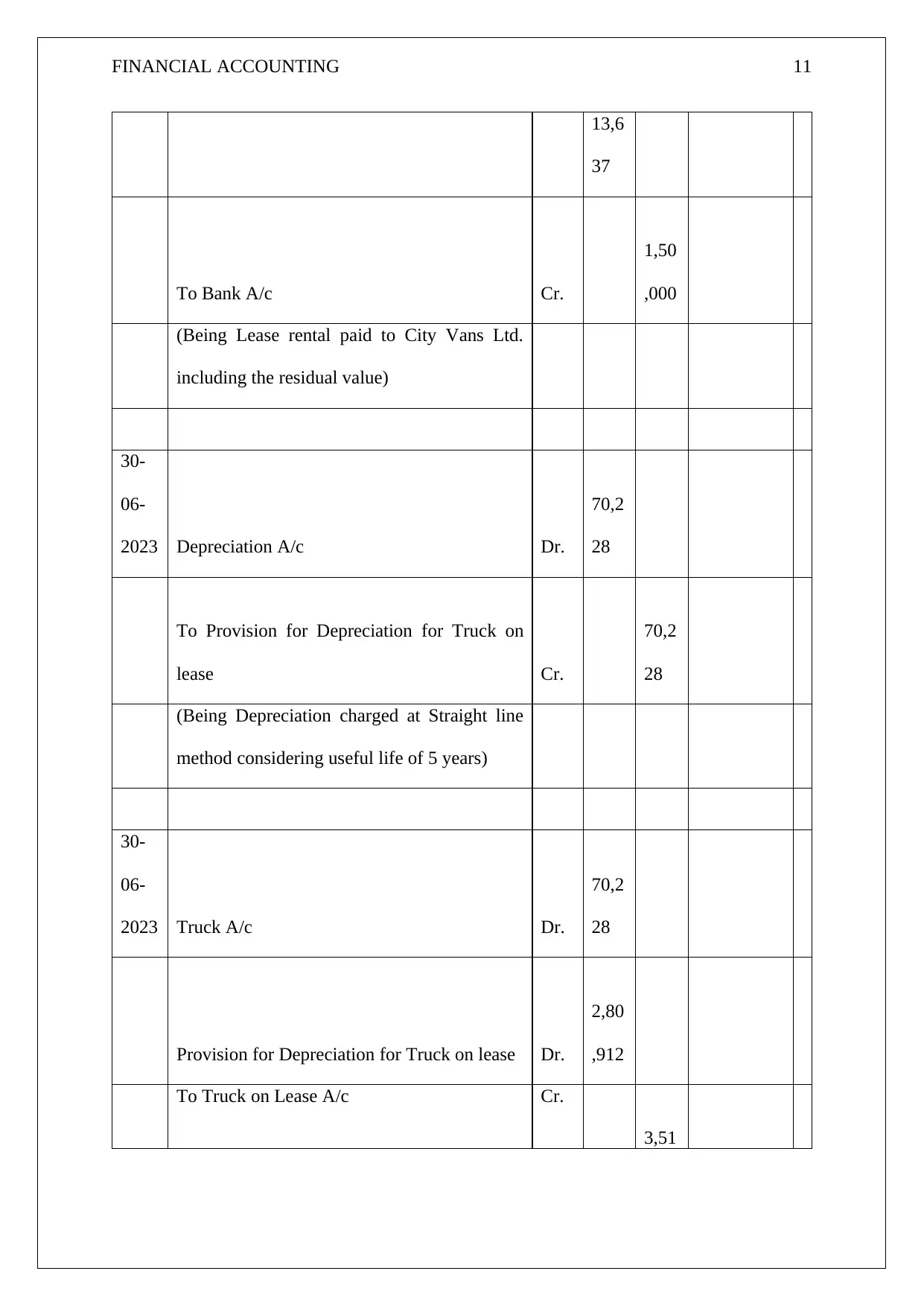

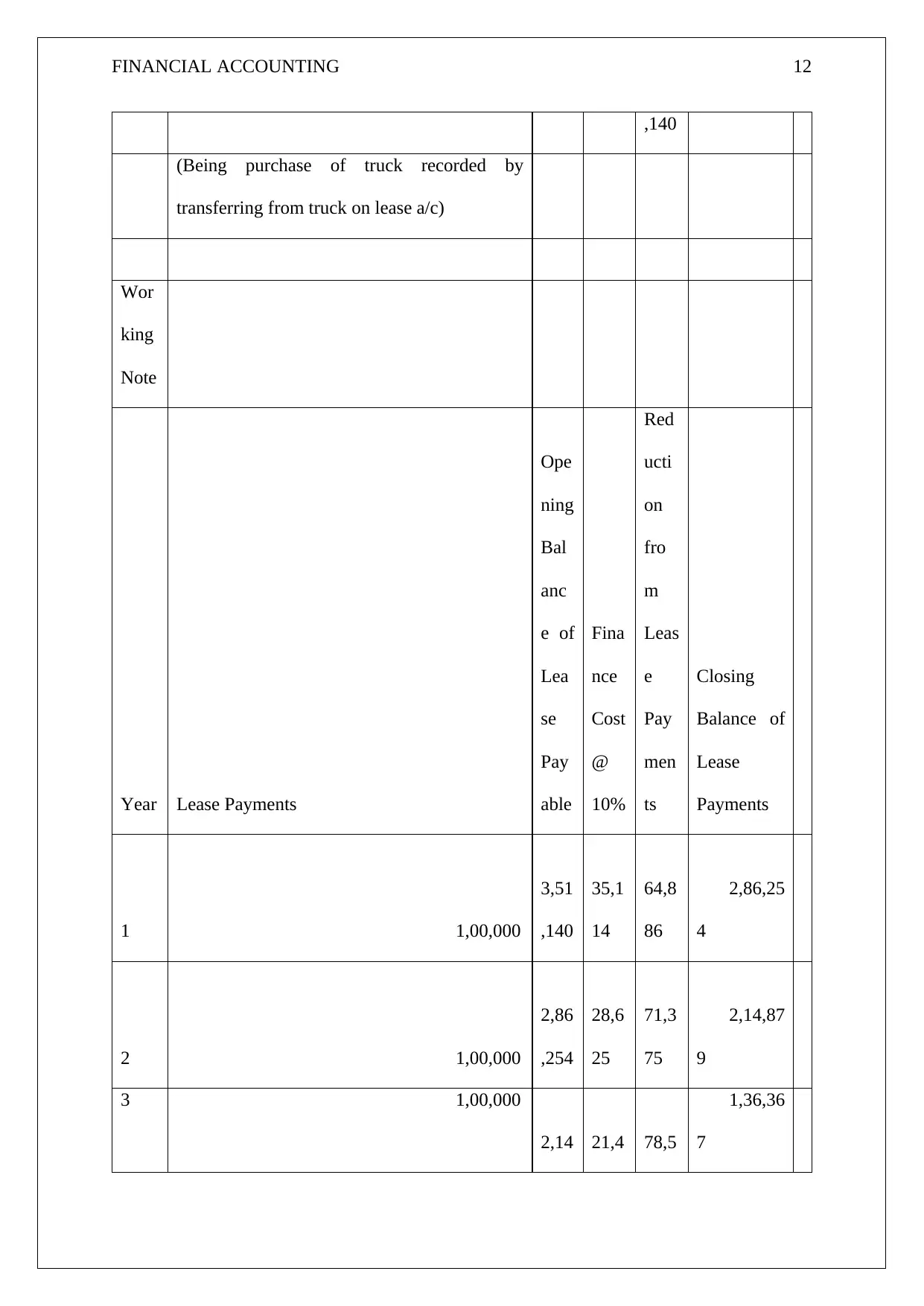

This document presents a comprehensive solution to a financial accounting assignment for the ACT204 unit. The solution encompasses several key accounting areas, including the calculation and accounting treatment of long service leave, with detailed workings and journal entries. It also covers share capital transactions, including share application, allotment, forfeiture, and reissue, with associated journal entries. Furthermore, the document addresses lease accounting, demonstrating the journal entries from both the lessor and lessee perspectives, including the calculation of implicit interest rates and depreciation. Finally, it explores creative accounting practices, defining the term, discussing its implications, and differentiating it from GAAP. The assignment provides a thorough understanding of various financial accounting concepts and their practical application.

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.